DeFi Uncovered: Farming With Stablecoins

An overview of the stablecoin landscape and opportunities for turning idle stablecoins into productive yield-generating assets.

Stablecoins have seen explosive adoption over the last few years. Their broad use started with trading and transferring across centralized exchanges. They have since found their way into DeFi as a staple primitive in the ecosystem.

Most importantly, perhaps, is a shift for many crypto natives to holding stablecoins instead of their native currency when exiting risk. The rise of DeFi has enabled users to put these idle assets to work. Once dormant, unproductive assets are leaving centralized exchanges and bank accounts in favor of economic utility in lending, market making, and other types of DeFi protocols.

In this piece we will explore:

- State of stablecoins

- Yield opportunities

State of Stablecoins

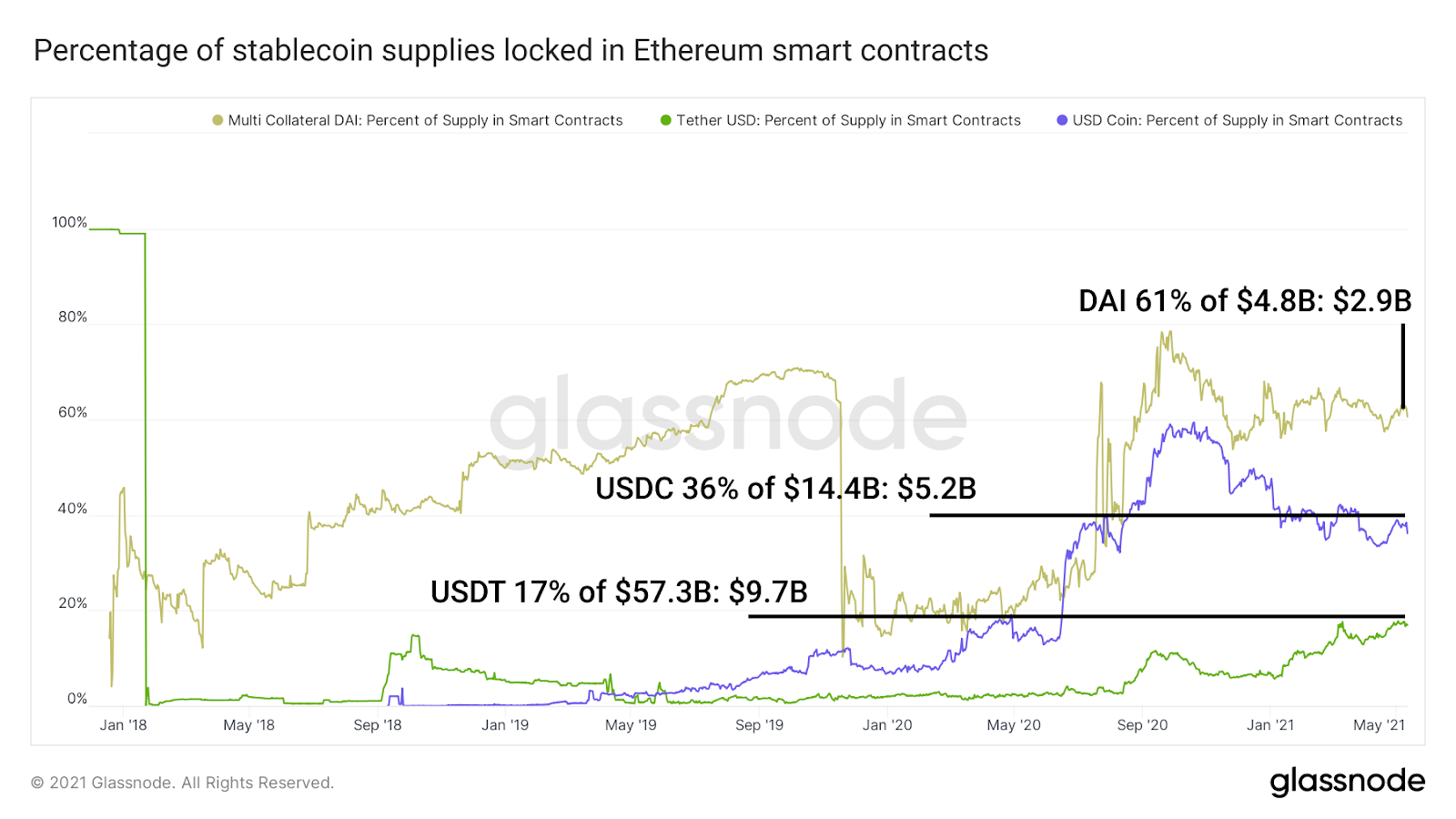

The current landscape of stables is dominated by a handful of players. USDC, USDT, and DAI dominate in circulating supply and use on Ethereum. USDC and USDT work using centralized collateral to maintain their dollar peg. For every 1 token issued of these stablecoins, 1 dollar backs the token.

DAI is the only major stable of this dominant group to manage its issuance in a decentralized fashion. It collateralizes DAI with on-chain assets.

All three of these stablecoins can be utilized in Ethereum DeFi. DAI is the leading major stablecoin by % of supply locked. 60%+ of the supply is locked in protocols for decentralized lending, exchanging, and other types of DeFi protocols.

Despite that high percentage, USDC and USDT still dominate in total value locked in smart contracts on Ethereum due to their larger circulating supplies.

Daily stablecoin transfers on Ethereum have exceeded $10B nearly every weekday for the past 3 months. This is the cumulative value of stablecoins being moved daily from one address to another. This includes deposits and withdrawals from smart contracts.

There are a number of demand drivers behind the growth of more than $75B in stablecoin supply, and greater than $20B in daily transfers.

- Flight to stability from volatility and risk exposure without using native currency

- Moving assets across centralized exchanges without holding risk

- Collateral for borrow and leverage

- Use in decentralized lending, exchanging, derivatives, etc. - using stables removes risk of exposure to volatile tokens, but is usually associated with lower returns because of lower risk

- Payments, salaries, forex, 3rd world access to non-hyperinflationary currencies, and other niche consumer use-cases

Pegged stablecoins dominate the space because of their ability to keep a strong peg to the US Dollar. Projects like EURS have done a solid job pegging to other currencies like the Euro. These historically successful pegs have given users faith in parking their assets in stablecoins instead of trading to native currencies like USD.

Pegged stablecoins exist along a spectrum of experimentation. Traders should diligence which stablecoin best aligns with their risk and objectives when considering allocation. Here are some additional stablecoins we did not mention.

Other centralized pegged stablecoins: HUSD, GUSD, EURS, TUSD,

Other decentralized pegged stablecoins: sUSD, FRAX, FEI, alUSD, RSV, PAX, UST, mUSD, LUSD, ESD, AMPL

Stablecoin Yield Opportunities in DeFi

Note: yields are extremely variable, yields listed at time of writing are prone to high volatility by the time you read this.

During user flight to stables, it is important to understand how and why to allocate to yield generating opportunities. Unproductive assets have a cost. While sitting idle, stable currencies often suffer from effects of inflation and fees. To counter these effects, investors can choose to put their idle assets to work, providing a service or taking on risk in exchange for yield.

In DeFi, these yields are currently quite high relative to their traditional counterparts. Various risks are priced in to these increased yields, such as:

- Potential permanent loss of 1:1 peg

- Risk of smart contract exploits (including economic/protocol design exploits)

- Volatility of yield: APRs can rapidly change from time of deposit

- Illiquidity: high volatility of rewarded tokens, inability to borrow from highly utilized pools, inability to withdraw a large position from a highly utilized pool, high slippage exiting positions

- Gas fees: high gas fees create friction and limit behavior of liquidity providers and users

Quantifying Returns

APR and APY are broadly used metrics for measuring returns in DeFi. Unfortunately, they are often misunderstood by users and unclearly labeled by developers. APR represents the returns of a pool without compounding your returns. APY assumes compounding rewards. If APR is listed in a project's UI it means your returns are not automatically compounding. If a pool has a "claim rewards" function the return is an APR.

With daily compounding, 40% APR becomes 49% APY. 400% APR becomes 5,242% APY with daily compounding. This is the power of compounding, and it can be especially prevalent in high rate environments like DeFi. Of course, small positions in Ethereum DeFi cannot benefit from this compounding because the gas fees to claim rewards and restake daily would exceed the returns. The following chart showcases a hypothetical investment of $1,000,000 growing at an APR of 50% and the possible boost from claiming rewards daily to compound.

With that in mind, here are 5 strategies of varying risk and return that center around stablecoins. Note that single-sided liquidity provision has reduced returns because the returns have limited underlying volatility.

An arbitrary risk rating is assigned to each. This rating takes into account the credibility of the project, inherent protocol risks, audits, and other factors. Risk is rated relative to the rest of DeFi, not independently. An A+ rating in this space still comes with plenty of risks.

Lending in Aave and Compound (4-16% APY, Risk: A)

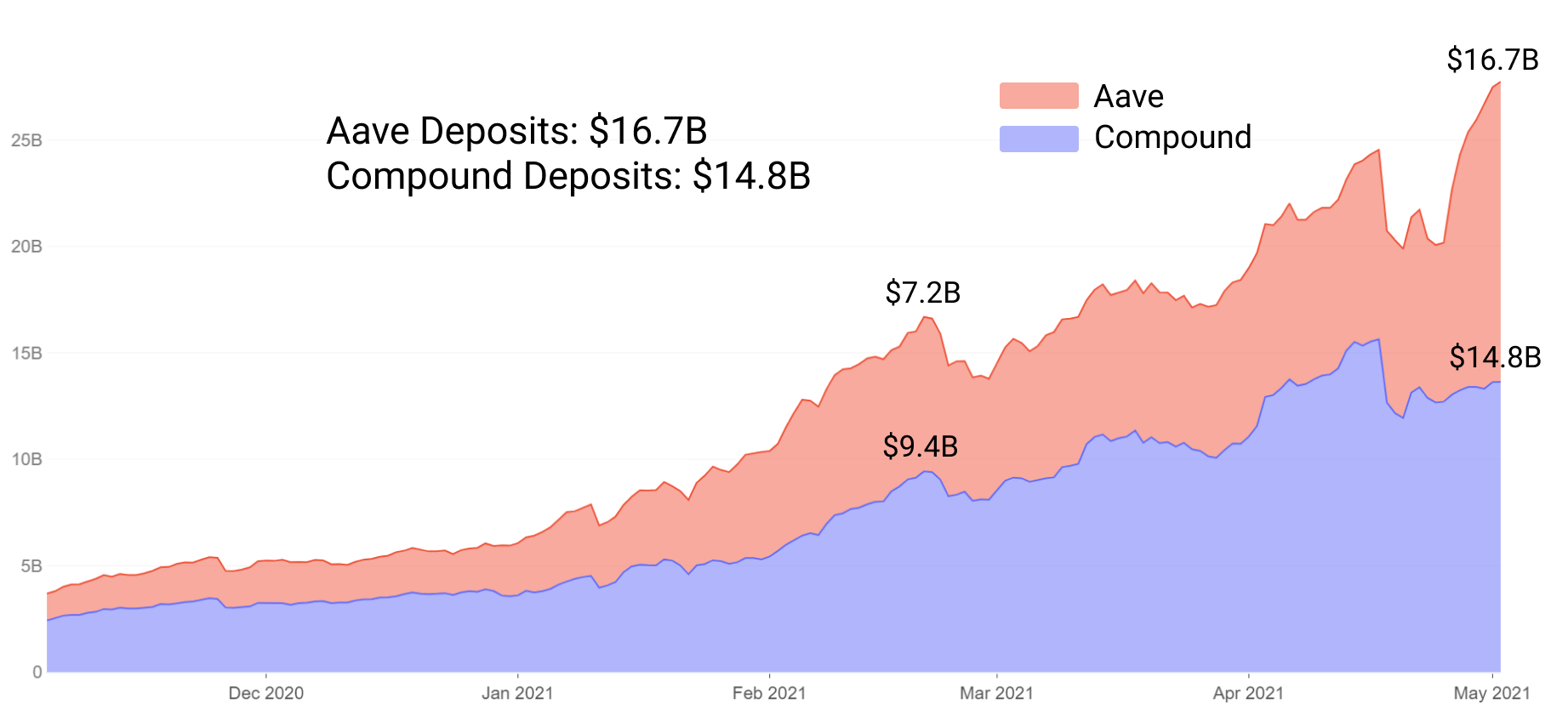

Aave and Compound are the largest lending protocols in DeFi. Until recently, Compound had held its dominance as the largest lending protocol in terms of total deposits. Aave has flipped this with its new liquidity incentives, taking the liquidity lead in lending.

These new Aave incentives provide an attractive opportunity for increased yield. The Aave incentives are scheduled to last until mid July. They present an opportunity for increased rewards in the form of the Aave governance token - the liquidity incentives are 2,200 stkAAVE per day until July. The stkAAVE is distributed proportionally among pools according to borrow activity.

For example, Aave currently has $5B outstanding borrow. The DAI pool has about $1B of borrow. $1B/$5B = .2 or 20%. 20% of the 2,200 stkAave/day rewards means the DAI pool currently receives 440 stkAave per day. Currently this means for every $1,000 deposited a user receives .0002 Aave/day (11c/day at current prices). This reward structure outpaces Compound's liquidity mining rewards on some stables, underperforms on others depending on utilization.

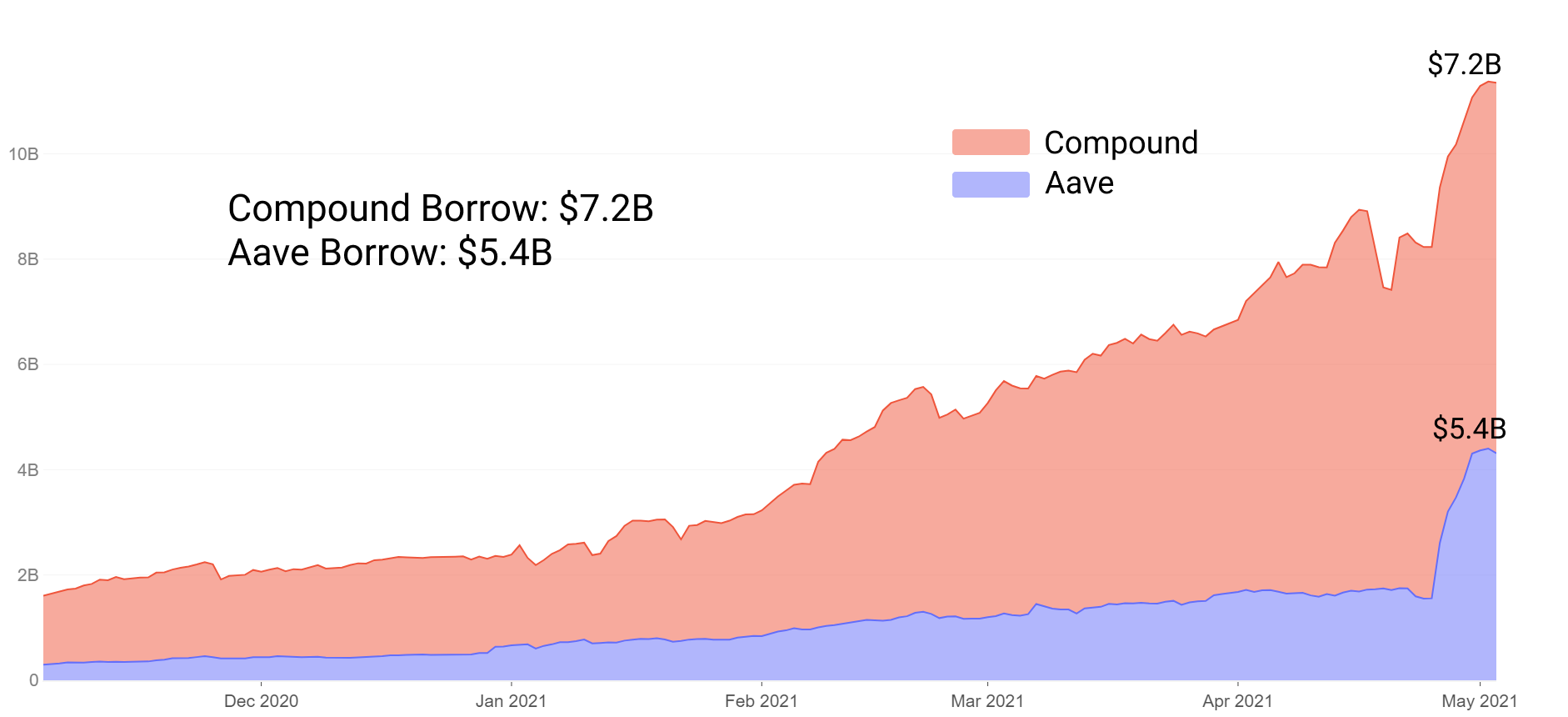

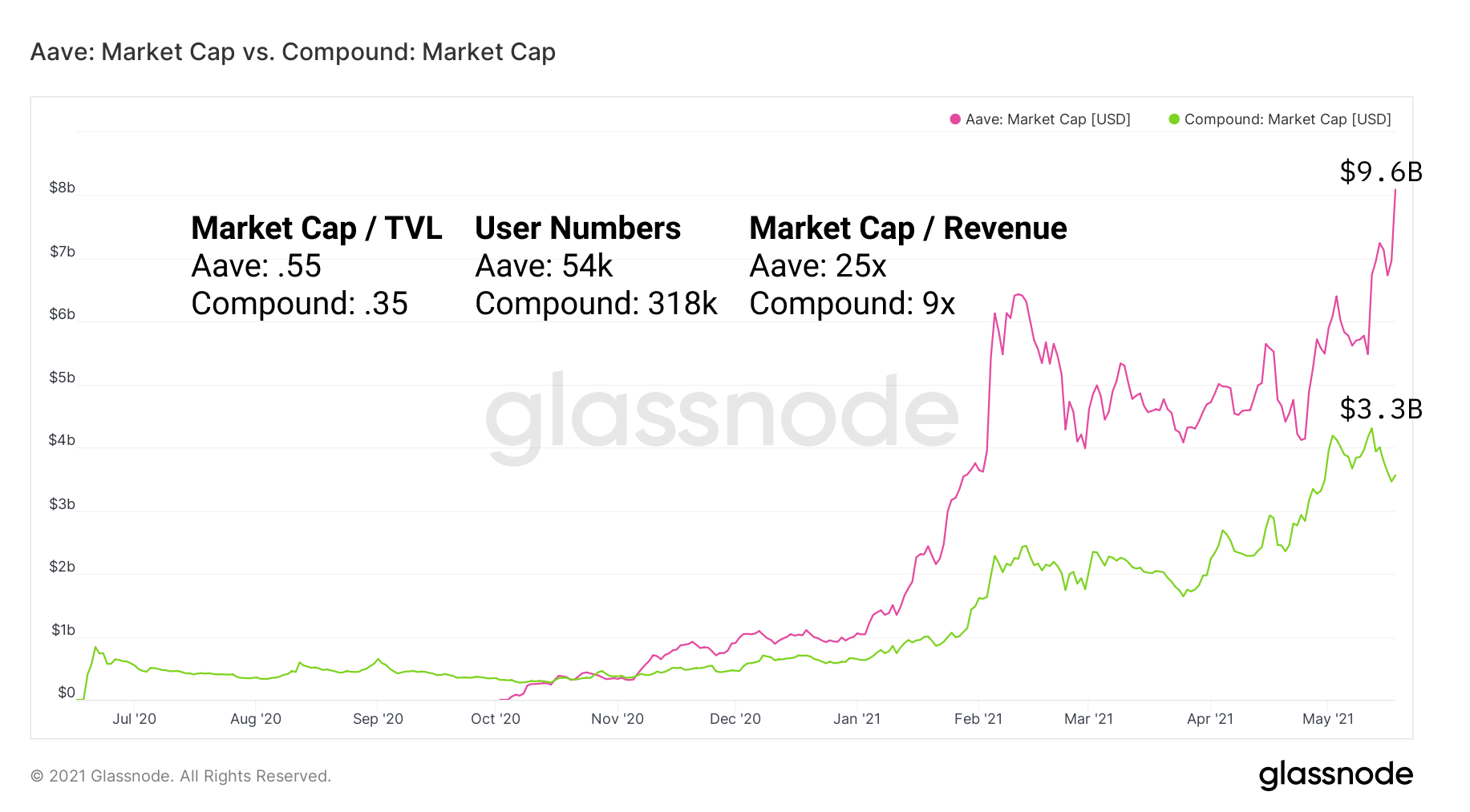

Despite Compound historically having the more mature market by size and utilization, Aave has historically commanded a higher market cap for its superior tokenomics, incentives, and experimental features like stable rates and support for more tokens as collateral. Note that while Aave has surpassed Compound by total collateral, total borrow remains well dominated by Compound.

With lower interest rates and larger market size, Compound remains a strong market for lenders of size who want stronger liquidity guarantees and low interest on their borrow. Aave, conversely, often offers better returns on higher risk, and incentives on both the supply and demand side of their lending markets. They additionally announced recently a pro version for institutions.

It will be fascinating to see how liquidity behaves when incentives run out in July.

Market Cap / TVL is commonly used as a metric to measure the valuation relative to how much liquidity the project has attracted. A higher Market Cap / TVL can be interpreted similarly to a high P/E ratio in traditional markets, where the higher the ratio the higher the valuation of the token per dollar of liquidity. User numbers and Market Cap / Revenue tell a similar story in the Aave valuation story.

The DAI lending market on Aave currently sits at an 11% interest rate for lenders. This means a lender can expect to receive 11% continuously compounding at current rates. Interest rates have been relatively volatile in this pool since Aave liquidity incentives were introduced in late April.

The bottom line in this chart represents the interest rate for lenders while the top line represents rates for borrowers.

Aave’s incentives mean an additional ~3-6% yield is typically rewarded as staked Aave tokens. These staked Aave tokens can be unstaked on a 10 day cooldown, or they can be left staked, yielding 7%.

Users can take on additional risk and potential returns by borrowing against their collateral, recursively lending to add leverage, or sending their borrow to other protocols. Those details are outside the scope of this simple strategy.

Strategy returns: Lent DAI in Aave (4-15%), Aave liquidity incentives (4%), Staked Aave (7%)

Risk: Smart contract exploits, DAI losing peg, Aave liquidity risk, gas fees exceeding returns of small positions (deposit collateral, unstake rewards, withdraw collateral)

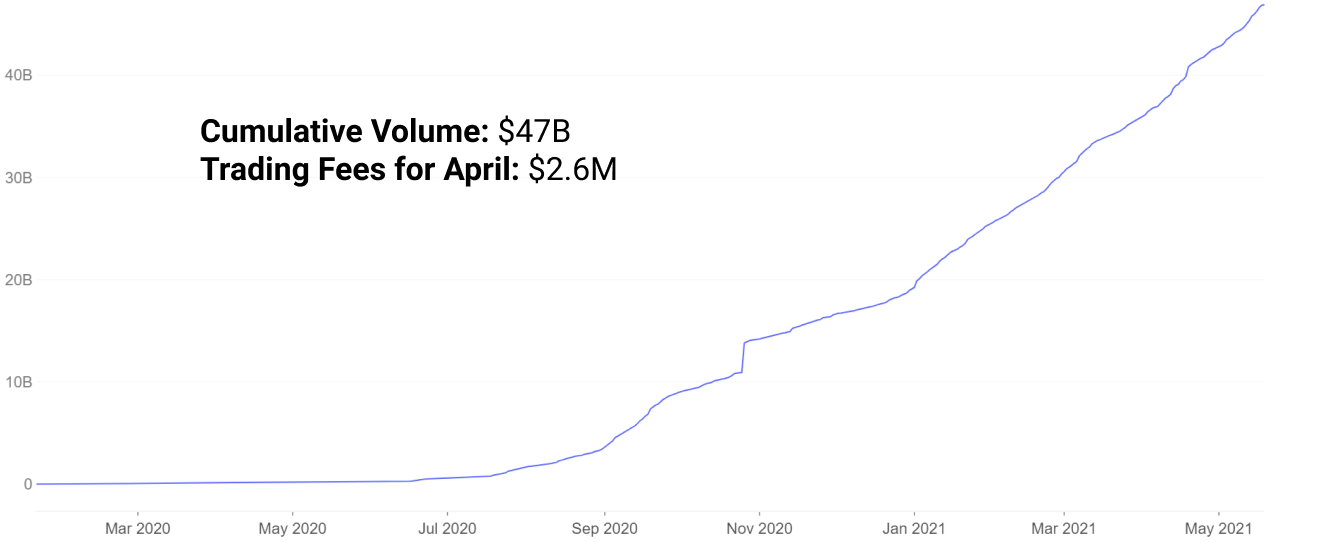

AMM Pooling and Staking in Curve (10-50% APR, Risk: B+)

As the primary venue for stablecoin DEX liquidity in DeFi, it is no surprise there are liquidity incentives in play. Curve boasts the lowest slippage trades for stablecoins, commanding the clear majority of stablecoin to stablecoin swaps until very recent history; Uniswap V3's stable pairs are gunning for Curve volume, but for now its nascent markets are busy playing catch up on price impact, especially in size.

Base APY for supplying to the protocol's largest pool (USDC+USDT+DAI) is 2% from trading fees. Volume continues to healthily push towards $50B.

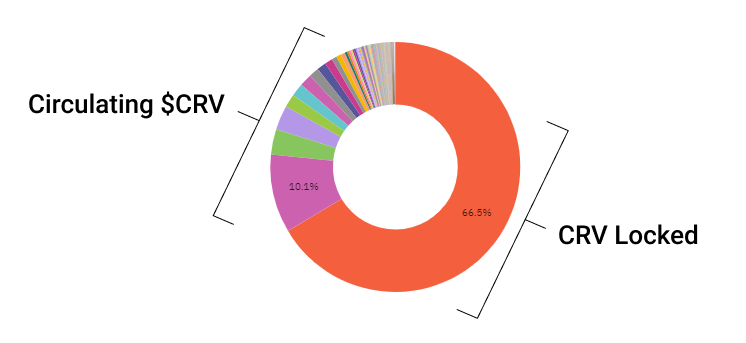

An additional incentive of 8% is layered on top of this 2% as rewards in the governance token CRV. Users can boost this 8% up to 20% by locking CRV for a determined period of time. The max reward boost is 2.5x for locking CRV for 4 years. Notice that 20% is 2.5*8 to arrive at the max reward of 20%.

Strategy returns: 3pool Base APR 2%, Rewards 8-20%, Locked CRV 11%

Risk: Smart contract exploits, DAI losing peg, gas fees exceeding returns

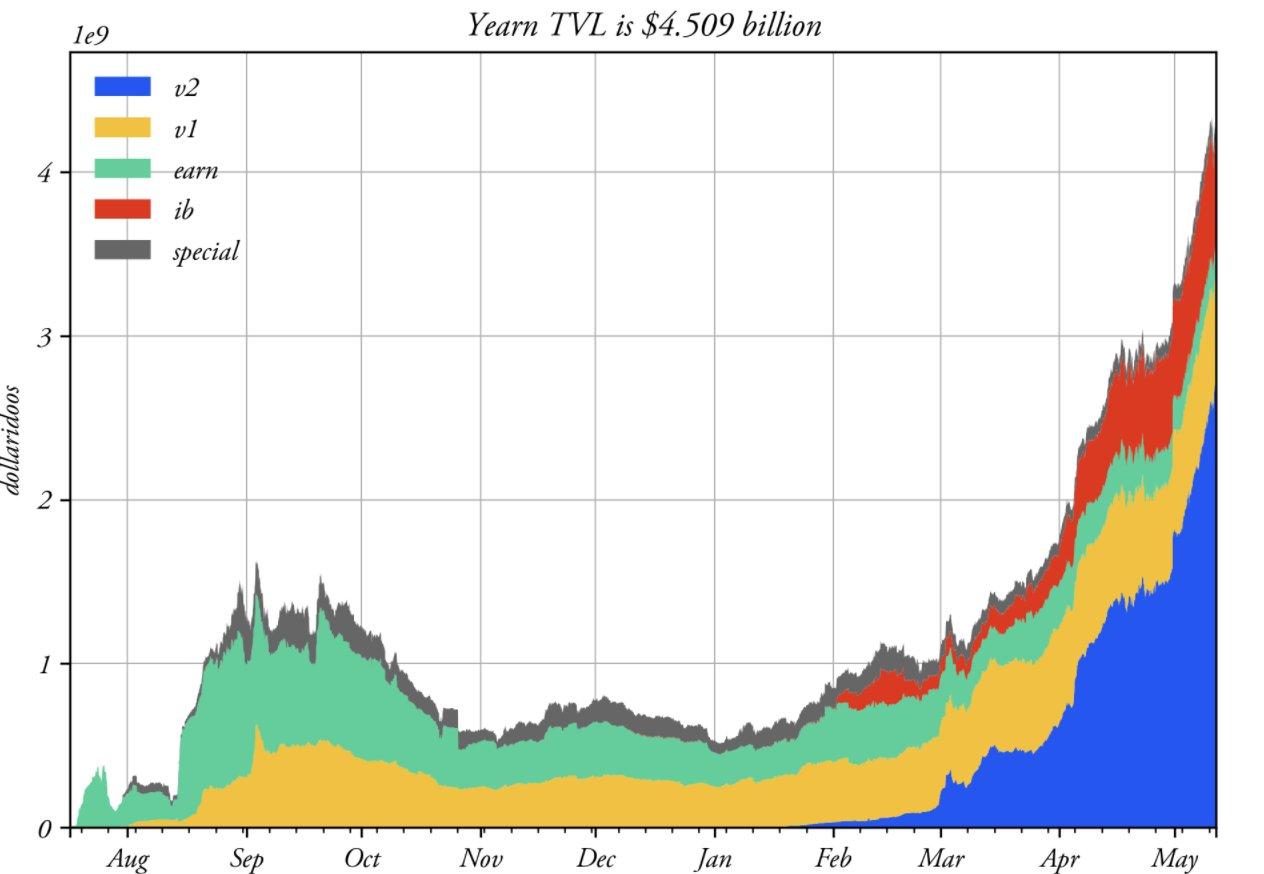

Yearn Finance DAI Vault (15% APY, Risk: B)

The yvDAI vault is currently the largest vault on Yearn Finance. It commands a healthy $700M+ of assets at a current APY of 15%.

These assets are put to work in the DAI strategy created by the Yearn developers. It works by depositing users’ DAI into various yield opportunities, moving users’ assets around to maximize yield within the strategies the developers have deemed appropriate.

Sample strategies allocated from the yvDAI vault:

- StrategyLenderYieldOptimiser: optimizes lent DAI between dYdX and Cream.

- SingleSidedCrvDAI: deposits DAI to highest yield pools in Curve.

- StrategyIdleDAIYield: deposits DAI to idle.finance farming COMP and IDLE governance tokens. The rewards are sold for DAI and reallocated to the vault.

The Yearn vaults have flown past $4.5B locked, being a popular place to park assets in DeFi for a healthy yield with low perceived risk relative to much of the space.

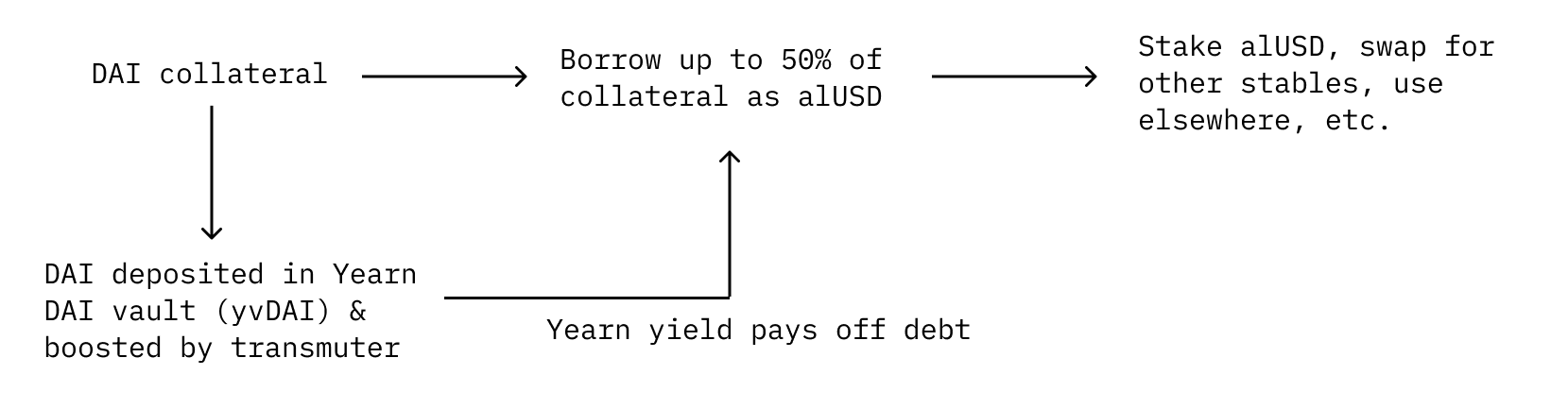

A large percentage of the Yearn yvDAI vault is deposits from Alchemix. The Alchemix protocol currently accounts for over $400M of value locked in the vault. Alchemix implements Yearn as a core piece of infrastructure for their protocol. Individual depositors in the yvDAI vault are investing their DAI alongside Alchemix, other projects, and other individual investors in the vault. In the case of Alchemix, returns from the Yearn vault are used to pay off Alchemix loans.

This diagram expresses how Alchemix integrates Yearn to offer a unique use-case.

The core returns of the Yearn vault have been historically quite good for being a single sided stablecoin deposit, at almost always >10% over the last few months.

Strategy returns: yvDAI Vault (15% APY), 2% management fee, 20% performance fee

Risk: Smart contract exploits in Yearn or projects they send funds to yield farm in, DAI losing peg

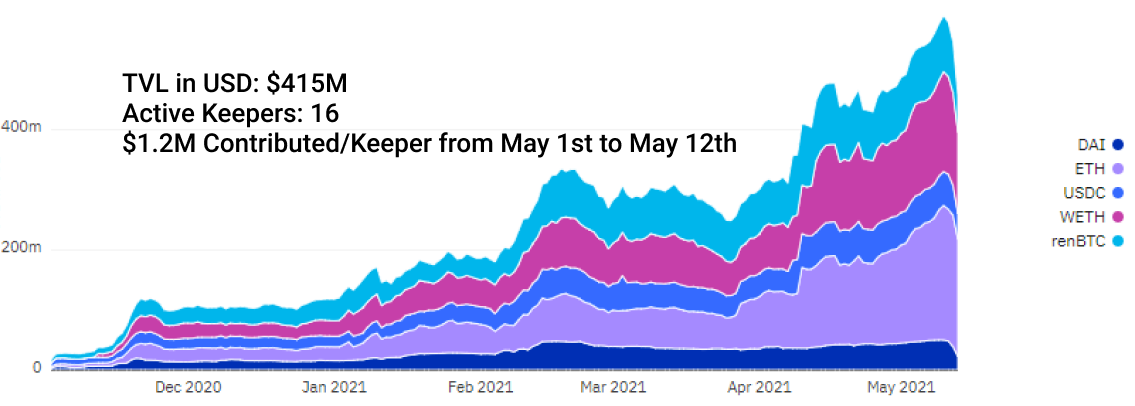

KeeperDAO Arbitrage (10-x% APY, Risk: B-)

KeeperDAO uses pooled assets to take advantage of opportunities for arbitrage, liquidation, and other activities. Many are playing the recent attention to Miner Extractable Value (MEV) through KeeperDAO and ROOK, the DAO's governance token.

Keepers borrow assets from the pools to perform these liquidations and arbitrage activities, generating returns for themselves and the depositors in the pool.

The following statistics are for v2 of KeeperDAO. V3 has recently shipped, causing these analytics to be out of date as well as the drop off in V2 liquidity.

These funds being borrowed are considered secured because they are borrowed, utilized, and returned to the pool in the same block using flash loans. This is a unique innovation of blockchain based smart contract systems whereby money can be borrowed without collateral because of the guarantee it will be returned in the same block. If the transaction does not guarantee this, the transaction will fail.

This chart represents the cumulative value of flash loans borrowed by Keepers from KeeperDAO liquidity providers.

Additionally, a percentage of pooled assets are given to yielders who create strategies to yield farm across the ecosystem. This is to take advantage of unproductive assets that are being underutilized by Keepers. The strategy allocation is determined by the KeeperDAO.

Returns in governance token ROOK are determined by the emission schedule. Base fees in deposited currency will change as Keepers perform more or less actions for the DAO.

Strategy returns: 15% APY in governance token ROOK, x% in base fees

Risk: Smart contract exploits, DAI losing peg, dependent on Yearn yield

Concluding Remarks

Stablecoin growth has been parabolic in recent history. With the advent of DeFi, stablecoin holders can now get access to attractive yields for their once idle assets.

Stablecoins have reached:

- $75B+ in circulating supply with consistently over $10B in daily transfers

- $15B+ deposited in Compound and Aave, $12B+ borrowed (>75% utilization)

- Healthy stable pairs in most major DEXs

- Non-pegged experiments finding success

- Yield available for almost all appetites of risk

Users will always seek stable assets when exiting risk. The question is how far will DeFi push users towards putting billions of dollars of once unproductive assets to productive use?

- Follow us and reach out on Twitter

- Join our Telegram channel

- For on–chain metrics and activity graphs, visit Glassnode Studio

- For automated alerts on core on–chain metrics and activity on exchanges, visit our Glassnode Alerts Twitter