Navigating Bitcoin Options

Explore Bitcoin options and their role in the financial landscape. This article provides insights into market volatility, key metrics, and a comparison of leading options platforms, including regulatory considerations.

Disclaimer: The analysis provided here offers a window into the world of crypto derivatives and Bitcoin options. Please remember that this represents just one element in the multifaceted realm of cryptocurrency. While data from Glassnode can provide valuable insights, it's essential to approach this information holistically, as the beginning of your personal research journey.

In the evolving world of modern finance, Bitcoin options have emerged as a significant instrument. These contracts allow holders to buy or sell Bitcoin at a predetermined price, providing avenues for leveraging, hedging, and speculating. Originating with platforms like Deribit in 2016, their reach extended when Bakkt and the Chicago Mercantile Exchange (CME) Group began offering them in December 2019 and January 2020, respectively.

Bitcoin Options Landscape

Bitcoin's price has shown extreme fluctuations, peaking at $69,000 in 2021 and plummeting to below $4,000 in March 2020. Within this volatile backdrop, Bitcoin options have proven crucial for traders. Institutional adoption from platforms like CME Group and Bakkt provides traders with a structured way to navigate these market conditions, thereby refining the role and impact of Bitcoin options in the broader financial landscape.

Recent Market Conditions

Given the historical volatility in the Bitcoin market, it's instructive to focus on more recent shifts, specifically in 2023. The futures markets experienced a period of low volatility until an abrupt shift occurred on August 17th. On that day, leverage decreased substantially, leading to long liquidations of over $2.5 billion, including $220 million within a single hour. This turn of events dramatically increased Options Implied Volatility, soaring from 24% to over 55%. This spike indicates a divergence in market sentiment and forewarns of potential abrupt price changes. These market behaviors are further elucidated by the Put/Call Ratio, a key indicator offering nuanced insights into market dynamics.

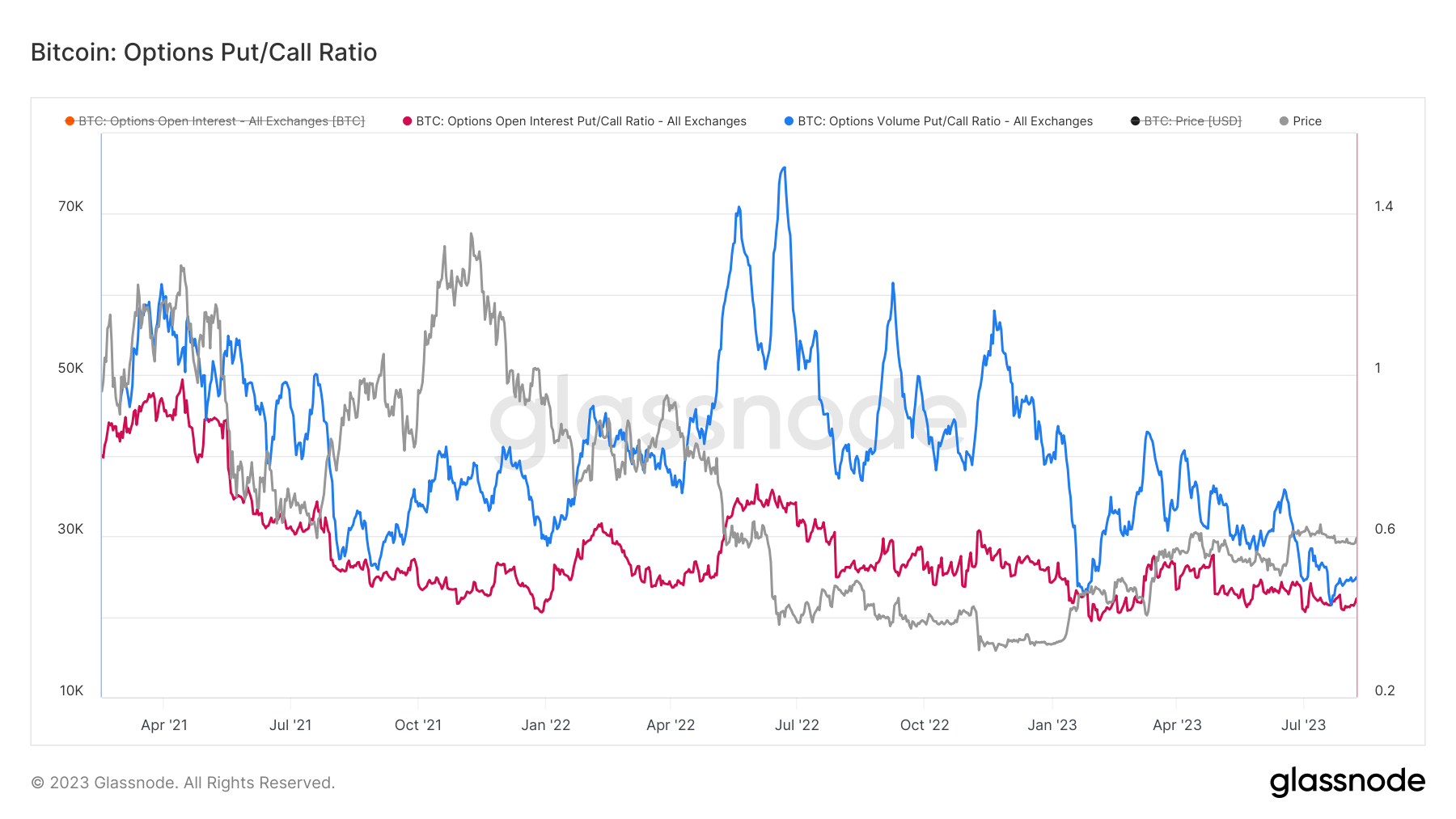

The Put/Call Ratio

Building on this recent volatility, as depicted in the Options Put/Call Ratio metric below, we are presented with the Put/Call Ratio for Options markets, distinctly divided for Open Interest (illustrated in red) and traded Volumes (showcased in blue). This metric offers a nuanced insight into the dynamics between the demand for put and call options.

As observed, both volume and open interest metrics are registering, or are closely approaching, their historic lows, oscillating between 0.42 and 0.48. Such low ratios are indicative of a prevailing bullish sentiment in the market. Interestingly, even in the face of the recent crash, these metrics haven't deviated much, suggesting a resilient optimistic stance among traders. This underscores the demand for call options, which bet on a price rise, significantly outstripping their put counterparts and further reinforcing the market's optimistic outlook. The notion of optimism or pessimism in the market brings us to another crucial metric: implied volatility.

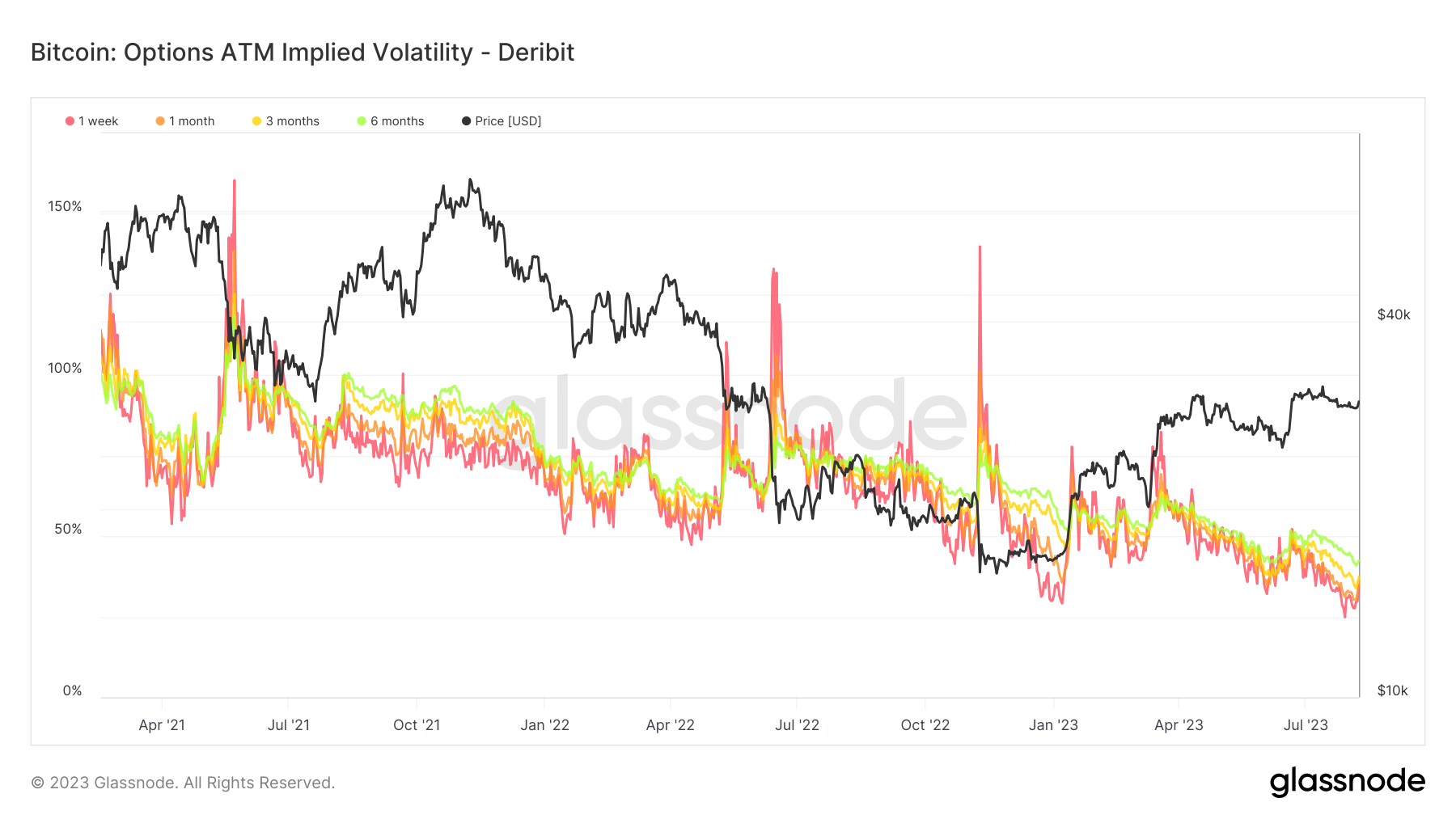

Implied Volatility

Following the patterns in the Put/Call Ratio At-The-Money (ATM) Implied Volatility, as portrayed in this metric below, provides a clear lens into the market's volatility expectations. By scrutinizing the price of an option, this metric allows us to extrapolate the anticipated volatility of the underlying asset. Defined formally, implied volatility (IV) represents the expected one standard deviation range of an asset’s price movement within a year's duration. By observing ATM IV across various timeframes, we gain a comprehensive perspective on volatility expectations, which typically fluctuate in tandem with realized volatility and overarching market sentiment.

Throughout its history, Bitcoin markets have been characterized by their marked volatility. This was evident during 2021-22 when options traded at an implied volatility (IV) oscillating between 60% and sometimes exceeding 100%. To put this into perspective, even during the most tumultuous times in traditional finance, the S&P 500's VIX rarely touches these heights, often peaking near 80% during significant market upheavals.

However, recent developments indicate a shift. At the start of the week, the implied volatility in Bitcoin's options markets had plummeted to all-time lows, trading at levels 50% below the long-term average observed throughout 2021-22. Yet, as the week's sell-off took center stage, there was a rapid repricing in volatility. Implied volatility surged, more than doubling for short-dated contracts set to expire by the end of September.

Options indicate a subdued volatility premium, with Implied Volatility (IV) figures ranging between 24% and 52%. This deviates from historical norms, showing one of the least volatile projections in Bitcoin's history. The 25-Delta Skew metric offers additional context for the relative demand between put and call options.

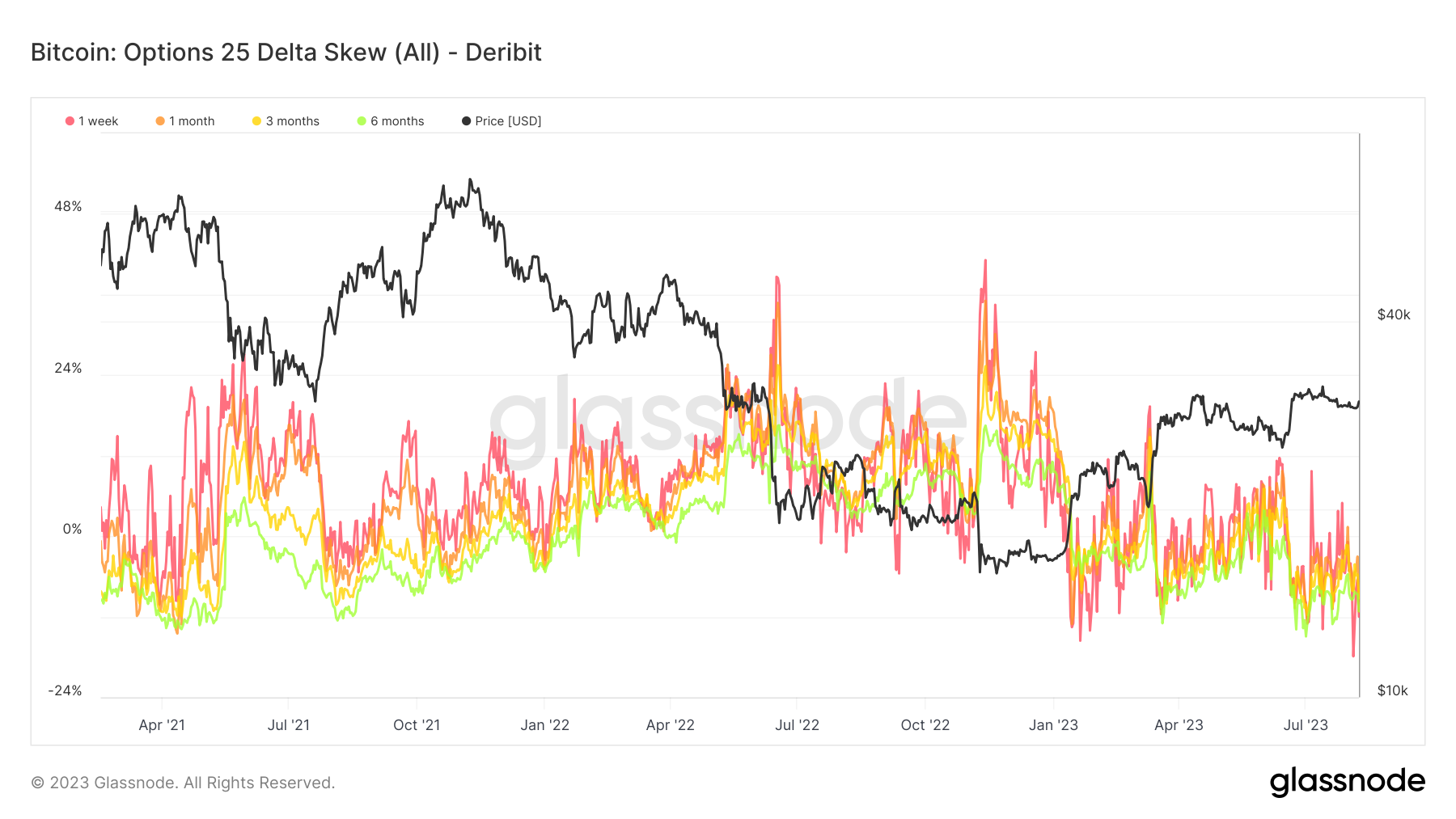

25-Delta Skew

Building on our examination of Implied Volatility, as we can discern from the Options 25 Delta Skew metric below, Skew articulates the comparative demand of put versus call options, all through the lens of Implied Volatility (IV). When we reference the "25 Delta Skew," we're specifically examining puts with a delta of -25% and calls with a delta of 25%. This effectively showcases the market’s perception of the differing implied volatility between these two types of options. The calculation of the 25 Delta Skew is grounded in the difference between a 25-delta put’s implied volatility and a 25-delta call’s implied volatility, and this difference is then normalized by the ATM Implied Volatility. For added granularity, this metric segregates option contracts based on their expiry periods: 1 week, 1 month, 3 months, and 6 months from the present.

As of the writing of this article, there's a noticeable trend where put options are considerably cheaper compared to their call counterparts, a pattern underscored by the all-time-low figures in the 25-delta skew metric. Interestingly, open interest for both call and put options remained surprisingly stable, with very little net change given the explosive price action. This suggests that whilst volatility was likely mispriced, there wasn't a great deal of forced deleveraging in options markets.

This finding is significant, especially considering that the options markets, in their current stature, stand toe-to-toe with futures markets in terms of magnitude. Most revealing is the implication that the market is anticipating historically low volatility in the foreseeable future. As of the 9th August 2023, we can see a skew of circa -10.9%, indicating that put options are trading at a discount compared to call options.

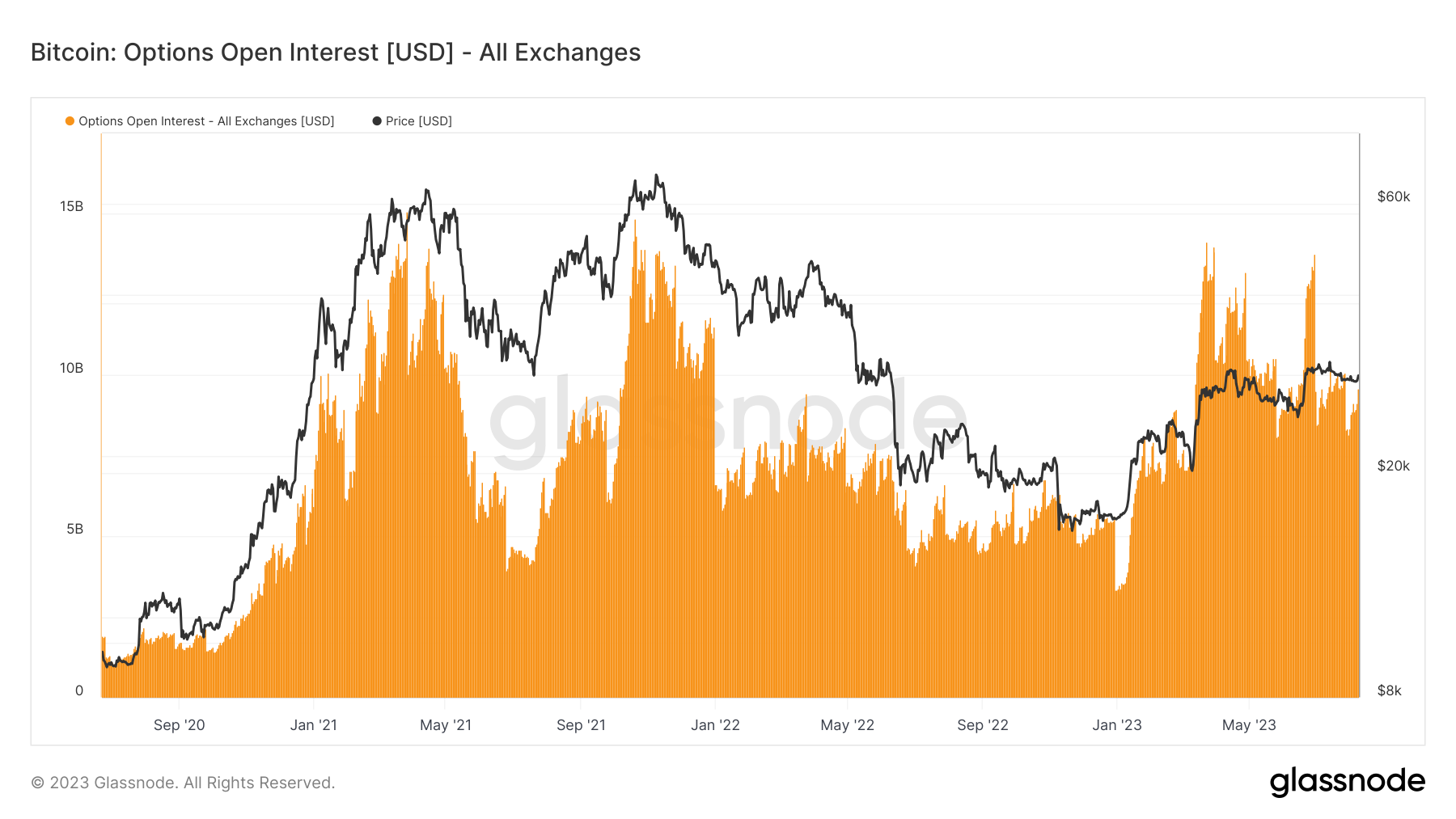

Options Open Interest

The Open Interest metric below offers additional insight into market sentiment. In 2023, the total volume of Bitcoin options trading surged by approximately 133%, likely indicating strong institutional and retail interest even amidst market compression. Even after the recent crash, open interest levels have continued to stay high.

Bitcoin Options for Institutions

To facilitate the decision-making process for institutional traders, we have outlined a concise comparison of several leading Bitcoin options platforms below. Regulatory standing is especially critical for institutional traders who must adhere to stricter compliance and risk management guidelines. This makes platforms like CME Group particularly appealing to this cohort.

This table aims to capture the nuances and unique offerings of each platform, focusing on their market position, key features, and regulatory standing.

Table: Comparison of Leading Bitcoin Options Platforms

| Platform | Market Position | Key Features | Regulation |

|---|---|---|---|

| Deribit | Market leader | Wide range of options, Various expiration dates | Offshore, Unregulated |

| CME Group | Institutional favorite | Limited range of options, Strong regulatory assurance | US-based, Regulated |

| LedgerX | Regulatory pioneer | Limited range of options | US-based, Regulated |

| OKEx | Major player | Wide trading pairs, Diverse order types, Advanced tools | Flexible regulatory environment |

| Binance | Largest by volume | Wide trading pairs, Flexible contracts, Reduced fees, Research tools | Offshore, Mixed regulation |

The Bigger Picture

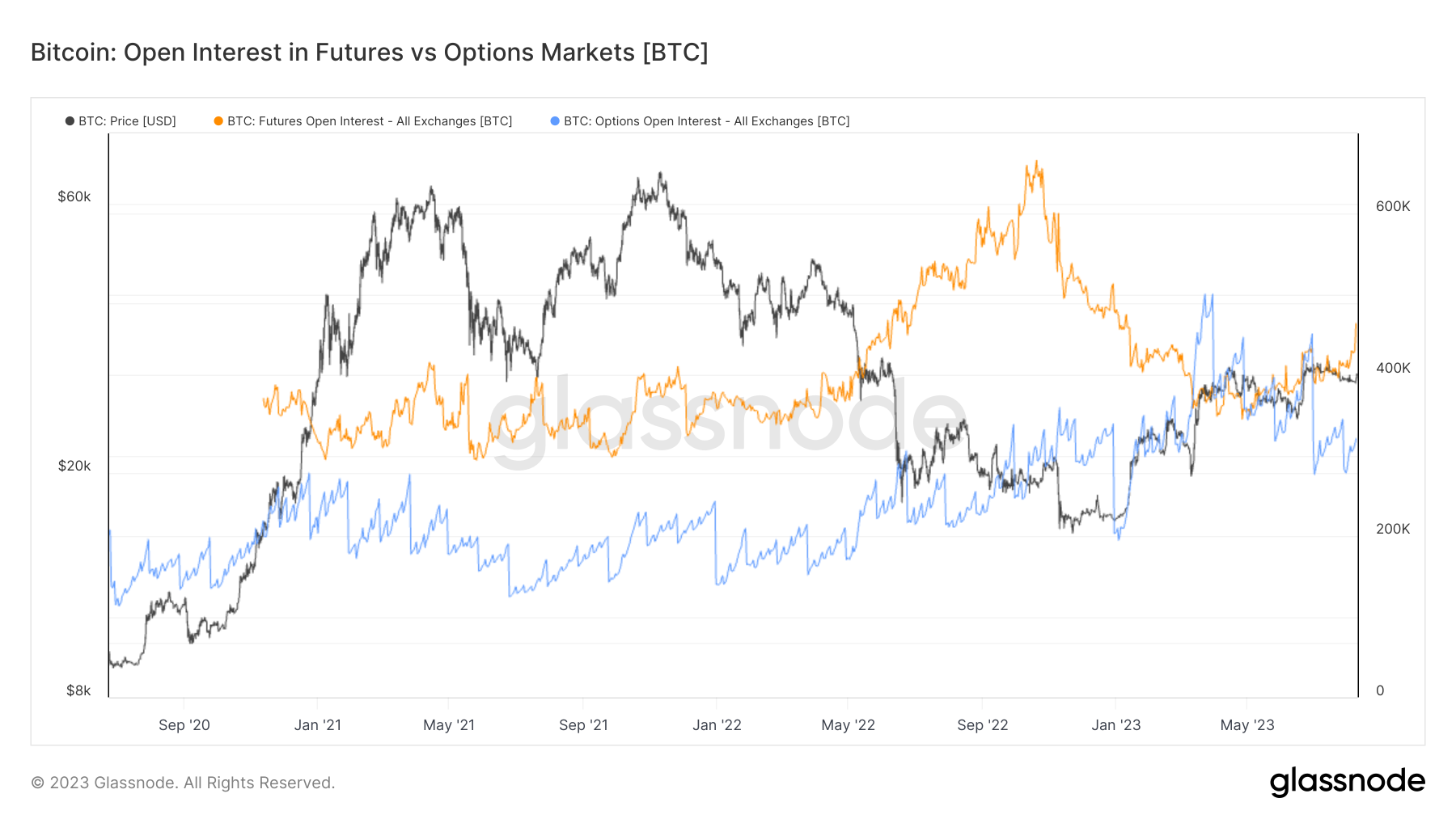

The table offers a platform-specific view, but market dynamics reveal a shift. Historically, Bitcoin futures dominated crypto financial products. However, data from Open Interest in Futures vs Options Markets indicates a change. In the past year, options markets have seen open interest more than double, approaching futures in scale.

In contrast, futures open interest declined in late 2022, specifically when FTX faced setbacks, and has shown only a modest recovery in 2023. This divergence underscores the unique appeal of options. Unlike futures, which commit institutions to buy or sell Bitcoin at a predetermined price, options provide more strategic flexibility. They offer the right, but not the obligation, to execute trades, opening up new tactical avenues. This trend was further validated when CME Group introduced Bitcoin options in early 2020, following the success of its futures contracts.

Conclusion

From their inception on pioneering platforms like Deribit, Bitcoin options have grown to become crucial instruments in the crypto financial ecosystem, especially with their adoption by major financial institutions such as CME Group and Bakkt.

As traders and institutions navigate this space, they are presented with a choice between platforms that are regulated, like CME Group, and those that operate in more flexible regulatory environments. Interestingly, while Bitcoin futures once held dominance in the crypto derivatives sector, the recent surge in the Bitcoin options market indicates a shift in preference among traders. This transformation underlines the ever-evolving nature of the crypto financial landscape and the need for adaptive, strategic instruments like Bitcoin options.

Disclaimer:Past performance is not indicative of future results. This article is intended for informational purposes only, and it does not constitute investment advice. Always conduct thorough research.