DeFi Uncovered: Adjusting to the New Normal

As DeFi continues its downward move, we present a short-term bearish but medium-term bullish case.

The broader crypto markets continue their slow walk down, BTC has found itself trading under $30,000, and ETH firmly under $2,000. This week we present a number of metrics that argue a case for short-term pain, but long-term gain in the DeFi sector. The battle between bulls and bears remains active as more money than ever remains sidelined.

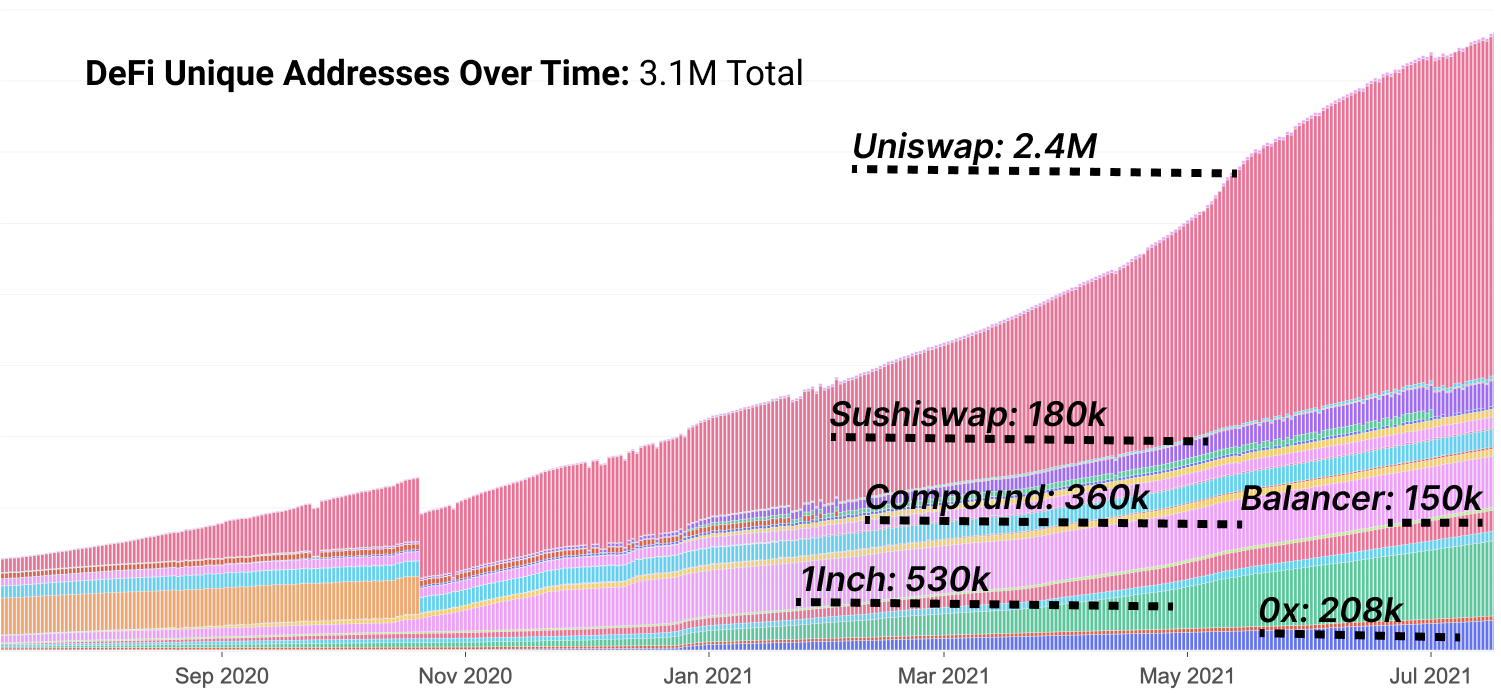

Bullish arguments for DeFi start with its trajectory of onboarding users. Being a nascent market, about a year out since starting its initial growth curve, DeFi remains a relatively undiscovered sector of crypto. The DeFi user-base growth has nonetheless been explosive, and even through a bearish period remain fairly impressive.

This ability to onboard during market distress is an important indicator of product market fit with DEX and DEX aggregators remaining the clear leaders in adoption. The growth over the last few months has slowly started to flatten from parabolic growth earlier in the year.

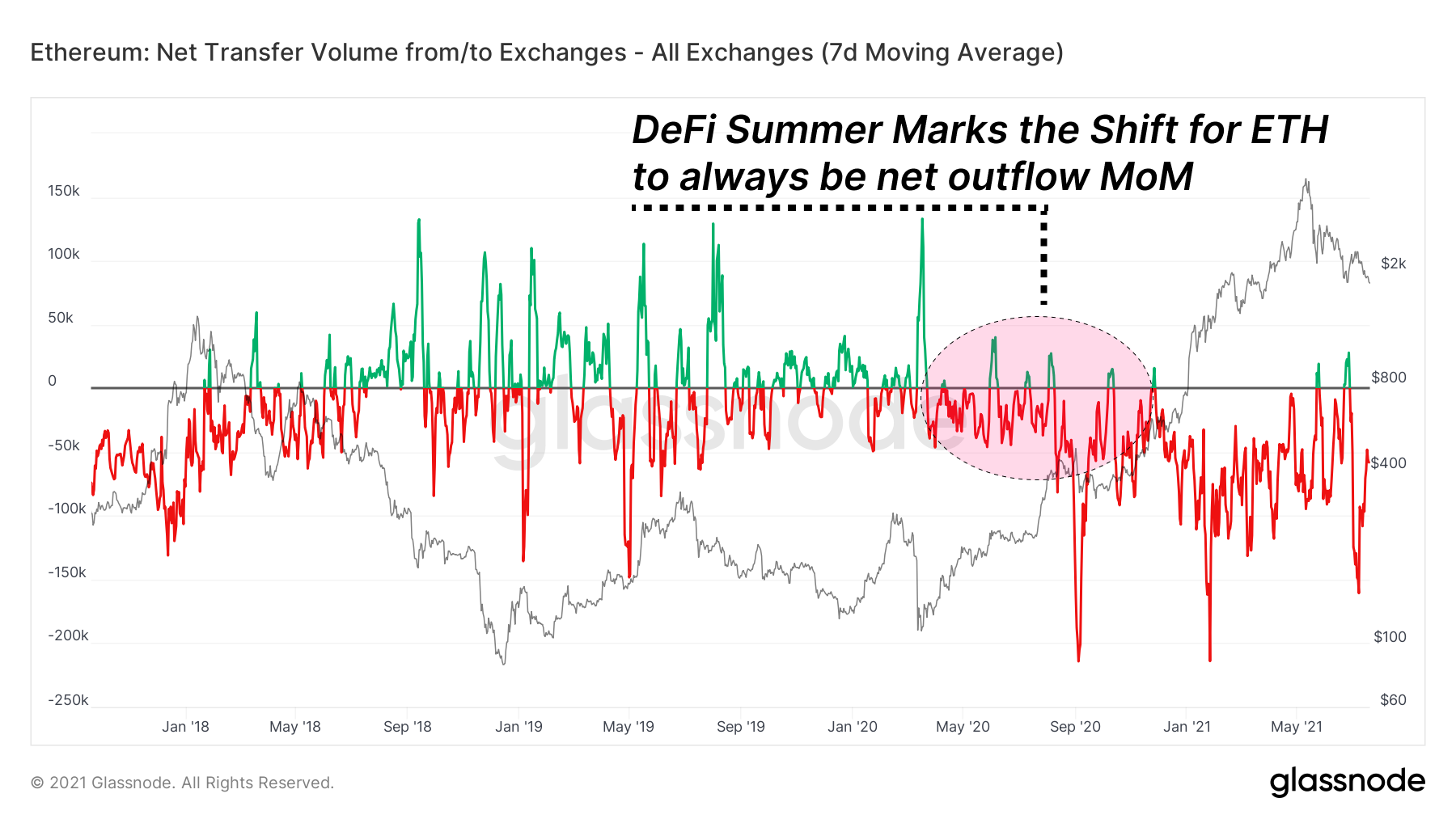

Exchange ETH balances continue to trend down, despite declining prices. This showcases the utility of Ethereum in its own ecosystem, with a persistent need for the ETH token as a base layer collateral. Since DeFi Summer, cumulative outflows month over monthhave been persistent, signalling continued movement of capital off centralised exchanges and into the DeFi ecosystem.

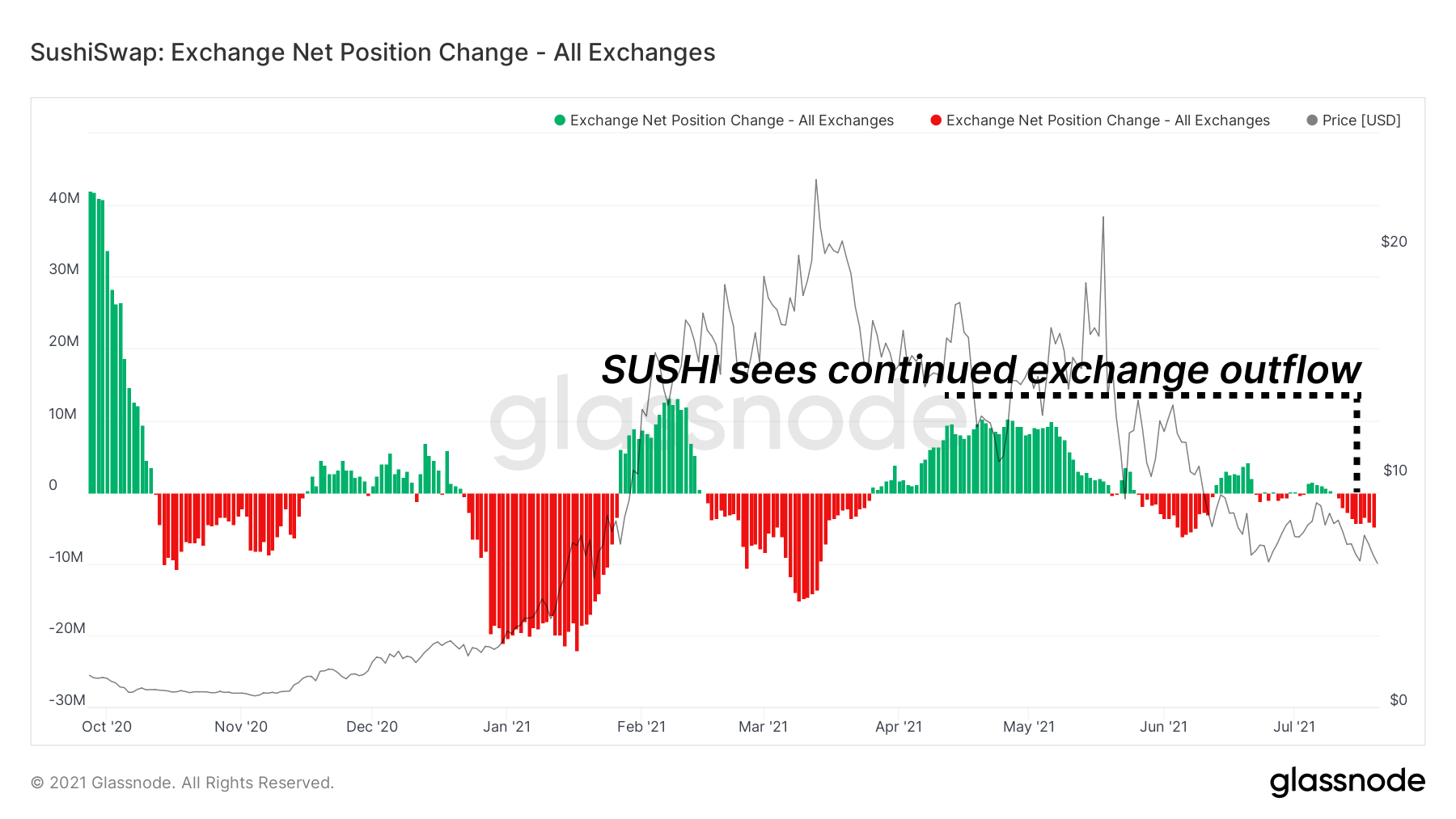

For governance tokens, we see similar stories across tokens with broad utility. Tokens demonstrating value for holders and ecosystem-wide integrations tend to maintain a stronger on-chain presence, with exchange flows consistently outbound. Tokens like SUSHI which boast strong on-chain incentives via staking to earn earning trading fees, and numerous integrations with lending markets, have seen net exchange outflows during this correction.

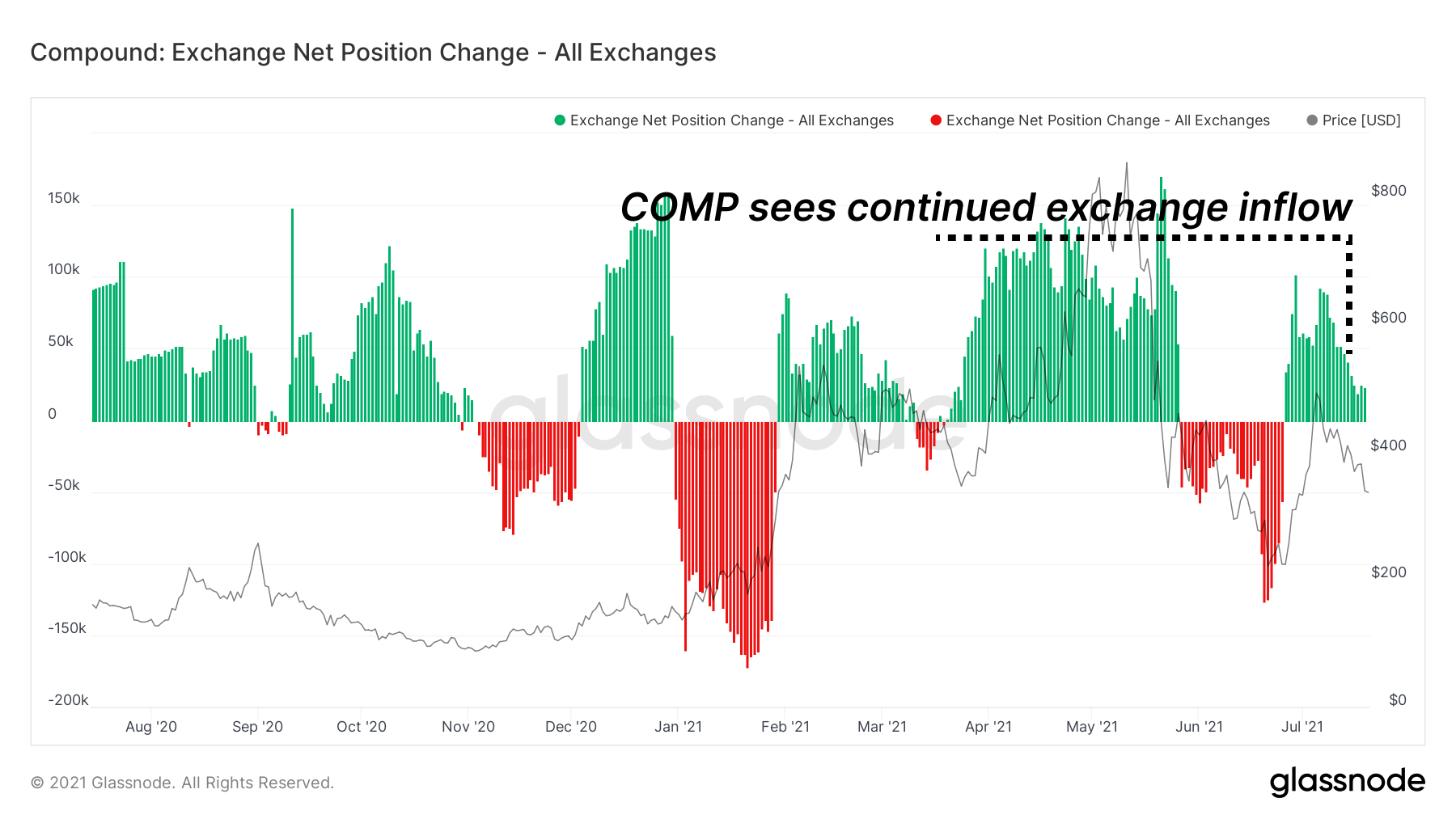

Simultaneously, tokens like COMP with limited usage for their token are consistently sent to exchanges to be held or sold rather than remain on-chain. Note that both SUSHI and COMP are aggressively farmed via liquidity incentives. One remains on-chain because of its usage in the ecosystem, the other finds its way to centralised exchanges.

Stablecoin Flows

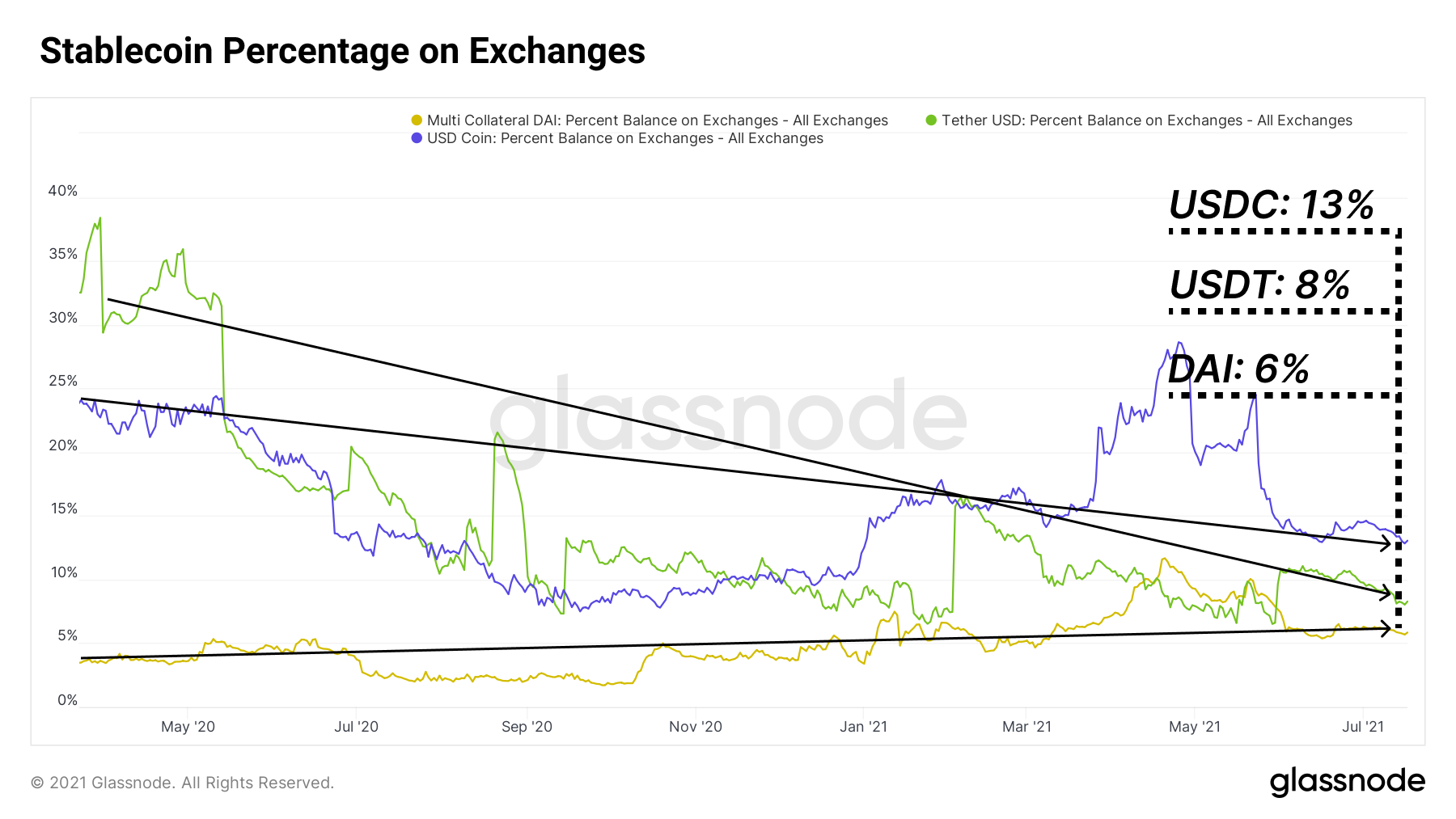

In risk-off capital (stablecoins), billions of dollars remain sloshing around the DeFi space. A commonly touted bearish prediction during the bull run was that once markets dipped, liquidity would drain from the ecosystem, sit in cash, and capital efficiency of DeFi would be an event isolated to bull markets. Instead, that risk-off capital has remained firmly on-chain, much of it positioned in DeFi.

During the bull market, stablecoin flows and pools were lead strongly by DEX protocols like Uniswap and Sushiswap because of the elevated demand for trades in risk-on pairs, and token farming.

During this risk-off period, naturally, the demand for risk-off capital in the ecosystem has strengthened. This is demonstrated in the emergence of a clear dominance for Aave (lending), Curve (stablecoin DEX), and Compound (lending) in hosting stablecoin liquidity pools. The current market behavior of depositing stablecoins to Aave, Compound, and Curve to earn yield appears favored to the alternative - leaving stablecoins on centralized exchanges waiting for buying opportunities.

While overall liquidity remains flat to down for risk-on platforms like Uniswap and Sushiswap, the market has seen a growth in flows into lending markets like Aave, Curve and Compound. A metric to watch for the turning of the tides would be when sentiment shifts, and risk-off capital starts to flow back into risk-on DEX markets.

While these arguments are largely in favor of a risk-off approach, they are medium to long-term bullish for the future of DeFi - capital remaining in the ecosystem as stables to farm governance tokens mean allocators believe in these projects and supporting the space. The fact allocators turn to DeFi instead of away during downturn speaks volumes for the future of decentralized finance.

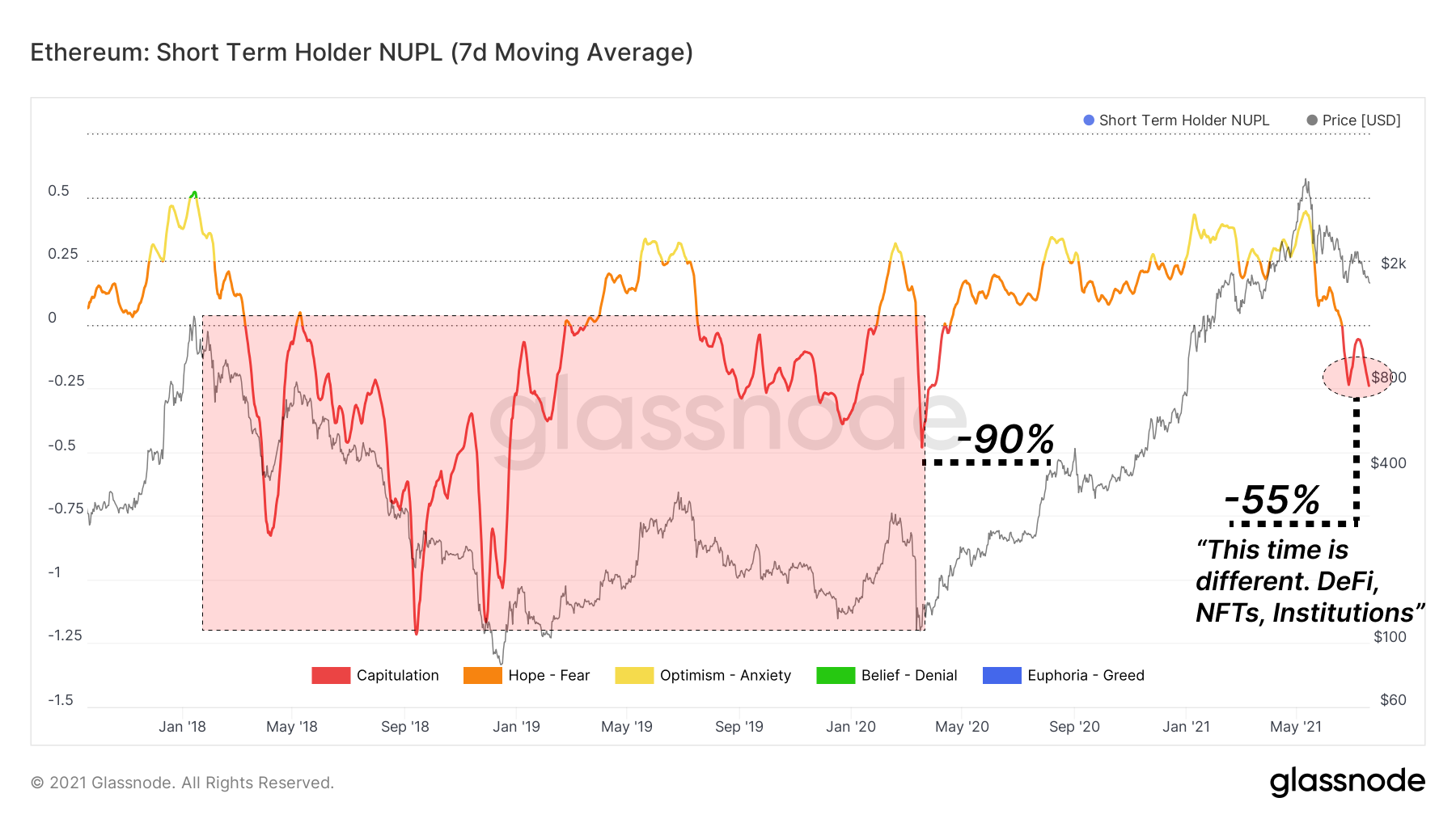

Short-term holders of ETH are in capitulation mode, with NUPL levels pushing to pain thresholds not felt since early 2020. With ETH prices down 55% from the highs, the total outstanding unrealized loss for ETH buyers in the bull market currently stand at -25% of the ETH market cap. If 2018 is any form of guide, there is still room to the downside before a capitulation of the same magnitude as mid 2018 to early 2020 is reached.

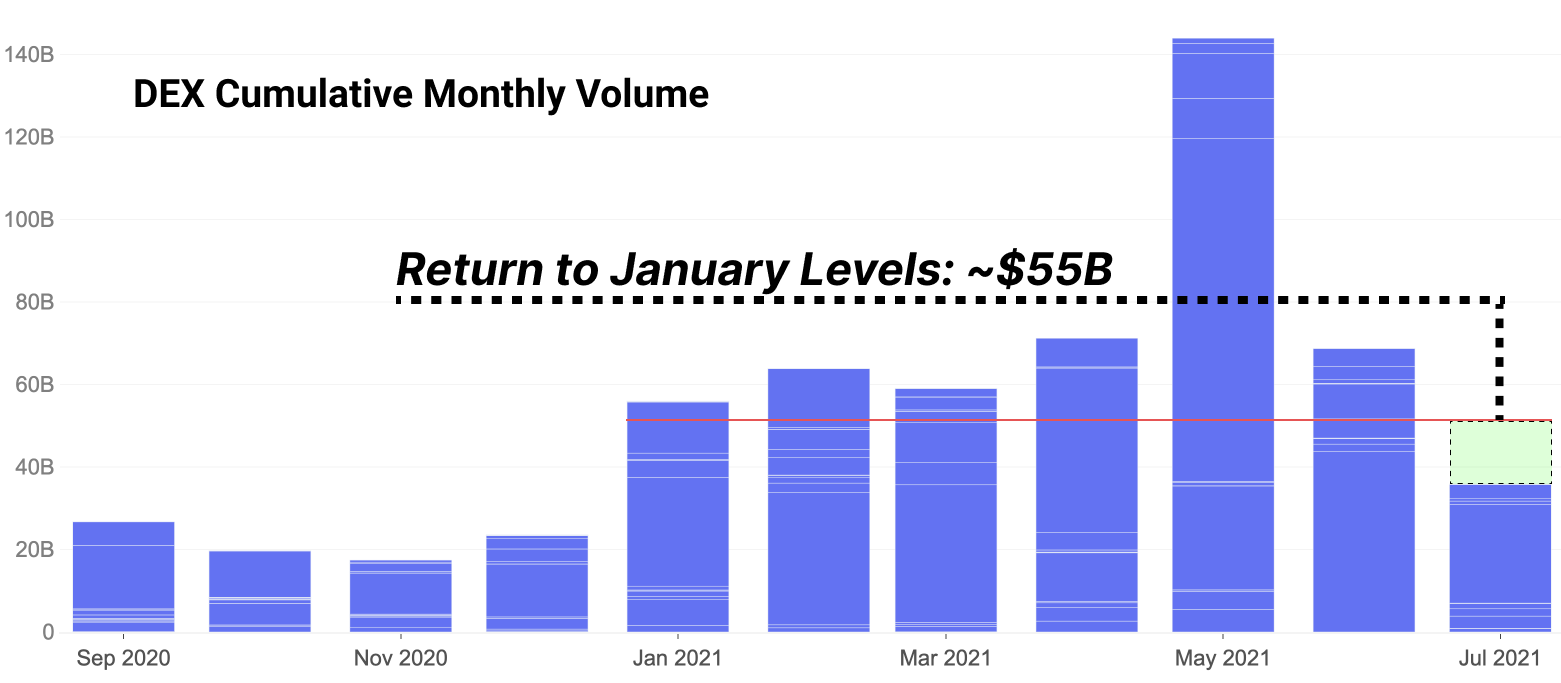

Volumes are flat across DEXs, with volatility in a lull. One can argue that in nascent markets, healthy growth looks like continued MoM growth as it grows the pie in a largely an untapped market. Clear product market fit is often driven by such unwavering growth that only slows or trends sideways at high market penetration. The key question is whether DEX growth is somewhat dependant on bull market speculation? Where do the next 3M users and $100B in marginal volume come from?

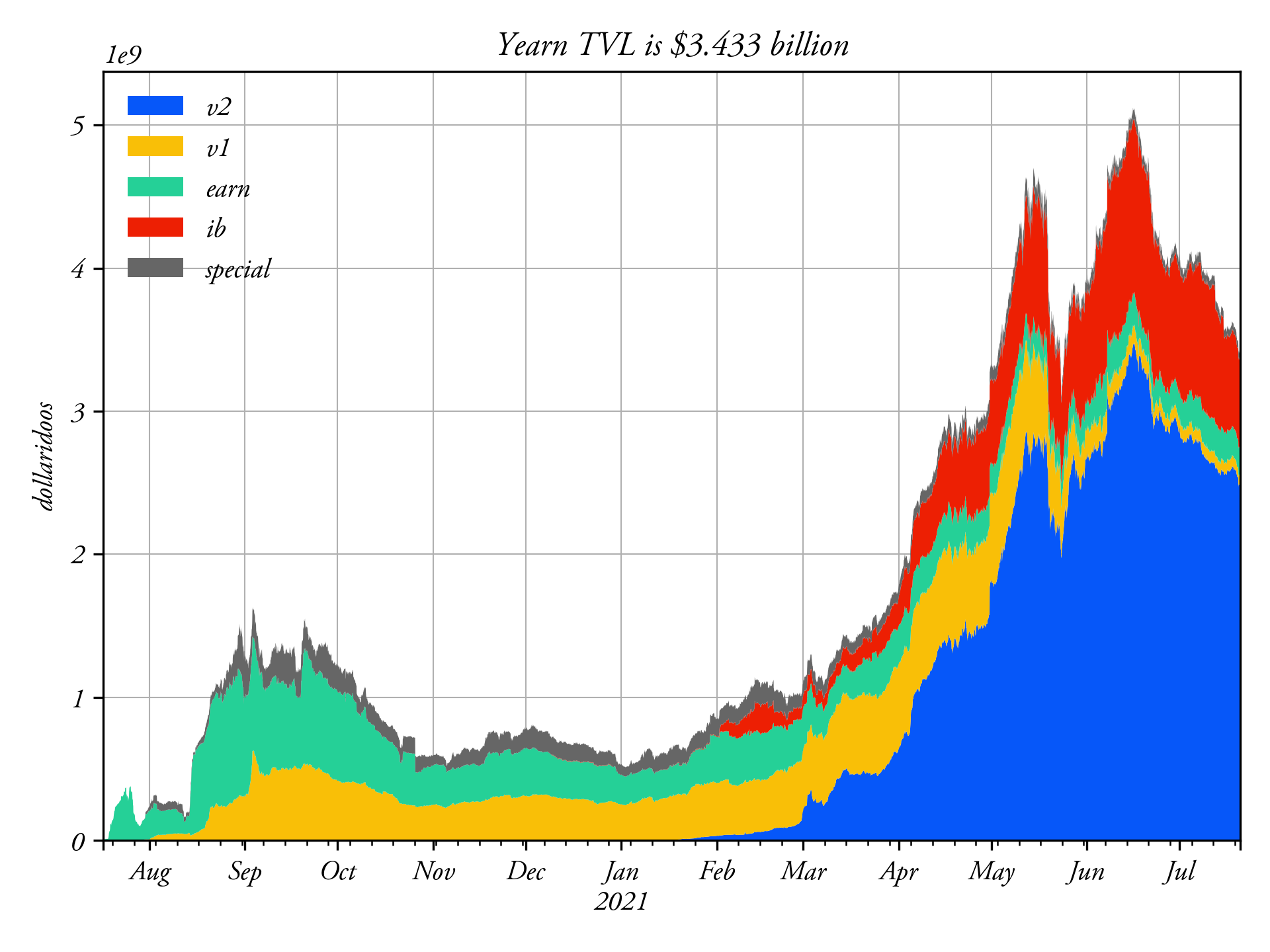

We've shown week after week the depression of risk-free rate in lending platform yield. Now firmly under 4% even with liquidity incentives, yield aggregators present the next line of defense for chasing yield. As a result, even for DeFi's darling of aggregators Yearn, yields have similarly compressed, now under 4%. Yearn has seen a corresponding drop in TVL after a period of strong growth following the launch of v2 vault products. Liquidity appears to be only as loyal as the differentiated yield it's chasing.

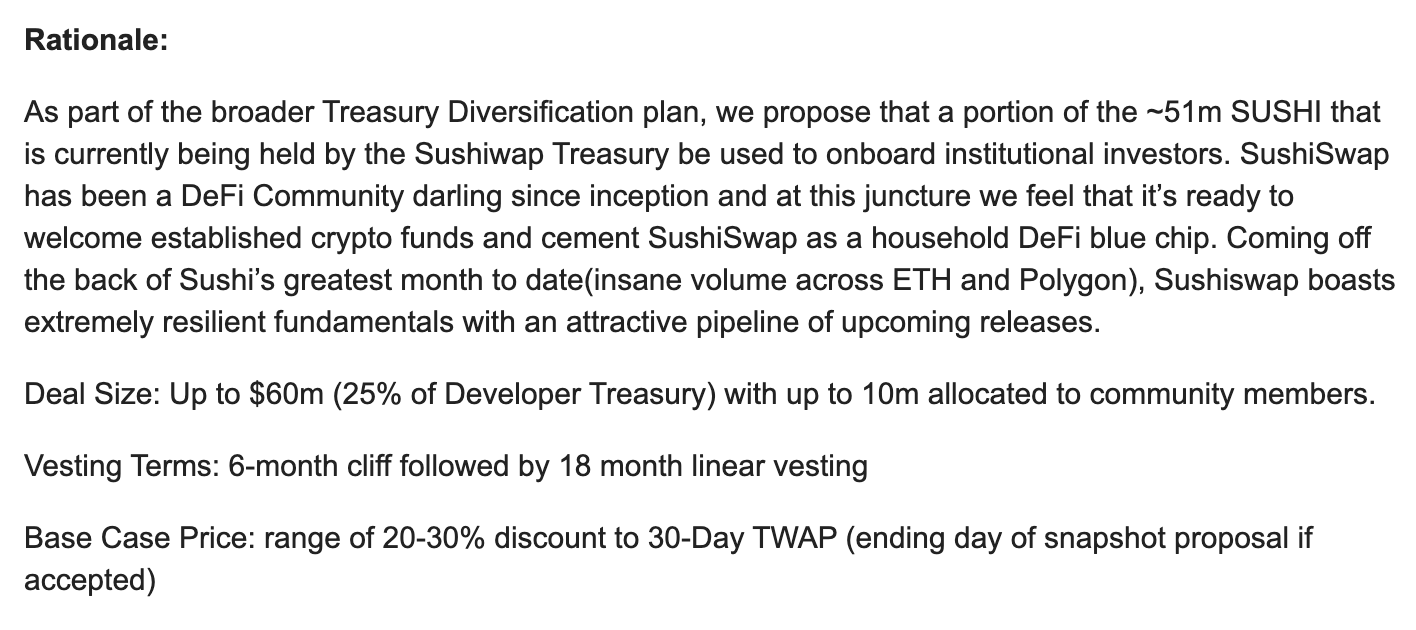

As liquidity exits, so too does protocol revenue. Fees to token holders shrink. Treasuries stop growing at previously meteoric paces. Teams that have grown quickly realize they need to diversify the funds in their treasury. Reliance on their own token for funding becomes a concern. Should the token depress in price too far, they will be unable to pay developers. Or the price to pay those developers in USD equivalents will be an excessive amount of tokens. Take the recent Sushiswap turn to institutional investors as a hint of what's going on.

The recent Sushiswap proposal for treasury diversification via institutional investors has been a hotly contested discussion on the governance forum:

More and more teams are selling tokens in the open market, selling equity and tokens to investors to get stablecoins in the treasury, and altogether taking steps that show there's clear desire in DeFi to hedge any further risk of downturn. Teams that sell tokens risk depressing price, teams that don't sell tokens risk shuttering the project or firing devs in severe downturn. There's a healthy balance teams will try to strike as we continue forward into uncharted territory.

Closing Remarks

As DeFi valuations work hard to catch a bid, fundamentals remained a mixed bag of short-term bearish activity, but medium-term bullish capital flows. While allocation remains risk-off, allocators have retained significant liquidity within the ecosystem. This signals a stockpile of capital is waiting to be deployed into risk-on assets should fundamentals and valuations find bullish ground.

Fundamentals driving a short-term bearish but medium-term bullish view:

- User growth continuing to grow however at a flattening rate.

- ETH persistent net exchange outflows.

- Utility-driven governance tokens see net exchange outflow, whilst governance tokens with less direct utility seeing net inflows.

- TVL for stablecoin centric platforms like Curve, Aave, and Compound remains sideways to up despite a tumultuous market.

- Volumes are back down to January levels, yields in the gutter and protocol revenues in steady decline.

Uncovering Alpha

This is our weekly segment that briefly discusses some of the most important developments of the prior and upcoming week.

Enthusiasm for building continues, regardless of the direction of price. We look to L2 especially as DeFi dev efforts remain hot.

- Maker launches a DAI bridge for Optimism. Users can now move DAI from mainnet Ethereum to Optimism L2. This marks an important step, adding support for one of DeFi's most important stablecoin assets.

- Curve updates Tri Pool. Curve's Tri Pool releases some important updates, with a migration tool included. The newest addition to Curve with USDT, wBTC, and ETH undergoes some important updates after a short period of being live.

- Sushiswap launches limit orders. Prior, limit orders would have required some custom work or an integration. From now on, users can execute on-chain limit orders via the Sushi UI. Note that this release is only supporting Polygon for now.

- Shapeshift airdrops for past users. The airdrop has happened along with plans to decentralize the project with a DAO, an important step for a previously popular product with highly centralized elements.

- Coinbase adds withdrawal support to Polygon. Users can now directly withdraw assets to Polygon network. Look to Coinbase and others with ties to Optimism and Arbitrum, especially through their venture arms to soon do the same.

- Alchemix relaunches alETH. The relaunch of their ETH collateral marks the transition from the previous turmoil from a bug that allowed withdrawals without paying back debt. The relaunch puts their TVL well over $1B.

- Much of the community in Europe gathers for ETH's largest European conference ETHCC. Tons of teams, devs, and community members are presenting on DeFi and many topics relative to dev efforts during the event.

- Follow us and reach out on Twitter

- Join our Telegram channel

- For on–chain metrics and activity graphs, visit Glassnode Studio

- For automated alerts on core on–chain metrics and activity on exchanges, visit our Glassnode Alerts Twitter

Disclaimer: This report does not provide any investment advice. All data is provided for information purposes only. No investment decision shall be based on the information provided here and you are solely responsible for your own investment decisions.