Keyrock + Glassnode: Bitcoin and Ethereum as Competing Store-of-Value

In partnership with Keyrock, we examine how Bitcoin and Ethereum exhibit store-of-value traits by analysing their supply structure and usage profiles through Glassnode’s on-chain lens.

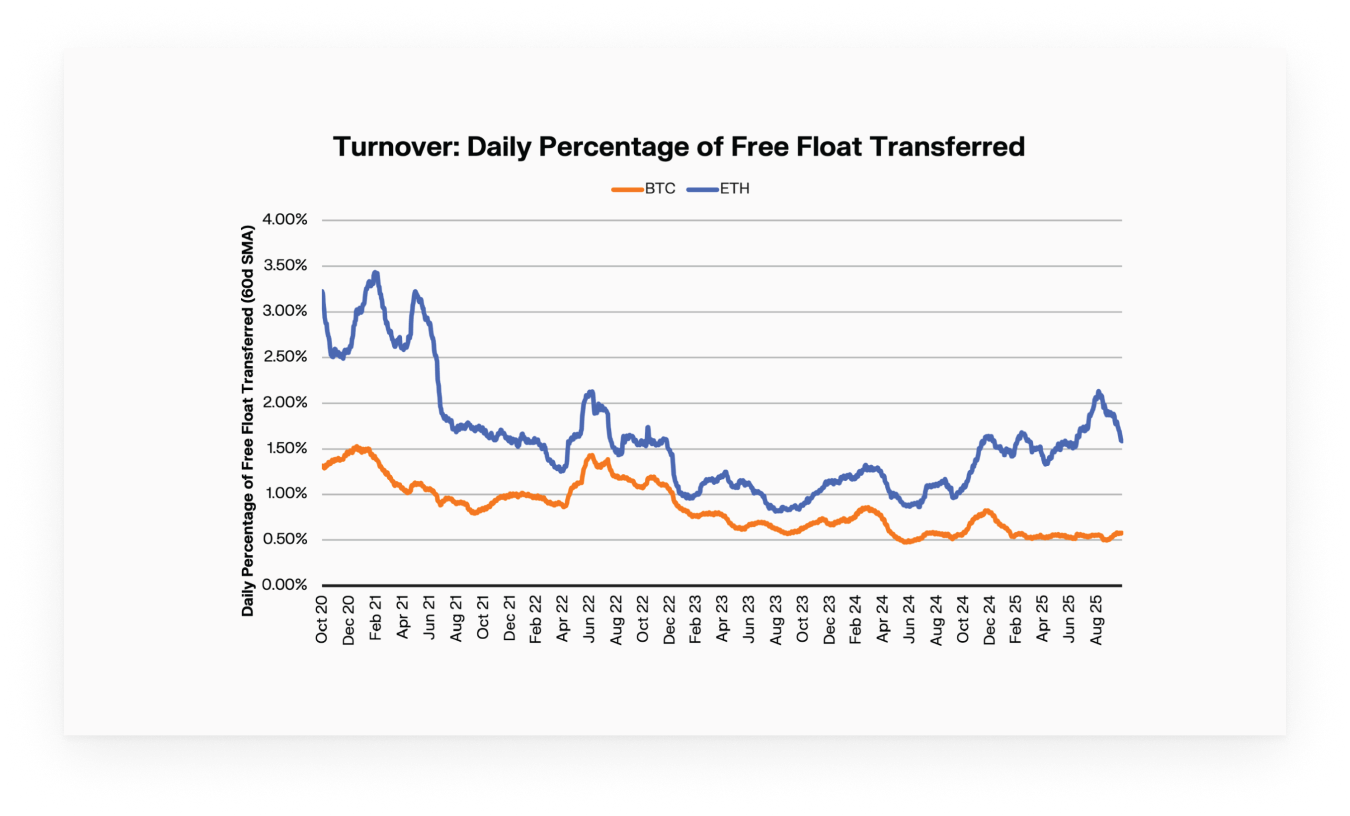

Bitcoin remains one of the lowest-velocity major assets, with over 61% of supply held dormant for more than a year. Ethereum, by contrast, rotates supply at roughly twice Bitcoin’s rate, reflecting a more active capital base. At the same time, exchange balances for both assets continue to contract, giving way to growing ETF holdings and institutional custody.

In our latest collaborative analysis with Keyrock, we unpack these shifts, examining how BTC and ETH are used today — and what that implies about their roles in the digital asset economy. Grounded in on-chain data, the report assesses where each asset sits on the Store-of-Value to Utility continuum, showing Bitcoin’s dominant savings-asset profile and Ethereum’s hybrid position as both reserve capital and working collateral within DeFi.

Key highlights from the report:

- Bitcoin diamond hands remain strong: More than 61% of supply hasn’t moved in over a year, and daily turnover sits at just 0.61%, reinforcing Bitcoin’s role as the market’s dominant store of value.

- Ethereum shows both utility and store of value behaviour: 1 out of 4 ETH is locked in native staking and ETFs. Yet it turns over at roughly twice BTC’s rate, reflecting the dual nature of ETH as a hoarded, yet productive asset.

- Dormancy between Bitcoin and Ethereum is diverging: ETH’s long-term holders are mobilising their old coins at a rate that’s 3x faster than BTC’s long-term holders, pointing to utility-driven behaviour.

- Ethereum powers the DeFi ecosystem: Around 16% of ETH supply is now deployed within liquid staking, and collateralised structures, highlighting Ethereum’s dual role as a reserve asset and working collateral underpinning DeFi.

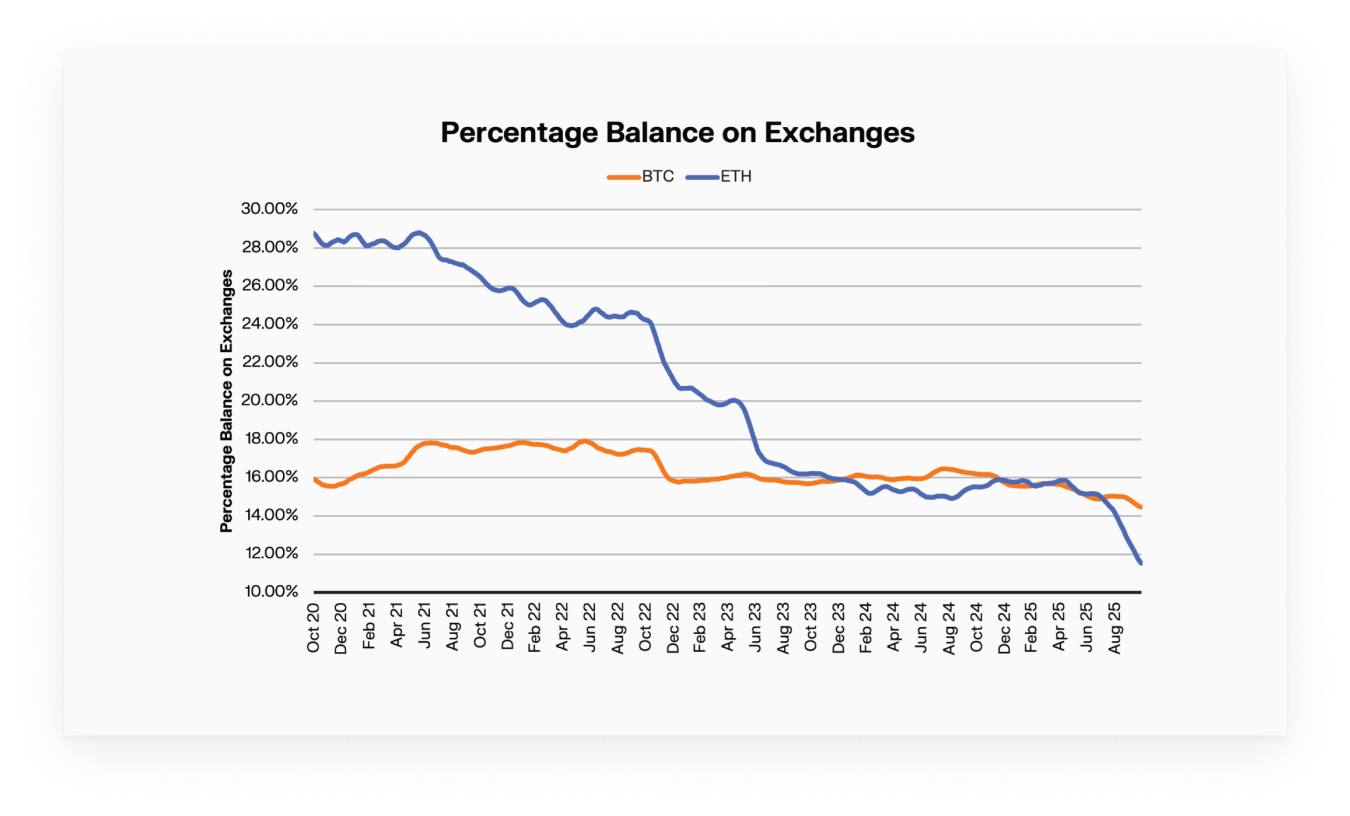

- Exchange balances are falling as institutional wrappers expand: Exchange-held BTC has declined by ~1.5% and ETH nearly 18%, as assets move into ETFs and DATs.

Context: Behavioural Framework & Definitions

Traditional economics defines Store-of-Value (SoV) as an asset that maintains purchasing power over time and can be saved and retrieved without significant depreciation. To evaluate BTC and ETH through a “store-of-value to utility” lens, we apply a behavioural framework using core Glassnode metrics and on-chain data:

- Dormancy – how long coins are held, assessed through Average Coin Dormancy and HODL waves.

- Turnover – how frequently coins move, or percentage of circulating or free float that changes addresses per day.

- Exchange-held supply – share of circulating supply held in centralised-exchange addresses, assessed using Glassnode's entity-adjusted exchange balance metrics.

- Anchored float – supply held in slow-mobilisation wrappers (staking, institutional custody, ETFs).

- Productive float – supply deployed as collateral, in lending protocols, liquidity pools or restaked structures.

Assets exhibit store-of-value traits when they show: high dormancy, low turnover, low exchange readiness, higher anchored float, and limited productive float.

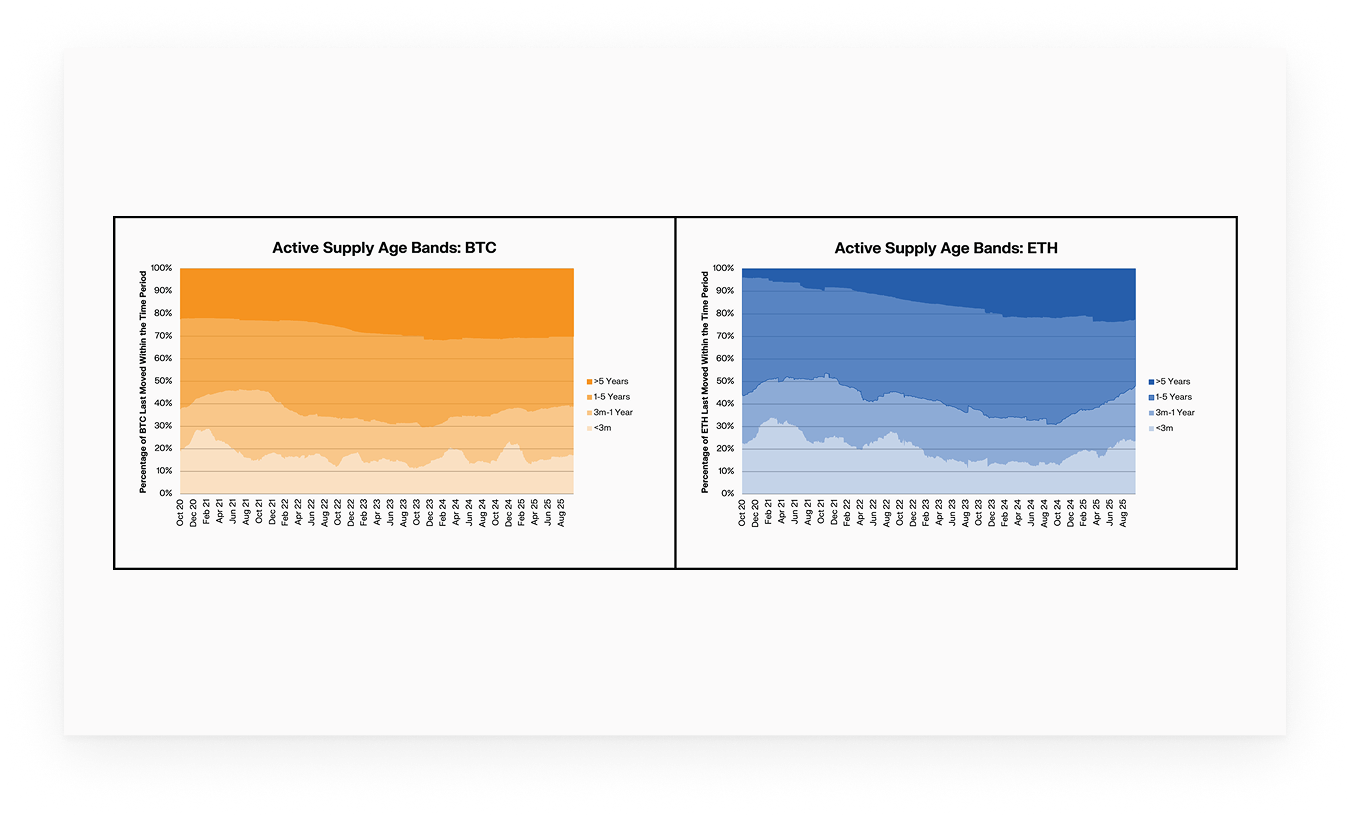

Dormancy: Bitcoin's and Ethereum's Patterns Diverge

Bitcoin’s supply continues to age, while Ethereum’s supply continues to mobilise. Bitcoin’s ≥1-year supply share is stable near 61%, indicating persistent long-term holding. Average coin dormancy for BTC has doubled over the past five years, despite temporary spikes driven by isolated legacy wallet movements.

Ethereum’s ≥1-year share declined more notably — from ~56% to ~52% — and average dormancy increased sharply into late-2025. This shows that older ETH is being re-activated more frequently, consistent with staking rotations, collateral shifts, and arbitrage activity.

Ethereum's Hybrid Utility and SoV Behaviour

Ethereum’s supply dynamics tell a different story. Long-term holders are mobilising older coins at three times the rate of Bitcoin’s, a trend captured in age-band shifts and rising dormancy.

ETH combines SoV-like anchoring (through native staking and ETF holdings) with productive use across DeFi. A large share of ETH participates in collateralised lending, perpetuals, restaking, LST/LRT structures, and liquidity pools — making it both a reserve asset and the operational capital of the on-chain economy.

Exchange-Held Balances Decline as Institutional Wrappers Expand

Both BTC and ETH continue to see supply migrate off centralised exchanges and into institutional wrappers and long-term custody. Exchange-linked BTC balances have declined by ~1.5%, while ETH’s exchange share has fallen sharply — from ~29% to ~11.3%.

This reduction is paired with the rise of spot ETFs and DATs. Bitcoin ETFs now hold ~6.7% of supply, with DAT structures accounting for ~3.6%. For ETH, ETFs hold ~5.2% and DATs ~4.9%. This shift reallocates supply out of highly liquid venues and into structures with slower mobilisation, narrowing effective float. For Bitcoin, this supports its low-turnover, savings-asset profile. For Ethereum, it complements its role as productive collateral.

Implications for Institutional Allocators

For institutions seeking a low-velocity, capital-preservation asset, Bitcoin remains behaviourally optimal. For entities looking for reserve exposure plus ecosystem participation, Ethereum offers a differentiated profile. Institutions modelling liquidity risk should also account for the structural migration of supply that is currently underway.

The clear divergence in usage patterns suggests that portfolio frameworks should treat Bitcoin and Ethereum as distinct exposure buckets rather than interchangeable ‘crypto’ risk. One is reserve-grade, the other is hybrid-growth.

🔗 Download your copy of the report

Disclaimer: This report is for informational and educational purposes only. The analysis represents a limited case study with significant constraints and should not be interpreted as investment advice or definitive trading signals. Past performance patterns do not guarantee future results. Always conduct thorough due diligence and consider multiple factors before making investment decisions.