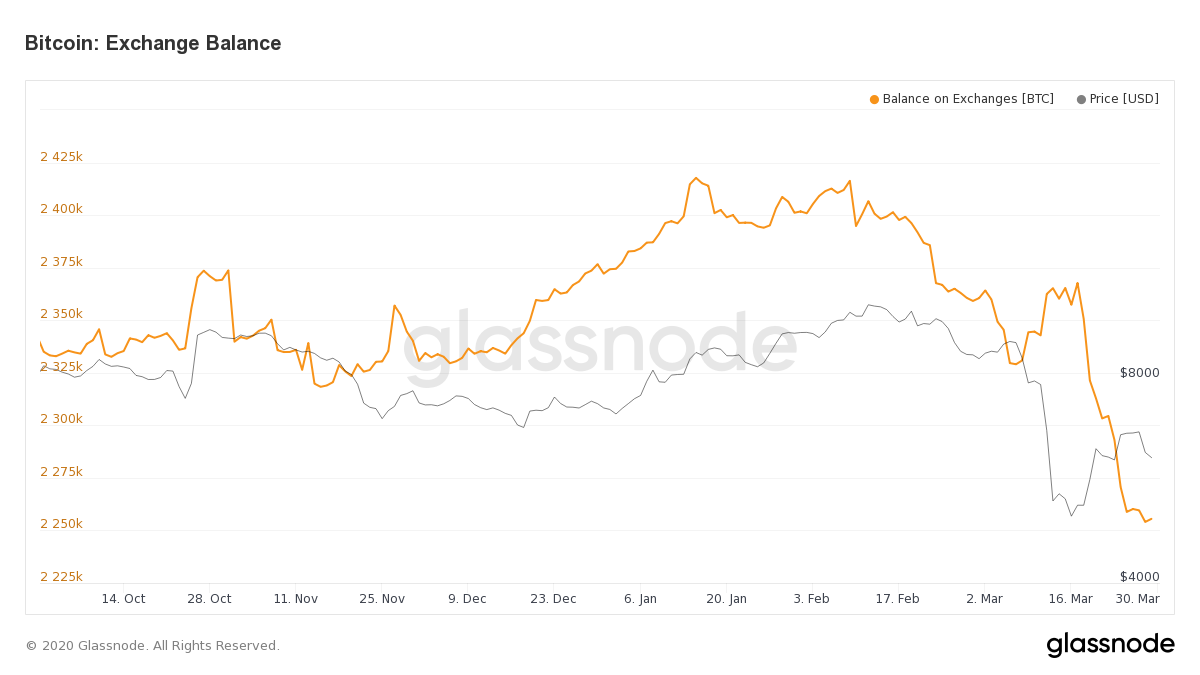

The Number of BTC On Exchanges Is Down Almost 7%

Following the recent price crash, the balance of BTC on exchanges has decreased by almost 7%, despite unusually large exchange deposits.

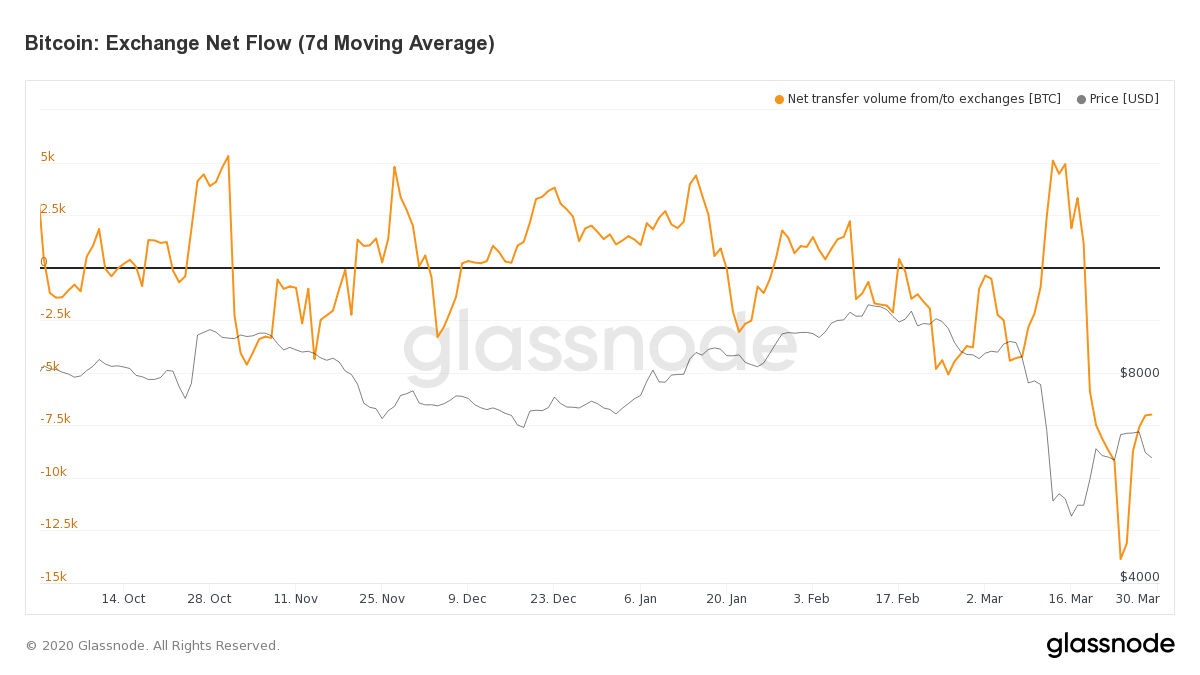

BTC is Leaving Exchanges

Bitcoin's exchange net flow shows that BTC has been leaving exchanges following the recent price dip.

While this has started to recover since the price has stabilized, net flow of BTC to exchanges is still extremely low compared to historical levels.

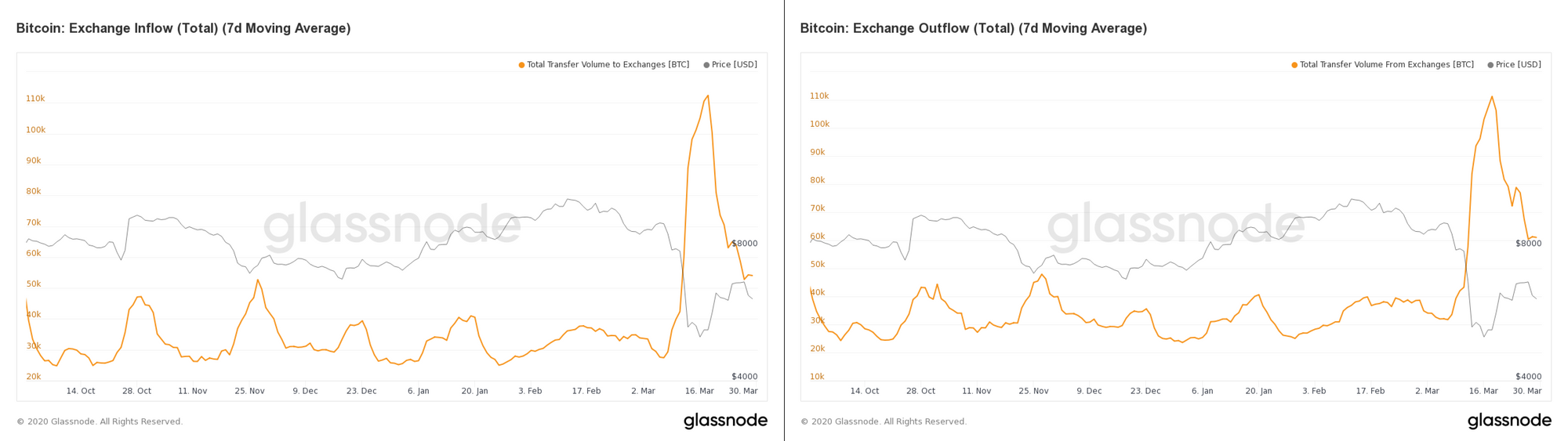

This is explained by the disparity between exchange inflow and outflow. The volume of BTC flowing into exchanges spiked significantly when the price crashed, but has since declined. Exchange outflow also experienced a spike, but its subsequent decline has been smaller than that of inflow.

In other words, exchange outflow is outpacing inflow. This has had the effect of reducing the total balance of BTC on exchanges, which has dropped by close to 7% from its February high.

Average Size of BTC Exchange Deposits Has Increased

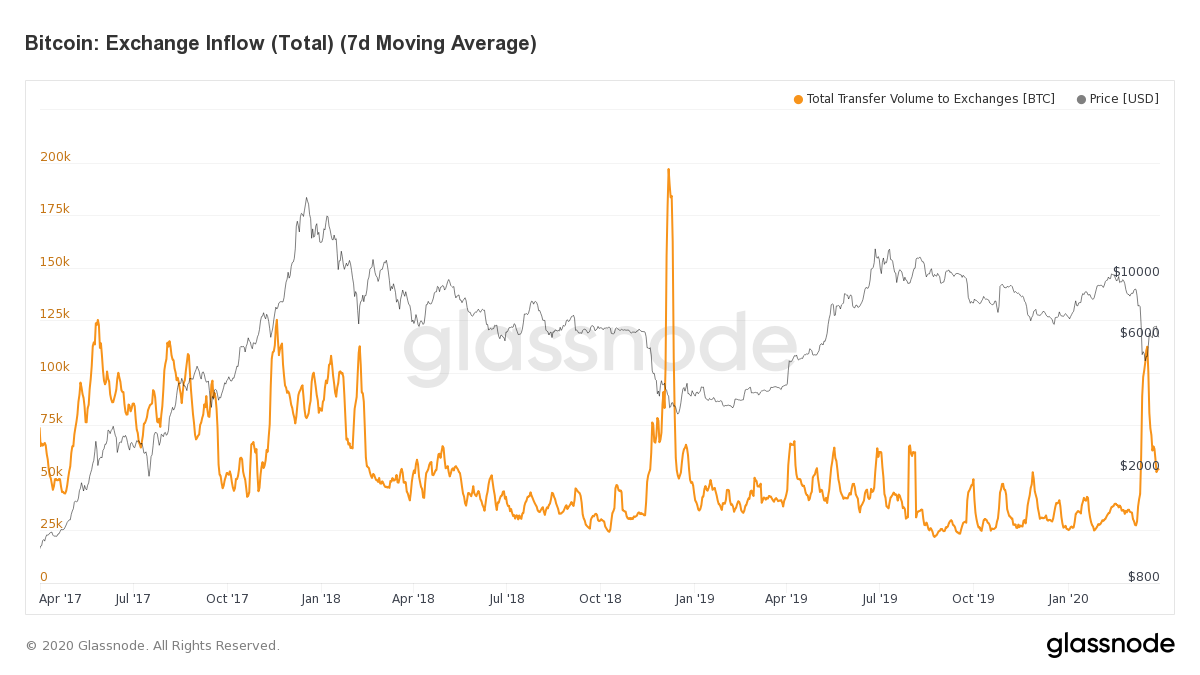

While the total volume of exchange inflow (in BTC terms) is lower than the total outflow, it is still at relatively high levels when compared to longer-term historical data.

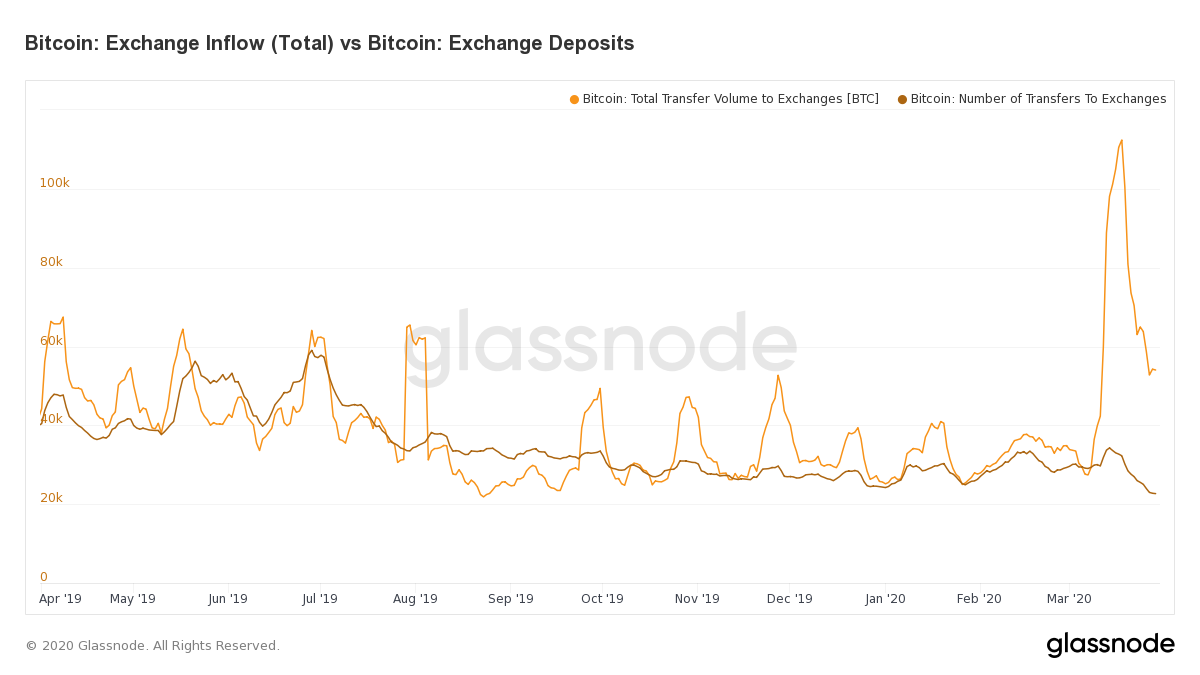

However, unlike deposit volume, the total number of daily deposits to exchanges is at its lowest level in the past 3 years. The number of daily BTC deposits to exchanges hasn't been this low since September 2016, 3 and a half years ago.

When compared on the same chart, we see that the current disparity between the number of deposits to exchanges vs. the volume of deposits to exchanges is uncharacteristically large.

This means that the average size of BTC deposits to exchanges is far higher than usual. This has been the case since early March 2020.

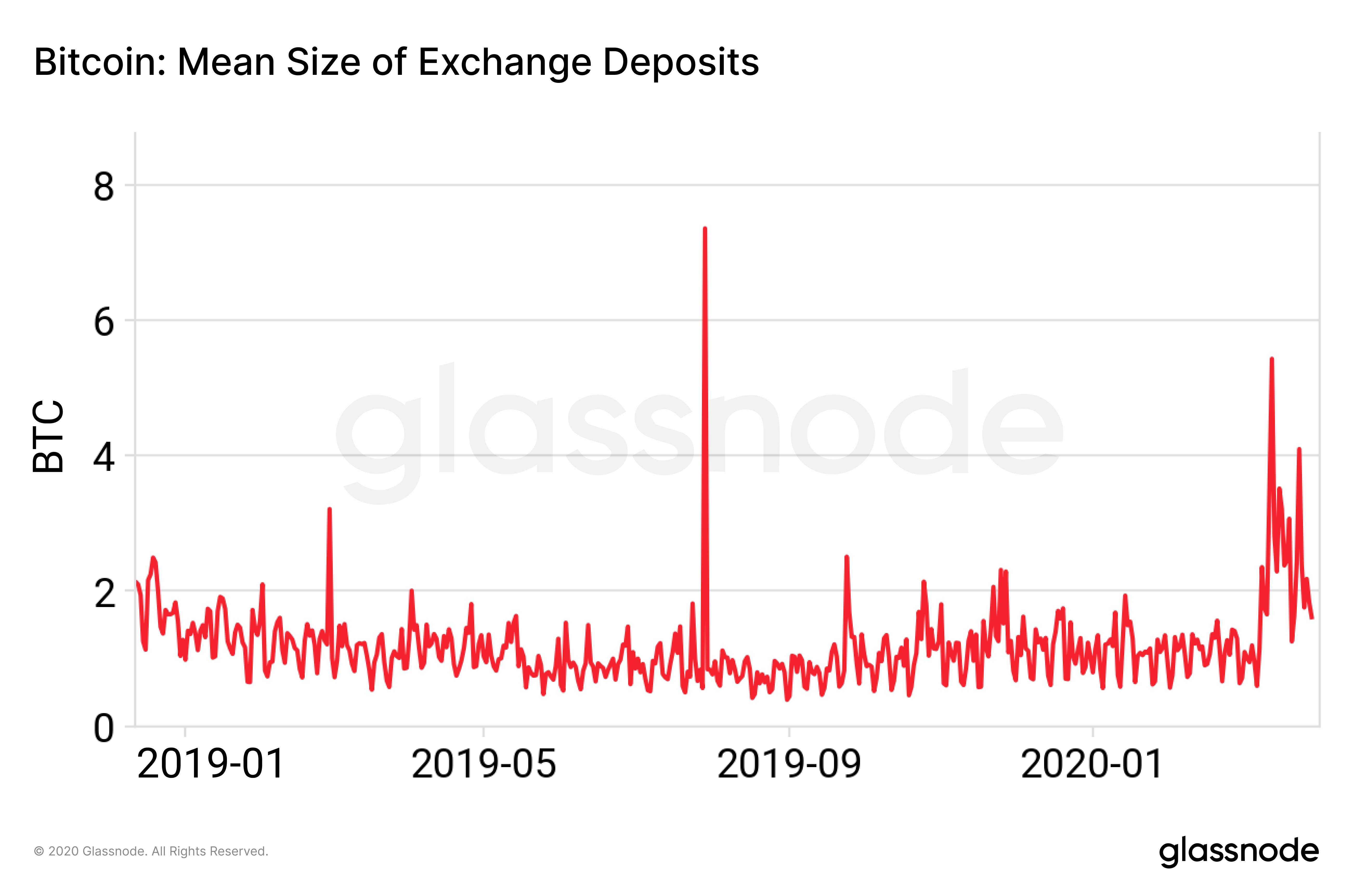

As this chart shows, the mean size of exchange deposits usually fluctuates around 1 BTC. However, during the recent price crash, the mean value of exchange deposits shot up to over 5 BTC, and is still hovering around the higher end of the range of normal fluctuations, at around 1.8 BTC per deposit (on average).

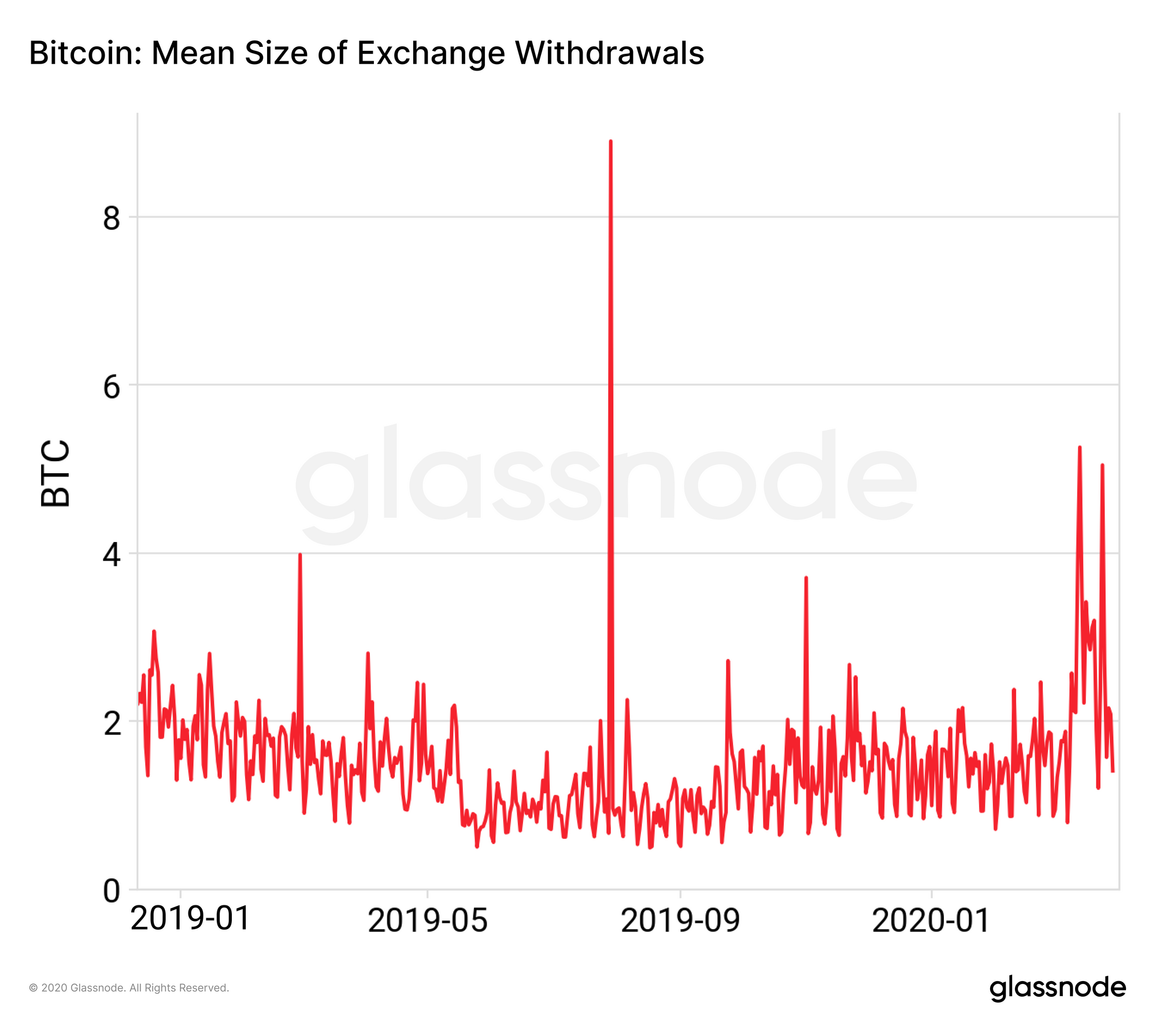

In contrast, the mean size of exchange withdrawals has returned to well within the range of normal fluctuations after experiencing a similar spike during the crash.

This disparity in the mean size of deposits vs. withdrawals, along with the disparity in the absolute amounts of deposits vs. withdrawals, explains why the net flow of BTC to exchanges is negative.

Conclusions

The significant spike in the size of deposits and withdrawals following the price crash in early March indicates that market participants were making larger-than-usual trades in response to the crash.

The fact that the number of deposits and withdrawals during this time period did not deviate significantly from their normal range suggests that the increase in exchange inflow and outflow was not caused by an influx of holders selling, but rather by active market participants increasing the size of their trades.

Overall, following the crash, the large (and so far sustained) decrease in the number of bitcoin on exchanges may be a positive sign, as it reduces BTC liquidity and thereby restricts the readily available supply. It may also signal that investors are solidifying longer-term positions after responding to the significant price movements earlier this month.

Keep an eye on BTC Exchange Balance to see whether this trend continues.

- Follow us and reach out on Twitter

- For on–chain metrics and activity graphs, visit Glassnode Studio

- For automated alerts on core on–chain metrics and activity on exchanges, visit our Glassnode Alerts Twitter

Disclaimer: This report does not provide any investment advice. All data is provided for information purposes only. No investment decision shall be based on the information provided here and you are solely responsible for your own investment decisions.