DeFi Uncovered: DeFi Valuations Dislocate

As a predominantly leverage driven correction hits the market, we continue to see expansion in DeFi protocol usage, whilst token valuations struggle to keep pace.

The broader crypto markets saw a pullback after a relatively exuberant period following the release of EIP-1559, punctuated by significant activity and speculation within the NFT markets. Ethereum prices pushed towards their ATH, reaching just shy of $4,000 before pulling back sharply to an intra-day low of $3,168.

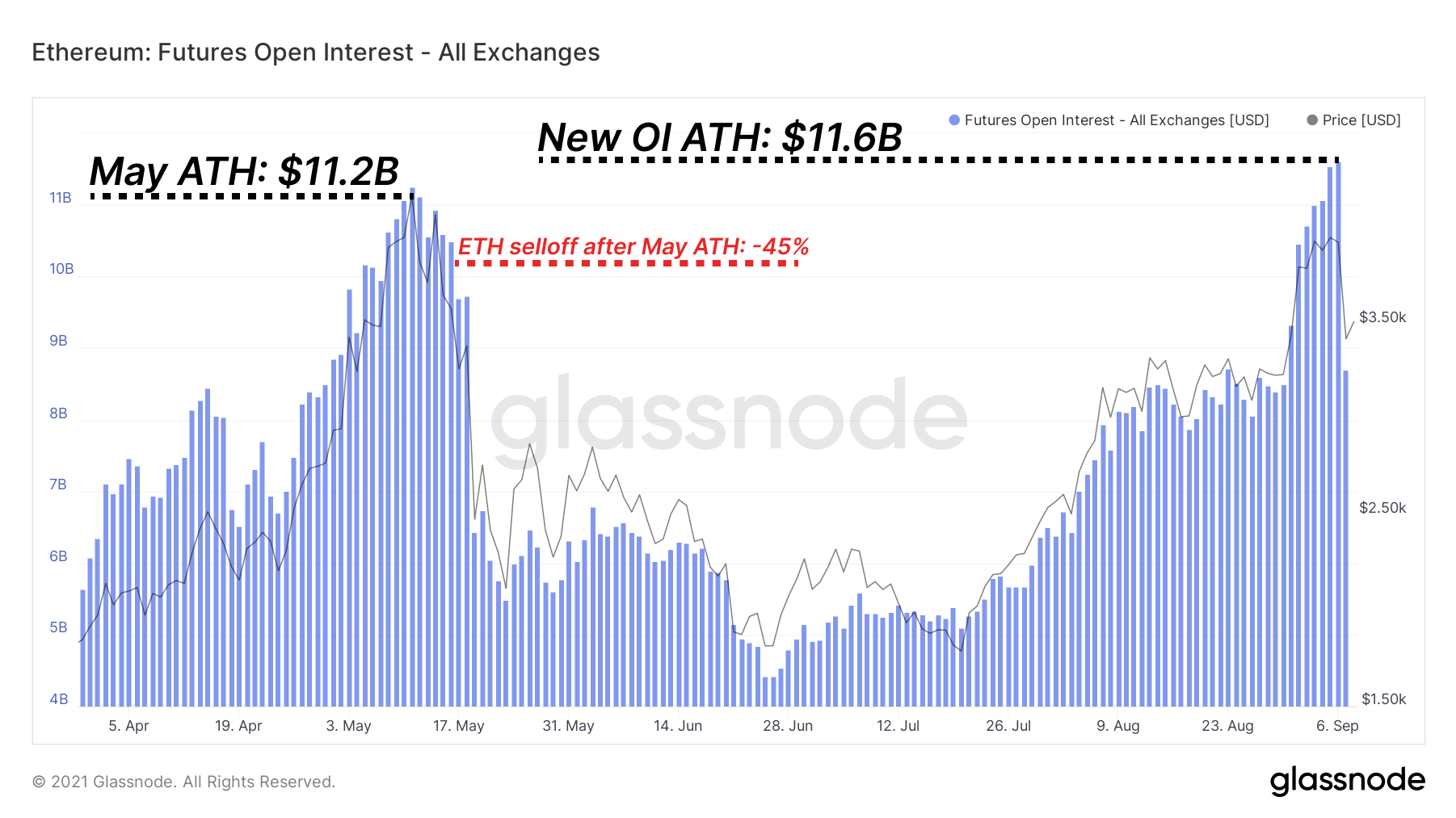

We saw quite the dramatic sell-off early this week as Ethereum traders saw leverage and exuberance flushed from the system. In our most recent newsletter, we noted that futures open interest for Bitcoin were elevated, whilst open interest for Ethereum futures had surpassed the previous ATH in the days before prices crashed.

This comes at a time when the Ethereum network continues to see massive usage and fee congestion, driven primarily by NFT minting and trades. Unsurprisingly, this massive interest and exuberance has been reflected in derivatives markets, with volumes and open interest reaching new heights.

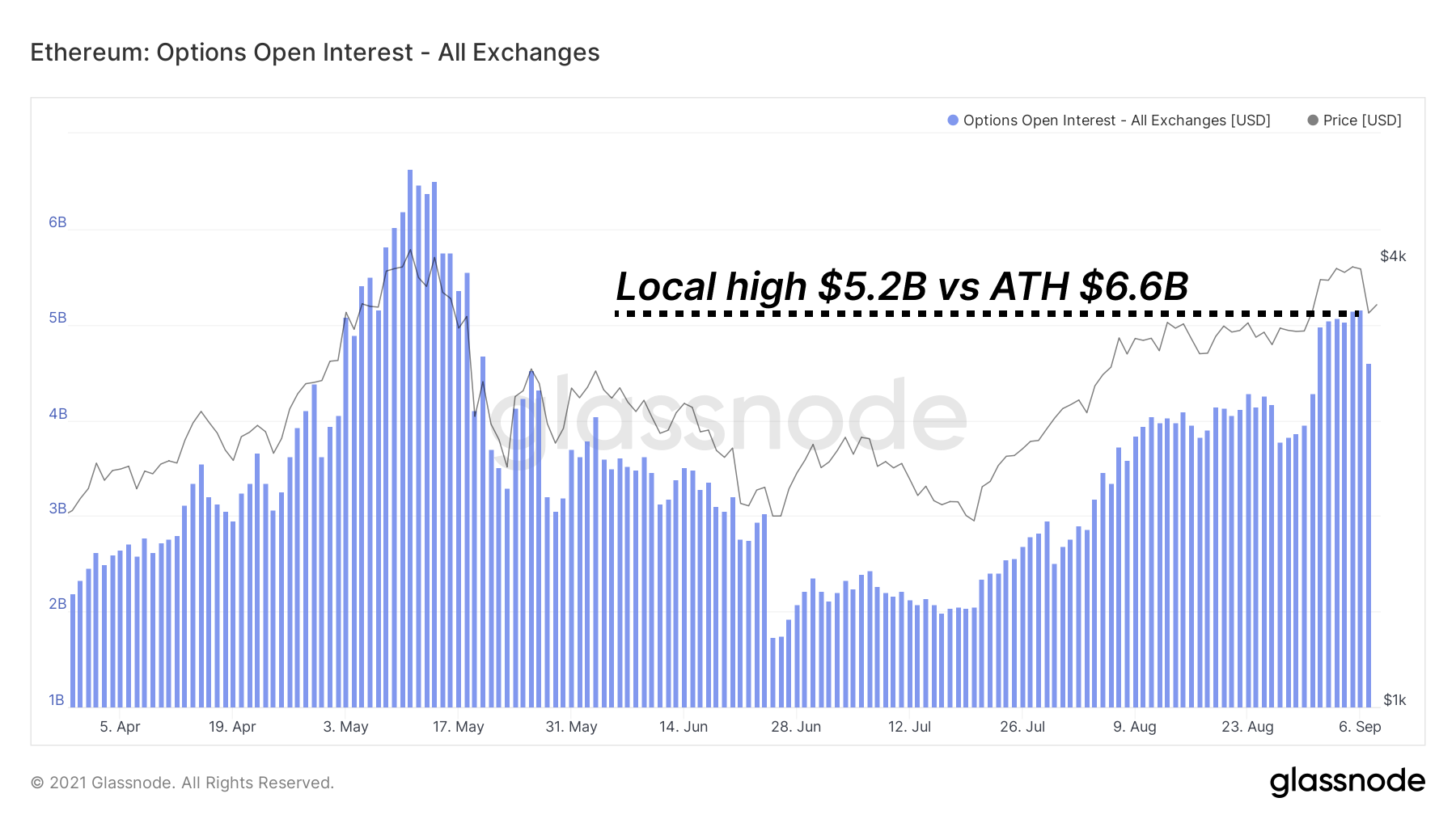

Ethereum options markets haven't seen quite the same spike or correction in open interest. Open interest in options can often express professional traders' view that a position needs hedging or that a large move is impending. It allows traders to manage position risk without needing to sell the base asset. Options OI certainly found a local high but far from an ATH.

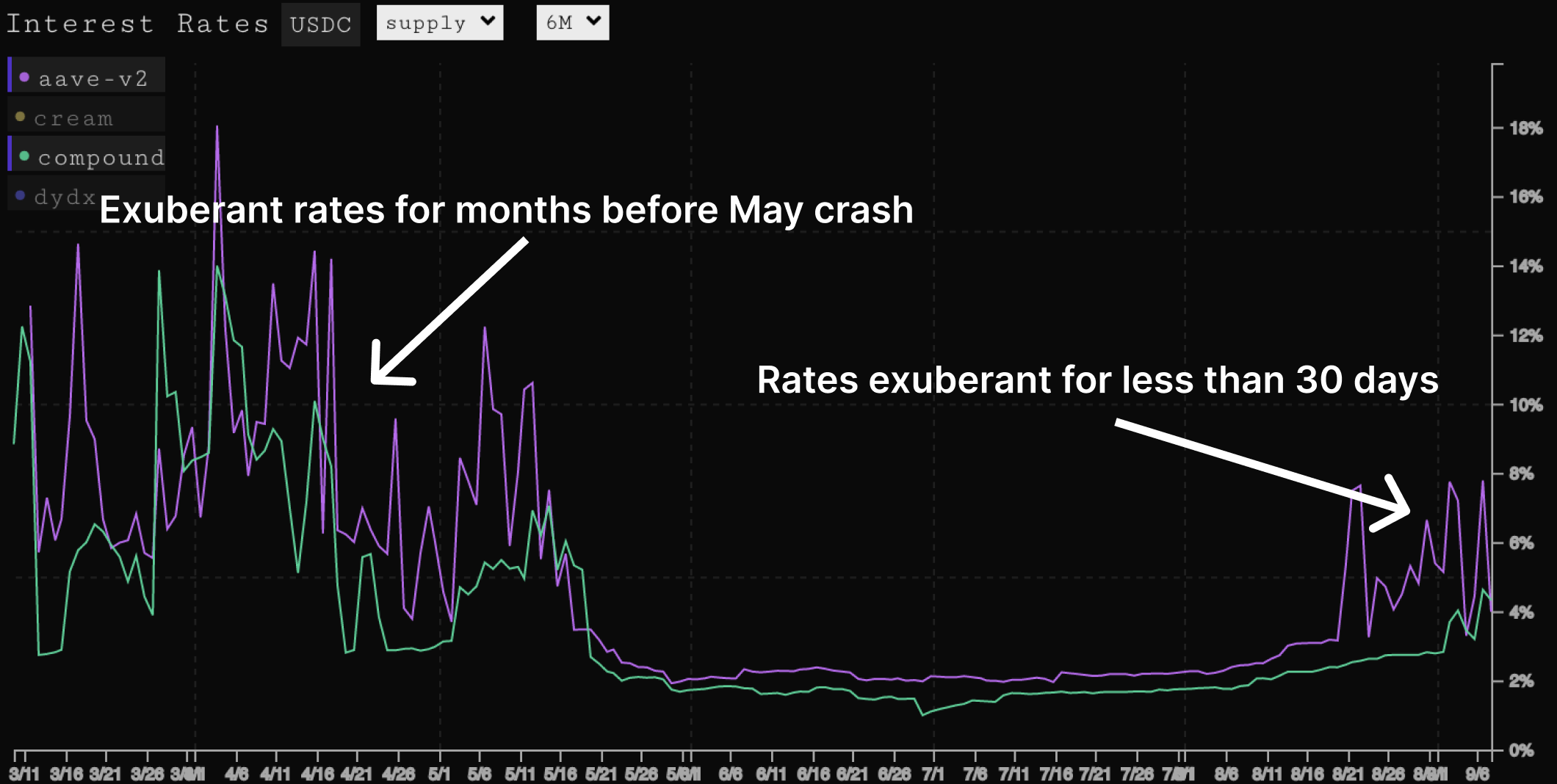

In times of exuberance, traders tend to take on leverage via borrowing funds against collateral. DeFi is a key benefactor of this borrow demand, with recent interest rates and yields rising throughout the ecosystem. These yields impact returns on major lending platforms like Compound and Aave, which are then in turn used heavily in aggregators like Yearn Finance.

A spike in rates can provide an indicator that the system has taken on significant amounts of leverage. Note this doesn't necessarily signal an impending crash, as rates can stay elevated for some time, and in this case, they were only elevated for a very limited period after an extended period at around ~2%. Rates peaked at 12% before the price crash flushed out leverage, with rates since returning to around 3-4%.

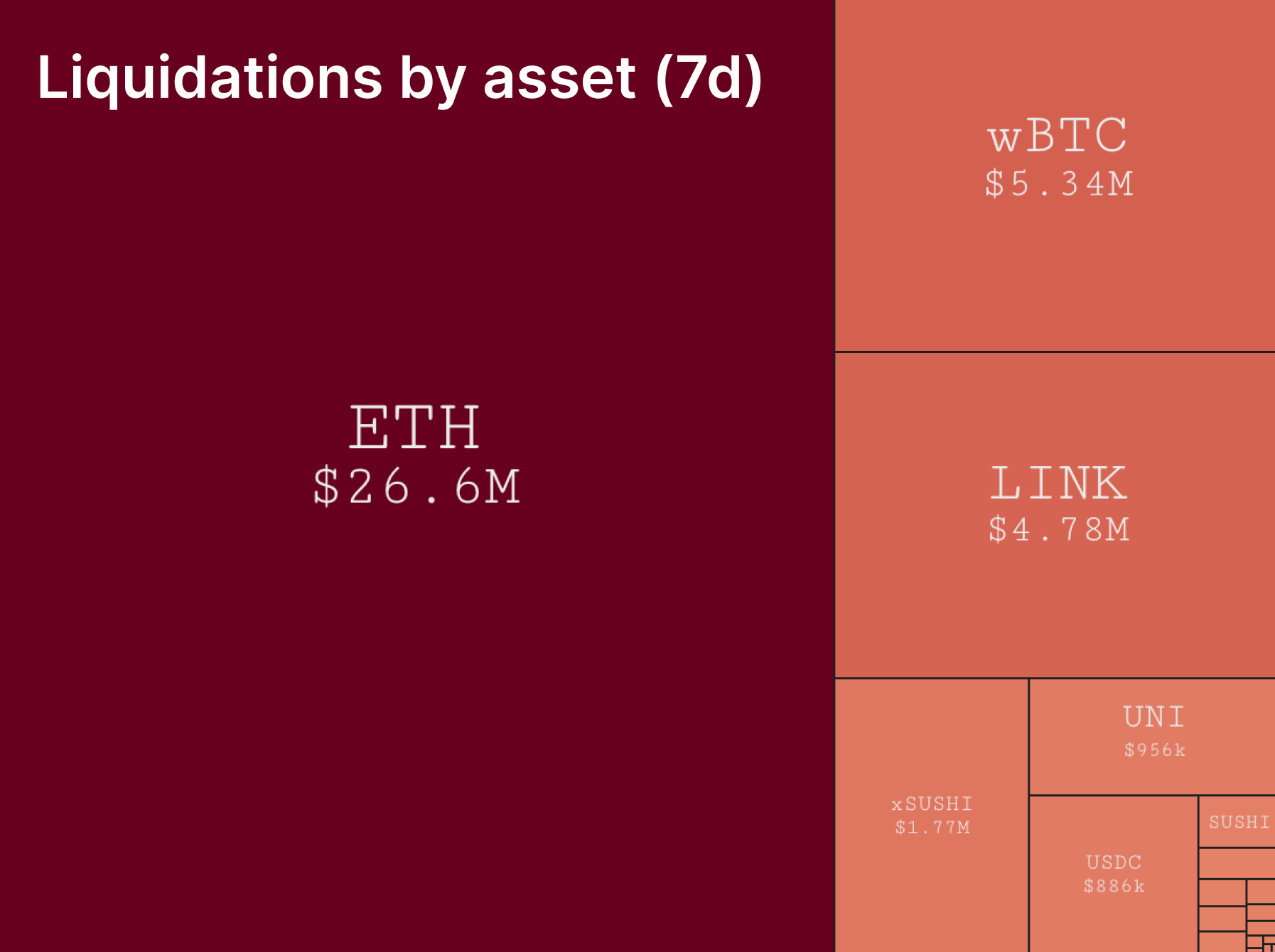

Leverage reduction during times of liquidations shows a clear picture of how the lending markets were been positioned going into the move. In this case, the market showed a clear dominance of ETH as the liquidated collateral suggesting a preference to borrow against and take on leverage via ETH. Per usual, governance tokens represented a comparatively smaller share of liquidations on-chain over the last 7-day period.

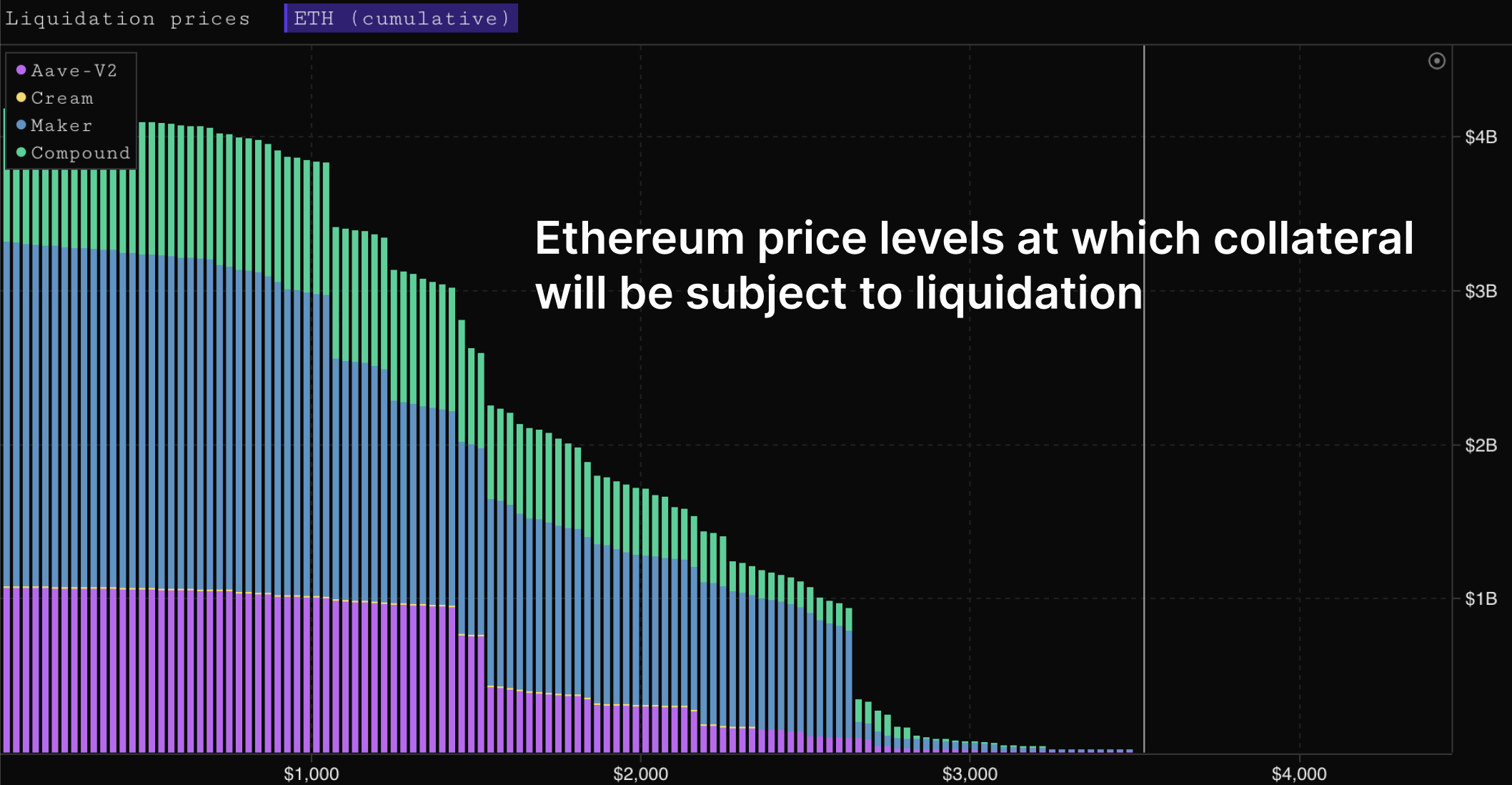

As liquidations occur, we can view the updated positioning of where liquidation thresholds exist and how traders have re-positioned themselves post-crash. We see that the next round of significant liquidations don't start until the ETH $2,600 level.

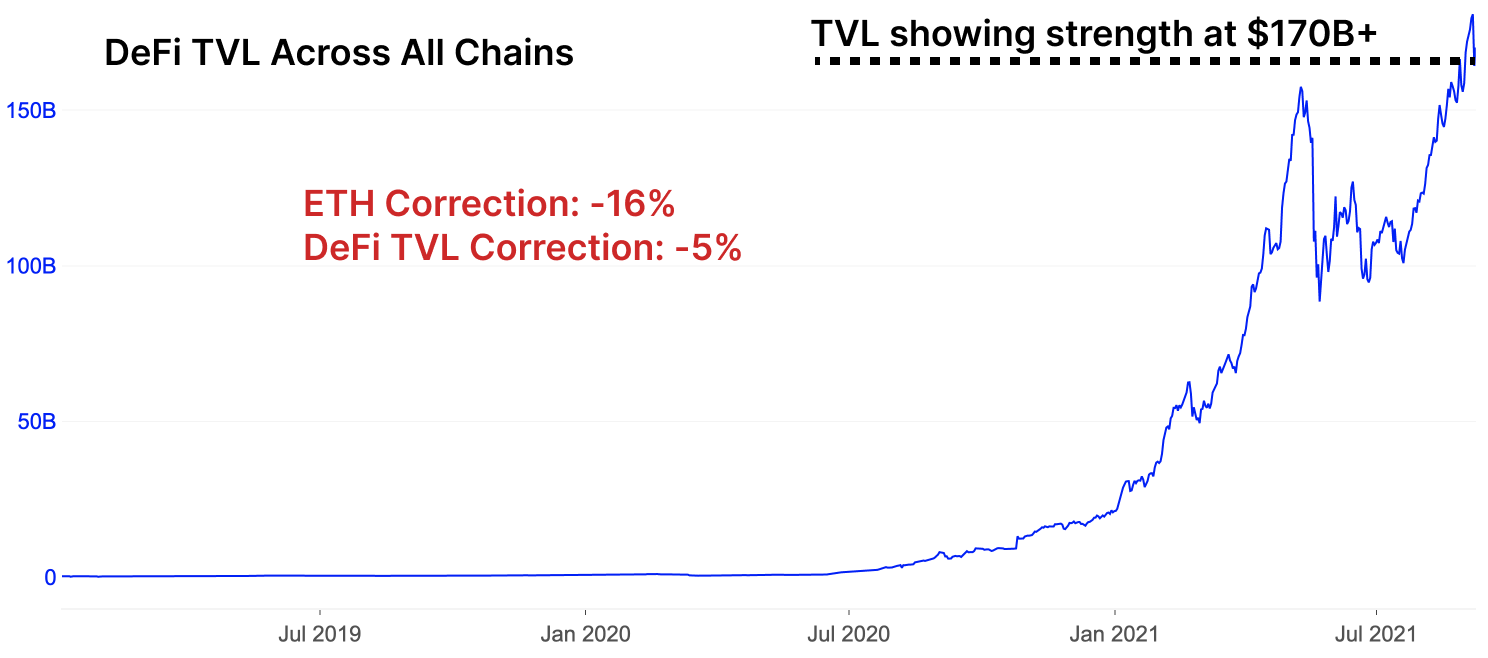

With the pain from a sharp decline in the price of beta (ETH and BTC) comes a corresponding move from alts, where governance tokens have been hit the hardest. We note, however, that despite the sell-off, DeFi protocol usage has pushed forward in its trajectory of capturing more and more value on-chain. Despite pullbacks in dollar value of ETH, cumulative dollar value in DeFi has propelled to new all-time highs.

Time and time again we've watched DeFi protocols show strength and absorb more capital even amongst market corrections. Simultaneously, governance tokens have failed to show the same level of strength suggesting a potential divergence between protocol usage and token valuations. As TVL has pushed past the ATHs set in May, governance token prices are still far from an equivalent recovery. The question is whether this presents a potential opportunity for locating value, or whether this divergence in valuation is a more structural phenomena.

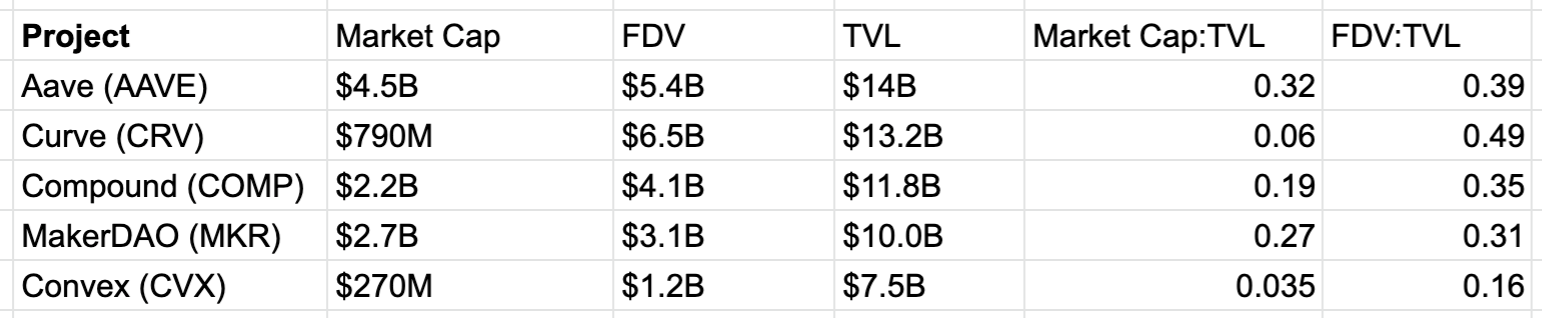

As the majority of activity in DeFi continues to center around stablecoins, the following governance tokens are still far off their ATH market cap, whilst protocol TVL has exceeded ATHs from the same period: Aave, Curve, Compound, MakerDAO, Convex.

First, we compare the Market Caps and Fully Diluted Values (FDV: market cap after including all future rewards/total supply, market cap only includes circulating tokens) vs the TVLs of the key players among the stablecoin heavy protocols. These are the five projects with the most TVL in DeFi by a wide margin.

Next we examine the present ratios against those from May. It tells a fascinating story of how much higher valuations were in May vs Present date. At present, each dollar in a protocol is being valued significantly lower than back in May.

The cause of governance tokens seeing less enthusiasm vs May, despite activity and value locked eclipsing previous highs is an intriguing observation. For now, interest in DeFi governance tokens remains in the back-seat relative to NFTs and even ETH itself while the actual usage of stablecoin-centric protocols continues to balloon.

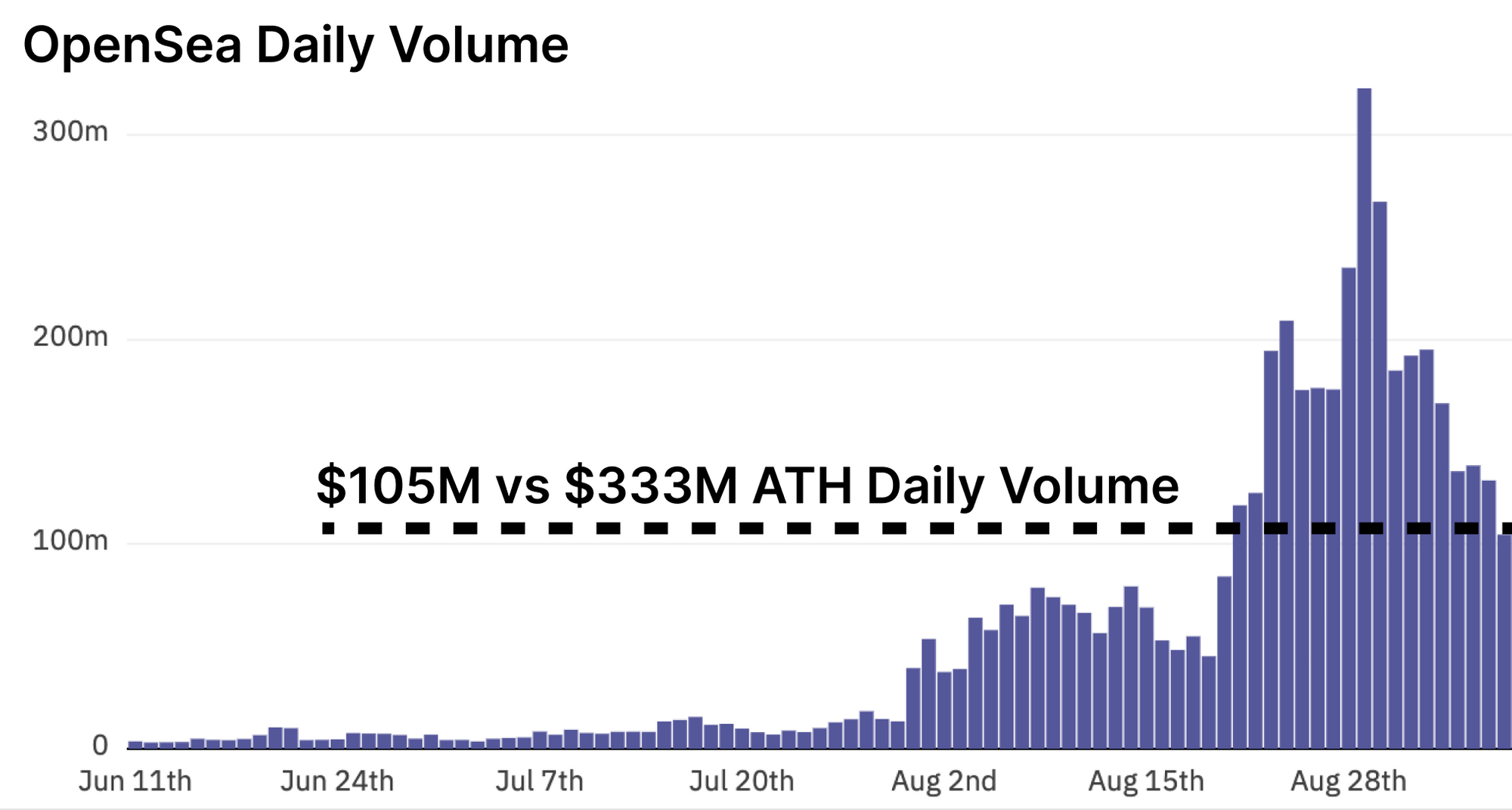

While attention in DeFi remains muted, attention in NFTs has seen a pullback from recent peaks. Volume on OpenSea has finally relaxed from its historic run, returning to a daily volume about 1/3 that of ATH. Regardless of that shift, floor prices in major collections have remained strong in ETH terms.

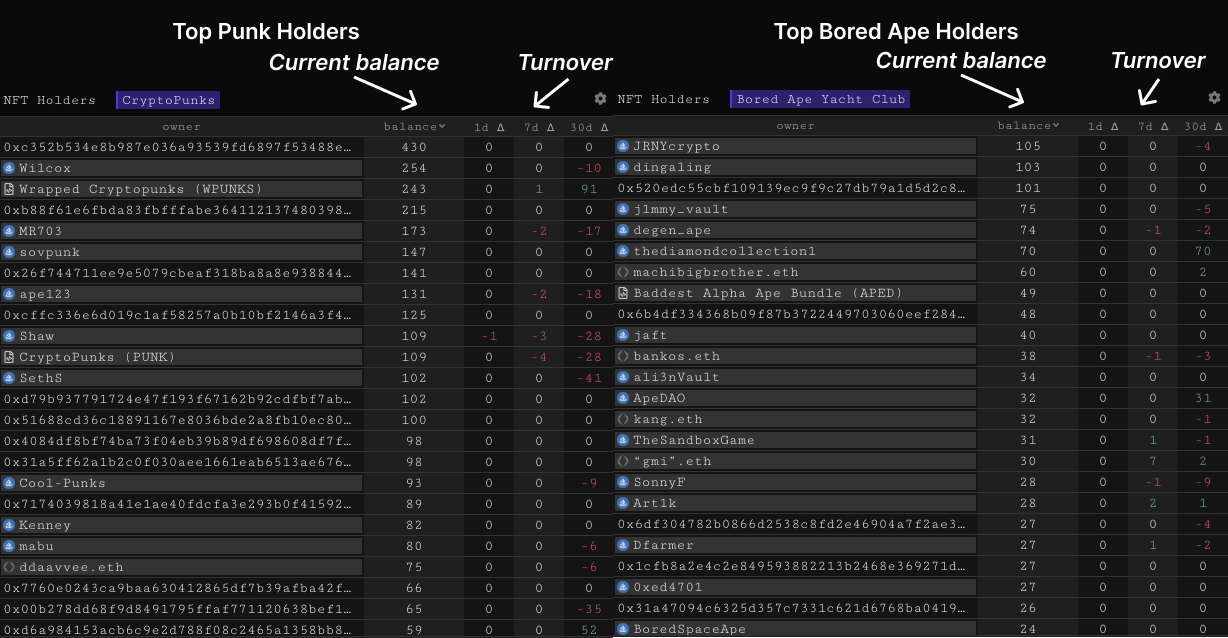

Distribution of NFTs is an interesting study. Seeking to understand who holds what and how these NFTs shift hands can give further insights into how the market functions.

Observing Cryptopunks and Bored Apes we can see the collections with the most holder turnover over various periods. While an older collection like Cryptopunks is seeing significant distribution from largest holders of Cryptopunks, Apes are being distributed from the largest holders less frequently.

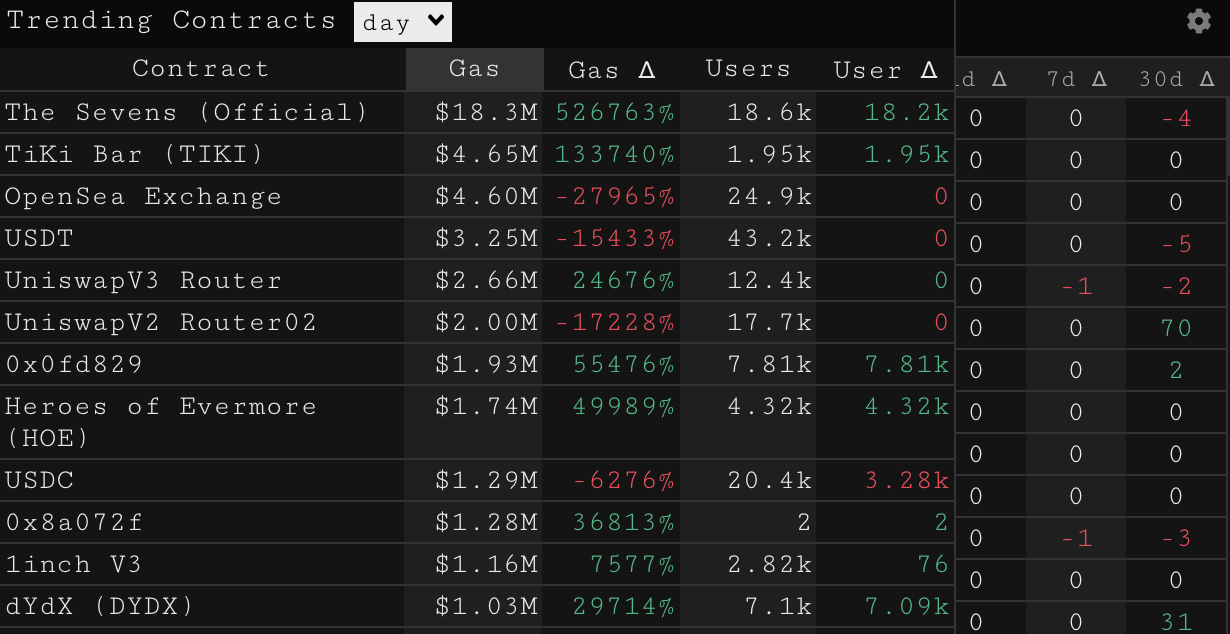

As NFTs remain the dominant gas consumers on Ethereum, the network has become quite congested as Uniswap V3 now regularly competes for gas consumption with V2.

One of the largest NFT events in history happened yesterday as 18k+ addresses looked to mint NFTs from a new collection called The Sevens. This marked one of the highest record sustained mean gas price and consumption over a 10-min period in the history of Ethereum. The only other event with more usage in recent history is the June crash. 18,000+ users went to battle over the 7,000 available NFTs in the collection. Floor price currently sits at 1 ETH.

Closing Thoughts

As broader crypto markets see a significant leverage driven correction, DeFi protocol usage has pushed forward to new heights, even whilst token prices remain somewhat lackluster. Stablecoin-centric usage in DeFi remains the leading application for the ecosystem, as the top 5 protocols by liquidity are all centered around stablecoin usage in borrow, lending and exchange. It's one party of stacking stablecoin yields.

Meanwhile, NFTs have seen a slight pullback in overall secondary market interest. However, one of the largest minting events in history went down with The Sevens, which saw 18,000+ minters competing for 7,000 unique collectables. On top of that, the largest holders of premium NFTs in the CryptoPunks and Bored Apes appear to have moved into HODL mode, with fewer and fewer trades and changes of ownership occurring.