Three Fallen Banks

After one of the most consequential weeks of 2023, the digital asset industry is short three crypto friendly banking institutions in the US. However the principle investor response thus far appears to be a seeking safety in the most trustless major assets BTC and ETH.

The last week has shaped up to be one of the fastest paced, and certainly most consequential for the digital asset space in 2023. In just a few short days, three primary banking institutions in the US, all of which serviced firms within the industry, entered voluntary liquidation, or were taken into receivership by US regulators.

- Silvergate (SI) announced intent to voluntarily wind down on 8-Mar, in what is expected to be an orderly manner, and returning capital in full to depositors.

- Silicon Valley Bank (SIVB), the 16th largest US bank, was closed and put into receivership by FDIC on 12-March, making the $209B bank failure the second largest in US history.

- Signature Bank New York (SBNY) has also been closed as of 12-Mar, per a Federal Reserve announcement on the matter.

For all three institutions, it is expected that full deposits will be returned, whether by reserves held, or via FDIC and US regulators deposit guarantees. With many large digital asset firms, and stablecoin issuers using one, or multiple of these banking partners, the weekend turned out to be a volatile one. Of particular interest is Circle, issuer of USDC, who notified of some $3.3B in cash held at SVB, creating conditions for a temporary breaking of the $1 peg.

In this edition, we will focus on some of the key effects playing out on-chain, and within wider in market structure, including:

- De-pegging of several stablecoins from $1, as well as dominance shifting back towards Tether (USDT).

- Net capital outflows from the digital asset market, observable across both stablecoins, and the two majors, BTC and ETH.

- Cyclical lows hit in futures open interest, despite elevated trade volumes, and speculative interest leading to an explosive rally back to $22k for BTC, and $1.6k for ETH.

🪟 View all charts covered in this report in The Week On-chain Dashboard.

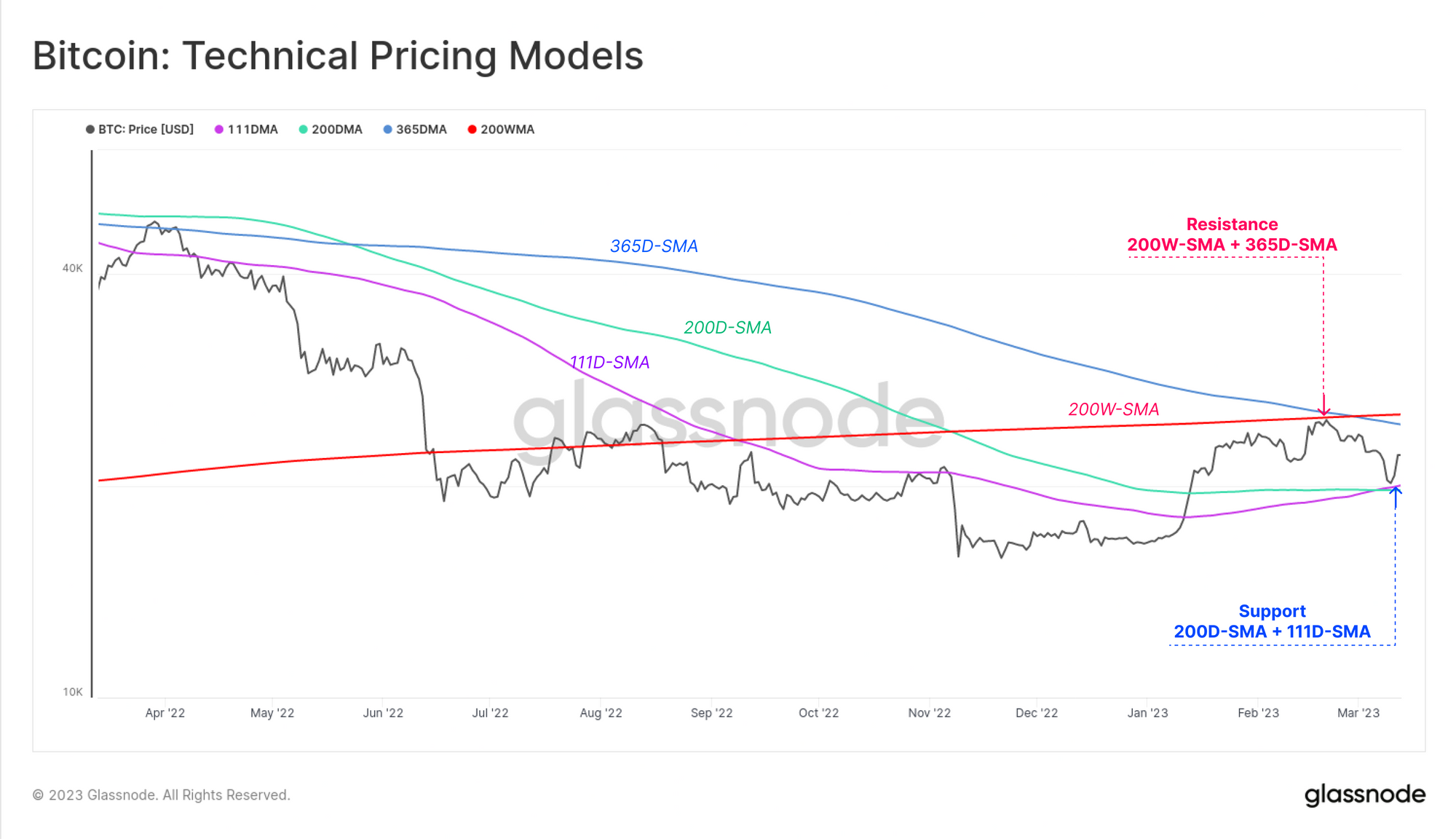

Bitcoin prices find themselves trading between several popular, and widely observed technical analysis pricing models. After finding resistance at the 200-week and 365-day moving average (~25.0k) in Feb, prices visited and then rallied off the 200-day and 111-day average (~$19.8k) this week.

Noting that this is the first cycle in history where BTC have traded below the 200-week MA, the market is in new territory from this perspective.

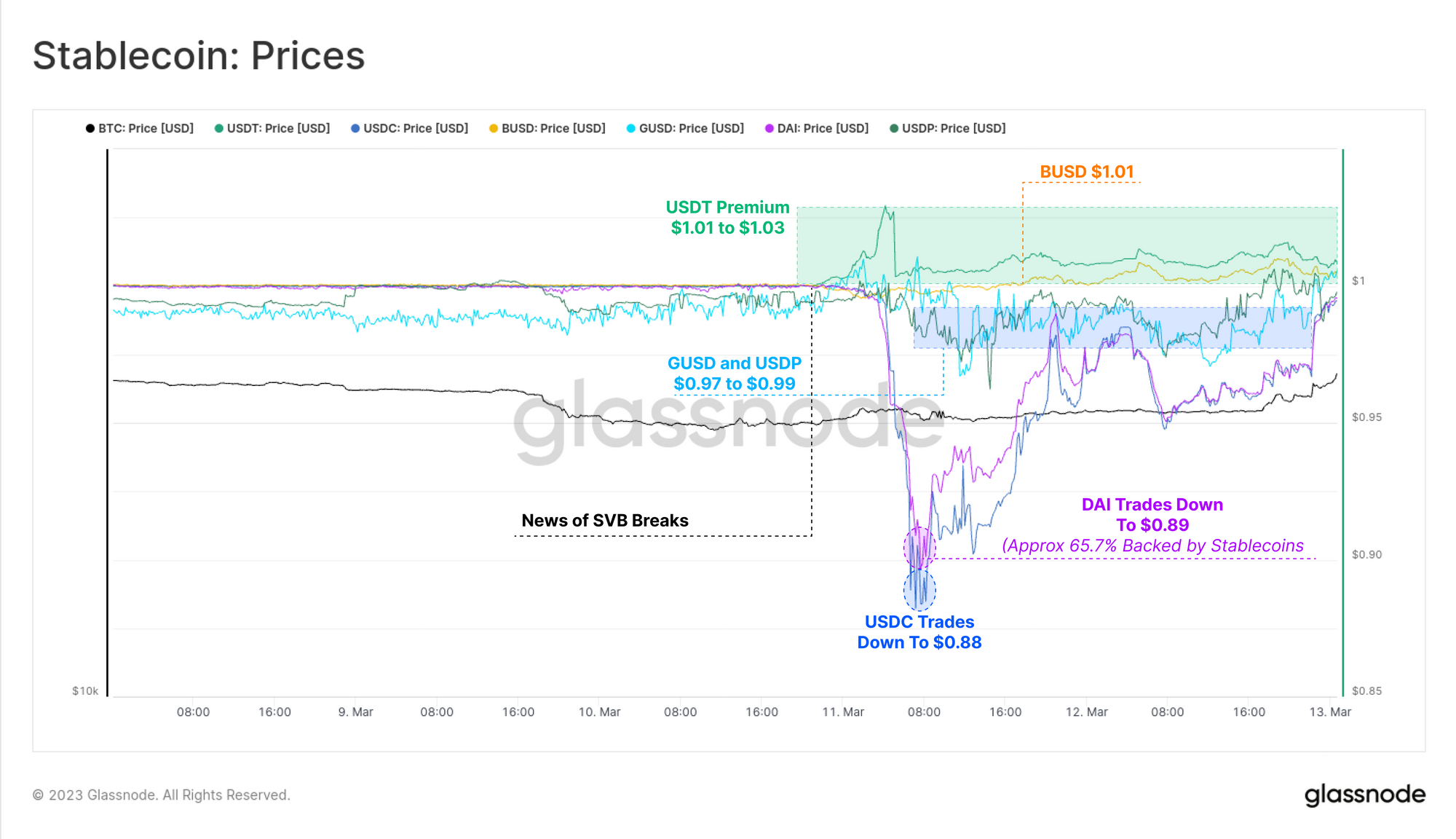

For the first time since the collapse of the LUNA-UST project, we have also seen volatility in stablecoin prices this week, driven by fears of USDC being partially un-backed. USDC traded down to a low of $0.88, followed closely by DAI at $0.89, with the latter a result DAI's approximately 65.7% backing by stablecoin collateral.

Both Gemini's GUSD, and Paxos' USDP deviated slightly below their $1 peg, whilst BUSD and Tether saw prices trade at a premium.

Tether in particular saw a premium emerge of between $1.01 and $1.03 for much of the weekend. It is somewhat ironic that Tether would be seen as a safe haven amidst fears of a wider contagion sourced from the heavily regulated US banking sector.

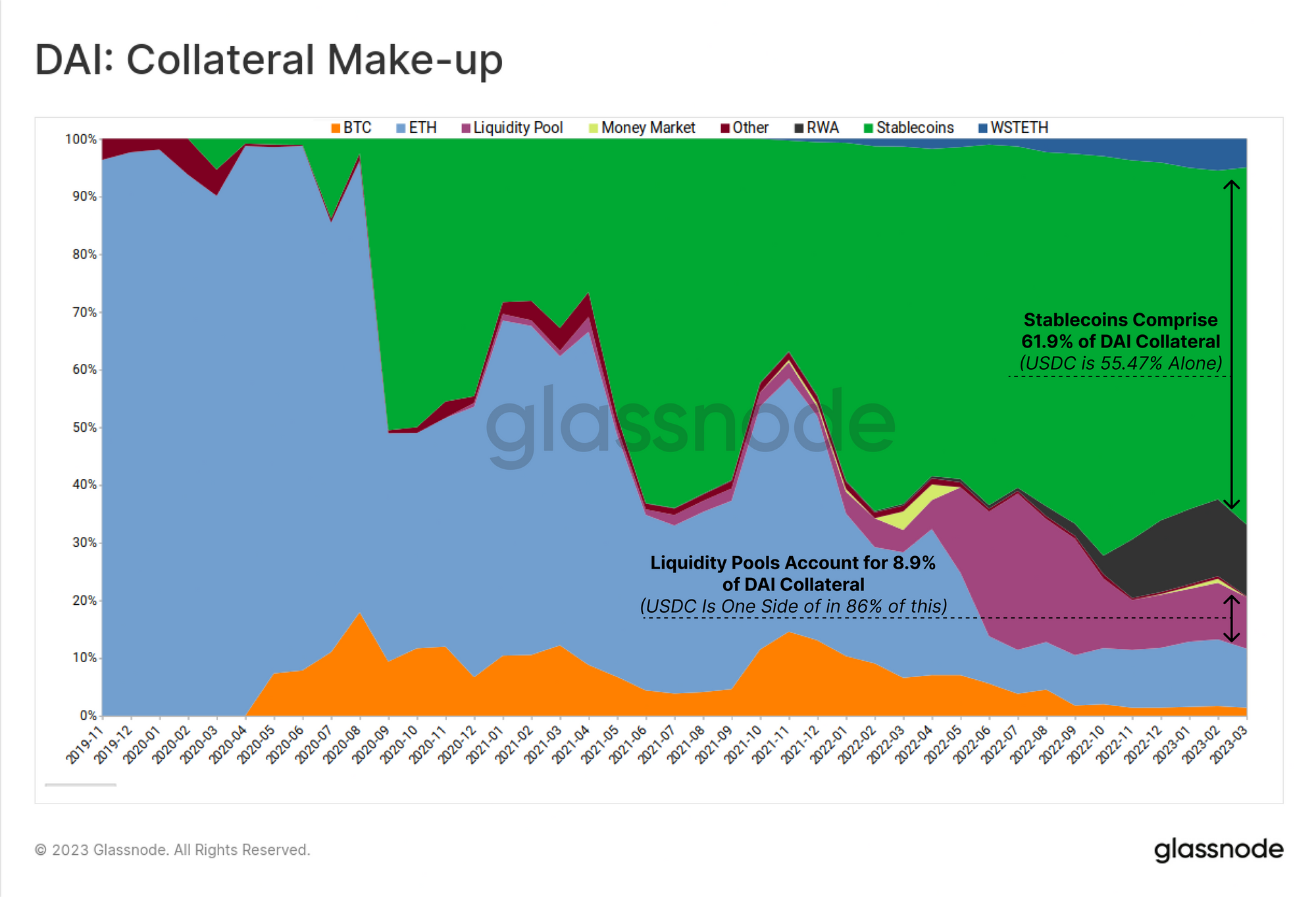

In the case of DAI, stablecoins have become the dominant form of collateral backing it, with this trend growing consistently since mid 2020. USDC accounts for approximately 55.5% of direct collateral, as well as a significant share of the various Uniswap liquidity positions used, in sum representing around 63% of all collateral.

This event certainly opens up discussions regarding longer-term implications for DAI, which is a purportedly decentralized stablecoin. This event however demonstrates how intimately linked DAI's price to the traditional banking system via the collateral mix (which also includes an additional 12.4% in tokenized real world assets).

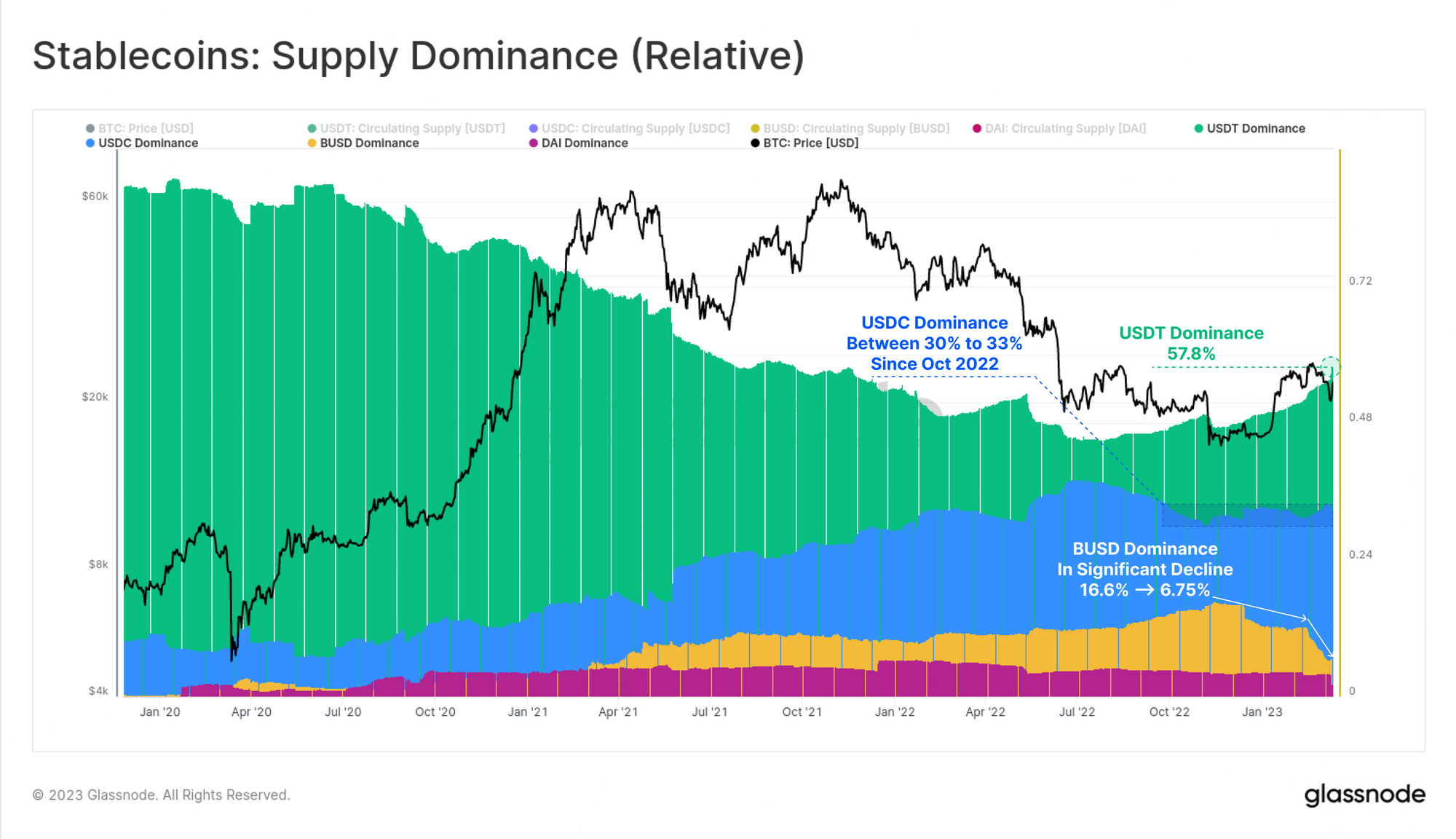

As we reported in mid-2022, Tether dominance within the stablecoin market had been in a structural decline since mid-2020. However, with recent regulatory moves against BUSD, and this week's concerns related to USDC, Tether dominance has climbed back above 57.8%.

USDC has maintained a dominance between 30% and 33% since October 2022, however it remains to be seen whether supply decreases as the redemption window re-opens on Monday. BUSD has seen a dramatic decline in recent months, with issuer Paxos ceasing new minting, and dominance falling from 16.6% in November, to just 6.8% today.

Aggregate Capital Outflows

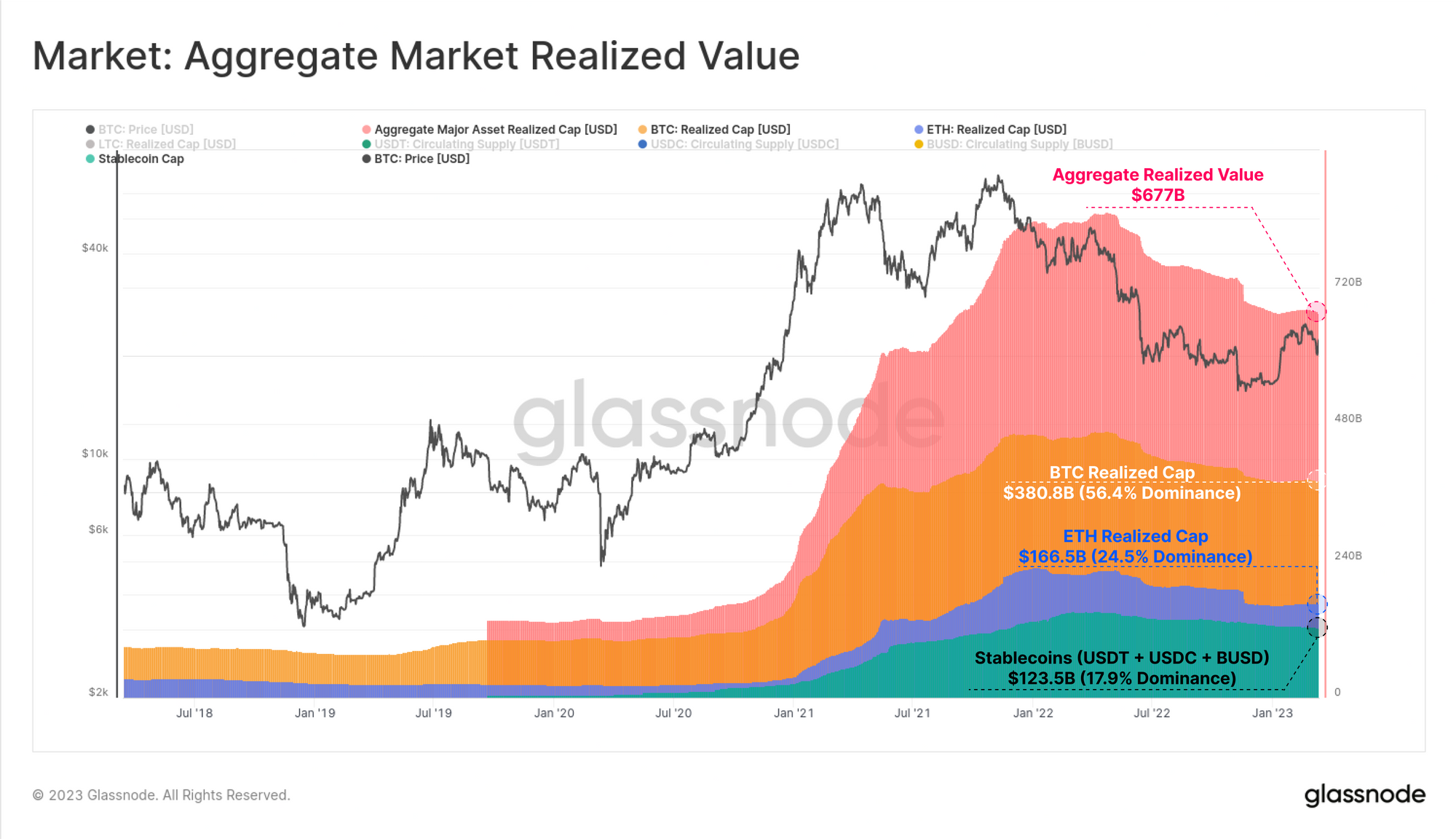

Estimation of the true capital inflows and outflows into the digital asset market can be tricky, however in most instances, capital initially flows in via the two majors (BTC and ETH), or via stablecoins. Thus, the combination of the Realized Cap for BTC and ETH, and the circulating supply of major stablecoins provides a fairly robust measure.

Here, we can see that the total market has a value of around $677B by this method, down around 20% from the ATH of $851B set one year ago. BTC commands a dominance of 56.4%, ETH of 24.5% and 17.9% in USDT, USDC, and BUSD, and the remaining 1.2% in LTC.

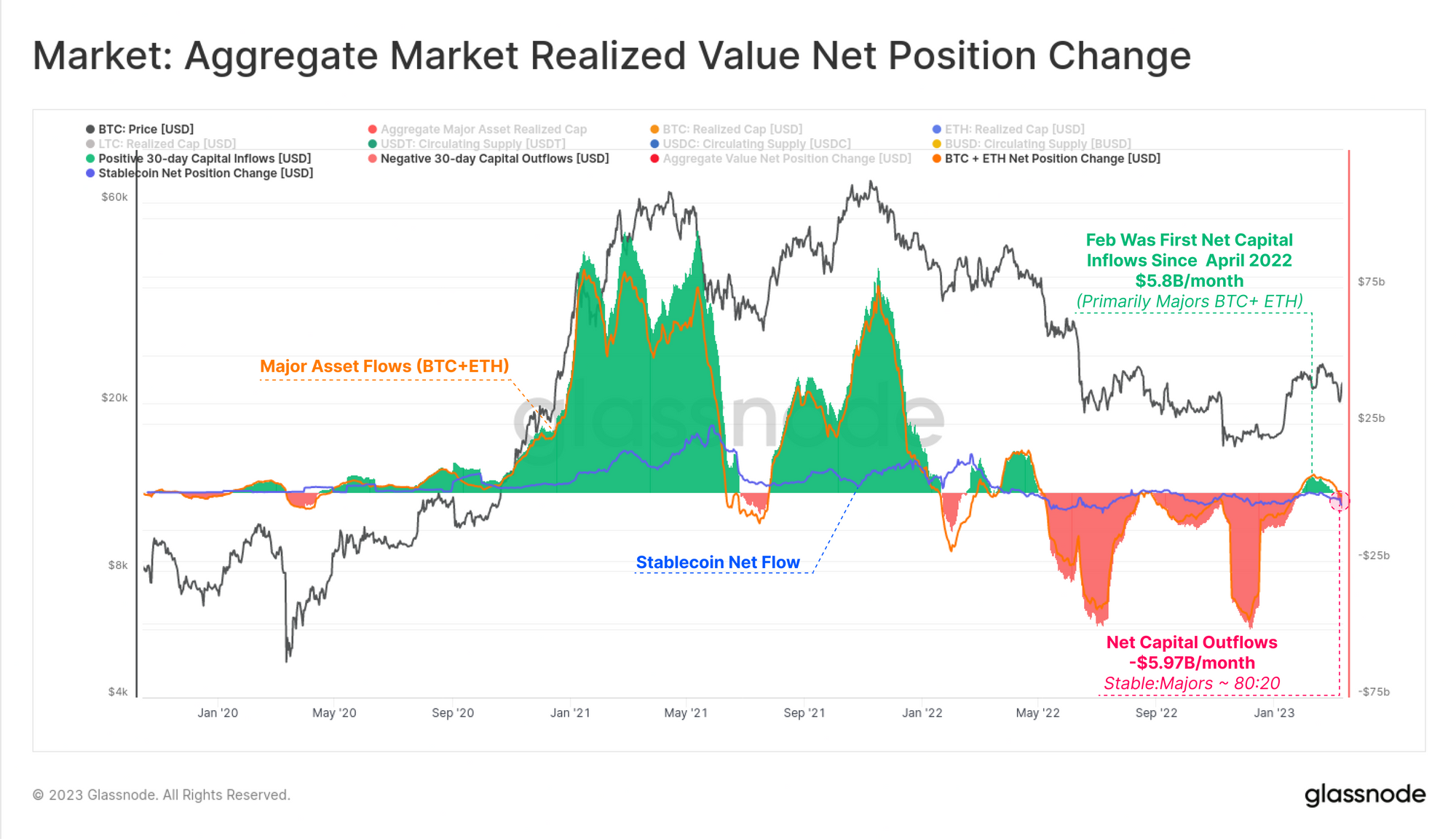

On a 30-day change basis, February was the first net capital inflow into the industry since April 2022, peaking at +$5.8B/month, and primarily led by BTC and ETH. The last month however, the market has seen a reversal outflow of -$5.97B, with 80% of that a result of stablecoin redemption (BUSD primarily), and 20% from realized losses across BTC and ETH.

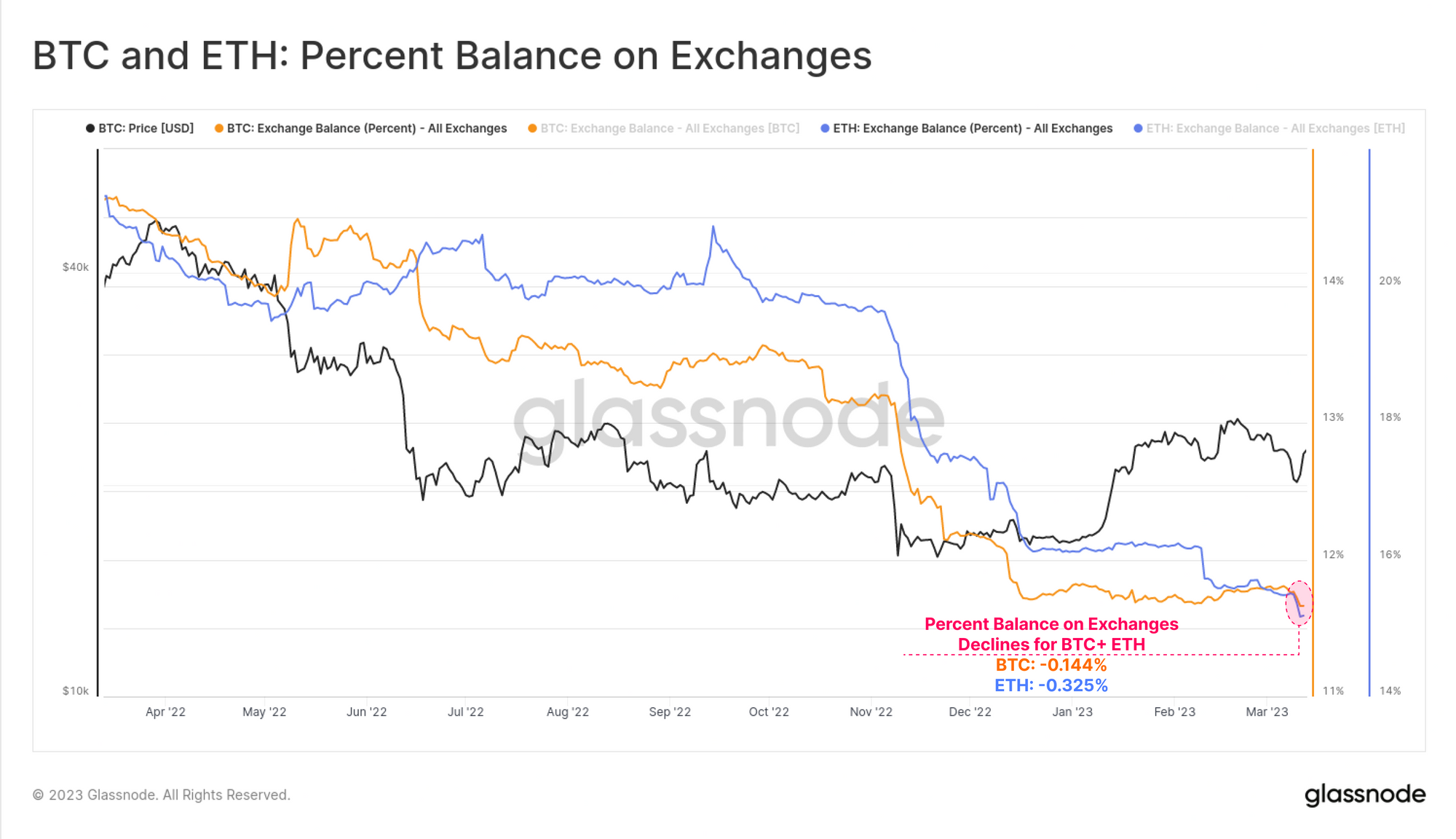

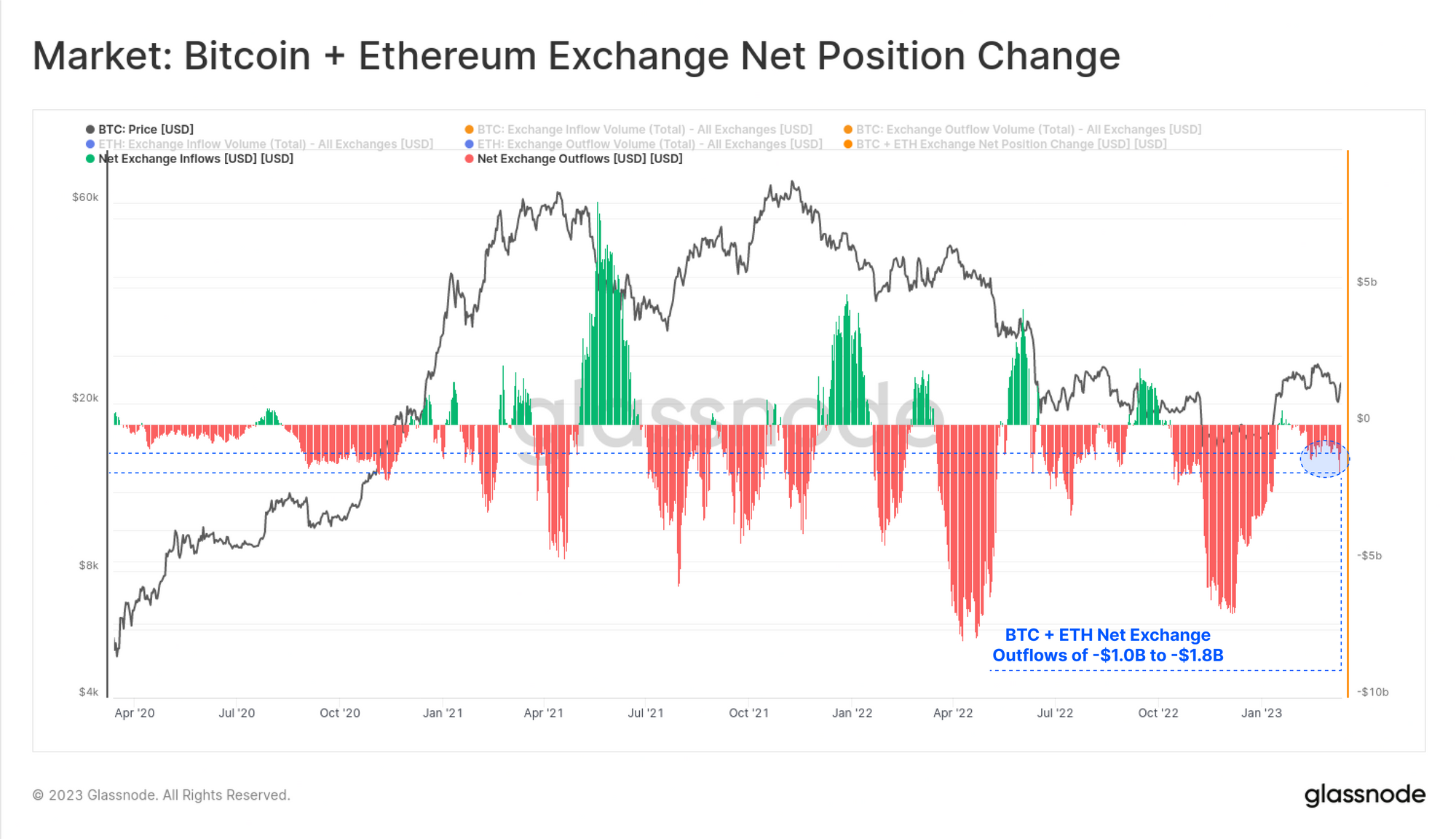

As the news of the Silicon Valley Bank failure hit, investors sought refuge in BTC and ETH, with notable outflows occurring across exchanges we monitor. Approximately 0.144% of all BTC, and 0.325% all ETH in circulation was withdrawn from exchange reserves, demonstrating a similar self-custody response pattern to the FTX collapse.

On a USD basis, the last month saw over $1.8B in combined BTC and ETH value flow out of exchanges. This is not necessarily large in relative scale, however observing net exchange withdrawals, especially within the current hostile regulatory environment, does speak to a degree of investor confidence that is worth noting.

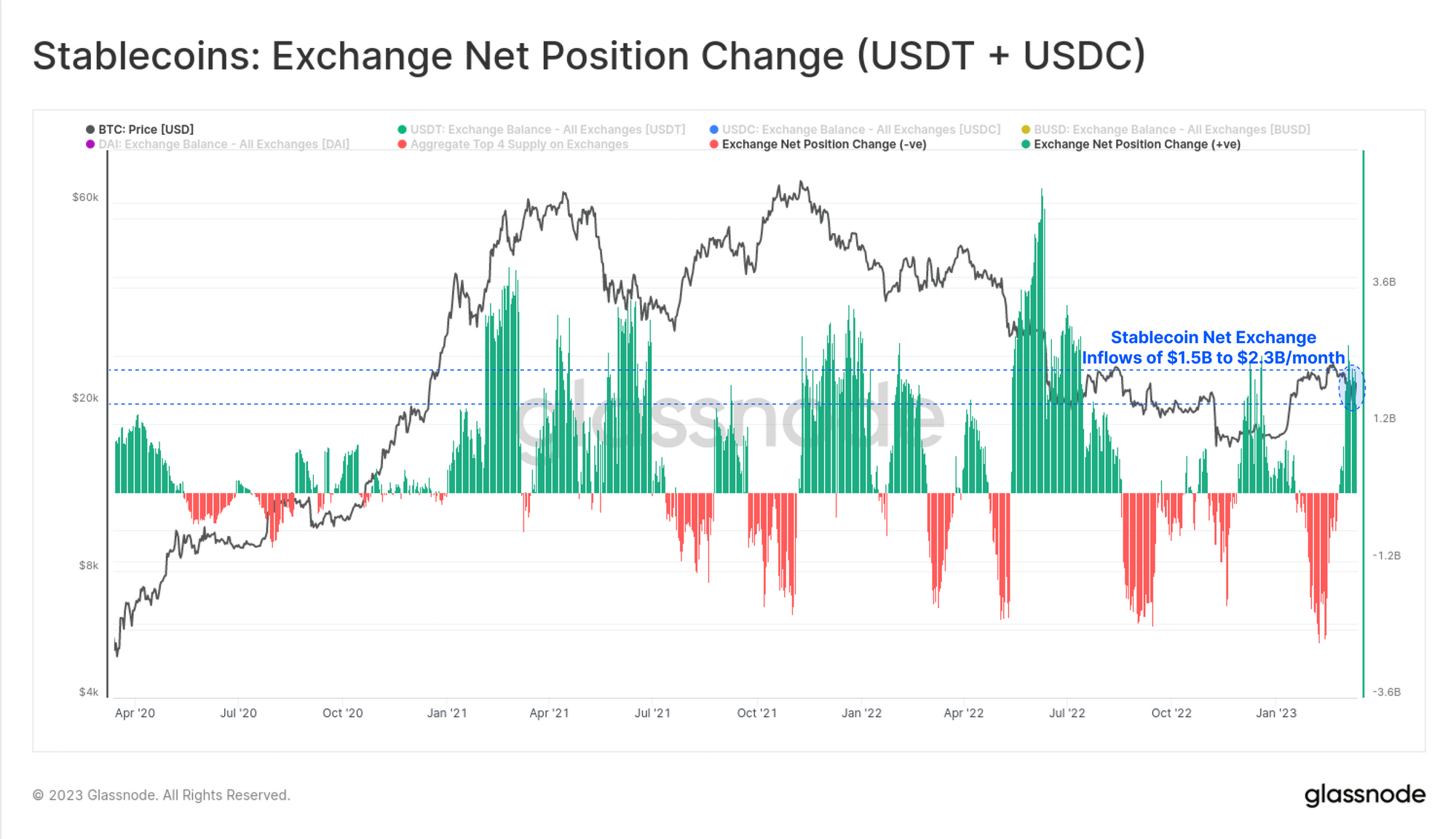

The two major stablecoins on the other hand have seen net inflows to exchanges on the order of $1.8B to $2.3B per month. It is important to note that this is more than counterbalanced by BUSD flowing out of exchanges at an eye-watering rate of -$6.8B/month. Thus it is likely that there is a degree of 'stablecoin switching' taking place.

However, overall, it appears to be a stablecoin in, BTC and ETH out response from the market, reflecting a remarkable appreciation for self-custody of trustless assets.

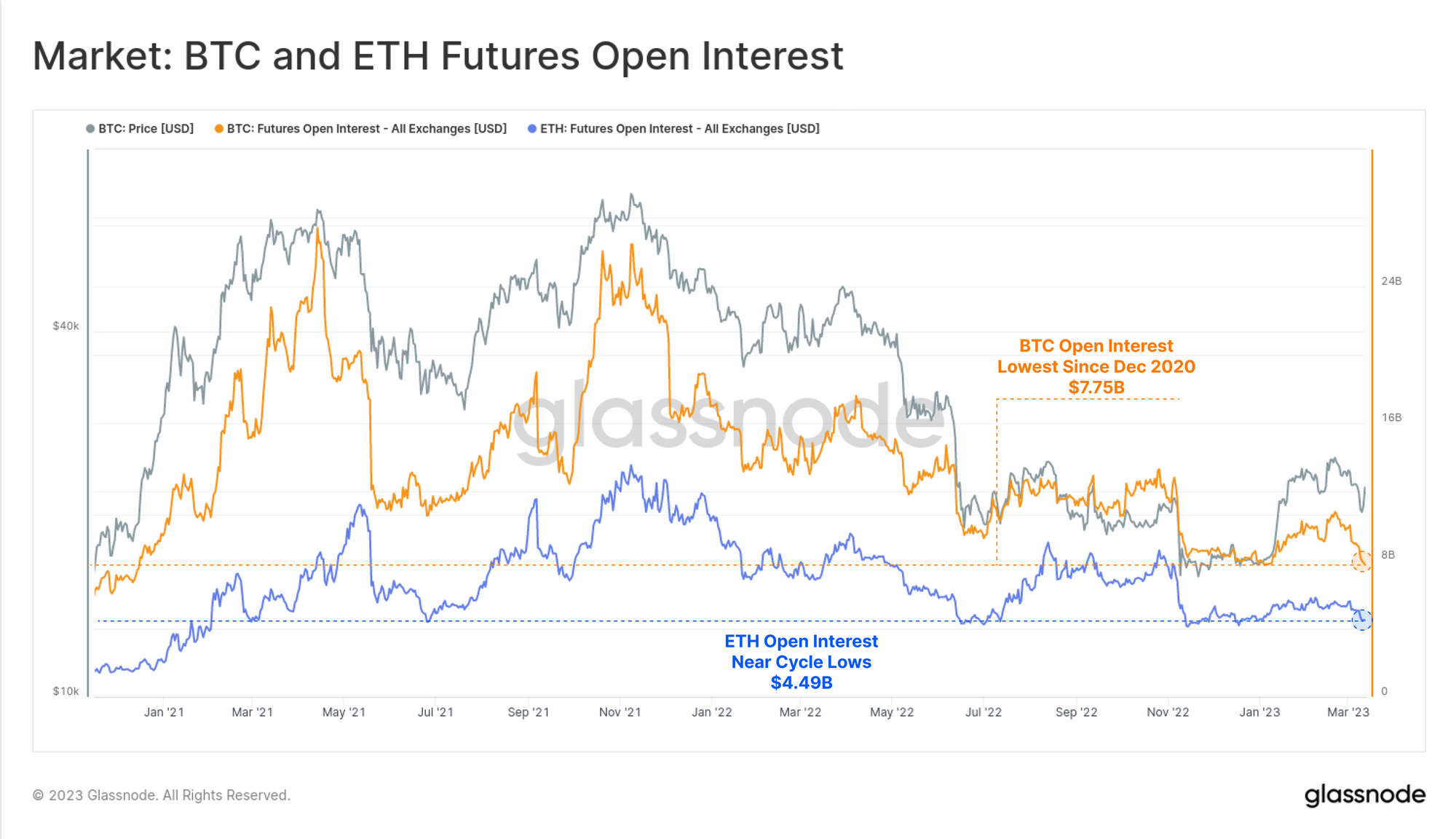

Flushing Futures

Lastly, we will assess the response expressed through futures markets. This week has seen total open interest fall to cyclical, and multi-year lows for the two major assets. Bitcoin futures positions have a notional value of $7.75B, and represent around 63% of the total open interest.

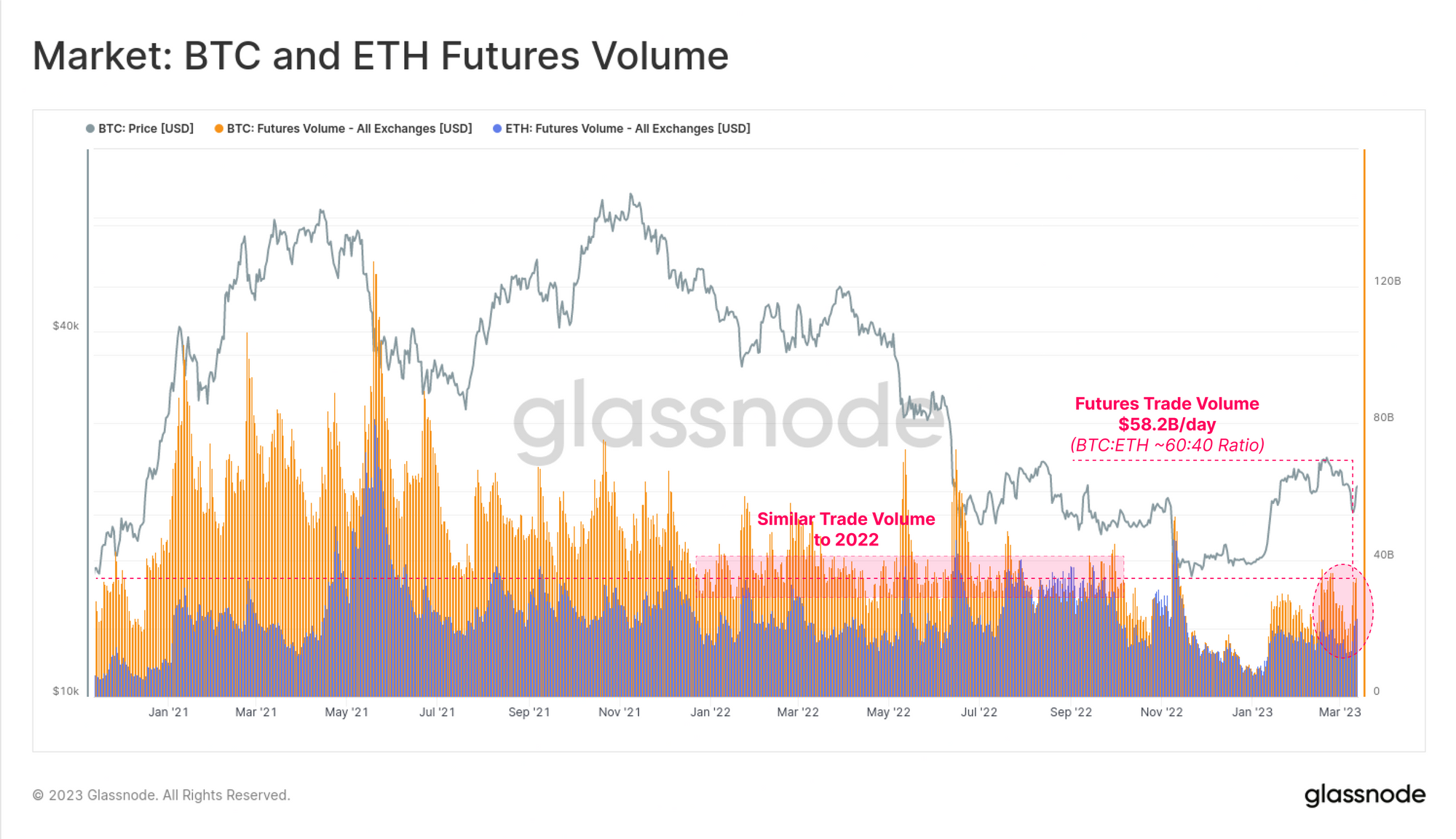

For futures trading volume, Bitcoin dominance is similar at around 60%, and volumes have picked back up after the post-FTX and end of year lull. Total trade volume is approximately $58.2B/day, and equivalent to levels seen throughout 2022.

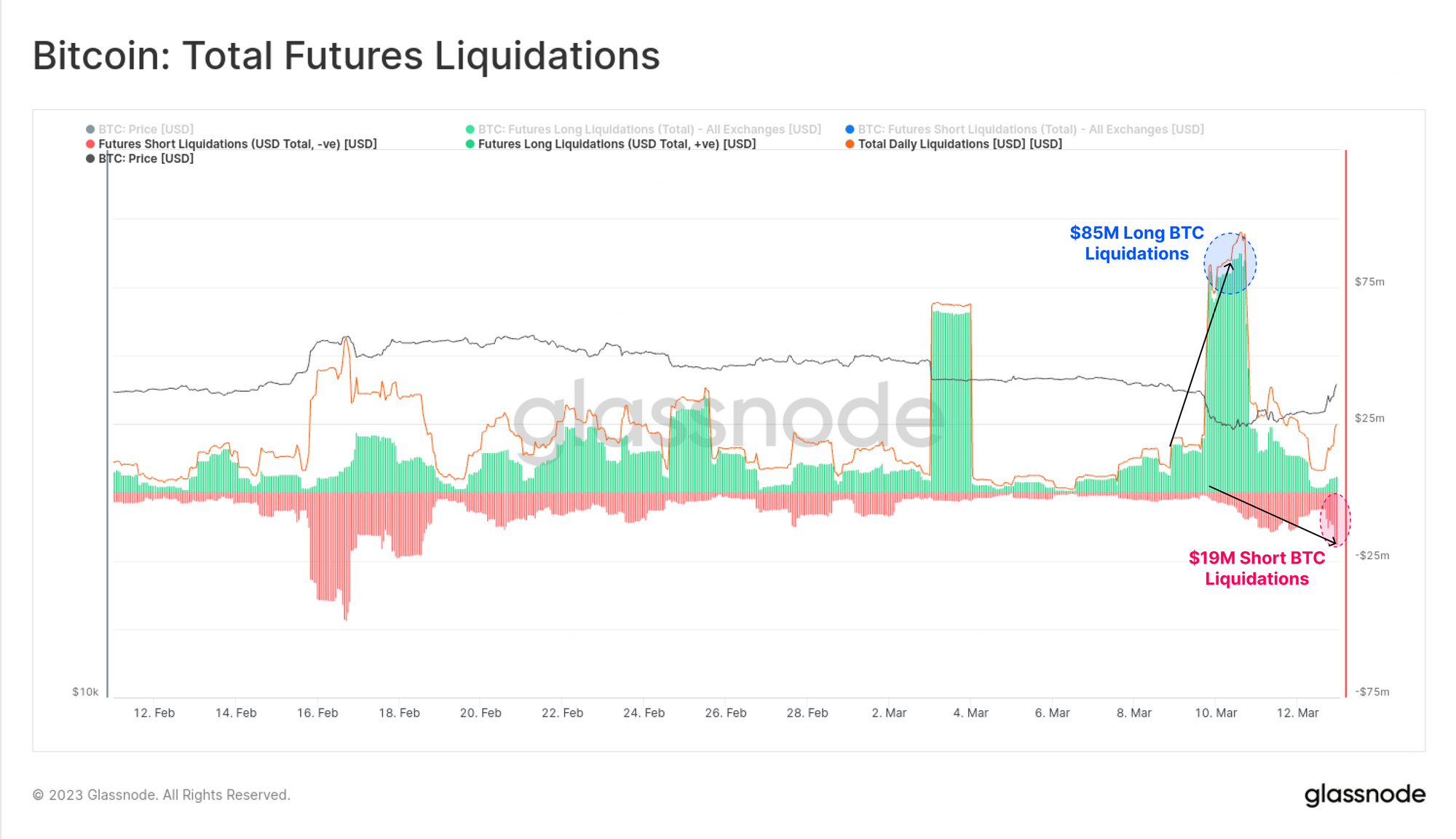

The volatile price action this week was in part fuelled by a series of both long and short squeezes. On the sell-off to $19.8k, approximately $85M in BTC long positions were liquidated. This was followed by around $19M in short positions flushed out on the recovery back above $22k.

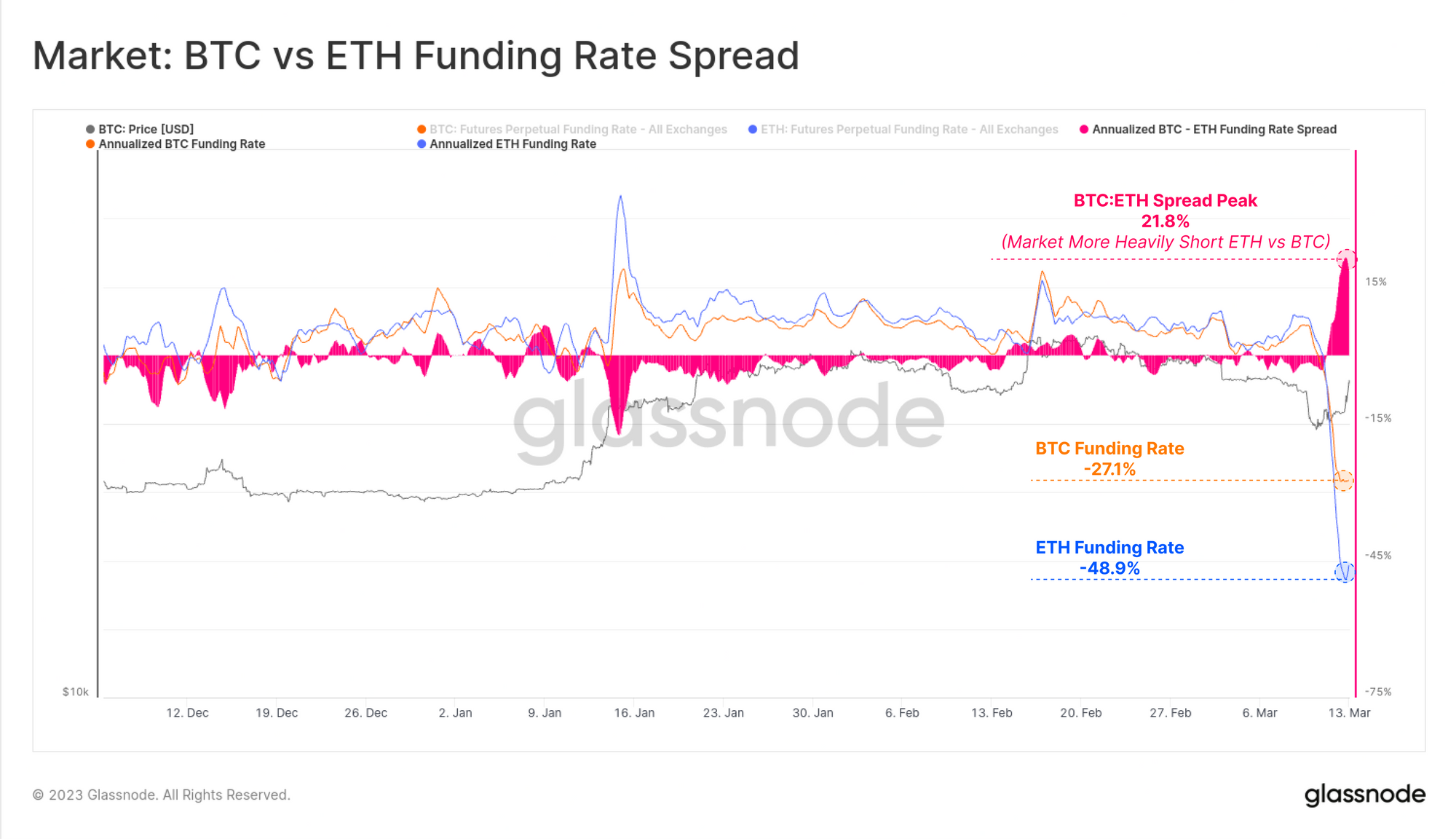

In the lead up to this rally, funding rates in perpetual swap markets entered an extreme level of backwardation. Traders were paying annualized funding rates of -27.1% and -48.9% to be short BTC and ETH, respectively. Traders were also much heavier short ETH, with the BTC:ETH spread hitting 21.8%, the largest since the FTX sell-off.

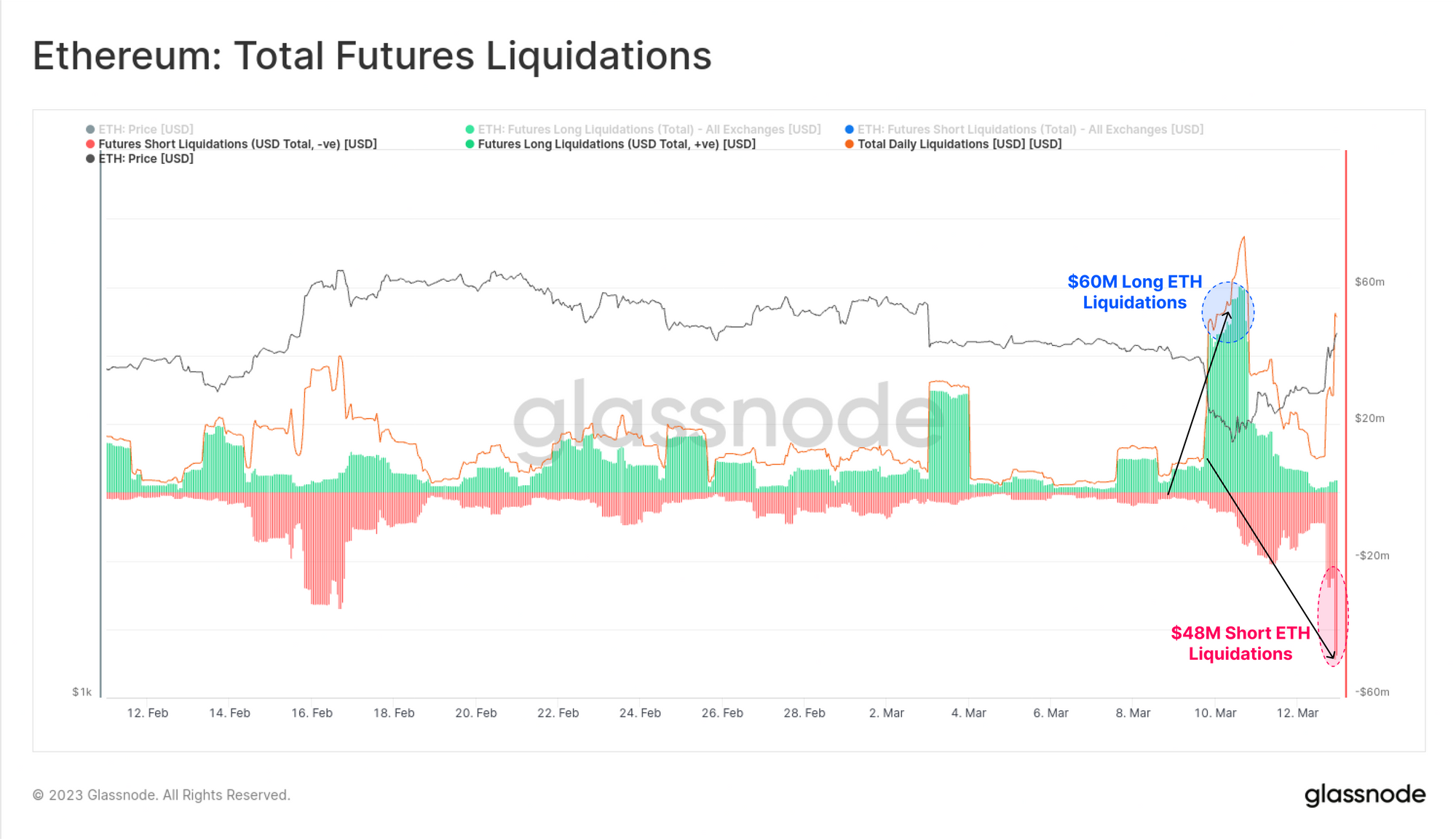

This exacerbated liquidations in ETH futures markets. Over $48M in shorts were liquidated on the market recovery back above $1.6k, which represents 2.5x more notional value forced closed relative to BTC.

This suggests that ETH markets are being utilized more heavily for expressing speculative interest of late, exacerbating volatility.

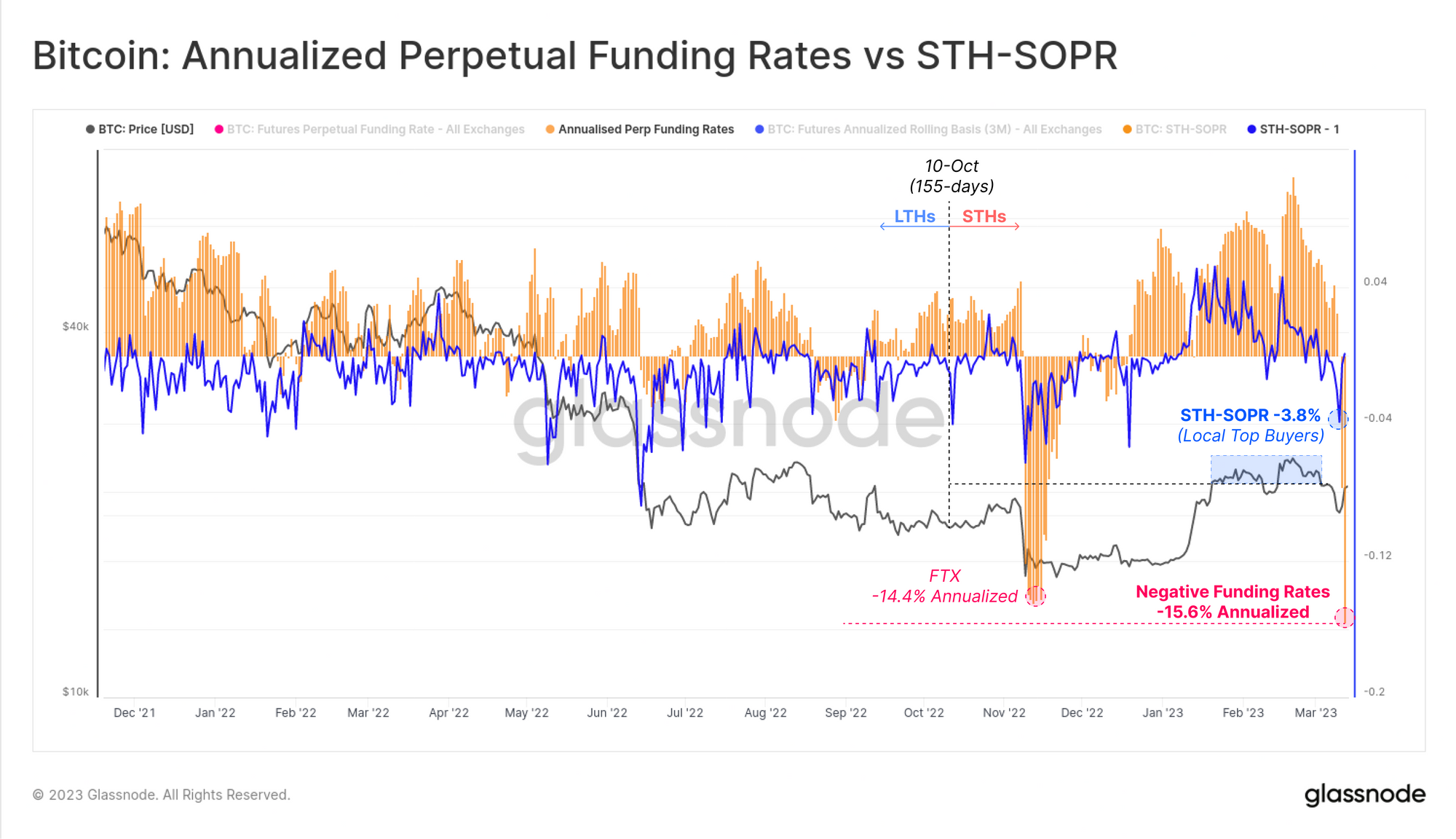

We will close with a final chart which overlays the on-chain response of Short-Term Holders (STHs), with the response in leveraged futures markets. The chart presents STH-SOPR minus 1 🔵, plotted over the annualized futures funding rate 🟠, with the following findings:

- By our defined age threshold of 155-days, almost all STH coins are likely in profit, with the exception of those who acquired near the local highs.

- STH-SOPR (minus 1) returned a value of -3.8%, which is a relatively large realized loss, and suggests local 'top buyers' dominate spending at present.

- The direction and performance of STH-SOPR tends to correlate with that of funding rates. Both metrics reflect a different, but meaningfully large sub-set of the BTC market, with one representing spot/on-chain, and the other leveraged futures.

With this as context, it appears as though the majority of coins spent this week were local top buyers realizing a loss (other holders are relatively dormant). This occurred just before futures entered a steep backwardation, and traders opened speculative short positions.

As news of bank deposits being guaranteed broke, a powerful rally pushed BTC back above $22k, and ETH above $1.6k, catching much of the market off-guard.

Summary and Conclusions

After one of the most consequential weeks of 2023, the digital asset industry is short three crypto friendly banking institutions in the US, and finds itself within an increasingly hostile regulatory environment. With traditional financial markets closed over the weekend, several stablecoins experienced a deviation from the $1 peg, recovering as news of guaranteed deposits filtered through on Sunday.

The response from investors has been somewhat similar to the post-FTX environment, with a net transfer of stablecoins into exchanges, and instead taking custody of BTC and ETH. However at the wider scale, the industry has experienced a net capital outflow of approximately $5.9B over the last month.

The industry, and indeed global financial system remains in uncharted waters. In many ways this week reinforces the very reasons why Satoshi created a trustless, scarce, digital asset in the first place.

Disclaimer: This report does not provide any investment advice. All data is provided for information and educational purposes only. No investment decision shall be based on the information provided here and you are solely responsible for your own investment decisions.