DeFi Uncovered: The Battle for Attention

DeFi flirts with renewed growth as NFTs lead capital back into the Ethereum ecosystem.

Title image made using a penguin from NFT collection Pudgy Penguins.

Activity and interest in the DeFi market have found strength this week as capital rotates into Ethereum and governance tokens. ETH has traded and found support above the $3,000 level as the market consolidates after three weeks of strong price performance.

In this weeks analysis, we explore the current flows of capital throughout the Ethereum ecosystem, alongside key metrics to keep watch on for the rest of August. We will also present a weekly feature for an experimental strategy that has seen recent growth in attention and adoption.

Capital Rotation

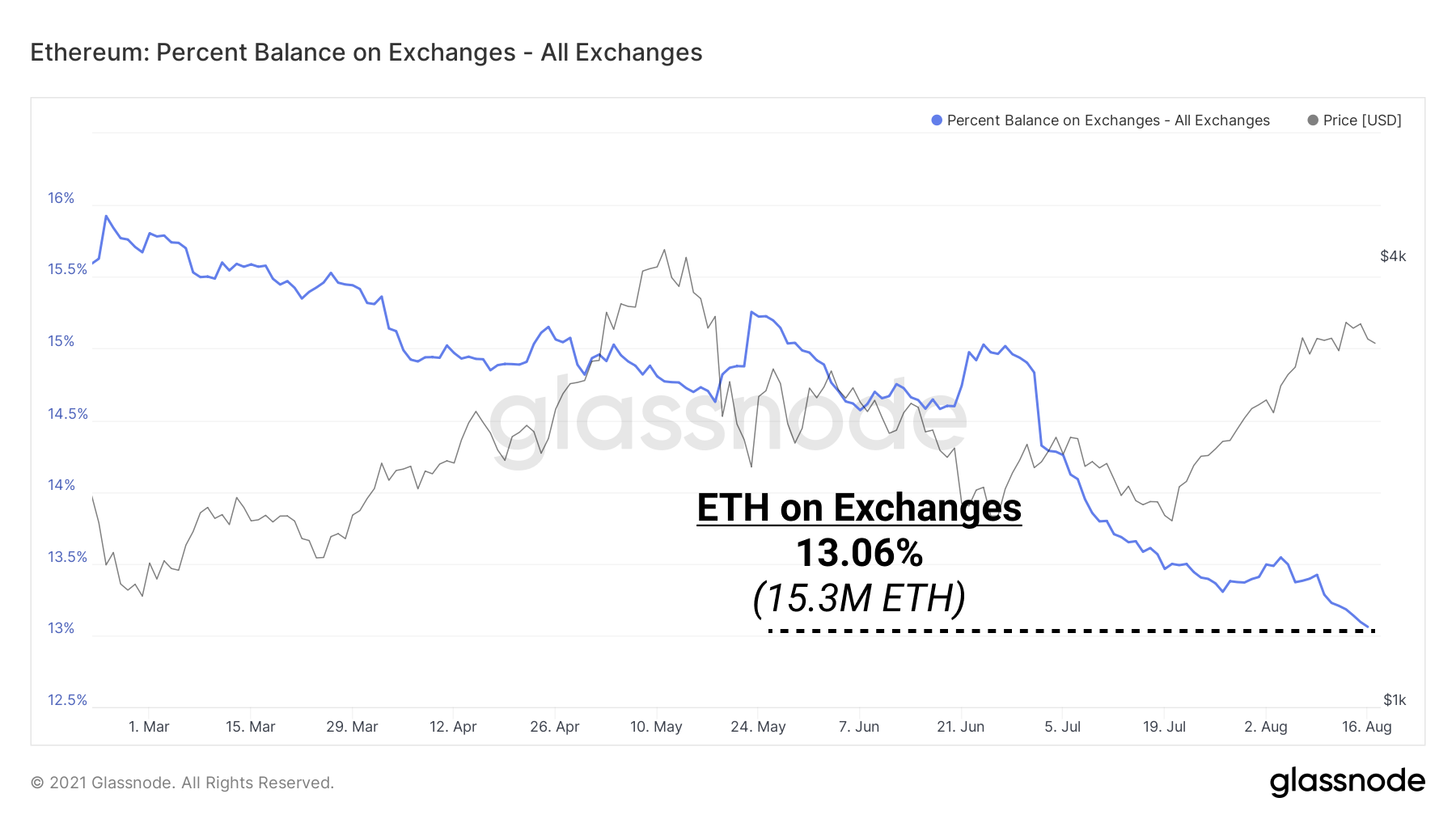

The recent tick up in ETH price has been supported by a continued outflow of ETH supply on exchanges. Exchange ETH balances have now declined to reach an all-time low of 13% of the circulating supply this week, equivalent to 15.3M ETH.

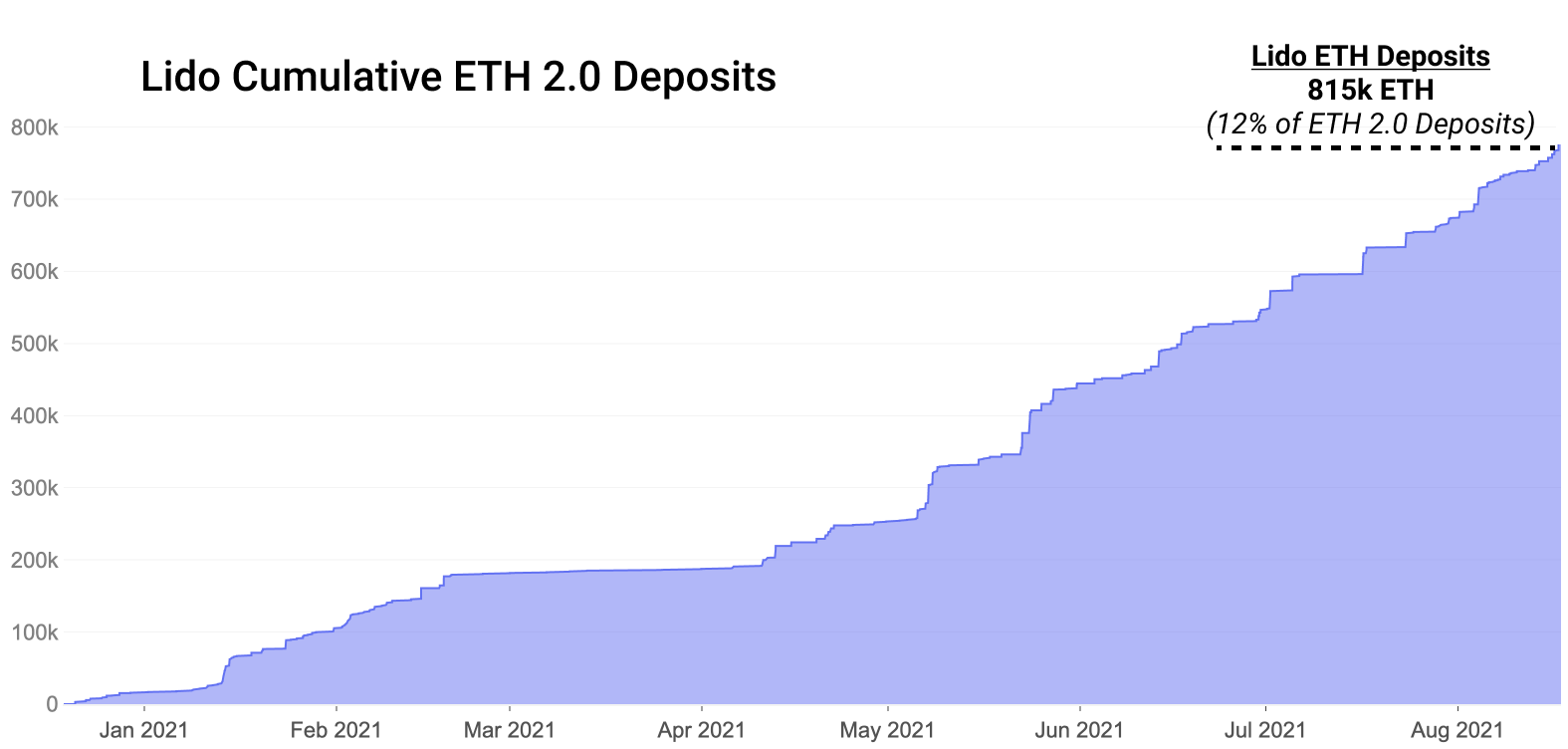

A reasonable volume of ETH is finding its way into the Ethereum 2.0 staking contract, preparing for the network transfer away from Proof-of-Work and towards Proof of Stake. One of the leaders in permissionless staking for ETH is via the DeFi project Lido.

Lido deposits have continued to rocket upward, hitting 12% of total staked supply this week.

That puts Lido total deposits at a value of $2.5B. Their governance token LDO is currently valued at a $100M market cap, and $3.7B fully-diluted valuation. With $2.5B in value staked, this makes for a FDV:TVL ratio equal to 1.48.

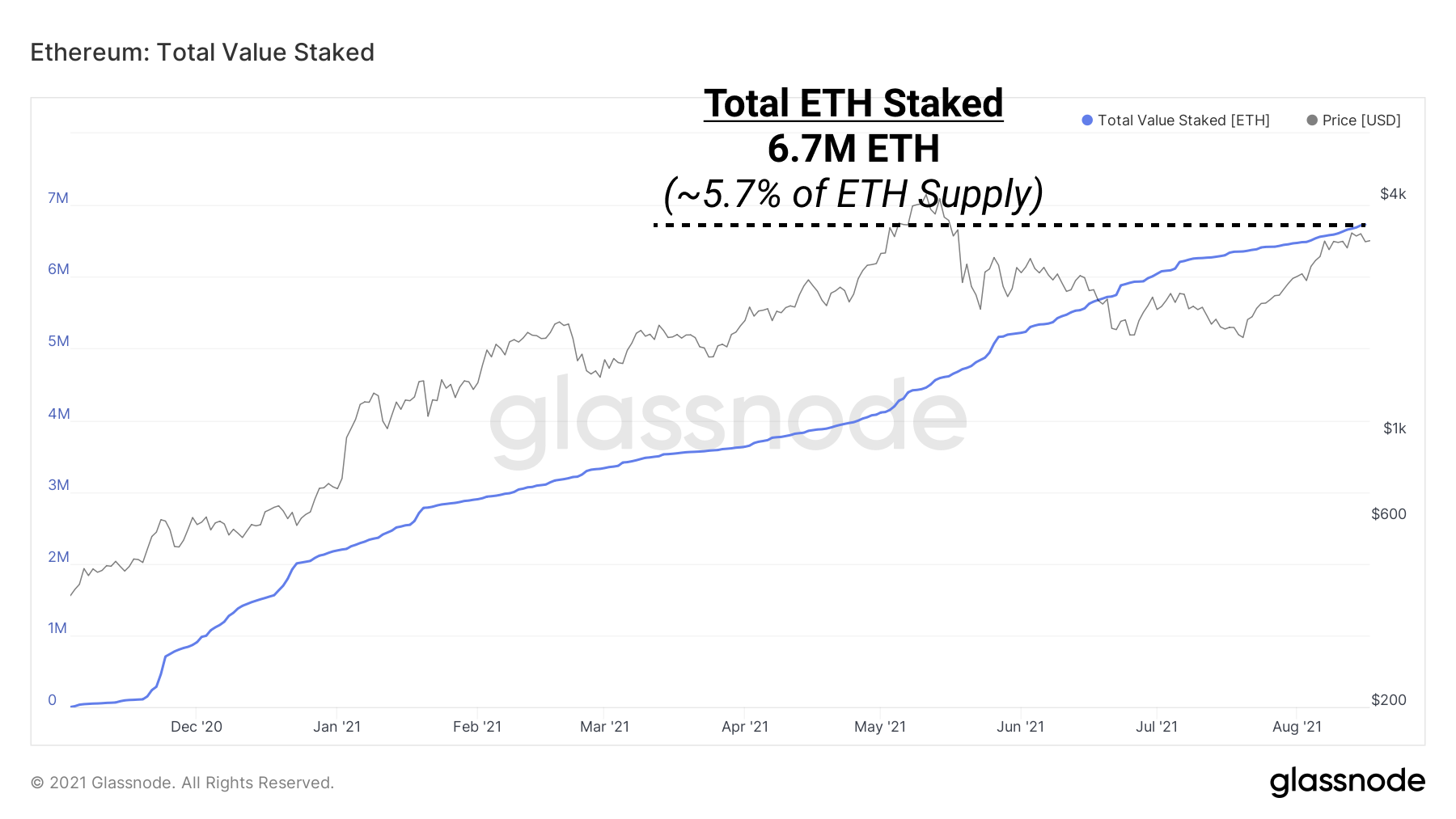

In terms of the total value currently staked in the ETH 2.0 contract, over 6.7M ETH has been deposited, representing 5.7% of the circulating supply. The trend of ETH being withdrawn from exchanges and deposited into yield bearing opportunities in the DeFi space remains a trend to pay attention to.

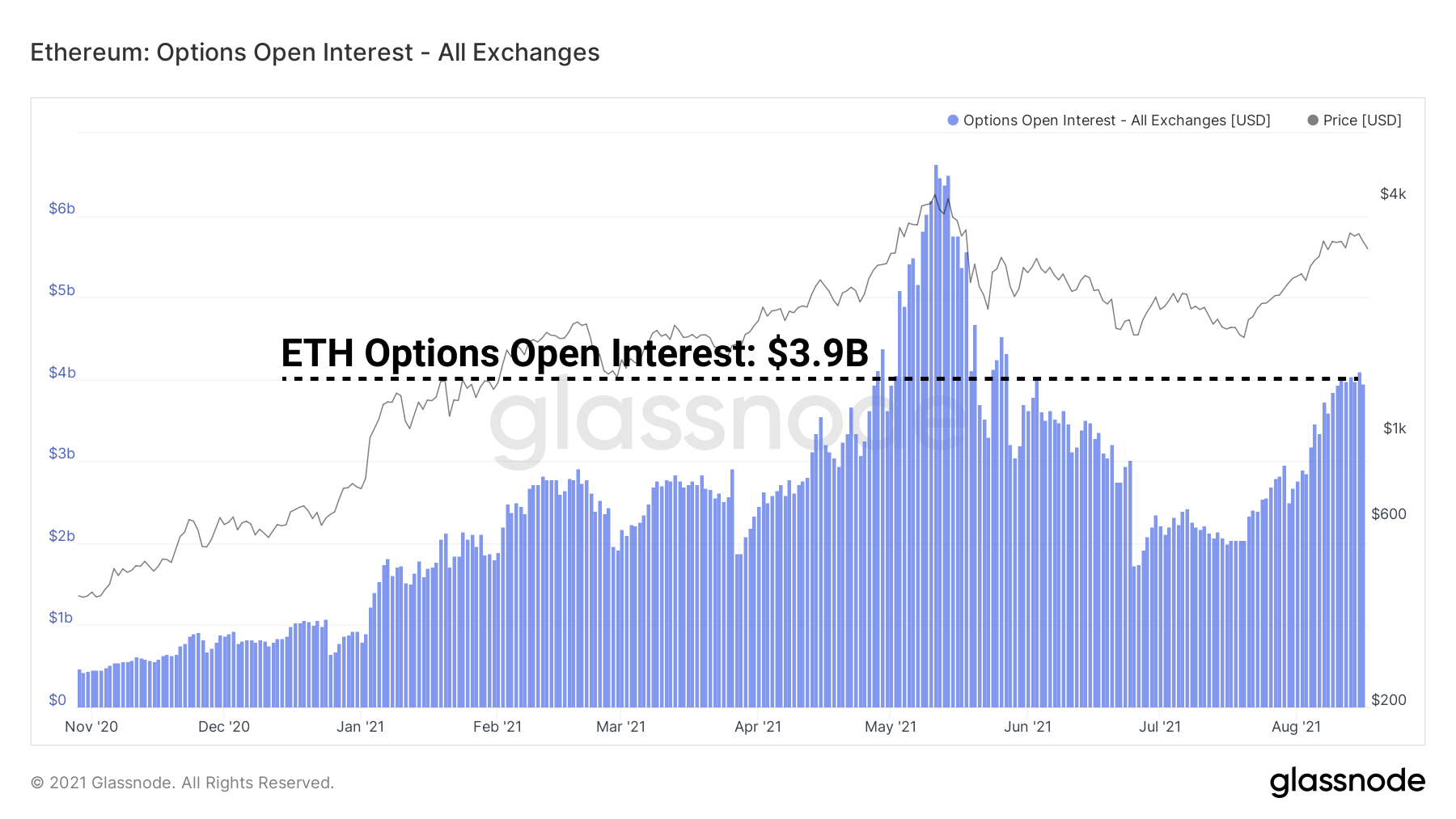

Interest in ETH options markets has also expanded over the last few weeks as traders deploy capital to express a directional view, or hedge existing positions. Open interest in options markets reached $3.9B this week, about 40% below the ATH set in May.

Open interest represents the value of contracts that aren't yet settled or exercised. We can total open interest as well as open option contracts at each strike price per expiration date.

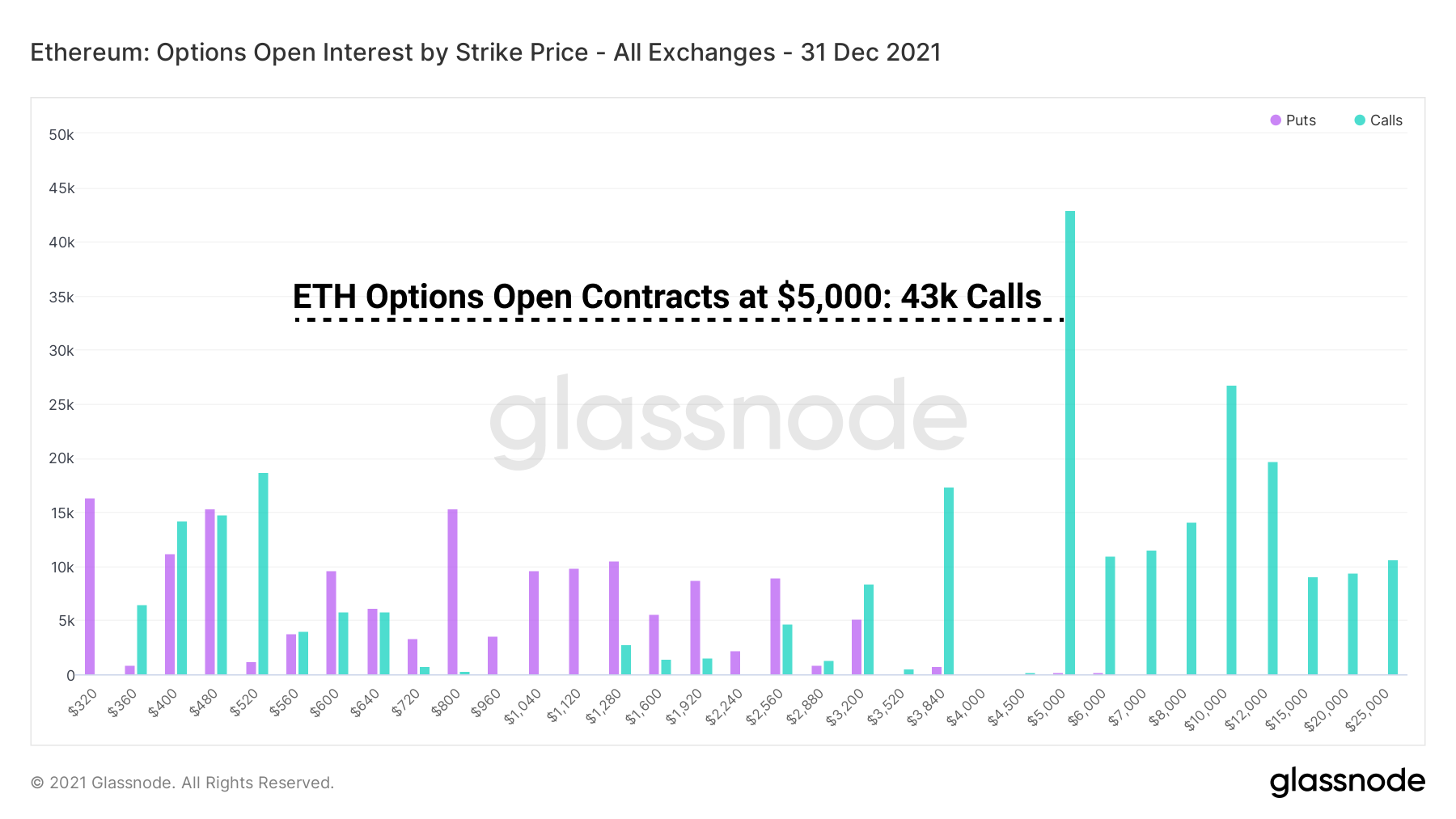

We can look to longer dated options with end of year expiration to get a view of what the options market expects of future price performance. We see a strong interest in out of the money (OTM) calls at the ETH $5,000 level for the end of year 31-Dec contracts. Over 43k call options are currently open at this strike and expiry, with non-trivial open interest also at ETH strike prices in excess of $10k.

Metrics to Watch

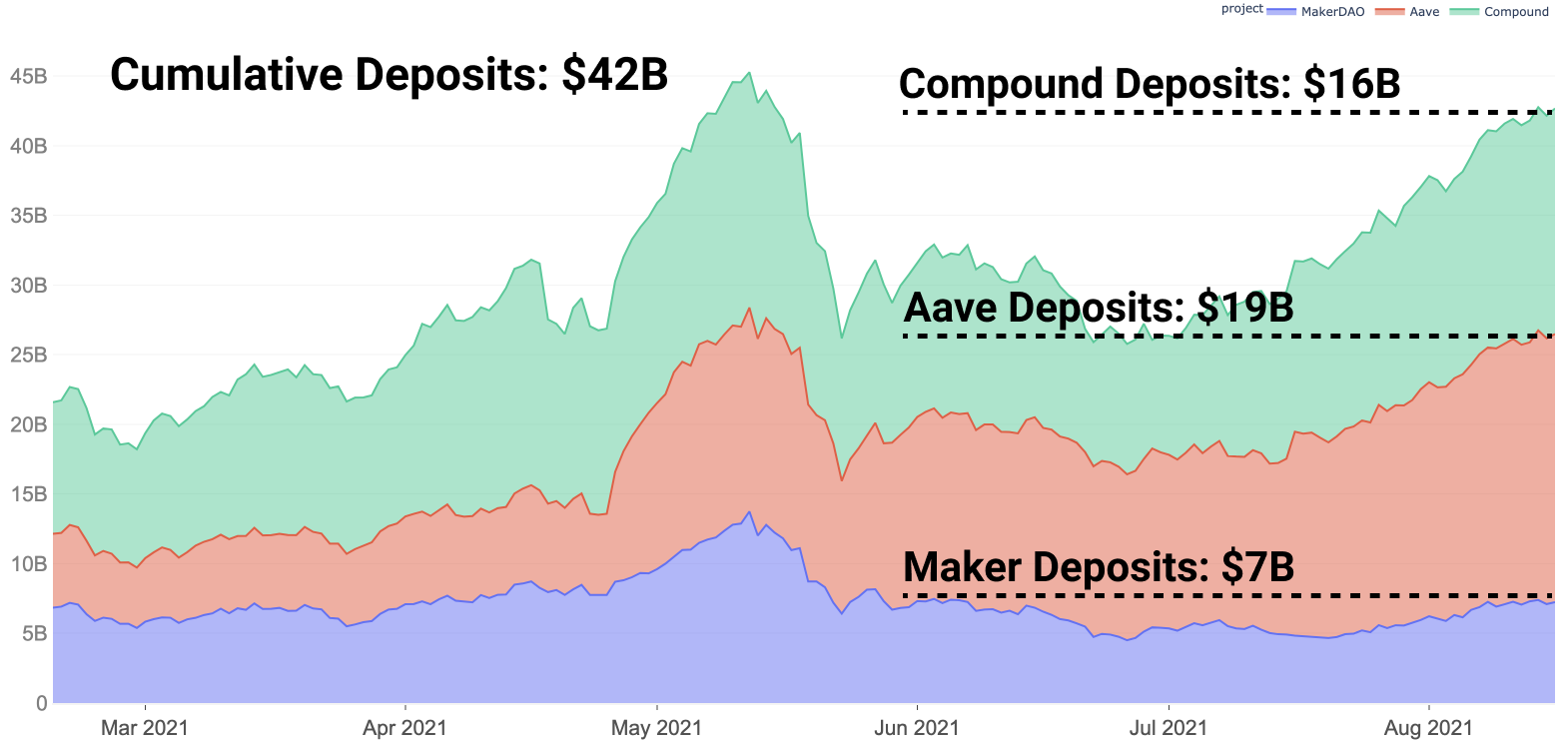

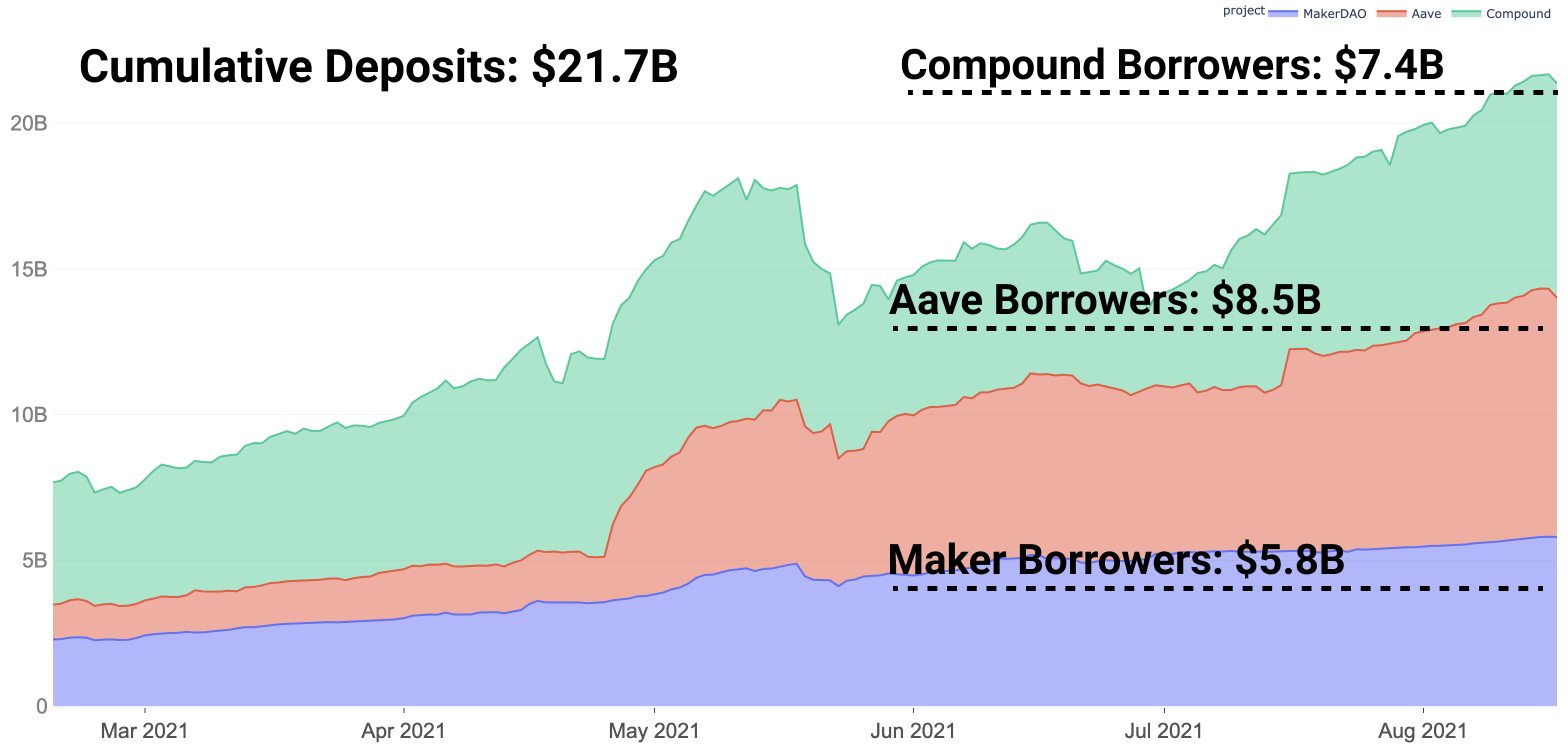

A number of DeFi metrics have ticked positive for the month of August. The first being the volume of deposits and borrow in lending protocols which have increased alongside positive price performance. Between the three market leaders Maker, Aave and Compound, a combined value of $42B is currently deposited as collateral.

Increased borrow marks a renewed interest in risk-on behaviour, with a combined value of borrowed capital hitting $21.7B. Interest rates have also shown some volatility of late, as demand for borrow livens up. Total value borrowed has surpassed the ATH set in May whilst total deposited collateral remains slightly below the ATH by $2B.

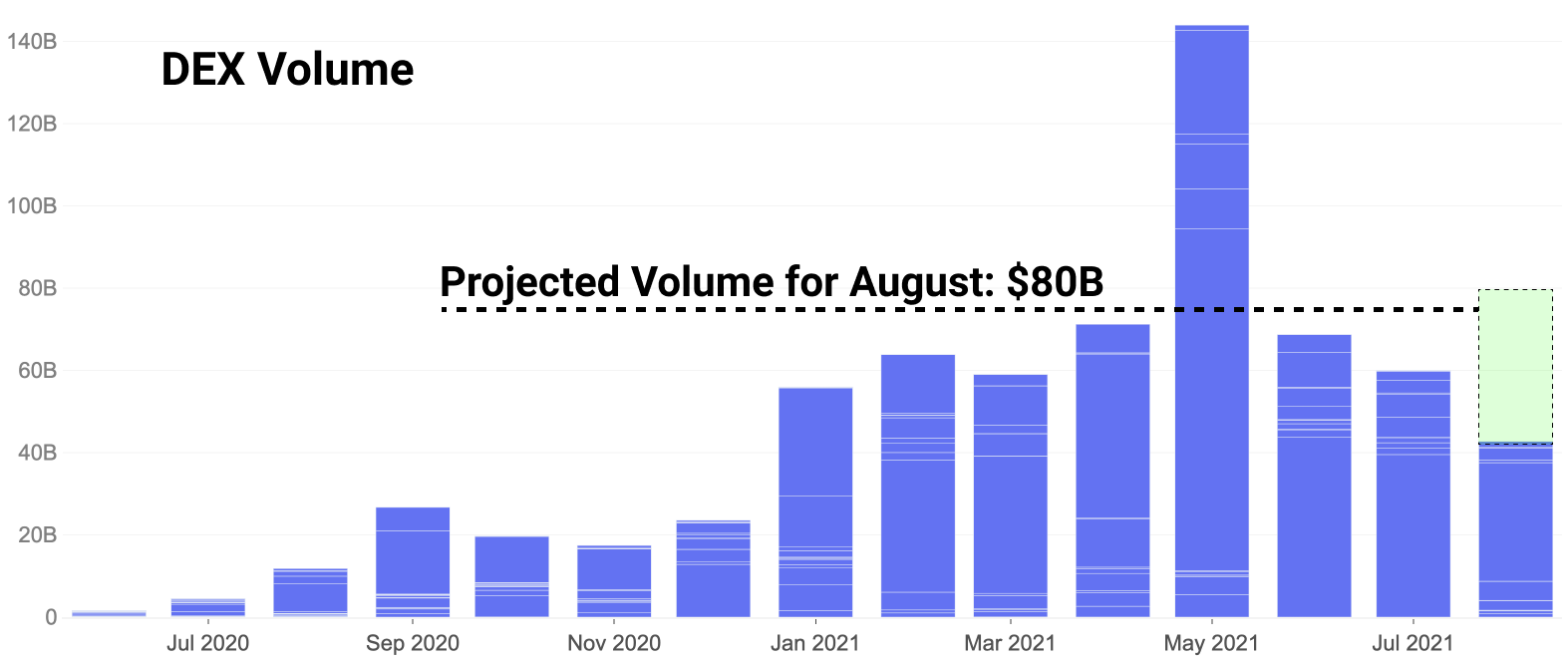

Meanwhile, DEX activity is looking healthier, with monthly estimates set to print a growth in volume relative to previous months. The total trade volume at the time of writing is $46B, and is on-track to reach approximately $80B for the month of August.

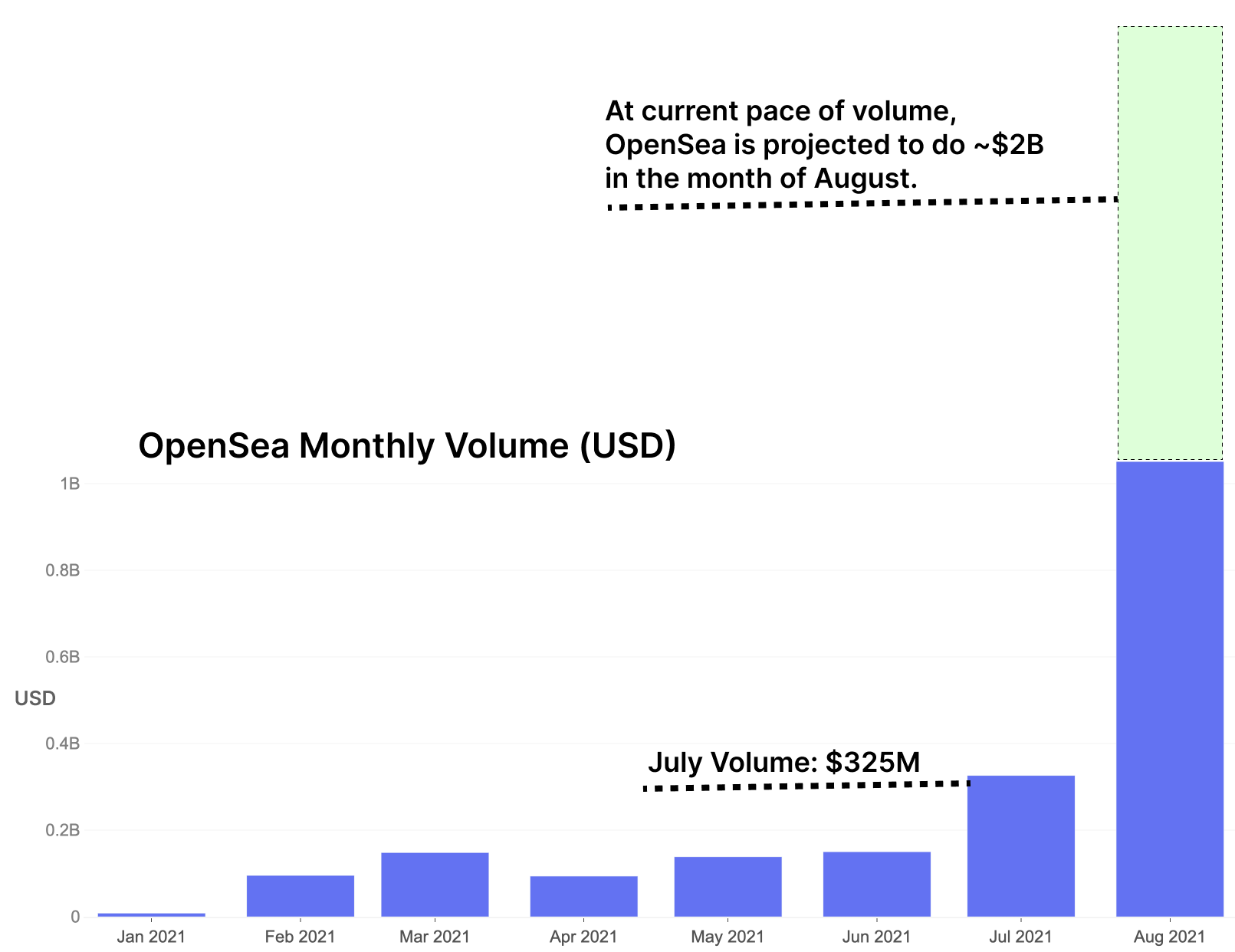

NFTs remain a leading narrative for Ethereum in the current market. In our introductory piece to NFTs we showed a projected OpenSea volume of $1B a few days into August. Half way through August the volume has already exceeded $1B.

Revised estimates now put OpenSea on track for a monthly volume just south of $2B for August. For comparison, number two DEX by volume Sushiswap has done about $4.7B in volume so far this month, putting Opensea's $1B at around 20% of Sushiswap's volume.

Featured Strategy: Tokemak, a New Strategy for Collectivized Liquidity

Note: this is a new and upcoming experimental protocol. Depositors should acknowledge the heightened risk of smart contract exploit or other potential issues.

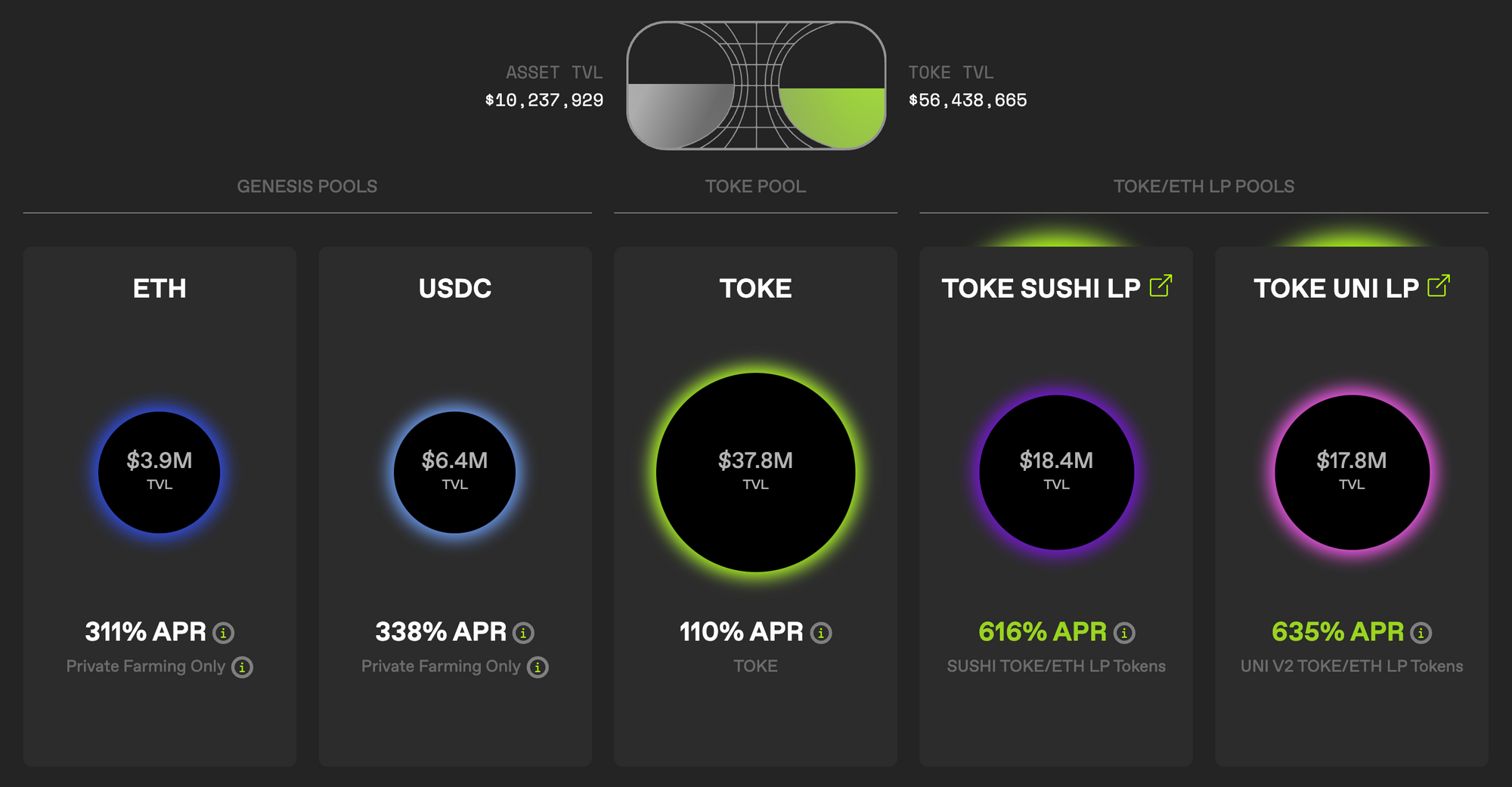

A new experiment in DEX liquidity provision has hopped on the scene in Tokemak. The protocol's intent is to provide a fresh new approach to the loyalty liquidity problem. It offers single-sided liquidity provision and impermanent loss protection for depositors. Funds deposited in Tokemak are put into pools on existing exchanges, earning yield for the Tokemak treasury backing $TOKE.

Depositors are incentivized by $TOKE rewards and protection against impermanent loss (IL) via governance token TOKE, not unlike how Bancor protects against IL with its governance token.

The protocol finished its so-called "DeGenesis" event, issuing its governance token TOKE to commitments in its initial offering. DeGenesis participants also get early access to the protocol during the private farming stage for the ETH/USDC pool.

So how does the protocol work?

Tokemak's ultimate goal is to present more sticky and predictable liquidity. At present, whales and traditional market makers play a significant role in liquidity provision, lacking loyalty and moving their funds as they see fit. This behaviour often results in liquidity leaving a protocol all at once. Without liquidity, token holders can be left holding the bag.

Tokemak thinks it can create more sticky liquidity by pooling users' capital and directing liquidity across pools via liquidity directors. Allocators can provide single-sided pool 1 liquidity, holding solely the governance token instead of exposing themselves to impermanent loss and an added asset.

How do these collective liquidity efforts create more sticky and efficient liquidity?

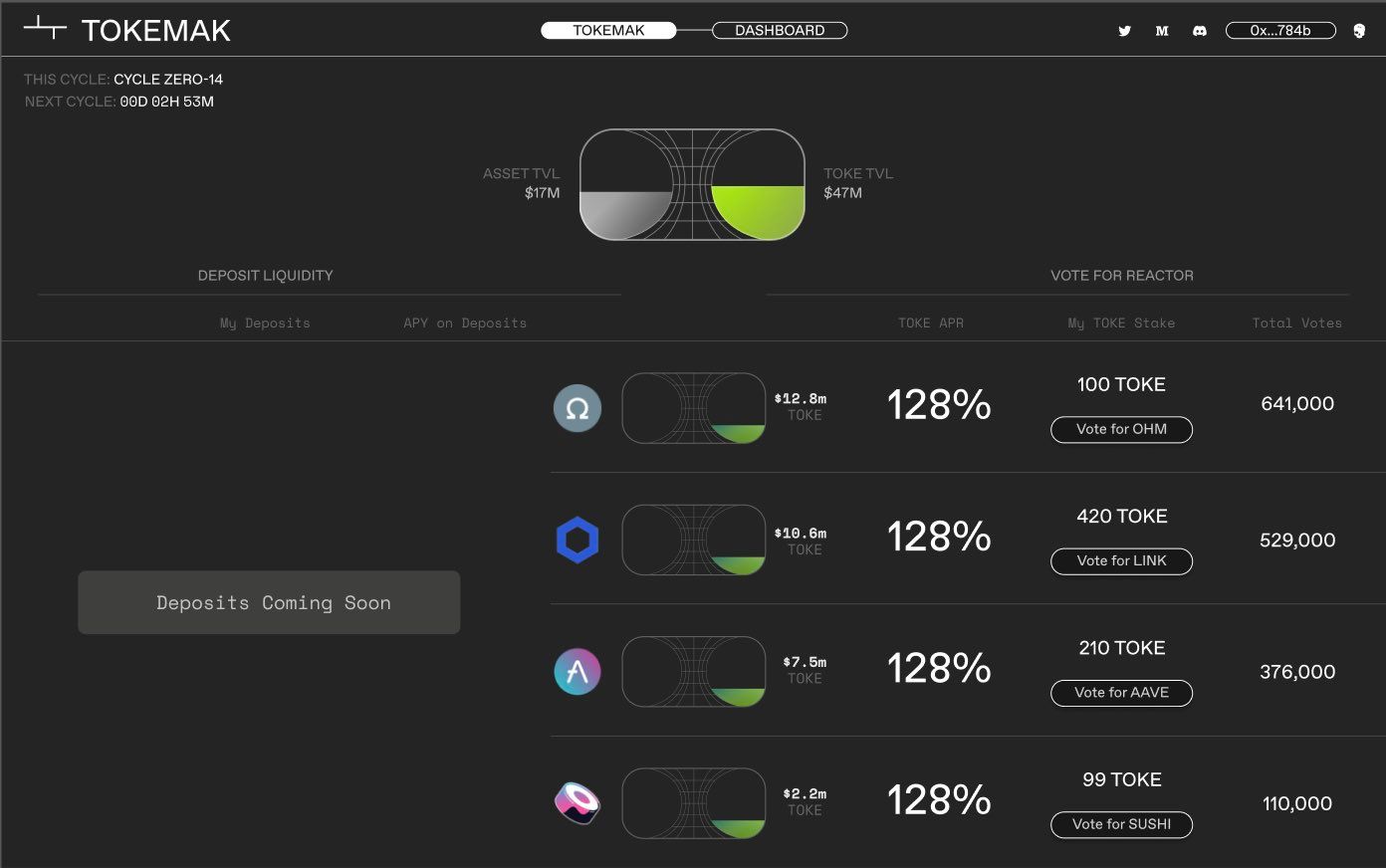

- Users vote in pools they would like to see on Tokemak. Single-sided liquidity becomes available for those pools.

- Liquidity directors actively vote for how liquidity should move between protocols.

- When deposits are unbalanced from how the liquidity directors have set them, added $TOKE incentives work to balance these pools of capital.

- Capital is slower moving, more predictable, and more sticky by merit of size, speed to coordinate, and set cycles for adding/withdrawing capital.

- Liquidity providers are offered protection against IL via subsidies from the $TOKE governance token.

- Users can allocate capital in and out of "reactors" in cycles, slowing down movement of liquidity and allowing longer signalling in each "reactor" for $TOKE rewards according to liquidity director set parameters. 24 hour cycles for now, eventually transitioning to 7 day.

This creates an interesting set of incentives at size. For example, projects may be incentivized to accumulate TOKE to try and vote to direct funds towards their project. All sorts of interesting game theory can arise if liquidity cabals that form in Tokemak reach considerable size.

Imagine I'm an early stage project with limited liquidity. One might be incentivized to purchase $TOKE and rally other holders to allocate liquidity in Tokemak towards my project's pools.

Larger projects can also play these games, not unlike what we've seen with Yearn vs Convex vs StakeDAO in battling on Curve via the $CRV governance token.

Already we've seen communities rally on Twitter around votes for adding their project to Tokemak for added liquidity. (Note: the below picture is just a mockup of the future voting process)

Why is sticky liquidity important? When liquidity exits a protocol the token price is vulnerable to added volatility. With low liquidity there are fat spreads and larger price impact. Token holders can't buy in and out without significantly moving markets. Added volatility can result in increased impermanent loss (IL) for liquidity providers. Increased IL can cause more liquidity to leave. A reflexive process ensues. Tokemak attempts to solve this with more sticky/predictable liquidity and subsidizing impermanent loss with their $TOKE governance token.

Tokemak is certainly no guarantee for fixing this problem, but it's an interesting experiment in shaking up liquidity provision.

How can Tokemak be an interesting strategy as an end-user of the protocol?

For now, their yields are inflated by heightened $TOKE rewards as an incentive for providing liquidity. Soon the private farms (reactors) will be released, offering single-sided yields at 300%+ APR for early depositors. Compounding monthly that's 2,000% APY. Expect this yield to quickly go down once deposits go public and liquidity floods into the protocol.

Should demand for the $TOKE token remain, strong rewards will remain strong, heavily incentivized by their governance token. Should $TOKE value depress yields from allocation to Tokemak will express depressed yield in $TOKE.

Take note that fees from the swaps are not rewarded to liquidity providers and liquidity directors in $TOKE. They are purely rewarded in $TOKE. Instead, those fees are given to the protocol treasury, growing a treasury full of assets controlled by $TOKE holders. This focus on "protocol controlled value" is not unlike how $OHM controls assets in a treasury that back the value of the asset.

Tokemak presents a potential new paradigm where collections of users and protocols can lobby and swing the weight of their votes towards managing large amounts of liquidity.

Will Tokemak democratize liquidity, giving smaller providers more weight, enabling a solution to the sticky liquidity problem? Or will this just result in a number of liquidity cabals, swinging large $TOKE swords to allocate capital according to handshake deals and decision making at the whims of large holders? Time will tell.

Closing Thoughts

The Ethereum ecosystem has found some strength this week as ETH tokens flow out of exchanges and staked ETH pushes to new all-time highs. Simultaneously, lending protocols also approach new all-time highs by the total deposit and total borrow. NFTs continue to be a leading narrative in crypto, with OpenSea volumes reaching new heights.

As sticky liquidity remains a key concern, Tokemak has hopped onto the scene as an interesting experiment towards incentivizing collectivized liquidity. The token has shown strength as many participants in DeFi bet on its capability to integrate with and incentivize liquidity in major projects across the space.

Uncovering Alpha

This is our weekly segment that briefly discusses some of the most important developments of the prior and upcoming weeks.

Builder momentum continues as products launch and new versions get released across all major chains.

- Yearn founder Andre Cronje continues the governance wars with bribe. Bribe is another active step in the governance battles, the largest stage being Curve. Bribe allows one to add incentives that will be distributed to voters. Other products have been launched recently which allow sale of votes.

- Cowswap adds Balancer support. MEV-protected trades come to Balancer with a partnership via Cowswap. Access Balancer liquidity alongside MEV protection from Cowswap.

- Paradigm security researcher samczsun finds a vulnerability in Sushi's Miso platform. His whitehat find saved the protocol from potential blackhat exploits, allowing the flaw to be patched before it could be exploited.

- Biconomy launches a faster Polygon bridge. Named Hyphen, the bridge is a high-speed bridge which offers instant deposit and withdrawals, vs the existing ~hour long withdrawals from Polygon to Ethereum.

- Research efforts from on-chain derivatives builders - options LM from Andre and Pods, power perps from Paradigm and Opyn. A few interesting research efforts were presented this week. options LM provides liquidity mining with an option layered on top. Power perps offer an instrument that reprices based on power law.

- Genie adds limit orders to their NFT marketplace. Genie, a platform for swapping NFTs added limit orders to their marketplace.

- Polygon acquires Hermez. In an attempt to improve and expand their scaling capabilities, Polygon acquires Hermez for their ZK-Rollups. Hermez token jumped up in response to the inflated token acquisition price.

- BitDAO raised $350M via a token sale on Sushi's Miso. The DAO seeks to build and support DeFi projects across the ecosystem.

- Cream Finance updates their staking. iceCream is the new name for the variable length staking contract.

- Follow us and reach out on Twitter

- Join our Telegram channel

- For on–chain metrics and activity graphs, visit Glassnode Studio

- For automated alerts on core on–chain metrics and activity on exchanges, visit our Glassnode Alerts Twitter

Disclaimer: This report does not provide any investment advice. All data is provided for information purposes only. No investment decision shall be based on the information provided here and you are solely responsible for your own investment decisions.