Simulating Shanghai Sell-side: Investigating the Ethereum Unlock

The highly anticipated Shanghai/Capella hard fork is scheduled to take place on 12-April-2023, which enables withdrawals of staked ETH. In this piece, we establish cohorts of stakers, and assess the potential sell-side pressure which may occur due to the unlock event.

Executive Summary

This report discusses the estimated amount of staked ETH that may be withdrawn and sold immediately after the Shanghai upgrade. After examining the different staking cohorts and their motivations for selling their unstaked ETH, we estimate a total of 170k ETH intended to be sold after the Shanghai upgrade.

We project that only 100k ETH ($190M) of the total accumulated rewards will be withdrawn and sold. Furthermore, we expect to see twice as many validators exiting, but only a limited amount of stake will be released per day. We believe only a fraction of that amount, around 70k ETH ($133M), will actually become liquid.

Even in the extreme case where the maximum amount of rewards and stake are withdrawn and sold, the sell-side volume still falls within the range of the average weekly exchange inflow volume. Therefore, we conclude that even the most extreme case will have an acceptable impact on the price of ETH.

The Shanghai Upgrade

The highly anticipated Shanghai/Capella hard fork is scheduled to take place on 12-April-2023, and will enable the withdrawals of ETH funds staked for Ethereum's new Proof-of-Stake consensus mechanism. The earliest deposits were made in November 2020, before the launch of the Beacon chain, and until now, stakers have not been able to access their staked ETH, or the rewards they've accumulated.

Given some stakers have been active since the Genesis of the Beacon Chain, their rewards have accumulated for over two years, alongside a full bull/bear market cycle since then. This has raised much speculation regarding the potential market, and supply impacts as the approximately 18M ETH staked ($33.92B, 15% of ETH's total circulating supply) becomes unlocked. Concerns largely revolve around whether the unlocks may flood the market and temporarily create significant sell-side pressure for ETH.

The objective of this report is to assess the ETH staking landscape, develop a framework to establish staking cohorts, and assess the potential impact of the Shanghai hardfork. To achieve this, we conduct several simulations to answer the following questions:

- Who is most likely to withdraw staked ETH?

- What is an estimated volume of staked ETH that will be withdrawn?

- How much sell-side pressure could we expect from these withdrawals?

Mapping the Ethereum Staking Landscape

In order to get the full picture of the current staking landscape, we will provide a brief technical overview of the existing actors within Ethereum’s Proof-of-Stake consensus mechanism:

- Depositors are private individuals, or entities that send 32 ETH to the Ethereum smart contract to activate a validator. A depositor can own as many validators as they are able to stake 32 ETH for.

- Validators are virtual entities that live on the Beacon Chain, servicing Ethereum’s consensus layer. They can be thought of as a private key and a balance, both recorded on the consensus layer. Validators are pseudorandomly chosen to verify and vouch for the validity of transactions and the information included into a block. Occasionally, they are assigned to propose blocks, in which those transactions are bundled. For their work, validators receive ETH staking rewards, which are split between consensus layer block rewards, and execution layer fee rewards for processing transactions (only the priority fee goes to the validator, whilst the base fee is burned).

- Nodes are the physical hardware which run the validator software. Each node can accommodate many validators. Nodes can be operated by the depositor themselves, or delegated to a third party staking service provider.

Depositors as the Primary Actor

Significant research has been conducted on Ethereum's staking economy, with much of it focused on validators as the primary actors in the staking economy.

For our analysis, we believe it makes more sense to focus on depositors, as depositors can own multiple validators, and ultimately, it is at the depositor (human) level where decisions about withdrawing funds, and usage of the funds will be made.

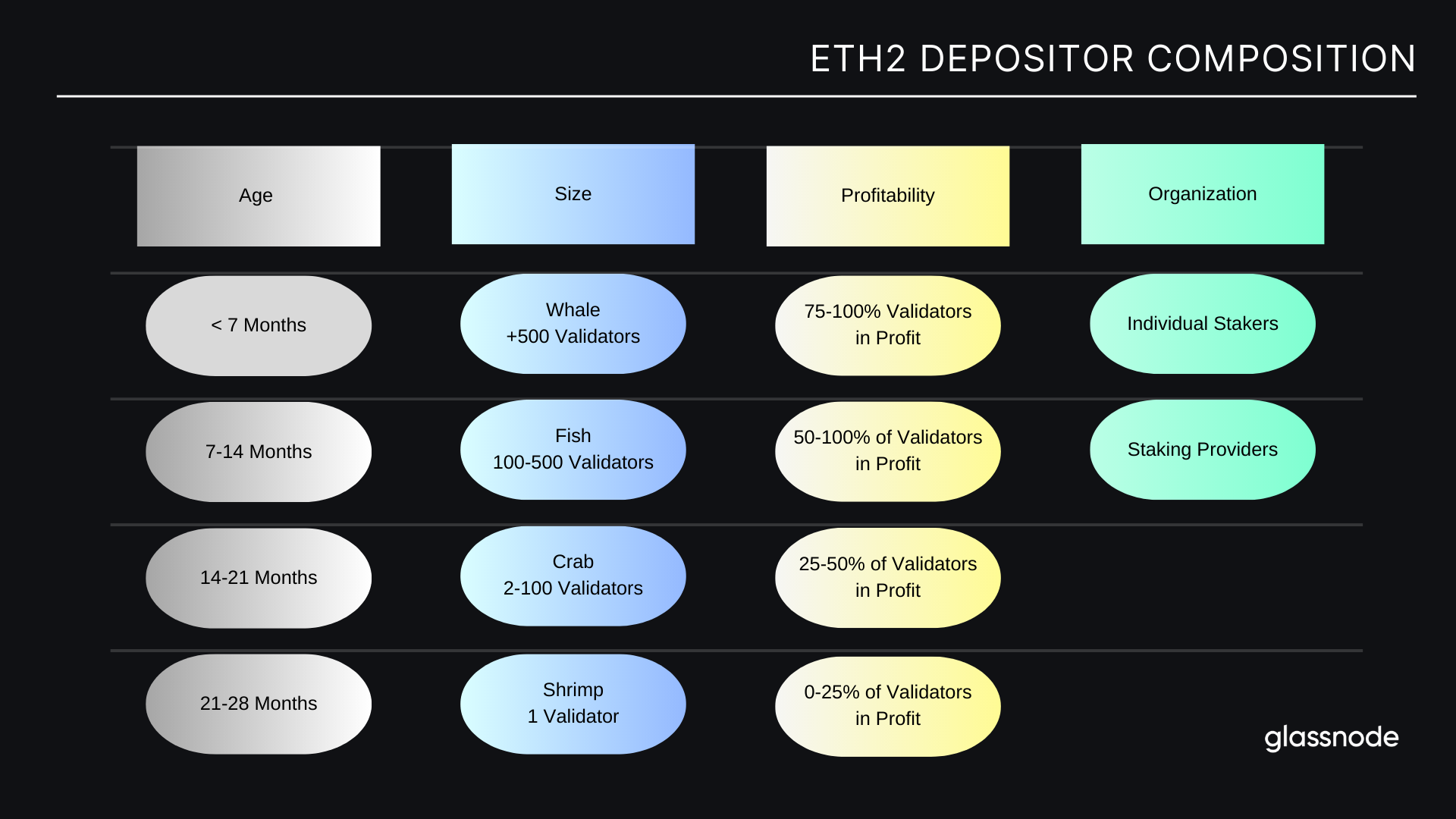

In order to understand the possibilities of the Shanghai/Capella update, we will segment the depositors into different cohorts based on the anticipated needs and motivations for staking or unstaking ETH. The following graphic illustrates the segmentations we have chosen, which largely consider four factors:

- Depositor Age: The length of time stake has been active.

- Depositor Size: The number of validators owned.

- Depositor Profitability: The unrealized profit/loss held across owned validators.

- Organization: Splitting into Individuals (solo-stakers) or third-party Staking Providers.

Please note: We understand that private individuals or entities may use different depositor wallet addresses to deploy stake to the network. This is often the case with Staking-as-a-Service providers. Therefore, we have separated depositor addresses belonging to these providers from our datasets, and analyzed them separately. This is to prevent any distortion of the signal we are trying to achieve with our analysis below.

Individual vs. Institutional Stakers

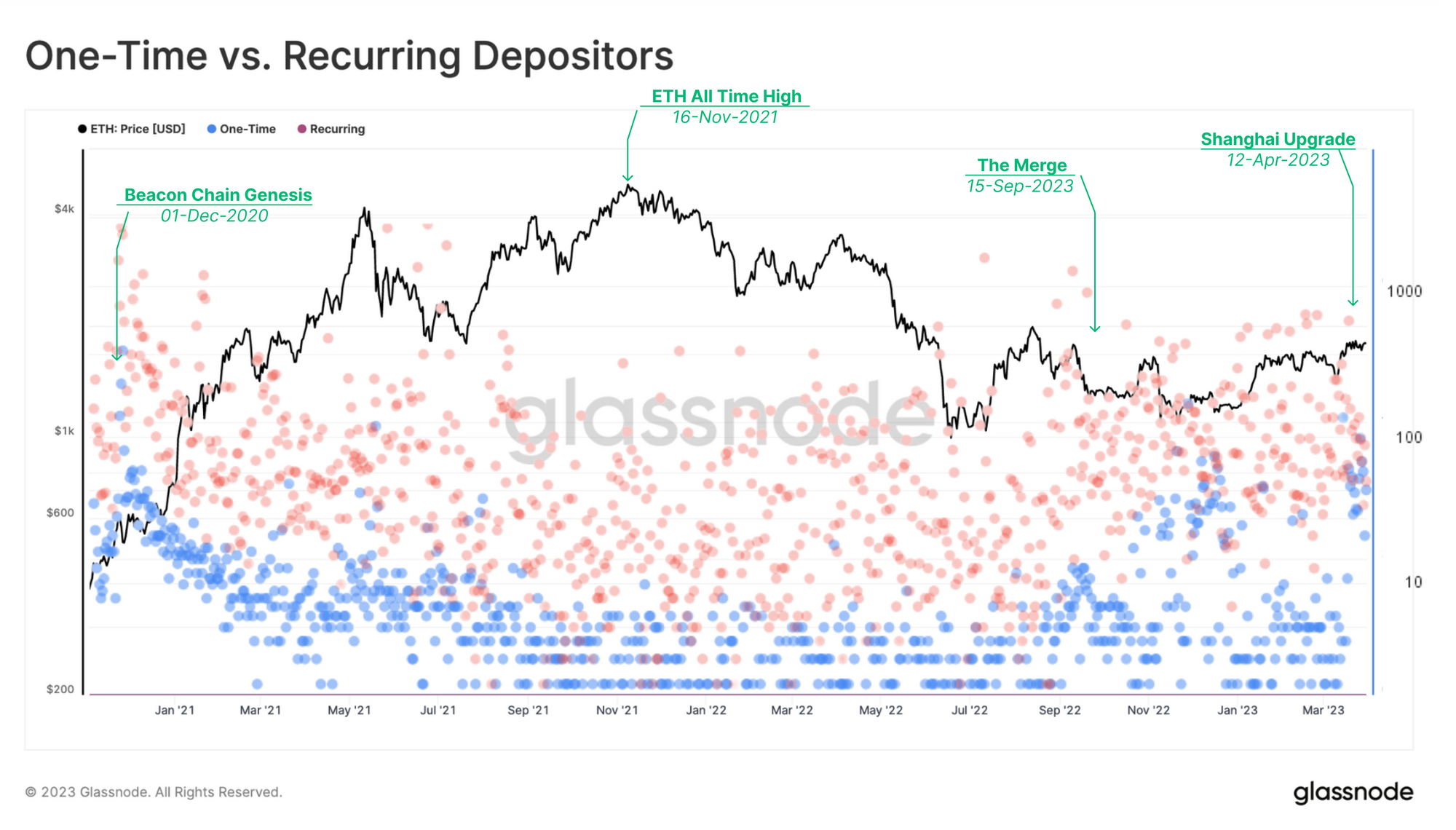

When mapping out the staking landscape, it is important to differentiate between private stakers, who have their own technical setups at home, and institutional/staking provider depositors. For the following chart, we exclude staking providers since many of these entities use disposable addresses for their deposits, which would distort the data.

Looking at the number of deposits made per day, and we can segment between one-time depositors 🔵, and wallet addresses that have deposited several times 🔴.

We can see that one-time depositors 🔵 who are predominantly active around major events such as the genesis of the Beacon Chain, the Merge, and now in anticipation of the Shanghai upgrade, suggesting a bias towards building confidence in the engineering. Events on the execution layer such the Terra collapse and its cascading consequences did not affect depositing activities.

We also note that the staking pool consists primarily of depositors that have staked multiple times 🔴 (note the log-scale) and thus hold more than one validator. We can see that over 1000 deposits per day have been made by some of these recurring depositors. Interestingly, during the bull run of 2021, the Beacon Chain saw a relative lull in these new deposits.

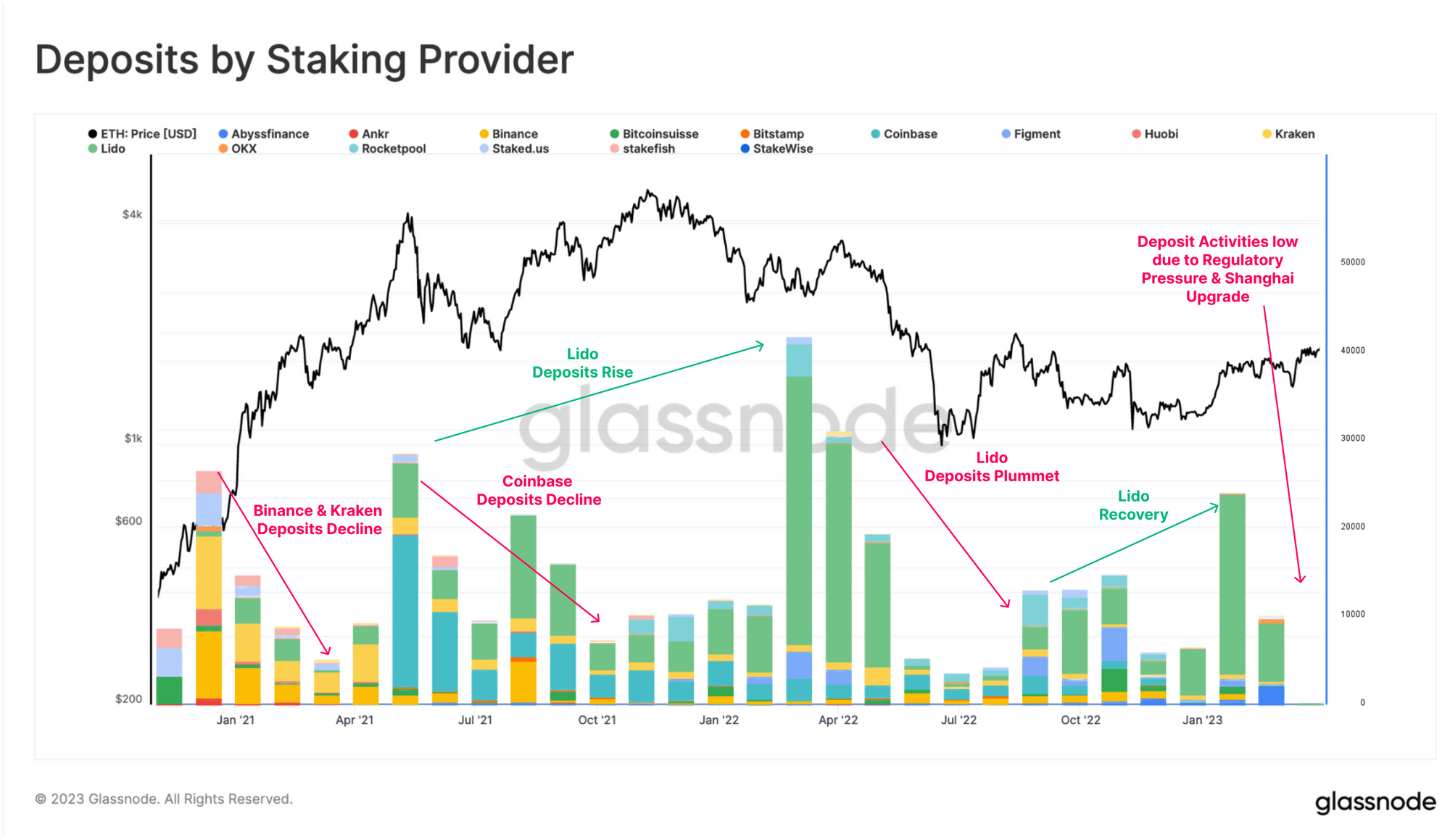

Staking Providers

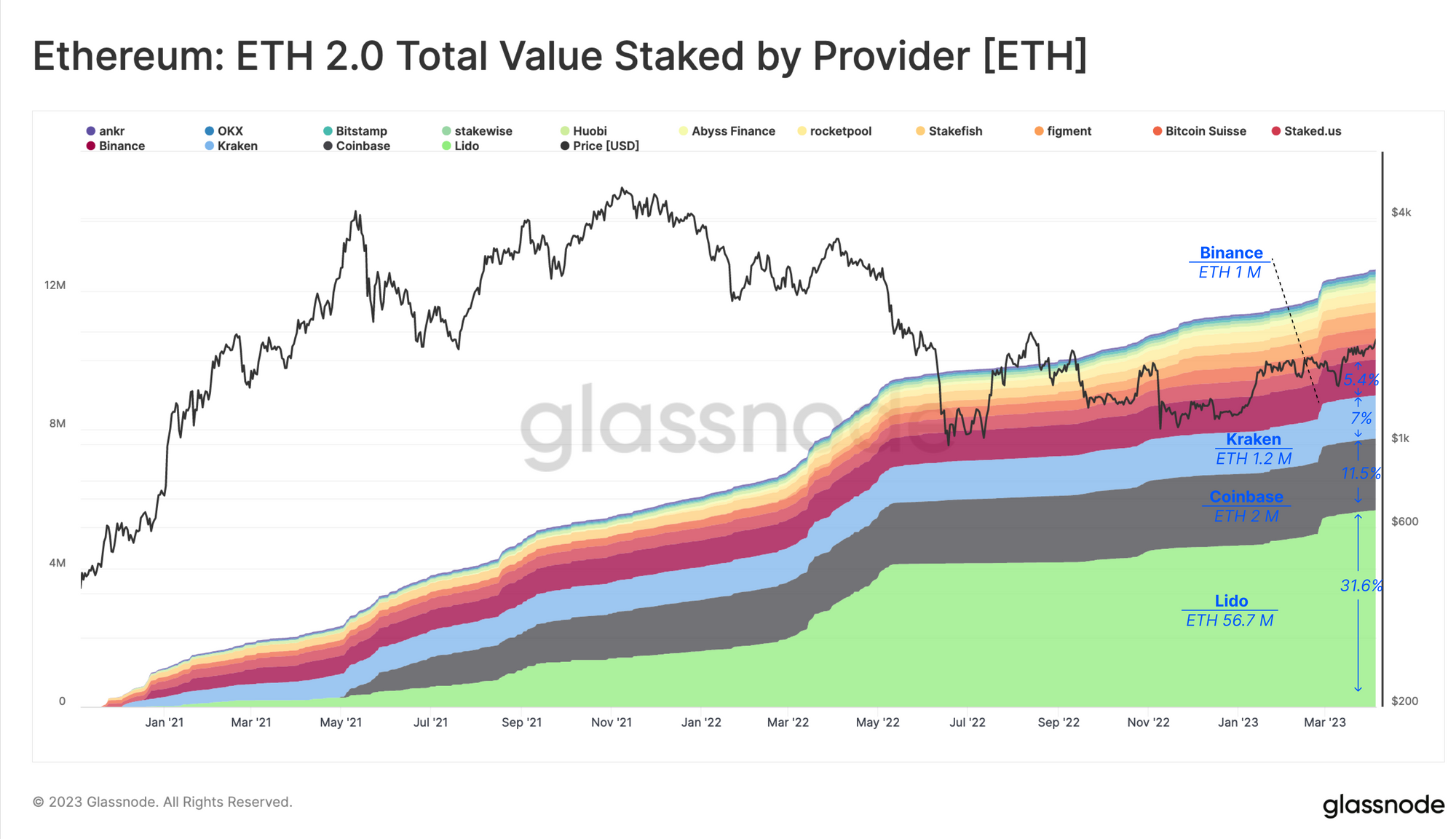

Staking providers are larger entities that allow users to delegate their ETH to the provider's validator nodes. By delegating their ETH to these nodes, users can earn rewards for supporting the network without the need to run their own validator node, or to provide the entire 32 ETH.

Liquid staking providers in particular, which return users a tradable token derivative for their stake, have gained massive market share over the course of the past 2 years. Currently, Lido is market leader, holding a market share of over 30% of the entire network stake. Centralized exchanges like Coinbase, Kraken, and Binance follow with a market share of 11.5%, 7.0%, and 5.4%, respectively.

Taking a closer look at the number of deposits made by staking providers over time, we can clearly see shifts in dominance:

- During the first half year after the genesis of the Beacon Chain, Kraken and Binance were the dominant depositors. However, they were eventually surpassed by Coinbase and Lido.

- Lido dominance expanded massively in the second half of 2021, however the stETH token was put under market stress during the LUNA-UST collapse, as well as the bankruptcies of Three Arrows Capital and Celsius. This was due to these entities having sizeable ties or positions in the token at the time.

Consequently, depositing activities by all staking providers, particularly Lido, plummeted in the middle of 2022, and slowly recovered towards the end of the year. Additionally, we observe a massive drawback of staking activities by centralized exchanges, which can be attributed to the increasing pressure by US regulators on these institutions. Kraken eventually ended its US-based staking service in February 2023 after being fined by the SEC, and Coinbase was served a Wells notice in March 2023 regarding its staking service.

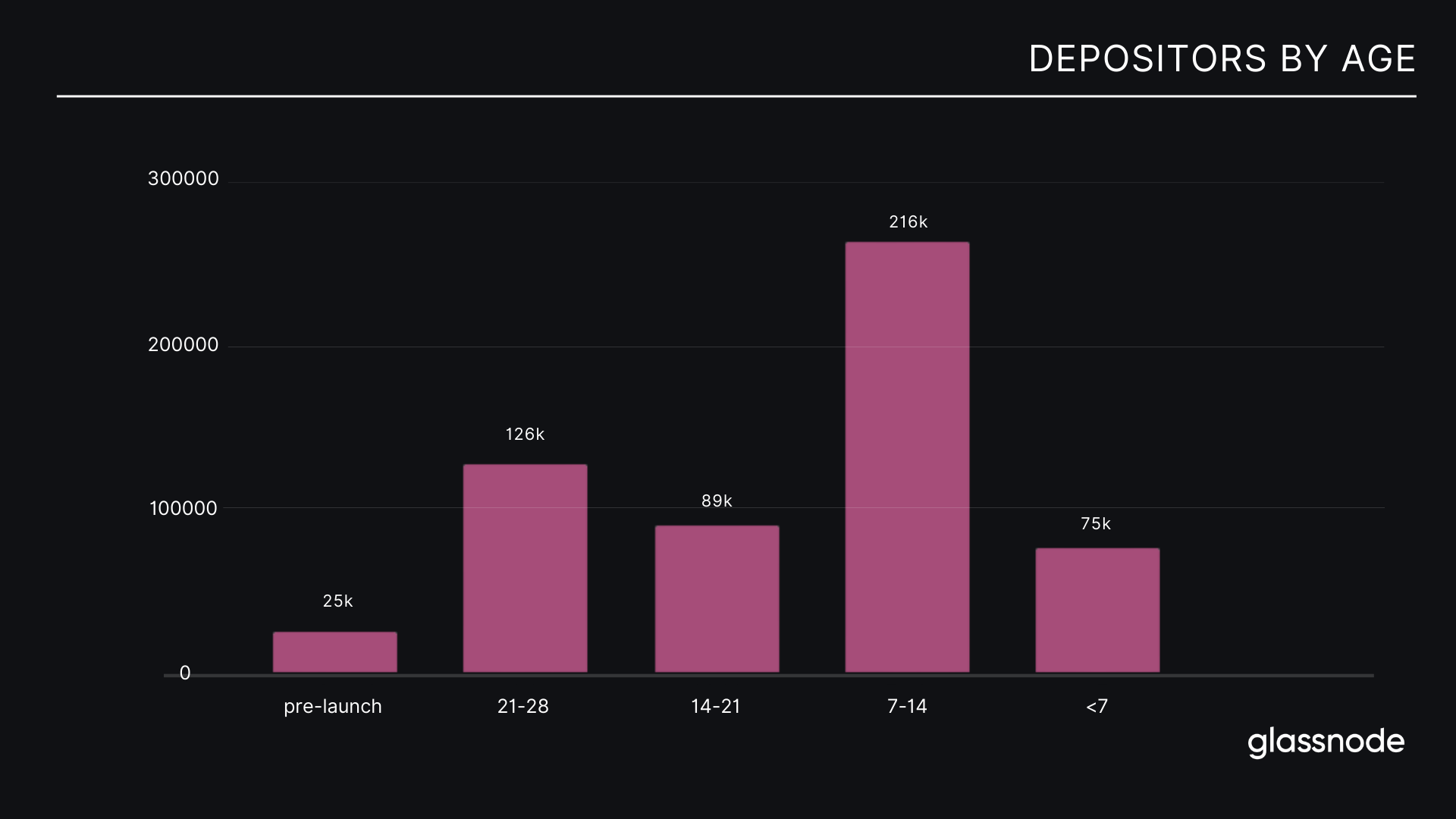

Depositor Age

The depositor age takes the deployment date of a validator to calculates the average amount of time a depositor is participating in the staking economy. This includes both one-time and recurring depositors, but again does not includes staking providers.

We then cluster depositors into five bins, reflecting a quarter of the Beacon Chain's lifespan (groups of 7 months), and one for those that pre-date the Beacon Chain launch. To our surprise we detected a relatively high number of 25k depositors, whose average age predates the launch of Ethereum's consensus layer. We attribute these depositors to those investors with very high conviction rate, since deploying validators at that time was highly risky. We even argue that these depositors do not see validating as an investment, but rather as either members of Ethereum's inner circle, or community members highly motivated to secure the network, rather than generate profit.

Furthermore, we can see that the majority of depositors are between six months and one year old. This indicates that there has been a growing confidence and trust in Ethereum's staking economy over the past year, especially after the successful execution of the Merge and the near-term prospect of withdrawals being enabled.

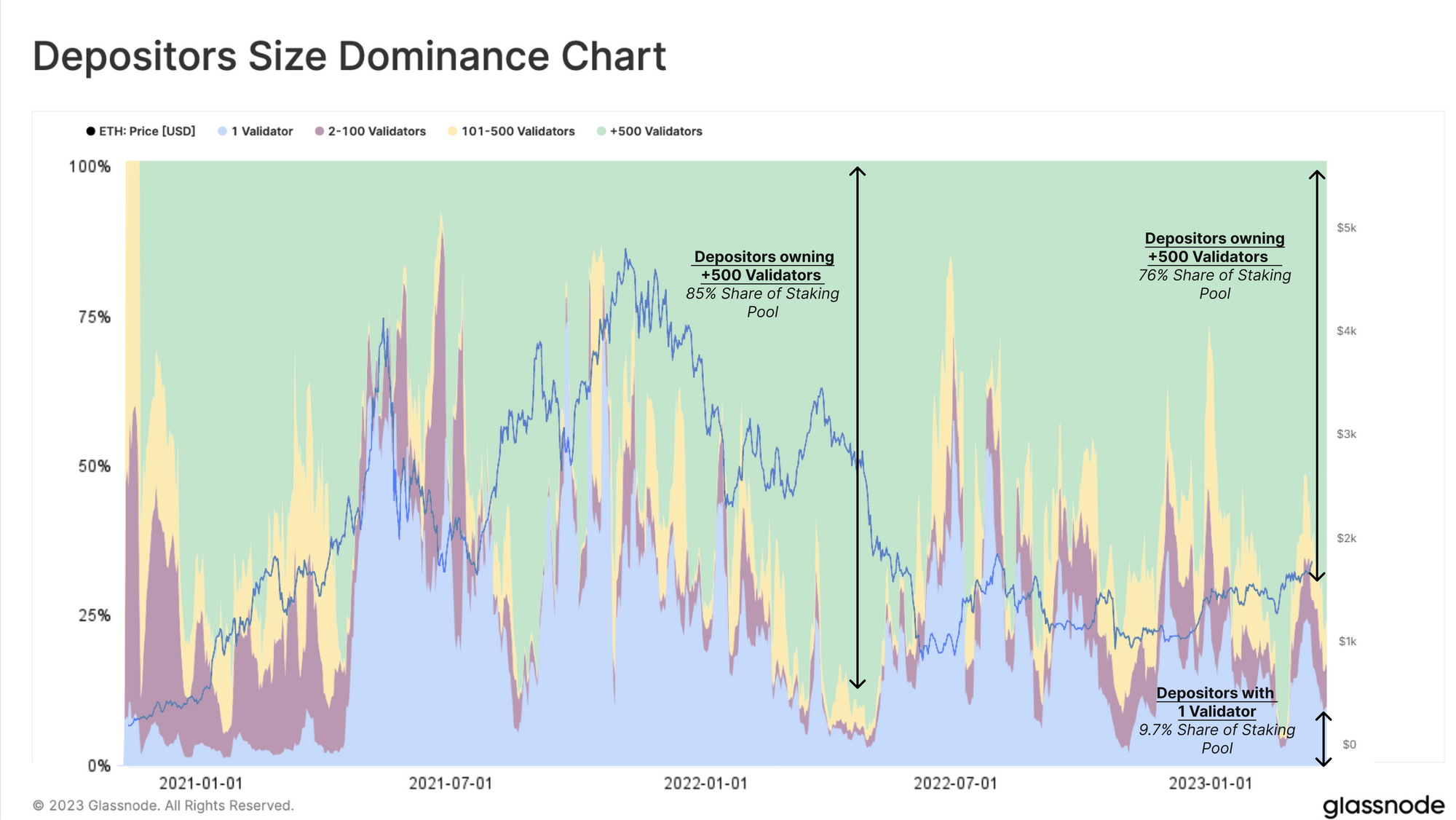

Depositor Size

The next step is to examine the size of individual depositors, once again excluding staking providers from our dataset. Unlike the chart above, which counted single deposit events, here we calculate the total number of validators that a depositor's wallet address accumulates over time. We then cluster these into different size bins.

Remarkably, six months after the Beacon Chain launch, the staking pool became split between depositors who held only one validator (shrimp) 🔵, and those who owned more than 500 validators (whales) 🟢. During the last bull run, there were a relatively high number of one-time depositors in the staking pool. However, they decreased sharply during the market turbulence of 2022, as new solo stakers were hesitant to enter the staking pool.

Crab 🔴 and Fish 🟡 entities with between 2 and 500 validators have a surprisingly small dominance of just 13.5% of the total.

Depositor Profitablity

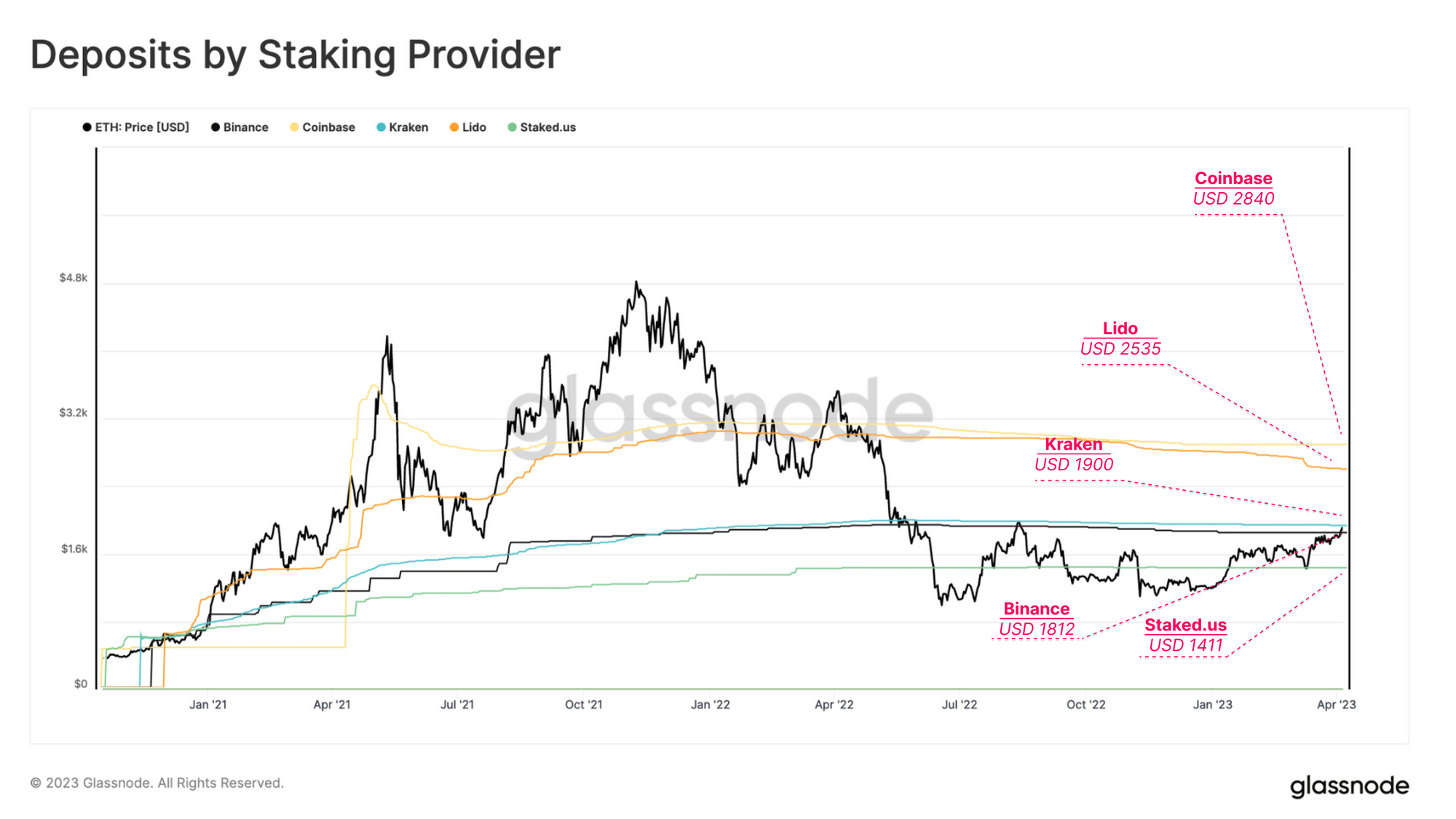

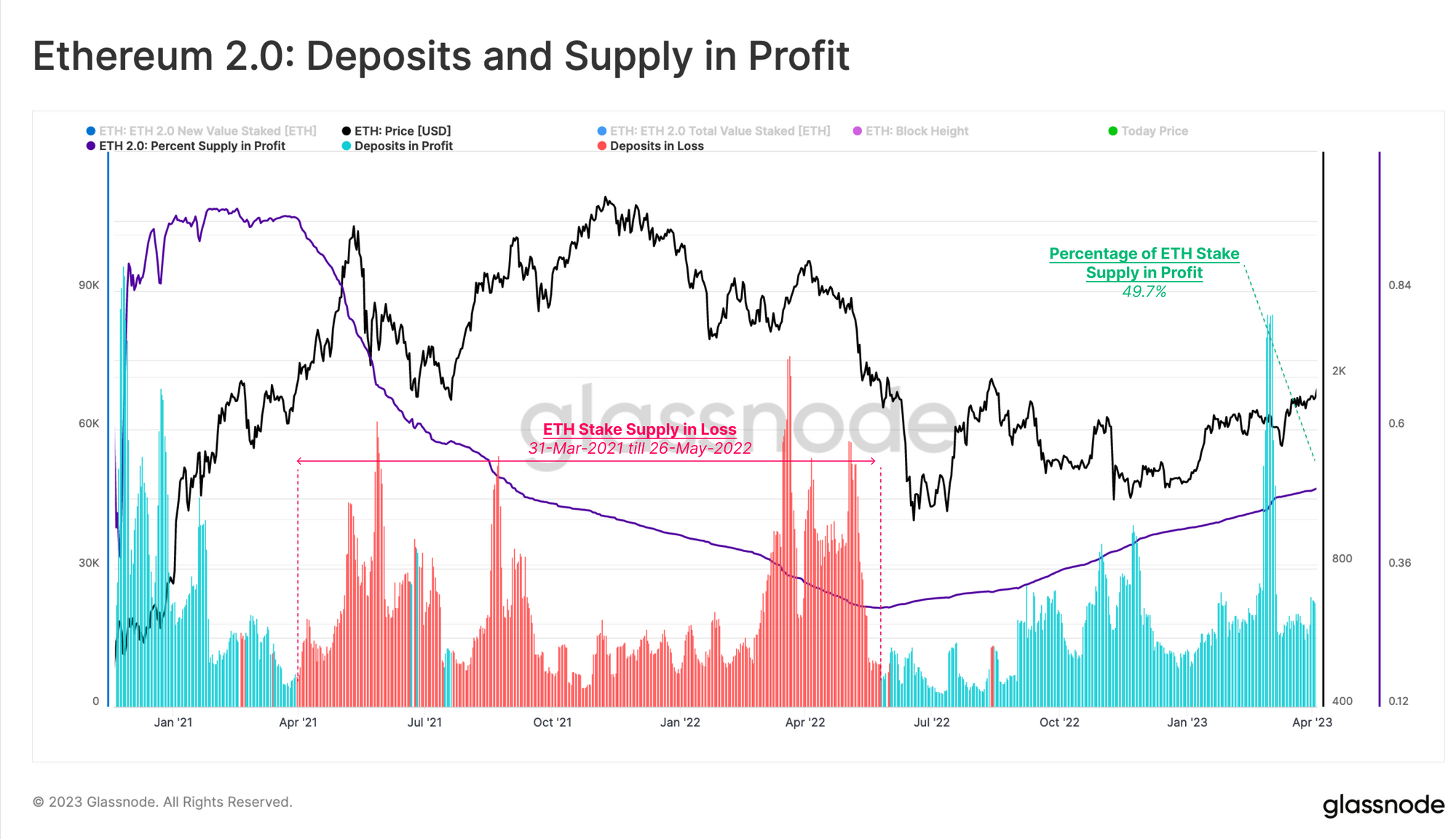

To evaluate a depositor's profitability, we calculate the realized price of their stake, which is the value of ETH at the time of deposit, compared to the current spot price. This provides a gauge on the Unrealized Profit/Loss held on average per depositor.

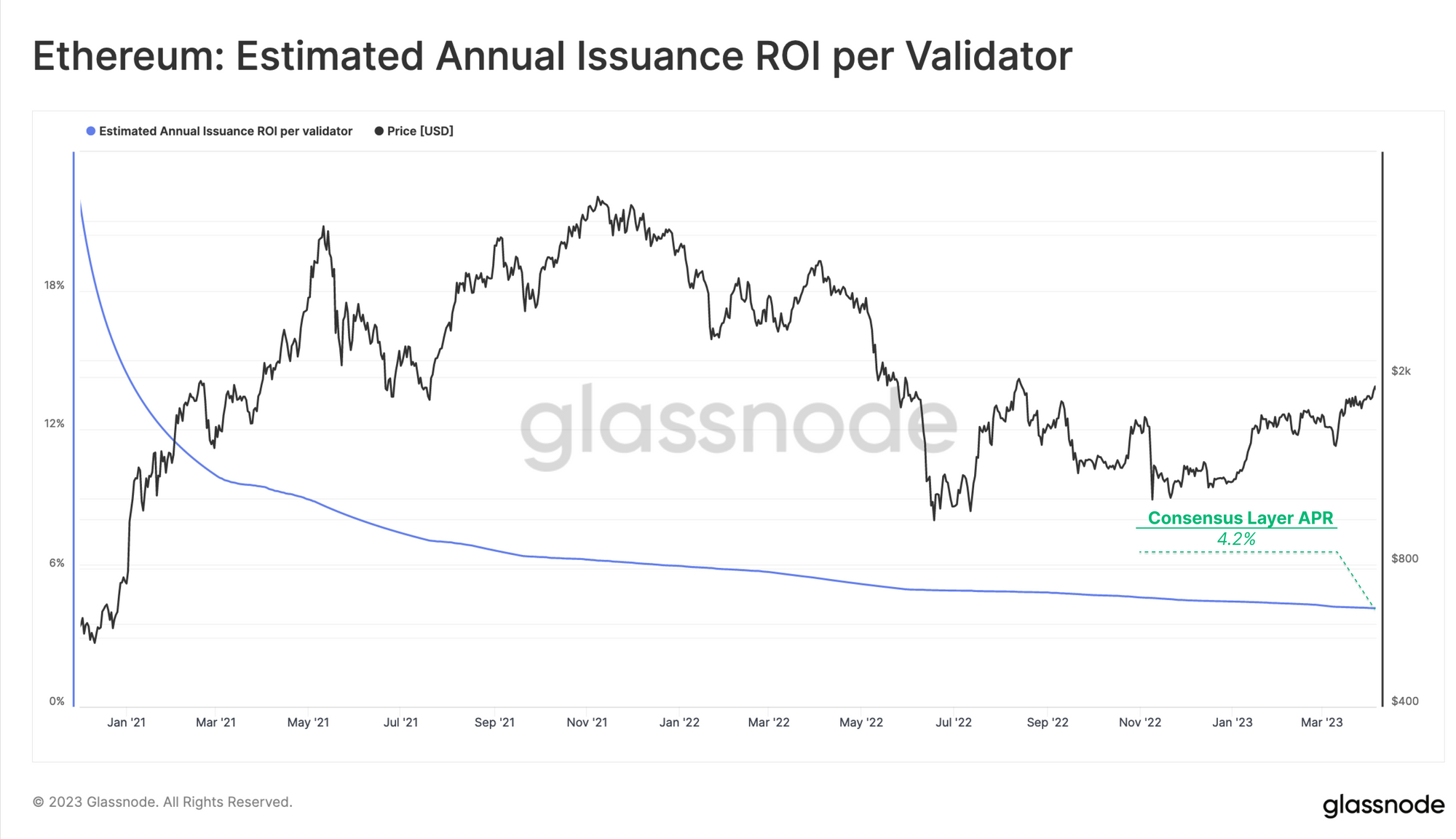

Currently, the average deposit price 🔴 across all staked ETH is $2,136, which indicates an average unrealized loss of -13% at current spot prices. In contrast, the realized price for the Ethereum network 🔵, which captures the average price at which the entire ETH supply last moved on-chain, is $1,403, an unrealized profit of +36%.

Upon examining the Realized Price per staking provider, we observe that Coinbase and Lido's average cost base is roughly 50% higher than the current ETH spot price. Binance and Kraken, which saw primary deposit activity at the beginning of the bull run, are at an approximate break-even level between $1,812 and $1,900, respectively.

The high realized price for Coinbase and Lido is an interesting dynamic because both offer a liquid staking derivative for their staked ETH, allowing holders to sell, or better hedge their risk, with depositors potentially securing a better Realized Price in secondary markets.

If the price of the ETH stake at the time of deposit is above today's ETH price, we consider the stake to be at a loss. Not surprisingly, ETH supply that was deposited during the peak bull run between mid-2021 and mid-2022 is held at an unrealized loss. Approximately up to half of the total stake amount is currently held at a loss, which provide some insight into the potential withdrawal dynamics after Shanghai.

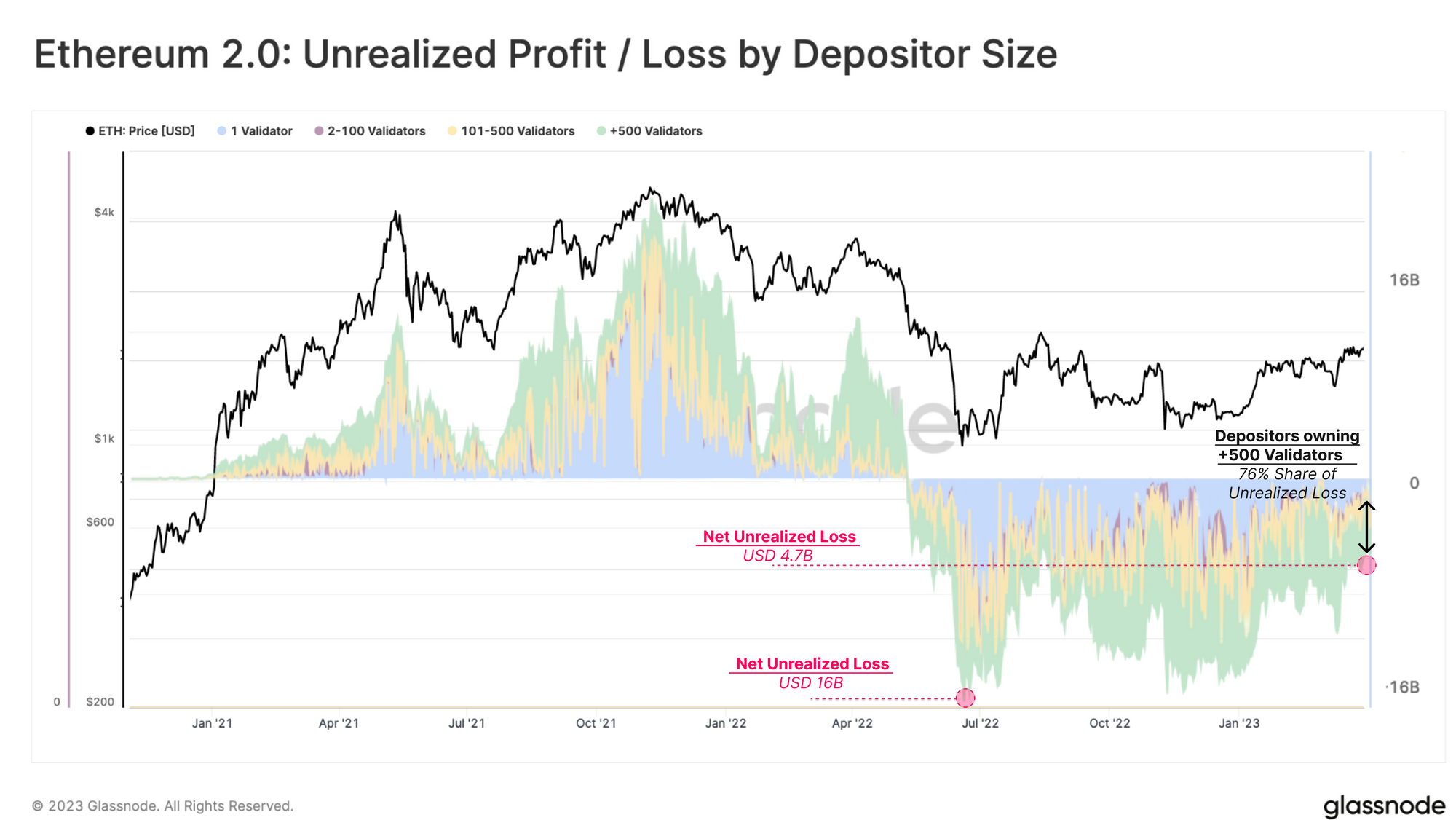

Taking the difference between the ETH Spot Price and the Realized Price for ETH deposits, we deduce the aggregated USD value of unrealized profit or loss held by stakers. Combining this with our depositor size segmentation, we can start to establish groups based on the division of unrealized profits or losses among depositor types. After the peak unrealized loss of $16B in July 2022, the net unrealized loss now amounts to $4.7B. It is mainly carried by the Whale sized depositors, who hold a 76% share of the unrealized losses.

Simulating Withdrawals after Shanghai

In this section, we estimate the amount of staked ETH that may be withdrawn immediately after the Shanghai upgrade.

Whilst depositors have been unable to withdraw their staked funds, they could still sign a voluntary exit message to signal their wish to exit the staking pool. There are currently 1,229 validators waiting to exit, as well as 214 slashed validators that will be forced out as soon as withdrawals are enabled (for a total of 46,176 ETH, $85.7M).

Shanghai allows for two types of withdrawals: partial and full. Partial withdrawals, often referred to as skimming, automatically withdraws each validator's cumulative staking rewards, reducing their validator balance to 32 ETH. Full withdrawals involve shutting down the validator entirely and retrieving the entire stake balance.

Validators undergo the same automatic withdrawal processing for partial as well as full withdrawals. An automatic sweep scans linearly through the entire validator set, starting from index 0. If a validator hasn't signed a voluntary exit message or was slashed, the excessive ETH balance is skimmed and automatically sent to the execution layer. If the validator has signed for a voluntary exit and has passed the waiting periods, it is exited. Every slot (12 seconds), 16 validators are scanned and processed. With the current number of validators, this process should take up to 4.5 days.

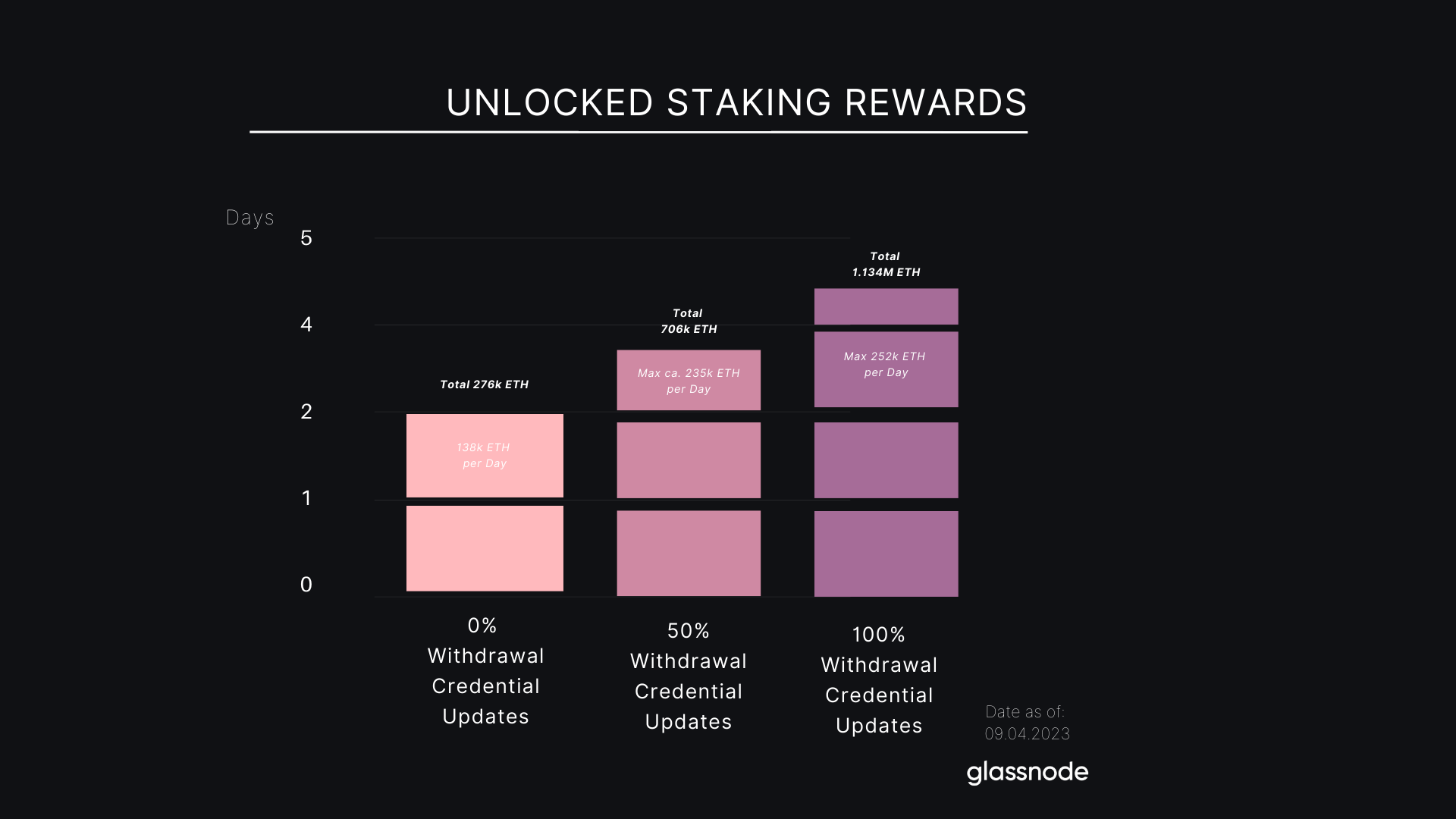

However, the scanning time to skim through the entire validator set is complicated by the number of validators that have to update their withdrawal credentials. The withdrawal credentials define where the withdrawn ETH is sent to. In the early days of Proof-of-Stake, validators were deployed with 0x00 credentials. These validators need to update their credentials to a 0x01 type in order to participate in the automatic processing. Currently, around 300k validators need to update their withdrawal credentials, which is only possible after the Shanghai/Capella update. For our analysis, we recalculate the duration of the automatic process to be a maximum of 2 days, based on the actual number of validators that are eligible to be skimmed right after the Shanghai update.

Expectations of Partial Withdrawals

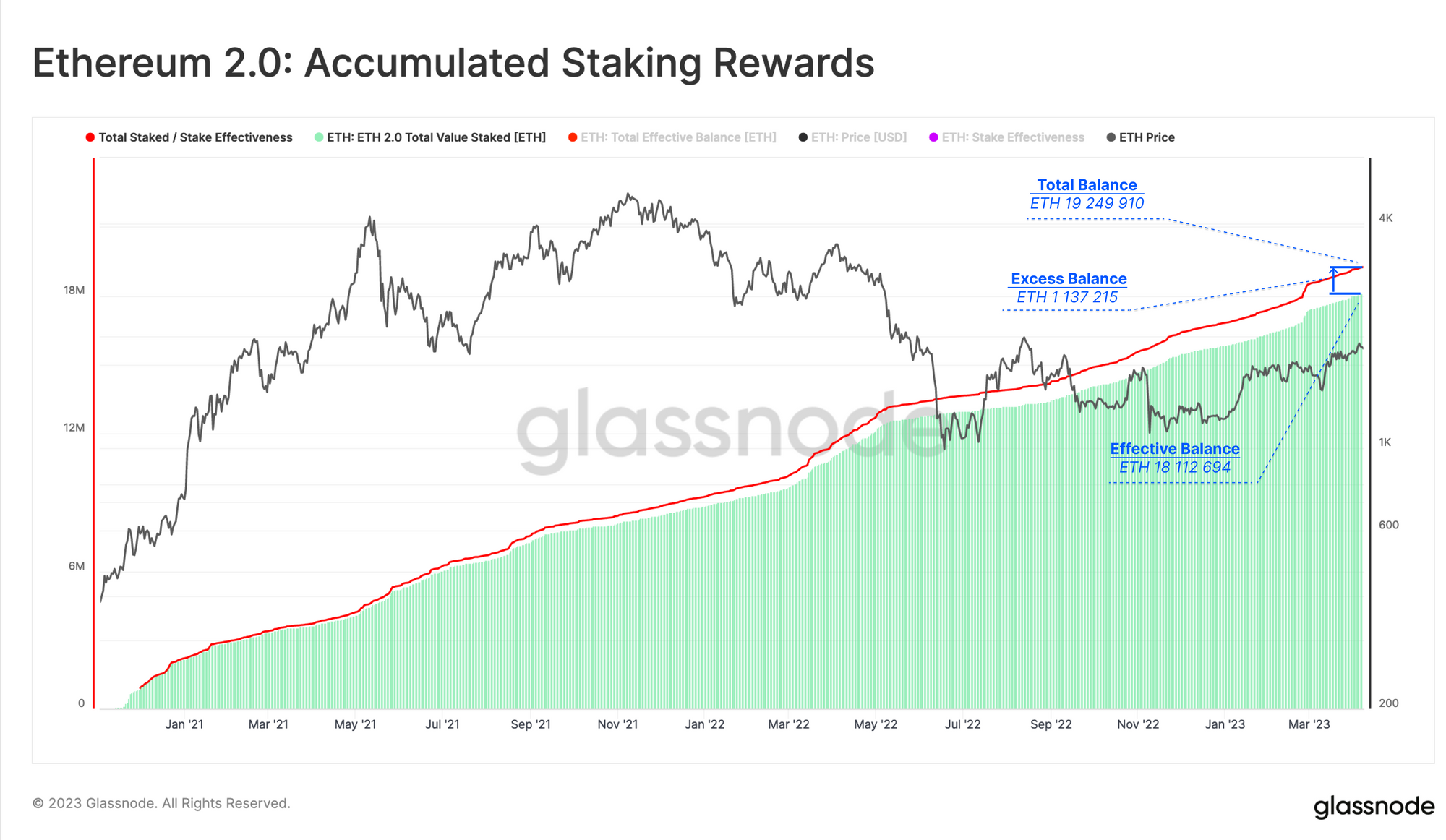

Shanghai presents a special case where rewards have accumulated over the course of more than two years, and will be unlocked all at once. Currently, the excess balance, which is not actively participating in Proof-of-Stake, is around 1.137M ETH, around $2.1B in value. After the Shanghai upgrade, this amount will be automatically withdrawn from the Beacon Chain and transferred as an automatic balance update to the depositor's Ethereum mainnet address.

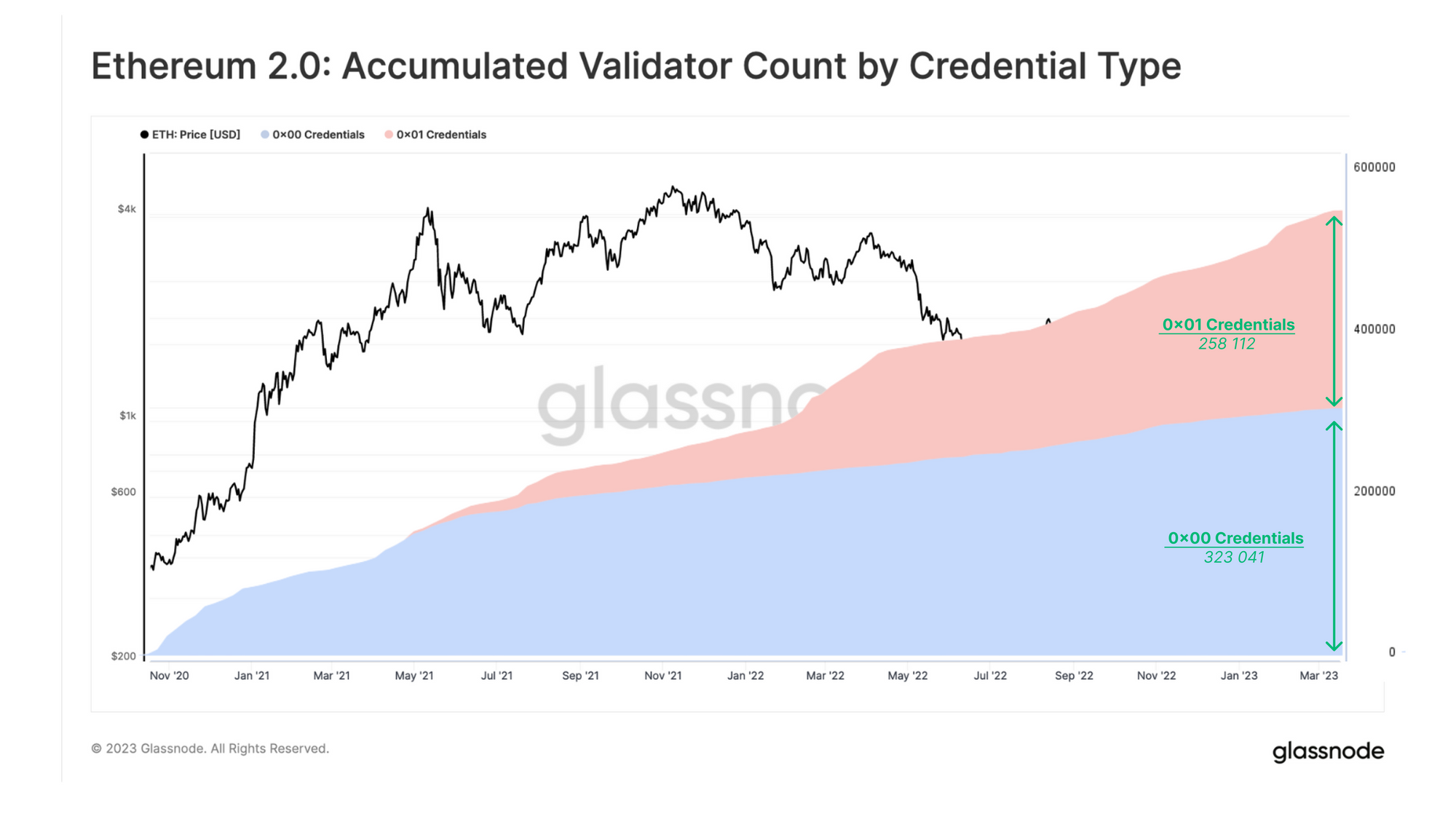

As described above, only validators with an 0x01 withdrawal credential will participate in the automatic withdrawal process. Currently, around 44% of validators have the right withdrawal credentials. However, there are many validators that still need to update their withdrawal credentials, many of which were deployed during the early days of the Beacon Chain, and have thus accumulated a larger volume of staking rewards. This was analyzed in detail by Data Always, and we have reproduced the chart below to demonstrate how the validator count of these two credential groups has developed.

Based on the ratio determined in the analysis, validators with 0x00 credentials own nearly 75% of the total accumulated rewards. As a result, validators with 0x01 credentials will have access to the remaining 25%, which is equivalent to 276k ETH being withdrawn over the course of two days.

In an extreme case where all remaining validators updated their withdrawal credentials after the Shanghai upgrade, which would occur at a rate of 16 validators per block, we would eventually see the entire sum of 1.137M ETH exit the Beacon Chain over a period of 4.5 days.

The chart below shows the minimum and maximum amount of reward payouts, including the maximum daily amount of ETH being unlocked in each case. The actual numbers will likely fall between these extreme values. We believe that many depositors may wait to unlock their accumulated rewards until after a successful implementation of Shanghai before upgrading their credentials, we therefore take a 50% withdrawal as our benchmark. Therefore, we would expect the actual numbers of unlocked stacking rewards to be closer to the minimum value of 706k ETH ($ 1.31B).

To estimate how much of the accumulated rewards will actually be sold, our depositor segmentation above comes in handy. Knowing that Lido holds a significant share in the accumulated rewards and has vowed to mainly re-stake its rewards, we believe other staking providers will follow suit, which would results in a big part of the staking rewards to be locked up again.

We can most likely rule out a high degree of sell-side pressure from the remaining cohorts as well. According to the Depositor Size Dominance Chart, around 75% of non-institutional depositors are large holders, with more than 500 validators or a stake balance of 16,000+ ETH. Depositors of this financial strength are less likely to feel pressure to sell, even if their validators are underwater. Given the positive market trend of the past week, it is more likely that this group of depositors will choose to restake or reinvest their accumulated rewards and wait for the next bull run.

This leaves us with a probable range between 76k ETH ($141M) and up to a likely maximum of 162k ETH ($300M) as a measure of potential sell-side pressure from partial withdrawals after the Shanghai upgrade.

Expectations for Full Withdrawals

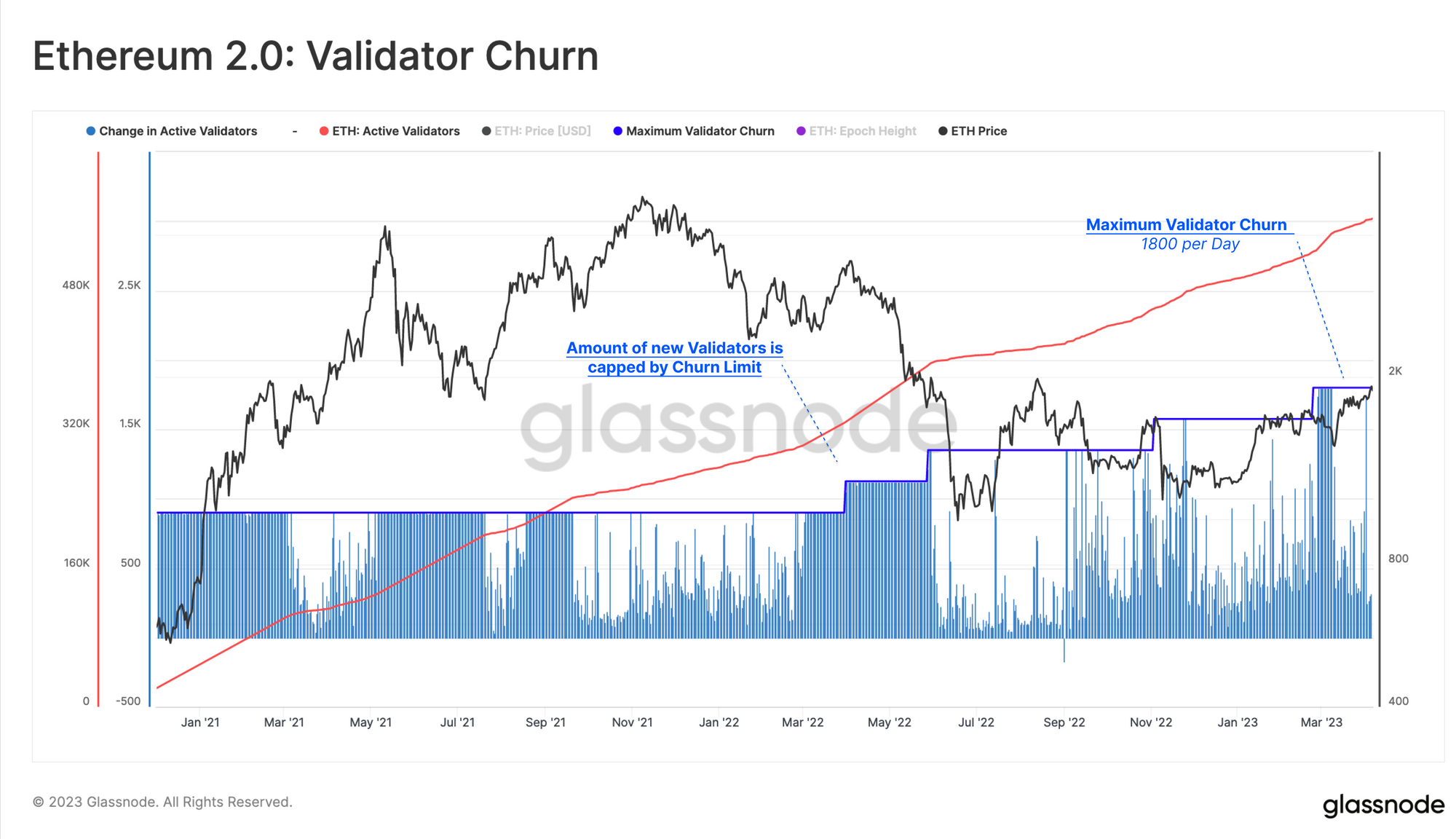

Looking at full withdrawals, it is important to note that only a limited number of validators can exit per day. Since the security of the Ethereum network depends on a stable set of validators, there are various mechanisms in place to prevent heavy churn of validators, and the rapid draining of stake.

This daily number is defined by the churn rate, which determines both the allowed number of incoming validators and exiting validators. The churn limit itself correlates with the number of active validators in the staking pool.

Churn Limit = Active_Validators/65536

With the current churn limit of 8 per epoch, and with 225 epochs per day, a limit maximum of 1800 validators can be withdrawn per day, equating to 57.6k ETH. From our historical data, we can see how the churn limit played out with incoming validators.

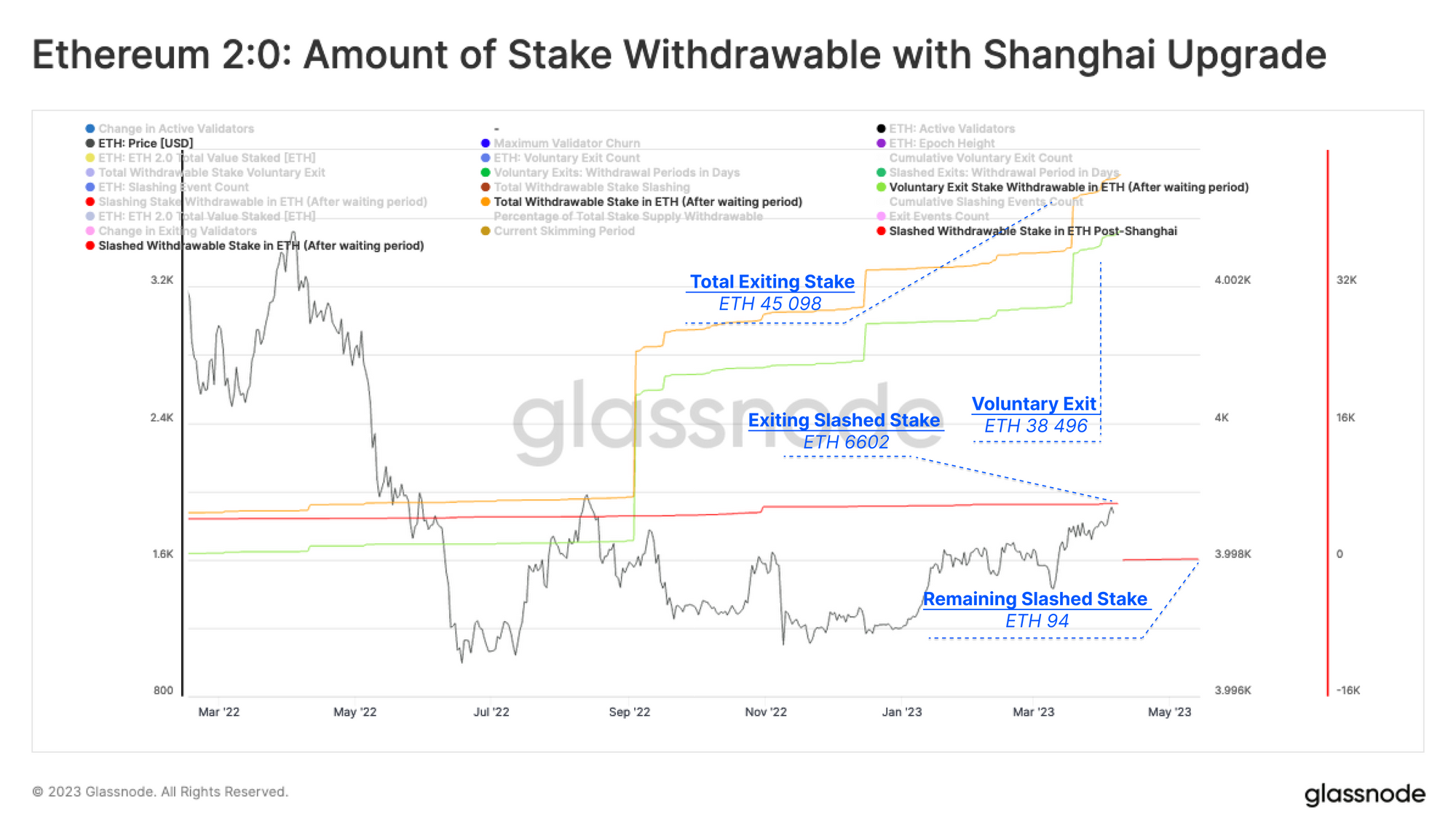

In addition to the withdrawal period determined by the churn limit, validators have to pass through a withdraw-ability delay. For voluntarily exited validators, this waiting period is 256 epochs, or around 27 hours long. For slashed validators, it is 8192 epochs, or around 36 days. We then again add the duration of the automatic withdrawal process, as described above.

Taking into consideration our data on exited and slashed validators, and accounting for the different waiting periods, we have simulated the accumulated amount of ETH, which is accessible right after the Shanghai upgrade.

After three significant jumps in validators signing for voluntary exits - one right after the Merge in September 2022, and two this year - we currently see an accumulated total of ETH 45,098 (equivalent to $83.3M) that will be made accessible for stakers.

As described above, the stake withdrawal process will take two days for the total amount to have exited the Beacon Chain, which means we will see at least 45,098 ETH ($83.3M) exiting the Beacon Chain between 12-Apr and the 14-Apr.

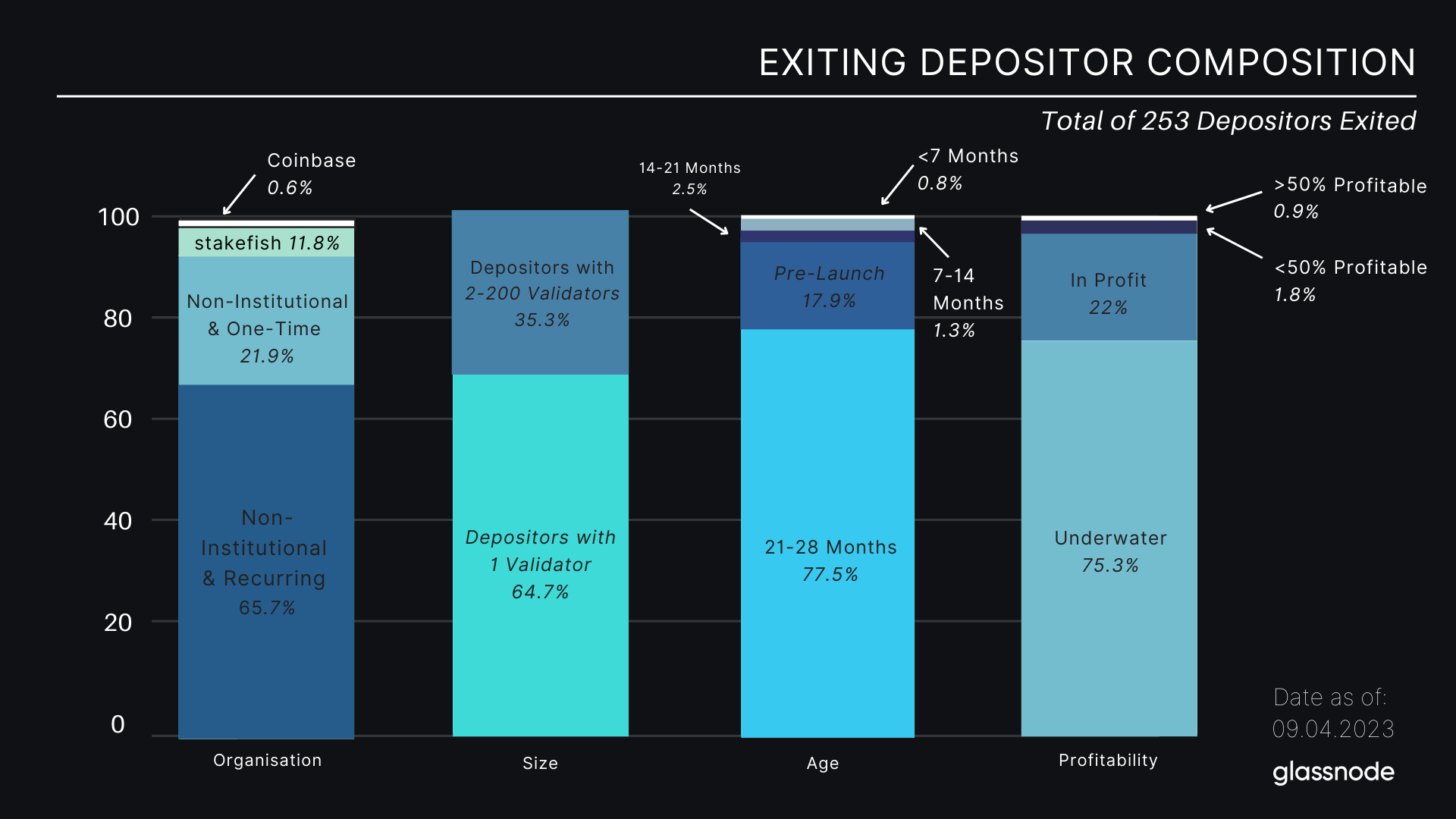

Referring back to our depositor segmentation, we can now determine the makeup of depositors who are likely to to initiate a full withdraw of their stake. We see that the already exited validators belong to a total of 253 depositors.

What stands out is that very few staking providers have withdrawn their validators. So far, of the top staking providers only Coinbase has announced that it will allow withdrawals immediately after the Shanghai upgrade. Lido is said to enable withdrawals only in May, and Kraken and Binance have not yet announced dates.

Additionally, we see exiting depositors are predominantly those with only one validator, and those who deployed their stake in the pre-launch phase or first quarter of the Beacon Chain lifespan. This timeframe coincides with the beginning of the bull run, which is why we see a high number of exiting depositors to be holding an unrealized loss.

We generally expect there to be little price pressure from these depositor groups, especially if we attribute a higher conviction to those early stakers. Given the staking landscape has evolved so significantly since genesis, these early solo-stakers are likely to be inclined towards withdrawing, and then redeploying it with a new staking provider setup to reduce the risks and overhead that come along with maintaining a staking setup. They may also wish to benefit from new or Liquid Staking Derivative tokens (LSDs), allowing them to maintain their ETH liquidity, and deploy it as collateral in DeFi, all while still earning Ethereum staking rewards.

Kraken is expected to shut down a significant number of its validators after its US staking service was challenged by the SEC. Another potential large withdrawal could come from Celsius Network, as it will reportedly sell its staked ETH as part of its bankruptcy process, although it is unlikely both institutions will immediately withdraw after the upgrade.

Even in the extreme case of a sudden rise in voluntary exits 27 hours prior to the Shanghai, we would still only see a limited increase in stake that actually becomes liquid due to the churn limit caps. At most, we can expect a maximum of 57,600 ETH ($109.4M) to be unstaked on the day of Shanghai. If the demand to exit remains high, we would see the same amount of ETH being unstaked on a daily basis until the churn limit readjusts.

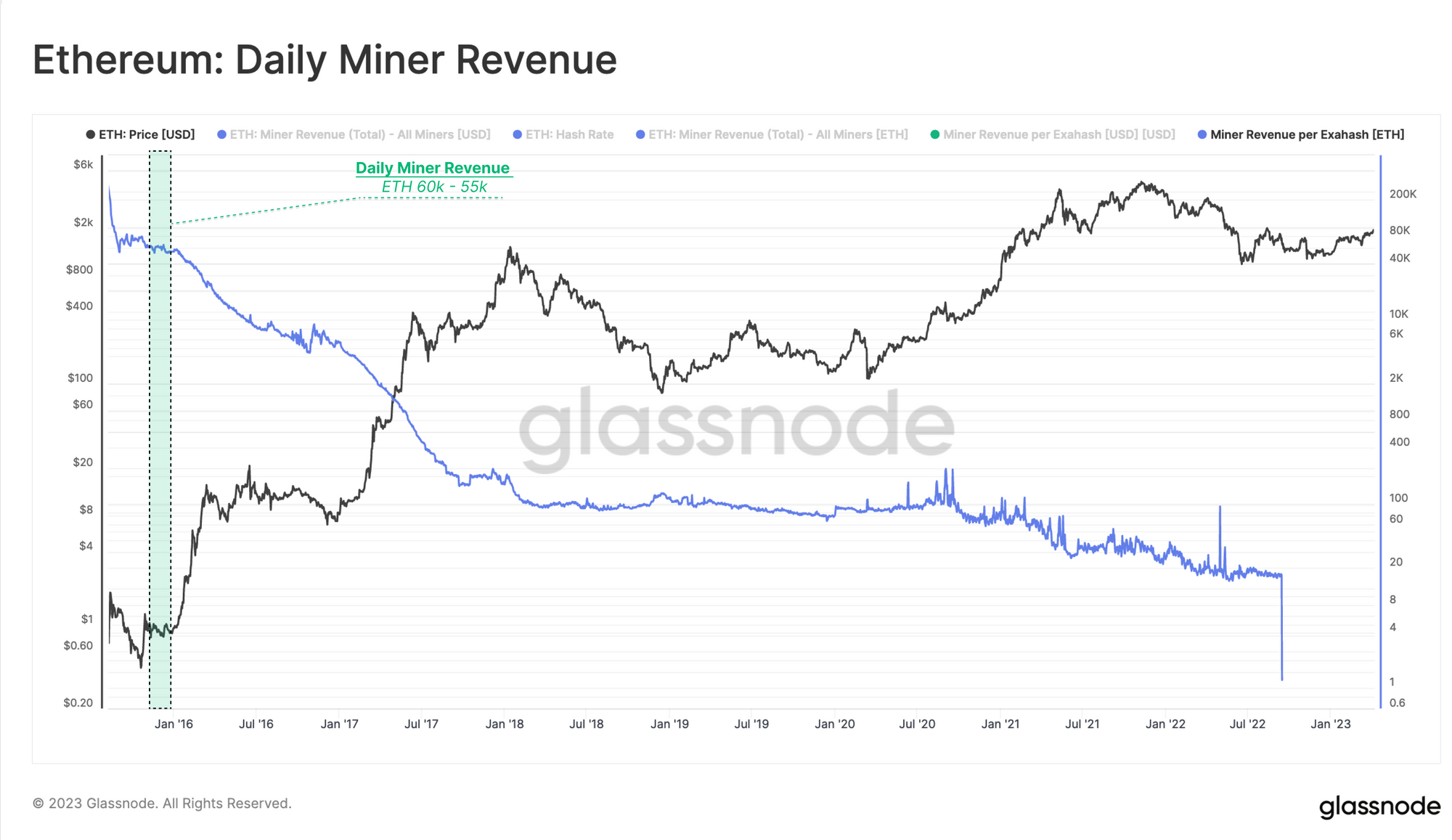

To put this into context, this amount of withdrawals would result in similar dynamics as we saw in the early days of Proof-of-Work, where miner revenues oscillated around that range (albeit at sub $1 ETH prices).

Estimating the Total Supply Impact

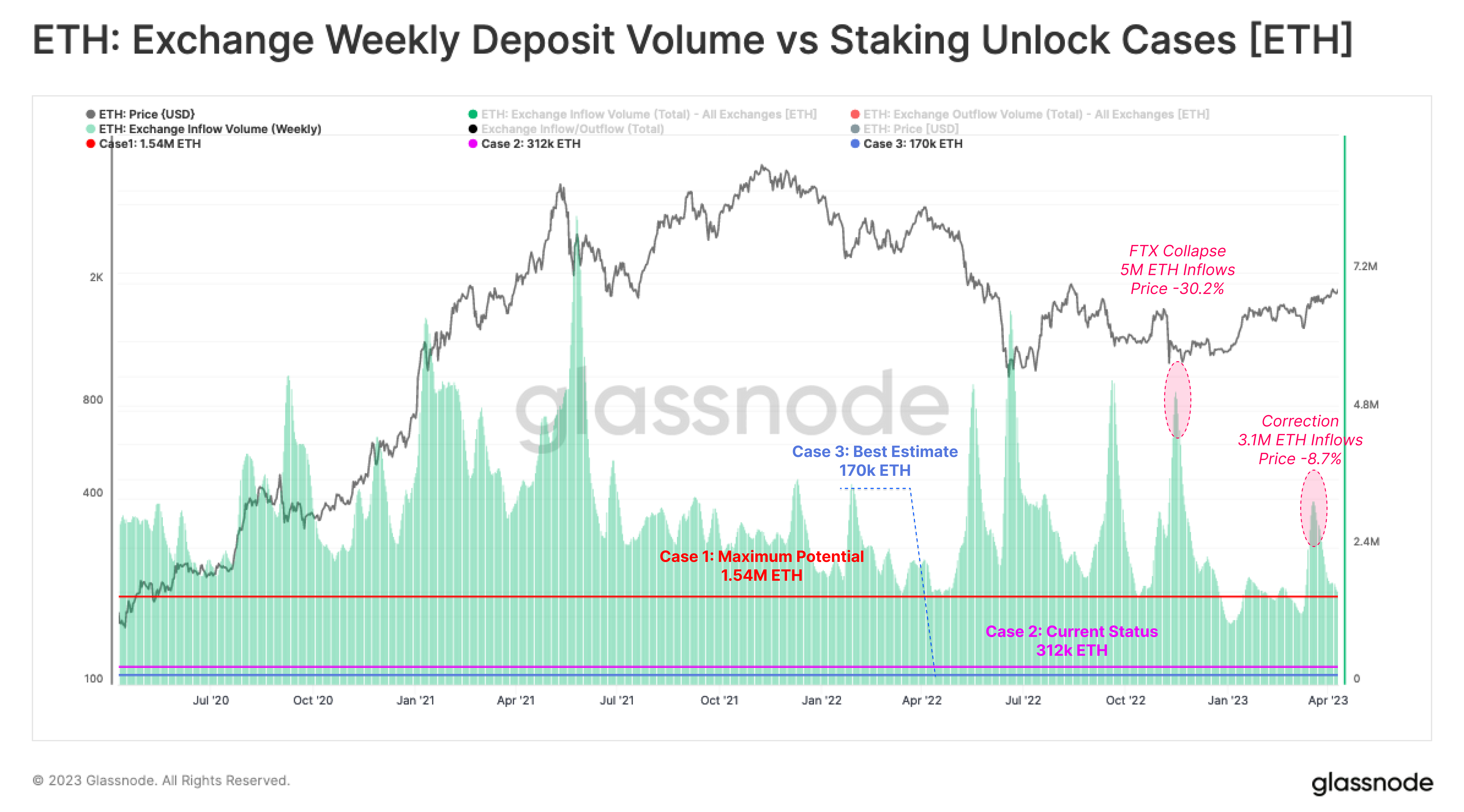

Taking into account both partial and full withdrawals, we can model the potential supply pressure during the first week after the Shanghai upgrade. We have three cases for the expected stake to be unlocked, and prone to be sold by the owner:

- Case 1: In the most extreme case, where the total accumulated rewards as well the permitted maximum amount of stake per week will be withdrawn and sold, we could see a total of 1.54M ETH ($2.93B) becoming liquid.

- Case 2: The current status quo, with only 00x0 credentials receiving staking rewards and 45k ETH to be exited and sold, would see around 312k ETH($592M) becoming liquid over the first week.

- Case 3: Our Best Estimate based on a 50% withdrawal credential update, our segmentation of depositors, and assumptions regarding investor conviction, and profitability. Also believing that the current number of exiting valiators will double around the Shanghai upgrade, we estimate a total of 170k ETH ($323M) to be sold.

To put these numbers into perspective, we can compare this to typical weekly exchange inflow volumes, with example events like FTX collapse to gauge potential scale. Here, we can see that even the most extreme case of 1.53M ETH is still within the range of average weekly exchange inflow. In other words, in the most extreme case the average weekly exchange inflow would double, which would fall into the scale of the recent market correction, with price falling 8.7% but will still be far below the scale of inflows during FTX collapse with price falling 30.2% respectively.

Given the Shanghai upgrade is widely expected and understood, based on this analysis, the unlock event is on a similar scale to day-to-day trade for ETH markets, and is therefore unlikely to be as dire as many speculate it to be.

Summary and Conclusions

While it is impossible to fully predict the outcomes of the Shanghai upgrade, this analysis sought to address circulating concerns about the economic implications of the supply unlock event.

When looking at staked ETH through the lens of depositors, and segmenting them into different groups, we shed light on the most likely cohorts to generate sell-side pressure. The main bulk of unlocked staking rewards are expected to be from users redeploying towards liquid staking providers, which already have little need to sell due to being underwater.

Currently, there are only 253 depositors waiting to exit their stake, which is a remarkably small number. Most of them are solo-stakers, or stakers from the early days of the Beacon Chain. This leads us to believe that they are the most likely to have a high conviction rate, and withdrawals are most likely related to a change in their technical setup, rather than exiting their position.

Even in the most extreme case of an exodus of validators, Ethereum’s design of the Proof-of-Stake exit queue will limit the amount of stake that can be drained form the pool at once. Therefore the economic impact of such an even would be stretched out over days to weeks. Based on our analysis, the impact on the Ethereum economy is expected to be a lot less dramatic than many have painted it to be. It is arguably more likely that the technical delivery of the upgrade will bolster a growing staking industry, which seeks to better serve holders of Ether over the long-term.

Disclaimer: This report does not provide any investment advice. All data is provided for information and educational purposes only. No investment decision shall be based on the information provided here and you are solely responsible for your own investment decisions.

- Join our Telegram channel

- Visit Glassnode Forum for long-form discussions and analysis.

- For on-chain metrics, dashboards, and alerts, visit Glassnode Studio

- For automated alerts on core on-chain metrics and activity on exchanges, visit our Glassnode Alerts Twitter