Resilience and Synchronicity

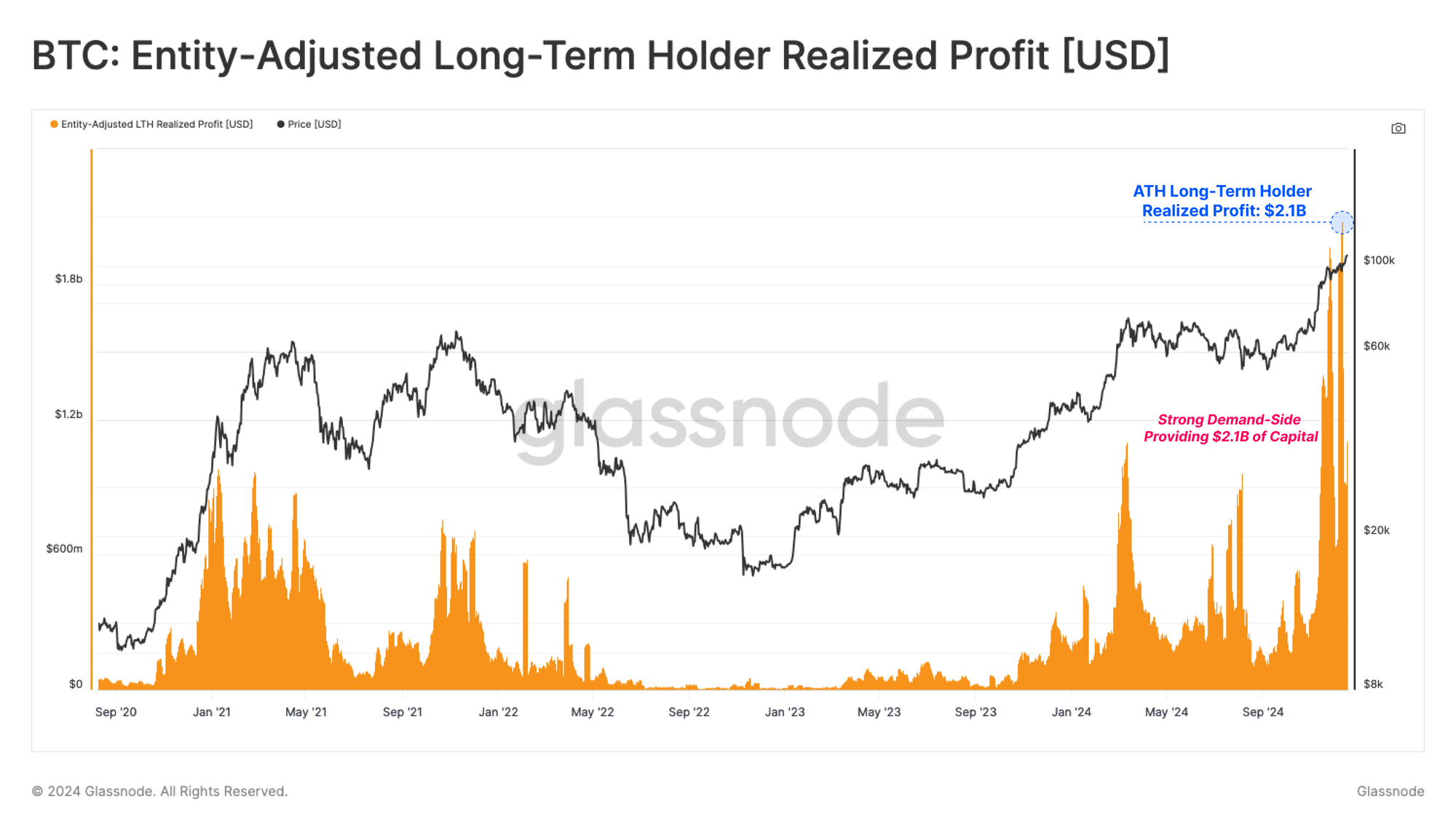

Bitcoin continues trading above the psychologically important $100k price level, supported by a consistent inflow of capital. Long-Term Holders are capitalizing on this liquidity, taking the opportunity to distribute supply at scale, setting a new ATH in profit realized of $2.1B.

Executive Summary:

- A striking degree of similarity in the Bitcoin price trajectory can be observed across prior cycles despite vastly differing market scales, investor composition, and market structure dynamics.

- With price trading above $100k for a few weeks now, Long-Term Holders are taking the opportunity to distribute supply into fresh demand. This has resulted in a new ATH in realized profit being set, breaching $2.1B.

- A notable portion of these profit taking volumes are originating from coins aged 6m-12m, with coins older than this remaining relatively dormant in comparison.

- The percentage of network wealth held by new investors has surged higher, highlighting a robust demand profile, but also reflects a transition in the balance of wealth away from longer-term HODLers.

Old But New

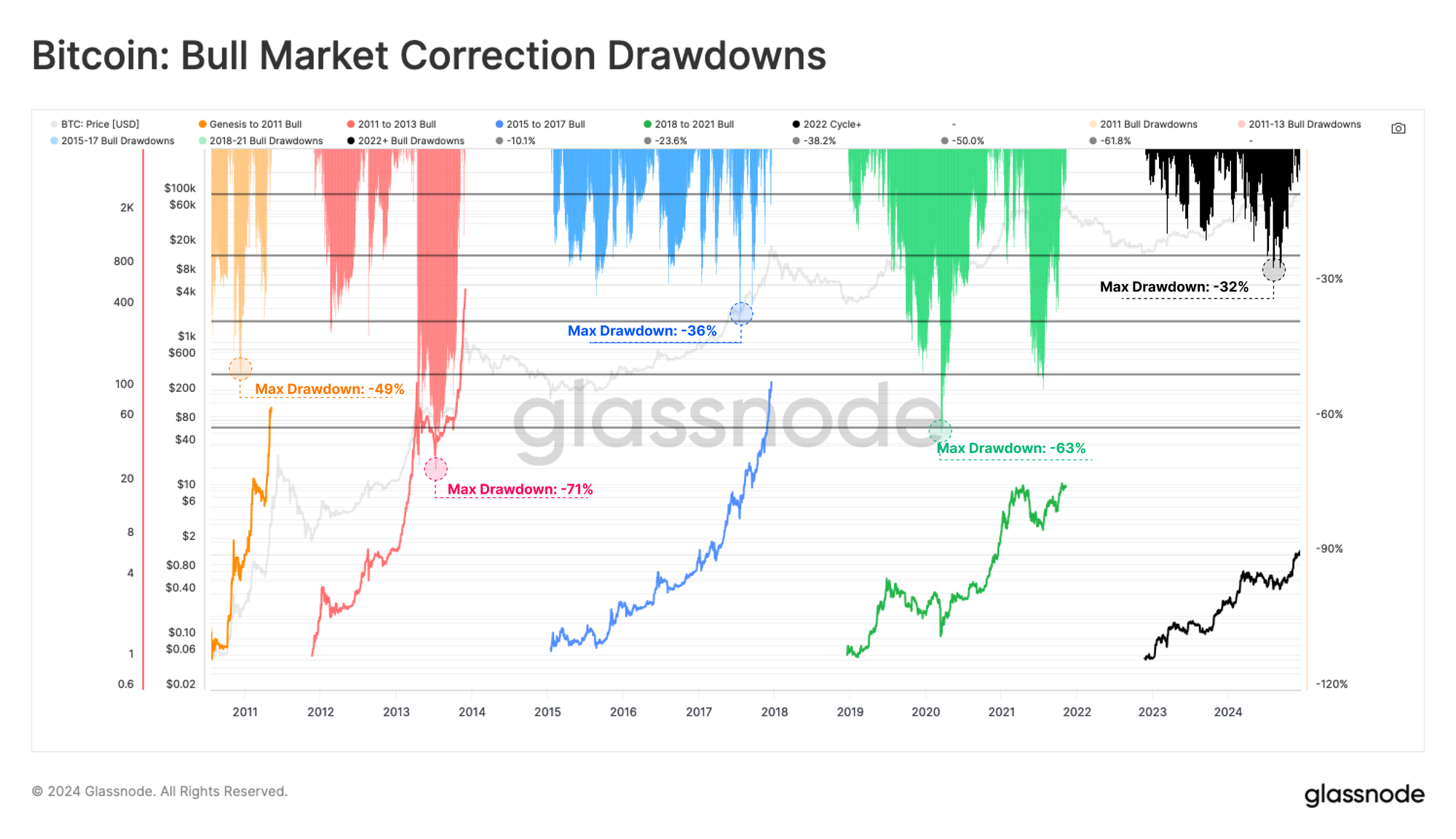

2024 has been another exceptional year for Bitcoin, with year to date returns of more than 150%, and the BTC price trading above $100k for a few weeks. When we compare price performance across cycles, we can see that the prevailing cycle is starkly similar to both the 2015-18, and 2018-21 cycles.

- 2015-2018: +501%

- 2018-2022: +1085%

- 2022+ Cycle: +638%

This parallel becomes even more impressive when we account for the order of magnitude larger the Market Cap is between these cycles, requiring increasingly larger capital flows to support the same degree of growth.

Interestingly, the severity of market drawdowns during each bull market uptrend has declined as the market grows, despite the extreme sell-side pressure which typically accompanies aggressive upward price movements.

The deepest drawdown in this cycle has been -32%, set on 5 August 2024. The majority of drawdowns have only seen the price fall -25% below the local high, masking this is one of the least volatile cycles to date. This may be a reflection of the significant demand opened up by the spot ETFs, as well as a growing interest from institutional investors.

Dissecting Losses

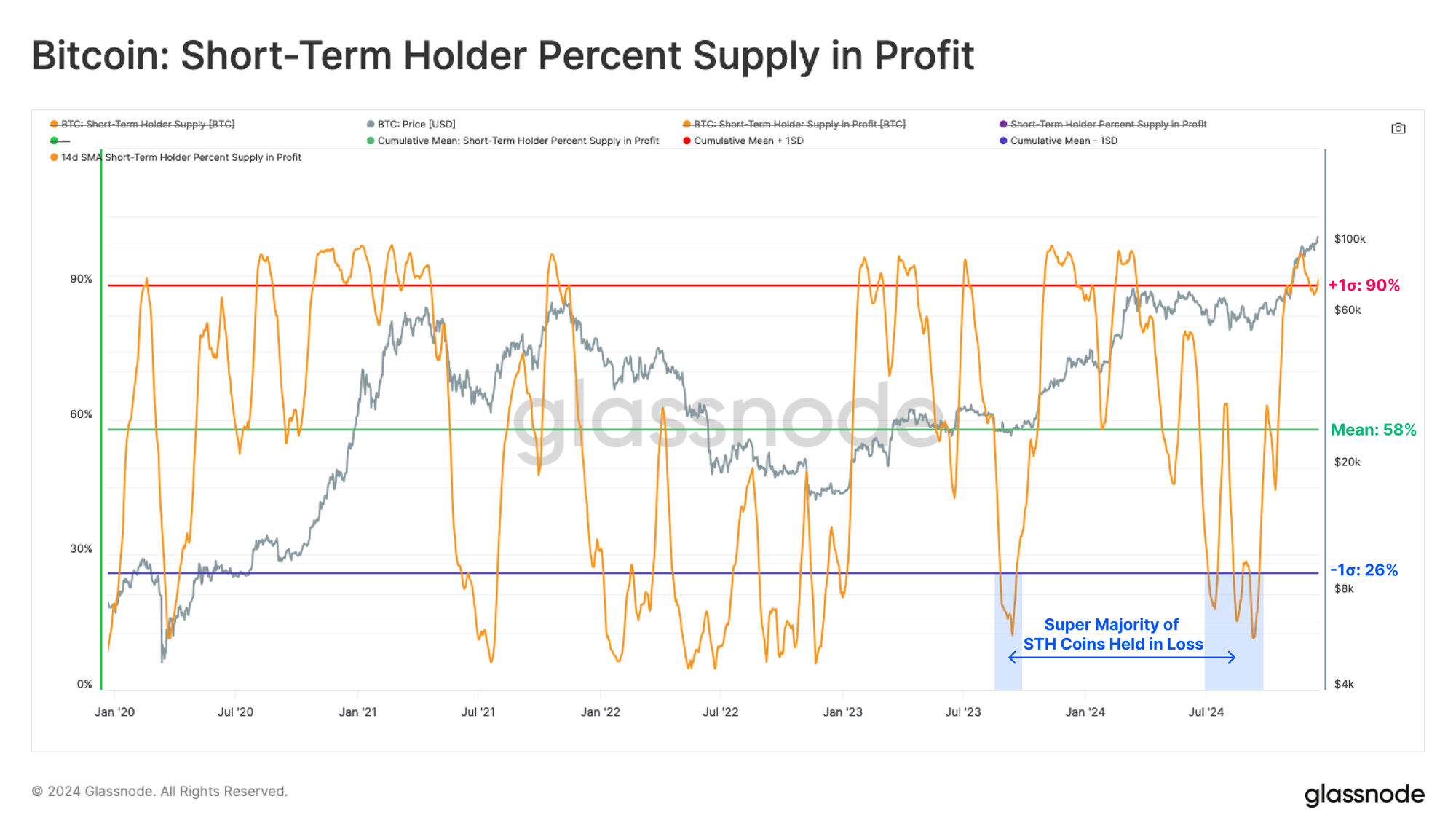

In the drawdown profile above, the declines in August 2023 and September 2024 are the two deepest drawdowns in the current up-cycle. Both of these periods can be characterized as a point of extreme market pressure, which carried significant potential to devolve into a regime of fear and accelerating losses.

We can visualize this using metrics associated with the Short-Term Holder (STH) cohort, which we often consider as a proxy for new market demand. As previously explored in our study on Seller Exhaustion, the STH cohort is the primary source of realized loss during uptrends, providing us with information regarding the top-heaviness of markets.

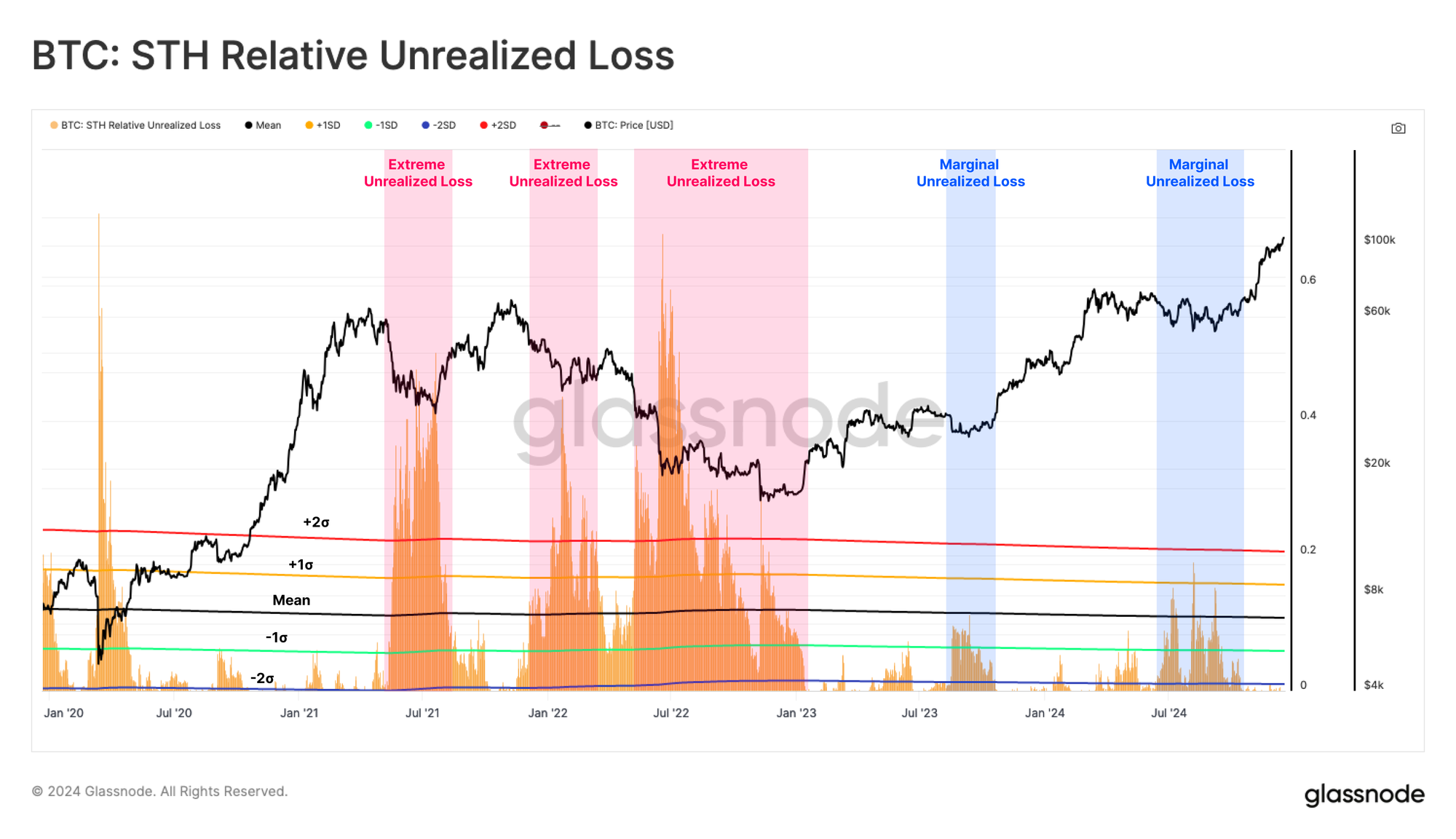

Typically, periods of extreme market distress are characterized by a dominant portion of the coin supply falling into a position of loss (coins underwater). We can see in both of these instances (August-23 and September-24) that a super-majority of STH coins were indeed held at an unrealized loss.

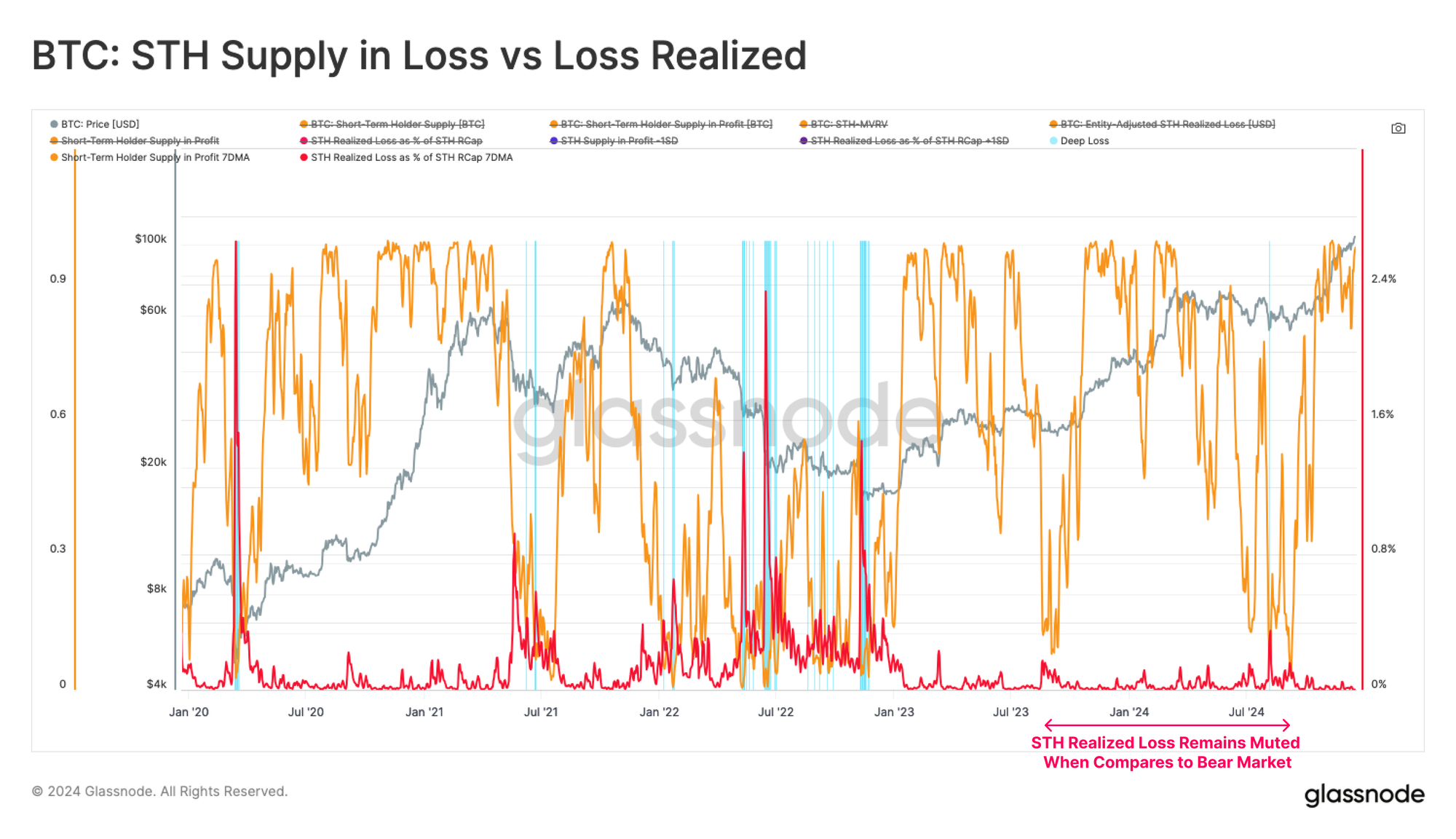

However, when we measure the magnitude of unrealized losses (paper losses rather than the number of coins held in loss), we encounter a different picture. Whilst a super-majority of the STH supply (coin count) was underwater relative to their cost basis, they did not carry the extreme unrealized losses typically associated with deteriorating markets.

A similar story is apparent when we denominate Short-Term Holder losses as a percentage of their total invested wealth (divided by the STH Realized Cap). The previously mentioned periods did not lead to cascading realized losses despite the entirety of the STH supply being underwater on the position.

In the chart below, we highlight (blue) periods of time where both the percentage of Short-Term Supply held in Loss and the magnitude of losses locked have moved more than 1 standard deviation from the mean. The yen-carry-trade unwind on 5 August is the only notable point where this condition was briefly flagged throughout this bull market uptrend.

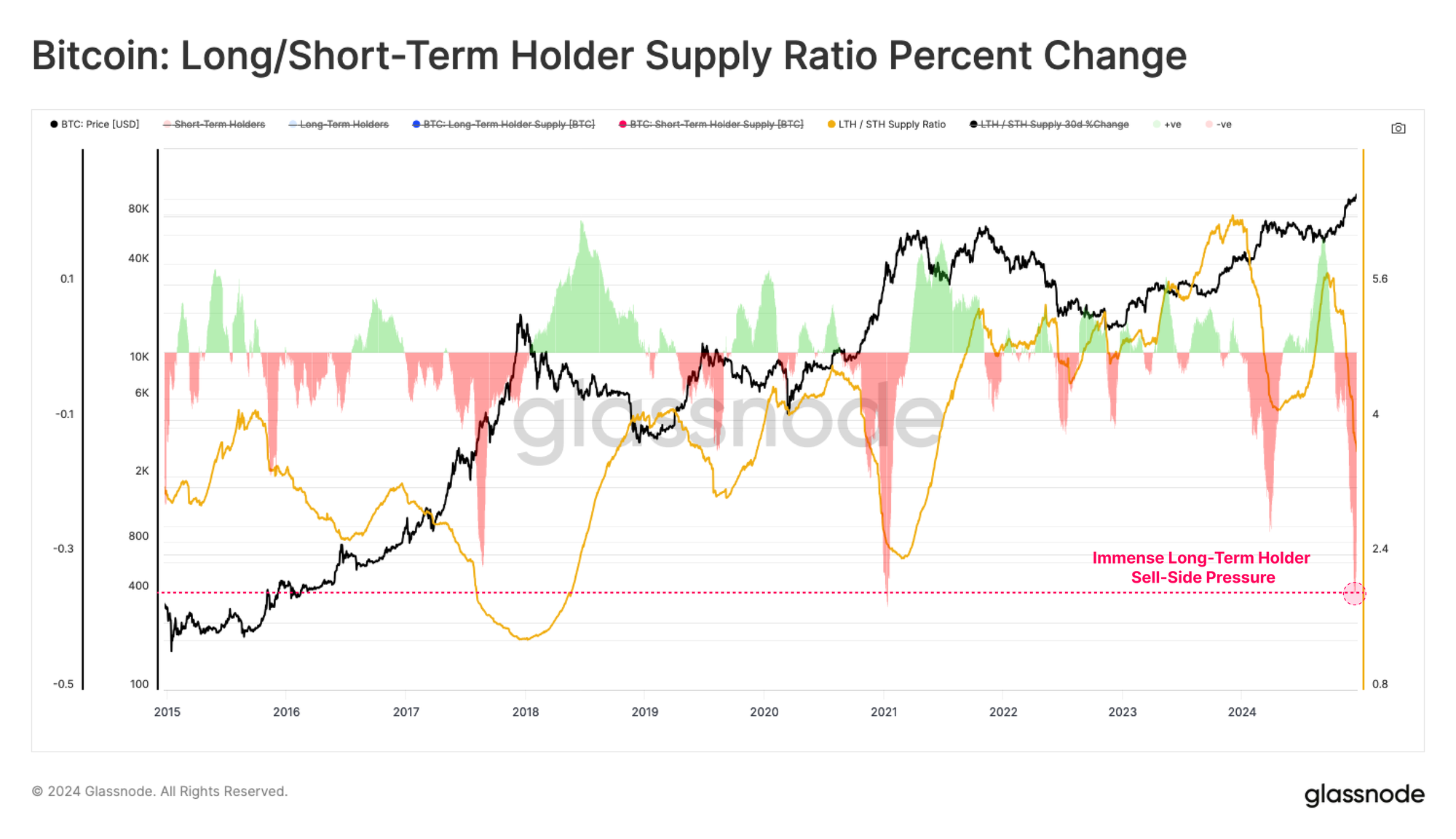

Ramping Up Sell-Side Pressure

In the previous section, we assessed and evaluated the impressive relative strength of the Bitcoin market, even during corrections. Next, we will switch our focus towards the demand profile, which is acting to offset sell-side pressure from existing holders, who are taking profits.

Long-Term Holders have distributed a significant volume of supply into the rally up to and through the $100k price point. Sell-side pressure from LTHs has eclipsed what was experienced in March when the market set the new ATH at the time of $73k.

The magnitude of this sell-side pressure is quite massive, but it is consistent with market dynamics typically experienced in the later phases of a Bitcoin bull cycle.

This has translated into a substantial volume of profits being taken by the LTH cohort, which has recently peaked at a new ATH of $2.1B/day.

If we adopt a simplified assumption that every seller is matched with a buyer, this observation provides some insight into the strength of the demand side, who, by contrast, has provided an estimated $2.1B of fresh capital into the market.

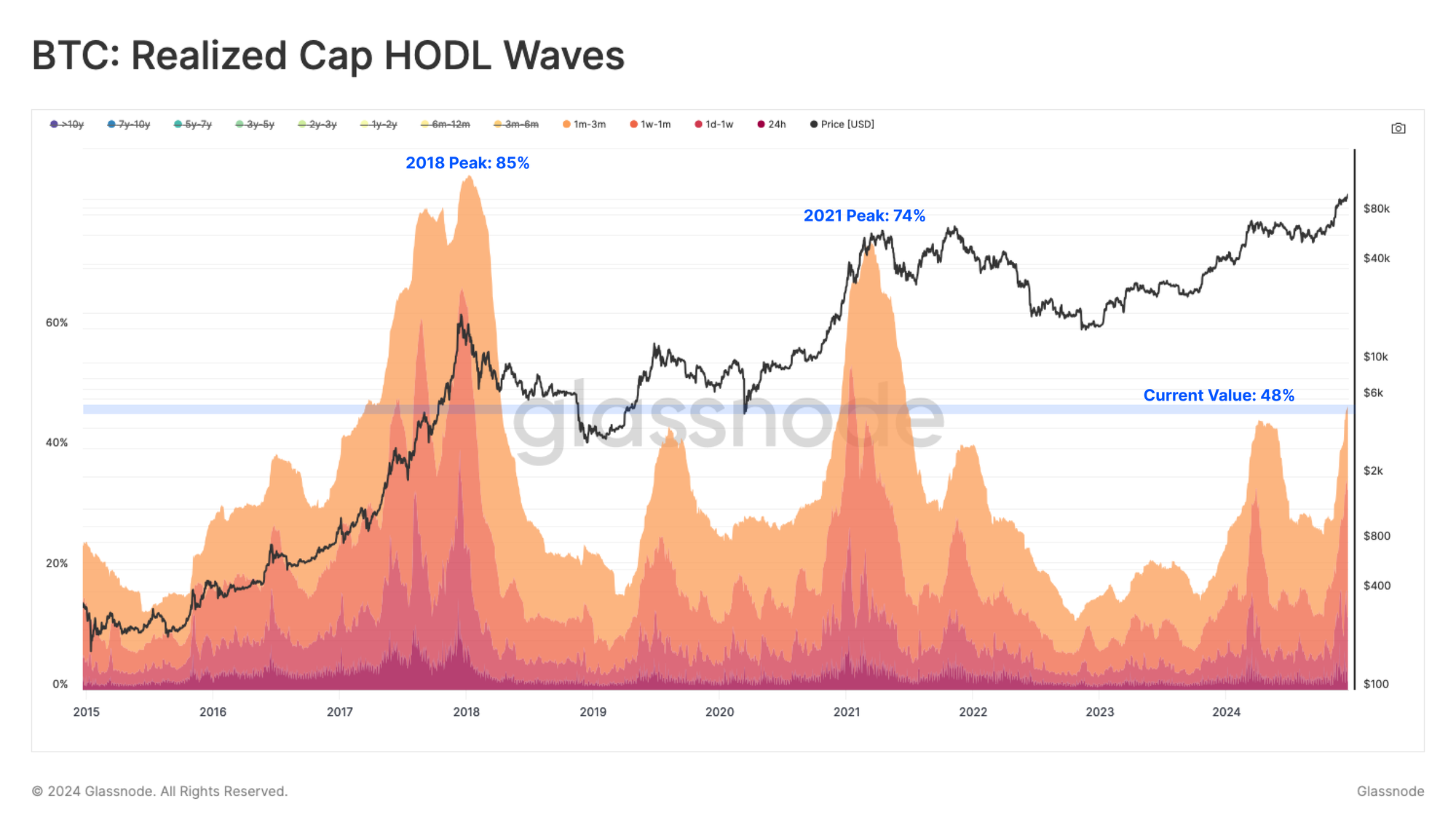

Compounding on the above observation, we can see the proportion of wealth held within recently moved supply has started to increase meaningfully in recent months. This occurs as coins held by Long-Term Holders are distributed to new investors, which in turn highlights a surge in new demand-side activity.

Nevertheless, the proportion of wealth held by these new investors has not yet reached the heights experienced during previous ATH cycle tops. The interpretation here is that the market may not have reached the level of euphoric fervour, and saturation by speculators seen in prior cycles.

Composition of Sell-Side

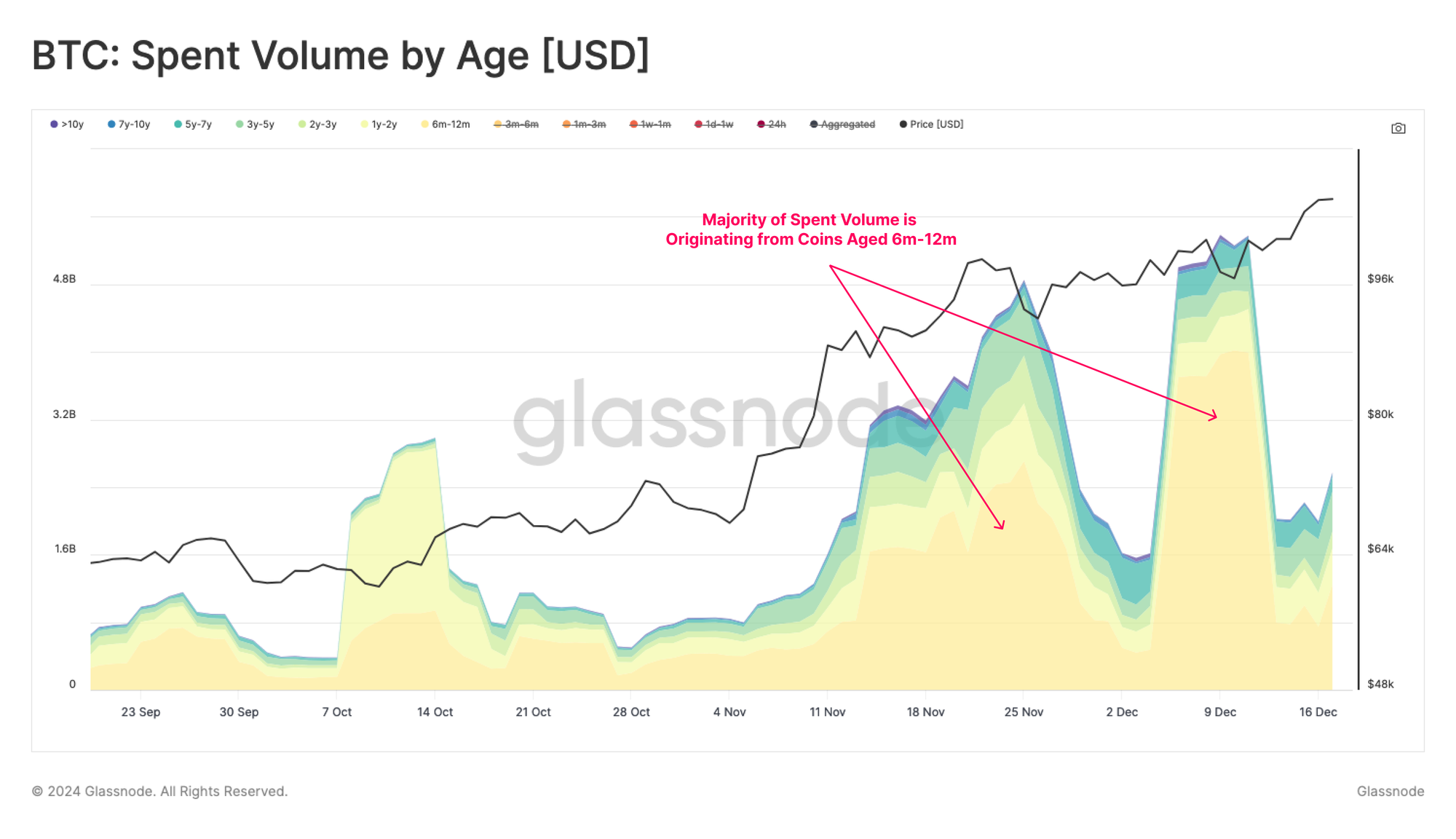

After demonstrating the scale of the sell-side pressure originating from Long-Term Holders, we can increase the granularity of our assessment using age-band sub-sets of this cohort.

By assessing the spent volume of coins aged older than 6 months, it appears as though the majority of sell-side pressure originates from the 6m-12m subset. These coins were more or less acquired in 2024. Notably, coins aged 3 years or more have remained relatively static in comparison, potentially requiring higher prices before the holders decide to release their coins.

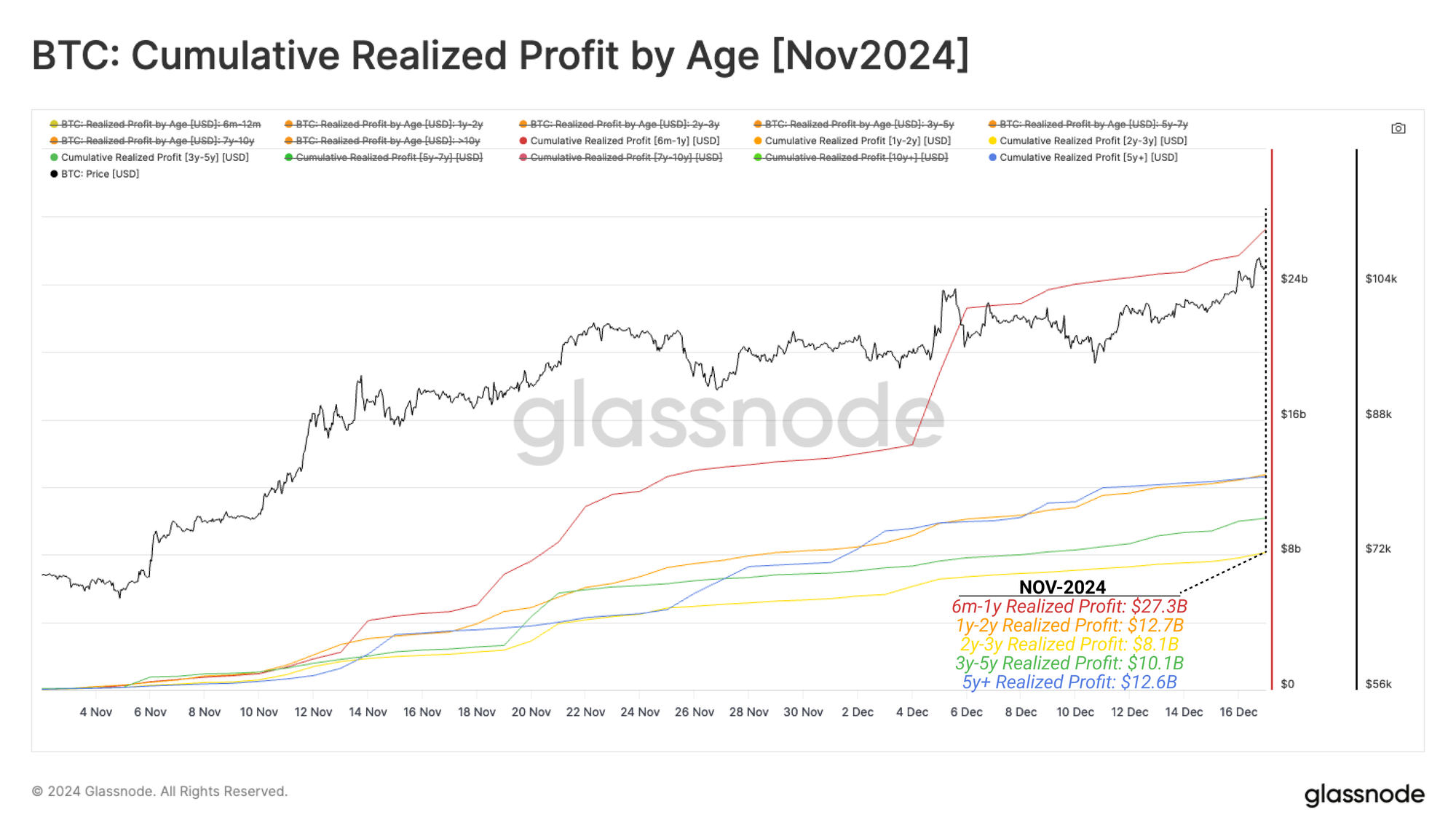

Additionally, we can employ our age breakdowns of the realized profit metric to evaluate which sub-cohorts are contributing the most to sell-side pressure. Here, we calculate the cumulative profit-taking volume by age since the start of the Nov-2024.

- 6m-1y Realized Profit: $27.3B

- 1y-2y Realized Profit: $12.7B

- 2y-3y Realized Profit: $8.1B

- 3y-5y Realized Profit: $10.1B

- 5y+ Realized Profit: $12.6B

Coins aged between 6 and 12 months dominate the prevailing sell-side pressure, accounting for 38.5% of the total, providing confluence to the above observation.

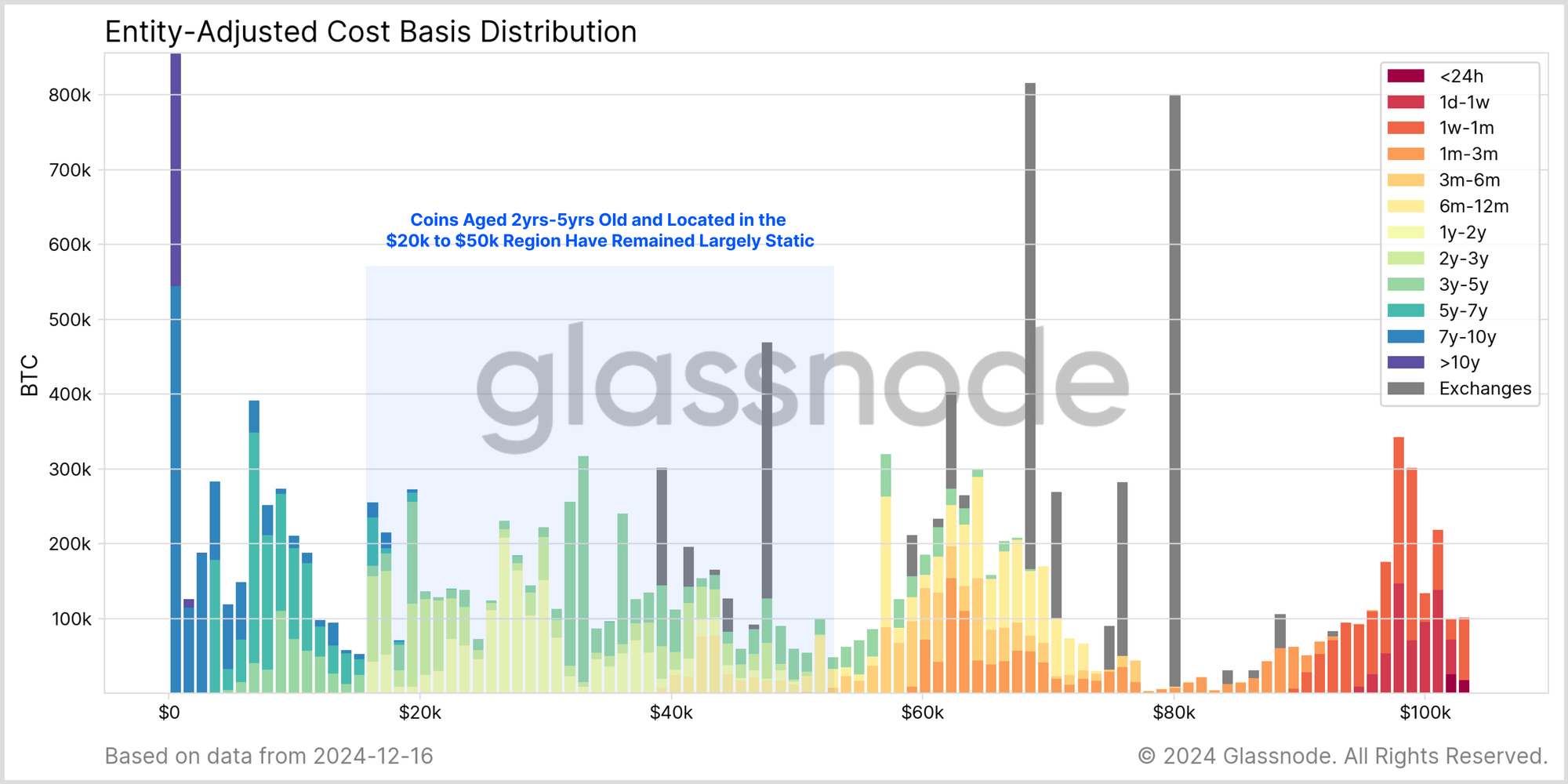

We can additionally bolster our thesis by assessing the URPD segregated by holding age. Here, we again note a significant amount of coins aged 2yrs-5yrs old remain changeless, underscoring the notion that higher prices are required to relinquish their coins.

Looking Upwards

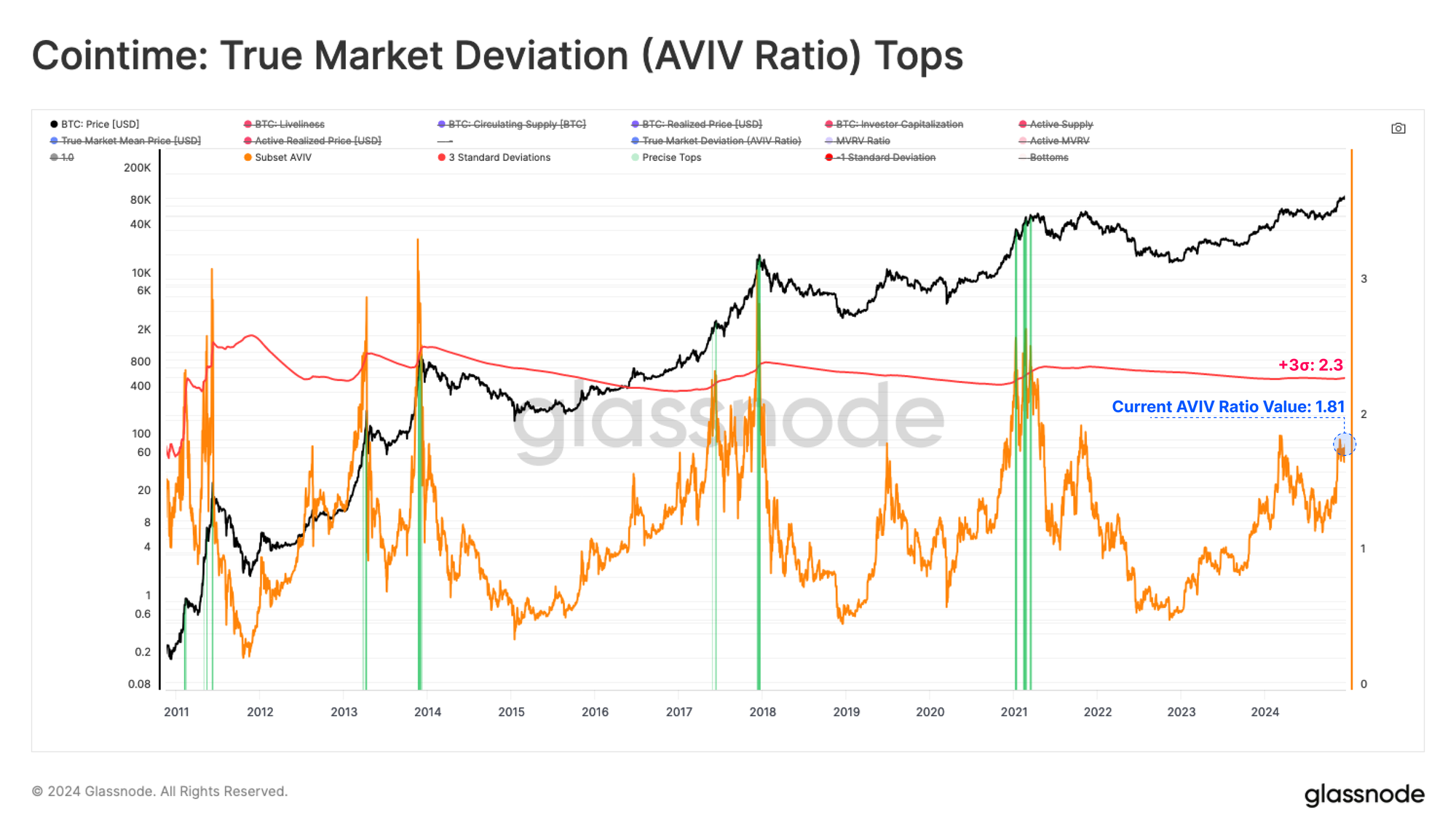

To close, we can now turn our attention to the AVIV Ratio which helps us assess the average unrealized profit (paper gains) held by investors that are active within the market.

We can utilize this metric to gauge whether the market is currently over/under heated relative to the profitability of its participants. Typically, Bull Markets reach their conclusion when all denominations of investors are in substantial profits, leading to enormous supply-side pressure coupled with an acute lack of new investors willing to buy at the current price.

At the moment, the AVIV Ratio has not yet reached its extreme band of +3σ, suggesting there may be room for the market to run before the profit held by the average investor becomes too tempting.

Summary and Conclusions

Supply-side forces are becoming increasingly prominent as Long-Term Holders continue to actively distribute coins on a large scale, resulting in an impressive $2.1 billion in realized profit. However, a strong demand side is also evident, largely counteracting the significant selling pressure from existing holders.

In addition, the proportion of network wealth held by new investors has risen sharply, supporting the notion of a robust demand profile. Nevertheless, this indicates a shift in wealth distribution away from mature investors, which typically occurs during the later stages of Bull Markets.

Disclaimer: This report does not provide any investment advice. All data is provided for information and educational purposes only. No investment decision shall be based on the information provided here and you are solely responsible for your own investment decisions.

Exchange balances presented are derived from Glassnode’s comprehensive database of address labels, which are amassed through both officially published exchange information and proprietary clustering algorithms. While we strive to ensure the utmost accuracy in representing exchange balances, it is important to note that these figures might not always encapsulate the entirety of an exchange’s reserves, particularly when exchanges refrain from disclosing their official addresses. We urge users to exercise caution and discretion when utilizing these metrics. Glassnode shall not be held responsible for any discrepancies or potential inaccuracies. Please read our Transparency Notice when using exchange data.

- Join our Telegram channel.

- For on-chain metrics, dashboards, and alerts, visit Glassnode Studio