DeFi Uncovered: The State of DeFi

An analysis of key metrics that describe the adoption, stickiness, and explosive growth of the DeFi ecosystem.

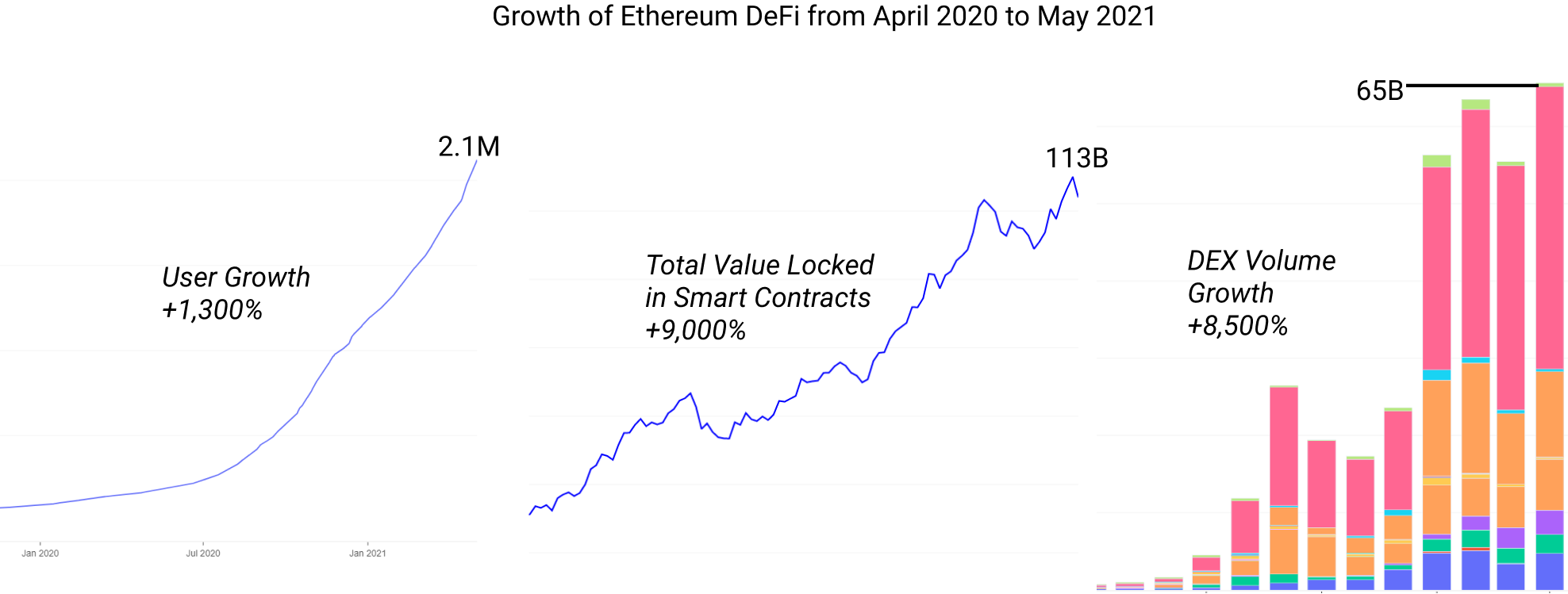

In 8 short months DeFi has attracted in excess of $100B into smart contracts. These contracts express both traditional financial schemes and entirely new financial primitives. These innovations afford the individual new opportunities to truly own their assets, participate in global coordination of capital, trade via decentralized exchanges, utilize lending and borrowing markets, and much more.

In this piece we will explore the current state of DeFi built on Ethereum, and study the key metrics that help us appreciate its explosive growth and usability.

The Grassroots Evolution of DeFi

DeFi is both a technology, and a movement, where teams of researchers and engineers have banded together to re-imagine financial services. The space has come a long way since the early days of smart contract innovation like raising capital through ICOs, early NFT experiments like CryptoKitties, and initial DEX implementations that first hinted of a decentralized future for finance.

The charts above showcase explosive growth in both user-base and value in the DeFi ecosystem. What we see is a perfect storm of innovation and a new ethos behind the alignment of financial incentives. Whole communities have been bootstrapped via incentivized participation in DeFi protocols. Incentives that drove users towards products that have effectively grown and retained both users and capital.

One of the first DeFi experiments in liquidity mining was by Synthetix in 2019 which incentivized bootstrapping the sETH/ETH Uniswap pool. This later inspired a wave of yield farming projects in 2020, most notably after Compound Finance enabled liquidity mining of COMP tokens in their borrowing and lending markets.

The launch of COMP incentives for lenders and borrowers to earn COMP popularized the protocol - total value in the protocol jumped in one week from $100M to $500M.

The key innovation here is actually a social one, in that participants are rewarded the protocol’s governance token for providing liquidity and using the protocol, and thus attracting users and liquidity became the name of the game for DeFi protocols.

Measuring DeFi Adoption

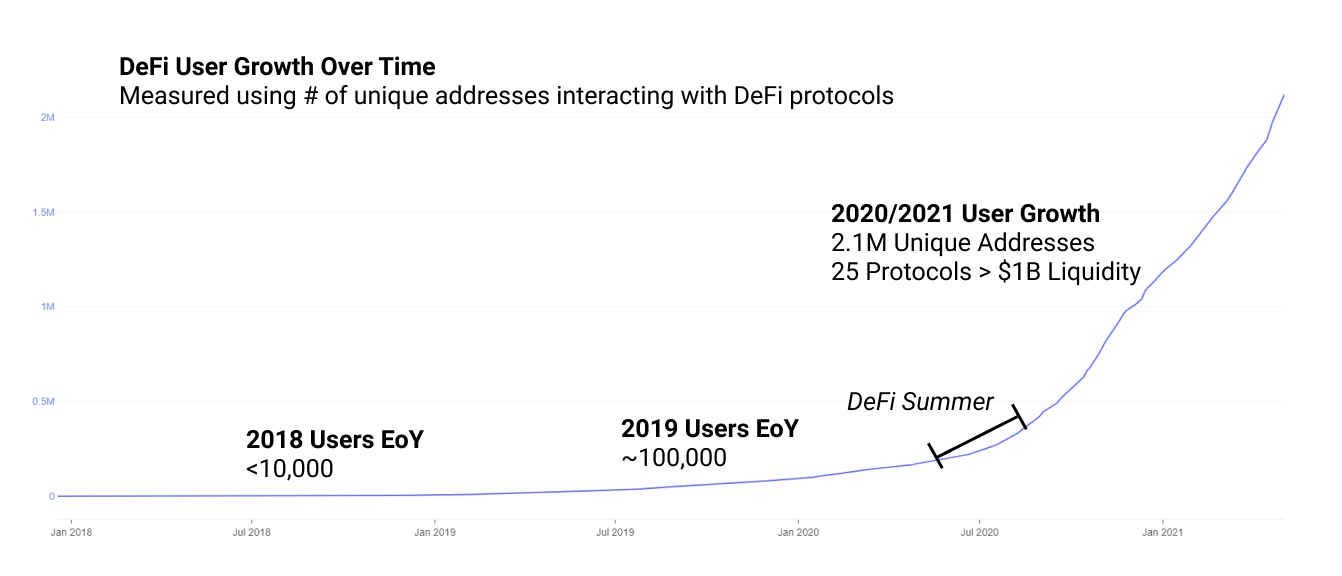

The growth of DeFi can be expressed in a number of ways, the most intuitive being measuring active users. User growth since the early days of DeFi experiments has been explosive, exceeding 2.1M unique addresses that have interacted with Ethereum DeFi in some way since early 2018.

If we believe every Ethereum address is part of the total addressable market (TAM), then we can say that DeFi has so far penetrated less than 3% of Ethereum addresses that have a non-zero balance (~58M addresses). As Ethereum adoption grows, so too does the potential TAM for DeFi applications.

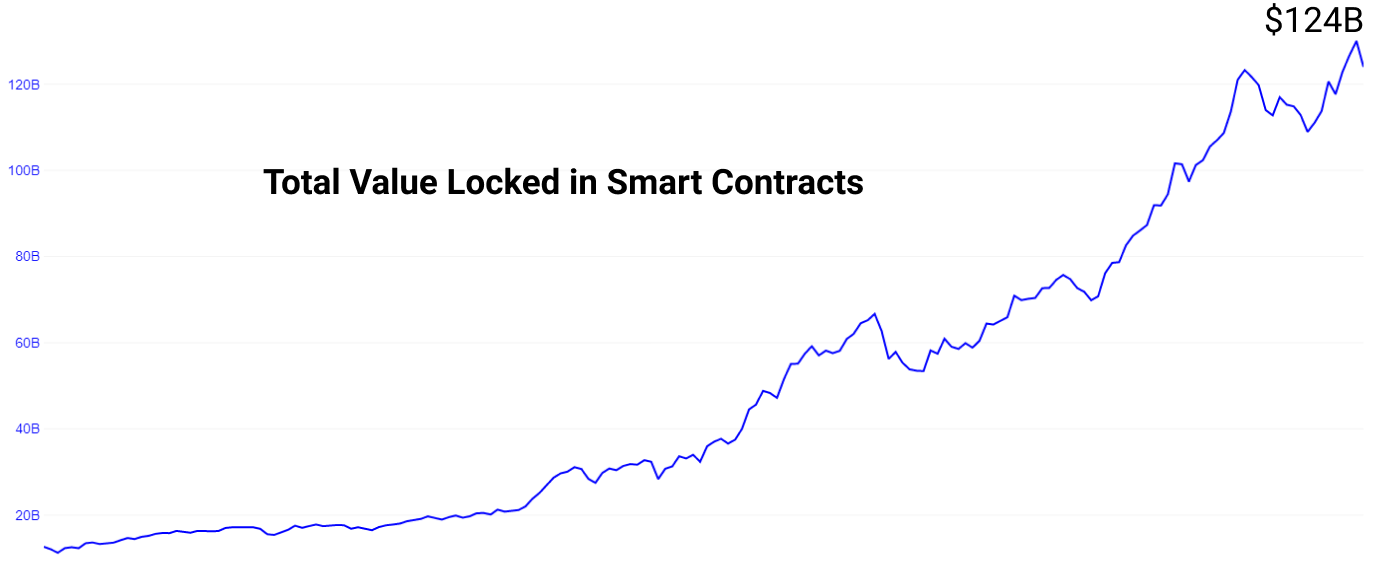

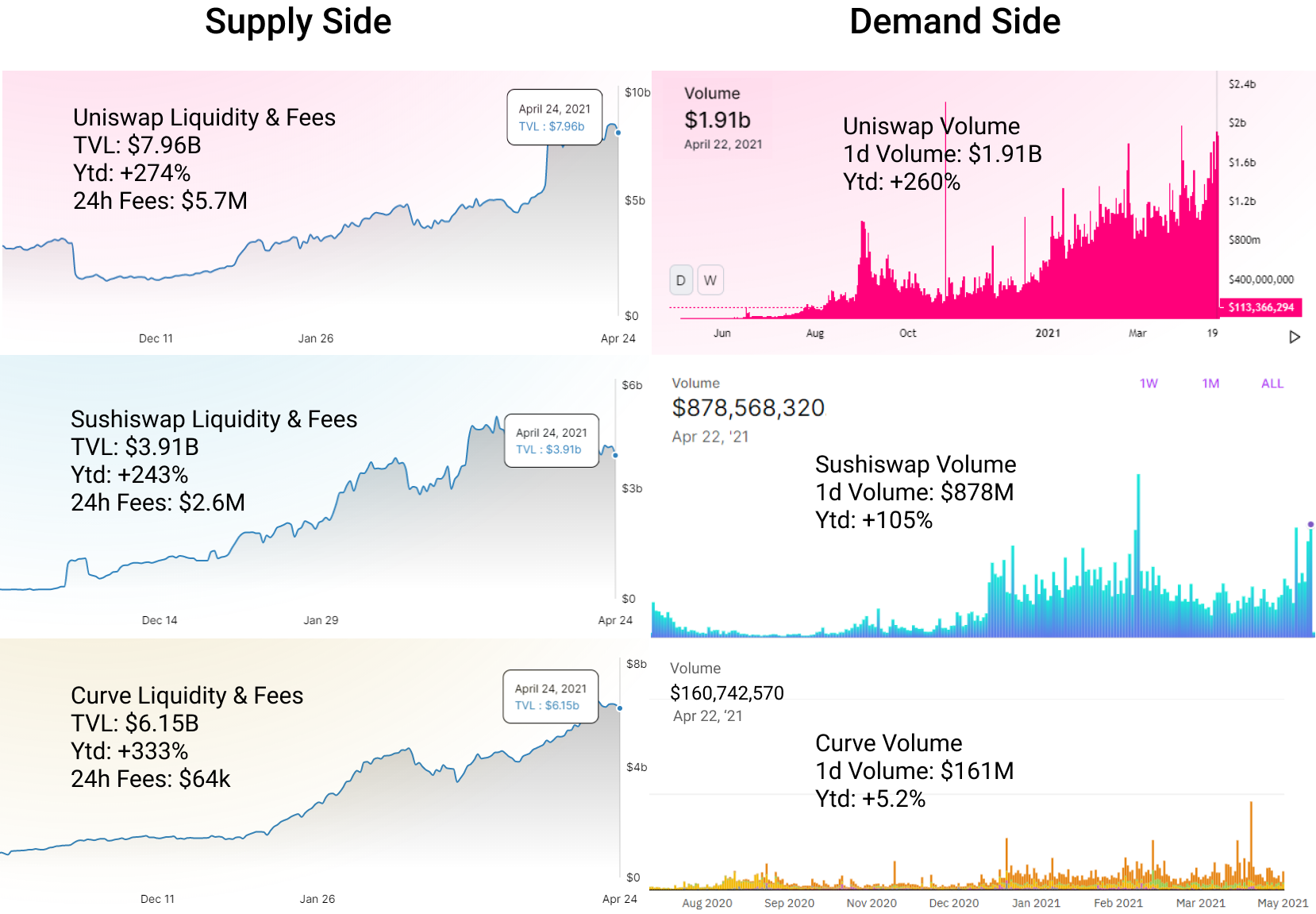

A metric called Total Value Locked (TVL) has been popularized to describe the total assets deployed in smart contracts. Locked, deposited, stored, sent, lent, provided, all meaning the same thing in the context of TVL. In exchanges we can think of these assets directly as liquidity and in lending protocols as collateral.

Relevance of TVL differs protocol to protocol, and it should always be considered alongside utilization, trading volume, and other usage metrics. Utilization describes how much of the supply side liquidity is being used productively by the demand side of a protocol. Take the classical econ example of a lemonade stand:

- Let’s say I produce 100 cups of lemonade every day. That’s 100 cups on the supply side that the demand side can utilize.

- Now let’s assume an average 70 of those cups are bought and consumed each day by the demand side. That’s 100-70=30 cups of lemonade going unused. We can assume that as the supply side I might start making less cups each day to more closely meet demand.

- But wait. What if the local government comes in and says they will subsidize my lemonade stand by buying those extra 30 cups each day irrespective of usage (this is the rough equivalent to liquidity mining rewards offered by the protocol)? We now have an argument for a rational lemonade producer to continue to supply 100 cups.

So while $124B in TVL may be sloshing around the system, this is a nascent market where that capital will flow to wherever it expects the best risk/return. If users are scarce but liquidity incentives are strong, rational actors will flow to those opportunities. In order to establish whether these protocols are developing a loyal user-base however, we must dig deeper into metrics that describe a stickiness for both end users and liquidity providers.

Adoption by DeFi Protocol Type

Borrow and Lending Markets

Lending protocols have exploded in interest as users are attracted by:

- earning interest on their tokens

- getting access to leverage and the ability to short on-chain

- accessing liquidity for other tokens without needing to sell their current holdings

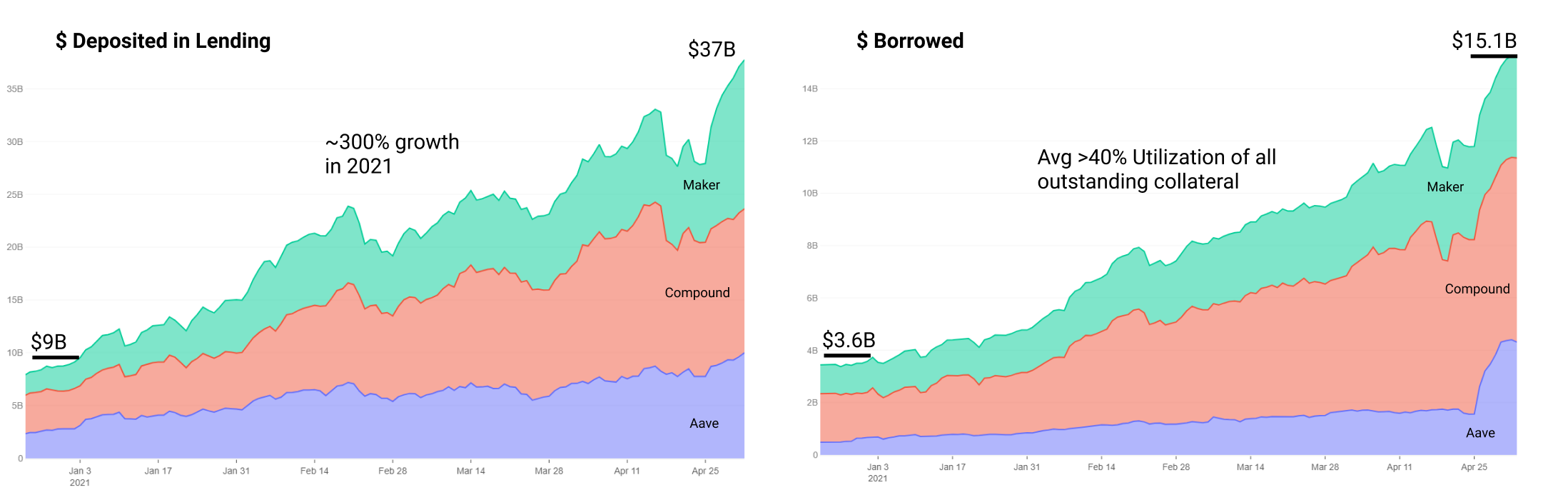

Maker introduced the first DeFi lending market, allowing users to generate DAI against deposits of ETH, with additional types of collateral being made available over time.

Compound popularized broader asset lending and borrowing, offering a larger array of tokens to lend/borrow. When lending positions are put on the lender receives cTokens that represent their deposit. These cTokens can be used as a primitive for other protocols.

Aave started competing with Compound by offering varying tokenomics, up to 75% borrow against a user’s collateral, and an even larger selection of tokens to lend/borrow.

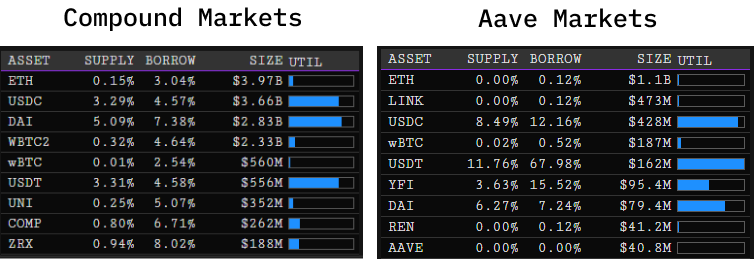

Within each protocol we have individual money markets with varying interest rates and utilization with examples for Compound and Aave shown below. Utilization = 1 - (free liquidity / market size). If there is $1B deposited and $100M borrowed then utilization would be ~10%.

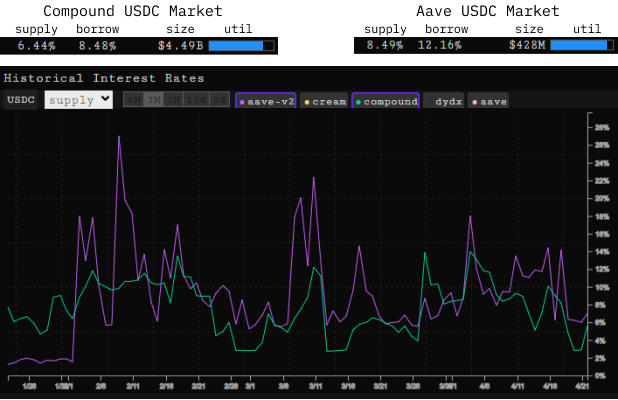

Rates change in these markets against utilization curves. As utilization of a total market increases, so too do interest rates to encourage more lenders to enter the market and borrowers to exit. In reverse, as utilization decreases, so too do interest rates to encourage more borrowers to enter. In the following chart we note how current utilization has affected the interest rates of the DAI market on Compound Finance.

You can see that markets with higher utilization reward lenders with higher yield to attract more liquidity. It also becomes more expensive for borrowers.

These markets have steadily grown since their inception, with stablecoin markets boasting the most activity and utilization. We see in the following chart that stablecoins command a healthy balance of borrowing and lending, with average utilization rates in excess of 75% in most cases. Volatile assets like ETH and wBTC are commonly collateral rich but borrower poor.

Arbitrageurs will move their deposits and borrowed capital wherever superior rates/risk and returns can be found. A risk premium exists for participating in lower liquidity markets. Rates tend to smooth out and normalize, as shown in USDC interest rates between Compound and Aave over time. New liquidity mining programs and other governance impacts can introduce new rate volatility.

Liquidity incentives and lenders drawn to attractive yields bootstrapped liquidity, while borrower adoption followed. This sustained liquidity and utilization have led to attractive rates and sustained adoption for both borrowers and lenders.

Decentralized Exchanges (DEXs)

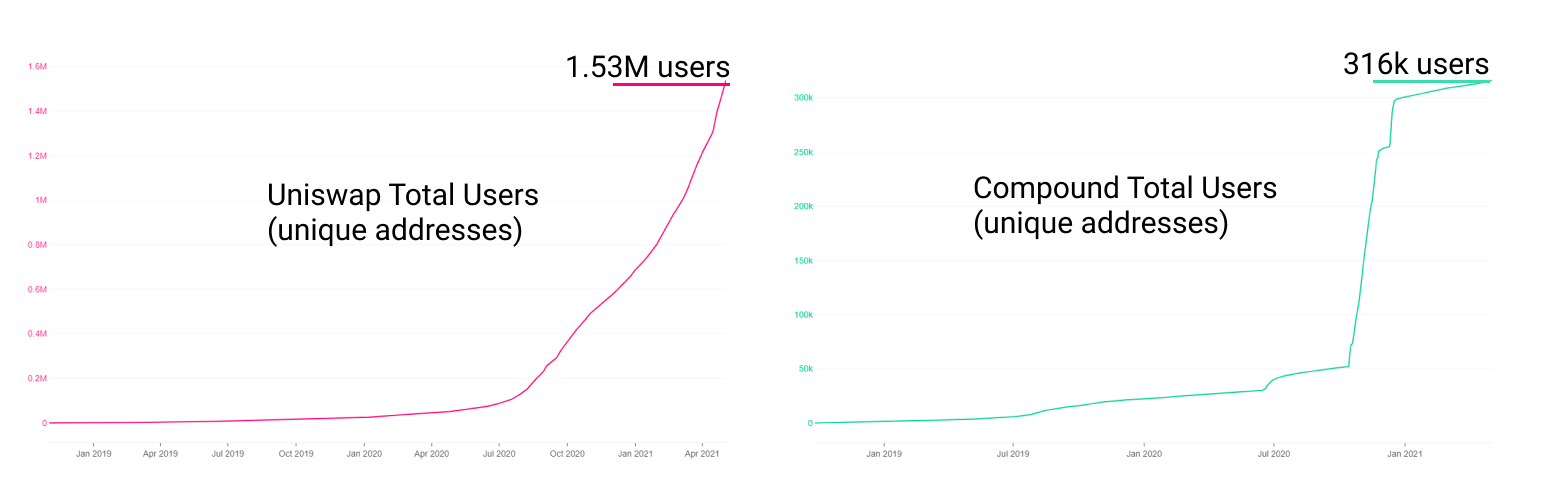

DEXs have exploded in use over the last year. While lending commands the most liquidity, DEXs command the most users by a large margin. Of the total 2.1M users who have interacted with DeFi, 1.53M of them have used Uniswap (~73%) at some point in time. Compare this with 316k users who have interacted with Compound at some point in time (~15%).

Liquidity providers deploy capital to earn a share of trading fees and liquidity rewards. The users are attracted to the platform by market depth and availability of their tokens of interest. A positive feedback loop is created where more users create more fees and more fees attract more liquidity. Sufficiently high users and revenue from fees keeps liquidity in the protocol when liquidity rewards expire.

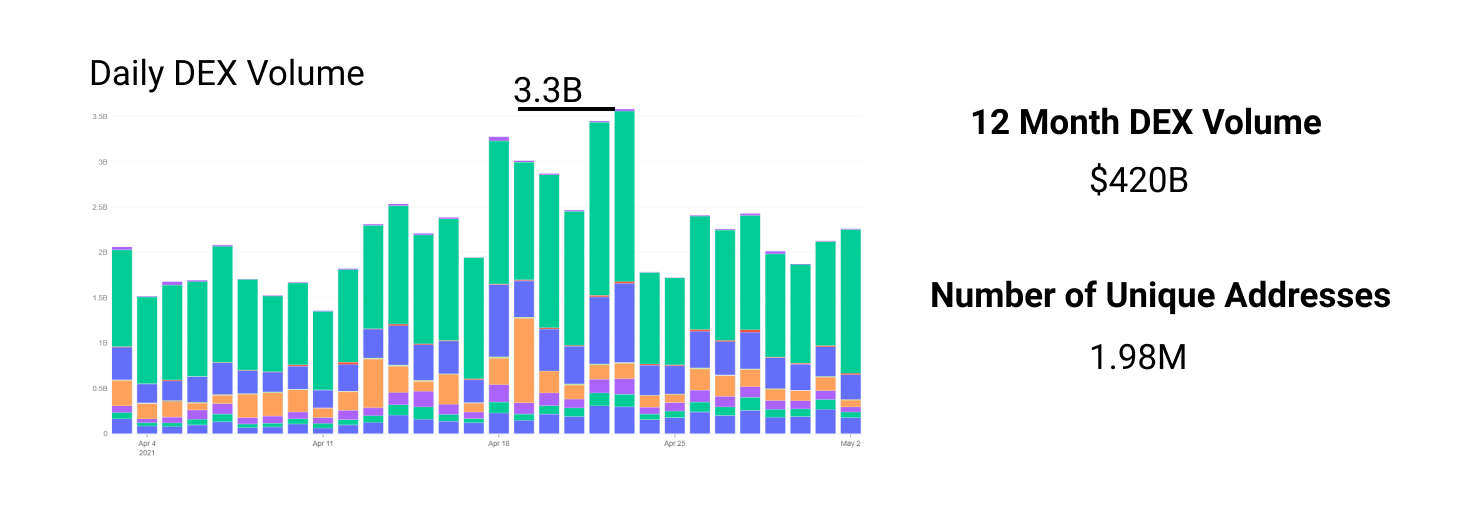

In terms of real demand side for these products, volume has been incredibly strong, with a 12 month volume of $420B, 30 day volume of $67B, and daily volume peaking in April above $3B daily volume among all Ethereum DEXs. Additionally, 1.98M unique addresses have interacted with DEXs to date.

Measuring liquidity vs users side by side, we get an interesting view at what exchanges are satisfying stickiness among both the supply and demand sides respectively. The holy grail of adoption is when a DEX can both attract strong persistent liquidity and volume over an extended period of time.

Keep in mind that while in the case of Curve their liquidity may seem inflated relative to volume and fees, Curve is focused on stablecoin pairs which are far less volatile. Additionally, Curve invests assets in the liquidity pool to Compound and Yearn Finance for additional yield on top of trading fees. They are an example of a DeFi project benefiting from the benefits of composability; projects like Yearn and others tap into their platform as a basis for stablecoin swaps and liquidity mining.

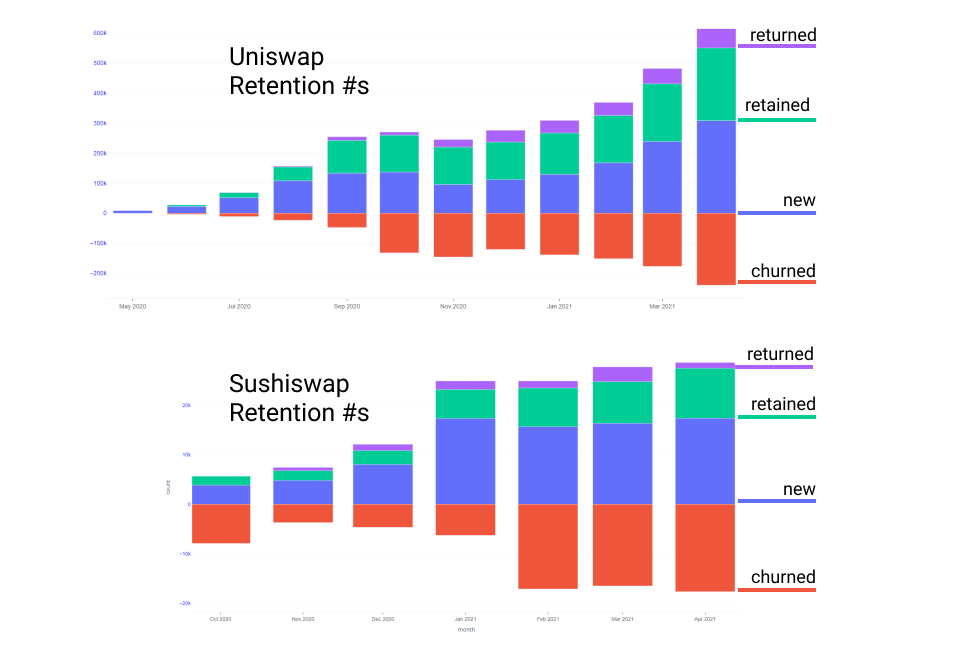

We can also measure the health of an exchange by user retention. Some exchanges persistently keep strong liquidity with incentive programs, but they leave a bit to be desired on user retention.

In the following breakdown we see Uniswap churn 240,000 addresses while retaining, returning, and creating 615,000 users in April. We see Sushiswap churn 18,000 addresses while retaining, returning, and creating 31,000 users. This puts Uniswap net retention at +375,000 users and Sushiswap net retention at +13,000 users.

Collateralized Stablecoins

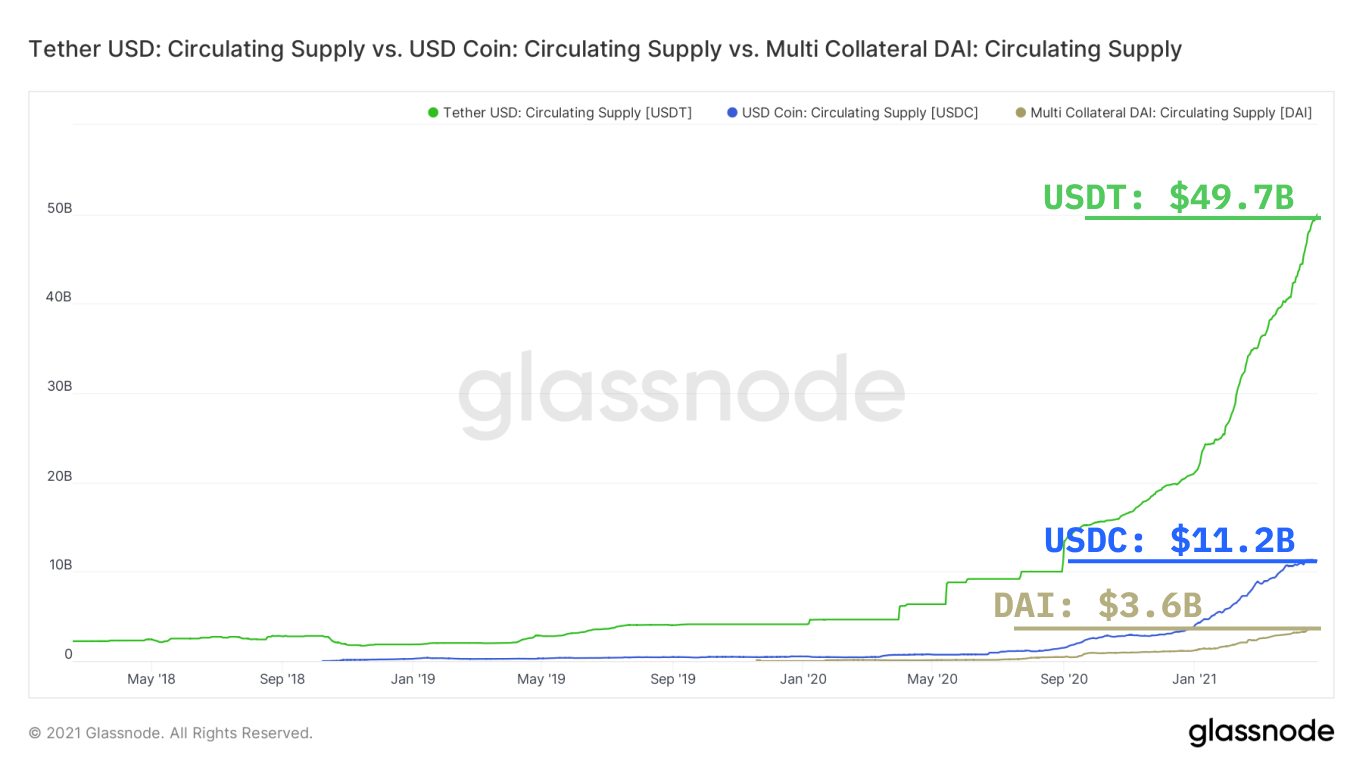

Stablecoin usage has become a core tenant of DeFi, with the centrally issued, reserve backed tokens USDT and USDC dominating the market share. Stablecoins have emerged as the base currency in most DEX pairs and lending markets.

The largest attempt at a decentralized stablecoin design is DAI, which maintains a soft peg to USD via market arbitrage without a central reserve. DAI is the currency of MakerDAO that is backed by collateralized debt positions of ETH and other tokens. The MKR token is used as an asset of last resort that can be spent to pay back lenders in case of any insolvency events. In order to incentivize MKR token holders, the MKR token is burned when debt holders pay back the stability fee which is akin to an interest rate that keeps the system stable.

While USDT and USDC are clearly dominant, DAI’s growth as a stablecoin remains impressive, having reached over $3.6B in circulating supply since inception.

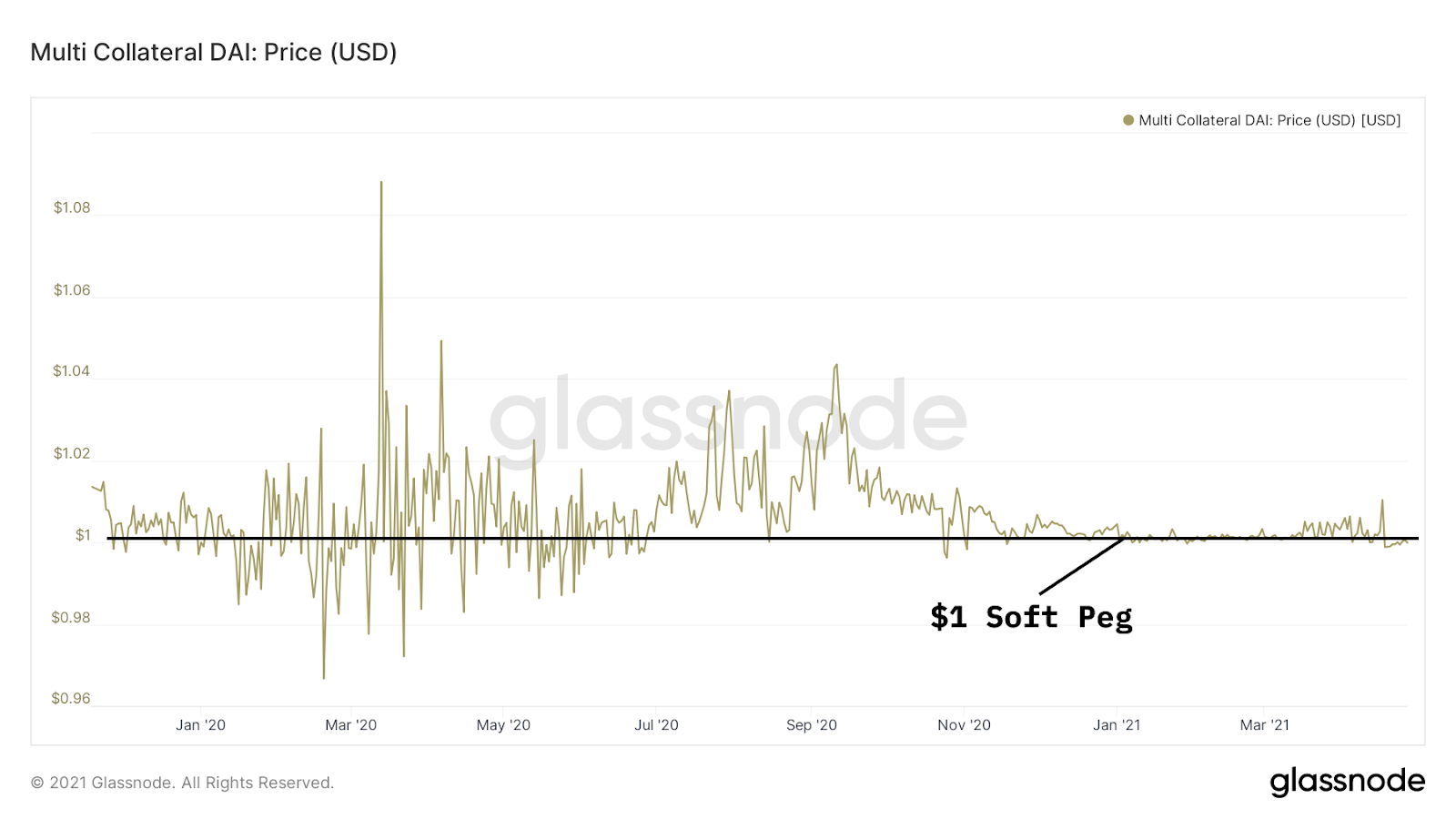

DAI has historically maintained a relatively stable peg to the US Dollar. While issuance is managed by the MakerDAO, traders will often try to profit off an arbitrage opportunity to short DAI above $1 and long DAI below $1. This trade can additionally be expressed by depositing ETH to mint DAI or conversely paying back CDPs to withdraw collateral.

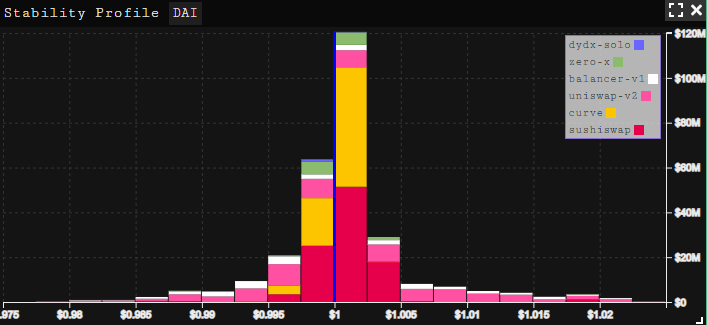

To demonstrate, we can see which DEX liquidity providers have established the deepest liquidity pools centered on a DAI peg around $1. This enables the capture of any spread and trading fees should the price of DAI drift too far in either direction.

We also note the use of DAI amongst various DeFi protocols. Maintaining a peg is nice, but actual usage inside of the top DeFi projects is even more important.

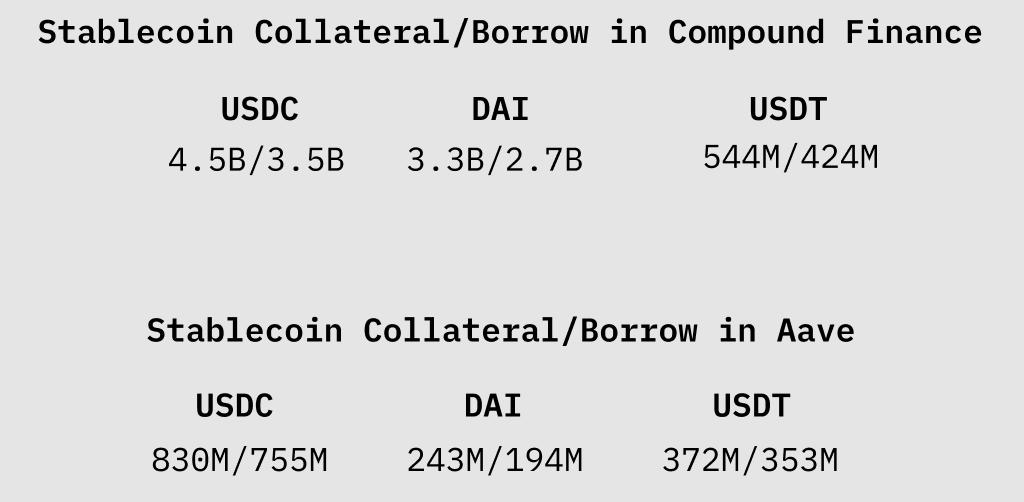

In lending markets, DAI is the stablecoin with the 2nd most collateral in Compound and a close third in Aave. This is quite healthy considering the total outstanding supply of DAI is <10% the total supply of USDC, USDT, and DAI.

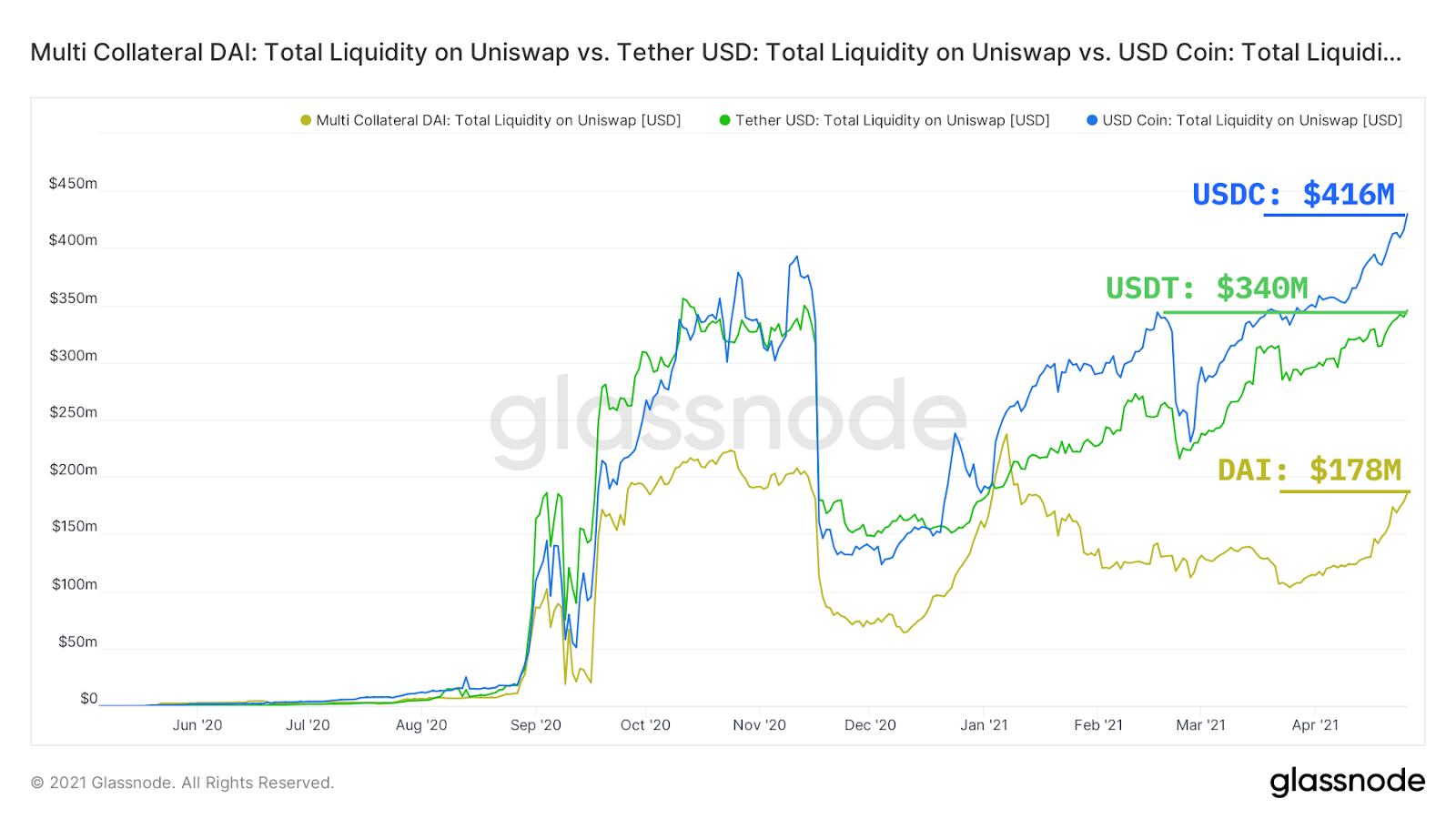

In decentralized exchanges, a look at the DAI supply side shows healthy liquidity, with DAI claiming about 19% of stablecoin liquidity on Uniswap.

On the demand side, DAI’s volume takes about 15% daily volume of Uniswap volume in pairs that include DAI. USDC and USDT each take about 43%.

Stablecoins are among the most adopted assets in DeFi. The strength and stickiness of stablecoins in DeFi are marked by some key characteristics:

- USDC, USDT, and DAI represent dominant DEX trading pairs

- Stablecoins offer ample liquidity and strong utilization in lending markets

- DAI maintains a peg and growing adoption without needing a USD-backed reserve

Yield Aggregators

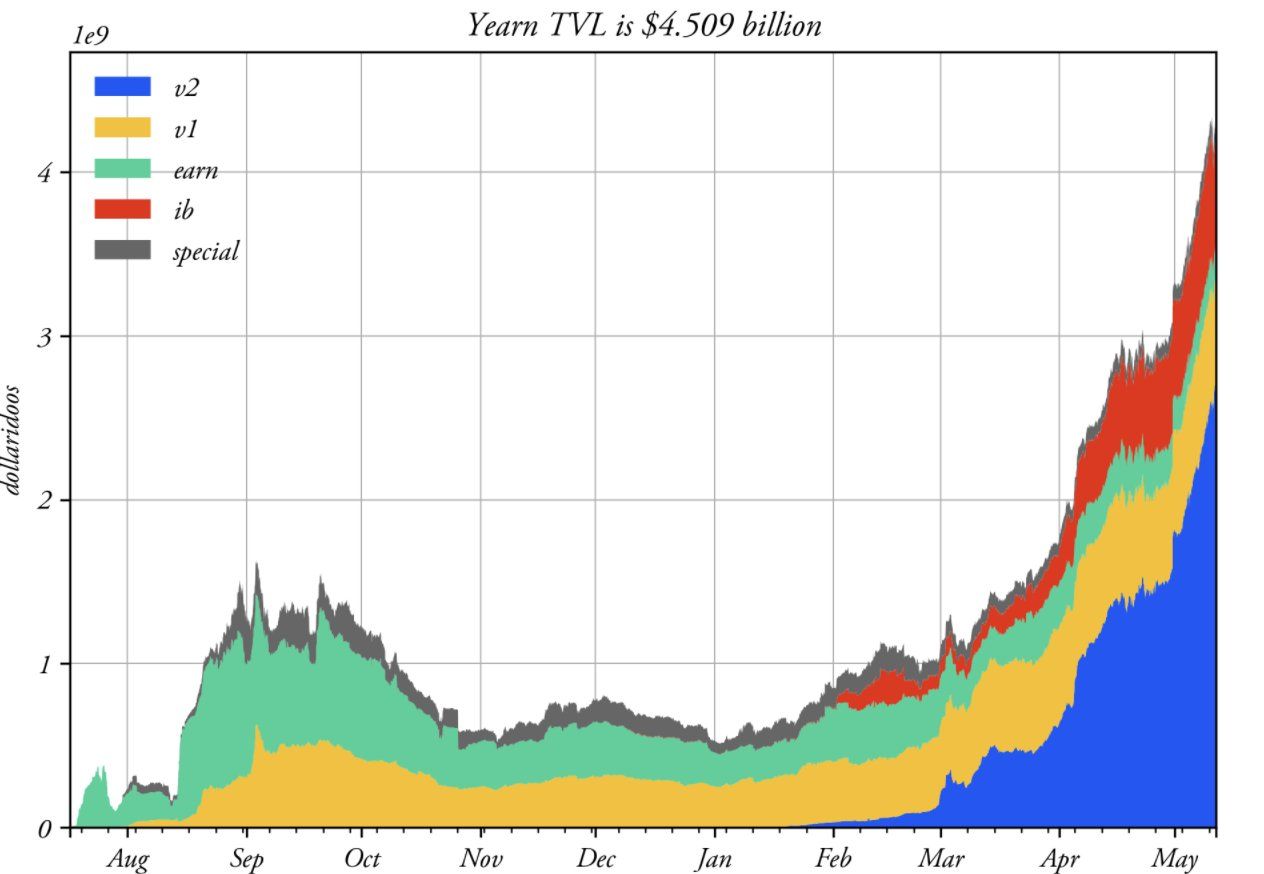

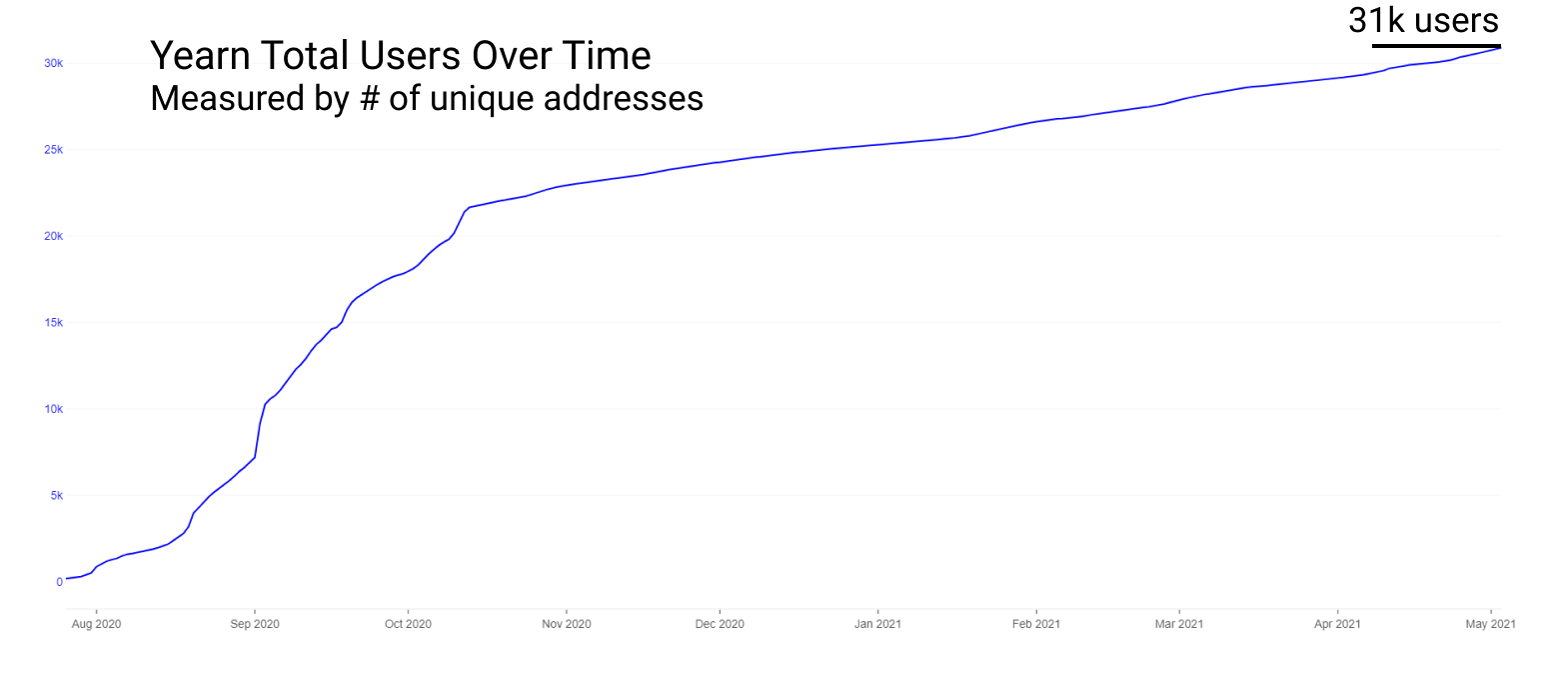

This is a competitive sector of DeFi with a clear winner thus far in Yearn Finance.

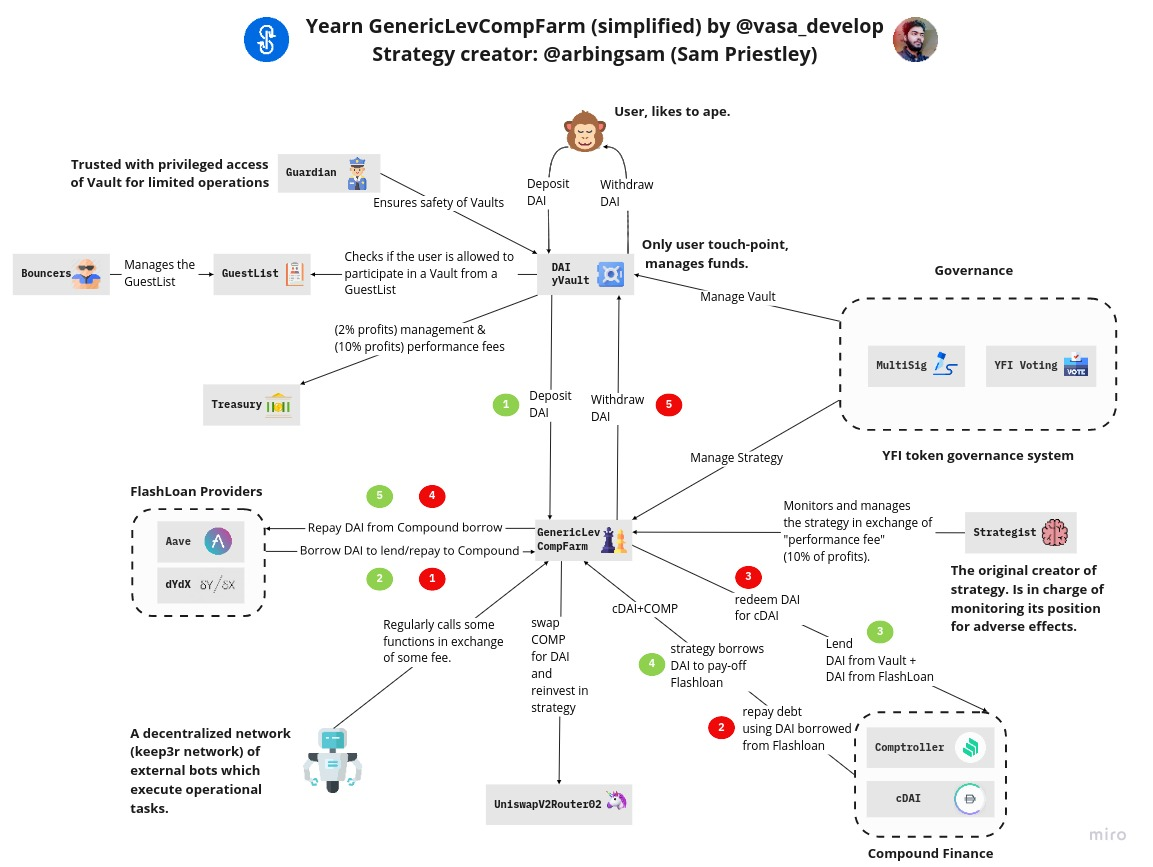

Yearn Finance is a yield aggregator which manages users’ capital with a variety of strategies designed to maximize yield. It works by moving pooled capital around various DeFi protocols with advantages of scale and ease of use for users.

Their pace of delivering competitive strategies and ease-of-use for project integrations and individual users alike has resulted in over $4.5B in TVL being attracted to the protocol as of May.

Users lock their assets in Yearn vaults that automatically allocate capital across various strategies. The basis for these strategies as described in Yearn docs goes like this:

- Use any asset as liquidity.

- Use liquidity as collateral and algorithmically manage collateral to avoid default.

- Borrow stablecoins.

- Put the stablecoins to work liquidity mining and/or earning fee revenue.

- Reinvest returns to create compounding growth.

The DAI vault for example utilizes a complex web of strategies and interoperable protocols to generate yield for depositors. This level of complexity and strategy is far too complex for the average user to implement, so Yearn offers users a single click solution, without needing to fully understand the complexities of how their money is put to work. They charge straightforward 2% management and 20% performance fees for their effort, not unlike typical hedge fund 2 and 20.

User trust in the Yearn system grows as a result of relatively few smart contract exploits, developer and strategist skill, and consistently competitive rates of return afforded by automatically finding and moving deposits to the source of highest yield.

Yield aggregators have found adoption both among individual DeFi users and projects as a key piece of infrastructure. Users go to Yearn looking for simple ways to participate in DeFi opportunities whilst minimizing gas fees, complexity and liquidation risks. Projects integrate Yearn as a key piece of infrastructure for their project - Badger DAO and Alchemix each having deposited over $300M in Yearn vaults, and more projects continue to add Yearn.

With strong growth to date, capital continues to accumulate in Yearn and other aggregators, with little sign of slowing down.

Concluding Remarks

Decentralized Finance has gone from a niche sector of crypto to a leading sector in less than 12 months. While total value locked ($124B) is a useful metric for overall DeFi adoption, it hardly tells the full story of true adoption and product market fit. Instead, more useful metrics can be used to get the full picture of both the supply side (liquidity) and demand side (volume, users, utilization, retention, etc.).

In 12 short months DeFi has reached:

- 2 million+ users (unique addresses)

- $120B+ value locked across all DeFi related smart contracts

- Daily volume regularly exceeding $2B on decentralized exchanges

- Stablecoin utilization on lending platforms regularly >80% on liquidity of $10B+

- A decentralized stablecoin (DAI) with $3B+ circulating and stability around its soft peg

The most exciting part, is this is just the opening chapter for the future of finance.

- Follow us and reach out on Twitter

- Join our Telegram channel

- For on–chain metrics and activity graphs, visit Glassnode Studio

- For automated alerts on core on–chain metrics and activity on exchanges, visit our Glassnode Alerts Twitter