BTC Market Pulse: Week 8

Bitcoin shows mixed signals: weak spot demand ($7.45B volume), cautious derivatives ($46.17B OI, -$169M CVD), and slowing ETF flows. On-chain activity and liquidity inflows are fading, while 86% of supply remains in profit. Without a catalyst, momentum may stall.

Overview

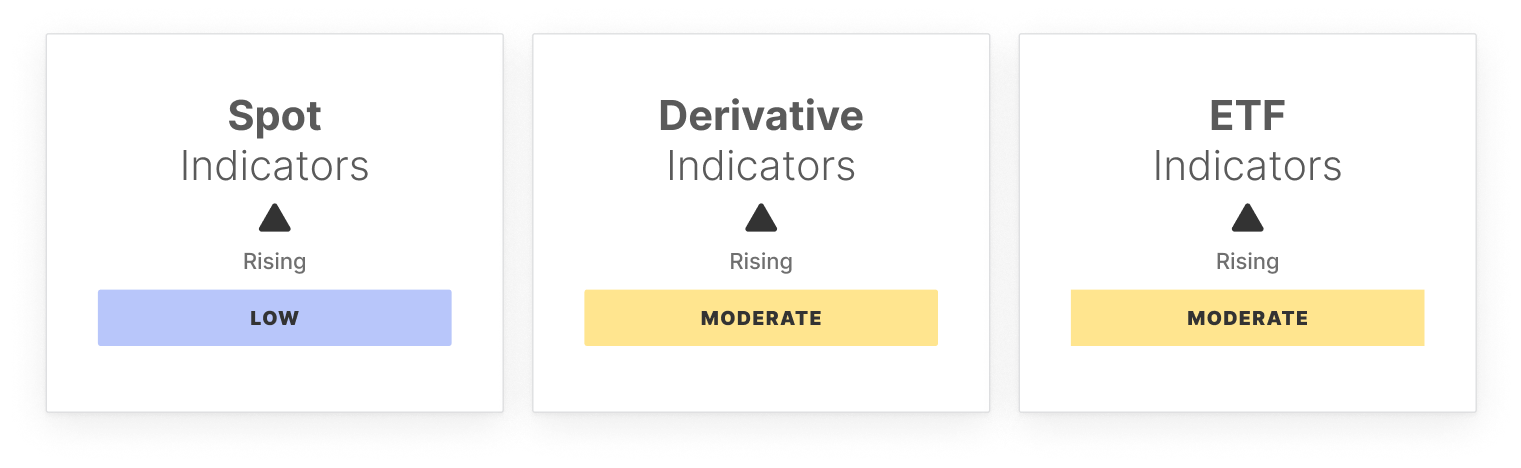

We can observe mixed signals across key sectors in the Bitcoin market. Spot markets remain weak, with volume down to $7.45B and persistent sell-side pressure (-200M CVD), indicating subdued demand. In contrast, derivatives are active, with Futures Open Interest at $46.17B, though funding rates ($1.18M) and Perpetual CVD (-169.63M) suggest a cautious stance among traders.

ETF markets show early signs of recovery, with net inflows rising to $399.71M, yet trade volume has slowed to $8.96B, signaling hesitation among institutional investors. ETF MVRV at 1.50 suggests most holders remain in profit but are not aggressively adding exposure.

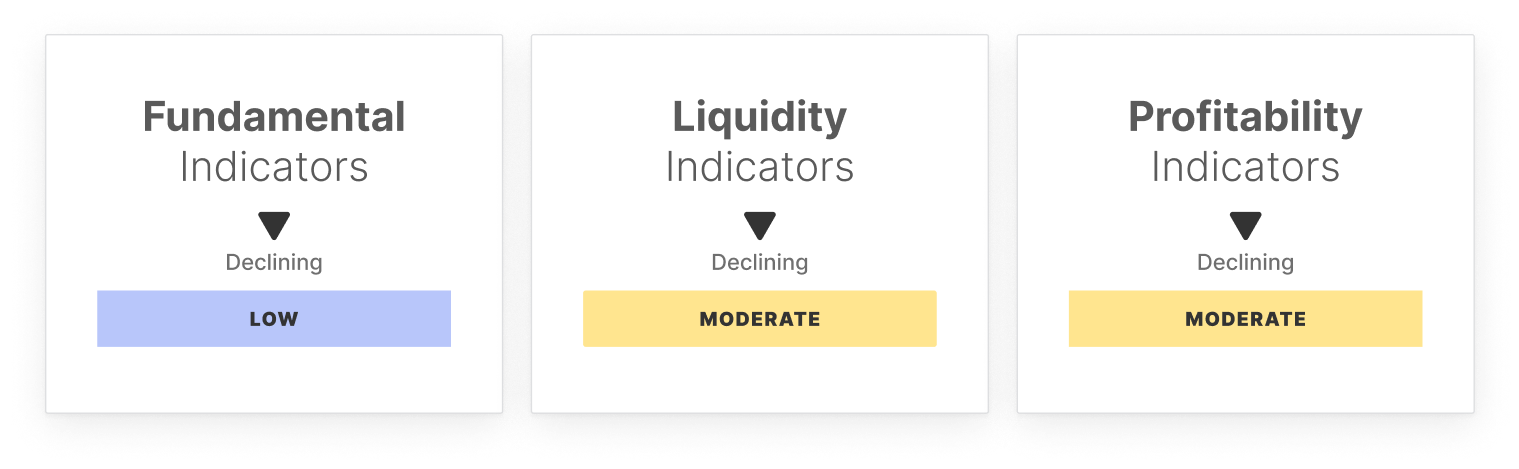

On-chain activity has weakened, with active addresses (694.53K) and transfer volume ($6.58B) declining, while low fees ($488.89K) confirm reduced network demand. Liquidity inflows are slowing, as Realized Cap Change (3.64) and Hot Capital Share (0.48) indicate fading new demand.

Despite this, profitability remains high, with 86% of supply in profit and NUPL at 0.55, though a declining Realized Profit/Loss Ratio (1.28) suggests profit-taking is cooling. While liquidity remains available, without a clear catalyst to ignite demand, this momentum may weaken, leading to further consolidation or downside risk as capital deployment slows.

Off-Chain Indicators

On-Chain Indicators

- Follow us and reach out on Twitter

- Join our Telegram channel

- For on-chain metrics, dashboards, and alerts, visit Glassnode Studio

Disclaimer: This report does not provide any investment advice. All data is provided for information and educational purposes only. No investment decision shall be based on the information provided here and you are solely responsible for your own investment decisions.

Exchange balances presented are derived from Glassnode’s comprehensive database of address labels, which are amassed through both officially published exchange information and proprietary clustering algorithms. While we strive to ensure the utmost accuracy in representing exchange balances, it is important to note that these figures might not always encapsulate the entirety of an exchange’s reserves, particularly when exchanges refrain from disclosing their official addresses. We urge users to exercise caution and discretion when utilizing these metrics. Glassnode shall not be held responsible for any discrepancies or potential inaccuracies.

Please read our Transparency Notice when using exchange data.