SUSHI Token Economics: The Impact of Inflation

In a short amount of time, the SUSHI token has seen a spectacular rise and a drastic fall. But beyond the hype and FUD, what are the fundamentals behind the token's value?

SushiSwap has taken the Ethereum and DeFi worlds by storm, garnering a range of reviews from incredibly positive to highly critical. But little analysis has been done on the true value of its native token, SUSHI. For an introduction to SushiSwap, read this article first:

Liesl Eichholz

Liesl Eichholz

If you're already familiar with the basics of the project, read on to learn more about the token economics of SUSHI.

SUSHI Token Basics

Token Launch

The SUSHI token is being launched via a ~2 week liquidity mining phase, using the increasingly popular "fair launch" model; no pre-sale, no VC allocation, and open access for everyone. Anyone can mine SUSHI by staking Uniswap LP tokens on SushiSwap.

However, despite claims of decentralization and total fairness, the token has proven to be controversial, and not as "fair" as initially claimed. When I started this analysis, I wrote:

It should be noted that 10% of all newly minted SUSHI will be allocated to a development fund for the protocol - essentially putting it into the hands of its creator(s) to be used at their discretion.

Since then, Chef Nomi - the creator of SushiSwap - dumped 2.5 million SUSHI acquired via this 10% devshare mechanism, crashing the price. As a result of the ensuing community backlash, Chef Nomi handed over the reigns, and the devshare will now be controlled by SUSHI whales via a multisig wallet.

Token Distribution

As of Ethereum block #10,750,000, SUSHI tokens started being minted, beginning at a supply of zero. Newly minted SUSHI - or SUSHI minted - are distributed (minus the 10% development allocation) among everyone providing liquidity to the protocol:

- Liquidity mining phase - For the first 100,000 blocks (about 2 weeks), 1000 SUSHI will be minted per block. These are being distributed to anyone staking Uniswap LP tokens from certain approved pools.

- Post-launch - After the liquidity mining phase, 100 SUSHI will be minted per block. These will be distributed among SushiSwap LP token holders (i.e. the protocol's liquidity providers).

Different liquidity pools have different weights, such that some will receive a greater portion of newly minted tokens than others. This pool weight is flexible, and can be changed via a governance vote or when new pools are added to the protocol.

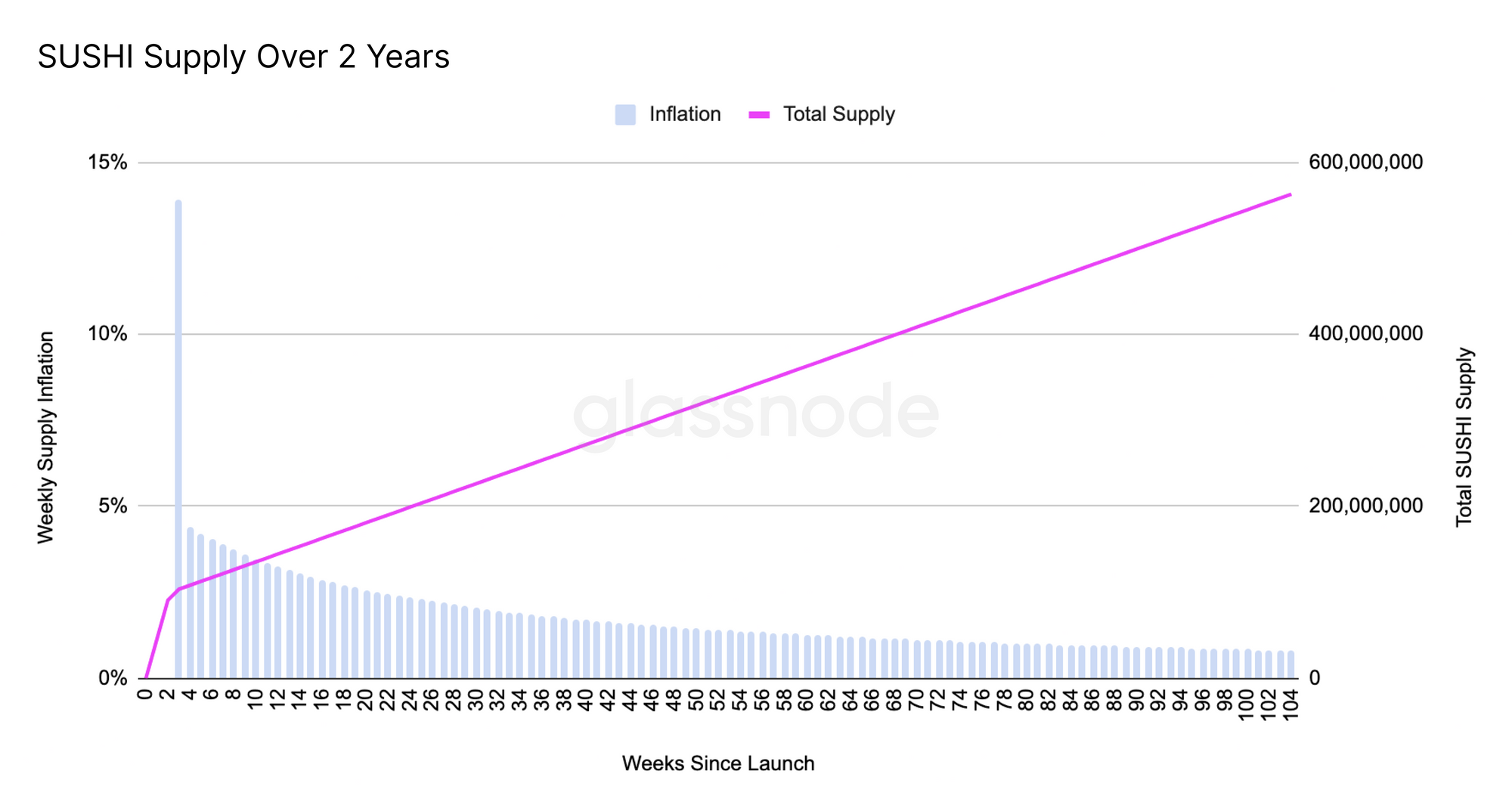

Token Supply

Based on Ethereum's current rate of approximately 6500 blocks per day, the SUSHI supply will be at 326.6 million one year after launch, and almost 600 million after two years.

supply of SUSHI and its weekly inflation rate over timeToken Utility

The SUSHI token is intended to perform several functions, all of which come down to one primary value proposition: protocol ownership.

- Revenue share - The SushiSwap protocol takes a 0.3% fee on each trade; 0.25% goes to liquidity providers, and the remaining 0.05% is converted into SUSHI and distributed to SUSHI token holders as the

0.05% reward amount. - Governance - SUSHI holders can use their tokens to vote on governance proposals regarding changes and upgrades to the protocol.

SUSHI Valuation

Although the value of protocol governance should not be understated, it is difficult to quantify. Similarly, the hype value of yield farming projects (especially in markets such as these) is not easily quanitifiable. As such, the quantitative aspect of this analysis only accounts for the SUSHI revenue share model - namely, the relationship between SUSHI minted and the 0.05% reward amount. Other factors will be addressed through qualitative discussion. Readers should keep in mind that the following figures are simply models, and are by no means comprehensive.

SUSHI Inflation

The primary issue to address when assessing SUSHI’s valuation is the rate of inflation. As the protocol generates new SUSHI minted, existing SUSHI holders will be diluted.

An important note: Inflation is not necessarily a bad thing; in fact, it was incorporated into the system by design, in order to encourage people to actively provide liquidity. This is not inherently negative - it will not decrease the market cap of SUSHI, but rather will increase the supply.

But investors should be aware: anyone holding SUSHI without providing liquidity will be diluted. As such, investors looking at buying SUSHI should do so with caution and with an understanding of the risks behind the underlying token mechanics.

In order for the inflationary token minting model not to dilute existing SUSHI holders (and therefore for SUSHI to maintain a given price), the value flowing into the token must match the value of new SUSHI entering circulation. In other words, if there is sufficient demand to buy up 100% of new SUSHI minted, there will be no inflation of supply in relation to demand; rather than the token price decreasing, market cap should increase to account for the inflated supply.

Disclaimers and Confounders

The following analysis of inflation is simplified, and as such does not account for several important factors which will impact the token price:

- Hodlers - The analysis assumes that all new

SUSHI mintedwill enter into circulation. However, some yield farmers and investors will HODL, decreasing the inflationary impact of the minting functionality. - Dumpers - The analysis does not account for the sell pressure generated by yield farmers and other speculators who will dump their SUSHI for quick returns or to get in on the next yield farming opportunity. Nor does it account for a situation where more of the devshare is dumped by the multisig key holders.

- FOMO and panic sellers - The analysis does not account for buy-side demand as a result of investors wanting to get in on the action, or for sell-side demand as a result of panic sellers. However, the impact of this over time is low, as FOMO- and panic-driven trades will eventually subside and the token price will correct.

- Liquidity - The analysis assumes that the contract executing the buy-back function for the

0.05% reward amountwill be able to purchase an arbitrary amount of SUSHI at market price. However, if liquidity in SushiSwap's SUSHI pool is low (see: hodlers), the buy-back will execute at above market price, impacting the proportion of newSUSHI mintedwhich is backed by real value. - Governance - The analysis does not factor in the perceived or real value of the SUSHI token's governance functionality. The ability for this to impact buy-side demand is hard to quantify, but it is certainly a non-zero amount.

- Opportunity cost - See below.

A further disclaimer regarding the definition of inflation. This analysis differentiates between inflation which is "backed" and "unbacked":

- Unbacked - All new

SUSHI mintedare treated as "unbacked" - and thus contribute to inflation - but this is offset by the number of "backed" tokens purchased in the same time period. - Backed - For the purposes of this analysis, SUSHI which is bought back from the market by the protocol in order to fulfil the

0.05% reward amountis considered to be "backed" by real value - thus offsetting the minting of unbacked tokens.

Note that this SUSHI is redistributed to token holders with no strings attached, and as such differs from assets like USDT, where the value backing the asset is locked and directly redeemable. It also differs from models which buy back tokens and burn them. However, the fact that these tokens are purchased using revenue generated by the protocol, and that they exert buy pressure on SUSHI, means they are treated as offsetting the minting of SUSHI tokens for the purposes of this analysis.

Counteracting Inflation

Luckily for SUSHI holders, the protocol already has a built-in demand generator that can serve to offset inflation. Recall that 0.05% of all trading volume will be used to buy back SUSHI tokens from the market and distribute them to existing SUSHI holders - this value is the 0.05% reward amount.

Based on the current rate of 6500 blocks per day, the amount of SUSHI minted per day is 650,000 (after the initial liquidity mining phase is over). If the daily 0.05% reward amount equates to 650,000 SUSHI at market price, then the built-in demand for SUSHI will counteract the protocol's built-in inflation. In other words, the SUSHI minted will be backed by the value flowing into the protocol in the form of the 0.05% reward amount.

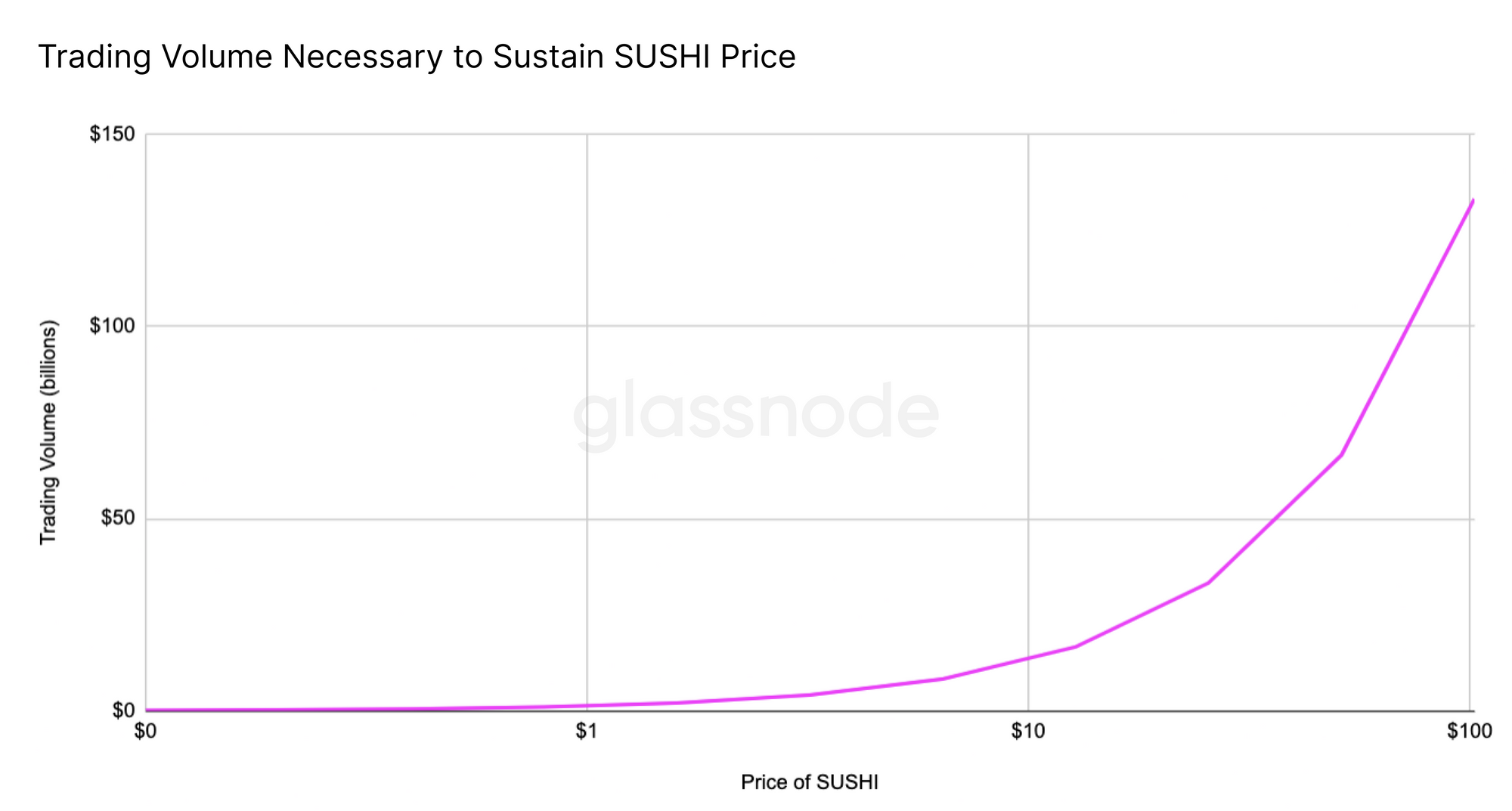

In order for the daily 0.05% reward amount and the daily SUSHI minted to be equal, the ratio of price to trading volume must be 1:1,300,000,000. This allows us to calculate the daily trading volume necessary to maintain a given price.

In theory (see disclaimers above), if the ratio of price to daily trading volume falls somewhere along this line, the price of SUSHI should remain stable. (Note that the x axis uses a log scale; the relationship here is linear.)

trading volume necessary to sustain SUSHI priceOne look at this chart's y axis should have caught your attention. It goes all the way up to $150b in trading volume, while Uniswap (the world's largest DEX by volume) has never even reached $1 billion. We have used this over-the-top scale to illustrate that without insanely high volumes, a SUSHI price above $10 (let alone higher) is preposterous, and could not be sustained for more than a short while before inflation causes it to plunge back down.

In reality, assuming that SushiSwap captures a more realistic daily trading volume of $400 million, the sustainable price for SUSHI (using the ratio defined above) would be $0.31 - a full 97% lower than its all-time high of $11.93.

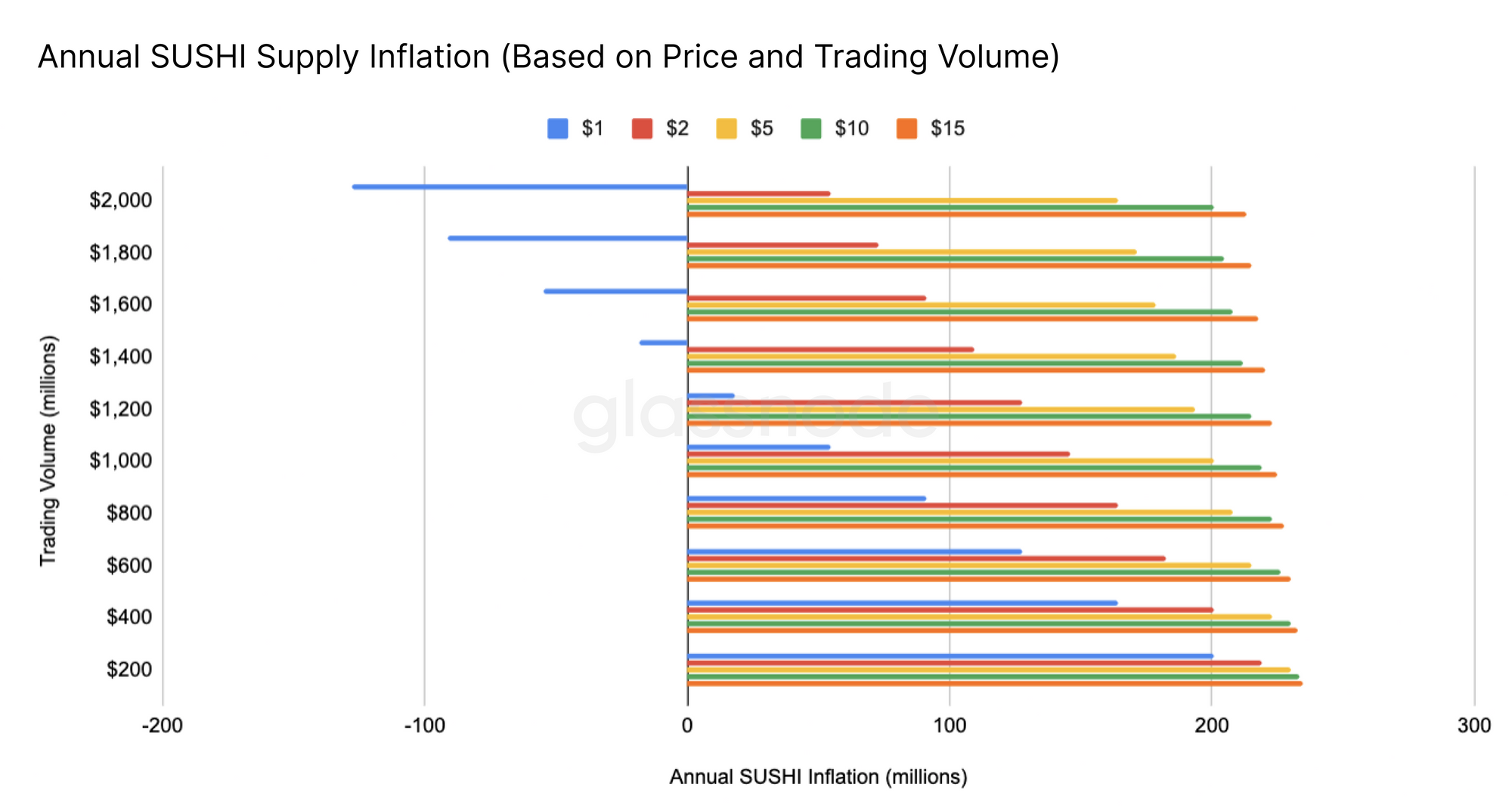

Annual Inflation (Absolute)

Due to hype and a lack of understanding about the token's fundamentals, the SUSHI price will likely remain higher than this sustainable point in the near-term, causing inflation. Below, using various possible values for price and trading volume, we calculate the annual inflation caused by the minting of "unbacked" tokens (i.e. total SUSHI minted minus SUSHI purchased with the 0.05% reward amount).

The values on this chart are calculated as follows:

- Based on daily

trading volume, calculate the annual value of the0.05% reward amount. - Based on a given SUSHI

price, calculate the number of SUSHI that will be purchased with the0.05% reward amount. - Subtract this number from the total number of

SUSHI mintedin a year. - The remainder, displayed below, represents the number of

SUSHI mintedwithout backing (i.e. without being paid for by the0.05% reward amount).

SUSHI minted each year without being backed by a market purchaseAt low trading volume and high price, hundreds of millions of SUSHI will be added into circulation every year - without having their value backed by money actually flowing into the system.

Conversely, at higher trading volume and lower price, the amount of inflation decreases, and eventually begins to fall into the negatives (i.e. below the pink line in Figure 2 above). For example, at a trading volume of $1.4 billion per day and a SUSHI price of $1, more SUSHI would be bought by the protocol than is being minted each day, exerting deflationary pressure and increasing the value of each SUSHI token.

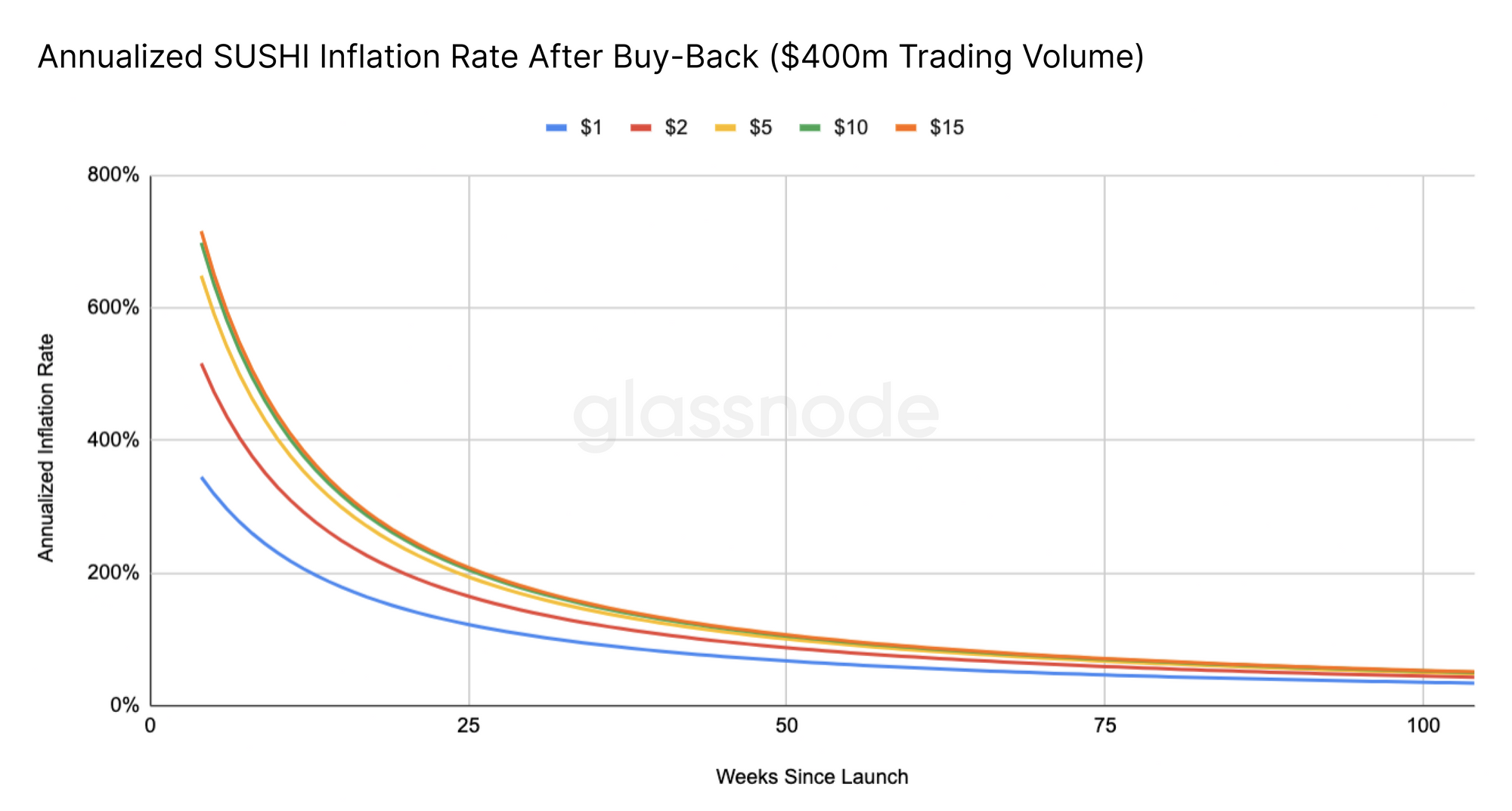

Annualized Inflation (Relative)

Because the SUSHI supply increases at a constant rate, the impact of each new minting event will decrease as the total supply grows over time. Therefore, it is helpful to look at inflation as a percentage over time, rather than in absolute numbers.

As in Figure 3 above, here we use various different price points to calculate buy-side demand (generated by the buy-back using the 0.05% reward amount) and subtract it from absolute SUSHI inflation caused by new SUSHI minted. To simplify, we assume a consistent daily trading volume of $400 million.

SUSHI minted without being backed by a market purchaseThe chart above illustrates how, as SUSHI's total supply grows over time, the impact of new SUSHI minted becomes weaker. As such, the price at which SUSHI is bought back from the market through the 0.05% reward amount - and therefore the number of SUSHI purchased from the market - has less of an effect on the inflation rate over time (as demonstrated by the lines converging).

Especially in the first few months of the protocol's existence, the price of SUSHI will have a significant effect on the degree of inflation. Prospective investors should be aware of this, and should also note that the inflationary impact of new SUSHI minted is disproportionately large in the earliest stages after the protocol is launched.

As a result, unless trading volume grows extremely high or price dips below the sustainable point, the general rule to go by is that the potential for the price of SUSHI to rapidly decrease is highest right now.

Opportunity Cost

Along with inflation, the opportunity cost of holding SUSHI will also impact its value. Aside from the potential yield investors may generate by selling SUSHI to allocate their funds to another protocol, in certain circumstances, SushiSwap's internal mechanics may drive investors to sell.

Depending on several variables relating to the SUSHI/WETH pool, it will often be more profitable for investors to sell half of their SUSHI into ETH and become a liquidity provider, rather than holding the full value in SUSHI and redeeming the 0.05% reward amount. The relevant variables are:

- The

pool weight(i.e. the proportion of newSUSHI mintedthat the pool receives - currently around 21% for SUSHI/WETH). - Total

liquidityin the pool. - The pool's daily

trading volume.

Calculating Opportunity Cost

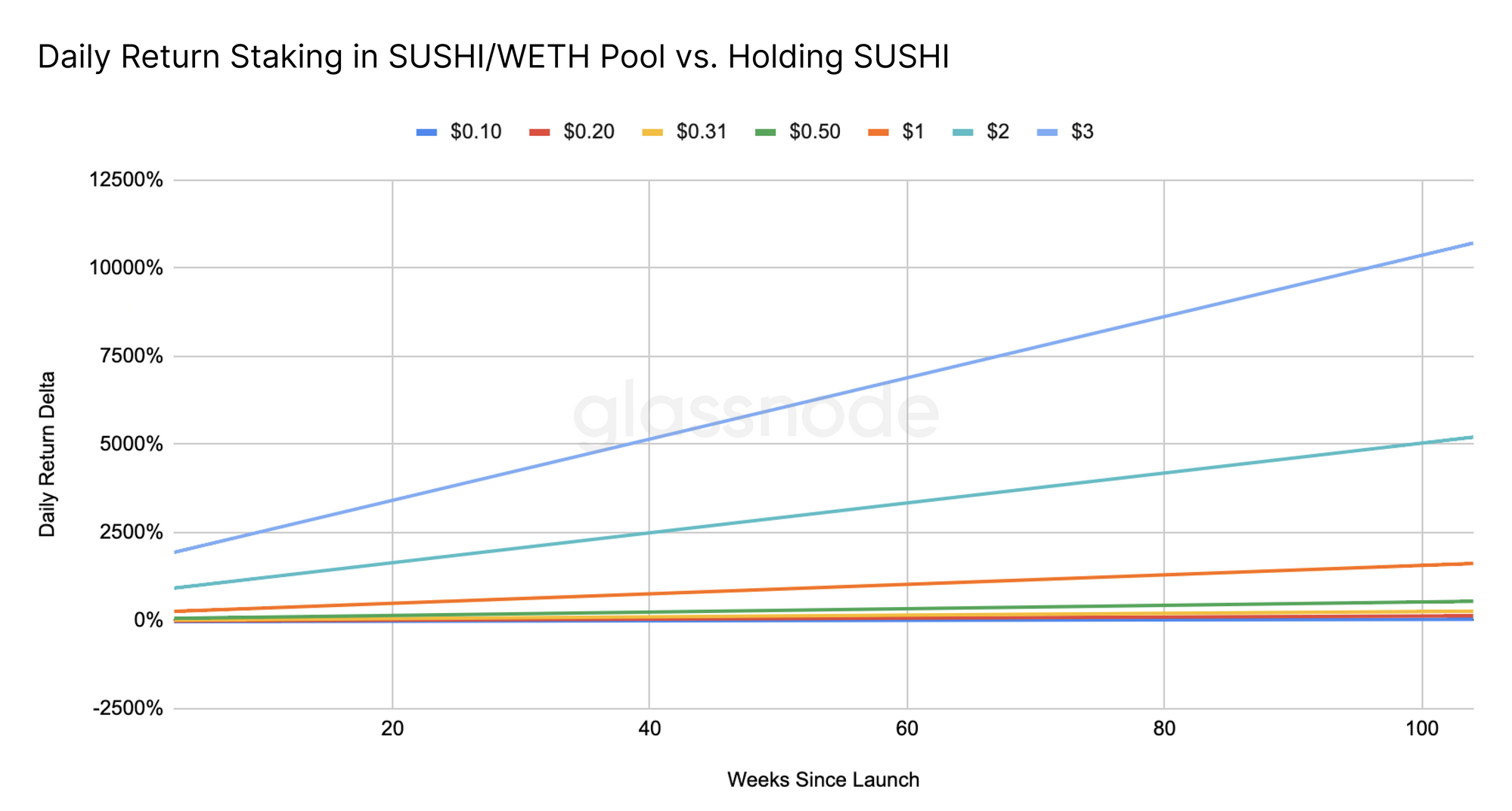

In the following chart, we look at the possible returns if an investor sells half of their SUSHI for ETH and becomes a liquidity provider for the SUSHI/WETH pool, versus simply holding the equivalent value in SUSHI. The figures show the delta in returns for a given week after SushiSwap's launch, if the investor were to make the change during that week.

Note that the calculations do not account for the compounding value of acquiring more SUSHI, as this will differ depending on when the investor sells their tokens. Also note that the x axis starts from week 3, as pools on SushiSwap will not be open until after the first 2 weeks.

If we make the following assumptions:

- SUSHI/WETH

pool weightis 21%; - SUSHI/WETH

liquidityis $40 million; - SUSHI/WETH

trading volumeis $40 million (10% of all volume);

We see that it is almost always more profitable for an investor to sell half of their SUSHI in order to provide liquidity to the SUSHI/WETH pool, rather than holding the full value in SUSHI.

priceBased on the assumptions above, this chart shows that for any SUSHI price above $0.28, it is always more profitable for an investor to sell 50% of their SUSHI and become a liquidity provider instead of holding 100% of their SUSHI tokens.

Even if the price were lower - say, $0.10 - it would only be more profitable to hold SUSHI for the first 57 weeks post-launch, after which point it would be more profitable to become a liquidity provider instead. Further, even if liquidity were higher - say, $80 million - becoming a SUSHI/WETH liquidity provider would still always be more profitable than holding SUSHI for any price over $0.48 - a price point which decreases continually as time goes on.

Consequences of this Opportunity Cost

The fact that SUSHI holders will be able to make more money selling half of their SUSHI as opposed to holding it means that SUSHI will see significant sell pressure, even if it stays at or below its "sustainable" price as dictated by the protocol's inherent inflationary mechanism.

Conclusions

Overall, holding SUSHI will be a risky investment decision if the holder is not using it to provide liquidity, as SUSHI holders will be constantly diluted due to the inflationary mechanism which mints new tokens for LPs.

In addition, even if the SUSHI price is at or below the "sustainable" point (at which inflation is counteracted by token buy-backs), the opportunity cost of holding SUSHI is high, creating sell pressure and driving the price down.

The token's governance functionality will be important in counteracting these price-depressing factors; those who relinquish control of their SUSHI by selling some of it and using it to provide liquidity risk being out-voted in governance proposals which impact their remaining SUSHI holdings (e.g. a vote to reduce the pool weight of the SUSHI/WETH pair). In addition, speculation may keep the token price high for a fair amount of time.

However, the combination of the protocol's inflationary nature and the opportunity cost of holding SUSHI tokens will likely cause the token price to drop until it reaches a sustainable level far lower than current market signals suggest.

- Follow us and reach out on Twitter

- Join our Telegram channel

- For on–chain metrics and activity graphs, visit Glassnode Studio

- For automated alerts on core on–chain metrics and activity on exchanges, visit our Glassnode Alerts Twitter