DeFi Uncovered: Experimental Lending Platforms

A dive into the nascent markets emerging from experimentation in DeFi lending. We explore some of the heightened rewards that can emerge from elevated risk.

Introductory Note: We have included a brief section at the end of this article (and in future DeFi articles) covering the most pressing news and events from the previous week. We will cover topics such as new product launches, important partnerships, and opportunities such as community airdrops or the launch of incentivized participation schemes.

Small and Mid-Cap Lending Platforms

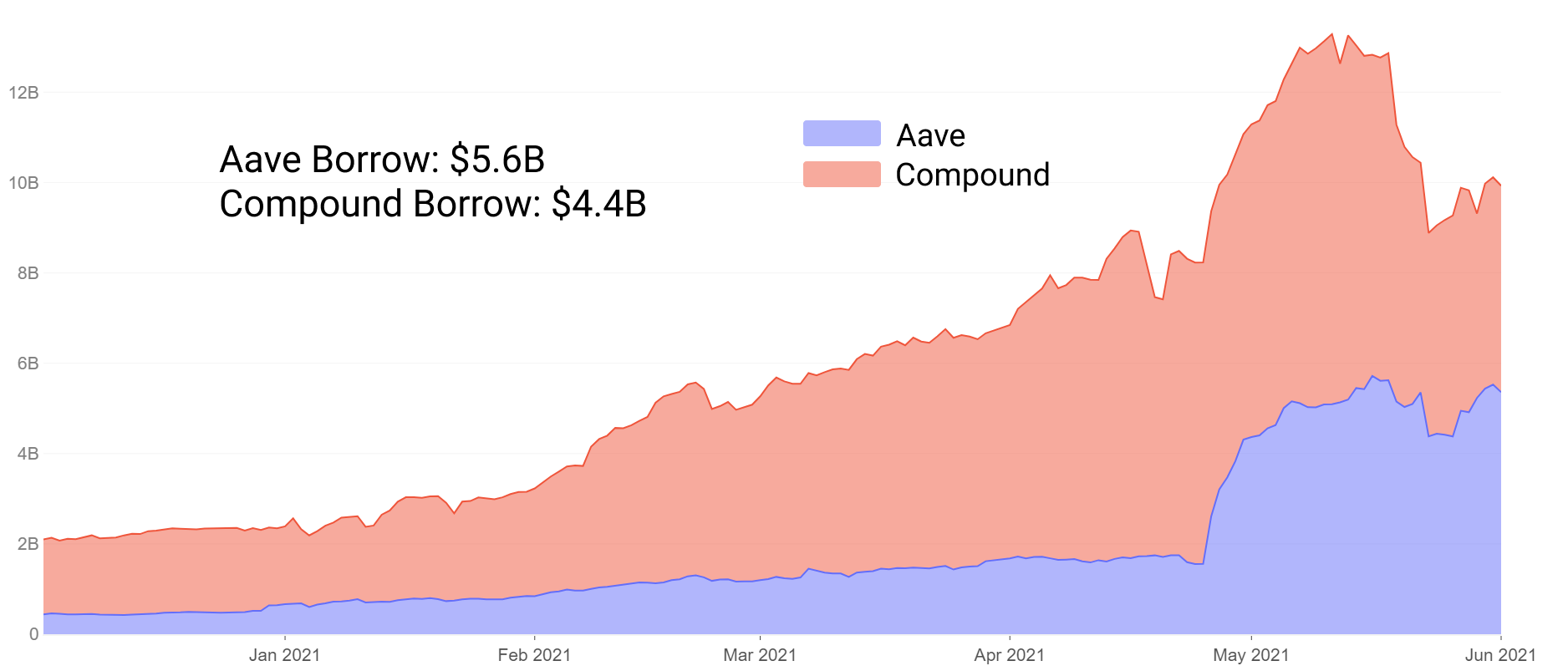

Lending has led the blue chip DeFi projects in total liquidity for some time with Aave and Compound remaining dominant in the sector. Their rise has seen total value locked rise from $100M to $15B+ collateral in less than 24 months. This is driven by a tried and true formula of multi-asset overcollateralized lending, with stablecoin liquidity having the lead in adoption amongst borrowers.

A few months ago Aave flipped Compound in total deposits, fuelled in part by its liquidity mining incentives, and added features like additional collateral options, stable rates, and more. As of June, Aave has also flipped total value borrowed, now dominating lending in both deposits and outstanding borrow.

We can partly attribute Aave's success to its willingness to innovate and align incentives with users. That said, with tried and true protocols comes difficulty to experiment.

There is limited incentive for markets of Aave or Compound size to experiment with entirely new ideas that could put >$10B in collateral at risk. Instead, we can look to younger projects and starry-eyed communities for new takes on what innovation in the lending market could provide DeFi participants going forward.

In this piece we will explore five young projects with market caps all <$300M, all of which are less than 10 months old, some as young as 3 months old. We will cover:

- Innovation/experimentation - how they differ from Aave and Compound

- Comparatively high risk/high yield farming opportunities among nascent lending projects

Self-Repaying Loans on Alchemix

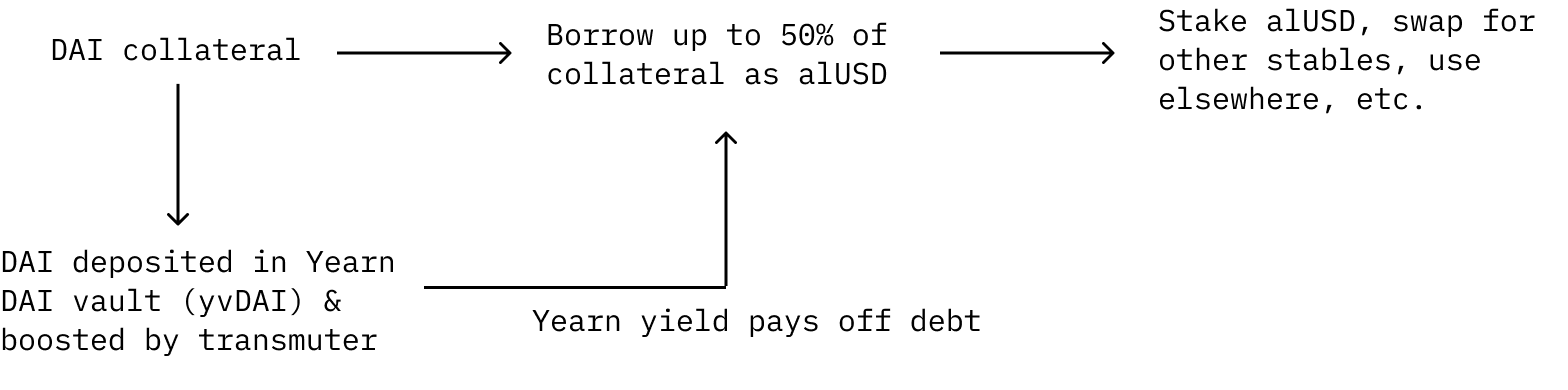

Alchemix has received lots of attention for its unique future yield scheme. DAI can be deposited as collateral from which users can borrow alUSD. Depositors can borrow up to 50% of their collateral as alUSD. Their debt is automatically payed down by yield from Yearn Finance.

The deposited DAI is sent to the Yearn Finance yvDAI vault to earn yield. Instead of paying interest on their loan, the debt is automatically paid off by yield generated from the DAI deposited in Yearn. Additionally, returns are boosted by yield from the “transmuter” which is a mechanism to backstop the protocol and act as the primary mechanism for pegging the protocol's synthetic token(s).

It’s important to note that in this setup user collateral can not be liquidated by outside forces since user debt is only decreasing over time as the protocol receives yield from the Yearn yvDAI vault. The obvious risk here is that if the Yearn yvDAI yield trended towards 0% the loan would theoretically never be paid off. Users can still manually repay their debt if rates become underwhelming.

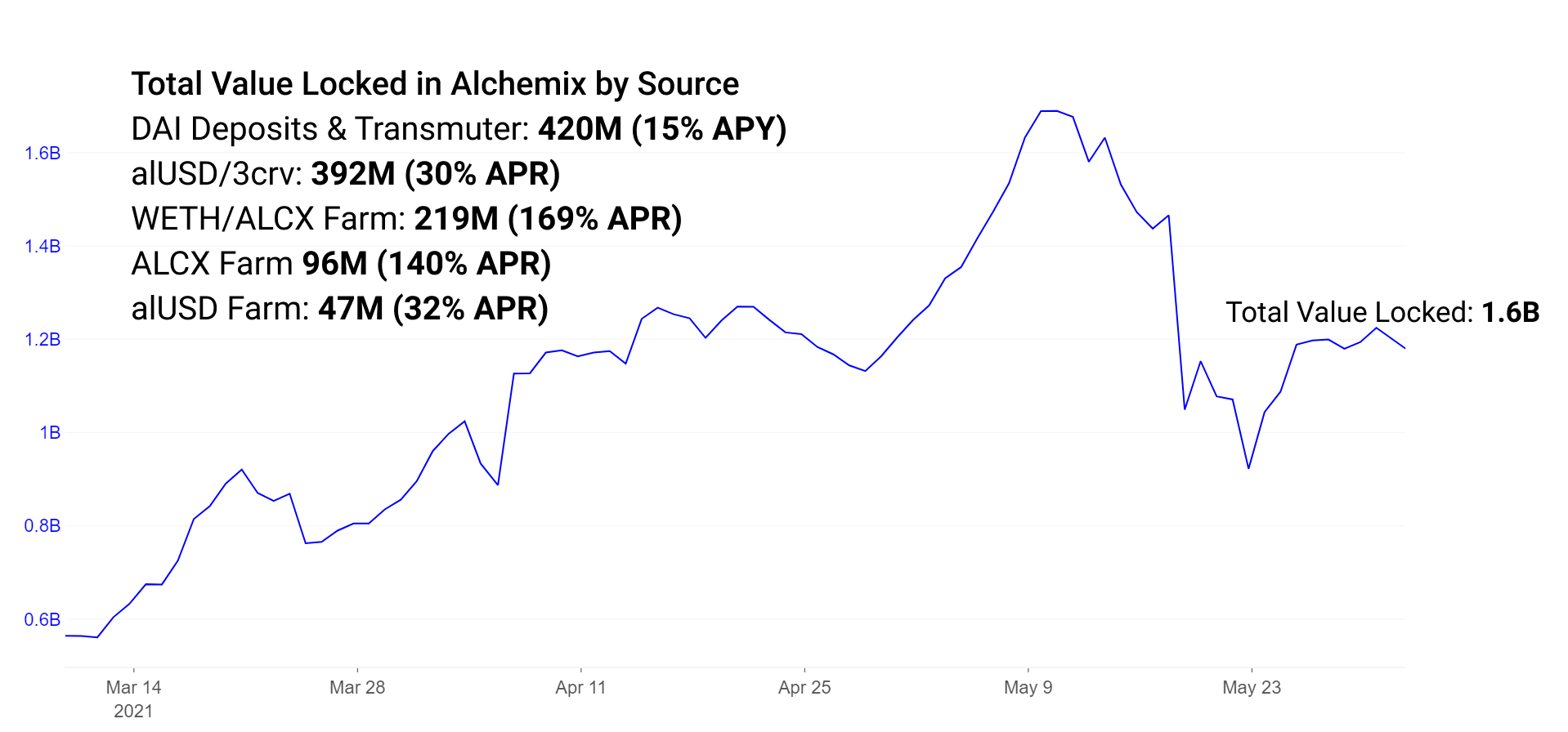

Alchemix currently accounts for over 260M of the DAI currently deposited in Yearn Finance from the Alchemix deposits and 150M alUSD currently sits in the transmuter, converting to DAI and boosting rewards through additional Yearn deposits. Additional TVL in the Alchemix ecosystem exists in liquidity incentives and single-sided reward mechanisms.

alUSD can be used like any other stablecoin in the DeFi ecosystem. Popularly it is used in either the alUSD pool on Curve + Convex or the single-sided alUSD farm on Alchemix. Note that this single-sided farm is slated to be retired. Incentives exist in the alUSD pool on Curve to encourage more liquidity for trading alUSD to other stable pairs.

Farms are additionally set up for incentivizing liquidity in an ETH/ALCX pair to trade the governance token on Sushiswap.

Returns of each farm currently sit as follows:

alUSD3CRV Pool: 30% APR

ETH/ALCX Pool: 170% APR (Note this is the pool 2 farm, meaning the farmer requires exposure to ALCX, the native governance token; this pool has high risk of impermanent loss should the price of ETH and ALCX diverge.)

Single-sided ALCX Pool: 140% APR

Single-sided alUSD Pool: 30% APR (soon to be discontinued)

The ETH/ALCX pool is slated to be migrated to the new Sushiswap Masterchefv2 contract in the coming days. This new contract from the Sushiswap team enables multi-reward liquidity incentives. This means in the case of Alchemix that the pool now rewards stakers in both the governance token ALCX and Sushiswap’s SUSHI token.

As Alchemix matures there are a number of experimental features and advances of the protocol that can be explored. Soon to be released features include alETH and alBTC, adding more forms of collateral to the protocol. Additional collateral is attractive for users who prefer holding these assets over stablecoins. Risk-on collateral has proven successful in Aave and Compound. In Compound, ETH is the largest source of collateral, whilst in Aave, ETH comes in second. It is likely that Alchemix collateral would spike once ETH deposits are enabled. Additional synthetic assets are additionally attractive to token holders who want access to varried sources of borrow through Alchemix.

Lending in Cream Finance and Under Collateralized Loans in the Iron Bank

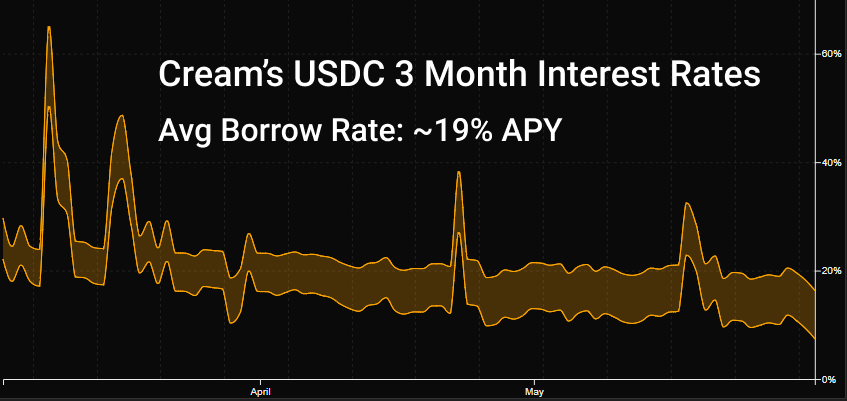

Cream is the oldest protocol on our list, having launched last August. The protocol has slowly found its place in the ecosystem, partnering with Yearn as the Yearn ecosystem’s preferred lending protocol. Due to the maturation of Aave and Compound, normal lending behavior is to find the best possible rates and deepest liquidity in those markets. Cream's wide array of assets allows it to be the commonly used third option that is utilized as necessary for niche borrowers.

Cream currently supports 78 assets of varying size and volatility, however notably smaller in market size than competitors. Large depositors can easily inflate the size of collateral pools to reduce lending APYs, and similarly, can withdraw in bulk and inflate the interest rates. The end result is that interest rates available at Cream are typically higher and more volatile than the larger lending markets.

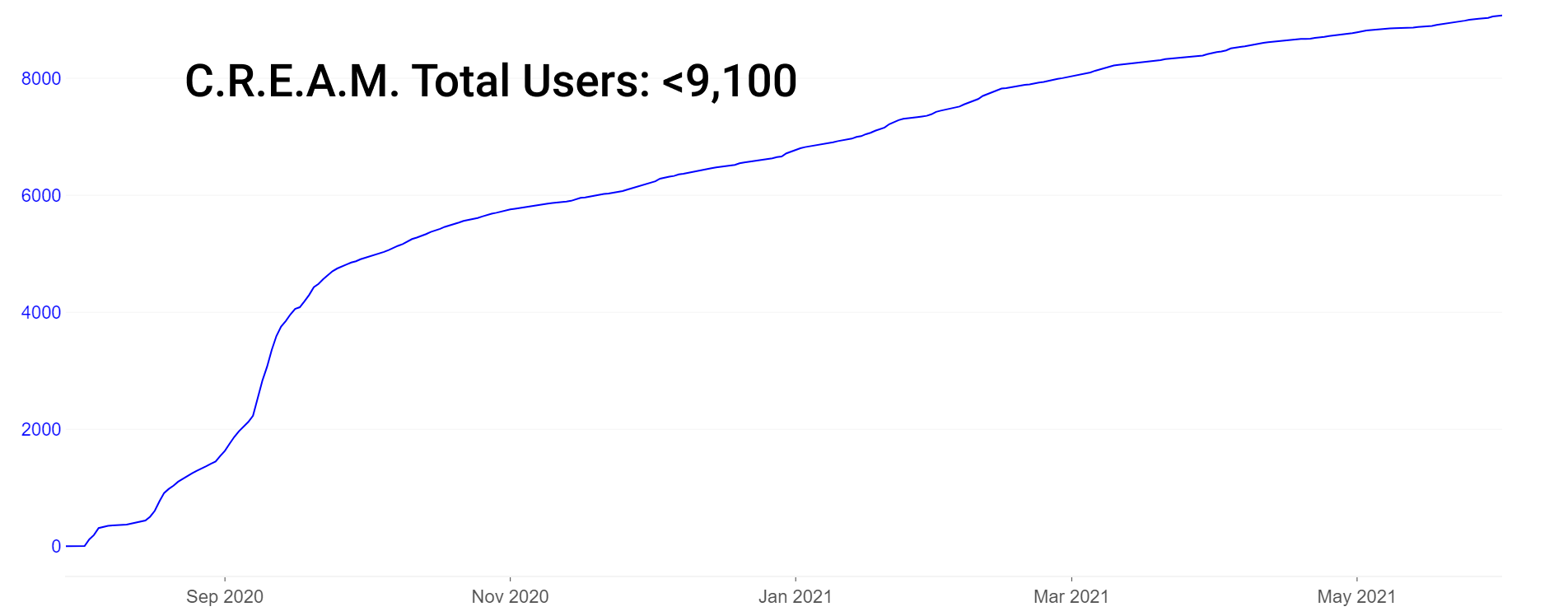

Note that Cream has a relatively low number of users (~9,000) alongside its $1B in TVL, however such low user number is actually not unique among DeFi protocols. Comparatively, Aave only boasts about 40,000 total users (unique addresses) having ever interacted with the protocol.

Cream’s largest innovation of late is its focus on protocol-to-protocol lending, potentially making excessive attention paid to user numbers less relevant. Instead, depositors and borrowers of both credibility and size are given far more weight. Cream sets credit limits on zero-collateral borrowers on a whitelist of addresses. These include trusted protocols like Yearn and Alpha Finance. This is an important innovation because it allows protocols to borrow assets without wasting their own liquidity as collateral. As such, the Iron Bank product currently boasts $770M in collateral.

Savvy yield farmers can bounce their assets around a number of high yielding markets. Here are some sample APYs in pools with healthy liquidity in the iron bank and Cream lending:

DAI, USDC: ~6% base APY in Iron Bank, ~10% in C.R.E.A.M

wBTC: ~7% base APY in Iron Bank, 1.4% in C.R.E.A.M

As time goes on, protocols which mimic features of the Iron Bank’s zero to undercollateralized credit approach have been released. Ideas in tying credit to bank accounts (Teller), through identity to social media accounts (unannounced), and through purely governance driven votes (TrueFi) on sizable lines of credit are being explored and implemented to some success.

Multi-Asset Lending Pools in Rari Capital’s Fuse

Rari Capital received increased interest of late due to its recent $15M smart contract exploit through an integration mistake with Alpha Finance. $15M of ETH was taken. In the wake of exploits we can make a judgement as investors as to the quality of response to turmoil. Those protocols which respond effectively to turmoil often gain increased trust and solidarity with their communities. Those who don’t respond effectively often do not recover from the stress put upon the team and protocol from lost trust. The jury is still out on Rari’s response.

Peak supply on Rari's Fuse capped in May at about $50M, falling to $26M amidst the exploit and subsequent market decline. Supply has since rebounded to $37M.

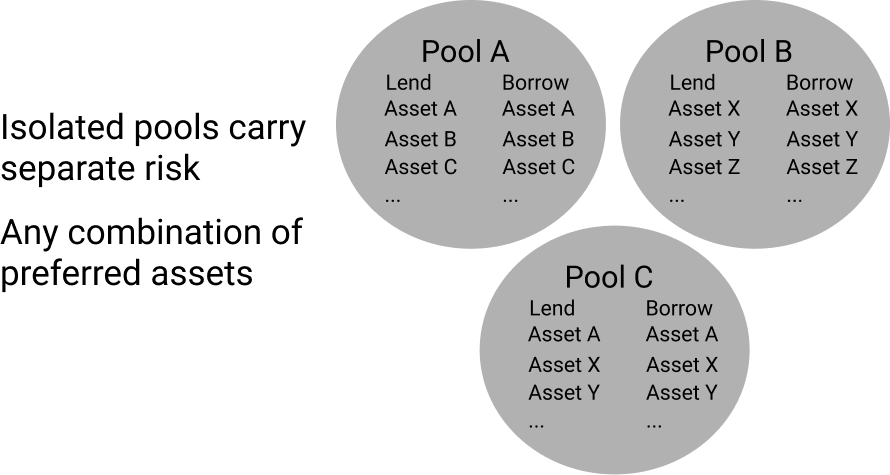

Despite the turmoil, Rari Capital has shown some resiliency thanks to its experimentation and pace of innovation. Their unique lending pools allow any combination of assets to be created. This creates a unique market structure unlike Aave and Compound where all collateral options are interfaced with all borrow options in isolated pools. In Fuse these individual pools are set up to isolate assets. This allows isolated risk and return, contrary to Aave/Compound where any added asset creates more or less risk for every lender/borrow in the platform. By isolating pools of assets, the assets in each pool share risk only within that pool, separate from the rest of the platform.

The nascent size and elevated risk of these markets enables increased yields for the prudent yield farmer. Interest rates act the same as in Aave/Compound where utilization curves govern interest rates. While lenders of size currently may not find this attractive, smaller farmers whose positions do not represent a sizable liquidity impact can enter and exit these markets profitably without impacting yields. And fortunately these entrants and exits only effect its individual pool.

It's not uncommon for niche assets to see high utilization in Fuse. Here are some sample rates from Rari Capital's largest Fuse pool (pool #3). Keep in mind the liquidity is usually extremely thin and bouncing around lending pools is usually not appropriate for lenders of size:

ALCX: 25% supply rate APY

USDC: 23% supply rate APY

DAI: 12% supply rate APY

Interest Free, Collateral Efficient Lending on Liquity

Liquity builds upon much of the innovation of MakerDAO, making unique and experimental changes. Similar to MakerDAO, Liquity manages issuance of a stablecoin backed by ETH and what they've dubbed "troves" that function similarly to Maker's CDP.

Some key changes from MakerDAO to Liquity:

- Governance token -> Zero Governance

- Varying collateral, dependence on USDC -> ETH-only collateral

- Interest controlled issuance -> Redemption controlled issuance

- MKR burns to inc value -> Single-sided LQTY staking to earn rewards

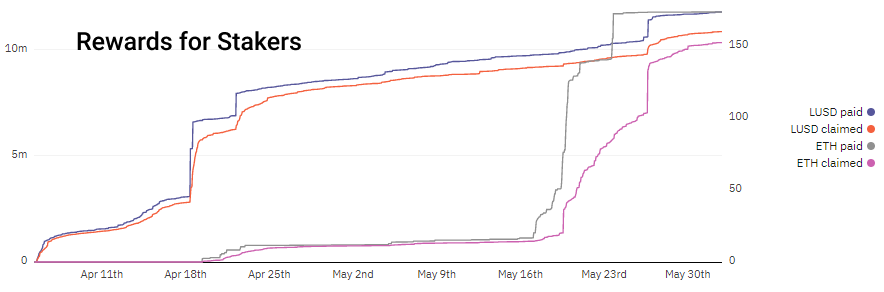

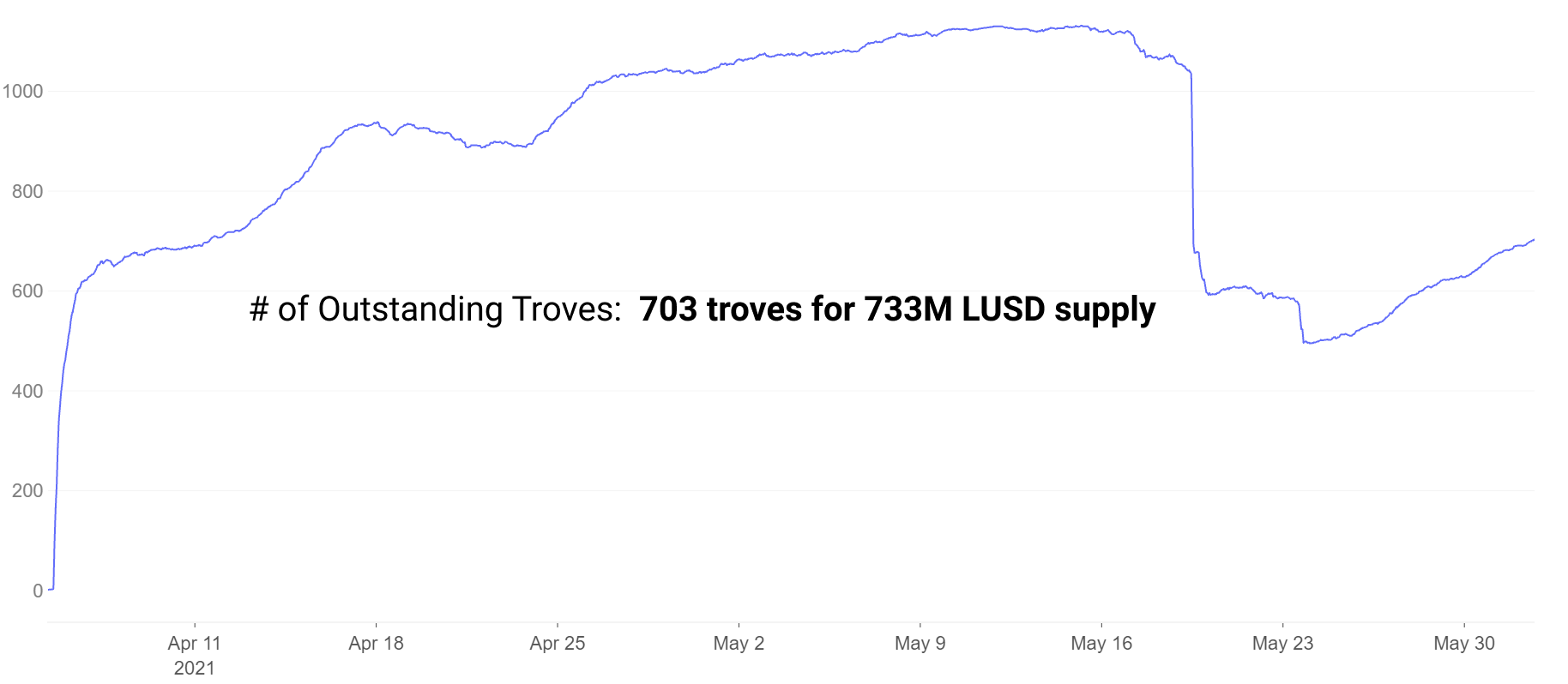

Liquity achieves interest free lending and stability by charging algorithmically priced one-time borrow and redemption fees and liquidating troves under 110% collateralization. In contrast, MakerDAO uses interest rates to encourage/discourage borrowers. By charging borrow and redemption fees on Liquity, lenders and stakers are incentivized by this potential profit and borrowers can calculate their fees up front without worrying about fluctuating interest rates. Notice how during times of increased deposits and repayments revenue goes up. LUSD is paid at time of borrow while ETH is paid during redemption.

Borrowers open troves that act similar to MakerDAO's CDPs. Trove numbers plummeted due to liquidation events in the recent market crash, however have since rebounded.

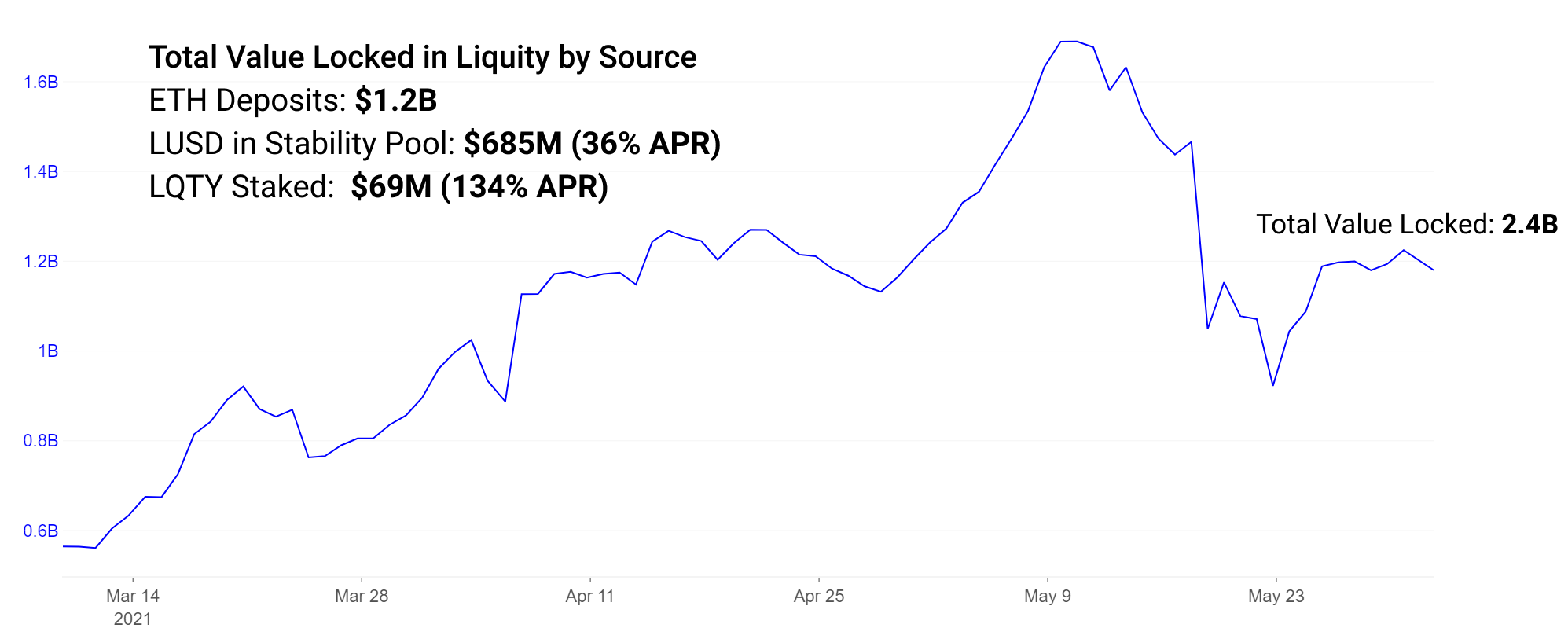

LUSD issued from troves at a minimum collateralization of 110% can be deposited to the stability pool, earning ~36% APR in LQTY token rewards. LQTY can earn up to 134% APR at present staking LQTY for rewards from redemptions.

Note that the LQTY staking reward rate of 134% APR is a highly variable 7-day rate. In periods of high redemption this reward can be very high, during other periods it can be much lower.

Appreciating Protocol Risks

We note that while elevated returns are attractive across all the protocols mentioned, increased risks are associated. Yield farmers holding newly minted governance tokens of failing projects can expect those high returns to become meaningless, while those projects with longevity are more likely to hold their value.

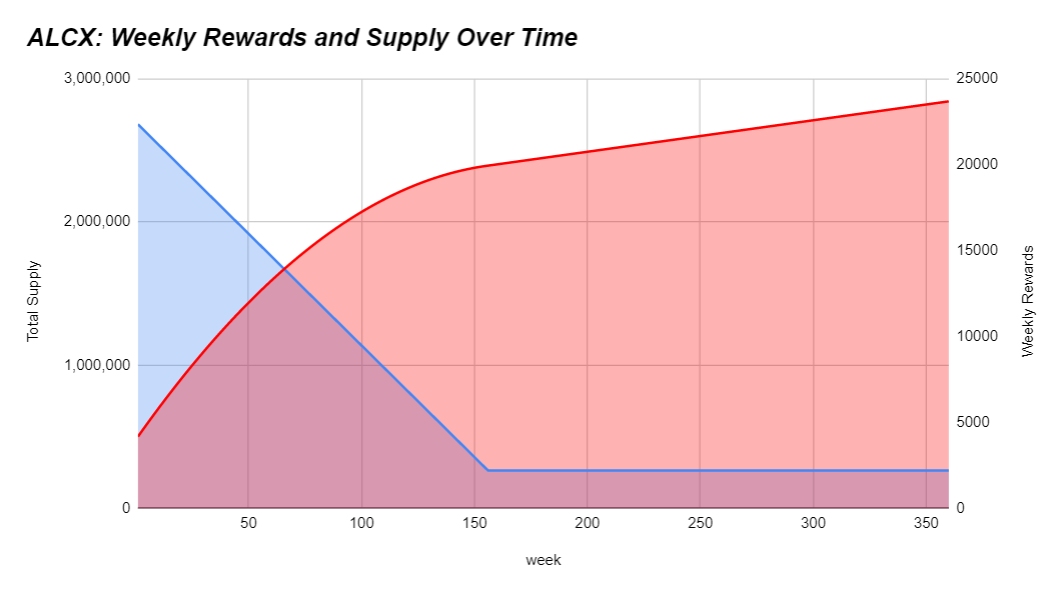

Additionally, as more tokens are minted, high inflation in token supply is prone to reducing price over time as more supply is in circulation. Farmers should do their best to understand if their returns are lagging, at pace, or outpacing token inflation. If rates seem too good to be true then one of two things are almost certainly true: a.) you are early and have truly found alpha or b.) there is heightened risk. As an example, here is the emission schedule of ALCX:

Emission schedules can vary widely project to project. At present the supply of ALCX inflates by about 43% monthly. If the holder has exposure to ALCX in their strategy their goal may be to outpace that inflation. If they believe in the long-term value of the governance token that may be less pressing to their strategy. Liquity's supply follows 32,000,000 * (1–0.5^year) annual inflation schedule. This means at present about 16M LQTY is emitted each year. This 12 month period will mark inflation of about 3.3x from current circulating supply. Rari's governance token plays less of a role in the ecosystem. It was emitted as 12.5% to the team and the rest to protocol users over a 60-day period. Emission schedules vary widely and it's worth understanding how any token you hold is being revalued over time.

Depending on your risk tolerance, your chosen strategy will fit in next to the inflation of the token. The ideal scenario is keeping risk at a minimum while outpacing inflation the best you can. Additionally, you hope a large enough number of buyers/holders see some value prop to holding the token. High inflation without sellers can create a strong market, high inflation with high turnover results in price charts with negative slopes. Token properties like protocol revenue and other value accrual mechanisms to the token holder incentivize token purchases and holding a farmed token for its utility past governance.

Understand that liquidity mining usually involves rewards in the form of governance tokens whose value is often tied to nothing. And even those tokens which reward holders with protocol revenues typically have slim revenue so slim rewards. Drawdowns in these tokens are usually severe and prolonged as farmers are quick to farm and sell their rewards. Purchasing these tokens purely for exposure without farming often carries significant dilution risk from token inflation. We see instances in DeFi where token inflation can exceed 100,000% annually. One should do their best to understand the inflation schedule and any other associated risks.

Concluding Remarks

New lending protocols continue to be released over the past year with varying levels of experimentation and innovation. They boast nascent markets with highly incentivized rewards, elevated risk, and plenty of room for pivoting with small user-bases and tight-knit, highly engaged communities. The larger a protocol and market size grows, the less malleable and easily changed it becomes. Some of the best returns often come from being actively involved in the communities of nascent projects and getting a pulse on the quality of both team and community.

Uncovering Alpha

This is our new weekly segment that briefly discusses some of the most important developments of the prior and upcoming week.

With token prices remaining volatile we get a glimpse at what projects have long-term resilience. Great builders often ignore short-term token prices and continue their commitment to development and community building in all conditions.

- Layer 2 season is nearly here.

Arbitrum released its developer beta this week, zkSync launched its testnet, and we’re expecting more news out of the Optimism team in July. Projects from Sushiswap to USDC and others have already announced they’ll be launching on Arbitrum soon. - Dev funding platform Gitcoin airdropped its governance token GTC and Ribbon Finance airdropped its governance token RBN.

As many have pointed out, any project in crypto without a clear source of revenue for the team and its investors is likely to launch a token eventually. - Alchemix is set to launch the first use-case of Sushiswap's new multi-incentive yield contract MasterChefV2.

Initially intended for Tuesday, the release has been pushed back 24-48 hours for logistical reasons. Stakers are set to receive both ALCX and SUSHI as rewards. This marks a new era for Sushiswap's famed Onsen rewards program. - alchemist launched mistX, a gasless trading platform.

mistX uses flashbots to remove the hassle of setting gas prices or using ETH to pay gas fees, instead subtracting the cost of bundling/bribes from the value of the trade, failed trades also pay nothing. - Pods released their options trading demo product on Polygon.

Options have struggled to gain traction in DeFi to date with expensive products, jurisdiction restrictions, and struggling liquidity. Pods is a highly anticipated options protocol which has been released as a demo with a $200k cap on TVL.

- Follow us and reach out on Twitter

- Join our Telegram channel

- For on–chain metrics and activity graphs, visit Glassnode Studio

- For automated alerts on core on–chain metrics and activity on exchanges, visit our Glassnode Alerts Twitter