DeFi Uncovered: Does DeFi Outperform ETH?

We asses how the risk-adjusted performance of active and passive DeFi strategies compare to the benchmark of holding spot ETH.

In the explosive growth of DeFi has come countless new projects, tooling, and completely re-imagined ways to engineer new financial products. With this innovation comes growing pains and risks. As such, DeFi typically demands a more hands-on, often active participation. This is a very different experience than the set it and forget it approach many crypto investors are accustomed to.

In this piece we will navigate some of the unique considerations of active participation in DeFi, exploring the difference in returns between holding spot ETH, a basket of DeFi governance tokens, and active participation in yield farming. We will cover concepts and tools for:

- Managing returns, risk, and exposure,

- Measure difference in returns between passive and active strategies,

- Costs to participate in active strategies.

Managing Returns, Risk, and Exposure

Accepting that the cryptocurrency space is experimental and full of risk does not mean one should neglect risk management. Instead, investors can develop awareness of how much risk they are taking on relative to established benchmarks and comparable strategies.

Understanding metrics used by legacy finance can often be useful for understanding a risk/return profile. Below we study a suite of metrics that traders commonly use to track risk and performance, while showcasing how these metrics have played out for DeFi vs ETH.

We compare four strategies over a six month period in our analysis:

- A.) Buy and hold ETH,

- B.) Buy and hold DeFi Pulse Index (DPI), basket of blue chip DeFi tokens,

- C.) Yield farming a popular Sushiswap farm (SUSHI-WETH),

- D.) Yield farming with stables on Yearn Finance.

Strategies Described

Before diving into a comparison of our four strategies, here is a basic intro to how each position works. Each are a simulated $10k position acquired on January 1st, 2021 to track performance.

Buy and Hold ETH

This strategy acts as the benchmark for many DeFi participants. It is the benchmark against which each strategy will be compared in this report.

Buy and Hold DeFi Pulse Index (DPI)

DPI is a market cap weighted basket of DeFi governance tokens. It is a passive index meant to mirror the performance of DeFi tokens. DPI is one of a number of available indices in DeFi. Index is rebalanced at the first of each month.

Governance Token Yield Farming on Sushiswap

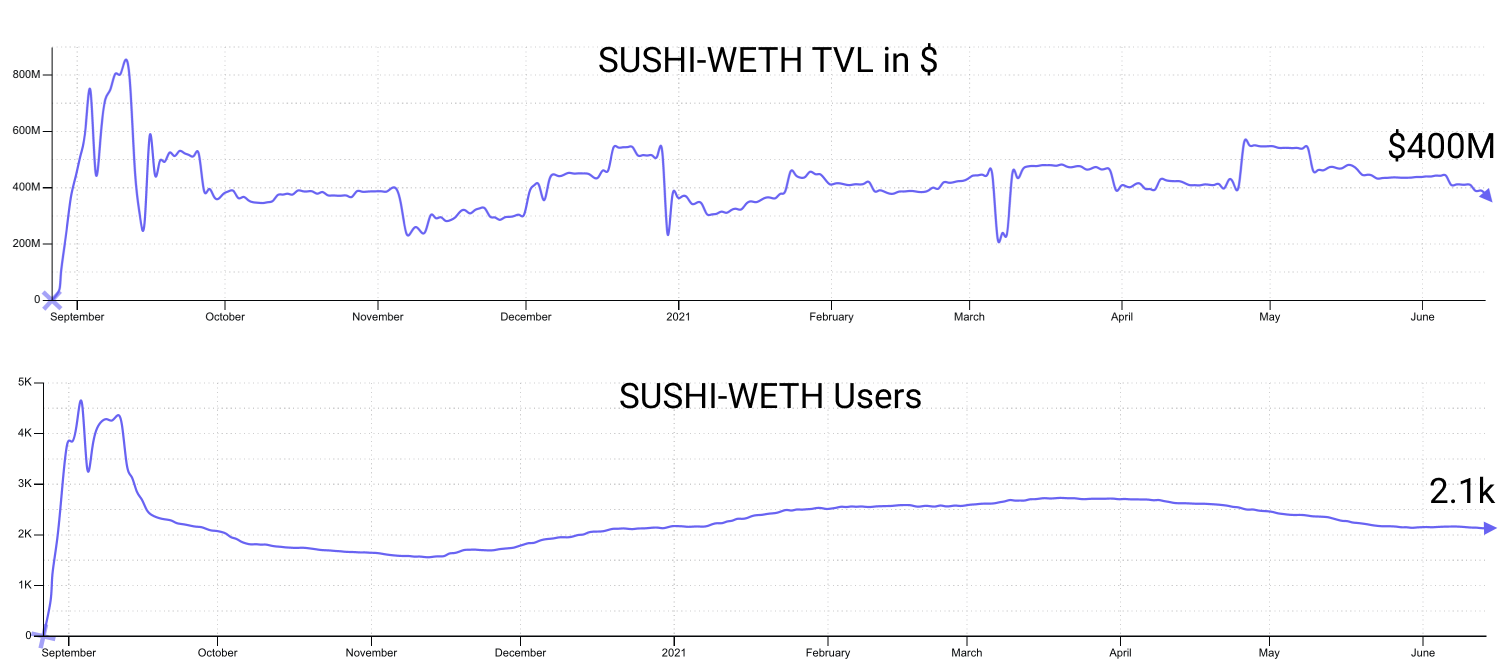

Many pools exist on Sushiswap with varying yield. For the purpose of this piece we will use the SUSHI/WETH pool, the 3rd largest in Sushiswap (~$400M TVL). This pool was especially popular in 2020 and early 2021 because of its boosted rewards relative to other pools in Sushiswap. $SUSHI rewards were in the 100s of % through early 2021, now ~20% APR in June of 2021.

Liquidity providers are able to stake their LP positions to receive yield in $SUSHI along with fees from the pool. Traders can choose to either hold their $SUSHI tokens received in the strategy or claim and sell immediately. For the purpose of this analysis returns are calculated assuming the trader sells immediately. We also ignore vesting schedules.

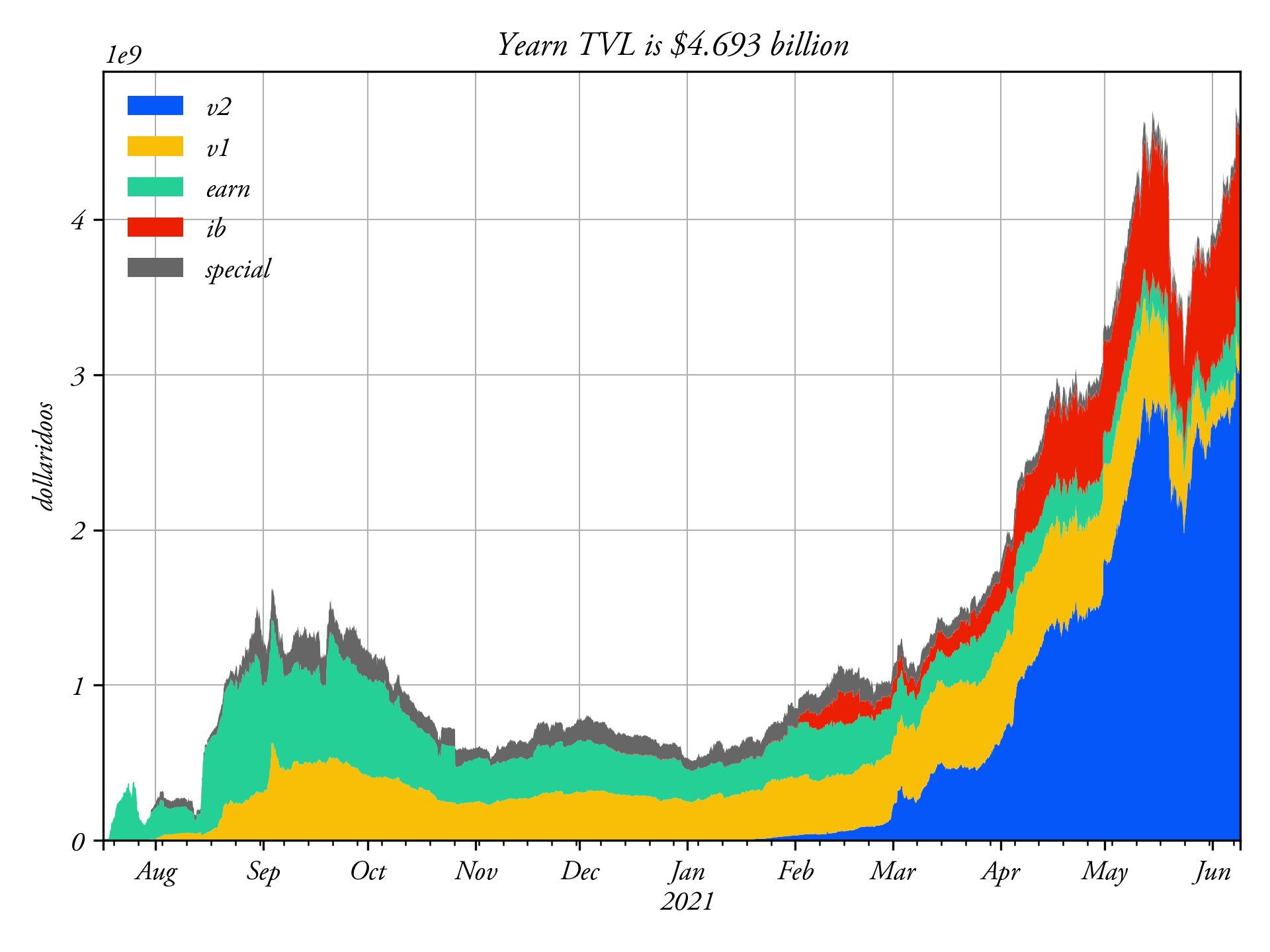

Stablecoin Yield Farming on Yearn Finance

Depositing stables in Yearn provides a yield to depositors. Yearn strategy providers create the strategies that produce the yield for depositors. In return, the platform charges a 2% management fee and 20% performance fee.

And traders are willing to pay these fees for the added value of Yearn strategists. Despite the market downturn, money in Yearn has rocketed to all-time highs.

Returns are calculated simply in this strategy by tracking the historical APY of the yvDAI vault, compounding the depositors returns.

We will now compare the historical performance of all four strategies from the beginning of the year, introducing a suite of basic performance metrics.

Measuring Alpha

When investors refer to alpha, they are typically referring to the excess return generated by a strategy relative to some defined benchmark. This is the non risk-adjusted measure of alpha.

We first measure Buy and Hold ETH against Buy and Hold DeFi governance tokens using the DeFi Pulse Index (DPI). We see that a simple comparison of returns shows DeFi governance tokens significantly underperforming ETH on most time periods this year. DPI suffered the worst returns against ETH from March declining -18% while ETH gained +30% over the same period. Since the start of 2021, DPI is up 2.8x and ETH is up 3.6x

DPI has produced negative alpha against ETH in 2021.

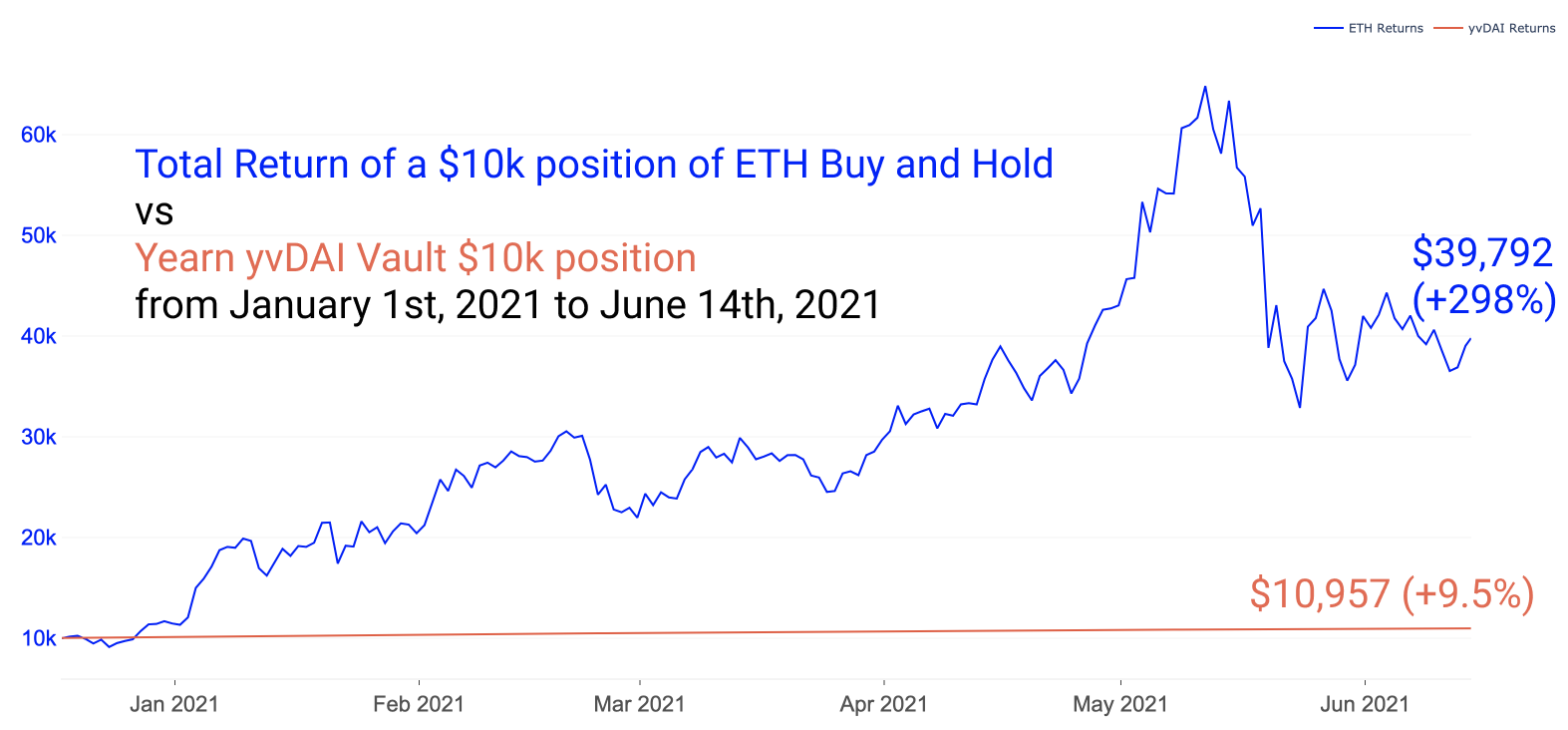

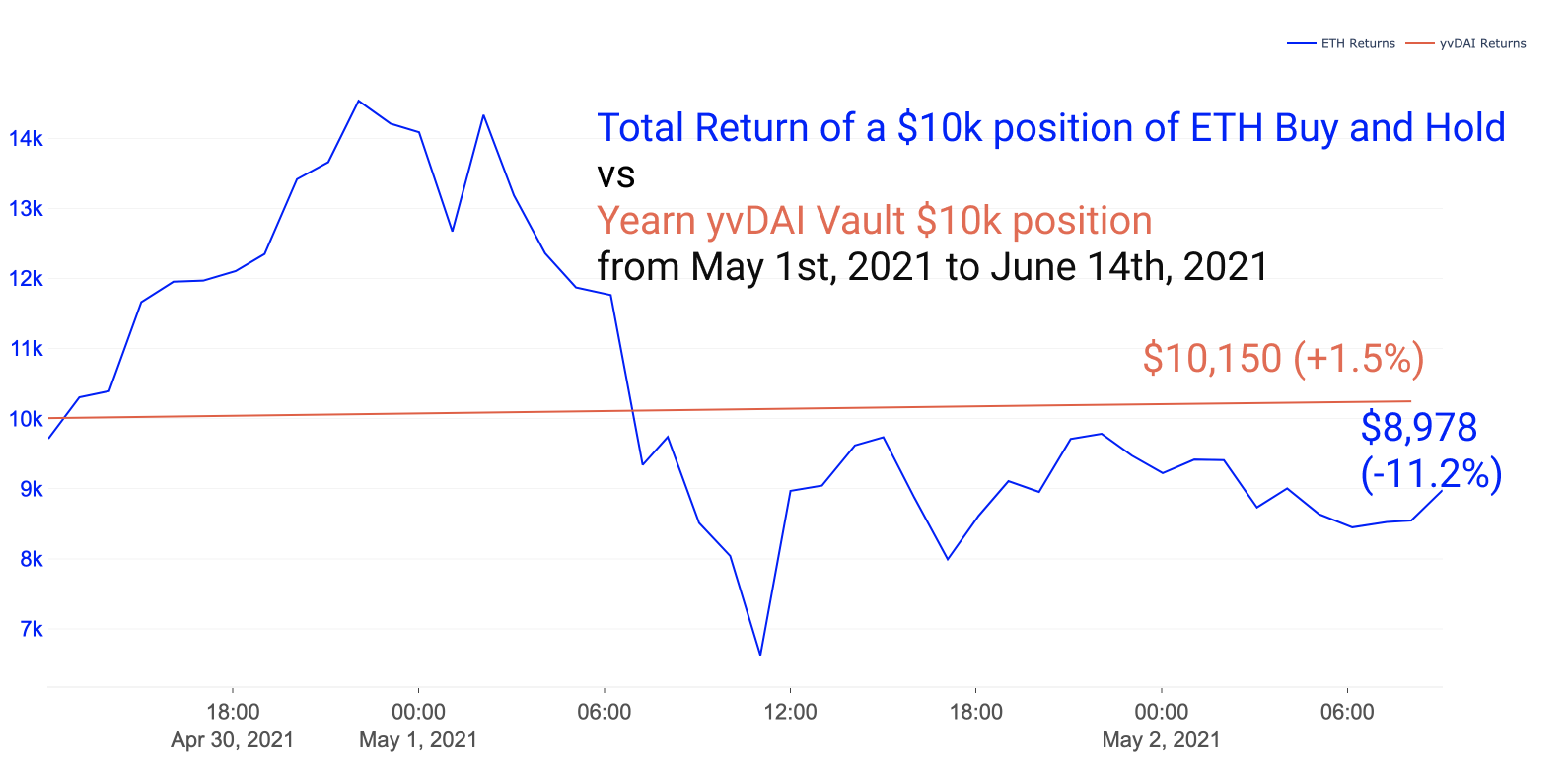

Passive participation in DeFi has largely underperformed ETH in terms of total return in 2021. Next, let's examine total return of ETH Buy and Hold vs Yearn Finance Stablecoin Farming.

ETH's run since the start of the year has been historic. As such, it's no surprise that a stablecoin strategy has underperformed ETH Buy and Hold. Over the course of the year the average APY of Yearn's yvDAI vault was about ~15%. Our stable strategy shows a flat line because of how much it underperformed ETH this year.

With that said, stable strategies outperform ETH on various cherry picked timeframes. For example, since the start of May, ETH Buy and Hold has underperformed by a significant margin while APYs on Yearn stables hovered around 8-12%. This is obviously a similar case for simply holding cash, but by depositing cash in Yearn the trader receives yield while being mostly risk-off.

Depending on the period we cherry pick, yvDAI has produced alpha over an ETH Buy and Hold strategy. Some traders keep a portion of their portfolio locked in yvDAI or other Yearn stable pools at all times to produce yield while holding stables for buying opportunities during a downswing or trendy pool opportunities with high yield.

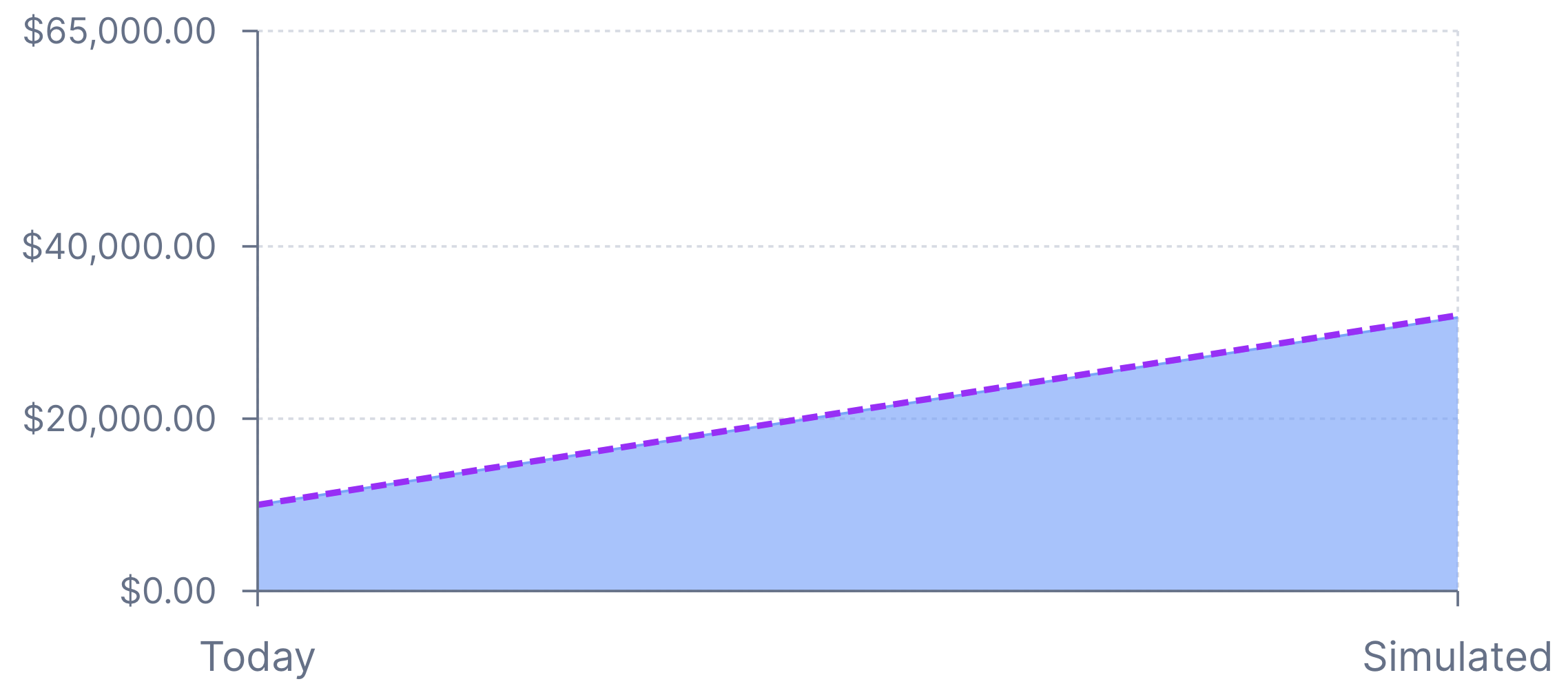

Finally, we measure the total return of ETH Buy and Hold vs farming yield on the boosted rewards from the SUSHI-WETH pool on Sushiswap. This analysis becomes a bit more complicated because of the choices presented to the user and the behavior of AMMs. In this simulation we ignore the SUSHI-WETH chop, assume immediate sale of rewards, and ignore the 6 month vesting period. We run a simple simulation in Croco Finance to see our pool started as $10k and ended the period with ~$32k after fees and impermanent loss.

On top of that $32k we add additional Sushiswap rewards. After all fees, impermanent loss, and incentivized liquidity rewards in $SUSHI are added together, the final value was achieved over this period. This is calculated with an average 140% APR in $SUSHI rewards for SUSHI-WETH LP stakers over the 6 month period. Returns are simulated as a worst possible scenario, with no compounding, bottom APR, poor timing for exposure to the underlying, etc.

As shown, simple buy and hold of DeFi governance tokens has significantly underperformed ETH buy and hold in total return YTD. Active participation in the SUSHI-WETH pool outperformed ETH Buy and Hold. This was the case in many major risk-on yield farming opportunities. Note that on most of the timeframes that stable strategies outperformed ETH, so did cash.

Total return is obviously not the only metric that matters. Next we measure volatility and risk-adjusted metrics.

Volatility

Volatility seeks to measure the dispersion of returns over time. Standard deviation is most commonly used to measure this value; it is calculated using the square root of the variance of historical returns. Higher standard deviation means higher volatility.

All things equal, traders desire lower volatility. Risk-adjusted alpha is acquired when a trader creates excess return without adding volatility relative to the benchmark.

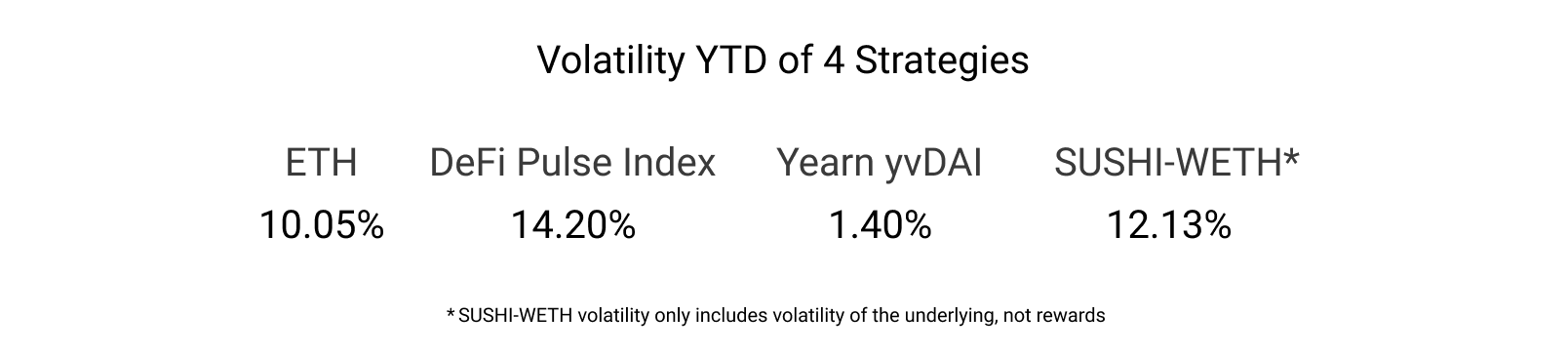

Crypto assets are notoriously volatile. That said, crypto strategies do not have to be. Let’s examine the volatility of our four strategies. We take note that while our Yearn Finance strategy underperformed in total return, its volatility was negligible. Traders looking for a consistent return but low volatility would likely find the yvDAI vault incredibly attractive. Similarly, the SUSHI-WETH strategy receives SUSHI rewards while absorbing some of the DeFi volatility with exposure to ETH. What volatility the SUSHI-WETH pair hedges, it suffers in impermanent loss. The below volatility only reflects the volatility of the underlying, after fees it actually absorbs some of this vol.

Note: risk can also manifest in ways other than pure price volatility in DeFi, i.e. smart contract risk.

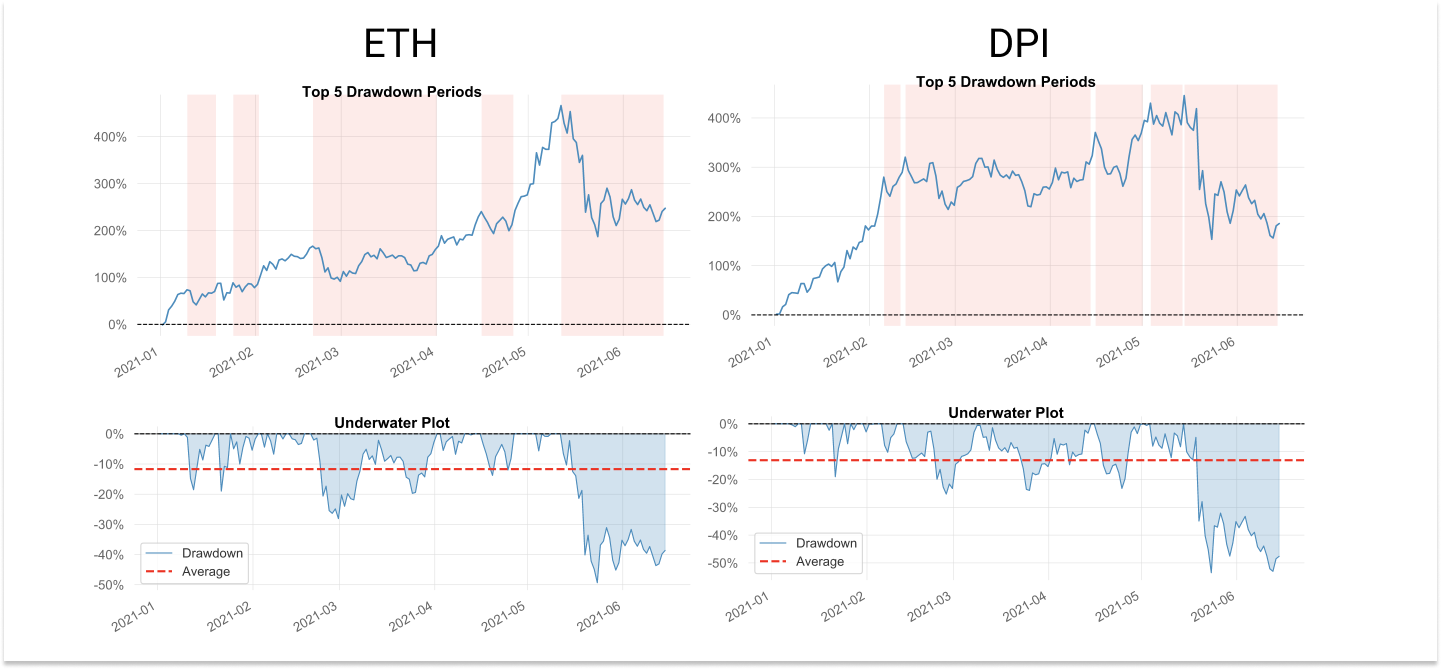

Traders also like to use drawdowns to understand how long periods of downturn last and to what magnitude. Drawdown periods and underwater plots are useful for this analysis. As an example, we study the difference between ETH and DPI.

The top charts represent length of drawdowns, while the underwater plots represent magnitude of drawdowns. We can find two key insights from these charts:

- DPI's length of drawdowns have been significantly longer than ETH.

- DPI's average magnitude of drawdowns have slightly exceeded that of ETH.

- Max drawdown of ETH hit about -49% while DPI managed to push to -52%.

Risk-Adjusted Metrics

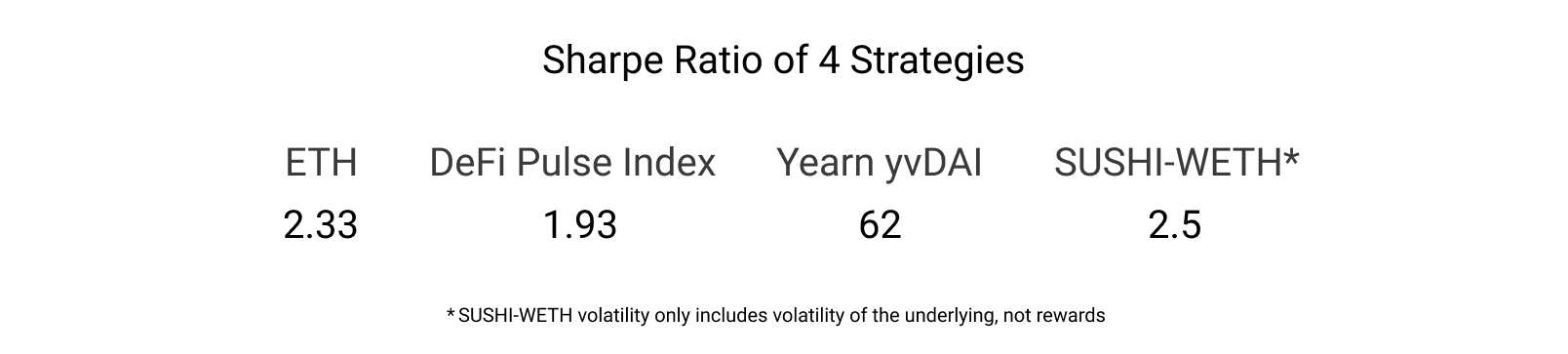

Sharpe Ratio is a popular risk-adjusted metrics that seek to measure returns against volatility. Traditional finance thinks constantly about risk-adjusted returns as they are always thinking about preservation of capital.

Sharpe Ratio is calculated by taking return minus the risk-free rate, and dividing by the return’s standard deviation. It captures both the upside and downside volatility in its calculation.

In this case, the 10-year is used as the risk-free rate. Note that the yvDAI Sharpe Ratio is wildly high because it's a stable strategy. Because we use the 10 year treasury rate (1.5%) in this case, the Sharpe Ratio on this strategy is incredibly high. This is because the position's volatility is negligible and the asset is up only against the risk-free rate. Strategies being this risk-off with returns this far in excess of the risk-free rate are incredibly rare. The Sharpe Ratio of SUSHI-WETH is also subsidized by the excess returns created by the $SUSHI reward and collected fees; any downside volatility is slightly dampened, upside volatility is boosted. 1 is generally considered a good sharpe and anything over 2 good to excellent.

Note: the unique risk of smart contract exploits or protocol failure does not manifest in purely price-based r/r metrics like Sharpe and Calmar Ratio.

Traders must take into consideration the unique risks presented in pools being drained by exploits.

Metrics Applied

By understanding and applying these metrics we can understand how strategies have performed historically in various environments. For example, while markets suffered, risk-on strategies suffered while the stable farming pools continued to see upside. Some traders choose to hold a percentage of their portfolio in stables in all markets to produce yield while also having capital available for buying dips.

Reminder that past performance is in no way indicative of future returns, and past safety from smart contract exploits is in no way indicative of future smart contract safety!

Costs of Active Strategies

A few major costs are induced by participating in active strategies. Our above analysis neglects these costs. At a large enough size, some costs become negligible, others remain relevant. We will cover:

- Gas Fees

- Impermanent Loss

- Market Impact, Transaction Fees, and Other Fees

Gas Fees

Gas costs are an important input that must be considered by yield farmers, becoming increasingly expensive for smaller position sizes. At a certain level of capital and participation, an investor becomes better off buying and holding beta.

Each core action in DeFi will have a gas cost associated:

- Basic Token Transfers

- Transaction Approvals

- Swaps

- Pooling Tokens

- Staking LP Position

- Claiming Rewards

- Pooling and Staking to Compound Claimed Rewards

Seven key actions, total Gwei for these actions >400 Gwei at current gas price of ~10 mean Gwei (>$50). Gas is down 90% off ATH gas prices during the peak of the bull run. At peak mean gas prices rarely dropped below 75-120 range, meaning the cost of these seven key actions regularly exceeded >1500 Gwei, at those gas prices meaning easily >$200 to swap, pool, stake, and claim rewards.

Manage a handful farming positions over the course of a month and your total cost of deposit and withdrawal can easily reach hundreds of dollars. For many DeFi participants, gas costs from entering and exiting pools and staking positions is often the largest expense. Then one must factor in volatility in gas prices which have historically reached and sustained far higher levels.

Impermanent Loss

We alluded to impermanent loss earlier in the piece. Pools with divergent assets can suffer significant downside from impermanent loss. Basic pools are a 50/50 pair of a governance tokens vs another token. Governance tokens suffer significant volatility. This "impermanent loss" is created due to the way AMM pools function. Arbitrageurs work to keep these 50/50 pools balanced and priced appropriately, pocketing profit from price arbitrage.

This price arbitrage results in impermanent loss as assets diverge in price from time of deposit. Larger divergence results in increased impermanent loss. Traders can expect some level of significant impermanent loss in almost all risk-on farms in DeFi. The goal is to outperform this loss in liquidity mining rewards and trading fees collected.

Notice in the following simulation that a 1.15x of UNI and a 0.83x of ETH results in 1.31% of a position lost to impermanent loss. Our simulation shows the number of days needed to reclaim this value in fees. Another way to reclaim this value is if the prices return to the original value - hence the "impermanent."

Other Fees

Many platforms have transaction fee structures in place for using the protocol. These are mechanisms for collecting revenue for protocol treasuries and token holders. Standard DEX fees for example are typically ~0.30%.

Slippage is the difference between a trader's expected price and resulting price from a trade. An expected $1,000 value trade that nets $990 would be 1% slippage.

Price impact is especially important to traders of size. Traders use aggregators and purpose built algorithms for minimizing price impact from hitting thin liquidity in AMMs and order books. Small traders can expect to minimally lose a few bps to price impact in low liquidity environments. Larger orders can expect to suffer significantly higher price impact. Large orders into thin liquidity can oftentimes create attractive opportunities for arbitrage.

Other fees in the ecosystem include fees like management fees, performance fees, and withdrawal fees, arguably all popularized by Yearn. These are basic fees that go to the strategy developers, treasury, and sometimes holders. Basic 2 & 20 structure is used by Yearn - 2% management fee and 20% performance fee.

Strategy Costs

- Buy and Hold ETH is obviously our strategy with the lowest costs. The only fees from this strategy would be fees to exchange.

- Buy and Hold DPI would have similarly low costs; this is an advantage of using an index like DPI. Additional costs would include a 0.95% streaming fee which can be thought of the same as a management fee.

- Yield Farming in Sushiswap would incur the gas costs of swapping to acquire the assets, pooling the assets, and staking the LP position. Over the 1 year period the SUSHI-WETH has not suffered significant impermanent loss, instead profiting 6% YTD from fees and the additional rewards from $SUSHI liquidity incentives.

- Yield Farming Stables in Yearn Finance is a relatively gas efficient strategy, only incurring the gas cost of swapping to stables and depositing to the pool. Yearn charges 2% for management and 20% for performance, taking 20 cents for every dollar Yearn makes you.

Concluding Remarks

DeFi’s returns have been lackluster for idle buy and hold strategies. A buy and hold strategy for DeFi governance tokens has broadly underperformed ETH over most timeframes. Many active strategies, however, have outperformed, and an active rotation into stablecoin farms during periods of increased downside volatility has similarly outperformed buy and hold ETH.

While returns in DeFi governance tokens have been underwhelming at times, access to yield on assets an investor would otherwise choose to hold regardless is incredibly powerful.

Uncovering Alpha

This is our weekly segment that briefly discusses some of the most important developments of the prior and upcoming week.

Gas prices have consistently touched single digits average gwei over short periods as activity has significantly slowed across the space. As activity slows, dev cycles are starting to come to fruition as tons of new products and versions are getting pushed.

- Alchemix releases alETH and Alchemix/Sushi Masterchefv2 double rewards expire. Alchemix added alETH with ETH as 4:1 collateral against alETH, the same self-repaying loans as with DAI and alUSD. Additionally, a week long of 2x rewards expired on the ALCX-ETH pool. Double-sided rewards persist with an APR of ~170% vs the single-sided pool at about ~95% as well.

Note: at time of writing the Alchemix team has discovered an exploit in the alETH pool. Borrow has been locked as they work on a fix.

- Arcx launched v3 of their DeFi passport. Arcx and others are toying with the idea of a DeFi style credit rating. The idea is that addresses who have historically had healthy behaviour, high participation, etc are better candidates for incentivized rewards, early features, etc.

- Siren launched their options market on Polygon.Another options protocol launching after derivatives have been healthily funded over the last 6 months. Expect more projects to continue to role out options, futures, and other instruments. For now adoption of on-chain options is negligible; perhaps with layer 2 this will change.

- Alpha Finance Lab launched a decentralized product launchpad. They intend to fund projects relevant to their ecosystem through this new decentralized investing vehicle.

- DFX launched their forex AMM.

- Curve V2 launched with a whitepaper full of complex math. Many are still toiling over the implications.

- Matcha released v2.0.DEX aggregator Matcha powered by 0x protocol released version 2.0, sporting Polygon support, a fiat on-ramp, and more.

- 1Inch added an OTC market and limit orders without extra fees. As more and more projects in the space look to combat front-running and other mempool externalities, 1Inch launched an OTC market aimed at reducing slippage, front-running, and other benefits for large trades. They additionally launched limit order swaps without extra fees.

- Sushiswap integrated with PoolTogether for added Sushi rewards on PoolTogether lotteries. PoolTogether is a platform for farming yield where users are additionally entered into lotteries. Sushiswap continues to actively forge partnerships across the ecosystem.

- Follow us and reach out on Twitter

- Join our Telegram channel

- For on–chain metrics and activity graphs, visit Glassnode Studio

- For automated alerts on core on–chain metrics and activity on exchanges, visit our Glassnode Alerts Twitter

Disclaimer: This report does not provide any investment advice. All data is provided for information purposes only. No investment decision shall be based on the information provided here and you are solely responsible for your own investment decisions.