Dealing With The DeFi Downtrend

DeFi on the Ethereum is a centrepiece of the ecosystem, with DeFi protocols being a destination for tokens, stablecoins and NFTs alike. However, DeFi tokens remain in a multi-year, and relentless bearish trend. In this piece, we uncover why this may be.

The flexibility of the Ethereum application layer has become a remarkable bedrock for innovation, narrative generation, and software development. As new primitives are created, it sparks both hype, excitement, and innovation, alongside its fair share of malicious activity taking advantage. Overall, this innovation builds towards longer-term adoption, and brings in new waves of capital and talent to the ecosystem.

New Cycle, New Narratives

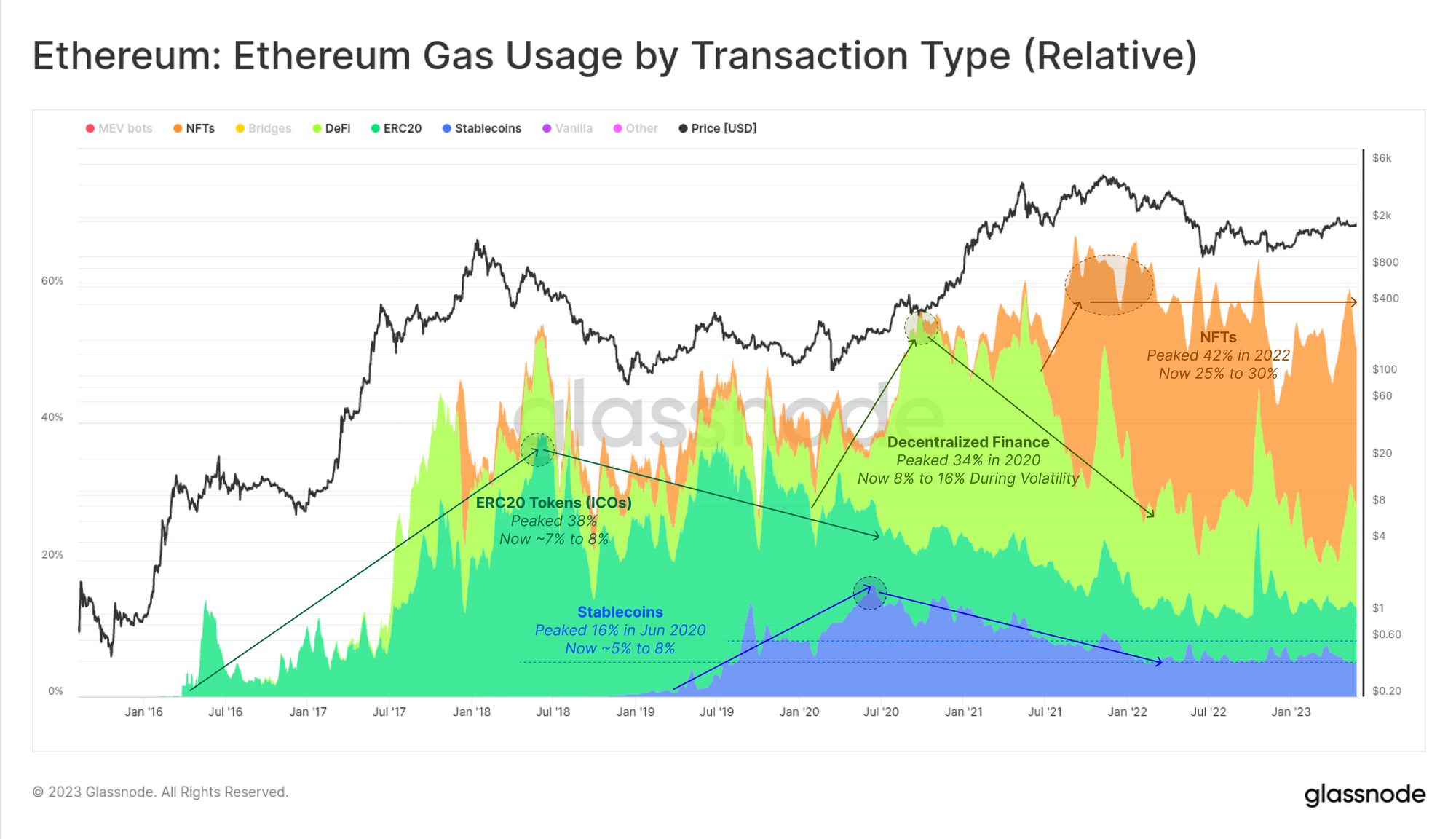

By comparing gas usage across a variety of major activity types, we can establish a baseline for user demand. From this, we can start to identify the four major narratives that have shaped the Ethereum ecosystem to date, often supporting a new all-time high for the ETH price during their peaks:

- 🟢 Initial Coin Offerings (ICOs). Crypto's equivalent of IPOs peaked in 2017 and 2018, with up to 40% of gas used on Ethereum being attributed to ERC-20 token transfers. Although demand for ERC-20 token transfers has decreased since then, it remains a notable source of gas consumption today, driven by the popularity of Memecoins, and new token distribution methods like Yield Farming and Airdrops.

- 🟡 Decentralized Finance (DeFi) rose to prominence in 2020, with the promise of creating on-chain financial primitives and instruments that can be used without traditional intermediaries. The DeFi wave also continues today, however its peak usage was reached June 2020 to 2021, where it accounted for around 30% of gas usage.

- 🟠 Non-Fungible Tokens (NFTs) introduced unique representations of digital or real-world assets. Whilst NFTs have been in existence for many years, it wasn't until mid-2021 that they found their way into mainstream awareness. Although the demand for NFTs decreased towards the end of 2022, they have recently made a comeback, which can be attributed to multiple factors (please refer to our report in WoC 09).

- 🔵 Stablecoins, particularly those pegged to the US dollar, have experienced a surge in user demand since mid-2020. The decrease in gas usage from stablecoin transactions reflects a shift in their change in utility more than a decrease in demand. Stablecoins are now used less as a payment method but more for hedging and as a store of value.

What we can see is a a pattern where an initial boom-bust cycle occurs, pushing the new application to 30% to 40% of all gas consumption. This is then followed by structural decline towards what appears to be a baseline 8% of consumption for these major application types.

The DeFi Downtrend

Of particular note in the chart above is the unique behaviour of the DeFi sector. Gas consumption has semi-regular bursts of activity, where gas demand for DeFi often doubles. This is usually centered around periods of elevated market volatility, as investors re-collateralise, deleverage, or get liquidated on their on-chain margined positions.

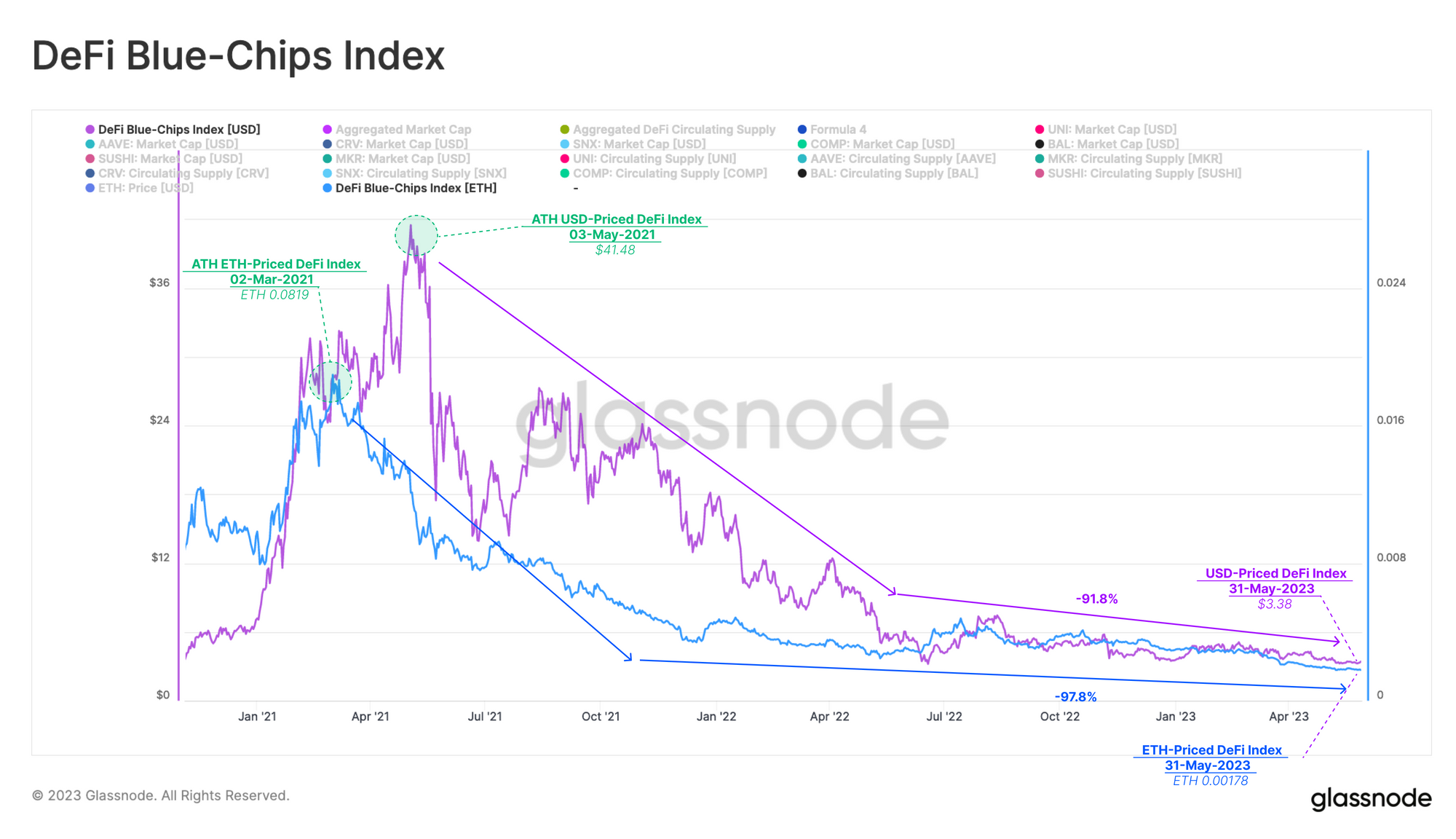

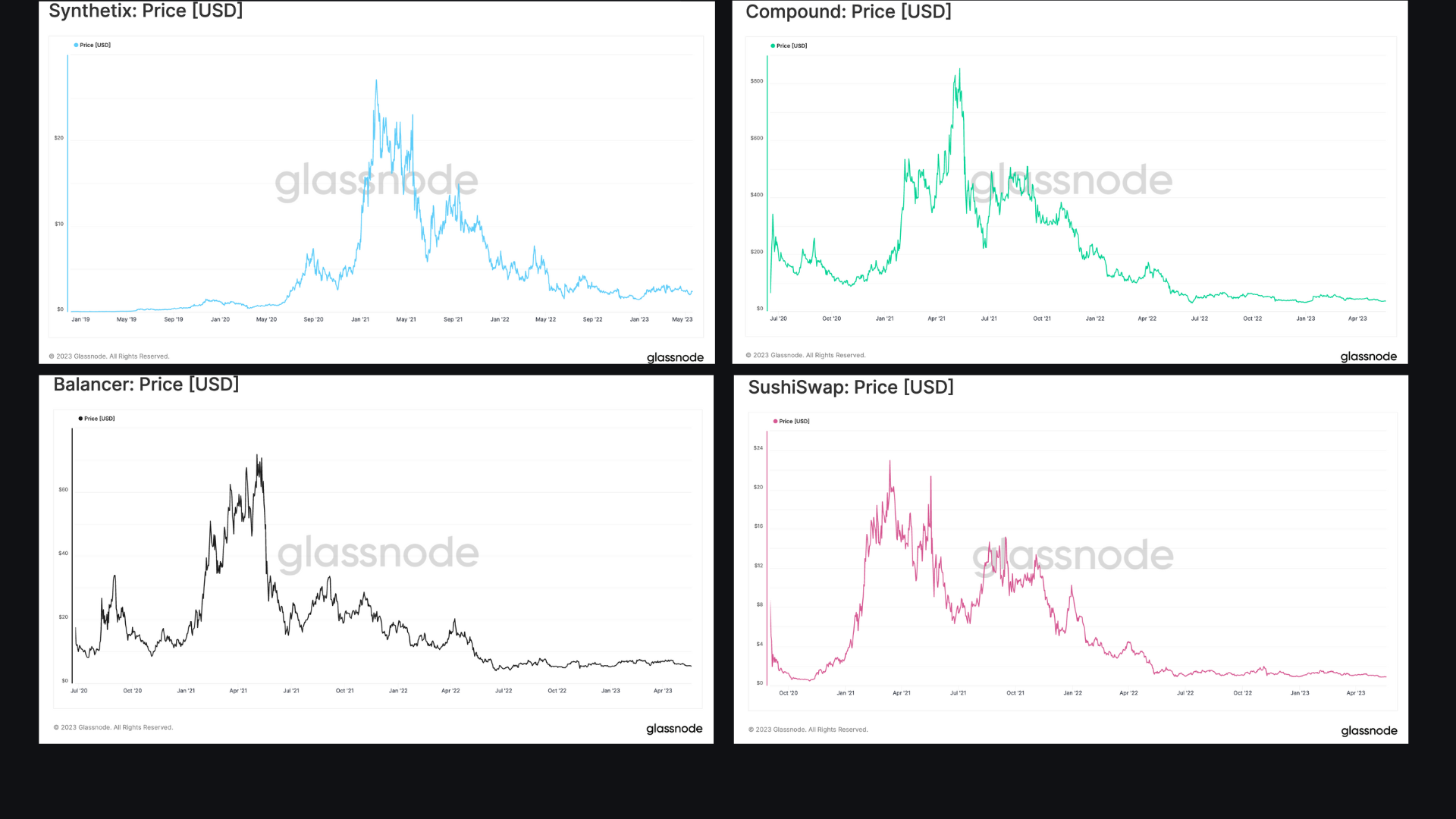

Given the DeFi sector is a primary source, and destination for both ERC20 tokens, stablecoins, and increasingly NFTs, one would expect strong performance from the tokens associated with these protocols. However, our supply weighted price index for DeFi, priced in both USD and ETH, seems to continue its endless descent, now down over 90% against both benchmarks since early 2021.

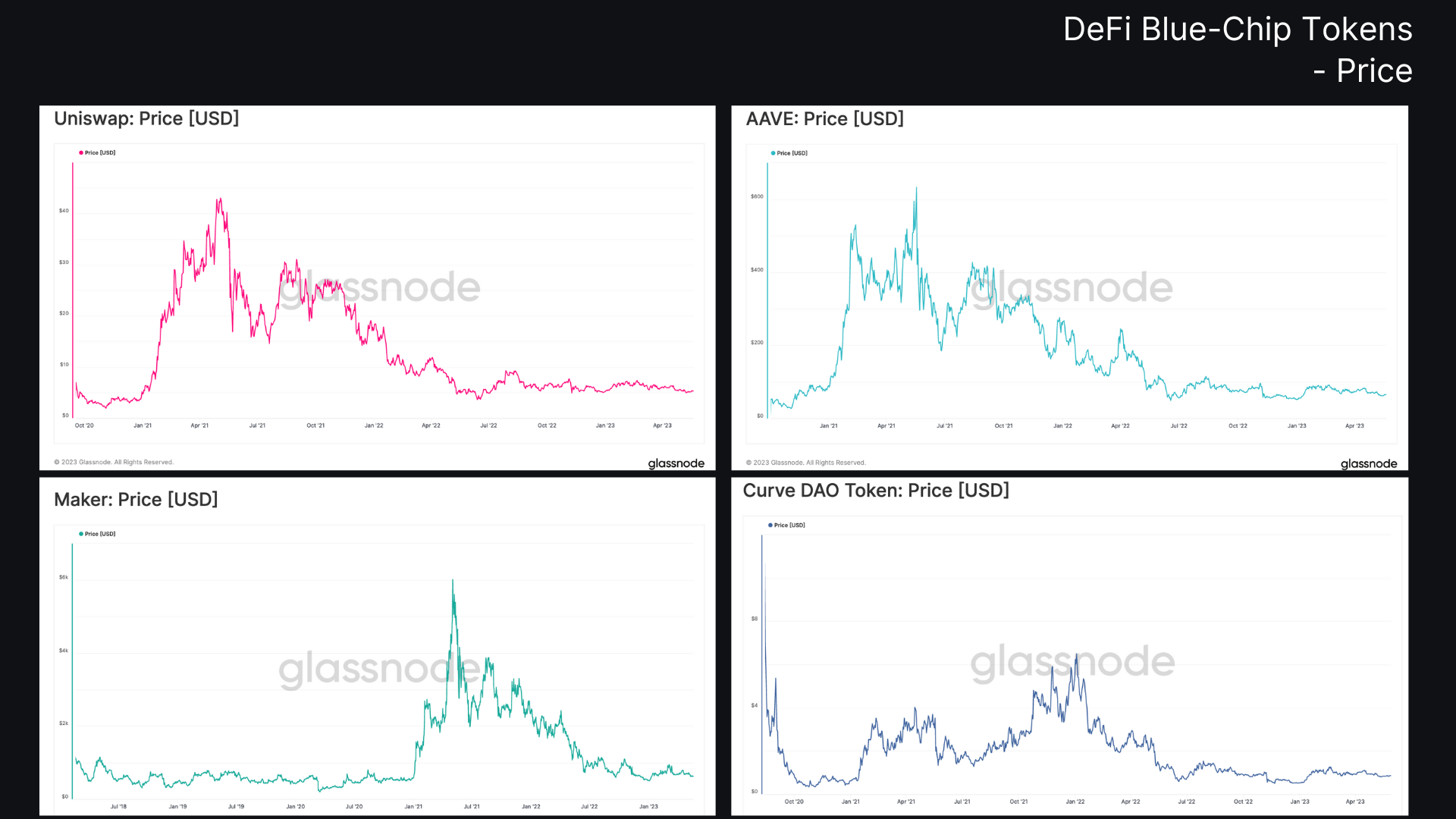

The remainder of this piece will zoom into the DeFi sector, and try to provide context regarding this remarkably poor token price performance. For this analysis, we will examine tokens of the top eight DeFi projects by market cap, without considering any metrics related to the underlying DeFi protocols themselves. This isolates only the relative price performance, ownership structure, and on-chain activity of the tokens, which remain the primary instrument through which investor preferences can be expressed.

Many argue that DeFi tokens do not reflect the true value of their underlying projects. However, we believe that in aggregation, the market performance of these tokens is a representative gauge for investor interest in the DeFi sector as a whole.

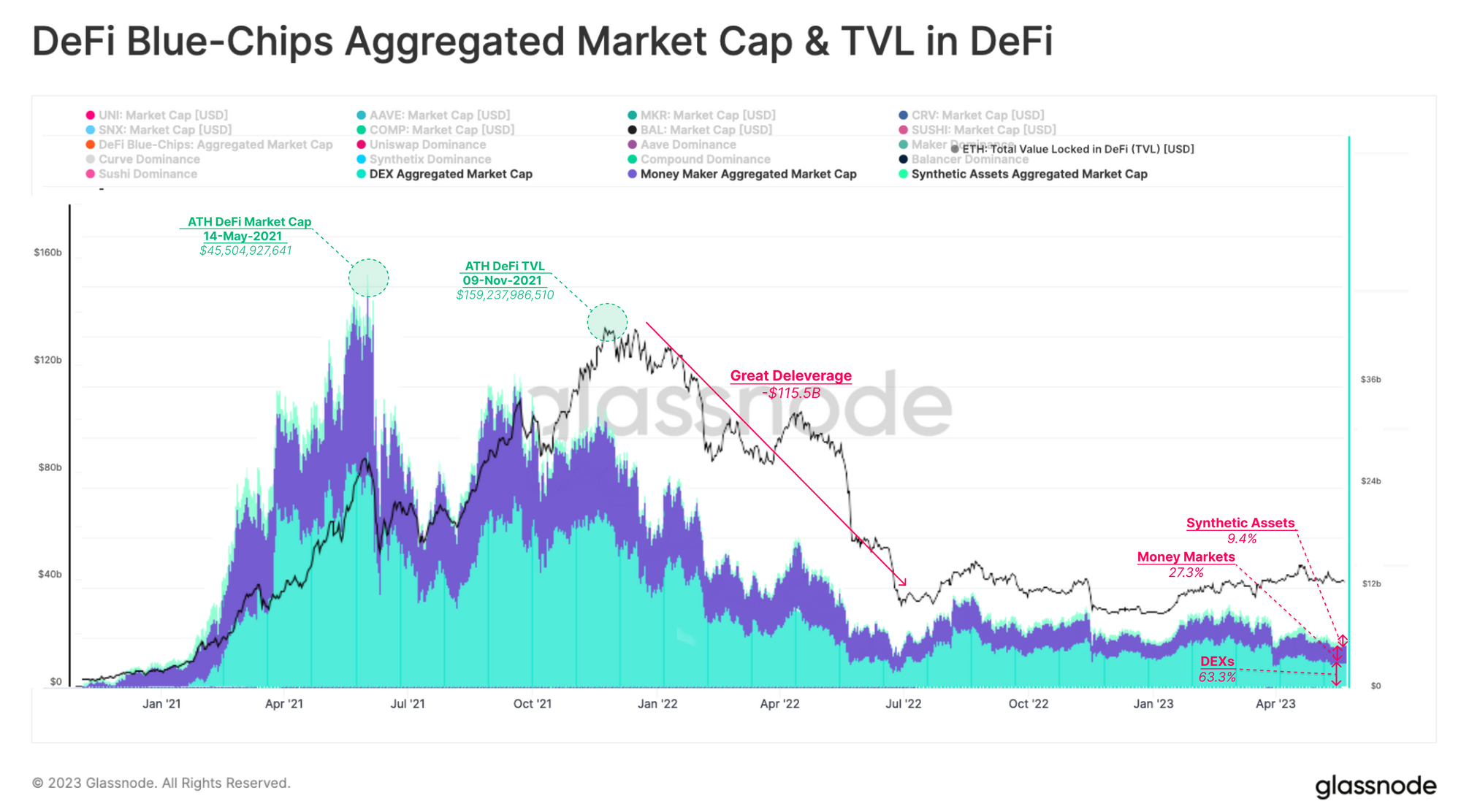

The aggregated market cap of these eight tokens reached peak popularity with investors around May 2021, approximately nine months after the 'DeFi summer' event in mid-2020, where most of these tokens were minted and issued. At its zenith, the total value of the DeFi Blue-Chips reached $45B, from which it has steadily declined. As of today, the DeFi market cap stands at just 12% of its all-time high.

Interestingly, since the Great Deleveraging in 2022, the valuation of DeFi tokens tends to move in accordance with the total value locked in DeFi protocols. It is possible that investor confidence is related to the performance of its underlying protocol after all.

When dividing DeFi into its different sub-sectors, we can see that Decentralized Exchanges (DEXs) have the largest market share, currently accounting for 63.3% of the aggregated DeFi market cap. Money Markets are the second most popular with 27.3%, whilst Synthethic Assets make up only a marginal component at 9.4%.

DeFi Tokens Must Compete With ETH

DeFi tokens are typically considered further out on the digital asset risk curve, and thus appeal to investors with higher risk appetites. These tokens are usually purchased using ETH or stablecoins as the quote currency, providing two benchmarks for performance.

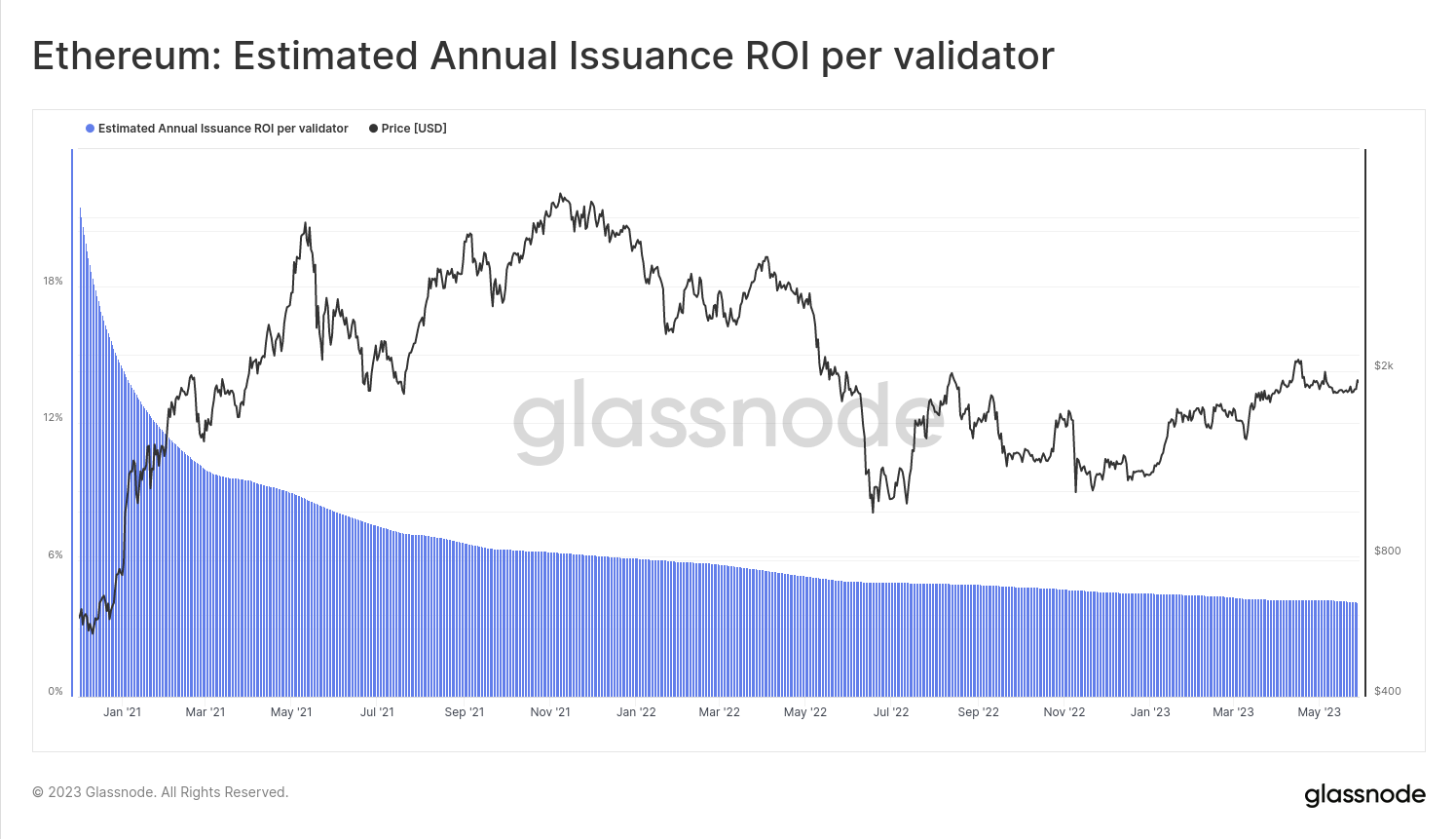

With this in mind, and with major events such as Proof-of-Stake finally coming to Ethereum, we must compare the relationship and performance of DeFi tokens against the now yield bearing benchmark asset ETH. Given the staking of ETH now yields 4.0% in ETH terms (without leverage), there is a new hurdle rate over which token returns must jump.

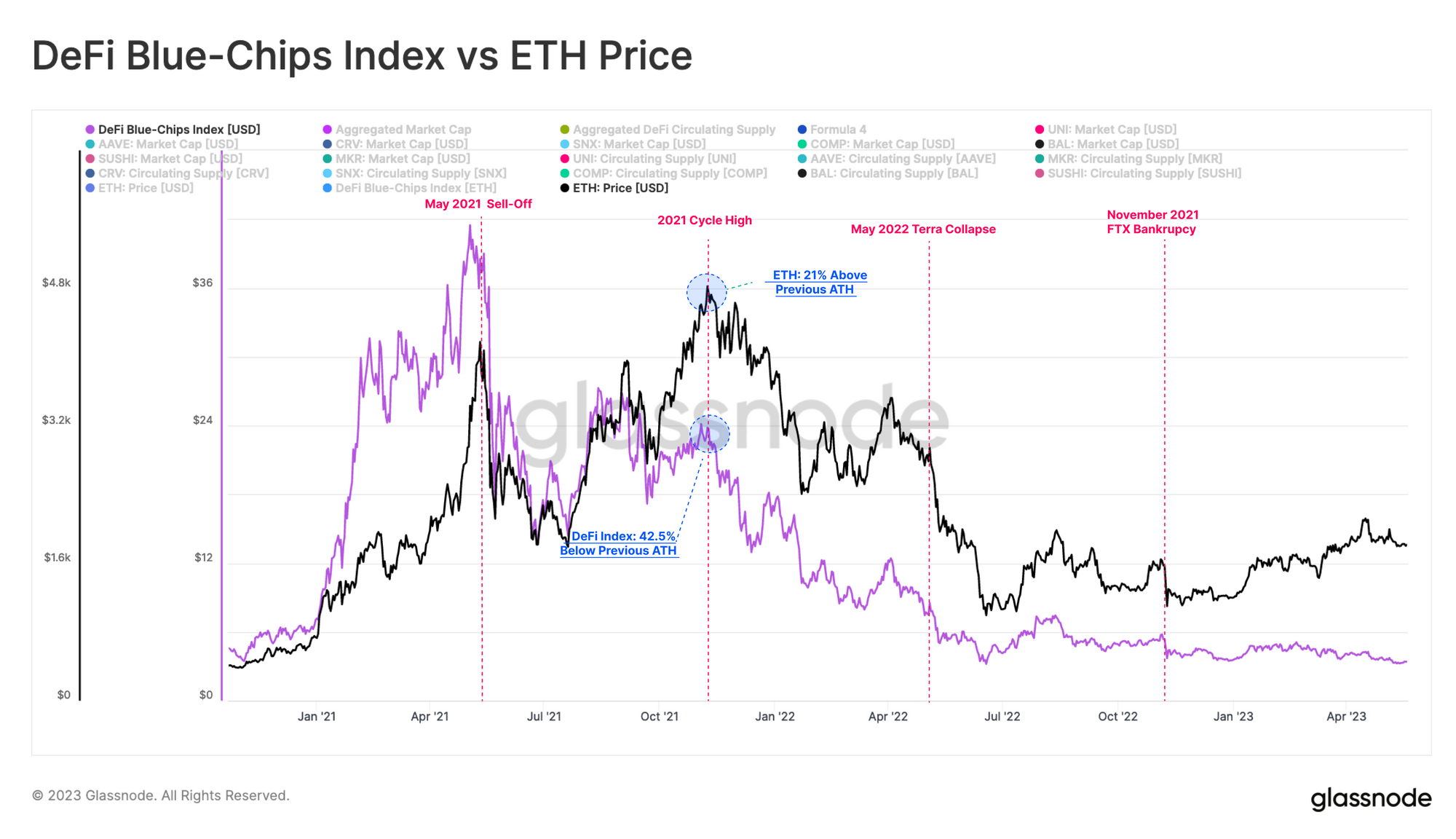

When comparing the price of ETH with the price of our DeFi Blue-Chip Index, we can observe that soon after 'DeFi Summer' in January 2021, DeFi tokens experienced a steeper bull run compared to ETH. However this remains the ultimate peak, and was followed by a massive drop in May 2021, and a relentless decline since.

Even during the second half of the 2021 bull cycle, DeFi tokens turned out to be far less responsive to the upside, perhaps a result of the markets preference for NFTs at the time. The DeFi index did not exceed its previous May all-time-high, remaining -42% below it despite ETH prices reaching new heights in Nov 2021.

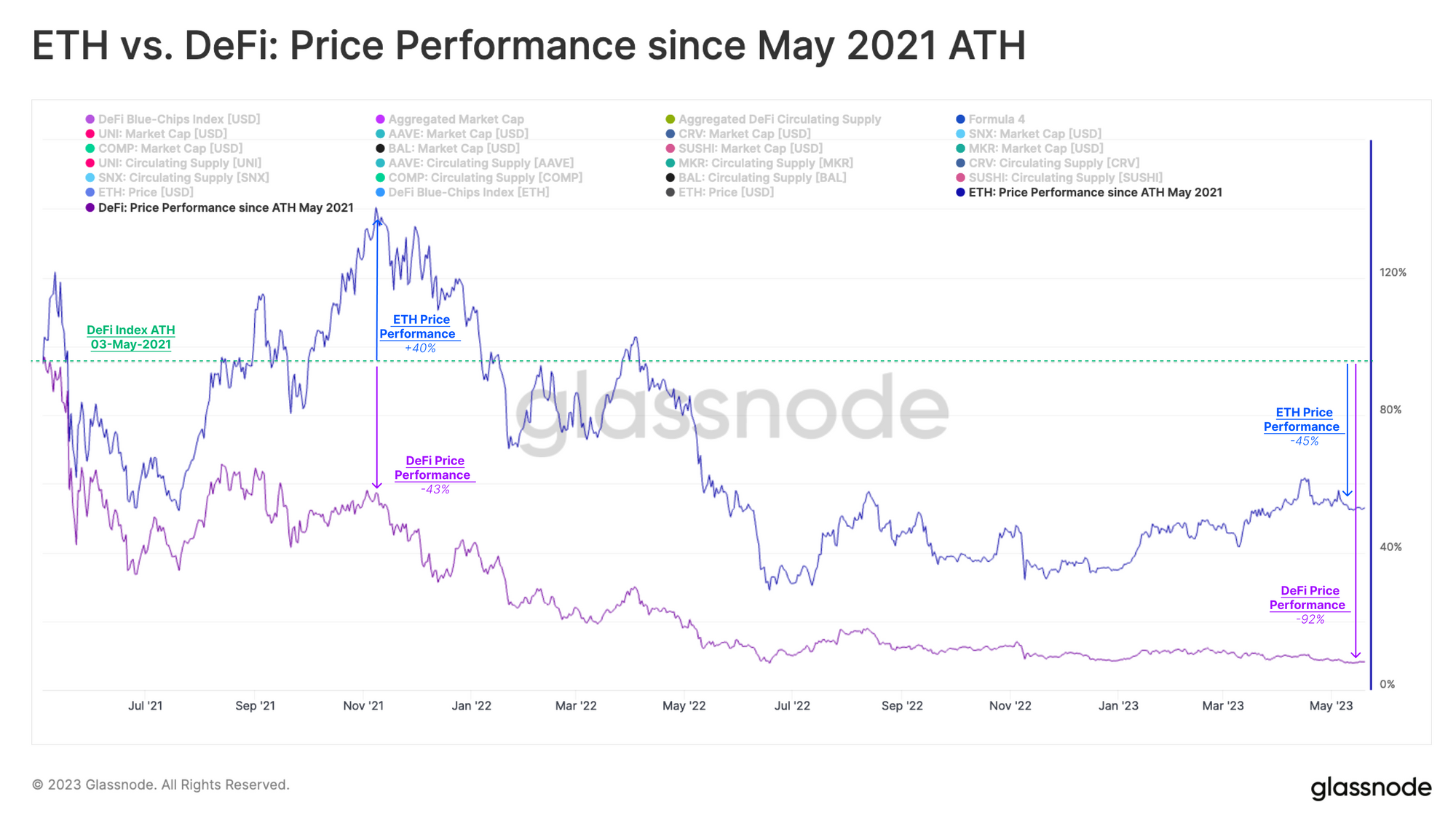

If we index performance since the DeFi Index ATH in May 2021 to that of ETH, we can see this poor performance in more detail.

- During second half of the 2021 bull cycle, ETH managed to rally 40% above its prior peak, whilst DeFi tokens set a lower high, down 43% since the May peak.

- In the wake of the 2022 bear market, DeFi tokens have fallen -92.1% below the May 2021 ATH, while ETH is down just 45%. This means ETH out-performed the DeFi Index by 6.7x during the bear cycle.

From this, it can be seen that DeFi tokens have in fact underperformed ETH to the upside during the bull, and then drawn down considerably more on the downside during the bear.

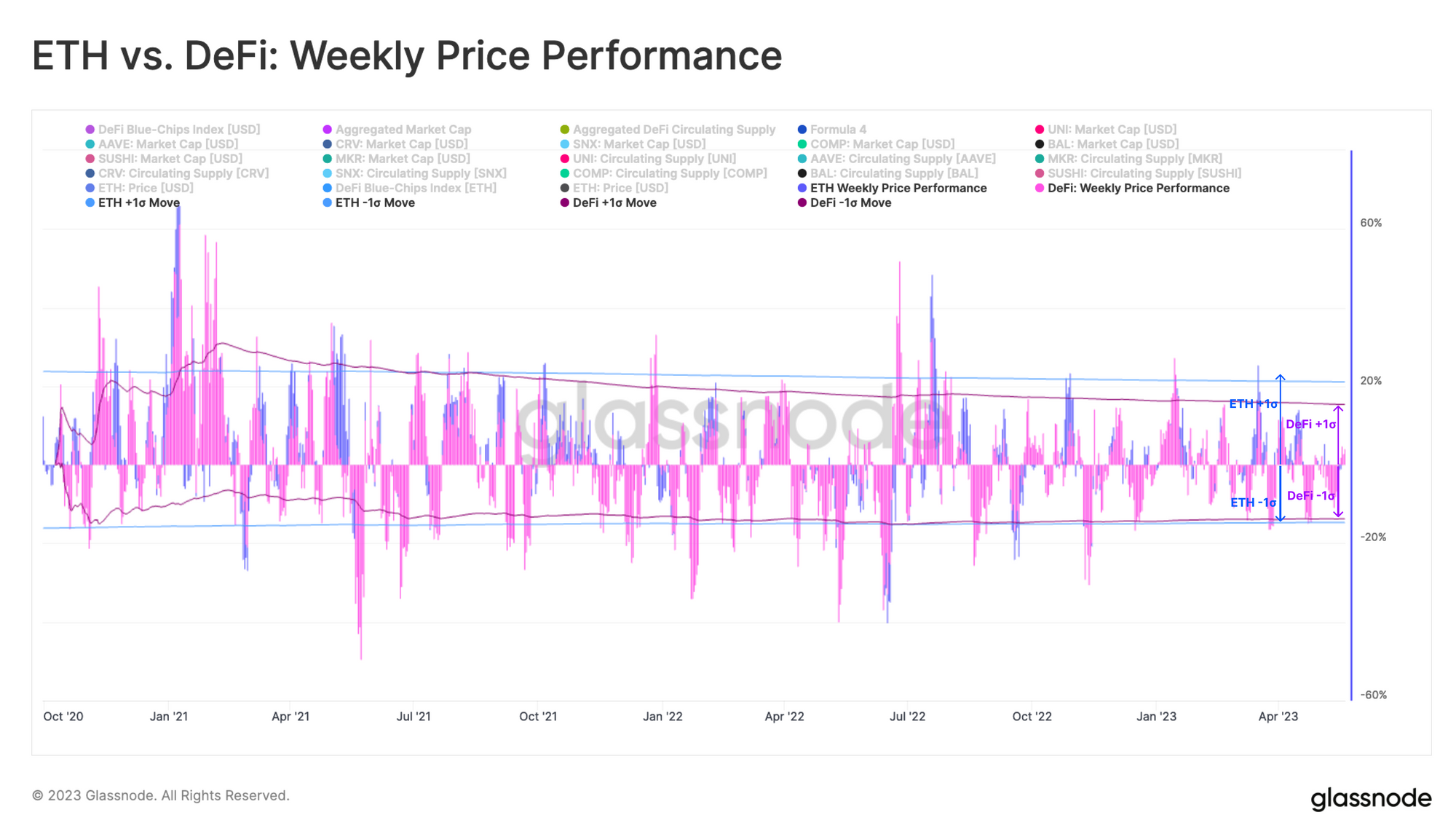

On a shorter-term horizon, we can compare the weekly price performance profile of the DeFi index and ETH. In general, DeFi's weekly performance tends to align with that of ETH, and the chart below overlays the one standard deviation bands for both.

The outcome is once again not in the favour of DeFi token holders. Not only is downside performance and volatility equivalent to ETH, but the upside performance is measurably less. This skews the already lopsided risk-to-reward balance further into ETHs favour.

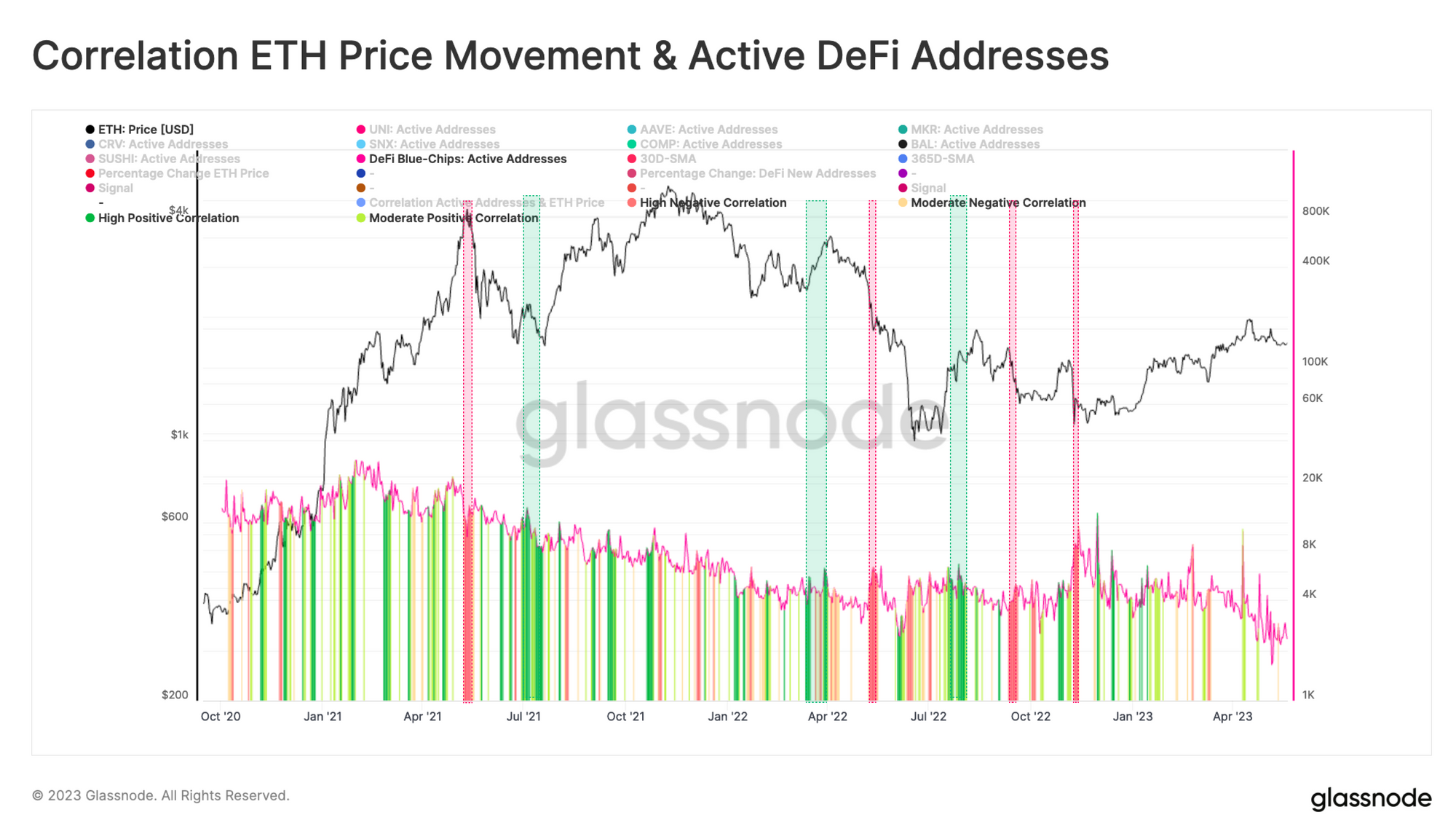

We can observe relative investor flows between the ETH and the DeFi sector using the correlation between ETH price movements, and active addresses transferring DeFi tokens. An increase in on-chain address activity is characteristic of periods of growing attention, as investors begin to trade, and acquire DeFi token holdings.

Not surprisingly, we observe a high negative correlation 🔴 around major ETH sell-off events. This suggests that DeFi token activity increases during ETH price drops, as investors respond to market turbulence by de-risking, and offloading riskier holdings. Conversely, we often see a high positive correlation 🟢 when ETH prices experience a sharp upswing, adding weight to the circulating thesis that enthusiasm for ETH, drives demand further out on the risk curve.

As of January 2023 however, we observe a breakdown in the correlation between the two, which suggests that activities around DeFi tokens have become somewhat detached from the ETH market YTD. One wonders if this is related to the successful Shapella upgrade, completing the final leg of the ETH staking yield trade.

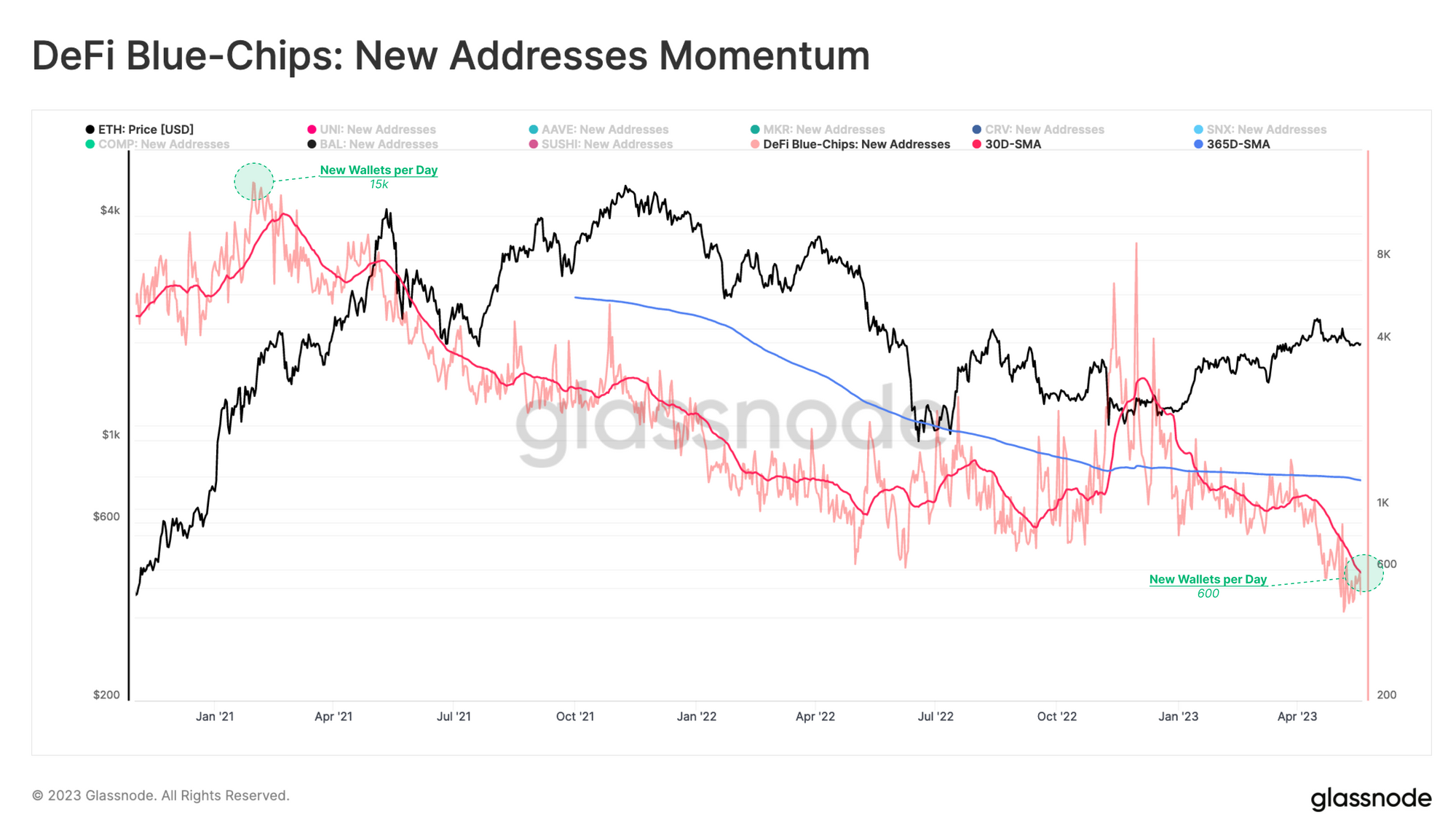

This can further be confirmed by looking at New Addresses Momentum for DeFi tokens. The monthly average of new addresses has been consistently below the yearly average since the beginning of our measurement, with the only notable spike being around the FTX collapse. Rather than indicating new demand for DeFi tokens, this spike is mostly associated with divestment from DeFi tokens, as the market perception of risk increased.

There has also been a rapid decline in new addresses since March of this year (again, approaching the Shapella upgrade). Currently, only around 600 new wallets holding a DeFi token in our index are created per day. This suggests that DeFi tokens continue their struggle at attracting investor attention, despite the recovery of ETH prices during the first quarter of 2023.

Considerations for DeFi Tokens

The augment for holding DeFi tokens differs greatly from investing in base layer assets like BTC or ETH in several ways. Each token has its own purpose, and relationship with the underlying protocol design.

These projects are still evolving, with many of them having turned into Decentralized Autonomous Organizations (DAOs), granting token holders a right to propose and vote on protocol changes. However few tokens have achieved the so called 'fee-switch', where cash flows, or dividends are paid to stakeholders. More often, tokens are staked to earn additional tokens from the protocol reserves, however this is an inflationary approach on net.

To aide in a comparative assessment of these tokens, we can explore two key aspects: Token Liquidity and Token Usage.

Token Liquidity

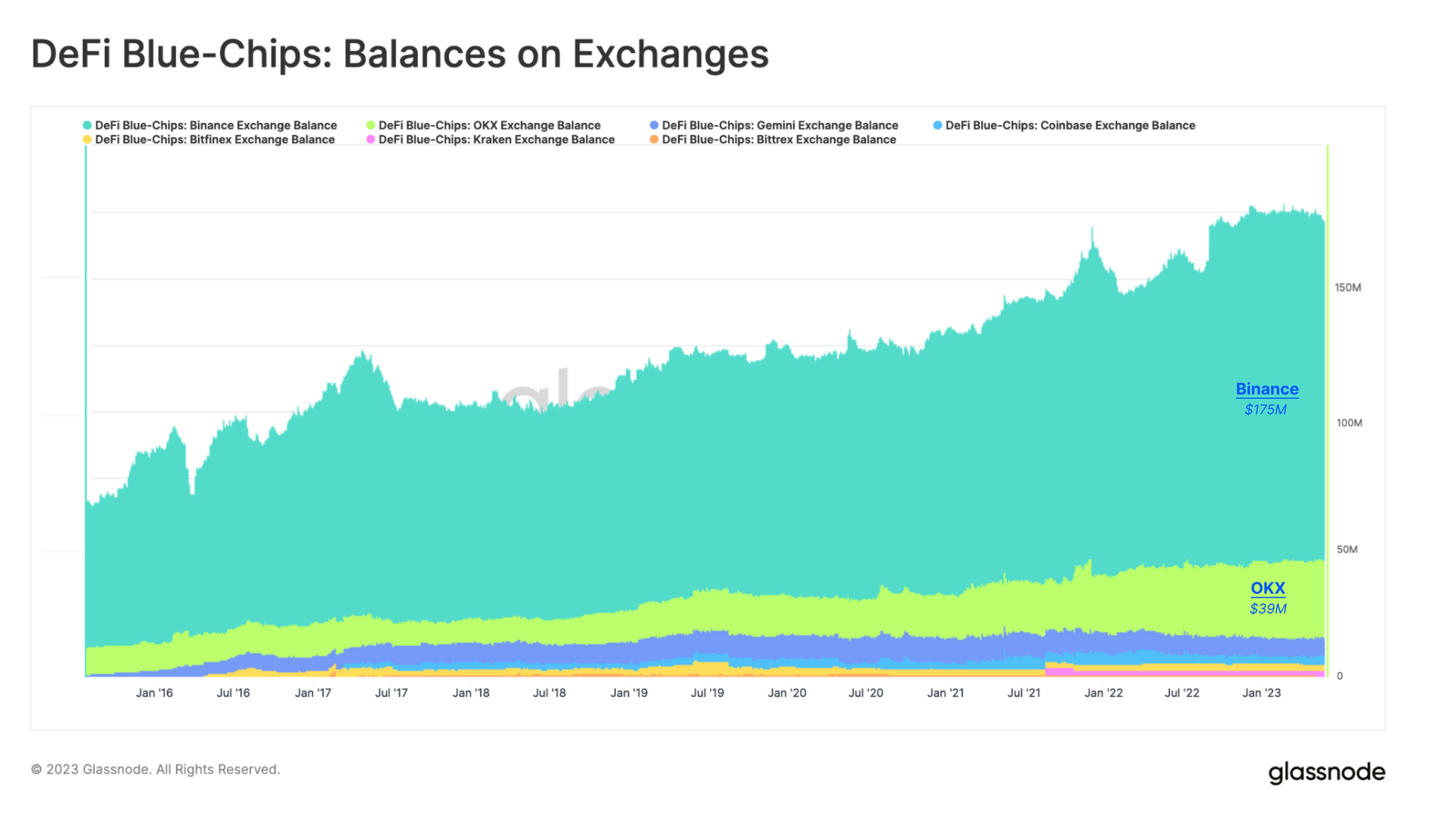

The biggest centralized marketplace for trading DeFi tokens remains Binance, which has a consistently growing, but relativly small balance. At present, the total balance of tokens in our our DeFi index held on Binance is over $175M. This represents just 2.70% of the $6.472B aggregated token market cap. The centralized exchange with the second biggest DeFi token balance sheet is OKX, with $39M.

Liquidity on DEXs is far less than what we have seen on centralized exchanges. DeFi tokens are traded primarily on Ethereum mainnet, but are expanding across to other layer 2 networks, and sidechains. Generally speaking, this results in fractured liquidity, which has historically resulted in Ethereum's mainnet being the dominant trading venue.

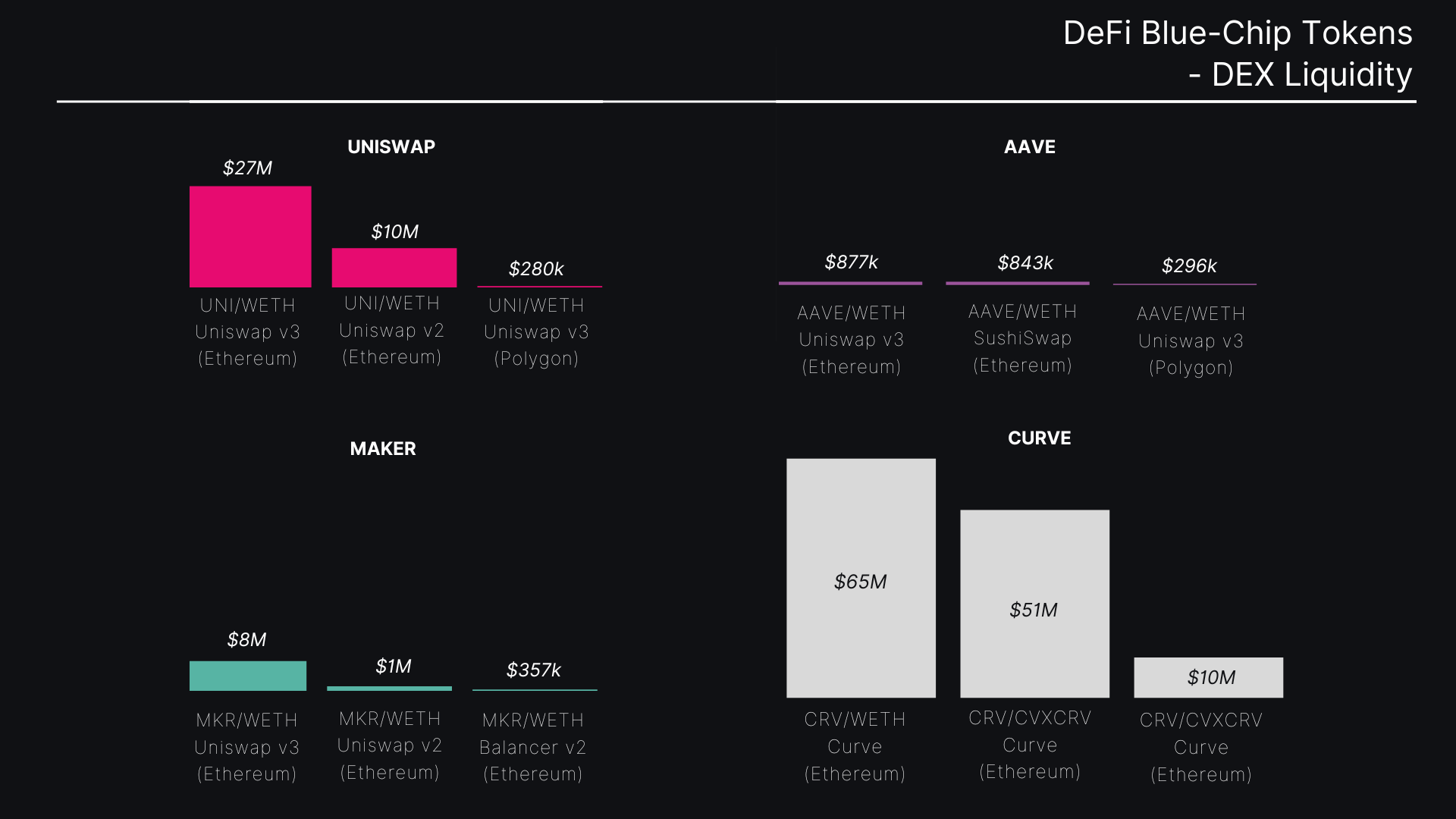

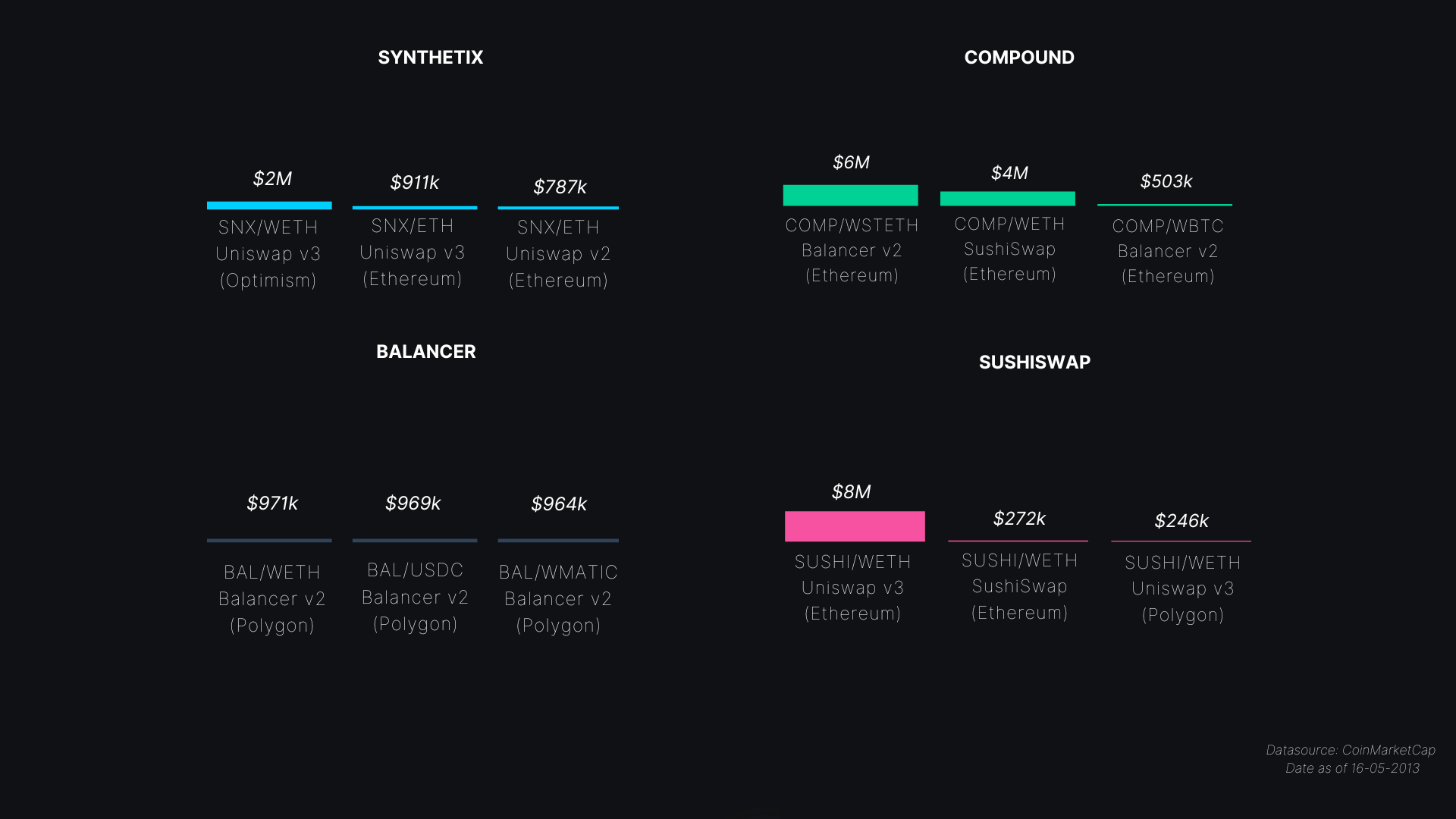

A token’s liquidity depends on the project’s ability to attract market makers for both centralized and decentralized exchanges. Decentralized Exchanges such as Curve have developed their own mechanism to foster liquid markets for the CRV token on their own platform.

The chart below shows TVL held in liquidity pools, with bars representing the aggregated USD denominated amount for the relevant trading pairs. The dominant liquidity pools for DeFi tokens are on Uniswap on Ethereum mainnet. However, Polygon hosts the most liquidity for BAL token, and Optimism has the most liquidity for SNX. The highest TVL value is actually found on the CRV/WETH pair on Curve, which is related to fact that CRV token holders are eligible to vote on rewards for liquidity pools on Curve.

When we analyze the distribution of DeFi tokens between centralized and decentralized exchanges, and express it as a proportion of the aggregated token market cap of $6.472 billion, we observe significantly small figures. Merely 3.8% of the overall supply is found on decentralized exchanges, while 4.17% exists on centralized exchanges. This prompts the question: what purpose does the remaining percentage of the token supply serve? By examining the breakdown of token distribution based on usage, we gain a different perspective on the utilization of DeFi tokens.

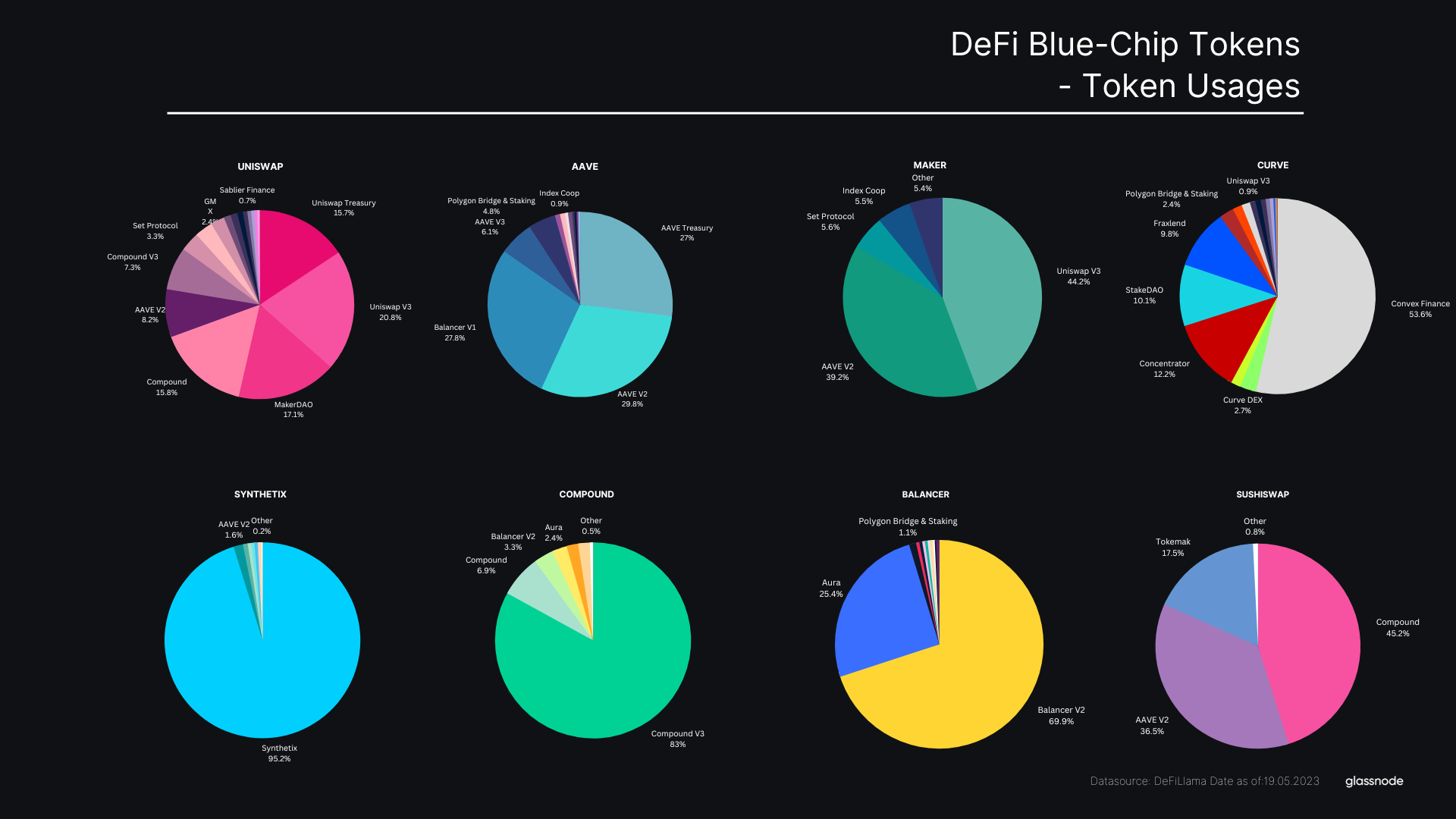

Token Usage

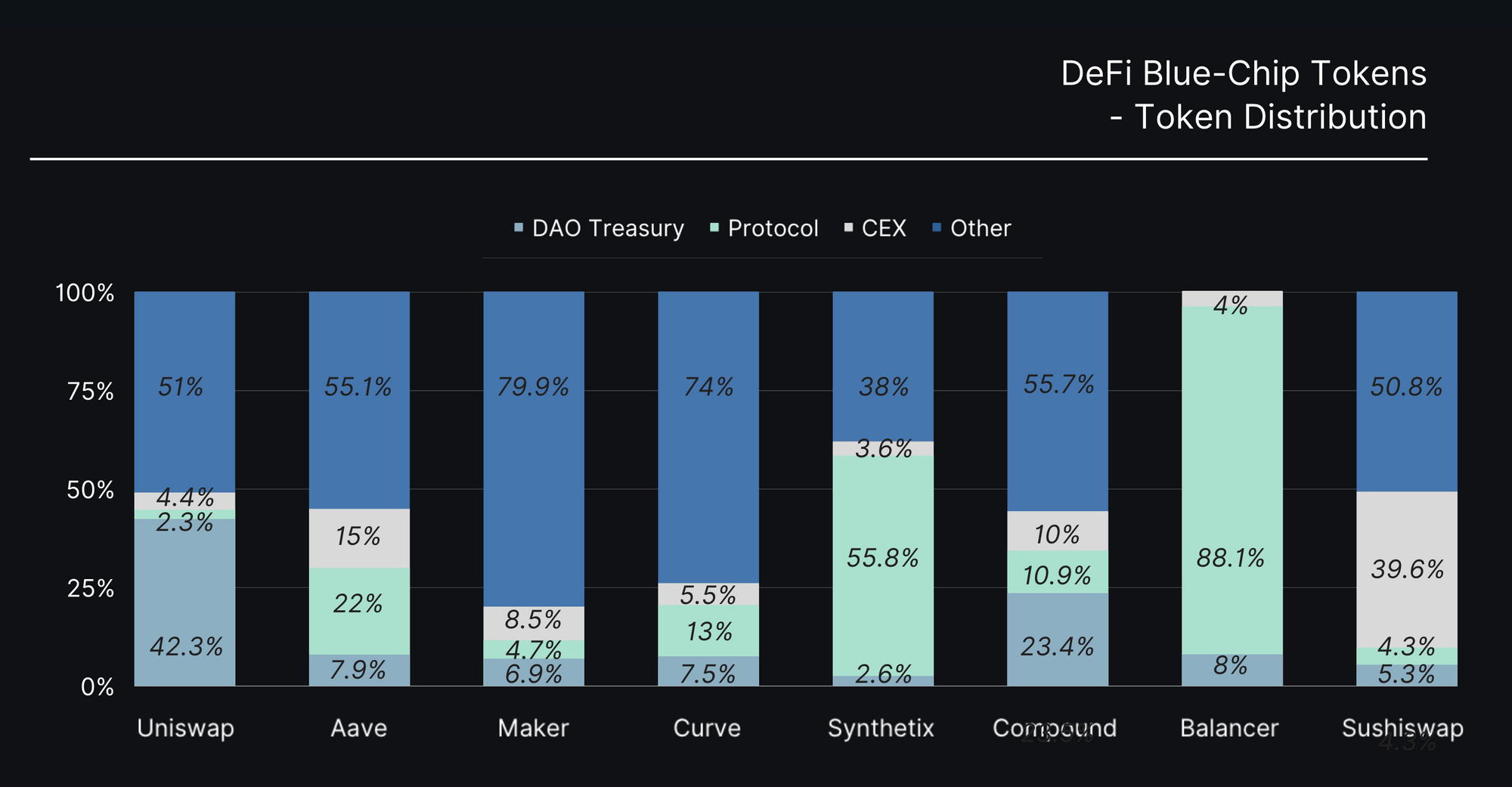

DeFi tokens can be used both in DeFi applications and in treasuries of DAOs. We can breakdown the percentage of each token held either within DeFi protocols, or held in the protocol's treasury.

Generally speaking, we can see that each protocol's DAO treasury tends to hold less than 10% of the token supply (with Uniswap and Compound being exceptions). We can also see that some tokens (SNX, BAL) have a much larger presence within DeFi protocols, often a result of token incentives and economic designs that create incentives for investor lockups.

In this view, we can see that for most DeFi tokens, except Balancer and Synthetix, more than half of the token supply has an undefined usage. Further research is needed, but it is possible that these tokens may be held by individuals, especially founders, team members, and VCs. Another potential usage for these tokens could be held as collateral in EOS or multisig wallets for derivatives such as wrapped tokens on sidechains, such as Binance Smart Chain.

Taking a more granular view, we can see that quite often, DeFi tokens tend to find usage most heavily within their own underlying protocol. For Money Market related tokens (AAVE, MKR, COMP) we can see a clear dominance of these tokens being deposited within Money Market protocols as collateral, or into DEX liquidity pools.

For specific tokens like SNX, BAL and CRV, we can see large proportion of usage is centered around their own underlying protocol, indicative of token design and staking economics. UNI stands out as having arguably the most diverse spread of applications, largely driven by it having the largest market cap, and thus broadest application as collateral in various forms.

Looking Ahead

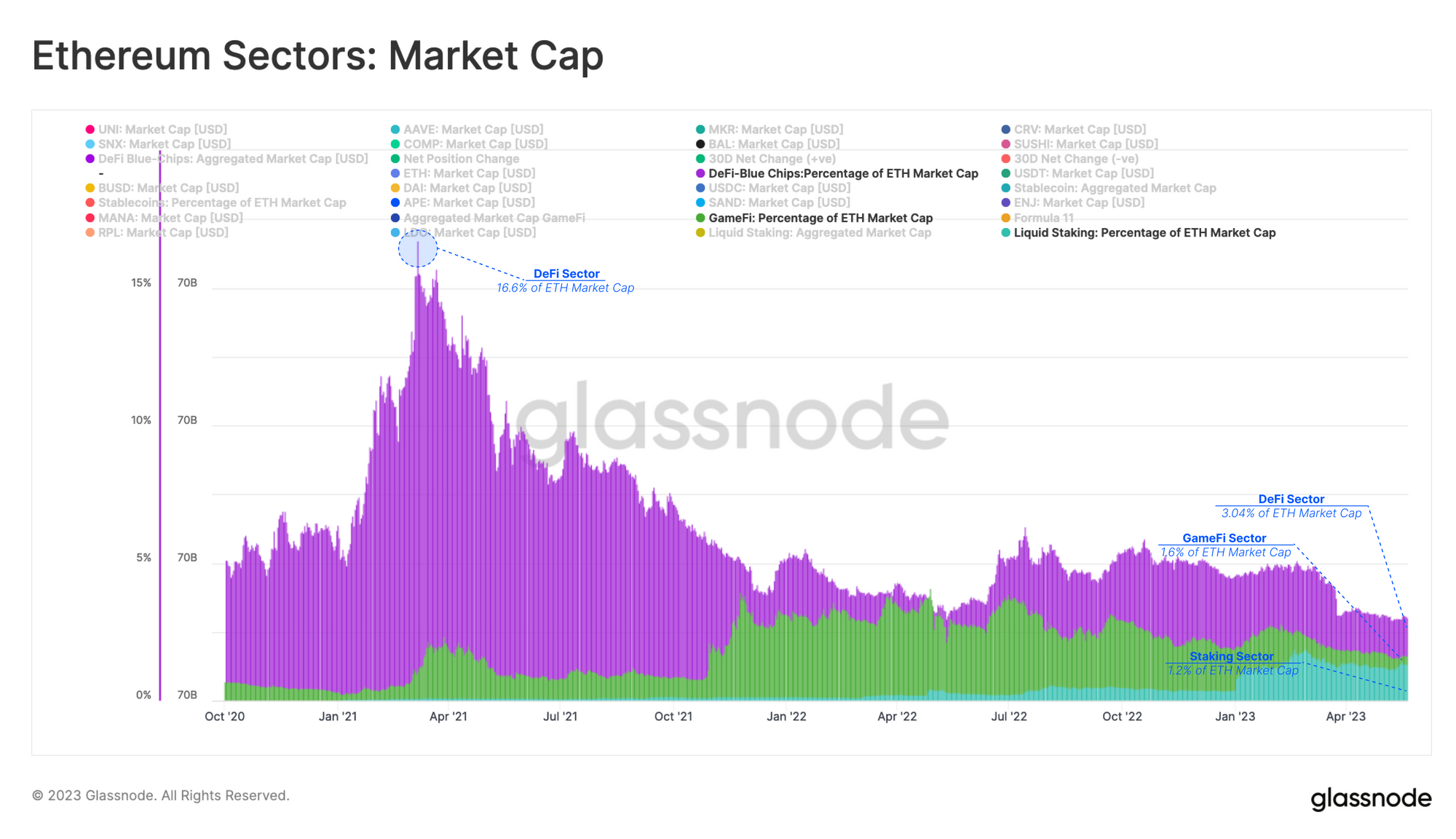

Over the past two years, two new sectors have emerged withing the Ethereum ecosystem; GameFi and Staking. Each sector has sparked varying degrees of investor interest, with GameFi almost overtaking DeFi in mid 2022. The Staking industry (represented here via the tokens of Liquid Staking Protocols) has been on the rise since the beginning of 2023, with the aggregated market cap exploding from $505M in Jan-2023 to over $3.20B in Apr-2023.

If we consider these sectors as parts of the wider Ethereum economy, and within the context of EIP1559 burn, we can also expect that some portion value accrued by these sectors, will also feed back into the valuation of ETH. As such, we can compare the market caps of these sectors relative to the ETH market cap.

From this lens, DeFi represents just 3.04% the size of Ethereum itself, and the up-and-coming GameFi and LSD tokens are just 1.2% and 1.6% the size, respectively. Whilst the DeFi peak, where DeFi tokens = 16.6% Ethereum, reached during the 2021 glory days may seem exciting, it remains to be seen whether any of these upcoming sectors are able to reach escape velocity from ETH itself.

In many ways, it is now up to the DAOs and token holders controlling these DeFi platforms to find new ways of redirecting value and revenue streams towards creating stakeholder value. With ETH now boasting its own native yield, the hurdle rate bar for DeFi tokens (and any other sector) has been set.

Like clockwork, last week saw two major DeFi projects release proposals seeking to address this disparity. A recent MakerDAO proposal introduced a new stablecoin, and governance token intended to be used within future sub-DAOs.

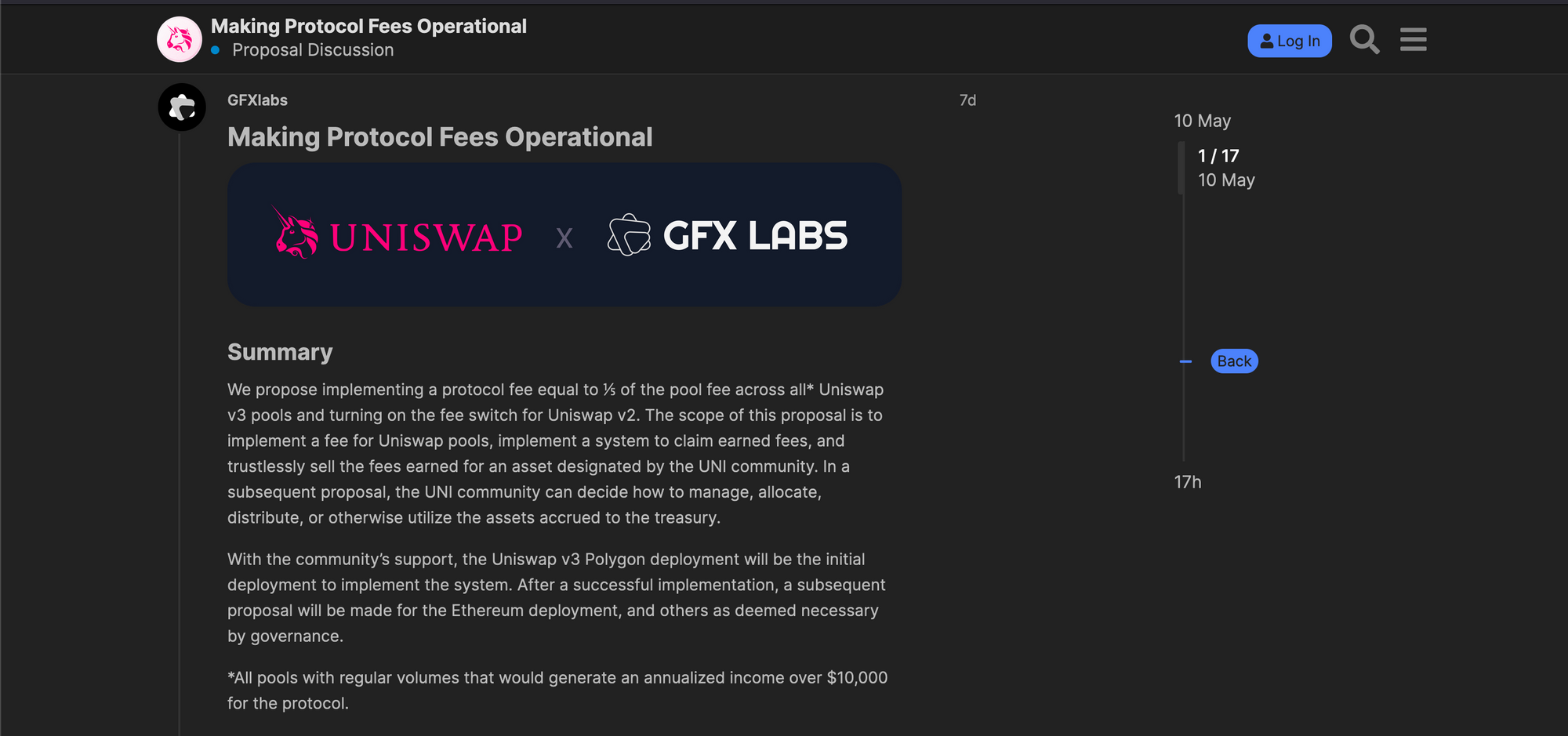

Similarly, Uniswap introduced a new governance proposal seeking to implement a long contemplated protocol fee switch. This proposal suggests setting the fee at 1/5th of the pool trading fee, with proceeds projected to accumulate an estimated $52M over a 6 month period. According to the proposal, the fees will go to the Uniswap DAO, which begs the question whether this is sufficient to drive new demand towards the UNI token.

Summary and Conclusions

These two proposals indicate a shift in focus for the established DeFi protocol cohorts, moving away from product development, and towards generating value for stakeholders in their ecosystem. It is highly likely that the lacklustre performance of DeFi tokens over the last two years is a factor or the emergence of native ETH staking yield.

It seems that within the Ethereum landscape, the native ETH token may in fact be a predator of value, with much of it sourced from the very tokens within its own orbit.

As a result, we may soon see a new wave of discussion, debates, and designs for token revenue models emerging within the DeFi sector. It now falls to the teams and stakeholders to shape and deliver a successful outcome of these proposals. The battle to re-ignite interest in DeFi tokens is likely under way, but given the new hurdle rate set by the ETH token itself, it is unlikely to be an easy one.

- Follow us and reach out on Twitter

- Join our Telegram channel

- Visit Glassnode Forum for long-form discussions and analysis.

- For on–chain metrics and activity graphs, visit Glassnode Studio

- For automated alerts on core on–chain metrics and activity on exchanges, visit our Glassnode Alerts Twitter

Disclaimer: This report does not provide any investment advice. All data is provided for information purposes only. No investment decision shall be based on the information provided here and you are solely responsible for your own investment decisions.