Spot Driven Rally

In this edition, we analyse the surge in both spot trading, and onchain exchange volumes for Bitcoin underlying the strong YTD performance. The market has also transitioned into a euphoric phase, as profit-taking has climbed accordingly.

Executive Summary

- Bitcoin’s strong performance over the last 12 months is supported by a surge in both spot trade volume but also exchange deposit and withdrawal volumes.

- By inspecting the cumulative volume delta (CVD), we can see that a majority of 2023 saw net selling activity on the taker side, even though corrections have been historically mild and less than 20%.

- Profit taking by long-term holders spiked meaningfully into the $73k ATH and is cooling down in recent weeks. This comes alongside an uptick in new demand brought on by the US spot ETFs.

Rising Speculation

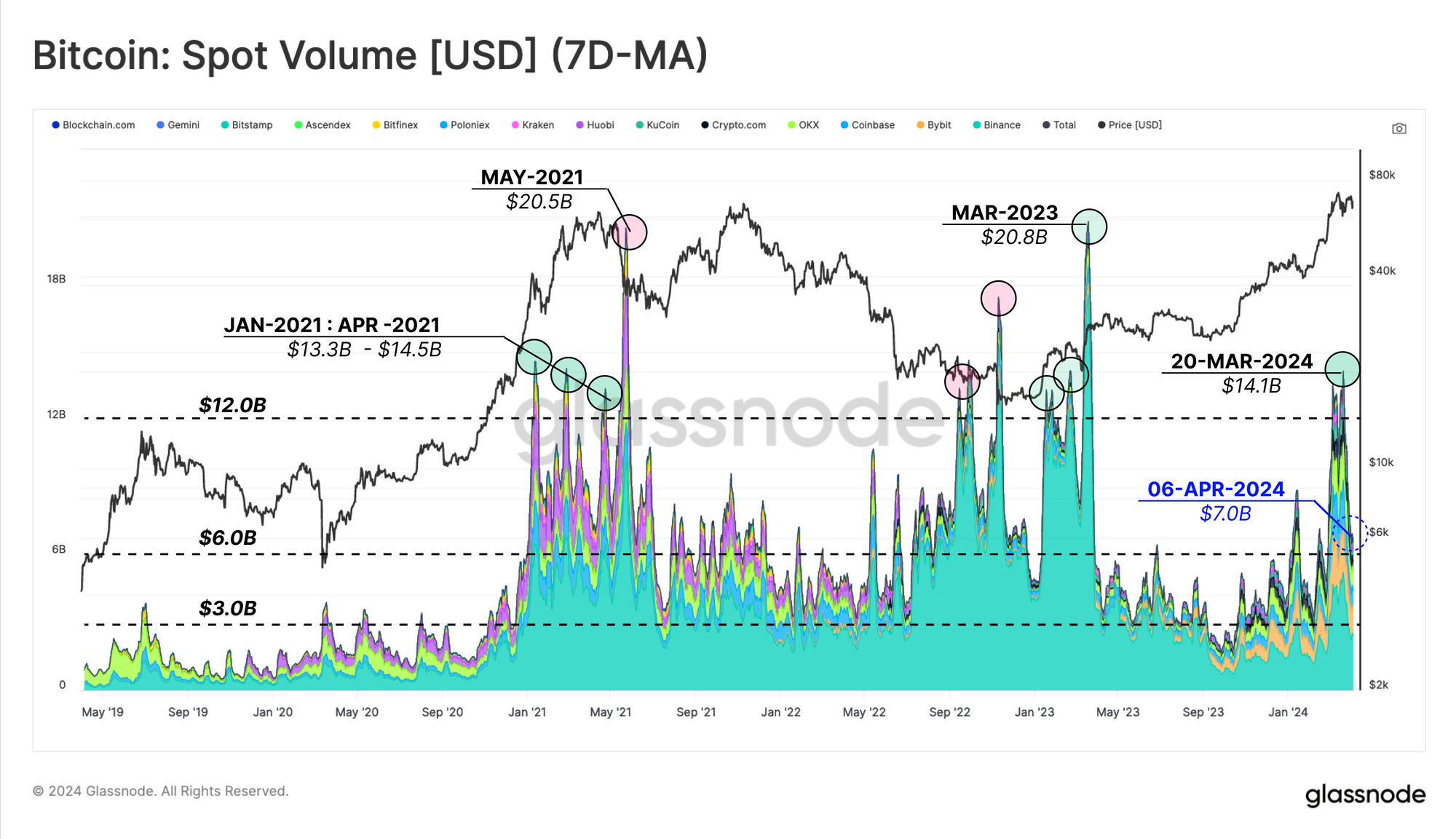

It continues to be an impressive year for Bitcoin, with prices consolidating between $64k and $73k over the last week. Bitcoin markets have seen a surge in spot trade volume since the US Spot ETFs went live in early January 2024, with daily volumes peaking at ~$14.1B in mid-March as the market reached the $73k ATH.

This magnitude of spot trade volume is equivalent to the height of the 2020-2021 bull market, although it has started to cool down in recent weeks, currently at $7B/day.

Binance still commands a 37.5% market share in spot markets; however, this dominance is declining relative to the prior cycle. In 2021, Binance accounted for around 50% of trade volume in 2021, but also an incredible 85%+ in the deepest phase of the 2022 bear market.

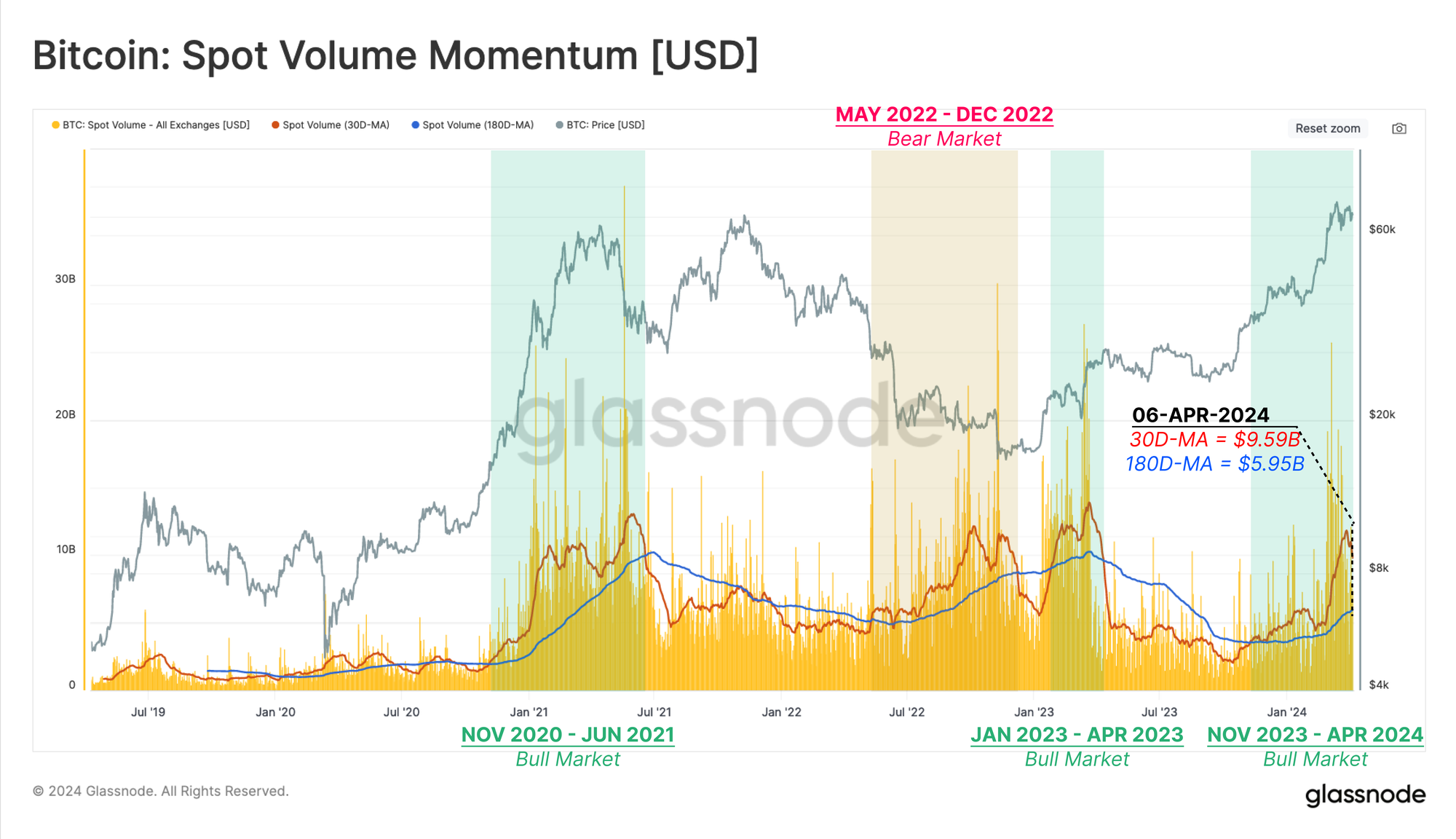

To assess overall market momentum, we can employ a simple slow/fast-moving average model applied to spot volumes. Here, we compare the 180D-MA (slow) and 30D-MA (fast) to assess whether spot trade volumes are warming up or cooling down.

Price action since October 2023 has seen the faster average trade significantly higher than the slower one, indicating that the YTD performance is supported by strong demand in spot markets. A similar structure is apparent during the 2021 bull run.

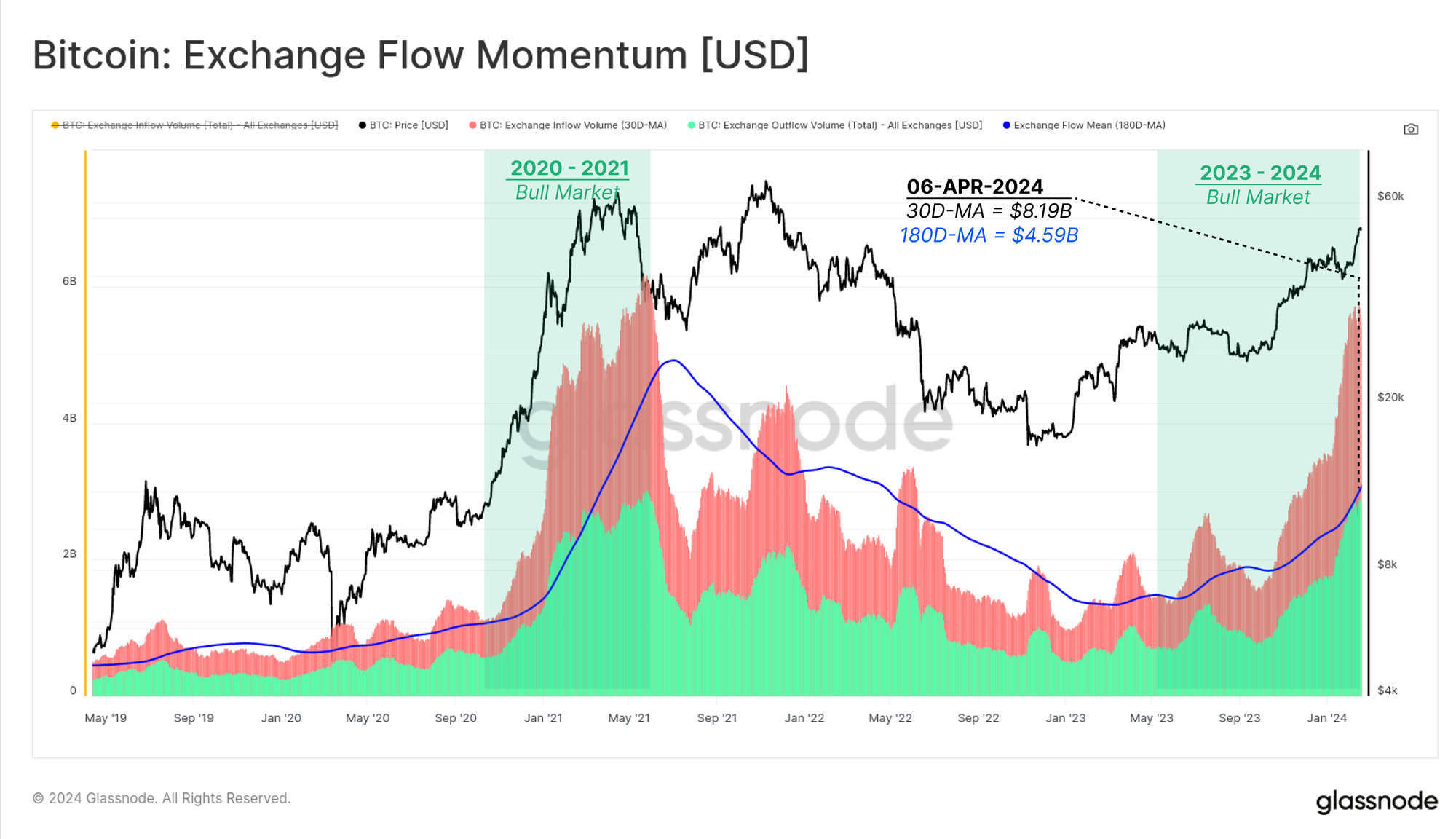

To bolster this observation, we can apply a similar fast/slow momentum indicator to the on-chain transfer volumes deposited 🔴 or withdrawn 🟢 from all exchanges wallets we monitor.

We can see a similar positive momentum signal to what has been in play since July 2023, suggesting the flow of coins in and out of exchanges is also heightened. The monthly average of total Exchange Flows (inflows plus outflows) is currently at $8.19B per day, significantly higher than the peak in the 2020-2021 bull market.

Overall, Bitcoin’s YTD price action is supported by a significant uptick in spot trade volume, and exchange flows onchain.

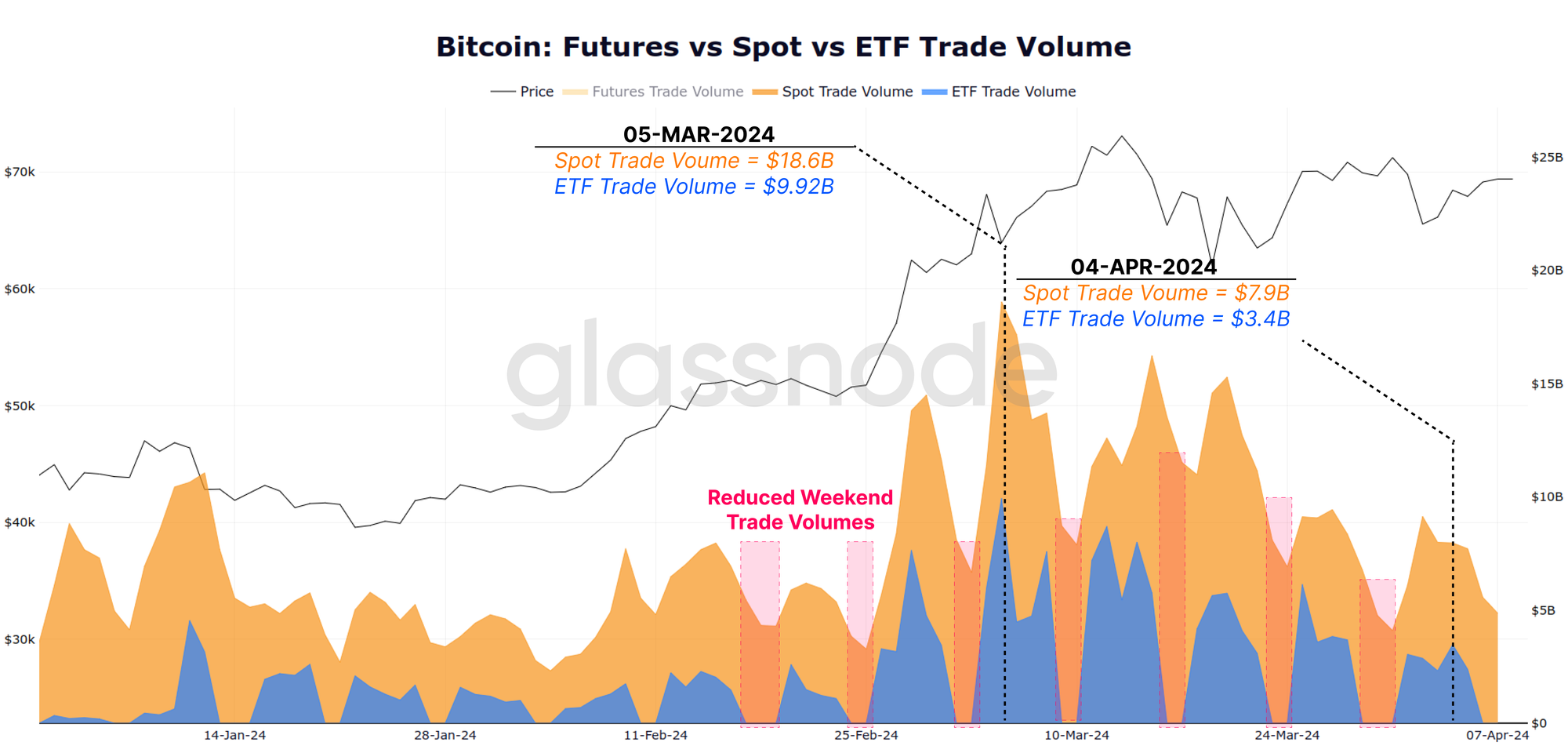

Our recent newsletter (WoC 10) showcased how the new US Spot ETFs have become a dominant force in the market. These new instruments introduced a significant source of new demand into the market, more than offsetting the daily issuance, as well as sell-side pressure from GBTC and existing holders.

This conclusion can be reinforced by comparing spot trade volumes 🟧 and ETF trade volumes 🟦. There is strong correlation between these markets, with ETFs trading around 30% of the size of global spot markets. We can also see the seasonality impact of weekends, where ETF markets are closed, and spot trade volumes are notably lower.

Buy Side vs Sell Side Volume

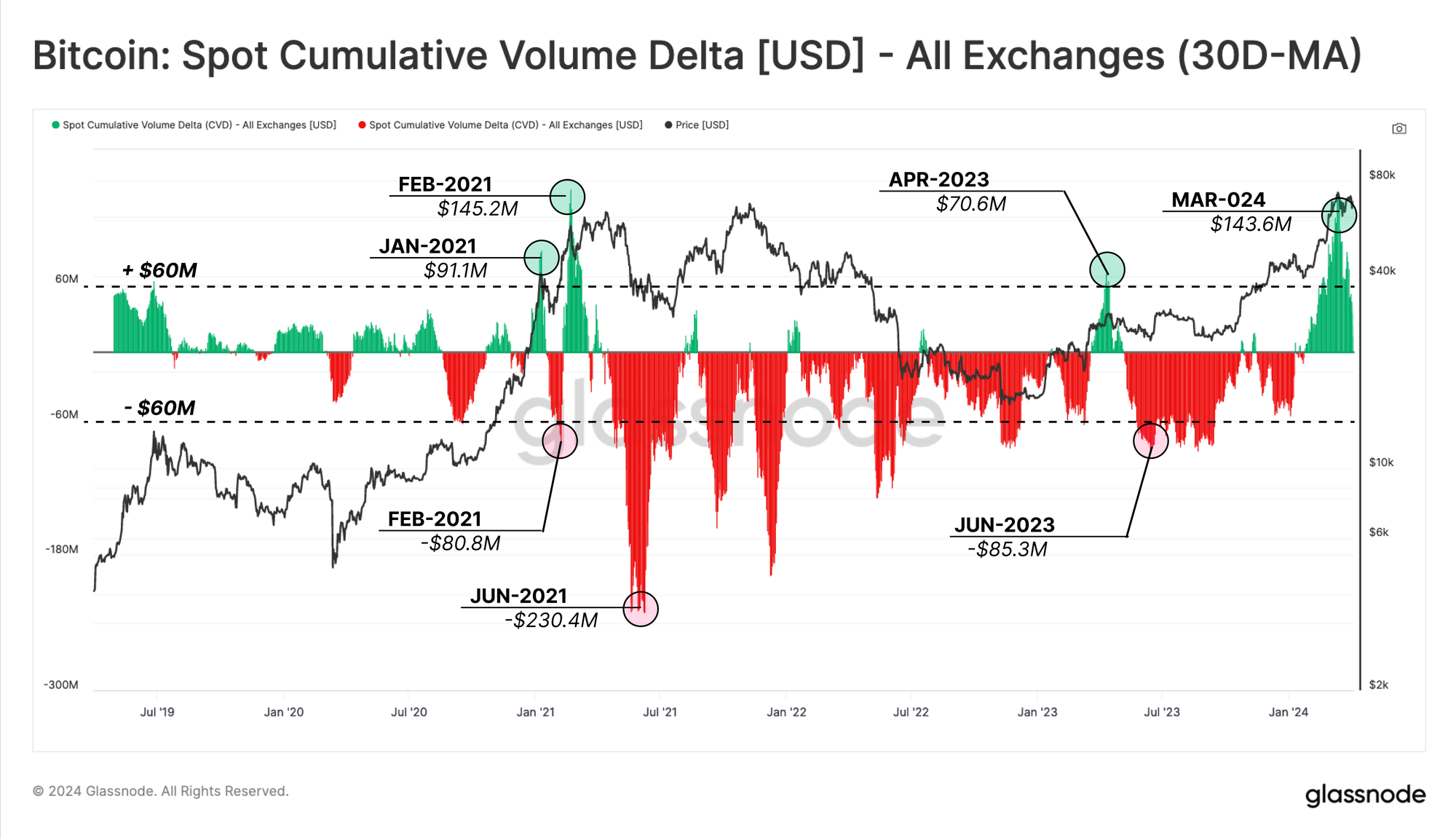

Another tool that enables us to characterise spot markets is the Spot Cumulative Volume Delta (CVD). This metric describes the net bias in market taker buy vs sell volume, measured in USD.

Suppose we isolate the major positive peaks 🟩, where the taker buy volume minus the taker sell volume exceeds $60M. In that case, we can see a remarkable similarity between market sentiment in Q1-2021 and the post-ETF market.

By mid-March, the spot volume delta reached +$143.6M, which is slightly lower than the peak in February 2021 ($145.2M) but indicates a major shift towards a net buy-side bias. Notably, most of 2023 experienced a net sell-side bias in spot markets despite the fact that markets had minimal pullbacks, and steadily climbed higher.

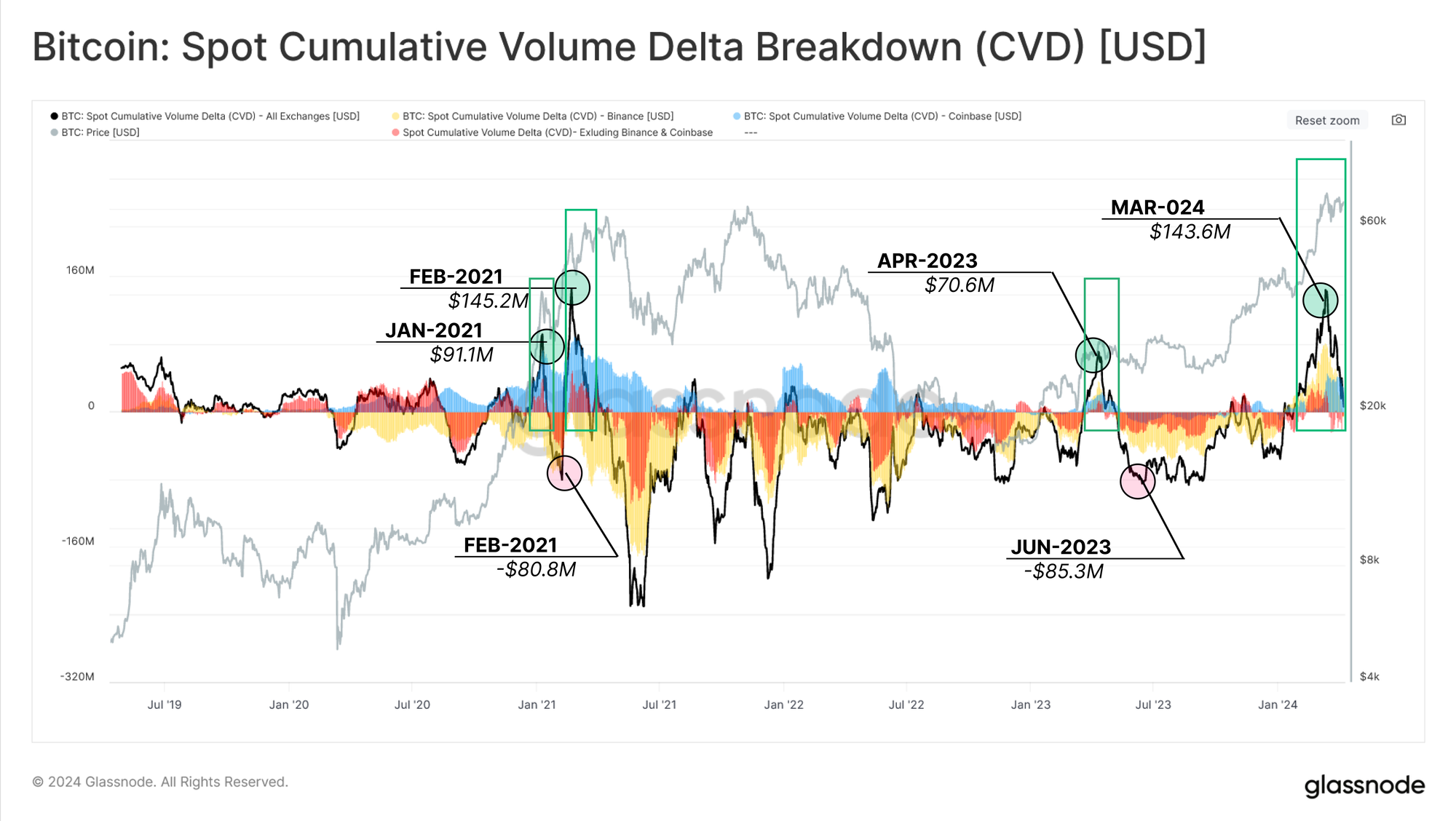

We can break this Spot CVD metric into individual volume deltas at specific exchanges. The chart below represents the following traces:

- Binance 🟨

- Coinbase 🟦

- All Other Exchanges 🟥

During the 2020-21 bull market, Coinbase and Other Exchanges experienced a net buy-side bias, while Binance saw the sell-side dominate. Much of 2023 saw a net sell-side bias across all exchanges until October, when this flipped into a net buy-side.

One interpretation would be that the significant sell-side bias by takers in 2023 was met with a comparatively larger bid on the maker side. This patient buy side throughout last year could be a key reason for the relatively light pullbacks (max -20%) seen since the FTX lows (stay tuned for a chart showing this later in this report).

Navigating The Cycle

We have established that the strong performance of Bitcoin over the last 12-18 months is supported by a meaningful uptick in trade volumes. Next, we will explore charts that can help us navigate the market cycle during price discovery.

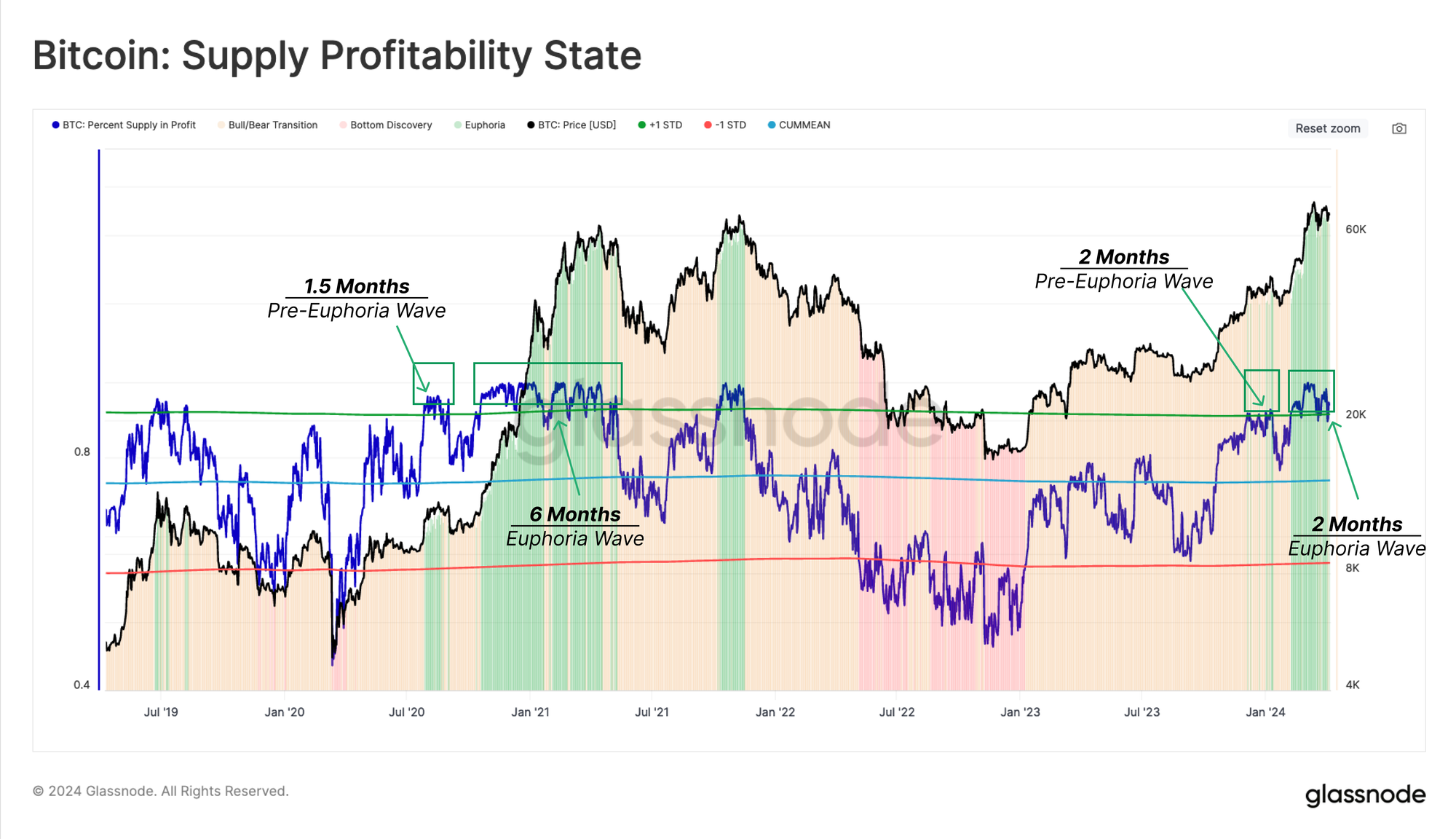

A vital tool for mapping bitcoin cycles is the Supply Profitability State, which considers the percentage of the total coin supply which are held in profit. The chart below represents the Percentage of Supply in Profit alongside two statistical bands, set at +1 SD 🟢 and -1 SD 🔴.

Periods when supply in profit trades above +1SD (~95% in profit) are naturally aligned with the market rallying towards the prior cycle ATH (Pre-Euphoria), as well as breaking beyond it (Euphoria).

We can see a common pattern in this tool in the prior cycle, where an initial Pre-Euphoria rally tests the upper band and puts a super-majority of coins into profit. After a period of correction and consolidation, the market finally rallies up to and through the prior ATH, driving the oscillator well above 95% in profit status.

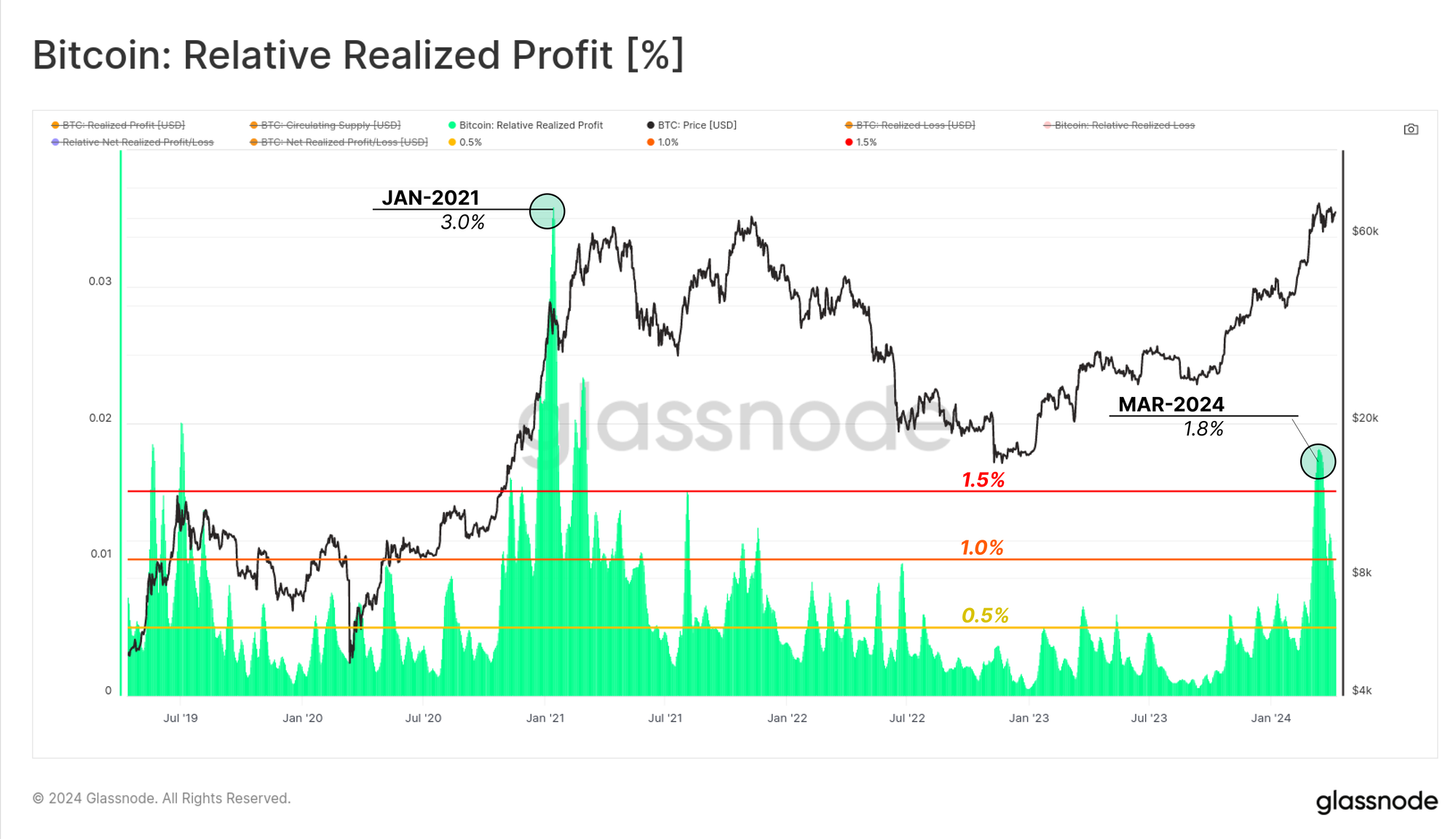

As a result, the unrealized profit held by market participants increases significantly. This of course, creates a growing incentive for investors to ramp up profit-taking (realizing profit). The following chart shows the weekly sum volume Realized Profit, normalized by market cap to compare across cycles 🟩.

As the market reclaimed the 2021 cycle high, this metric peaked at 1.8%, suggesting 1.8% of the market cap was locked in as profit over a 7-day period. This is significant but remains comparatively lower than the profit-taking intensity during the January 2021 rally (3.0%.)

In terms of market mechanics, this dynamic provides us with a few pieces of information:

- Profit-taking, typically by long-term holders, tends to ramp up around ATH breaks.

- Local and global market peaks are often established after major profit-taking events.

- Profit taken by one investor is matched by inflowing demand from the buying party on the other side. This gives us an insight into the magnitude of new capital flowing into Bitcoin.

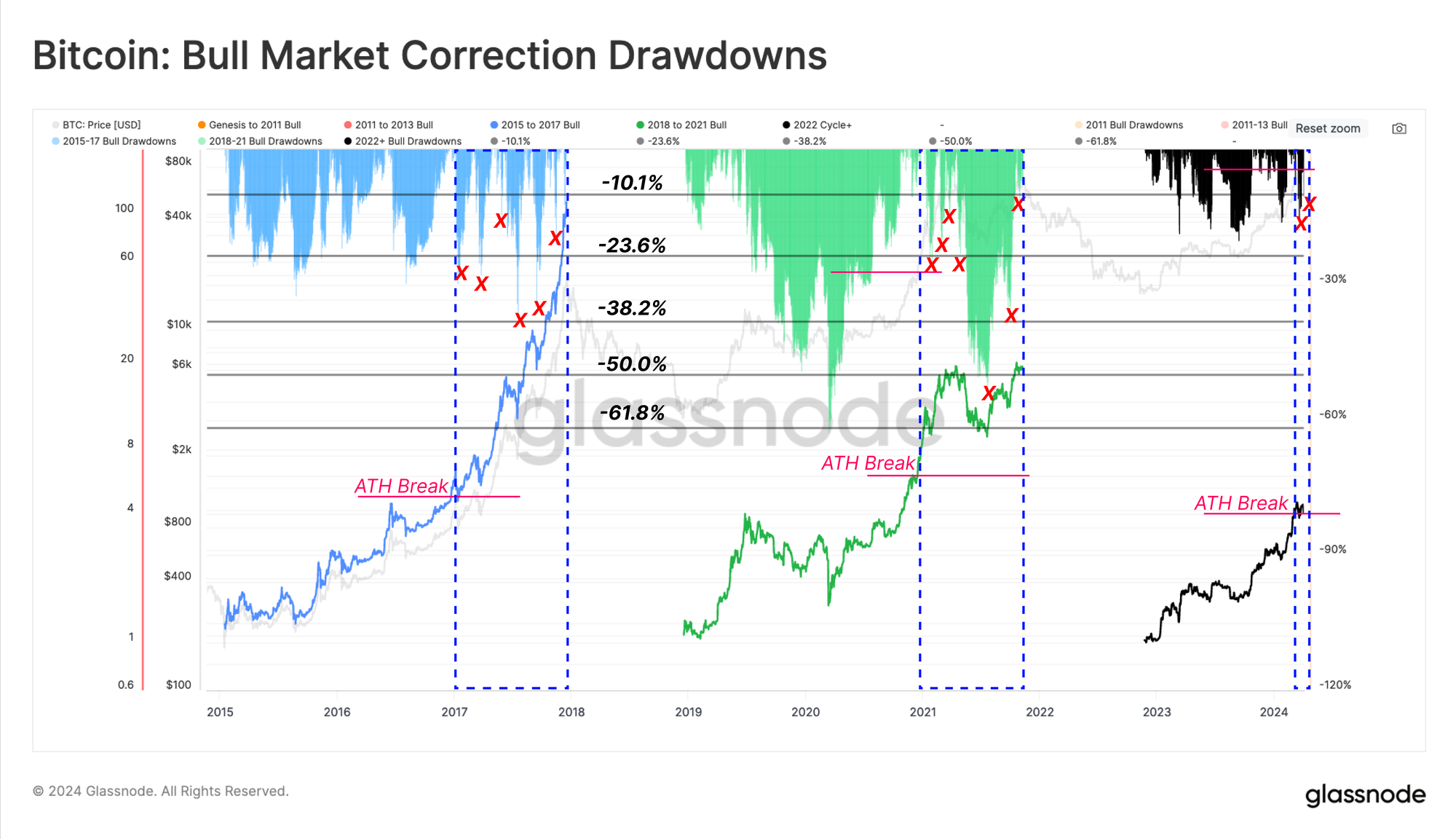

If we return to the magnitude of drawdowns we alluded to earlier, we can see that despite the large-scale profit taking by existing holders, the magnitude of pullbacks remains historically small.

If we compare the ATH break in prior cycles, it could be argued that current Euphoria phase (market in price discovery) is still relatively young. Previous Euphoria phases have seen numerous price drawdowns exceeding -10%, with the majority being much deeper, with 25%+ being commonplace.

The current market has seen just two ~10%+ corrections since the ATH was broken.

An Influx of New Investors

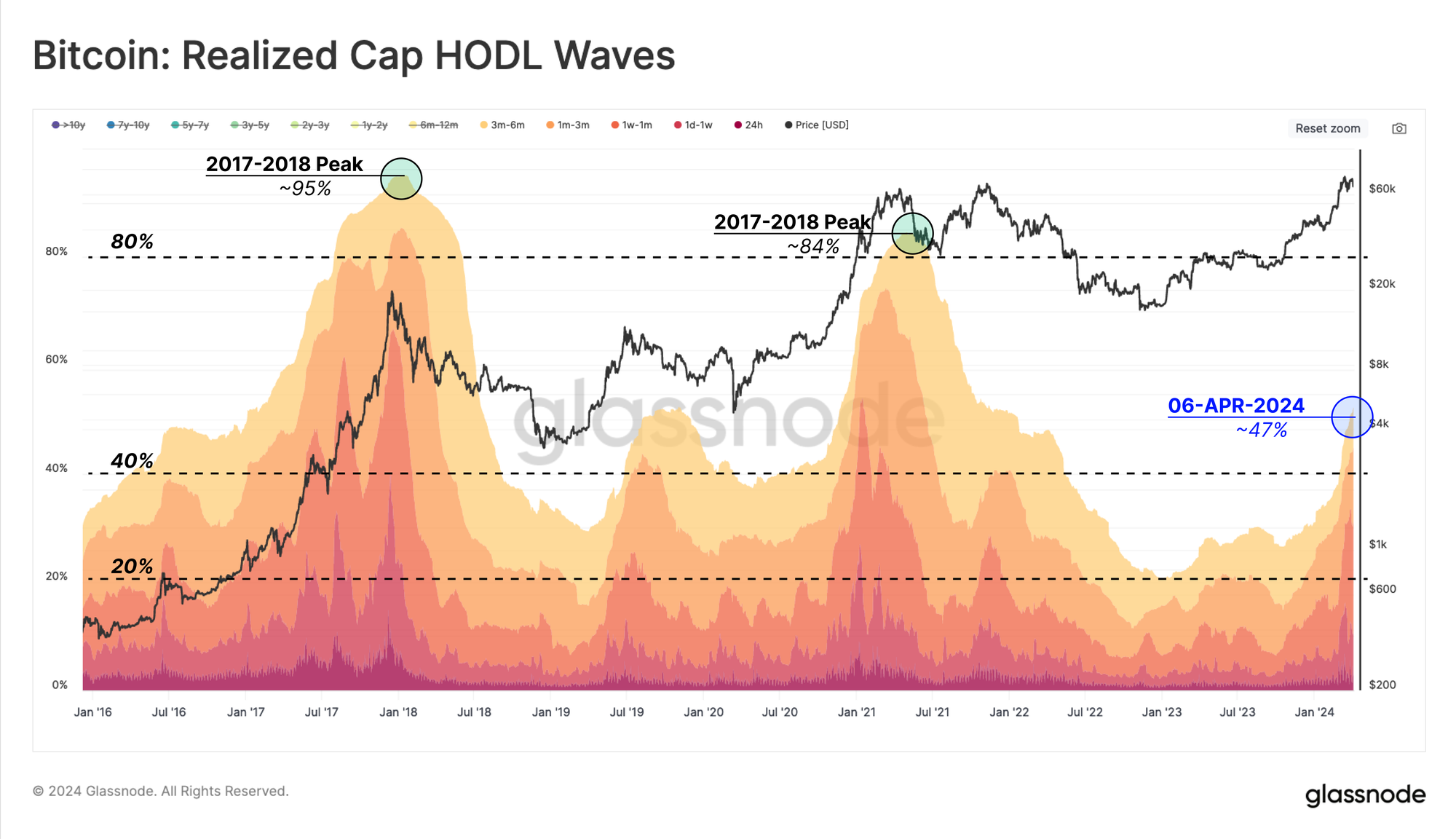

There are always two sides to a market; for every investor taking profits, another investor acquires those coins at a higher cost. We can visualise this influx of new investors by the rising share of wealth held by coins younger than 6-months in the Realized Cap HODL Waves.

During the last two bull markets, the aggregate share of < 6-month-old wealth reached between 84% and 95%, indicating a saturation of newer holders. This metric has increased dramatically since early 2023, rising from 20% on 1-Jan-2023 to 47% today.

This suggests that the capital held within the Bitcoin holder base is roughly balanced between long-term holders and new demand.

This also means that analysts should start to pay more attention to the behaviour of these new investors as their share of the capital increases.

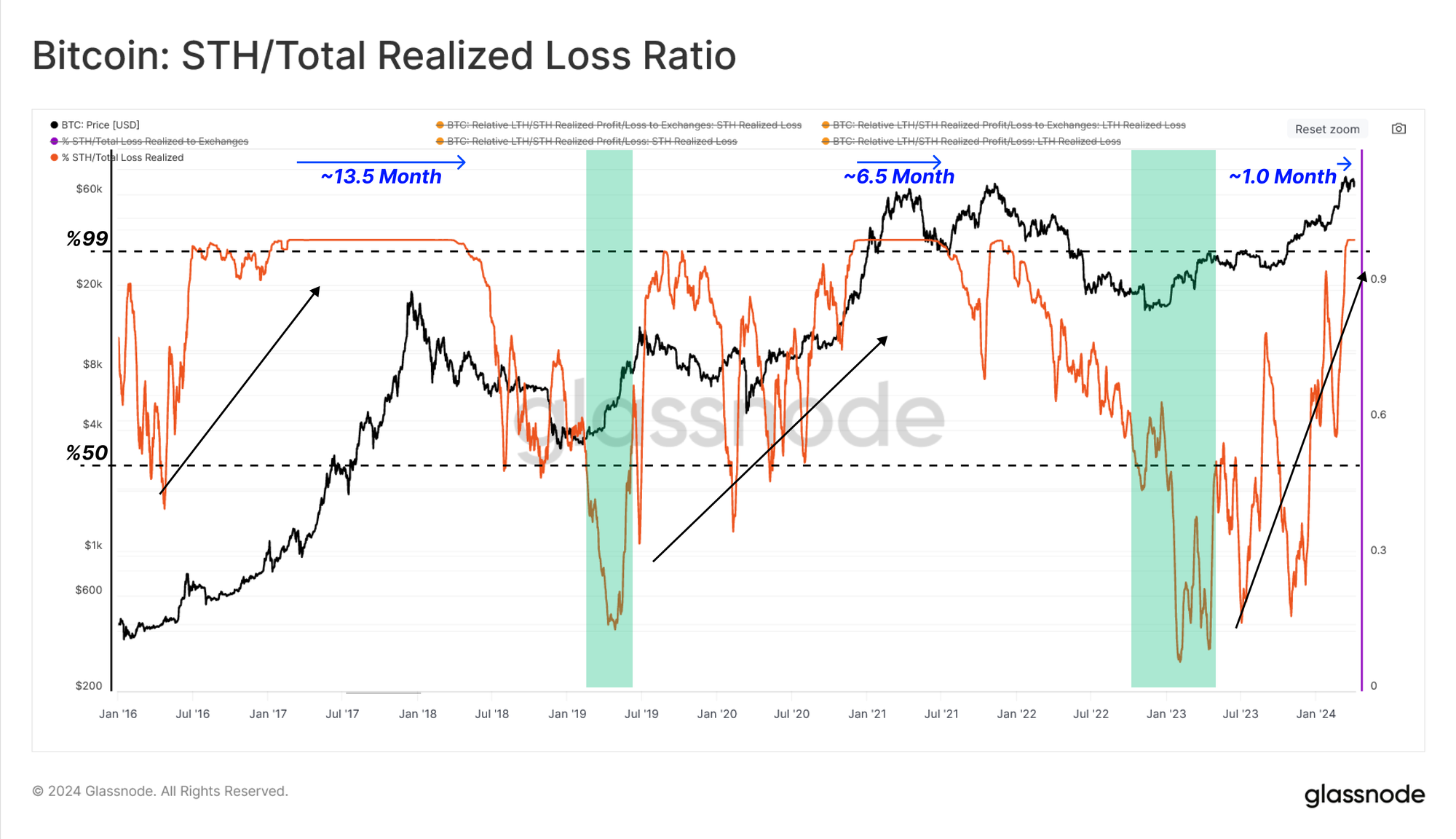

By definition, there are no Long-Term Holders with coins held at a loss shortly after a new ATH break (at least 155 days after the event). As such, Short-Term Holders (STHs) will dominate all onchain metrics describing supply or volume ‘in-loss’. Accordingly, STH now represents ~100% of the Total Realized Losses on spent coins 🔴.

If we consider this ‘STH Loss Dominance’ across prior cycles, we can see that this condition has lasted for between 6.5 and 13.5 months until the bear market sets in. The current market has only entered this condition for around 1-month so far.

Summary and Conclusions

The strong market performance of Bitcoin over the last 12 months is supported by a remarkable uptick in both spot trade volumes and onchain flows associated with exchanges. By analysing the Cumulative Volume Delta, we can also gauge that the demand side has been remarkably strong, albeit with bids patiently taking the maker side rather than the taker side.

With the market now above the 2021 ATH, profit-taking has ramped up but is cooling down in recent weeks. The balance of wealth is approximately balanced between long-term holders and new demand, suggesting the ‘Euphoria’ phase is still relatively early from a historical perspective.

Disclaimer: This report does not provide any investment advice. All data is provided for information and educational purposes only. No investment decision shall be based on the information provided here and you are solely responsible for your own investment decisions.

Exchange balances presented are derived from Glassnode’s comprehensive database of address labels, which are amassed through both officially published exchange information and proprietary clustering algorithms. While we strive to ensure the utmost accuracy in representing exchange balances, it is important to note that these figures might not always encapsulate the entirety of an exchange’s reserves, particularly when exchanges refrain from disclosing their official addresses. We urge users to exercise caution and discretion when utilizing these metrics. Glassnode shall not be held responsible for any discrepancies or potential inaccuracies. Please read our Transparency Notice when using exchange data.

- Join our Telegram channel

- For on-chain metrics, dashboards, and alerts, visit Glassnode Studio

- For automated alerts on core on-chain metrics and activity on exchanges, visit our Glassnode Alerts Twitter