Pickle Finance: The Tastiest New Yield Farming Protocol

Among a deluge of food tokens and copycat projects, Pickle Finance has set itself apart with its ambitious plan to bring stablecoins closer to their pegs using its PICKLE token and "pickle jars".

Pickle Finance appears to be the next big thing in the world of yield farming protocols. The project launched to little fanfare on 11 September, but quickly picked up in popularity to become the latest trending "food token".

After the release of Uniswap's UNI token, it risked losing much of its liquidity before the launch phase was even over - but a new proposal may have saved the protocol just in time.

What is Pickle? 💸

According to the project's launch announcement, Pickle is "an experimental protocol to bring stablecoins closer to their pegs using farming incentives, vaults, and governance".

The protocol identifies a core problem in the world of DeFi: despite the prevalence of low-slippage stablecoin trading platforms like Curve.fi, stablecoins still often trade a few percent above or below their pegs. This problem has worsened with the rise of yield farming, as farmers trade large volumes of stable tokens in pursuit of the highest yield.

As an answer to this problem, Pickle introduces incentives to encourage capital movement between stablecoins in order to bring them closer to their intended value while simultaneously rewarding participants in the protocol.

To achieve this, the protocol has introduced the PICKLE token to reward arbitrage between off-peg stablecoins, as well as vault-based strategies which will use arbitrage techniques and flash loans to short overvalued stablecoins.

The PICKLE Token 🥒

Token Launch

The PICKLE token is being launched via an ongoing liquidity mine, with the increasingly popular "fair launch" model; no VC allocation, no pre-mine, and no ICO.

However, like other recent fair launch tokens (see: SUSHI), a portion of PICKLE will be set aside for a development fund. This devshare will consist of 2% of newly minted PICKLE on top of what is being minted to reward stakers. While this devshare model is usually not controversial, some investors are skeptical after the SushiSwap saga.

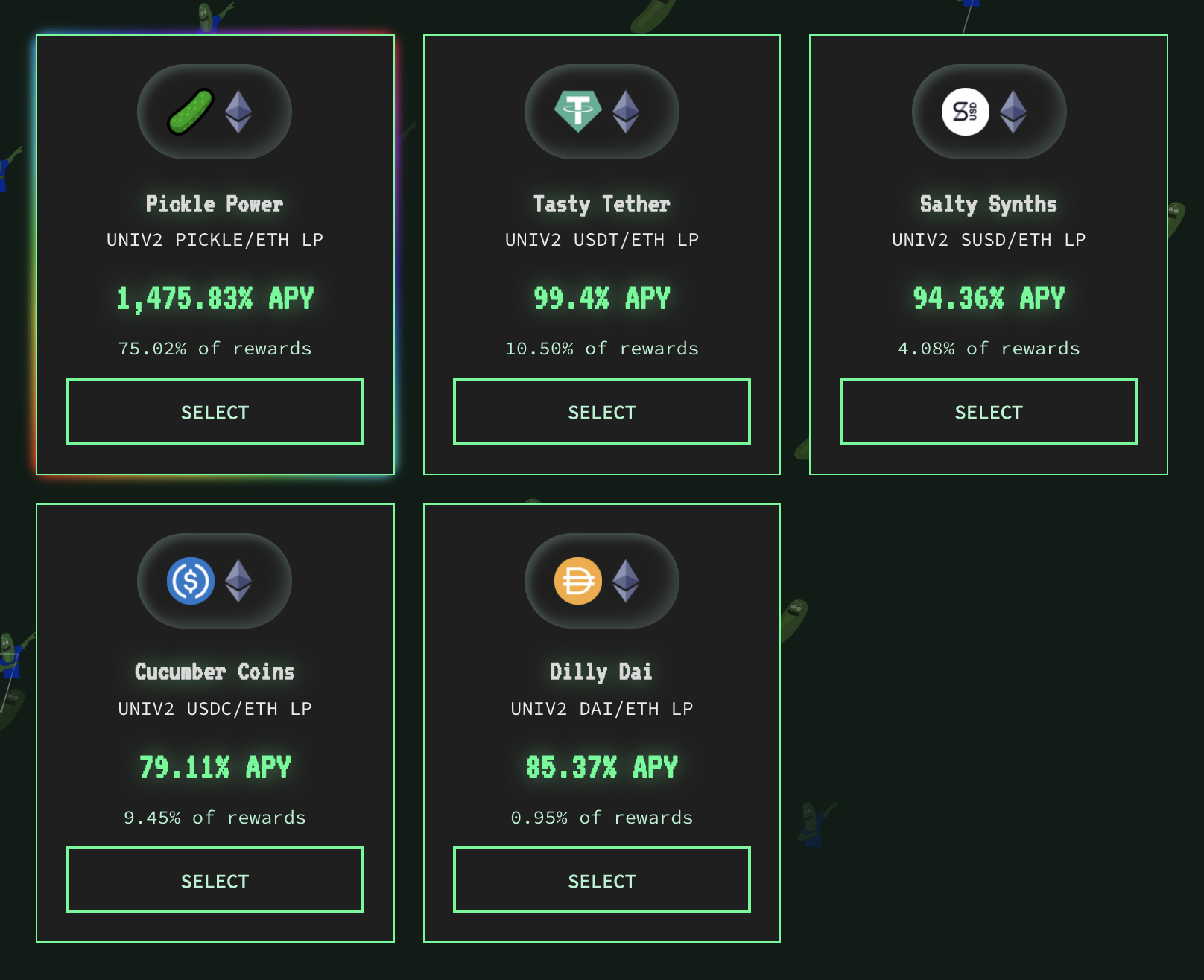

Anyone can mine PICKLE tokens by staking Uniswap LP tokens for several stablecoin pools: DAI/ETH, USDC/ETH, USDT/ETH, sUSD/ETH, and of course PICKLE/ETH.

Token Distribution

As of Ethereum block #10,838,600, PICKLE tokens started being minted, beginning at a supply of zero. Newly minted PICKLE are distributed among everyone staking LP tokens for the above pools.

As a result of a governance vote on Monday, the distribution schedule is as follows:

- 1st week: 10 PICKLE per block

- 2nd week: 5 PICKLE per block

- 3rd week: 2.5 PICKLE per block

- 4th week: 1.25 PICKLE per block

- After: 1 PICKLE per block

Note this this is subject to further governance. The distribution schedule is constantly evolving, and there are ongoing conversations within the Pickle governance community around introducing a potential hard cap on supply in the future.

UPDATE: The Pickle community has voted in favor of a proposal to continually reduce token emissions over the first year. The following analysis does not take these changes into account. As always, in the era of decentralized governance, make sure to always check for current information, as things are always evolving!

The portion of newly minted PICKLE tokens distributed to each pool depends on the price of the underlying stablecoin. If the stablecoin is above peg, fewer PICKLE will be distributed to that pool, creating sell pressure as yield farmers re-allocate their capital to different pools. Stablecoins that are below peg will receive a larger portion of the distribution.

In theory, this mechanic should encourage LPs to reallocate between stablecoins in order to reap the highest yield, altering market demand for stablecoins and bringing them closer to their pegs.

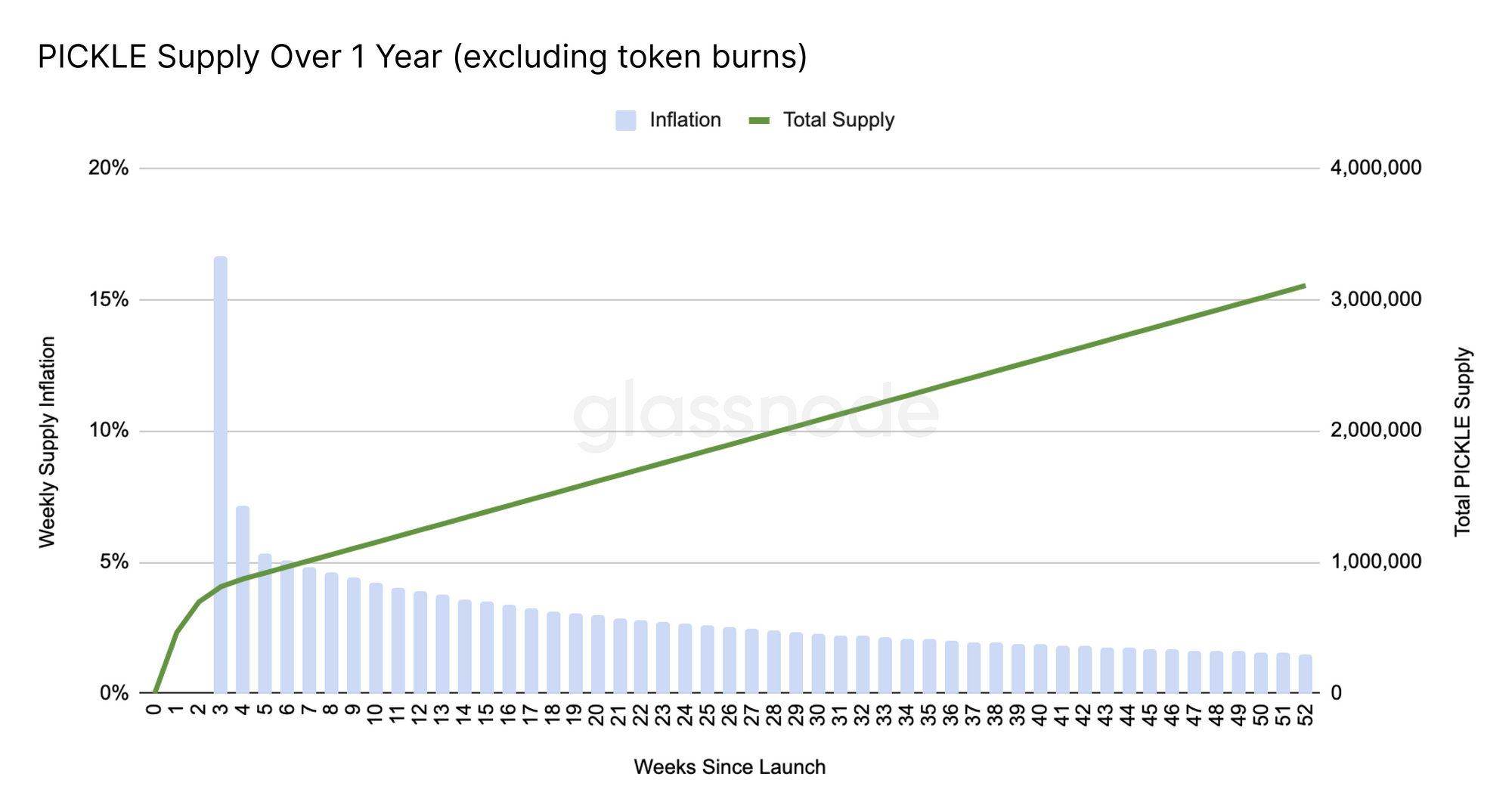

Token Supply

The Pickle team have estimated a block rate of approximately 6646 blocks per day. Based on this figure, and the current distribution schedule as outlined above, the PICKLE supply would reach just over 3 million after the first year.

UPDATE: Reminder - This chart does not account for the latest proposal to reduce token emissions over the first year. See the full proposal for the new supply chart.

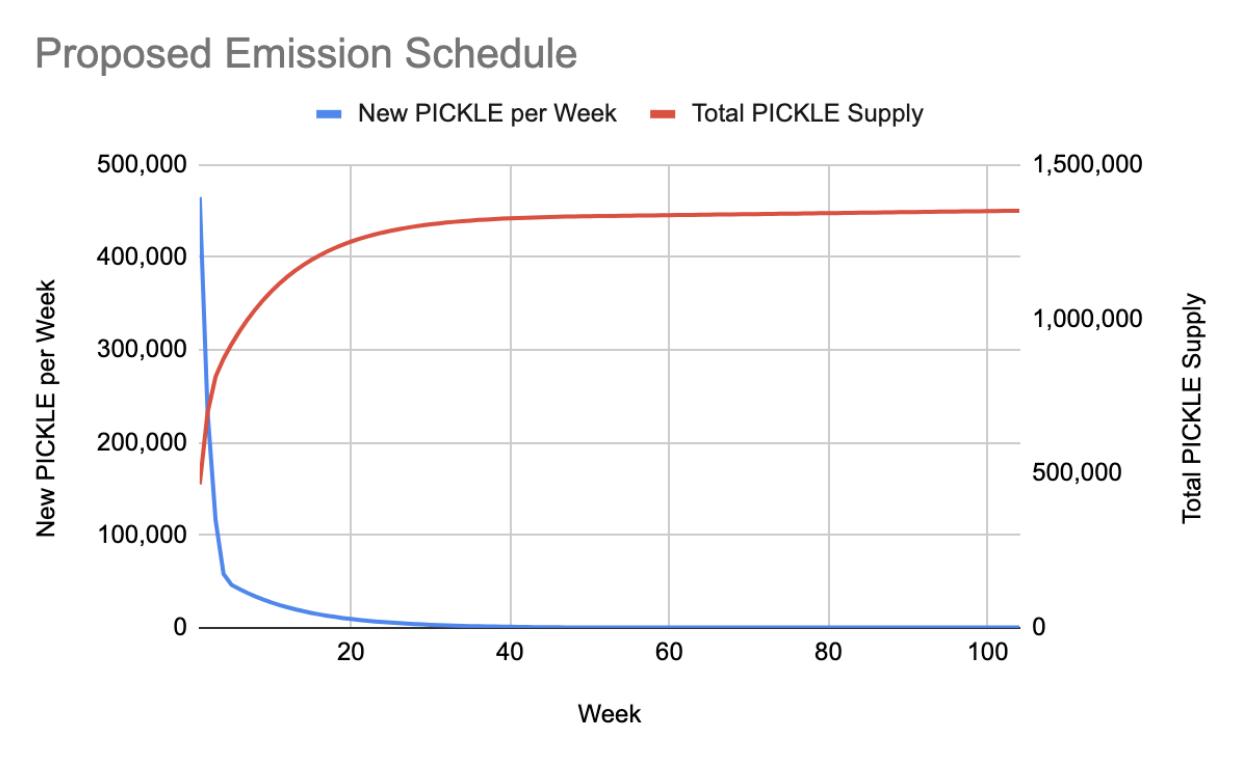

UPDATE: The new PICKLE emission schedule, as outlined in the full proposal, is as follows - bringing the total supply to around 1.35 million PICKLE after two years.

However, the token will also adopt a buy back and burn model (on top of any future governance decisions to reduce the emission rate), which will slow inflation, and possibly even create a deflationary issuance rate if the protocol achieves widespread success. The mechanism for this burn model will be implemented via "pickle jars", discussed below.

Token Utility

The PICKLE token represents ownership in the protocol, with its primary utility function being protocol governance. PICKLE holders who participate in governance decisions will receive a share of the 3% governance fee and 0.5% withdrawal fee on pickle jars.

The protocol has adopted a quadratic voting mechanism in order to prevent whales from gaining asymmetric influence over governance decisions.

🎉🎉🎉 Pickle governance is now up on https://t.co/1OdSNwZljT

— Pickle Finance 🥒 (bluepickle.eth) (@picklefinance) September 13, 2020

We use quadratic voting to prevent whales from having too much influence. ⛔⛔⛔🐋🐋🐋

Instead of counting votes nominally, we take the square root of it for each account 🤓🤓🤓

Unroll thread to learn more👇

This system is by no means perfect. For example, it has garnered criticism from Vitalik for its poor sybil resistance; whales can simply split their funds over many wallets to give their tokens more voting power. However, it represents a good start in the protocol's journey toward more equitable governance.

Pickle Jars 🏦

Alongside the PICKLE mining mechanic, the Pickle protocol will employ a strategy of vault-based yield farming, dubbed "pickle jars" (or pJars), to apply additional pressure to stablecoins in order to bring them closer to their pegs.

Similar to Yearn vaults, these pJars will utilize pooled assets deposited by LPs to generate yield (for example, by farming sCRV tokens via Curve.fi stablecoin pools). A portion of these returns - currently 1.5% - will be used to buy back and burn PICKLE tokens, applying deflationary pressure to the token supply.

pJar Plans

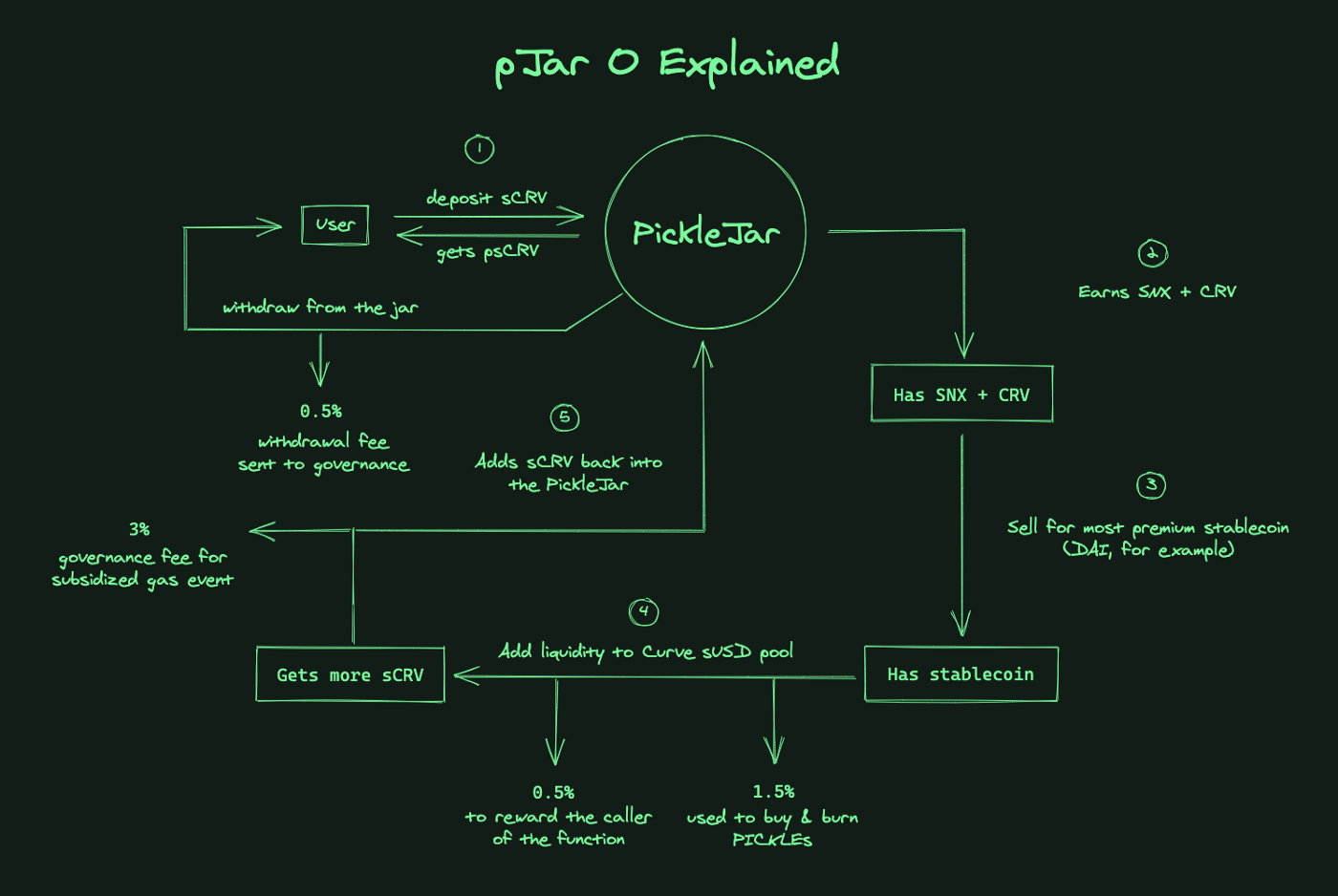

The first experimental pJar is the sCRV pJar, which generates yield by farming sCRV tokens. According to the announcement, the mechanics work as follows:

- LP deposits sCRV (acquired by depositing sUSD into the Curve sUSDv2 pool) into into the pJar and gets psCRV in return.

- sCRV from the pJar is staked to earn CRV and SNX.

- CRV and SNX are market sold for the stablecoin with the least liquidity in the Curve sUSDv2 pool.

- This stablecoin is added into the Curve sUSDv2 pool for more sCRV.

- The additional sCRV are deposited back into the pJar and the cycle continues.

This strategy will generate the yield required to burn PICKLE tokens, as well as rewarding liquidity providers. In addition, by using the yield from this strategy to buy the stablecoin with the least liquidity in the sUSDv2 pool (see step 3), it aims to bring the price of the stablecoins in the pool closer to their $1 peg.

In addition to this first pJar, the Pickle community will continue to build and deploy more pJars over time. Along with pJar 0.69 (see below), there is a plan to launch a leveraged-short DAI pJar in the near future. Named pJar 1, this strategy will use flash loans to arbitrage overpriced DAI.

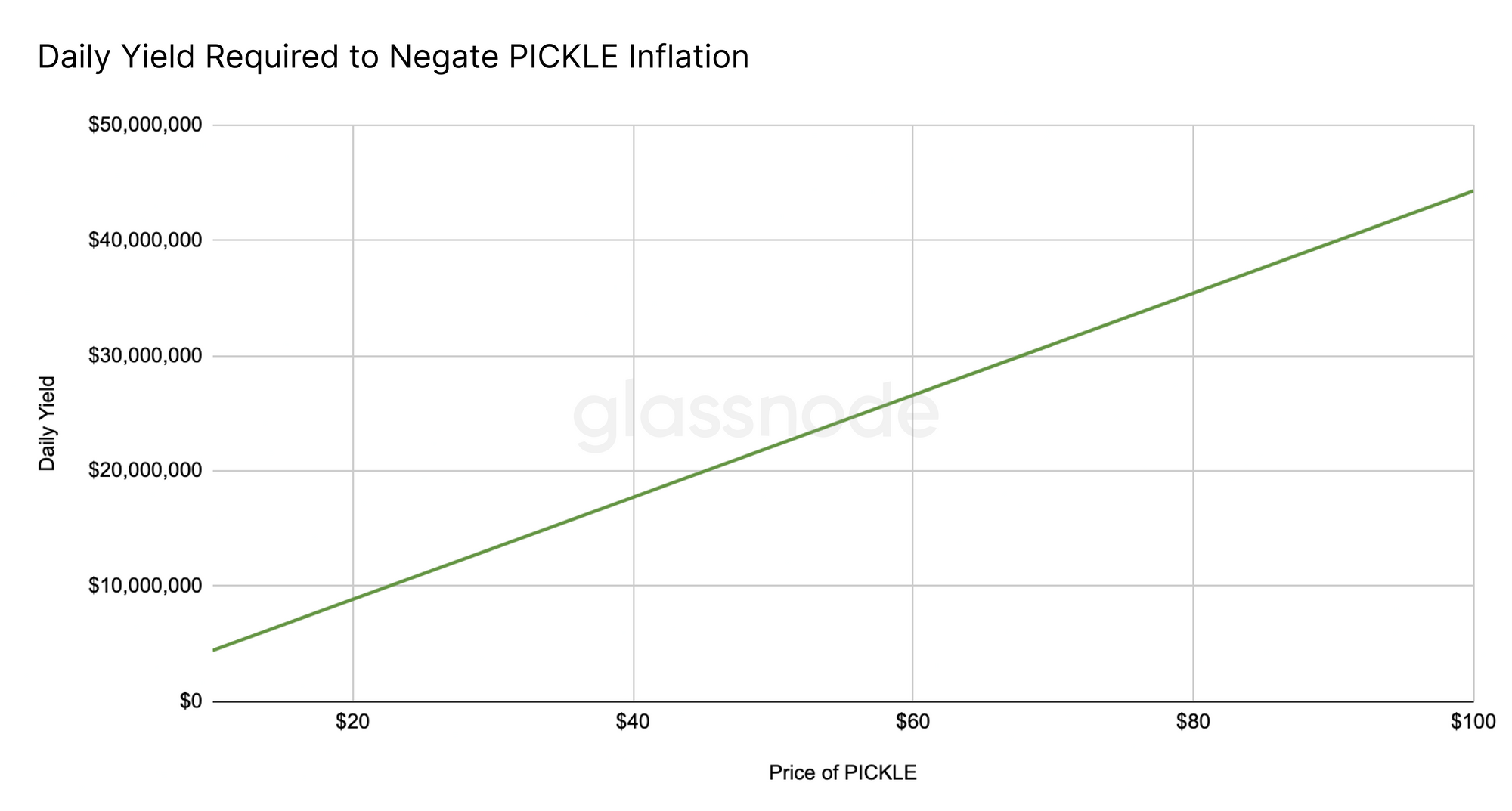

Burn Model: Impact on Inflation

Based on the specified burn rate (1.5% of yield) and an inflation rate of 1 PICKLE per block, we can calculate the pJar yield required to counteract inflation.

UPDATE: As mentioned above, the following inflation rate will no longer be followed. Note that this change will significantly impact the pJar yield required to counteract PICKLE inflation.

At the current PICKLE price of around $30, the protocol would need to generate $13.3m of yield per day to counteract inflation. This translates to $4.9 billion in annual yield, which (at the current estimated APY of 40.5%) would required $12 billion of capital to be staked in pJars.

Assuming a more realistic (but still optimistic) figure of $500 million staked in pJars, the protocol would on average generate $554,795 in daily yield, supporting a zero-inflation PICKLE price of $1.25.

Of course, the price at which inflation is zero is not necessarily its viable market price. The price will almost certainly be driven up due to speculation, demand for voting power, and expectation of future returns. However, the zero-inflation PICKLE price is a helpful starting point when looking at a valuation for the token.

Pickle's UNI Liquidity Crisis 🦄

On Thursday, Uniswap launched their new token, UNI. Now, on top of competing with other yield farming protocols, Pickle also has to compete with the UNI liquidity mining phase, which requires yield farmers to hold LP tokens in one of four pools, three of which overlap with the pools used to farm PICKLE (DAI/ETH, USDC/ETH, and USDT/ETH).

This means that yield farmers have to choose between holding their Uniswap LP tokens and farming UNI, or depositing them into the Pickle protocol to farm PICKLE.

In order to overcome this problem, Pickle introduced pJar 0.69, which allows stakers to farm LP tokens for these pools by farming and dumping UNI. There is also a proposal underway to enable stakers in these pJars to farm PICKLE on top of their LP token returns.

🎉🎉🎉 You no longer have to choose between $PICKLE and $UNI

— Pickle Finance 🥒 (bluepickle.eth) (@picklefinance) September 18, 2020

PickleJar 0.69 is here!

🦄🦄🦄💖💖💖🥒🥒🥒

To start there will be two pools:

1. pJar 0.69a (DAI/ETH)

2. pJar 0.69b (USDC/ETH)

Just put in LP tokens, sit back, and get out MORE LP tokens like magic✨✨✨

This new pJar could likely rescue the Pickle protocol from a massive outflow of liquidity caused by opportunists preferring to mine UNI tokens, by having those stakers reallocate their capital from PICKLE farming pools into the pJar.

Outlook 🔮

Pickle is a compelling new protocol that appears to be well on its way to achieving its goal of bringing stablecoins closer to their peg. If it can capture a large community of stakers, it should be able to support a strong market cap while also providing value to the wider DeFi community.

However, in its early stages, while liquidity is low, the token price may suffer as a result of inflation. In addition, because of the tumultuous nature of the DeFi space, calculating potential future returns is difficult, making a cost/benefit analysis difficult to conduct and potentially scaring some investors away.

On top of this, Pickle has to compete for liquidity with other liquidity mining projects, similar protocols like Yearn's yVaults, and now with Uniswap's UNI token launch - but it is taking these challenges in its stride and rapidly making the necessary changes to avoid an outflow of liquidity.

Overall, while the PICKLE token may not live up to investors' expectations in the short term, Pickle appears to be a promising addition to the DeFi space.

Next Up: The Infamous UNI Token 🦄

As discussed above, the brand new UNI token is making waves in the world of DeFi. The token is Uniswap's answer to the SUSHI token and the community's demands for more decentralized protocol ownership.

Next week, we'll be looking into UNI and its impact on the rest of the industry. Subscribe to Glassnode Insights to stay updated on this and more developments in the rapidly growing DeFi space.

In the meantime, check out our analysis of the SUSHI token:

Liesl Eichholz

Liesl Eichholz

- Follow us and reach out on Twitter

- Join our Telegram channel

- For on–chain metrics and activity graphs, visit Glassnode Studio

- For automated alerts on core on–chain metrics and activity on exchanges, visit our Glassnode Alerts Twitter