Seeking Equilibrium

With prices tight, and the volatility spring coiled, the Bitcoin market looks increasingly ready to move out of the current equilibrium. As Long-Term Holder spending ticks marginally higher, we present a series of on-chain tools to help navigate the volatile road ahead.

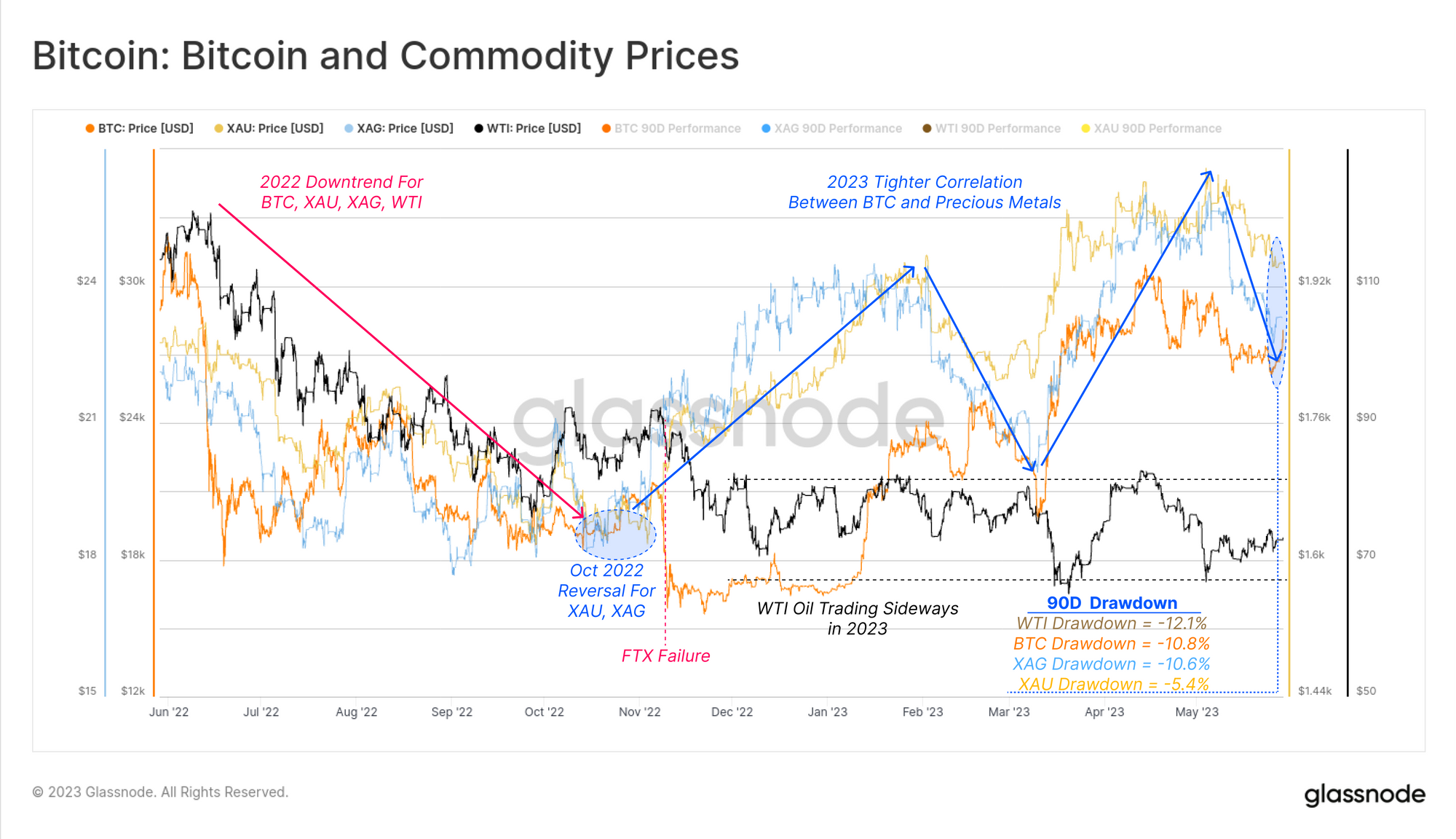

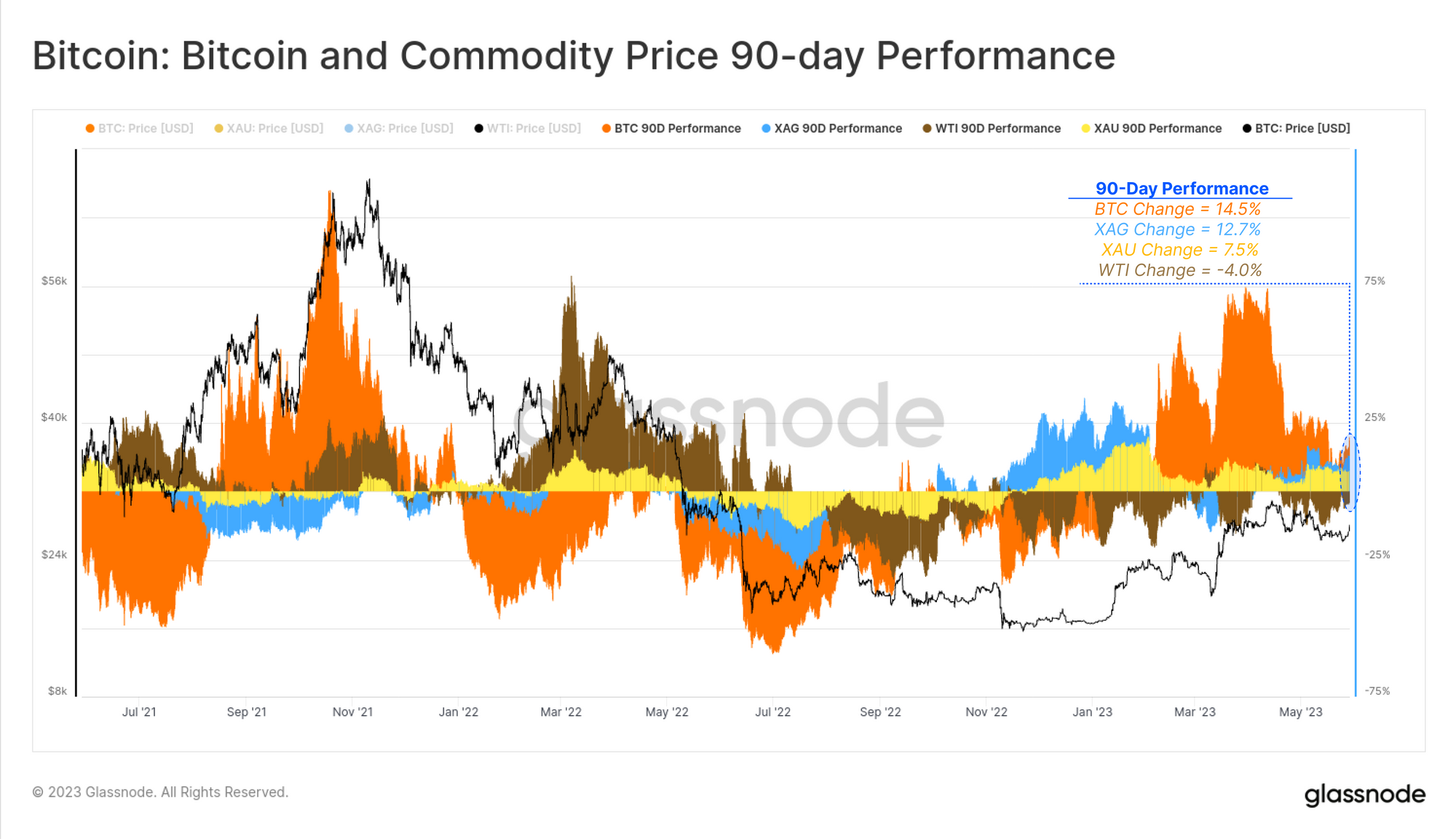

Since October 2022, global market liquidity has seen an uptick, with digital assets, and precious metal prices responding positively, and in an increasingly coupled manner. Both asset classes are currently experiencing their second uptrend correction of the year, with BTC and Silver down -10.8% and -10.6%, from their respective 90-day highs. Gold is holding up best, posting a -5.4% drawdown so far, whilst WTI Crude Oil prices continue to struggle, trading range-bound and down -12.1% since the April high.

Over the last 90-days, Crude Oil (WTI) declined -4.0%, whilst Gold (XAU) and Silver (XAG) have rallied 7.5% and 12.7%, respectively. Bitcoin however, continues to outperform, remaining 14.5% above the February close. BTC performance is weaker than the peak first quarter performance of 72%, but remains the strongest performer amongst these major commodities.

As we covered last week, the market appears to be gearing up for a regime of higher volatility. In this weeks report, we will seek to bound the problem, and assess the upper and lower psychological levels, where renewed investor participation is likely to come into play.

🪟 View all charts covered in this report in The Week On-chain Dashboard.

🔔 Alert Ideas presented in this edition can be set within Glassnode Studio.

Diminishing Momentum

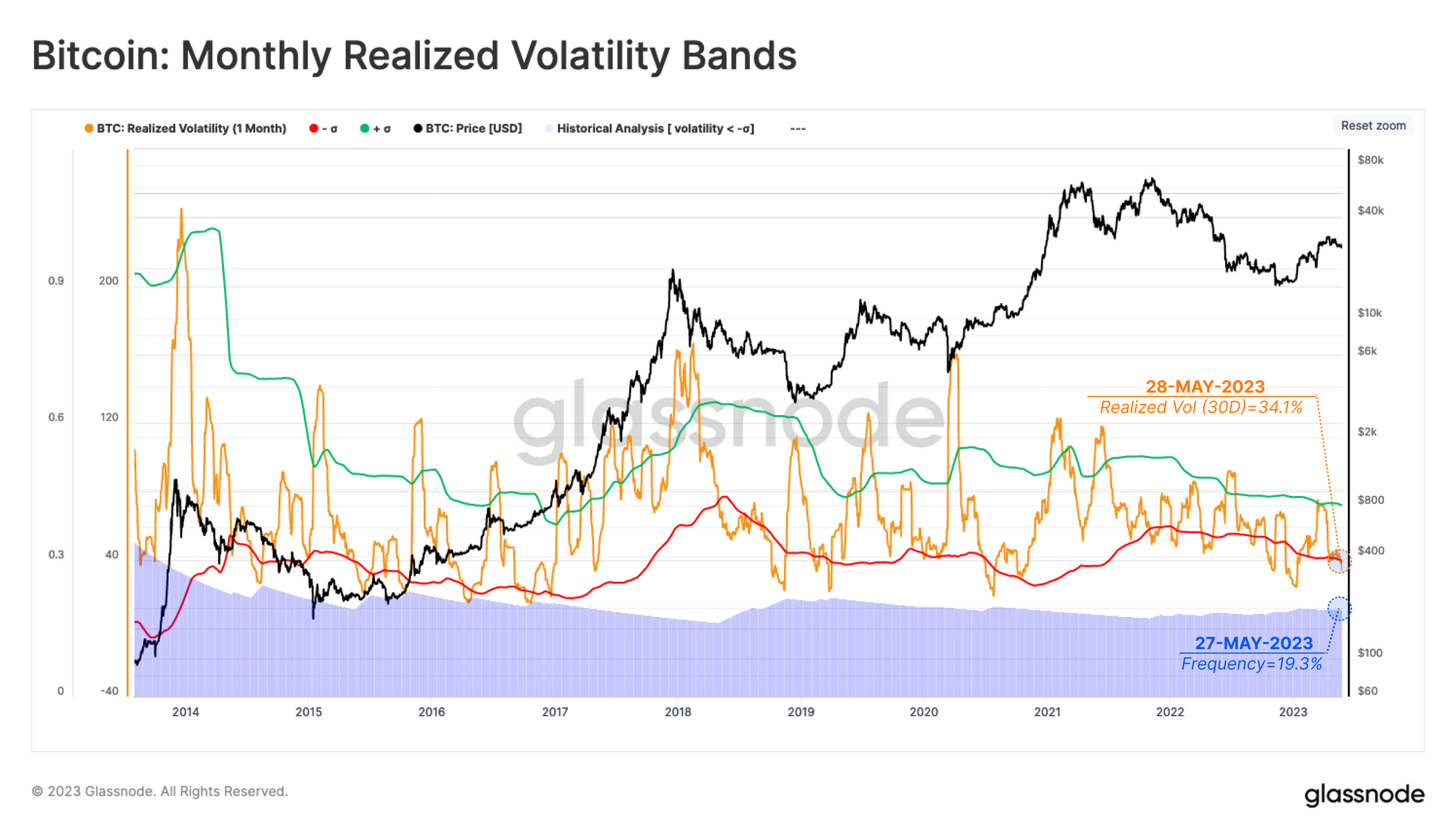

As momentum slows down in the Bitcoin market, the Monthly Realized Volatility has dropped to 34.1%, which is below the 1-standard deviation Bollinger Band. Historically, such low-volatility regimes only account for 19.3% of market history, and therefore expectations of elevated volatility on the near-term horizon is a logical conclusion.

🗜️ Workbench Tip: This chart is constructed using the standard deviation function std(m2, 365) to calculate Bollinger style bands for Realized Volatility.

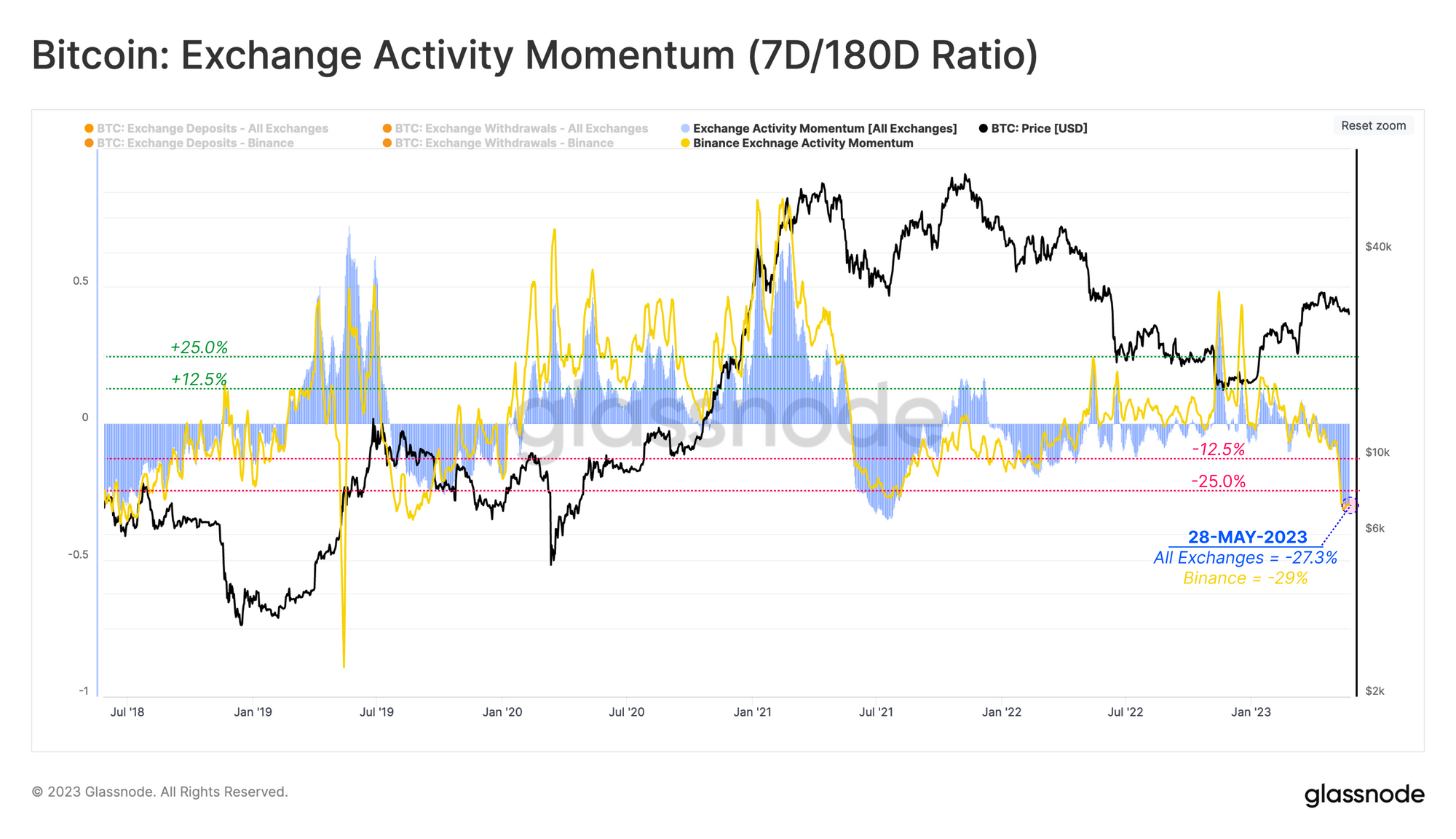

Transfer volumes on-chain remain cyclically low (WoC 21), which translates into a decline in activity associated with exchanges. To quantify this concept, we can compare the average number of exchange deposit/withdrawal transactions happening this week, to the 6-month median, producing an activity ratio.

We can see the cyclical trend of exchange activity for All Exchanges 🟦, and note that recent activity has dropped -27.3% relative to the last six months. To account for FTX, which completely ceased operations in Nov 2022, we can see a similar activity momentum for Binance only 🟨, suggesting investor activity is indeed exceptionally light.

Mapping Out An Equilibrium

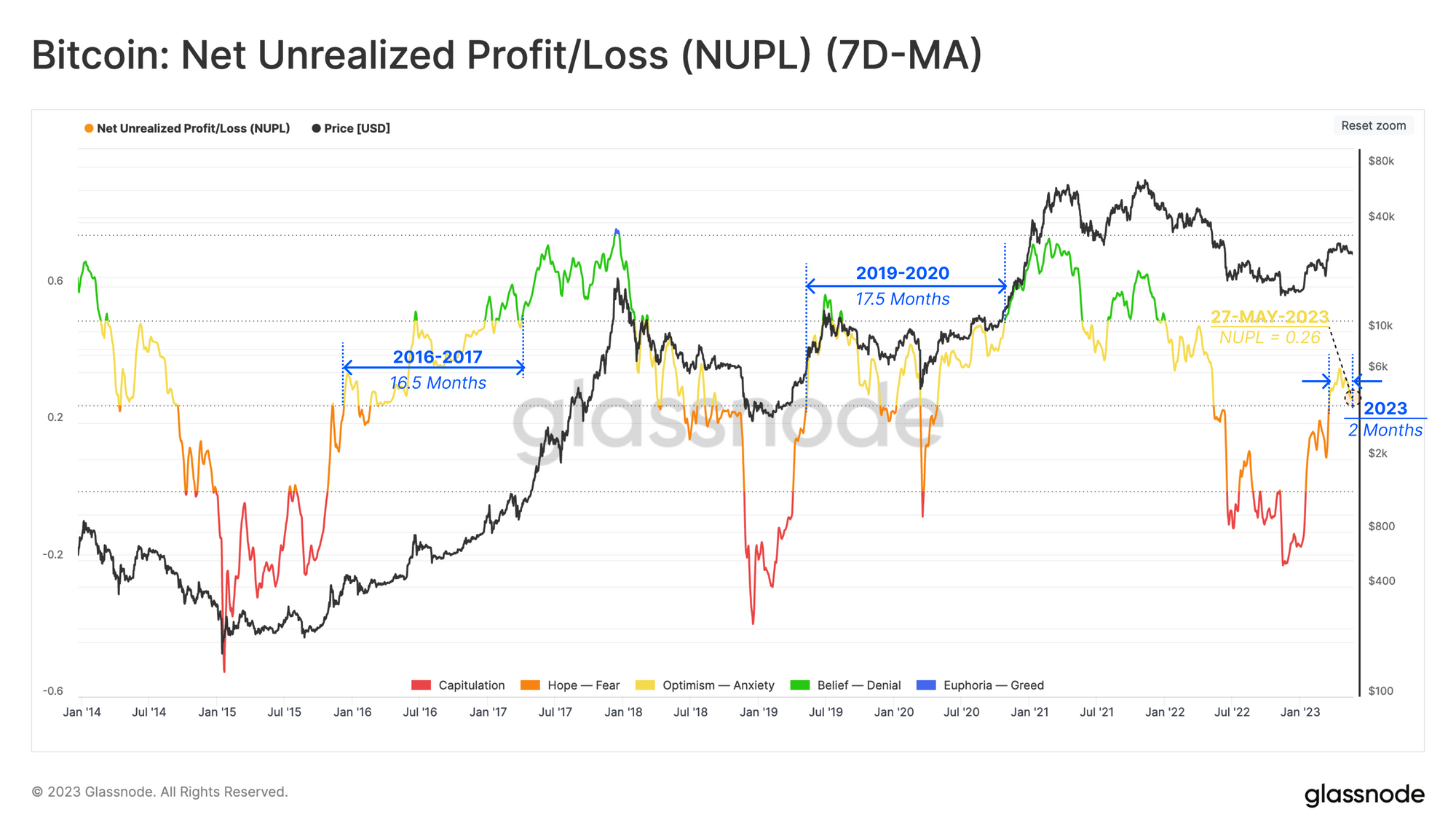

The lower volatility, and declining on-chain activity all point towards a sort of equilibrium phase. We will now leverage the Net Unrealized Profit/Loss (NUPL) metric to verify this hypothesis.

This indicator examines the dollar value of the total net profit or loss as a percentage of the market cap. From a macro perspective, we can define four phases in a cycle:

- Bottom Discovery 🔴: NUPL < 0

- Capitulation and Recovery 🟠: 0 < NUPL < 0.25

- Equilibrium Phase 🟡: 0.25 < NUPL < 0.5

- Bull Market Euphoria 🟢: 0.5 < NUPL

The current NUPL value of 0.29 is at the lower bound of the equilibrium phase, which is a zone where 37.5% of all Bitcoin trading days have been. This zone was reached in early March 2023, and persisted for around 16 months in the last two cycles.

🔔 Alert Idea: NUPL (7-day SMA) breaking below 0.25 would indicate that market profitability has declined back into the Capitulation and Recovery phase, and may suggest weakness.

Psychological Ranges

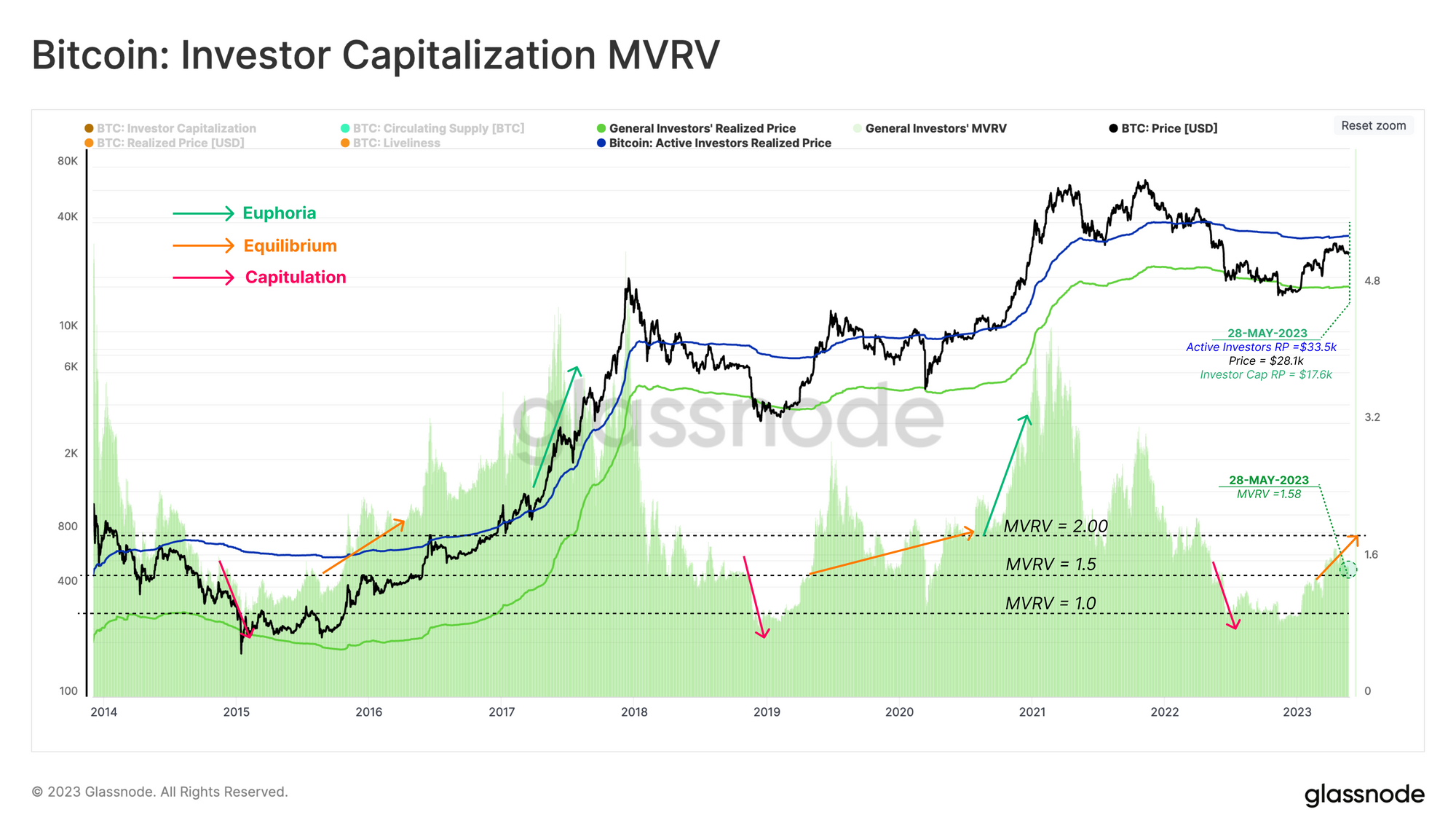

We can also utilize a set of investor cost basis to bound the likely boundaries of near-term volatility. The goal is to find price levels which are likely to elicit a significant psychological response from a larger proportion of holders.

The Active Investor Cost Basis 🔵 is currently trading at $33.5k, which accounts only for investors actively participating in the market, and provides a near-term upper bound price model. With the Active Investor MVRV at 0.83, it suggests that many 2021-22 cycle buyers are still underwater, and may be waiting for break-even prices to liquidate their holdings.

🔔 Alert Idea: Price breaking above $33.5k would indicate that the average investor from the 2021-22 cycle is now back in profit, and reflects a psychological area of interest.

A lower bound pricing model can also be identified, seeking an approximate macro support in the case of a significant market deterioration, such as the COVID Crash March of 2020. The Investor Cap Price model is calculated as the difference between the Realized Cap and the Thermocap, reflecting a floor model based on investor holdings, excluding miners.

We can see that the Investor Price model was briefly intersected during the March 2020 sell-off, and is currently trading at $17.65k. With Investor Capital MVRV currently at 1.58, it falls within a very similar equilibrium range to the 2019-20 mini-market cycle.

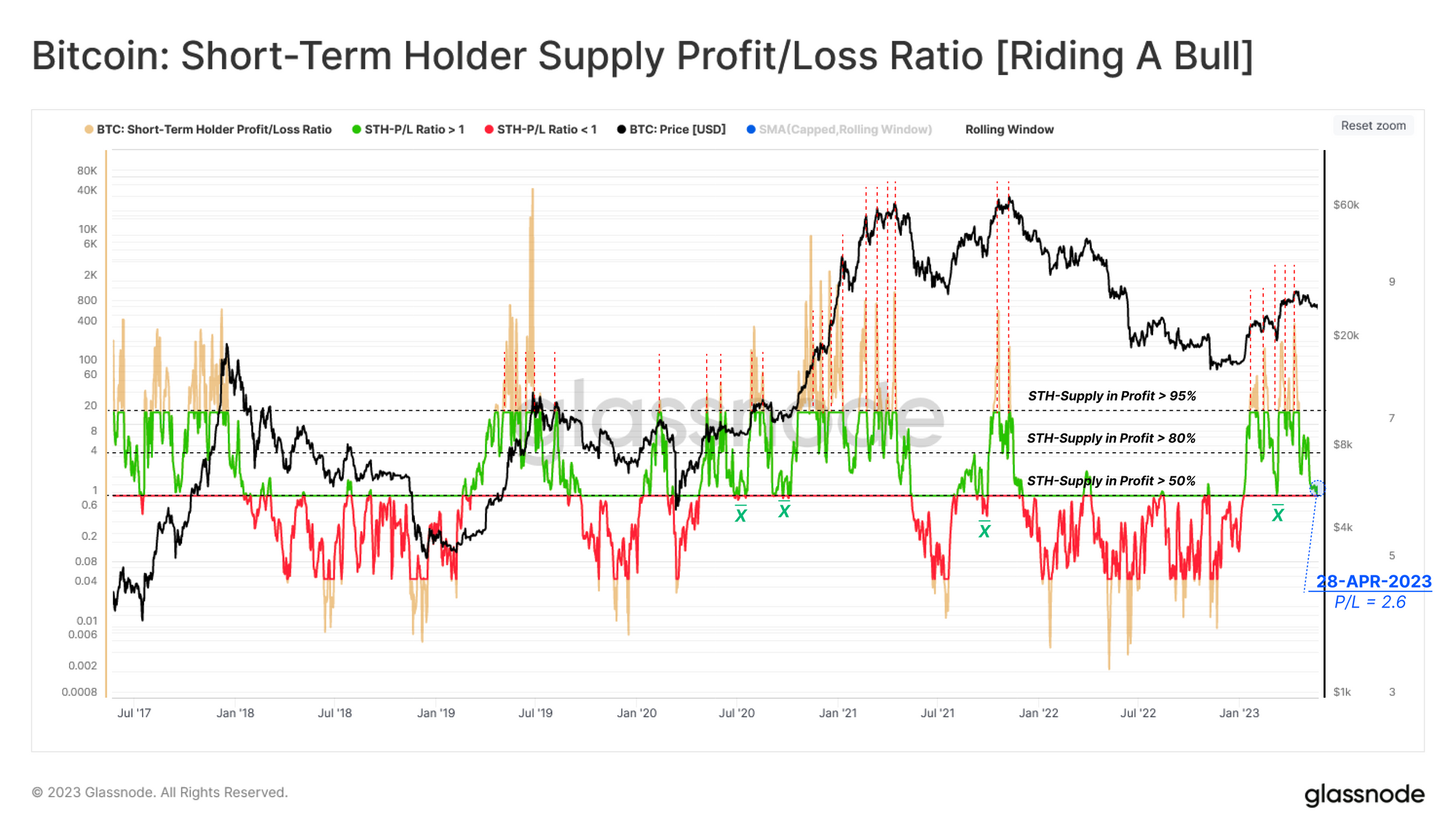

The market seems to have little gravity pulling it in either direction at present. We can also see that prices have returned to the Short-Term Holder (STH) cost basis, and reset several unrealized profit/loss metrics.

The STH Unrealized Profit / Loss Ratio (introduced in WoC 18) has cooled off significantly, returning to a break-even level of 1.0 and then bouncing back to 2.6. This indicates a balanced position of profit and loss for new investors. Falling below this level tends to precede a more extensive price contraction, however, the market tends to find support at this level during resilient bull runs.

The Road Higher

Having established that the market is in equilibrium, we can use on-chain tools to provide a macro roadmap of this phase from prior cycles.

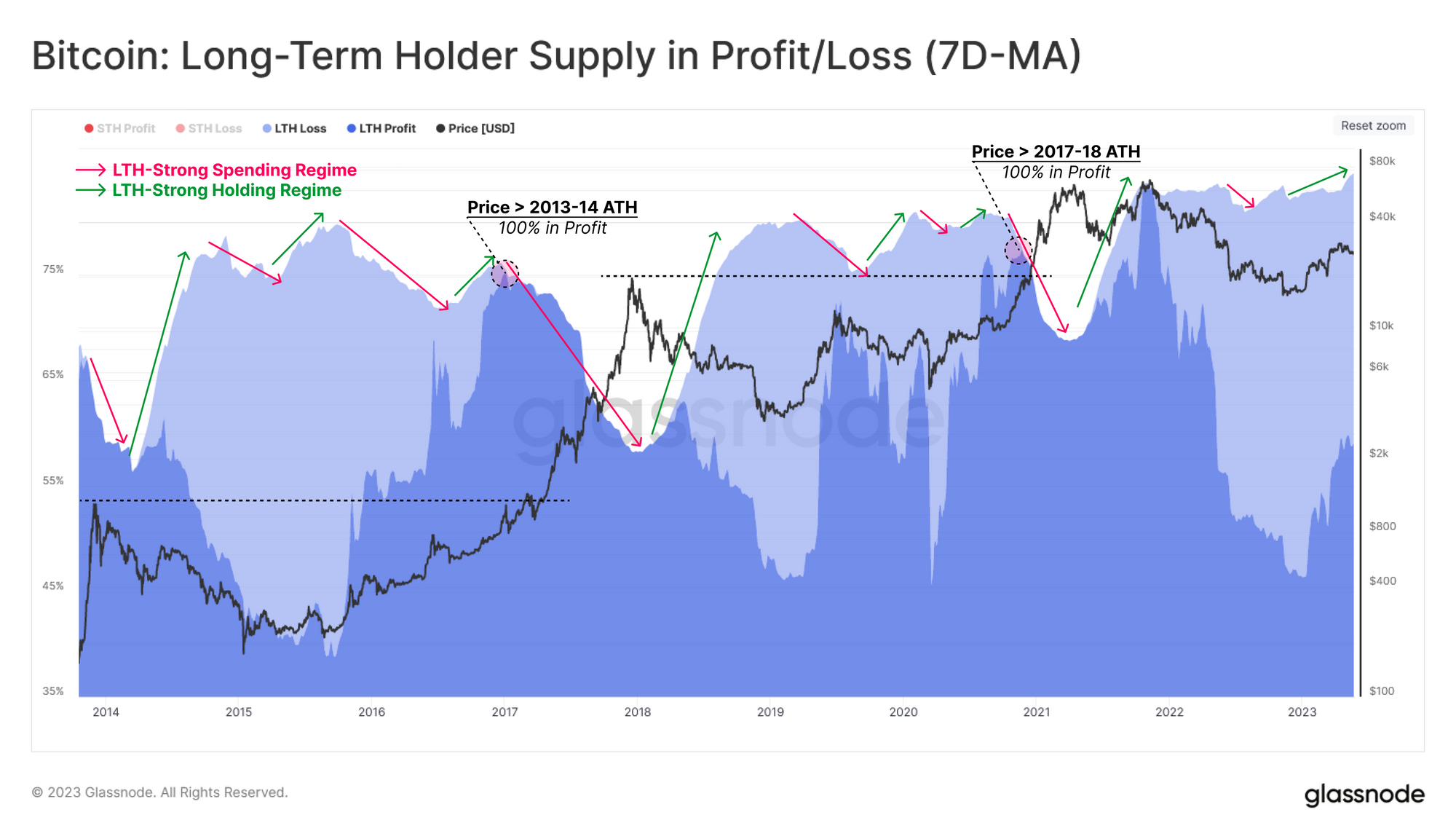

The first tool tracks the Supply side of Long-Term Holders (LTH). We can see that Long-Term Supply tends to be quite cyclical, and we have highlighted various regimes of strong spending 🔴, and strong holding 🟢 patterns on the chart below.

- Before reclaiming the ATH, the Long-term holder supply goes through a lengthy re-accumulation period, with a generally flat, to a modest rise in aggregate supply held.

- As the market breaks the previous cycle ATH, the incentive to ramp up spending increases significantly. This results in a dramatic decline in LTH supply, transferring coins to newer buyers, at expensive prices.

Throughout the 2022 bear market, the first phase LTH supply pattern has played out exactly, showing the remarkable resilience of BTC holders amidst extreme volatility.

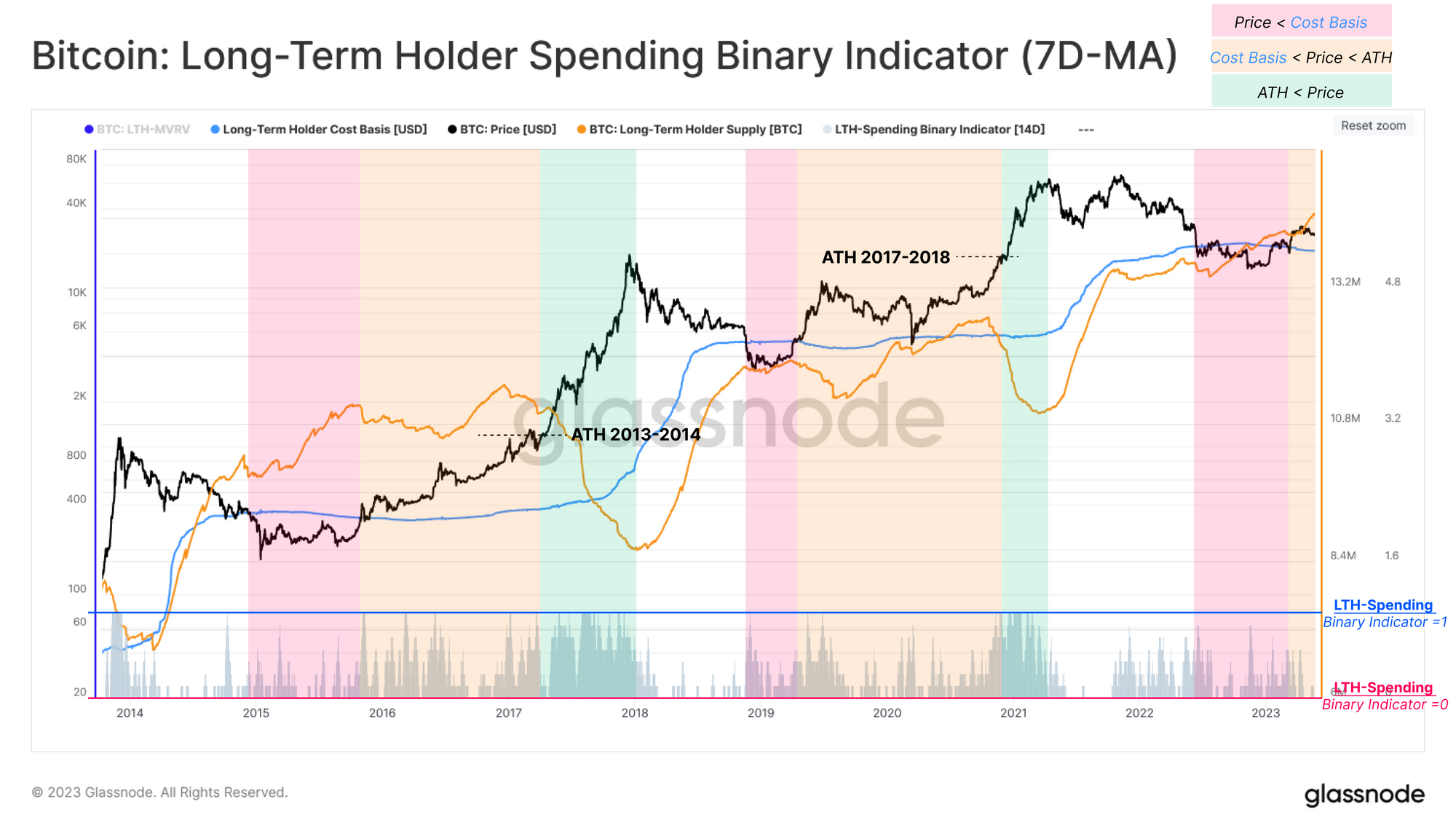

We can use these observations to build a tool that gauges market sentiment. First, we will break the long and rocky road between bear market lows, and the last cycle ATH into three sub-intervals:

- Bottom Discovery 🟥: Price below Long-Term Holders Cost Basis.

- Equilibrium 🟧: Price is above Long-Term Holders Cost Basis. but below the previous ATH.

- Price Discovery 🟩: Price is above the last cycle ATH.

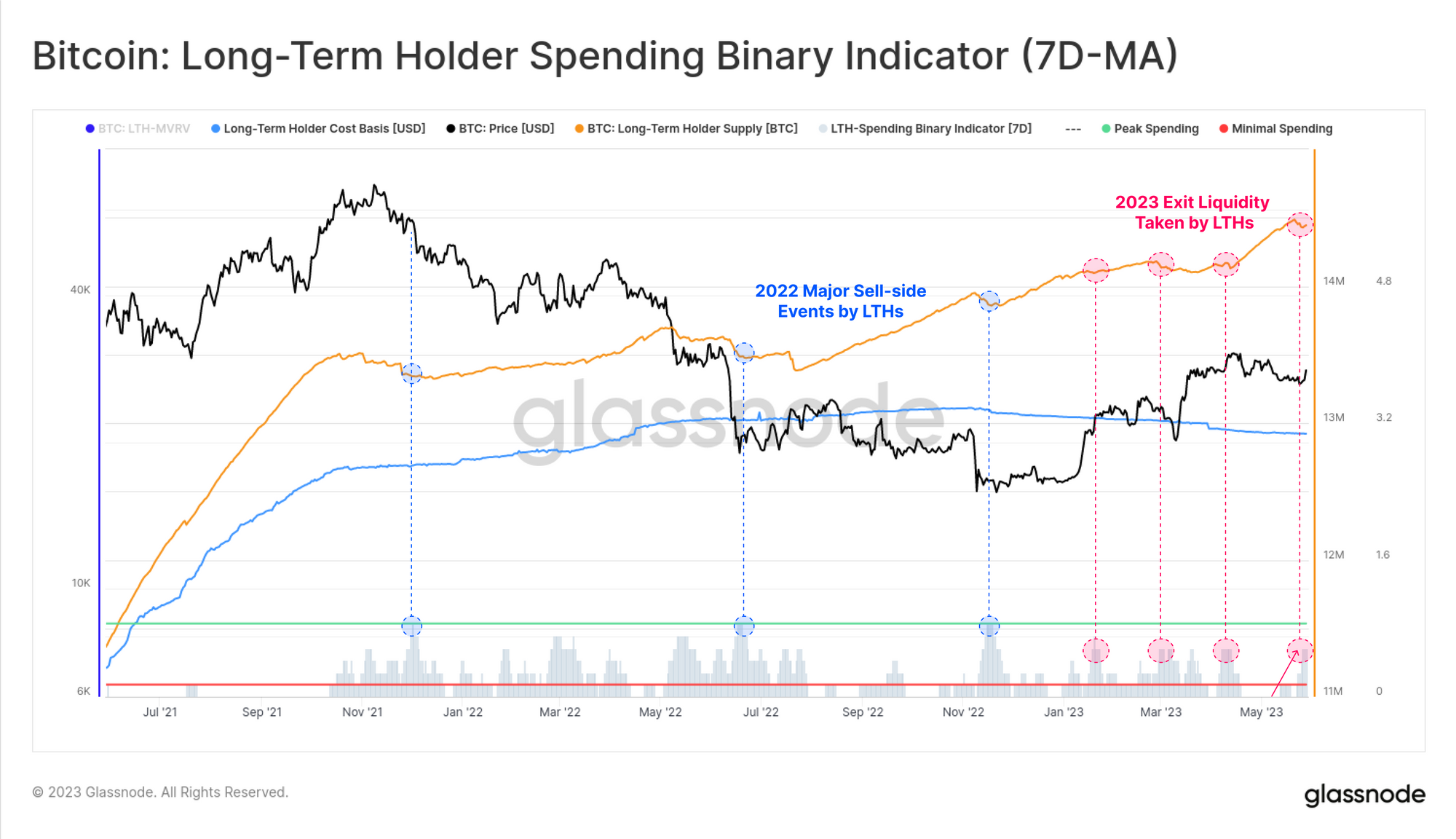

Next, we overlay market performance with the intensity of LTH spending (usually associated with either profit-taking, or capitulation). Here, we display LTH spending via the Spending Binary Indicator (SBI), which simply tracks whether LTH spending is of an intensity sufficient to decrease the total LTH Supply, averaged over the last 7-days.

From this, we can see that LTH spending was been extremely light over recent weeks, but has ticked higher during this correction. The Indicator reached a level suggesting 4-of-7 days experienced a net divestment by LTHs, which is a level similar to exit liquidity events seen YTD.

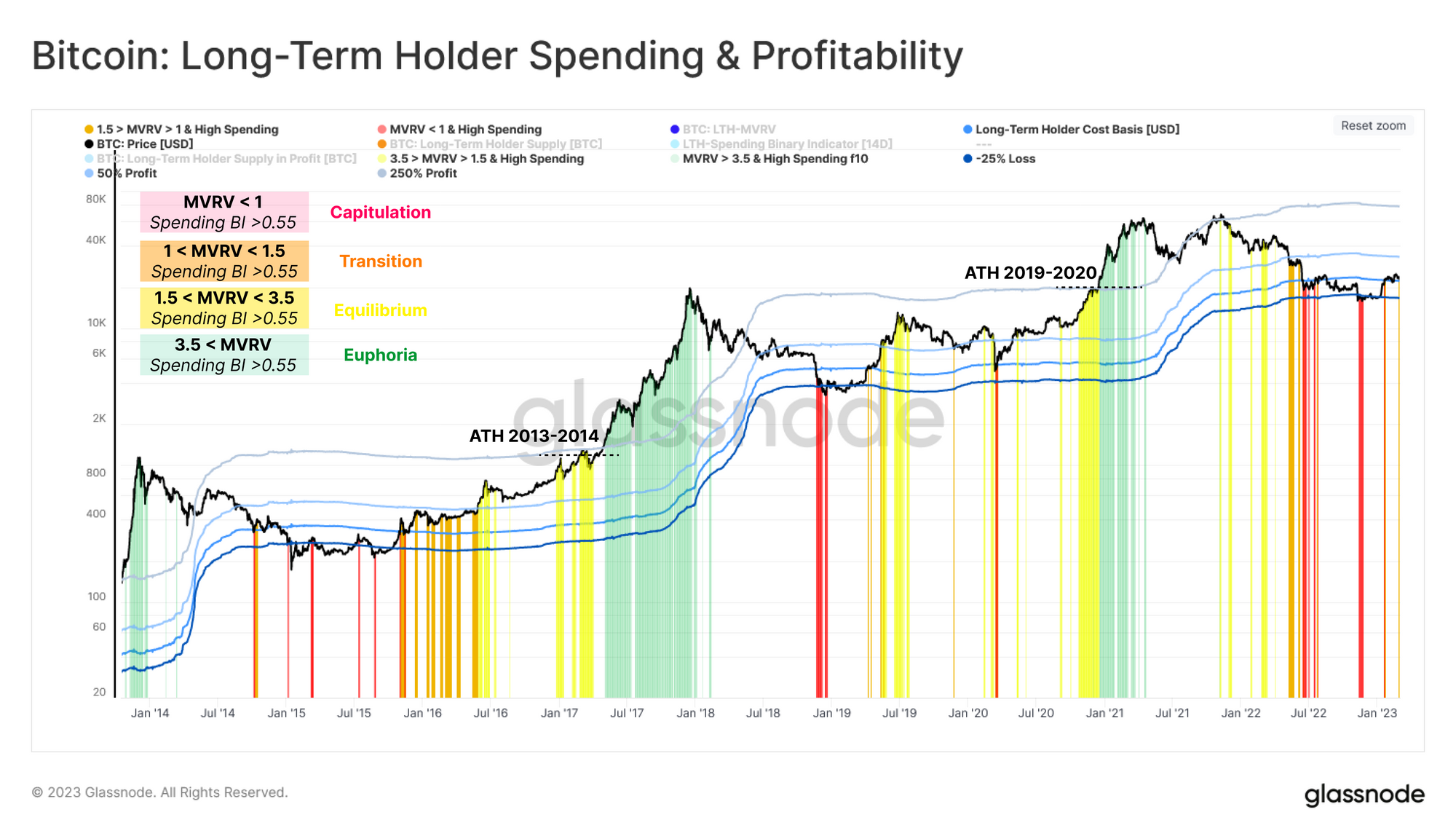

To wrap up, we can merge these two indicators to construct a new tool for breaking up market sentiment into four sub-categories, and spotting periods of elevated LTH divestment:

- Capitulation 🟥: Spot price is lower than the LTH cost basis and therefore any strong spending is likely due to financial pressure and capitulation (Conditions: LTH-MVRV < 1 and SBI > 0.55).

- Transition 🟧: Market is trading slightly above the long-term holders cost basis, and occasional light spending is part of day-to-day trade (Conditions: 1.0 < LTH-MVRV < 1.5 and SBI > 0.55).

- Equilibrium 🟨: After recovering from a prolonged bear, the market seeks a new balance between minimal in-flowing demand, lighter liquidity, and underwater holders from the previous cycle. Strong LTH spending during this stage is usually associated with sudden rallies or corrections (Conditions: 1.5 < LTH-MVRV < 3.5 and SBI > 0.55).

- Euphoria 🟩: As LTH-MVRV reaches 3.5 (historically aligned with the market hitting the prior ATH), LTHs are holding upwards of 250% profit on average. The market enters a euphoria phase, which motivates these investors to spend at very high, and accelerating rates (Conditions: LTH-MVRV > 3.5 and SBI = 1.00).

Our current market has recently reached the Transition phase, flagging a local uptick in LTH spending this week. Depending on what direction volatility erupts next, we can employ this tool to locate local periods of overheated conditions, as observed from the lens of Long-Term Holders.

Summary and Conclusions

The digital asset market continues to outperform major commodities in 2023, however all are currently experiencing a meaningful correction. Having recovered from the depths of the 2022 bear market, Bitcoin investors find themselves in a form of equilibrium, with little gravity in either direction.

Given the extremely low volatility, and narrow trading ranges of late, it seems this equilibrium is soon to be disturbed. In response, we have seen a modest uptick in Long-Term Holder spending, and developed a suite of price levels, and behavior patterns to monitor as the situation unfolds.

Disclaimer: This report does not provide any investment advice. All data is provided for information and educational purposes only. No investment decision shall be based on the information provided here and you are solely responsible for your own investment decisions.

- Join our Telegram channel

- Follow us and reach out on Twitter

- Visit Glassnode Forum for long-form discussions and analysis.

- For on-chain metrics, dashboards, and alerts, visit Glassnode Studio

- For automated alerts on core on-chain metrics and activity on exchanges, visit our Glassnode Alerts Twitter