Bitcoin Breaks To New ATHs

In the wake of the highly anticipated US Presidential Election, Bitcoin has broken to a new ATH of $75.4k. Under the surface, volatility continues to brew across option markets while on-chain capital inflows continue to expand, suggesting a persistent inflow of new demand.

Executive Summary

- Bitcoin has broken to a new ATH of $75.4k, sparked by the high likelihood of President Trump winning the US election.

- Capital inflows into the Bitcoin asset continue to grow, suggesting a persistent inflow of new demand.

- Profit-taking activities have seen a non-trivial increase, while losses realized remain negligible. However, both values are relatively modest compared to volumes seen around market extremes.

- Options markets are pricing in higher volatility expectations as investors hedge their positions in both directions.

New ATHs

Following many months of consolidation and side-ways price action, Bitcoin has broken to a new ATH, sparked by the high likelihood of President Trump winning the US election. Price successfully cleared the $73.7k level and has rallied to over $75.3k, entering a phase of price discovery and pushing investor sentiment closer to Euphoria.

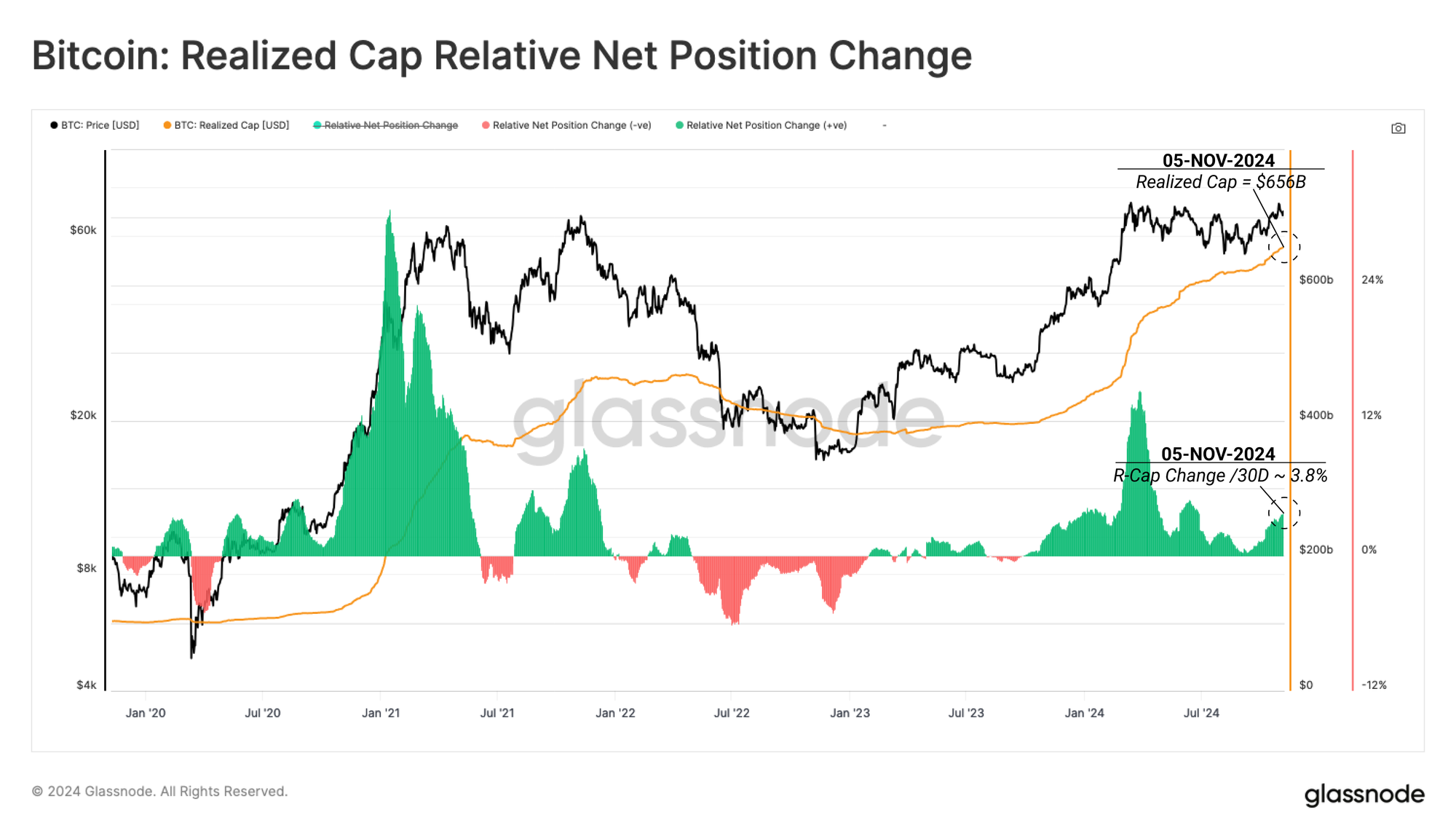

Growing Liquidity and Rising Profits

Since the start of September, net capital inflows into Bitcoin have increased significantly. This showcases a rising appetite for investors to allocate capital, as well as traders taking profit into market strength.

The Bitcoin Realized Cap has increased by 3.8% over the last 30 days, which is one of the higher inflow levels since January 2023. The Realized Cap is currently trading at an ATH value of $656B, supported by a net 30-day capital inflow of $2.5B.

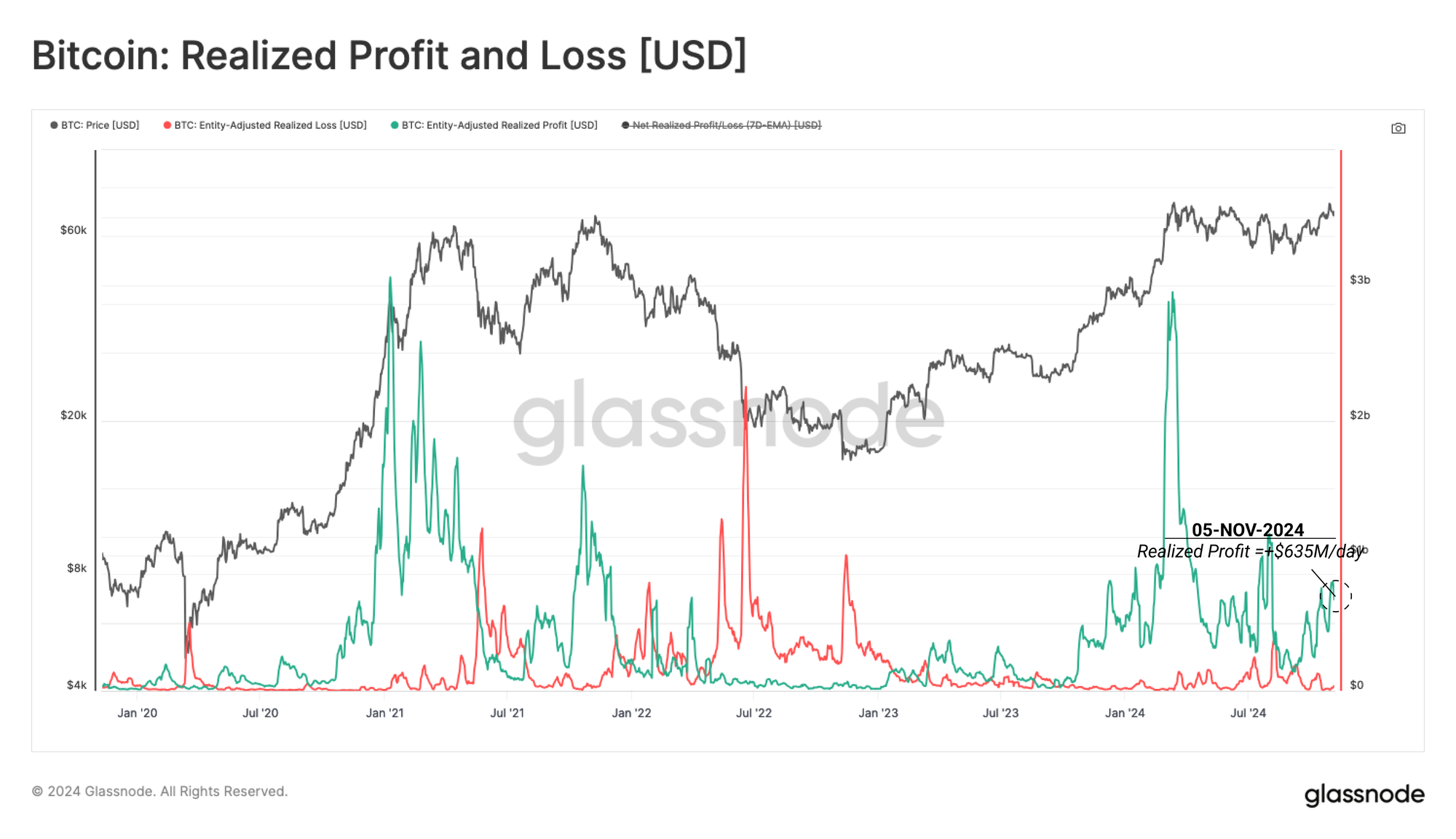

The explosive wave of profit taking into the March ATH culminated with a peak realized profit volume of +$3.1B.

As the market digested this move over the last seven months, realized profit and loss volumes both subsided towards an equilibrium position. This suggests a complete reset of supply and demand forces has occurred.

Alongside this, we can see a structural increase in profit taking, which is starting to re-emerge, suggesting a new wave of demand is entering the market.

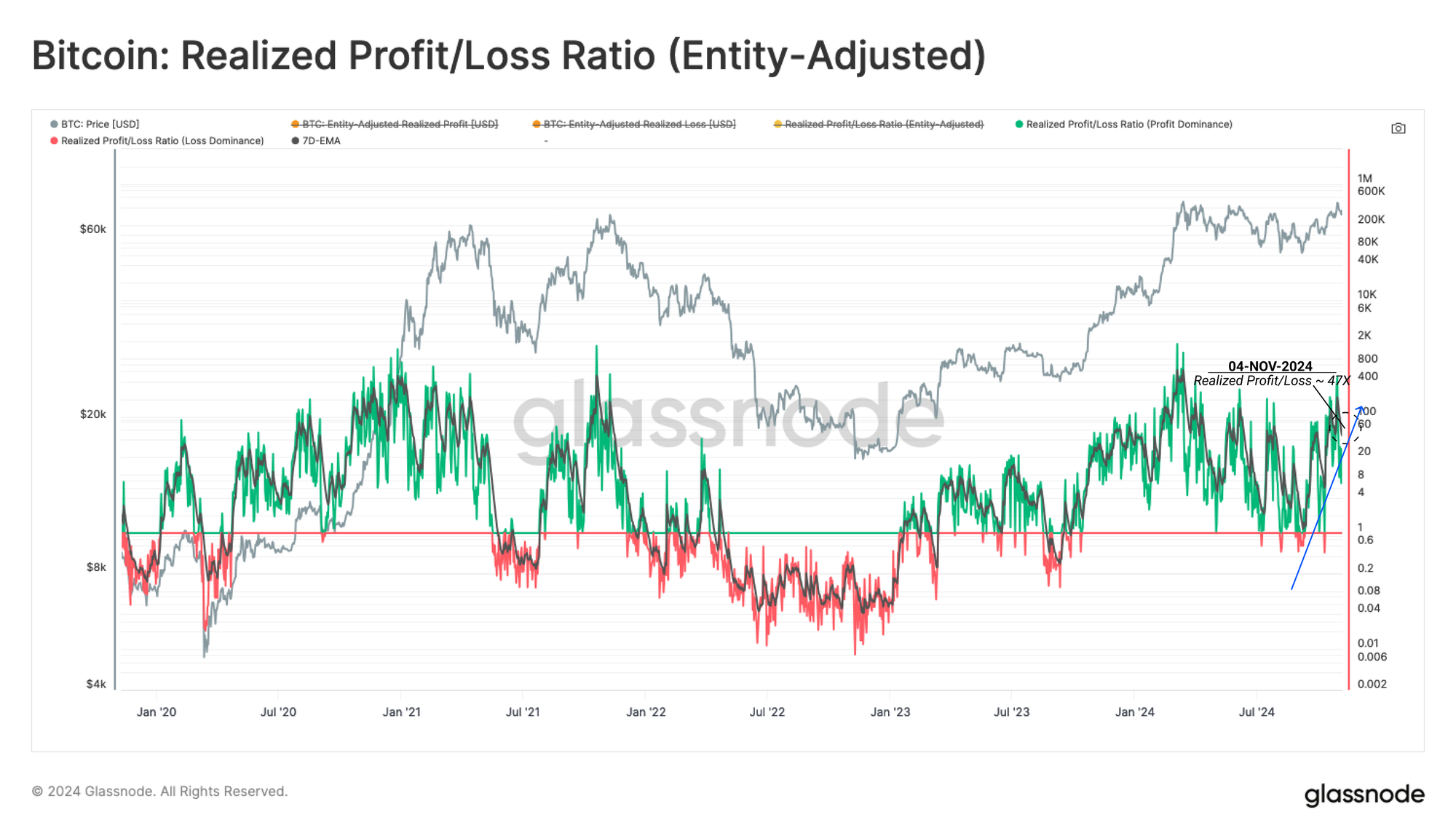

We can also see the shifting market dynamics using the ratio between profit and loss volumes.

The market currently resides in a profit-dominant regime, with the volume of profit realized being a staggering ~47x larger than losses. This reflects the increasingly thin volume of supply held at a loss as the market pushes up to and through to a new ATH.

We can also observe a non-trivial increase in profit-taking volume, which is up by +$635M/day.

While this is a considerable USD value compared to the euphoria experienced near the extremes of previous bull cycles, this remains relatively modest.

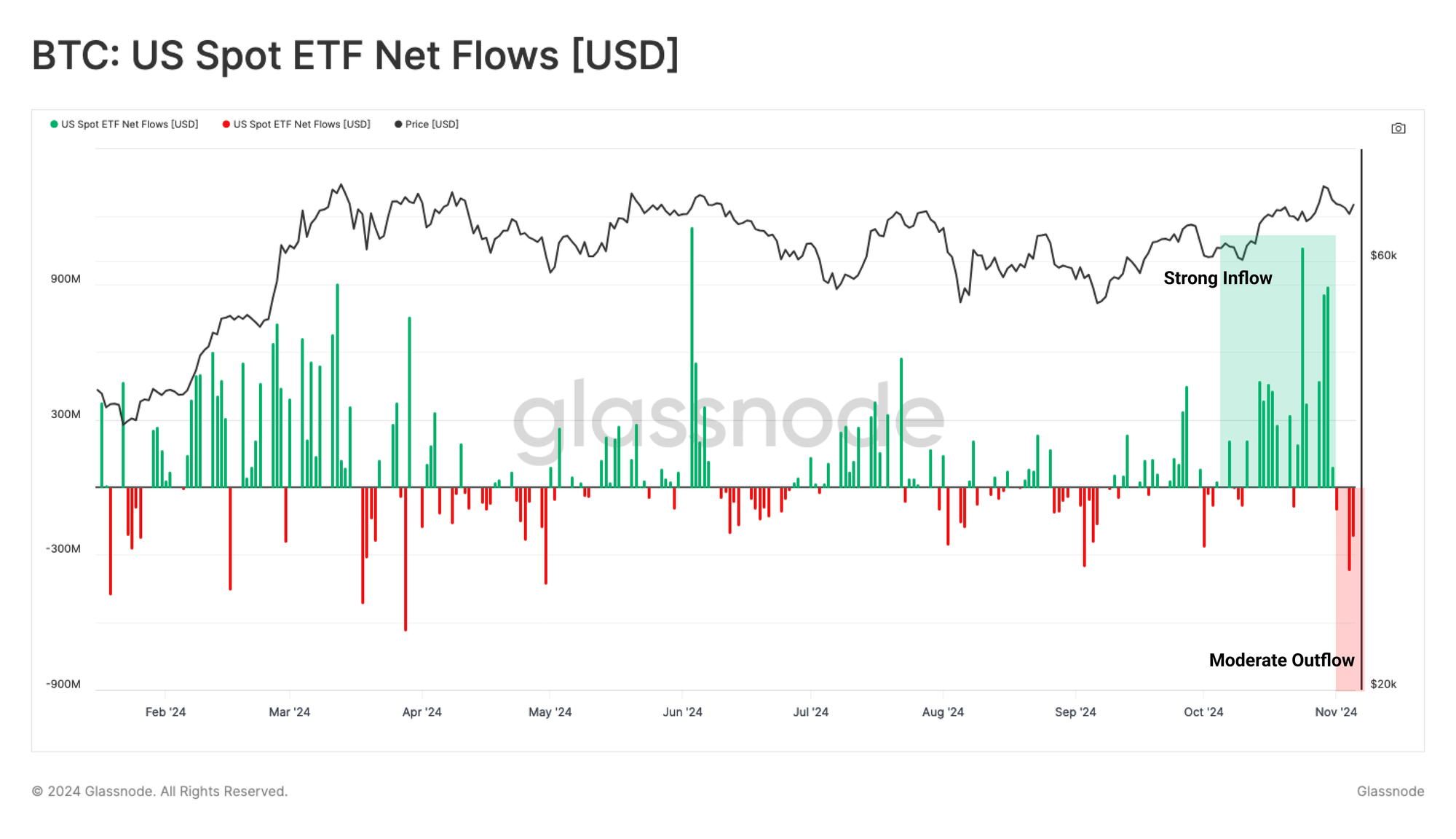

ETFs Experience Outflows

Over the month, US Bitcoin ETFs have experienced remarkable demand, recording a surge of inflows which have rivalled the success observed across the product's initial launch.

However, investors appear to have de-risked in the run-up to the US Presidential Election, highlighted by the notable outflows across the last 3 days. Nevertheless, with the formation of a new ATH, ETFs may see new demand and momentum chasers.

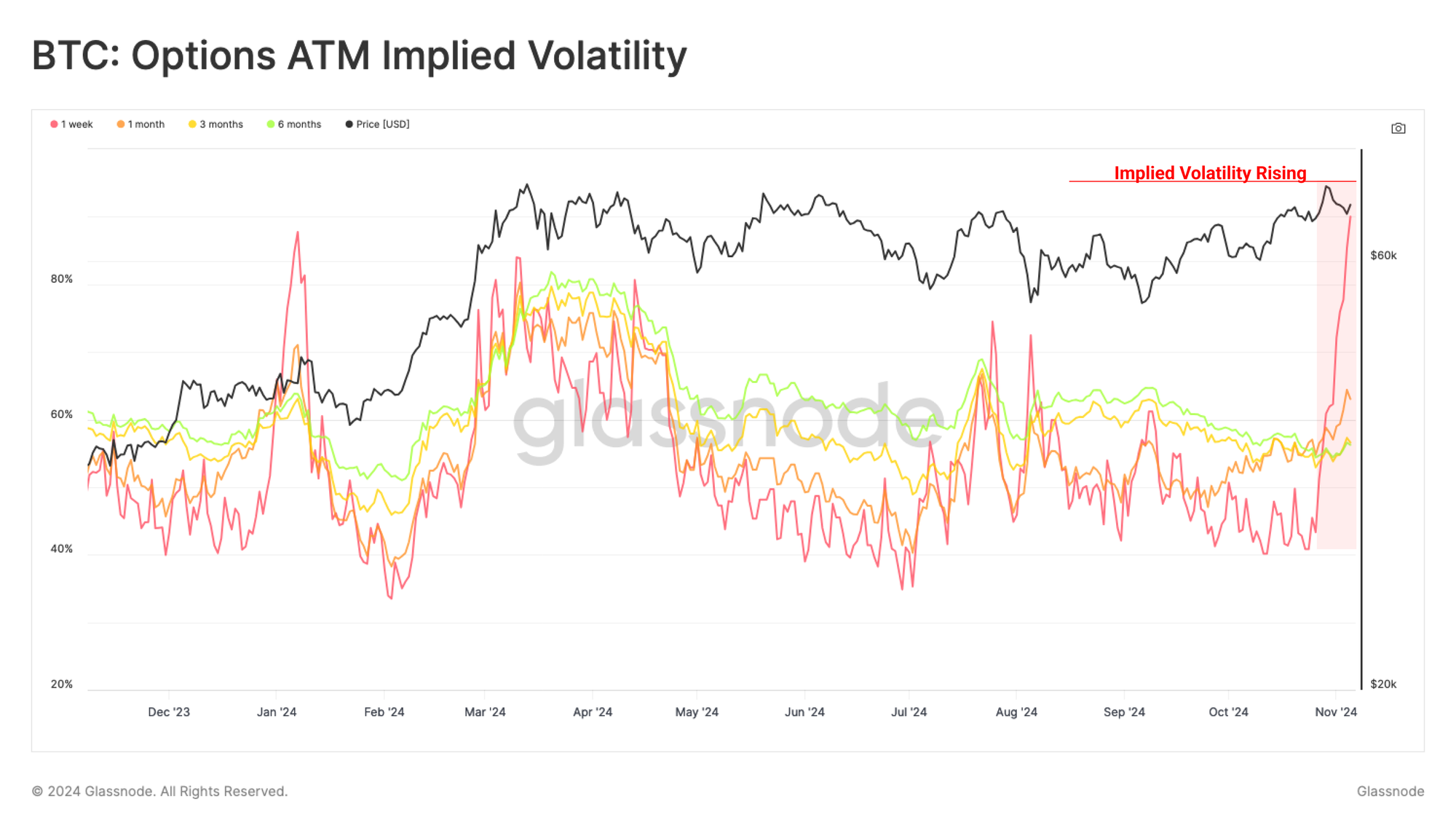

Heightened Volatility Expectations

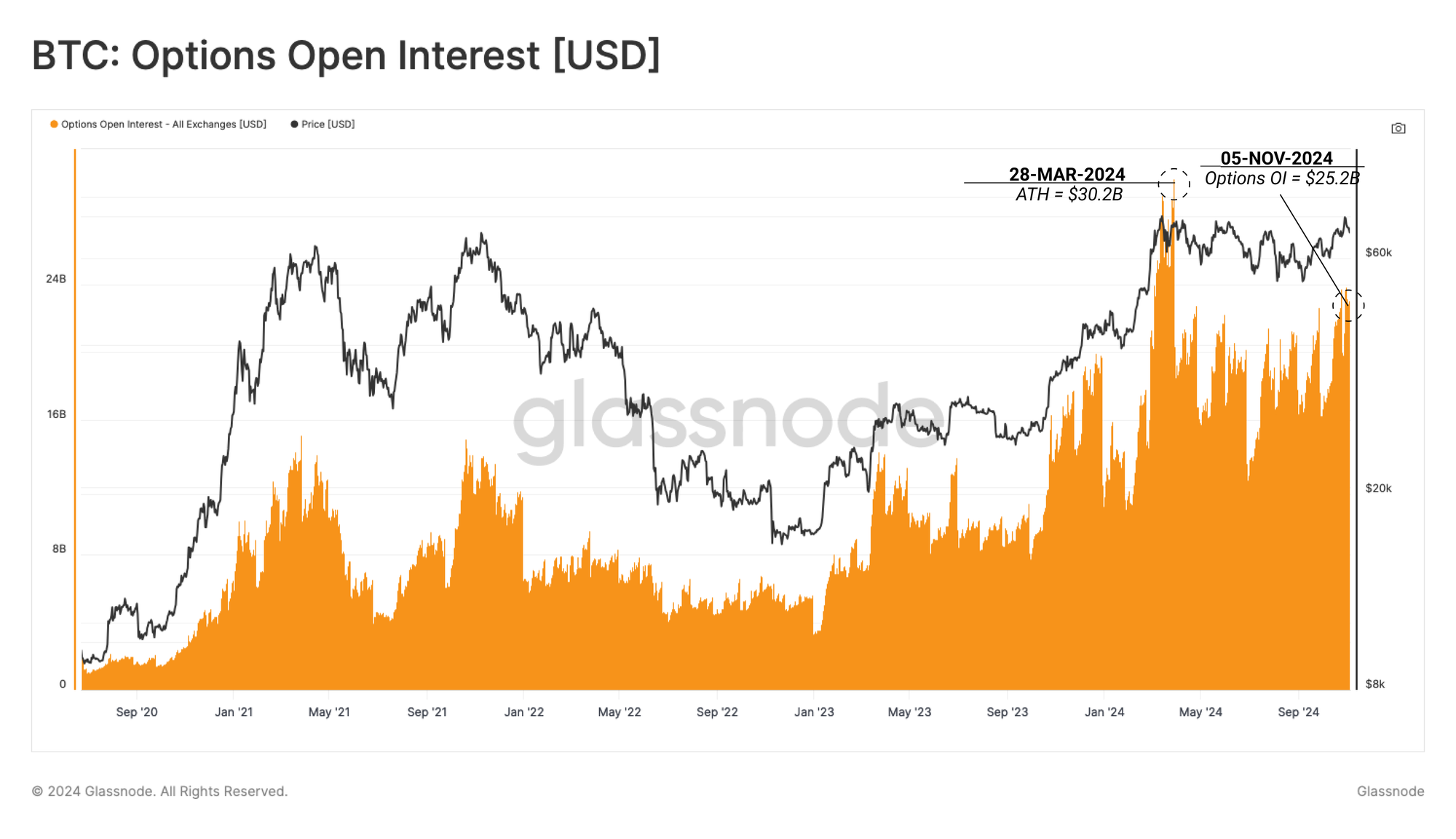

The US Presidential Election has been a dominant focal point for investors, with expectations for heightened volatility being priced in for several weeks. Since 2023, options markets have grown to become a significant component of the Bitcoin market structure, enabling investors to express increasingly sophisticated views on the market.

The amount of open interest deployed across options contracts has surged to a value of $25.2B, with only the March ATH recording a higher value of $30.2B.

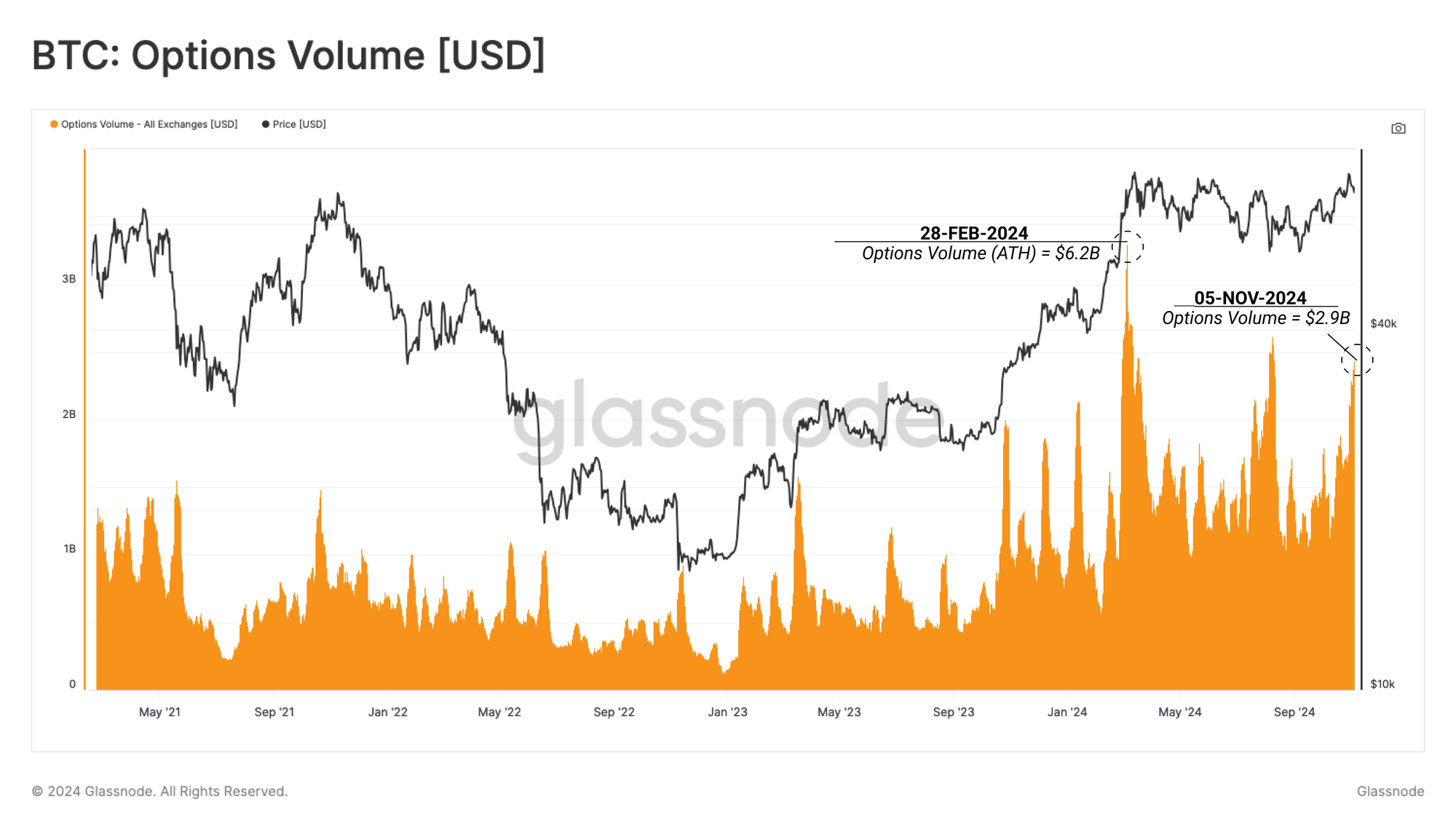

Options trade volume is also ticking higher, now reaching a value of $2.9B, also bested only by the volume trading into the March ATH, and during the 5-Aug yen-carry unwind. This again highlights the growing presence of institutional-grade investors, utilizing sophisticated instruments to express their market opinion.

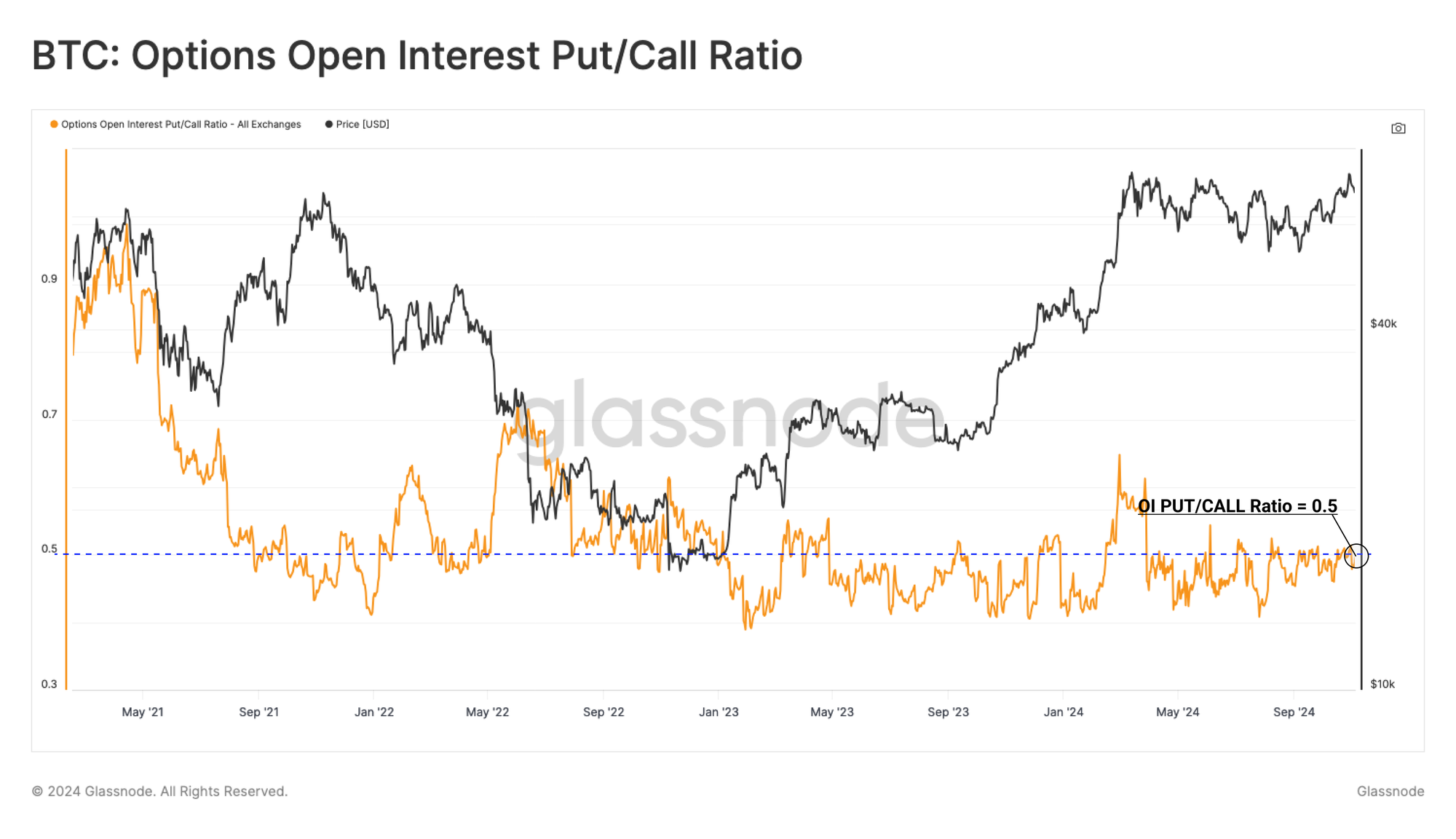

Assessing the ratio between open interest allocated to put and call contracts, there is an even split between both sides. This suggests that investors and speculators have hedged and bet on large market moves in both market directions.

This idea that investors expect rising volatility ahead is also visible in options implied volatility (IV) priced into options.

Currently, we are seeing a surge in IV across all contract expiration dates, most notably across the short-dated 1-week expiration. This confluences that the investors are forecasting and betting on a higher volatility regime both into and after the US election results are known.

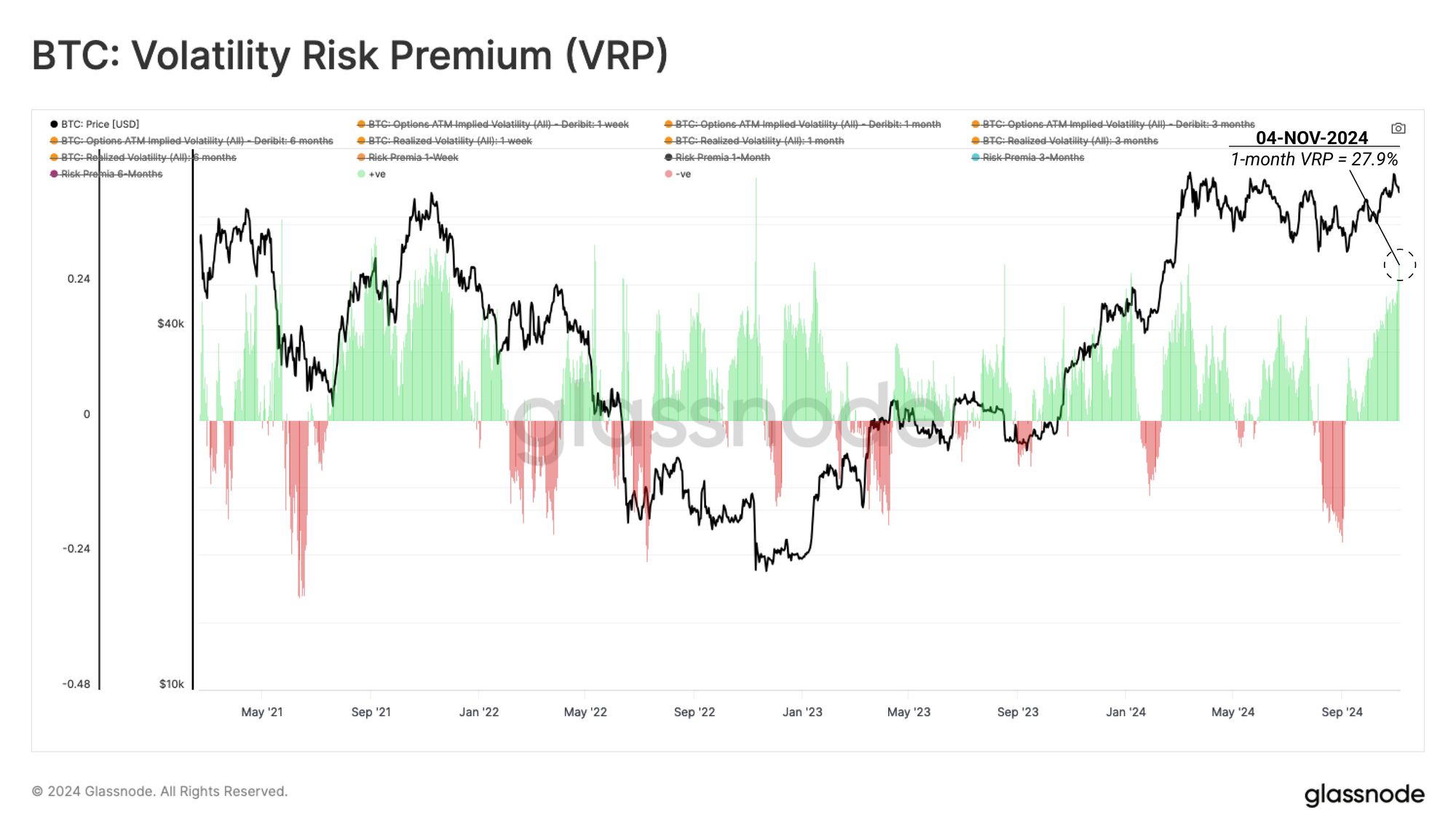

By comparing the difference between the options implied volatility and realized volatility over the same time period, we can calculate the volatility risk premium (VRP). This metric represents the compensation options writers require to take on volatility risk.

Presently, the 1-month VRP resides at a value of 27.9%, with only 1.4% of trading days recording a larger value. This highlights how extreme the volatility profile is that is priced into options markets.

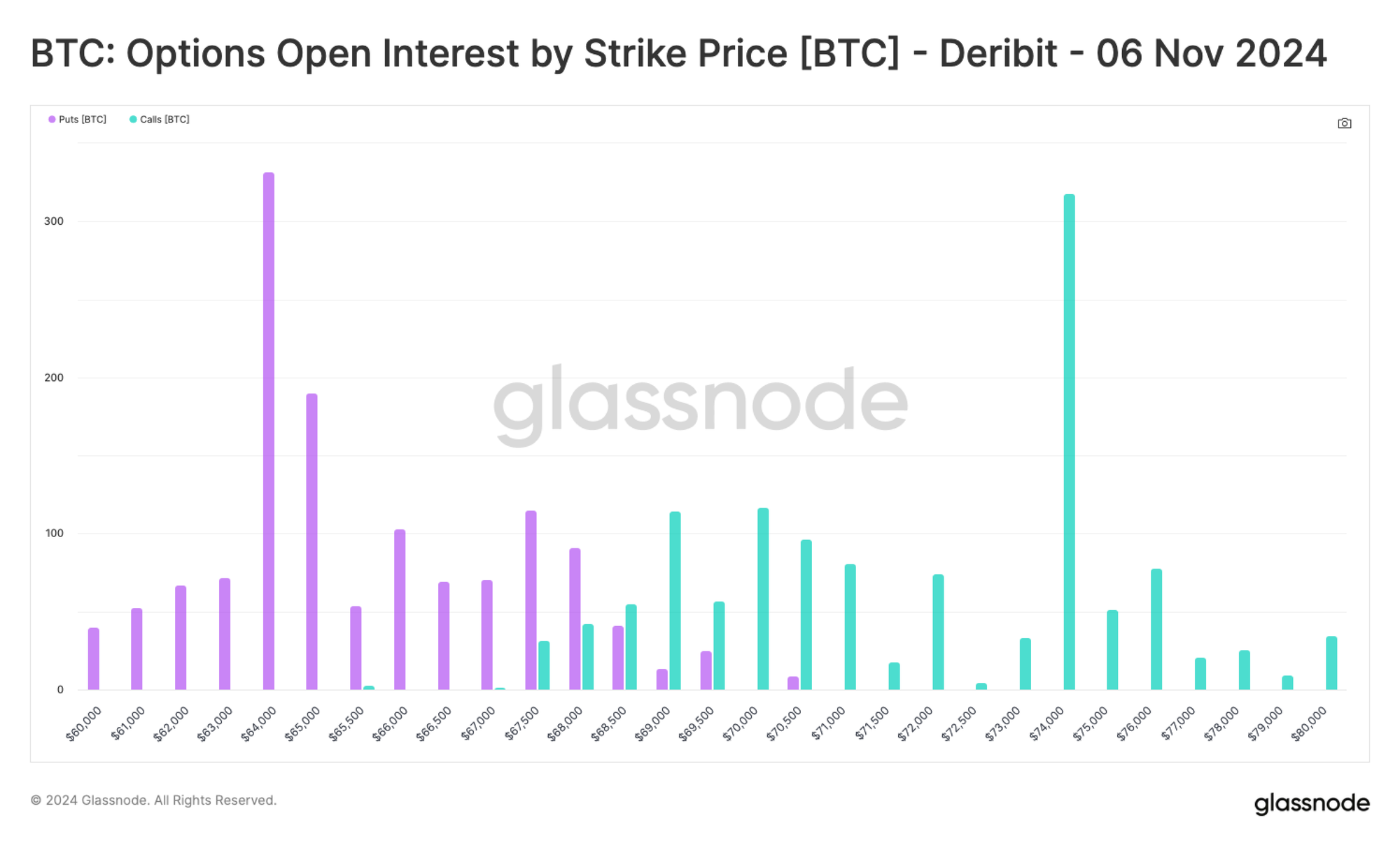

Evaluating the distribution of both puts and calls, which have an expiration on 6-Nov, just after US election day, we can see a near-even split between each side. Put options have a total open interest of 1348 BTC, whilst call options have an open interest of 1271 BTC.

This suggests that investors have hedged for both downside protection and upside exposure, highlighting the degree of uncertainty on the ultimate market direction.

Summary and Conclusion

In the aftermath of the US presidential election, Bitcoin reached a new all-time high, trading above $75,000 for the first time this week. This move is supported by modest capital inflows of $2.5B/month, indicating the potential for further growth amidst a consistent influx of new demand.

With an increasing demand side, alongside expanding volatility expectations across option instruments, the market appears poised for further fluctuations.

Disclaimer: This report does not provide any investment advice. All data is provided for information and educational purposes only. No investment decision shall be based on the information provided here and you are solely responsible for your own investment decisions.

Exchange balances presented are derived from Glassnode’s comprehensive database of address labels, which are amassed through both officially published exchange information and proprietary clustering algorithms. While we strive to ensure the utmost accuracy in representing exchange balances, it is important to note that these figures might not always encapsulate the entirety of an exchange’s reserves, particularly when exchanges refrain from disclosing their official addresses. We urge users to exercise caution and discretion when utilizing these metrics. Glassnode shall not be held responsible for any discrepancies or potential inaccuracies. Please read our Transparency Notice when using exchange data.

- Join our Telegram channel.

- For on-chain metrics, dashboards, and alerts, visit Glassnode Studio