Bouncing Into Supply

Bitcoin has entered the new year with constructive momentum, posting two consecutive higher highs and extending price to $95.6k. This early-year advance, however, has carried price directly into a historically significant supply zone.

Executive Summary

- Bitcoin remains locked in a low-volatility consolidation regime, with compressed ranges masking rising underlying fragility and unresolved directional conviction.

- Options markets continue to price elevated downside convexity, signalling that tail-risk demand remains firm despite improving spot and derivatives positioning.

- Volatility risk is being deferred rather than resolved, leaving the market vulnerable to abrupt repricing once liquidity conditions shift.

- Institutional balance-sheet flows have stabilised following a full de-risking cycle, but accumulation remains uneven and event-driven rather than structurally persistent.

- Spot market behaviour has turned constructive, with Binance and aggregate exchange flows transitioning into buy-dominant regimes while Coinbase sell pressure has materially eased.

- The recent push into the $96K region was mechanically driven by a derivatives-led short squeeze on comparatively thin futures volume.

- Long-term holder distribution has slowed, with cost-basis clusters and confidence bands forming a developing structural price floor.

- Broader market direction remains increasingly dependent on liquidity conditions and derivatives positioning until persistent spot accumulation re-emerges.

On-chain Insight

Overhead Supply Test

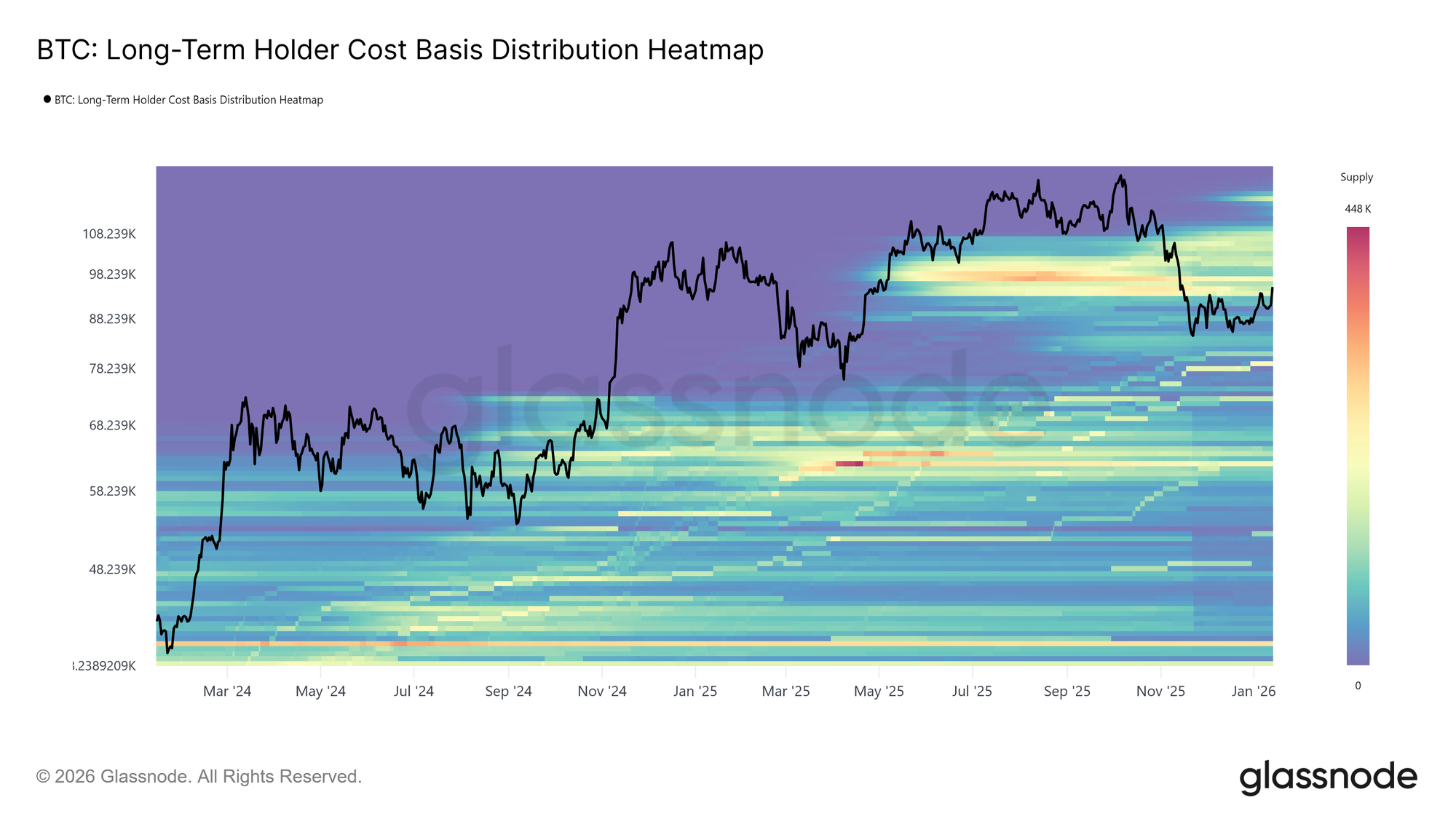

Bitcoin has entered the new year with constructive momentum, posting two consecutive higher highs and extending price to $95.6k. This early-year advance, however, has carried price directly into a historically significant supply zone. The current market level sits within a dense cluster of Long-Term Holder supply accumulated between April and July 2025, a period marked by sustained distribution near cycle highs.

As shown by the Long-Term Holder Cost Basis Distribution Heatmap, rebounds since November 2025 have repeatedly stalled at the lower boundary of this cluster, spanning approximately $93k to $110k. Each attempt higher has encountered renewed sell-side pressure, preventing price from sustaining a structural recovery.

This region has consistently acted as a transition barrier, separating corrective phases from durable bull regimes. With price once again pressing into this overhead supply, the market now faces a familiar test of resilience, where absorbing long-term holder distribution remains a prerequisite for any broader trend reversal.

Confidence at Cost Basis

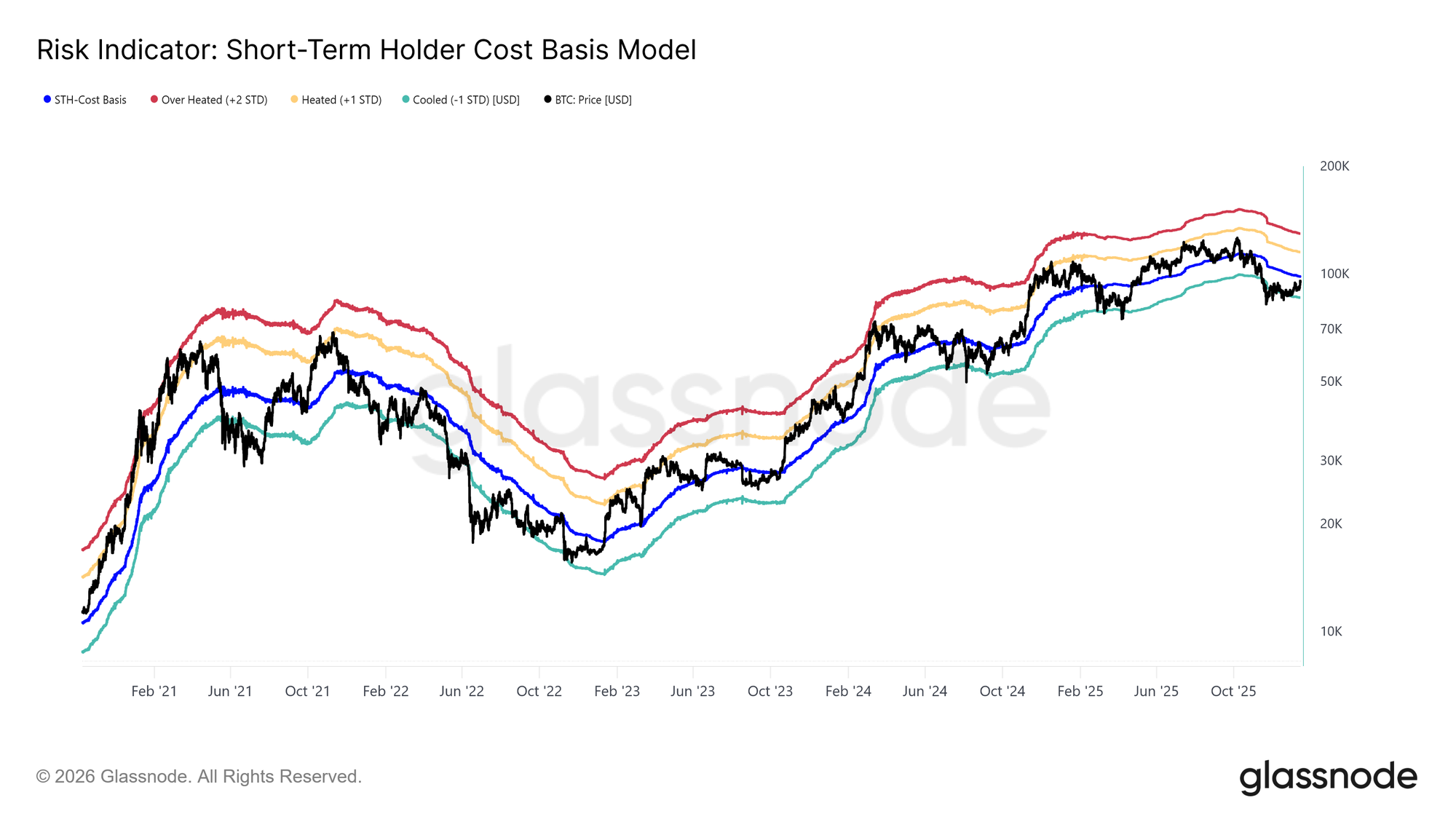

Facing renewed sell-side pressure from top buyers, attention shifts toward the Short-Term Holder cost basis, currently situated at $98.3k. This level represents the aggregate entry price of recent investors and serves as a critical gauge of market confidence. Sustained trading above this threshold would indicate that new demand is absorbing overhead supply, allowing recent buyers to remain profitable.

Historically, reclaiming and holding above the Short-Term Holder cost basis has marked the transition from corrective phases into more durable uptrends. Conversely, repeated failure to stabilize above this level risks reinforcing defensive behaviour among newer participants. As such, the ability of price to consolidate above $98.3k remains a necessary condition for restoring confidence in trend continuation and establishing the foundations for a sustainable rally.

LTH Distribution Slows

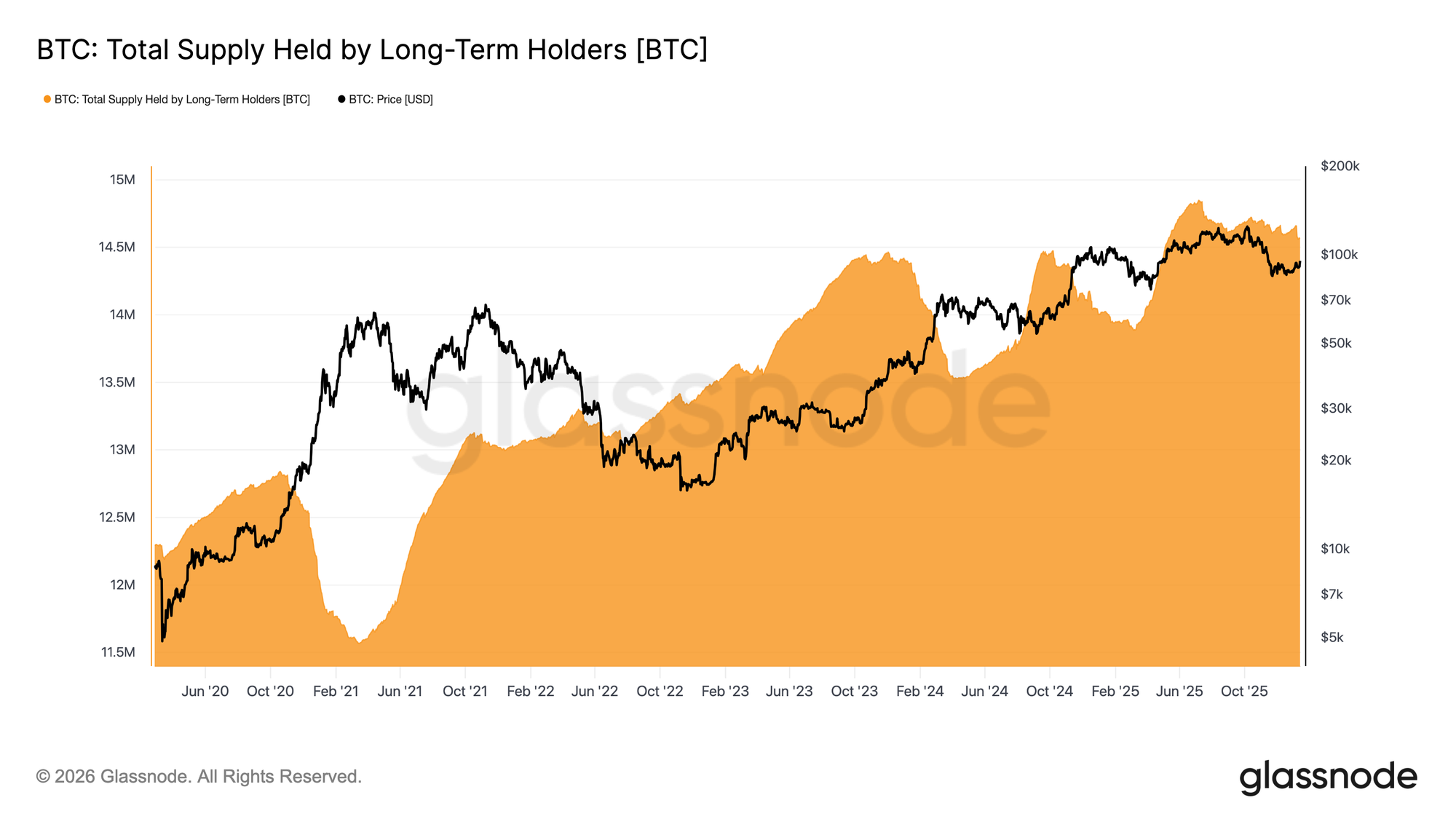

With price pressing into long-term holder supply, focus shifts to whether these investors are accelerating distribution or beginning to ease sell-side pressure. One useful gauge is the Total Supply Held by Long-Term Holders, which reflects the balance between coins maturing beyond the ~155-day threshold and coins being spent.

Currently, Long-Term Holder supply continues to trend lower, but the rate of decline has slowed materially compared to the aggressive distribution seen throughout Q3 and Q4 2025. This indicates that long-term holders remain net sellers, though their selling intensity is moderating.

For a sustainable rally to emerge, the market must transition into a regime where maturation supply outpaces long-term holder spending. Such a shift would push LTH supply higher, a structure last observed during Aug 2022–Sep 2023 and Mar 2024–Jul 2025, both periods that preceded stronger and more durable trend recoveries.

Demand Versus Distribution

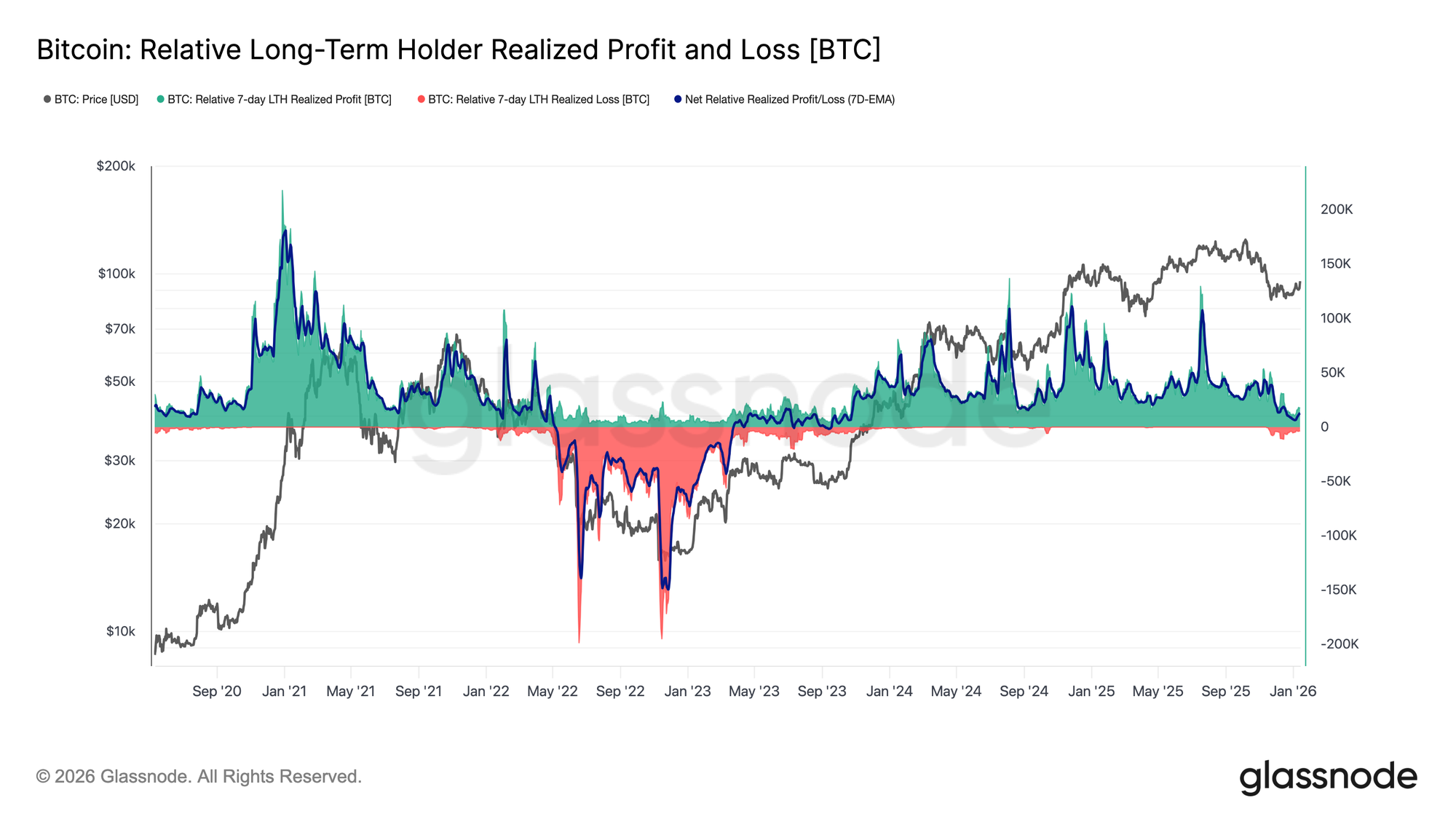

All in all, long-term holders who accumulated during Q2 2025 remain the most likely source of sell-side pressure should price decisively cut through the upper supply cluster. Their behaviour is well captured by the Net Realized Profit and Loss of Long-Term Holders, which currently reflects a markedly cooler distribution regime.

At present, long-term holders are realizing approximately 12.8k BTC per week in net profit, a substantial slowdown compared to the cycle peaks above 100k BTC per week. This moderation suggests profit-taking remains active, but far less aggressive than during prior distribution phases.

What follows will depend primarily on the demand side’s ability to absorb this supply, particularly from investors accumulated over Q2 2025. Failure to hold above the True Market Mean at ~$81k, in the long term, would significantly increase the risk of a deeper capitulation phase, reminiscent of the April 2022 to April 2023 period.

Off-Chain Insights

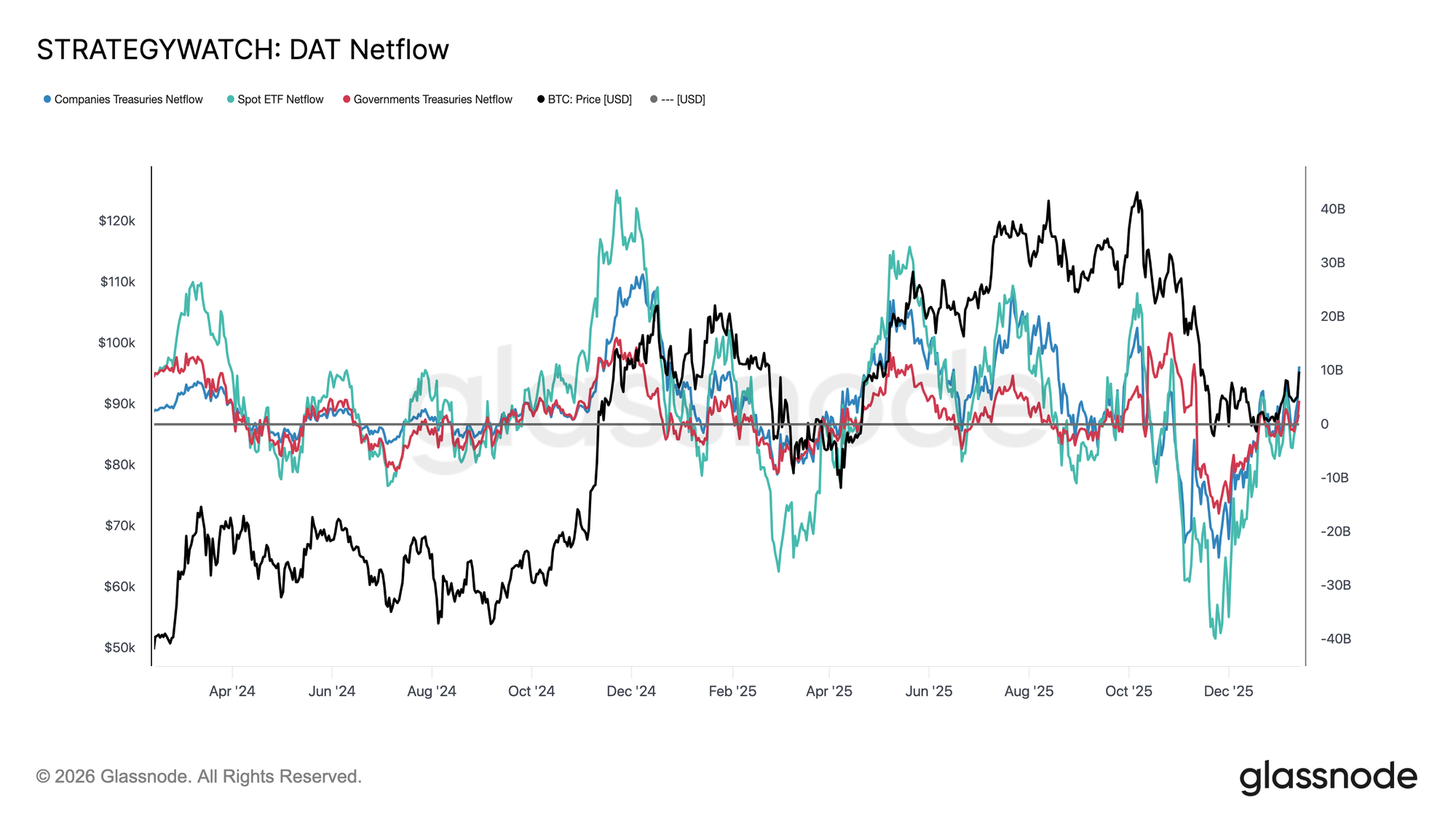

Institutional Flow Resets

Institutional balance-sheet flows have gone through a full reset over the past few months. After a prolonged period of heavy outflows across spot ETFs, corporates, and sovereign entities, netflows have now stabilised, marking a clear exhaustion of sell-side pressure from long-term structural holders.

Spot ETFs have been the first to turn, moving back into positive territory and re-establishing themselves as the primary marginal buyer. Since their inception, Spot ETFs have played a major role in every expansion phase, and their renewed inflows suggest that real-money allocators are once again beginning to rebuild exposure rather than simply trading volatility.

Corporate and sovereign treasury flows have also flattened out, with inflows appearing sporadically around consolidation phases. However, accumulation remains uneven and event-driven rather than consistent.

In this environment, balance-sheet demand is acting more as a price stabiliser than a growth engine, leaving near-term direction increasingly sensitive to derivatives positioning and short-term liquidity conditions.

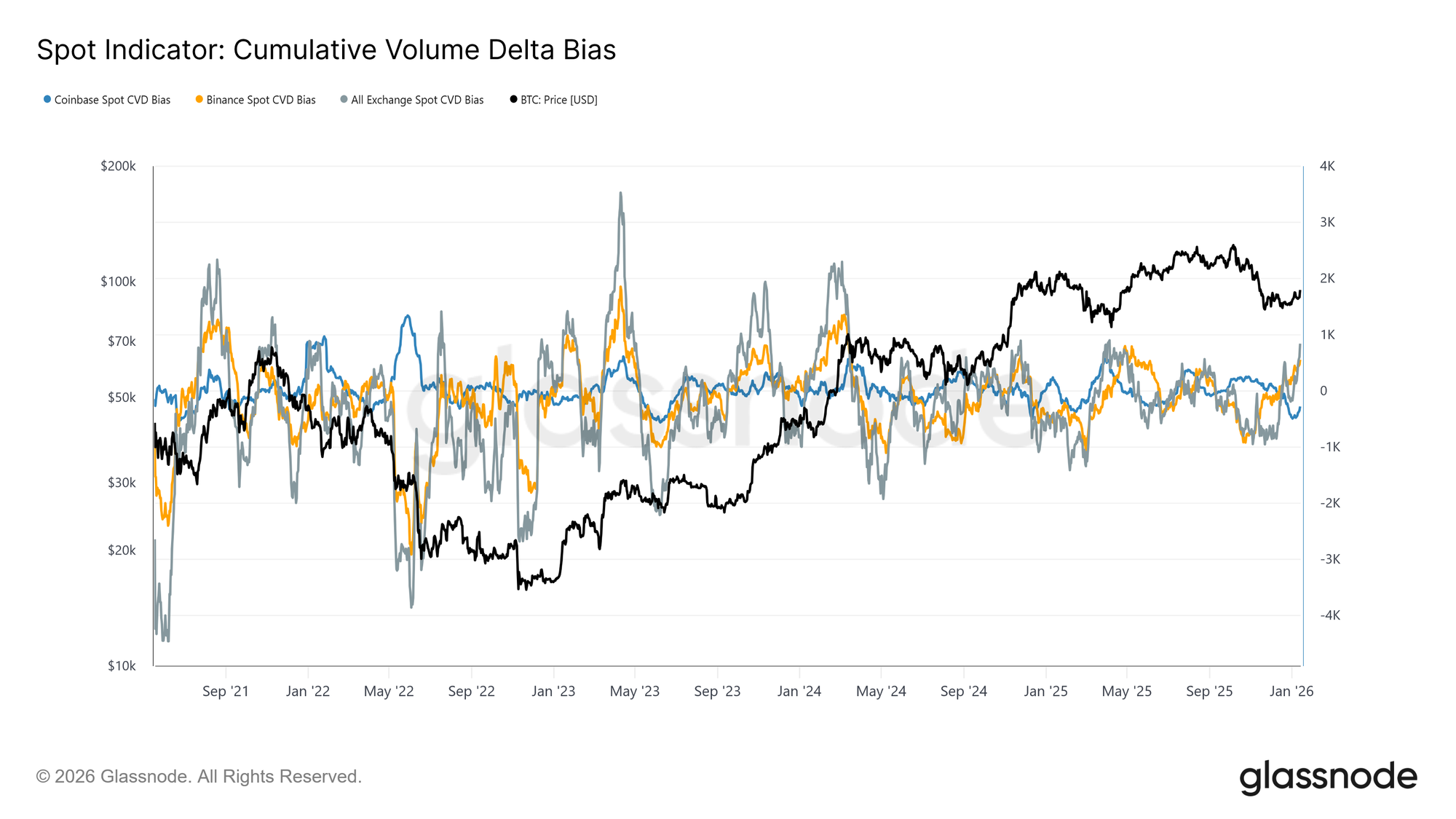

Spot Flows Turn Constructive

Spot market behaviour has begun to improve following the recent drawdown, with Binance and aggregate exchange CVD measures transitioning back into a buy-dominant regime. This reflects a shift away from persistent sell-side pressure and signals that market participants are once again absorbing supply rather than distributing into strength.

At the same time, Coinbase, which has been the most consistent source of sell-side aggression throughout the consolidation, has meaningfully slowed its selling activity. The easing of Coinbase-led distribution has removed a key source of overhead supply, helping to stabilise price and clear the way for the ongoing rally.

While spot participation is not yet displaying the persistent, aggressive accumulation typically seen during full trend expansion phases, the transition back into a net-buying posture across major venues represents a constructive structural shift.

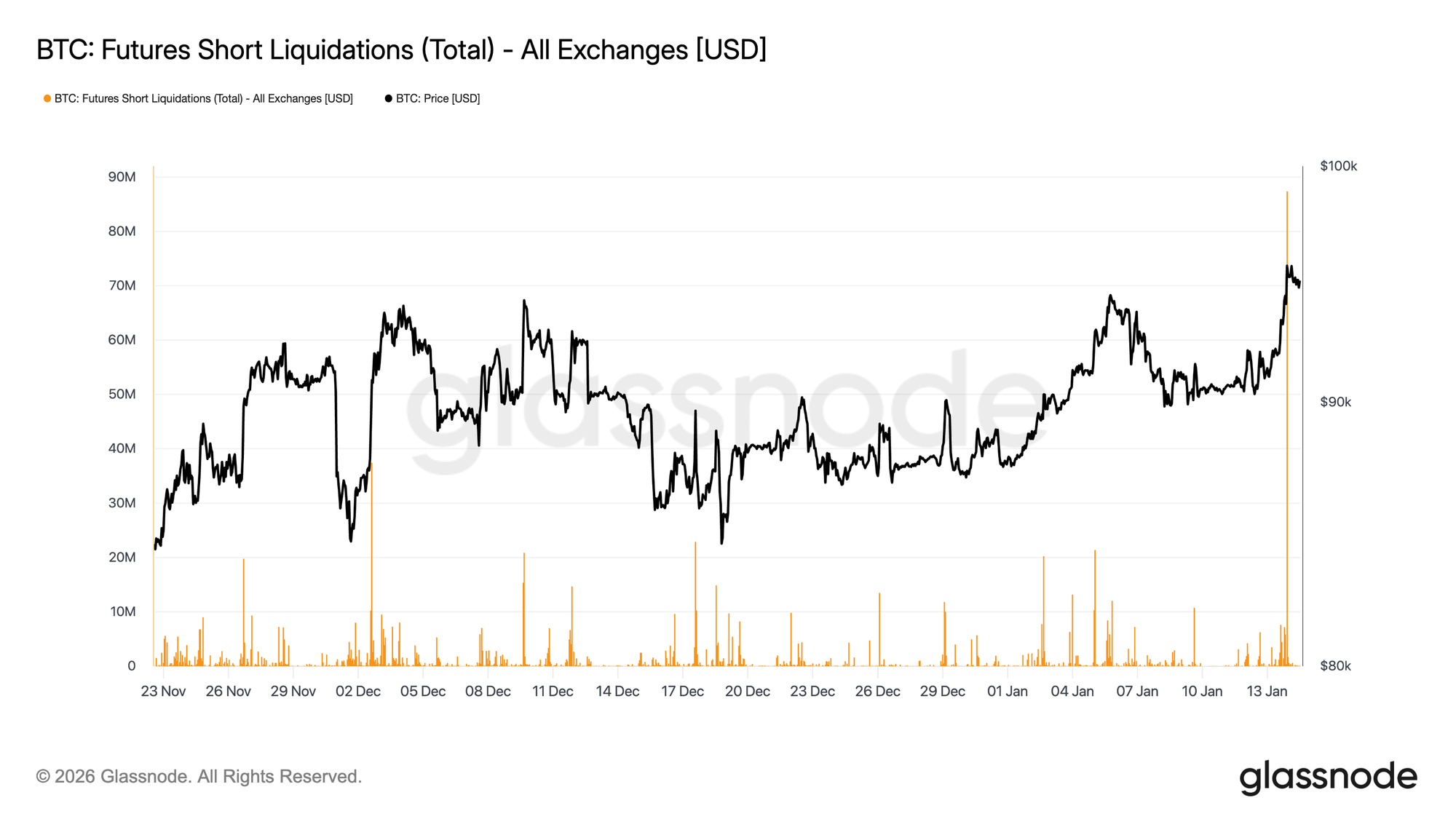

Futures Traders Squeeze Shorts

While the push into the $96K region was mechanically reinforced by short liquidations, it also unfolded on relatively thin derivatives volume. Futures turnover has remained well below the elevated activity seen throughout most of 2025, even as prices reclaimed higher levels.

This indicates that the breakout occurred in a comparatively light liquidity environment, where modest positioning shifts were able to drive disproportionately large price responses. In practical terms, it did not take significant new capital to force shorts out of the market and lift price through resistance.

This leaves the market reliant on whether spot demand and sustained volume can now step in to support continuation, or whether the rally risks fading once the mechanical buying pressure from forced covering is exhausted.

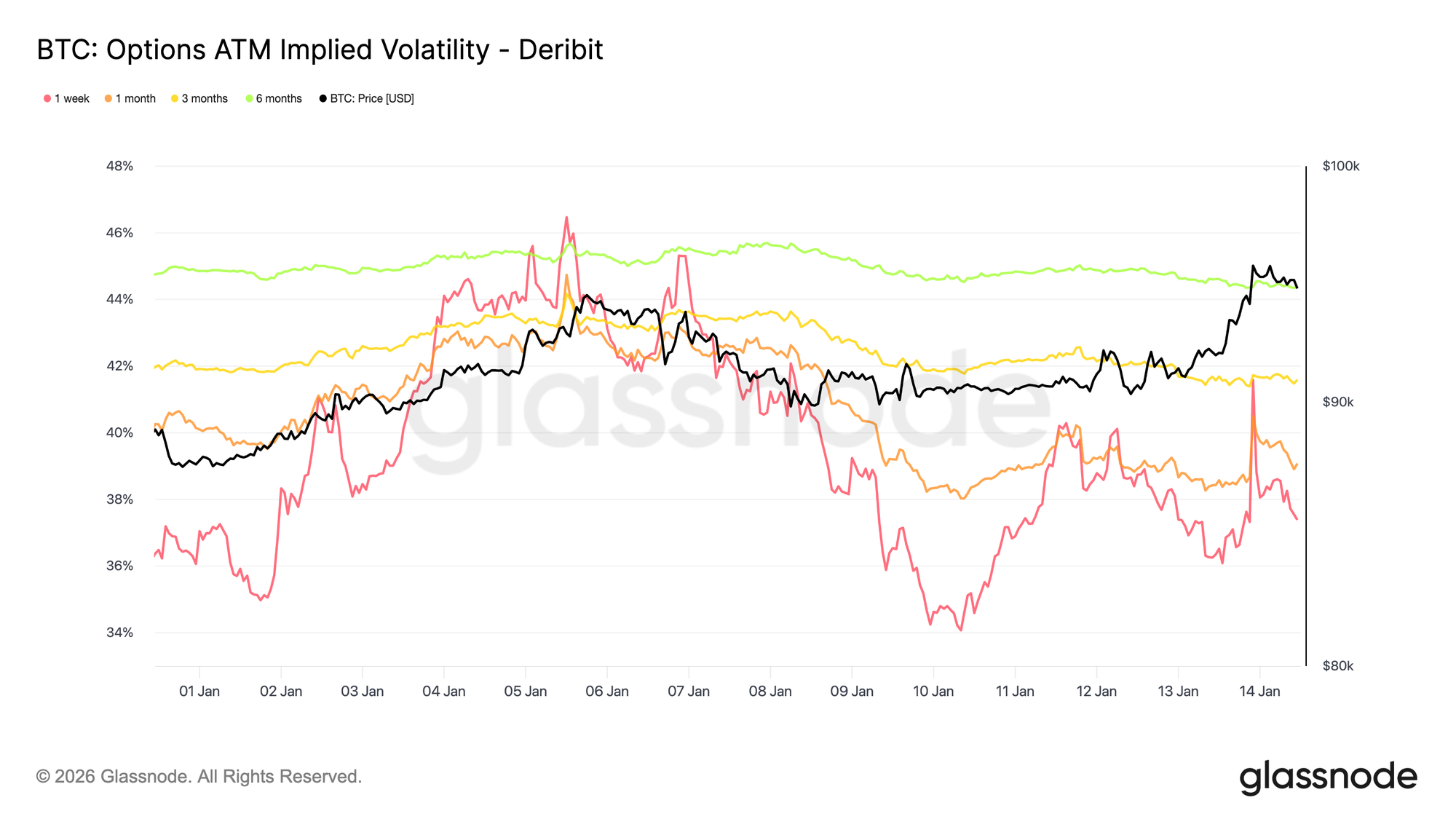

Low Volatility, Unresolved Risk

Implied volatility remains low across the curve, reinforcing the calm observed in recent price action. Longer-dated maturities have been drifting modestly lower, while short-dated implied volatility reacts more directly to spot moves. Those front-end reactions, however, fail to propagate up the curve, indicating limited demand for near-term convexity.

This is not a signal that uncertainty has disappeared. Rather, it suggests that risk is being deferred. The options market is not expressing confidence, but a view that any meaningful repricing is more likely to occur later than immediately.

Volatility increases gradually with maturity, pointing to uncertainty being assigned to time rather than to a specific near-term catalyst. The term structure is adjusting in level, not shape, consistent with a market that expects short-term stability while remaining exposed to latent risk.

This matters because volatility suppressed by positioning rather than clarity tends to reprice abruptly when conditions change.

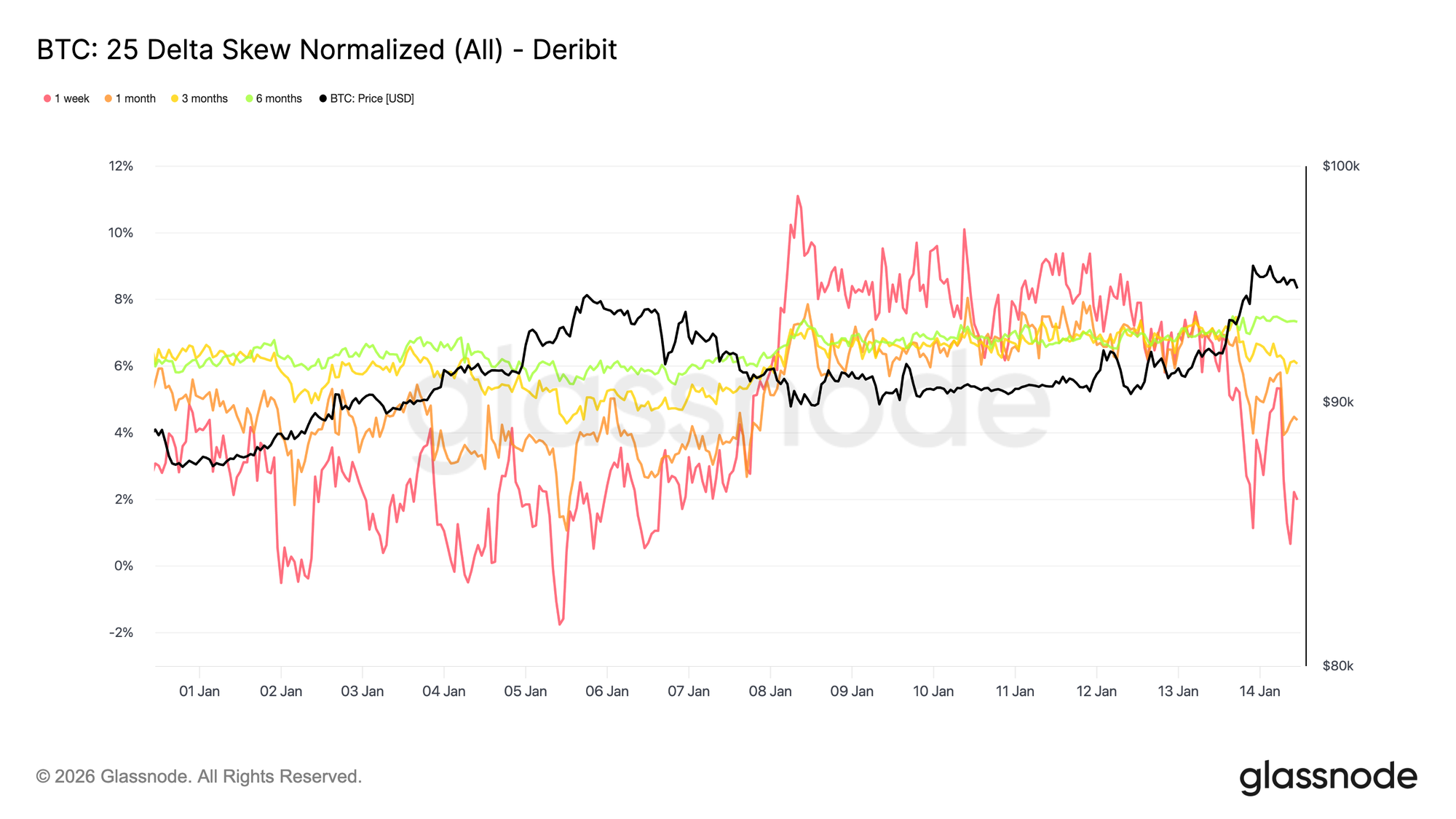

Downside Asymmetry Remains Firmly Priced

While overall volatility remains low, skew continues to price downside risk. The 25 delta skew stays biased toward puts, particularly in mid and longer maturities, pointing to persistent demand for longer-dated downside protection even as spot stabilizes and reclaims the 95K level.

This reflects a market that is comfortable carrying exposure but unwilling to do so without insurance. Protection is being maintained rather than aggressively added, signaling caution rather than stress. Short-dated skew briefly moved toward balance before rotating back in favor of puts, while longer-dated skew has shown little reaction to the move back above 95K.

The coexistence of low volatility and negative skew highlights a key tension. Participants are not positioning for immediate downside, but they continue to pay for asymmetric protection.

That combination is typical of range-bound markets where risks are acknowledged but not expected to materialize immediately.

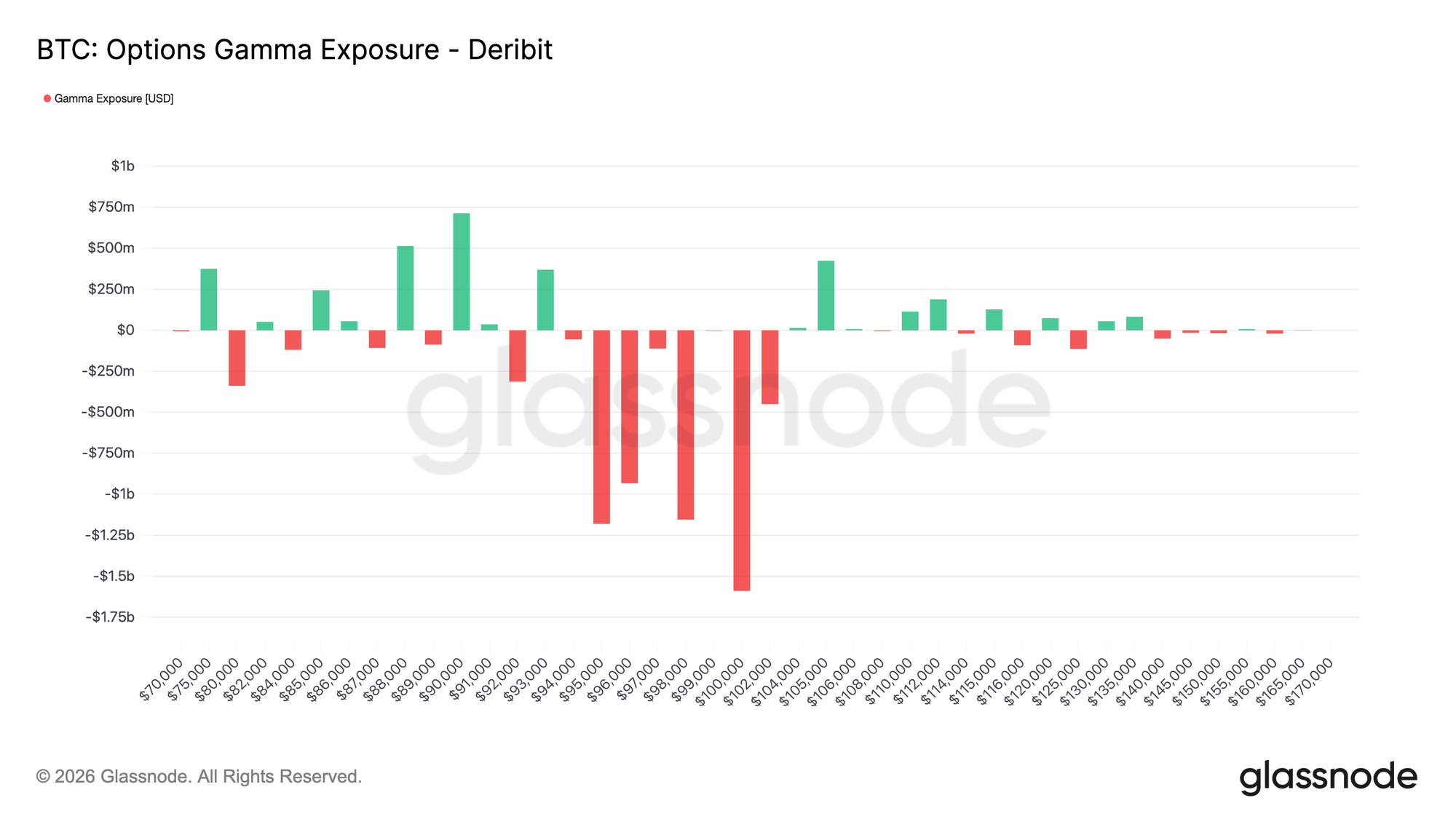

Short Gamma and Fragile Stability

The current strike distribution places dealers short gamma around spot, altering the market’s short-term dynamics. In a short gamma environment, hedging flows no longer absorb price moves. Instead, they tend to reinforce them, with dealers buying into rising prices and selling into declines.

With spot trading around the 95–96K area at the time of writing, price has moved into a short gamma zone that extends roughly from 94K to 104K. Within this range, sustained price action supported by volume is more likely to trigger directional hedging flows, increasing the potential for faster movement toward nearby high-interest strikes, including the 100K level.

This structure creates a fragile form of stability. Volatility can remain low while price is contained, but once momentum develops, moves are more likely to accelerate than fade. In this context, calm price behavior reflects positioning rather than balance, leaving the market more exposed to abrupt repricing than gradual adjustment.

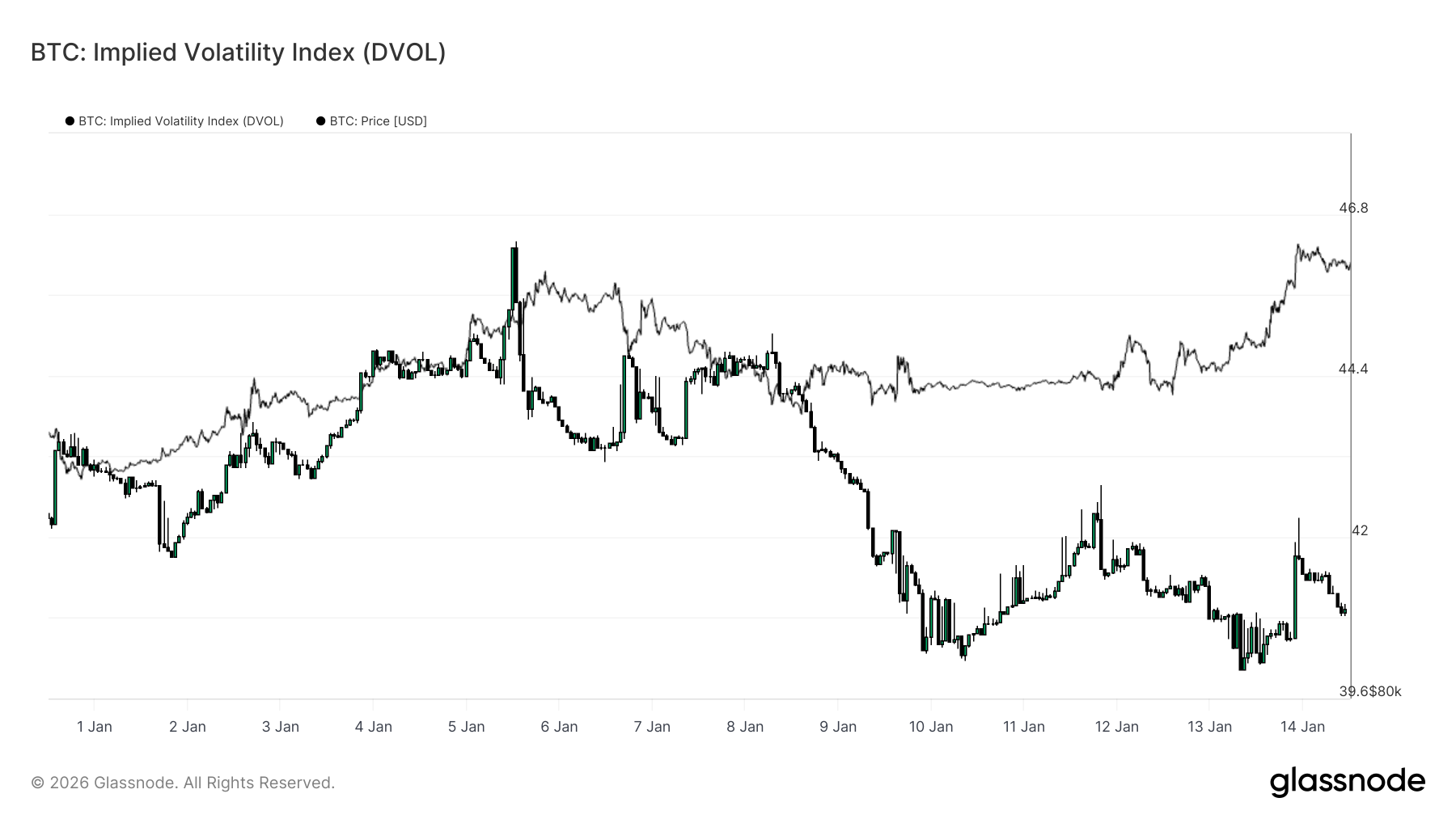

DVOL Confirms Volatility Is Being Deferred

The Implied Volatility Index (DVOL) provides a surface-wide view of option-implied uncertainty by aggregating volatility across strikes and maturities. Unlike at-the-money implied volatility, which reflects pricing at a specific point on the curve, DVOL captures how much volatility the market is embedding overall.

At present, DVOL remains relatively low and range-bound, even as spot has moved through key levels. This confirms what the term structure and skew already suggest: the options market is not paying up for immediate volatility. Uncertainty is acknowledged, but it is not being expressed through higher aggregate volatility pricing.

Importantly, this low DVOL reading coincides with downside-biased skew and short gamma positioning near spot. Volatility is therefore not being compressed by stabilizing hedging flows, but simply deferred at the surface level. This combination creates conditions where volatility can remain dormant, yet reprice sharply once a catalyst forces positioning to adjust.

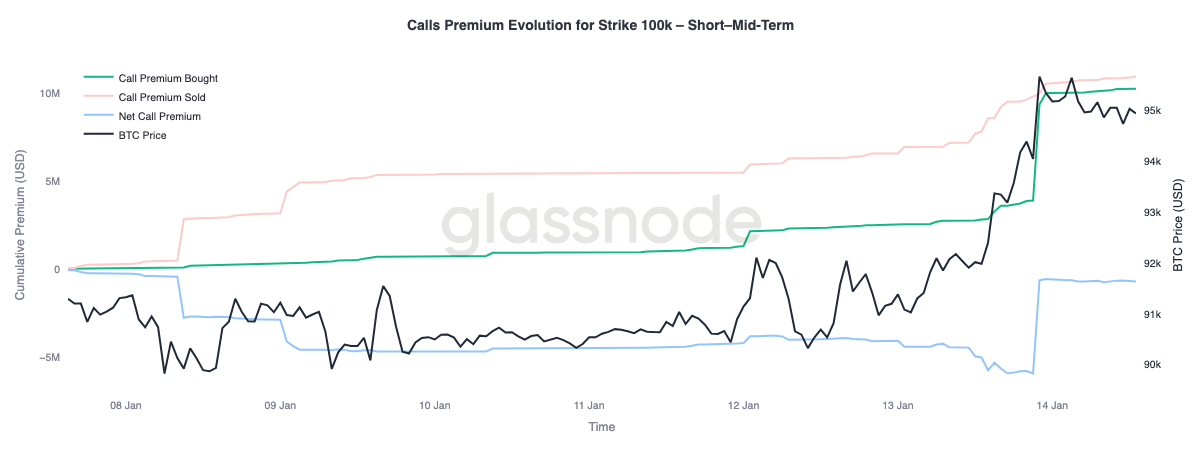

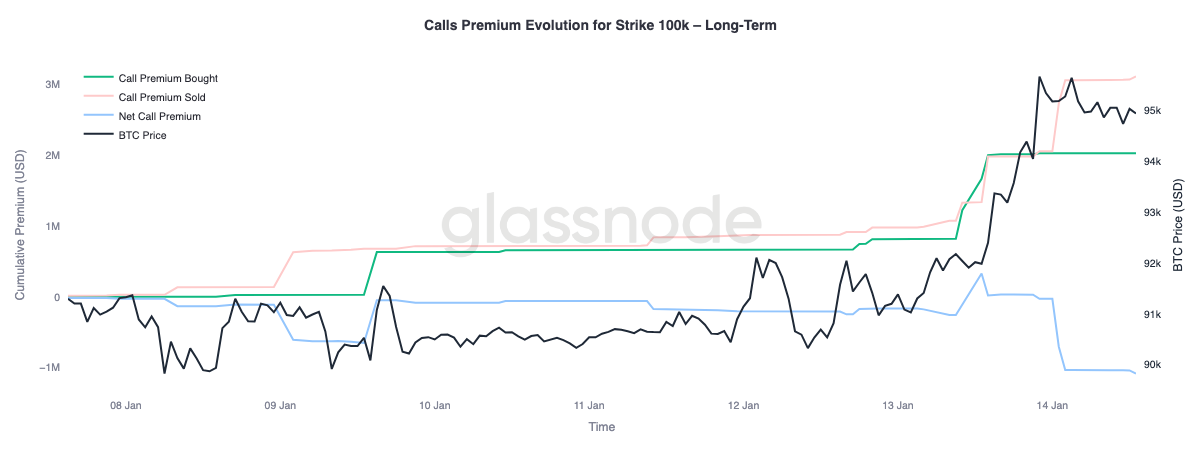

Call Premium Signals Conditional Upside

A closer look at the premium behavior of the 100K call strike highlights a clear divergence across maturities. This level remains the next major psychological threshold, and option flows show how the market is positioning around it.

In short to mid-term maturities, up to roughly three months, call premium bought has significantly outweighed call premium sold. This imbalance has driven net call premium higher, indicating active demand for near-dated upside exposure as spot approaches the level. In contrast, longer-dated maturities show the opposite behavior. As spot rallied, richer call premiums further out the curve were used as opportunities to sell upside.

This split suggests the market is positioning for a potential retest of the 100K area, while simultaneously expressing hesitation about sustained acceptance above that level over longer horizons. Upside is being targeted tactically in the near term, but monetized at longer maturities.

Conclusion

Bitcoin has entered a transitional phase marked by stabilising structural flows, improving spot behaviour, and a derivatives complex still shaped by deferred volatility risk. Long-term holder distribution has slowed, institutional balance-sheet flows have stabilised, and spot markets have begun to shift back into buy-dominant regimes, suggesting that much of the late-2025 sell-side pressure has now been absorbed.

However, the recent move into the $96K region was driven more by mechanical positioning dynamics than broad-based organic demand. Futures liquidity remains thin, and spot participation, while improving, has yet to show the persistent accumulation typically seen during full trend expansion.

Looking ahead to Q1, the underlying setup appears increasingly constructive. With sell pressure easing and volatility risk deferred rather than discharged, relatively modest inflows may once again generate outsized price responses. If spot accumulation and ETF-led institutional demand continue to rebuild, the current consolidation phase may serve as a base for renewed trend expansion.