DeFi Uncovered: Finding Alternative Sources of Yield

As crypto continues its sideways walk, finding alternative sources of yield become attractive in an environment of depressed rates.

As crypto continues its sideways walk, traders and investors continue to seek opportunity amongst low volatility market conditions. Finding alternative sources of yield usually requires more a active involvement in the fast evolving DeFi sector.

In this piece we will cover:

- The state of Ethereum DeFi during depressed volatility,

- Assess the underlying drivers of the recent attention on Synthetix

- Review of 'blue chip' sources of yield in DeFi

- Template for finding alternative sources of yield in DeFi

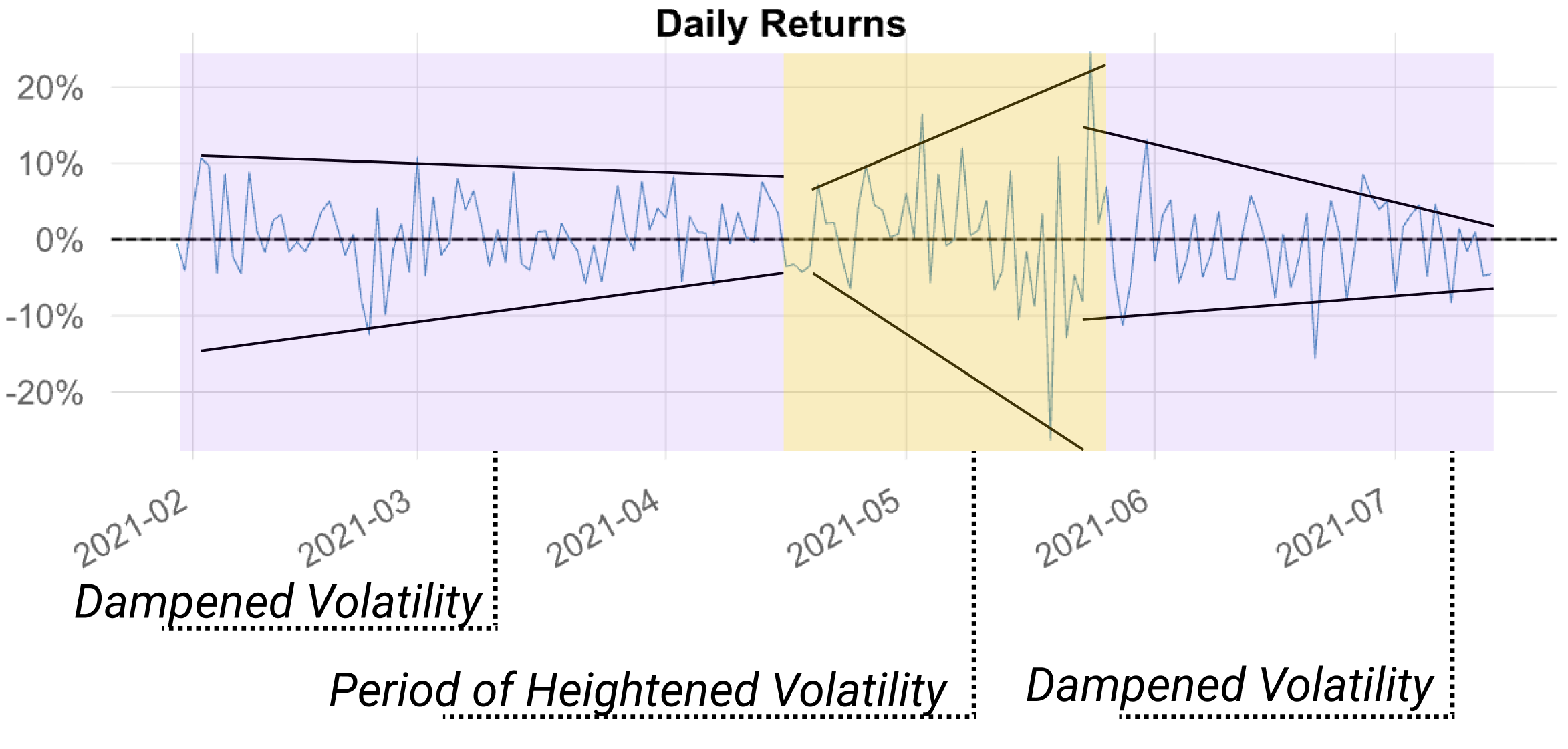

Dampened Volatility

Ethereum prices have slumped once again after a brief period of relief, while some DeFi tokens experience isolated breakouts despite mostly static fundamentals.

Dampened volatility historically precedes more volatile moves, and the longer the spring coil ups, the larger the impulse that follows. In this first chart, we can note how daily returns dampening off from June to July after a highly volatile period in May.

ETH prices still have a lot of ground to make up to exit its current drawdown period should volatility return to the upside. Conversely, a volatile move to the downside would likely erase the remaining gains from 2021.

Synthetix Catches an Isolated Bid

As Ethereum continues its nervous sideways walk, isolated pockets of uncorrelated returns are finding their way to popular DeFi tokens. Synthetix is the latest such story, finding strength amidst founder Kain's return to the project. Synthetix has announced its plan to transition the project's focus and liquidity over to Optimism (an Ethereum Layer 2). Simultaneously, news that SNX stakers could be receiving a series of airdrops in the future has led to even more bullish narratives supporting the token.

Returns for Optimism stakers reached an absolute bottom of ~15% APY in July while L1 staking remains relatively lucrative. Following the transition of liquidity to L2, Optimism stakers are now receiving ~50% APY, and can expect sUSD/sETH, sUSD/sBTC, and other trading pairs to launch in July/August.

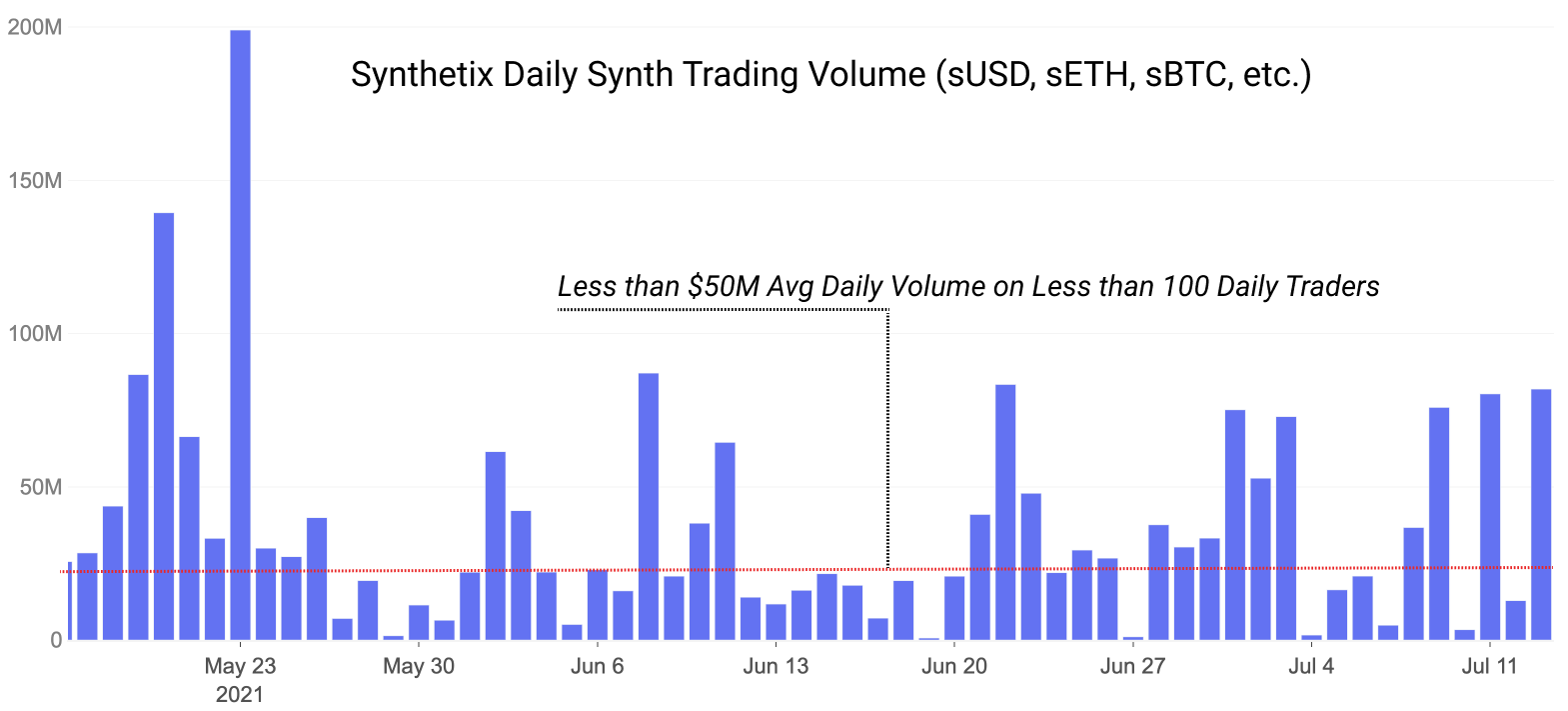

Synthetix is hoping the transition to L2 will mark a new age for the product, one with more users, more volume, and more activity. To date, the project has struggled with relatively high fees on L1, oftentimes with less than 100 daily traders and regularly seeing <$50M in daily volume. Additionally, Synthetix booked numerous days of <$15M in volume and less than 50 users through June. Token holders of SNX can now look forward to the transition to Optimism, benefiting from lower fees and a hopeful uptick in trading activity.

Synthetix presents a case study of a well established project making the one of the many leaps into Layer 2.

Blue Chip Yield

We have discussed a number of projects and yield farming opportunities throughout the space in DeFi Uncovered. As a reminder, here are some of the principle categories of earning yield in the form of fees and liquidity mining incentives:

- Earning fees via liquidity provision in decentralized exchanges

- Yield from lending assets in lending pools

- Earning governance tokens from liquidity mining incentives

As demand for risk-off capital (stablecoins) increases, DeFi tokens are seeing depressed valuations, and active risk-on capital is dwindling, all leading to a general contraction of yields across the space. To understand how these pieces all fit together, consider each piece one at a time:

- Stablecoin Capital is increasing: a steady flow of capital is fighting over the same share of value. As more capital enters yield generating protocols, yield is diluted across all participant dollars.

And we're seeing this is clearly the case, as dollar equivalents in DeFi are outpacing the market cap growth of Ethereum and token valuations. There's clear demand for DeFi yield based on the volumes of capital sloshing around. However that capital isn't being deployed into buying spot ETH or governance tokens; it's largely staying risk-off.

With increased capital comes increased competition for the same pie.

- Decreased on-chain activity: if the available fees from user activity (e.g. trading volume) are decreasing but the capital trying to soak up those fees is static or increasing, this leads to less available yield opportunity for liquidity providers.

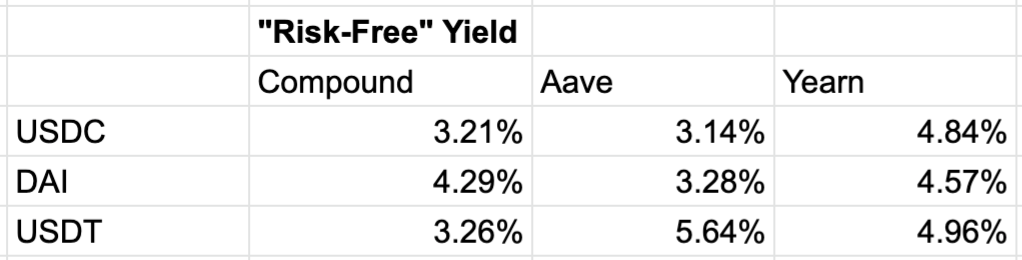

Usage of decentralized exchanges is down across all blockchains. Demand for borrowing, speculation, and thus utilization metrics are depressed. Overall, despite investment in DeFi remaining strong, the actual usage metrics of DeFi are relatively weak. As a result, risk-off yield in well-known venues like Aave, Compound, and Yearn are all falling to below 5% base APY, 3-5% after liquidity incentives in Aave and Compound.

- Depressed token prices: if the rewards subsidizing liquidity in these protocols are losing value in dollar equivalents, so too is the overall yield. As more capital flows in to farm these tokens but the tokens continue to drop in value, the dollar value of farming these tokens continues to trend down.

A handful of tokens are making uncorrelated moves to the upside against ETH, but as a whole, token prices remain heavily depressed from ATH. Stakers of governance tokens have already lost 60%+ in their staked capital. The tokens being farmed are typically rewarded as the same token that is being staked, and thus rewards have also lost ~60%+ in value.

Summary: yields are continuing to compress across the sector as an aggregate impact of decreased usage and fee generation, depressed token prices (and thus reward values) and an increasingly large volume of stablecoin capital participation.

In such an environment where capital is abundant, but most tokens are failing to find marginal buyers, how can traders find new sources of yield?

Alternative Sources of Yield

These can difficult to find and in many instances require enhanced risk management and deeper insight into the underlying mechanics. Highly active traders can do extra legwork to find these alternative sources of yield in an attempt to boost returns through any market conditions.

These are sources of yield that are generally less crowded by merit of being less well-known, more esoteric, and likely riskier than the average DeFi protocol.

Risk-On Early Emissions

We discussed in traditional yield the three factors dragging down traders' yield:

- Lots of participants/liquidity

- Low utilization/volume

- Declining token prices

Naturally, traders can look to counter these 3 factors by:

- Finding early pools with low participation

- Finding diamonds in the rough with high utilization

- Identifying projects with appreciating token prices

Saddle is an AMM that borrows many mechanisms from Curve, particularly its low slippage stablecoin pools. Unlike Curve, most of its lockups/staking opportunities are elsewhere.

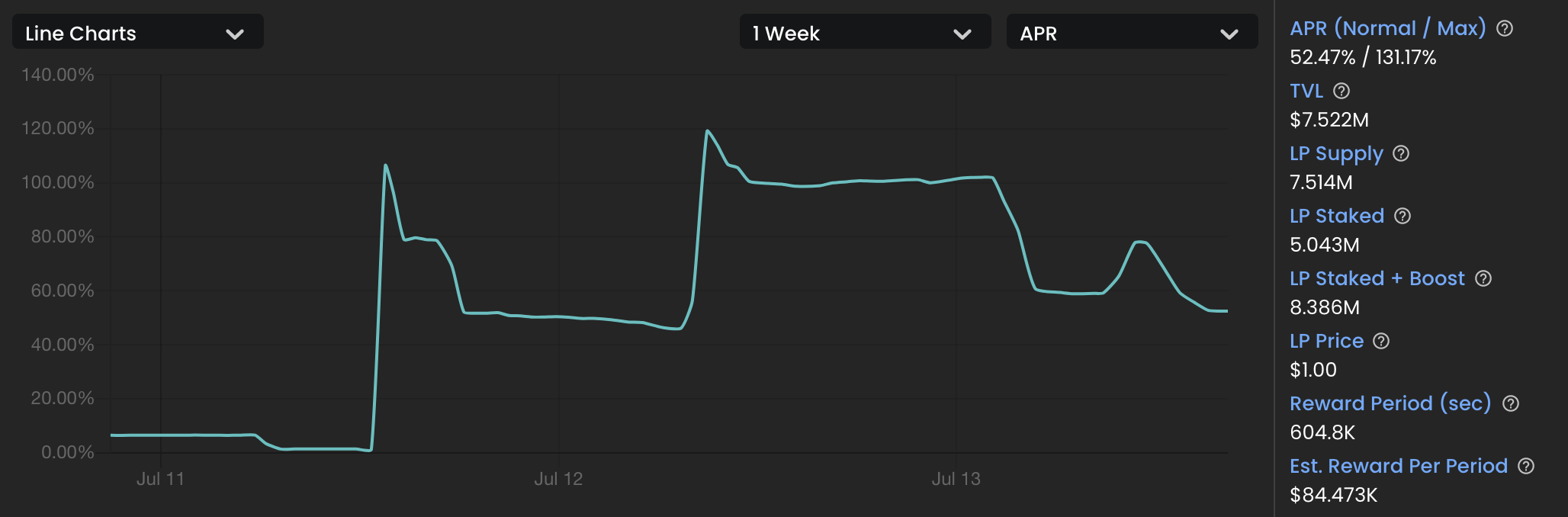

Staking Saddle Finance's "D4" stable pool of alUSD/FEI/FRAX/LUSD pool is an example of an early entry (launched 11 July) with inflated returns. Liquidity providers receive a base APY from fees (5%) and additional boosted rewards from staking, not unlike Curve. Boosted stakers with a 1 year lock are earning up to 110% at current participation levels.

The "D4 Pool" of alUSD/FEI/FRAX/LUSD is a Saddle pool comprised of 4 experimental stablecoins, each experimenting with novel ideas. Stakers can lock their liquidity provider positions for up to a year for boosted rewards.

Reminder on the assets in this pool (all experimental):

- alUSD: Alchemix's zero liquidation stablecoin, collateralized by DAI.

- FEI: Fei Protocol's algorithmic stablecoin that struggled to maintain a peg at launch, but has since recovered.

- FRAX: Frax Finance's partial algorithmic, partially backed stablecoin.

- LUSD: Liquity's ETH collateralized stablecoin.

Of course, with anything new, less time has passed for potential exploits to be uncovered. We do our best in DeFi Uncovered to identify higher quality risk-on projects, but exploits are abundant in new experiments so participants should always approach with caution.

Derivatives

Derivatives are a relatively quiet corner of DeFi. This is largely due to the high cost of gas on Layer 1 for most derivatives products and other added frictions that have kept liquidity low, degrading from the overall user experience.

Despite the lack of traction to date, many popular derivatives from legacy finance, as well as fresh ideas on derivatives have been, or are being built out. Derivatives ported over from legacy finance include options, futures, swaps, and other products. The markets for these products are often unique from the rest of crypto, offering different kinds of risk/return profiles.

Options

Many options platforms exist, however most with poor liquidity and with high gas costs. Dozens of venture deals have been made to fund new options platforms, however most are either unlaunched or unable to find liquidity/users to date.

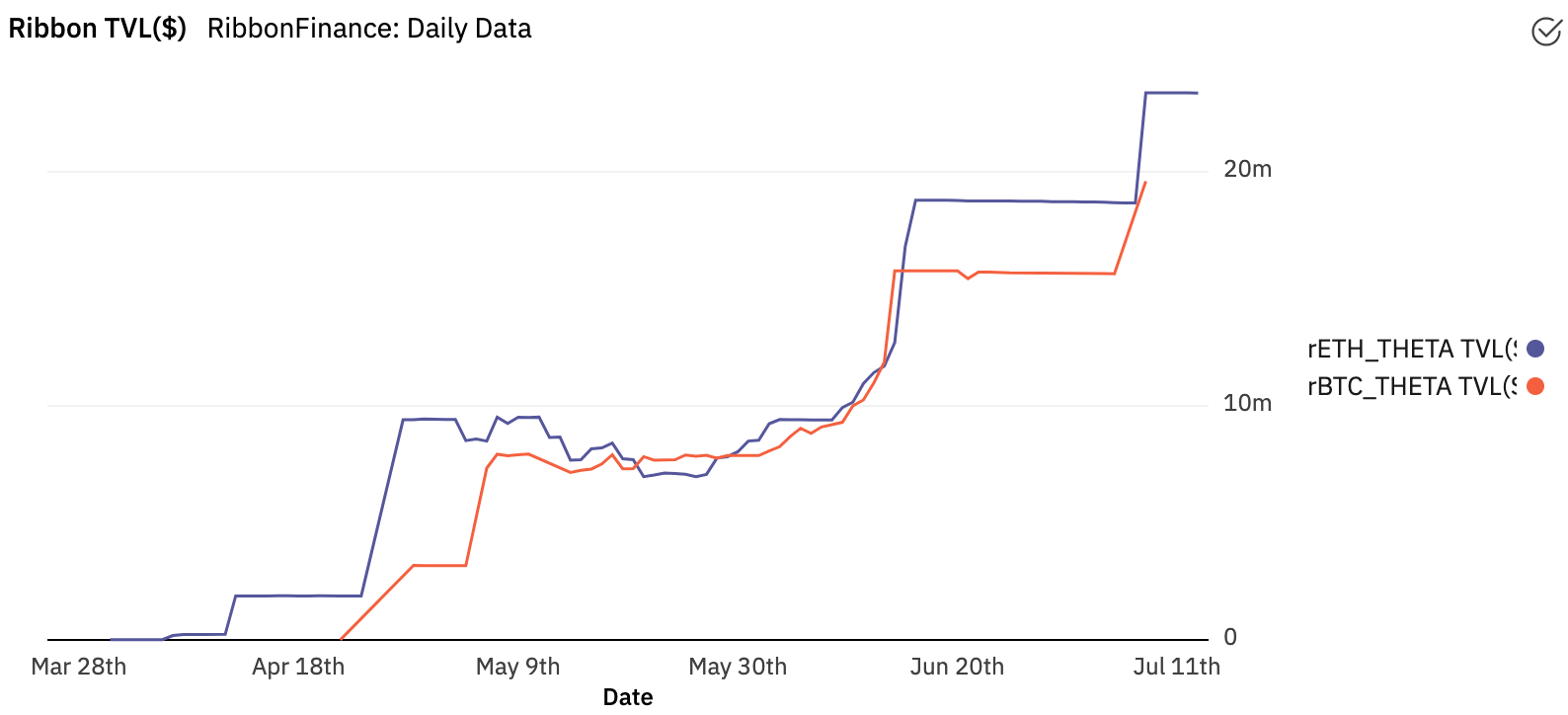

Ribbon Finance is an example of one protocol that has managed to create some activity in the space. Their product makes it easier for participants to put on automated positions like rolling put selling strategies and covered calls. Previously, participants would have had to scour the options landscape for sparse liquidity and manually put on positions, usually taking on massive gas fees and inflated option prices. Ribbon uses options from Opyn to put on positions, composability at work.

Their marquee vaults involve automated buying of covered calls and selling of out of the money puts. Each time vaults have had available liquidity they are quickly filled. There's clearly demand for this kind of yield, just a limited availability for liquidity and differentiated products.

Put selling: strategy profits if ETH stays above strike price (set by vault manager) by a certain date; good position if believe in low volatility or low likelihood of high downside volatility. (vault projects ~30% APY + RBN staking rewards)

Covered calls: profit from strike price of the bought option minus the cost of underlying + option premiums.

Perpetual Contracts

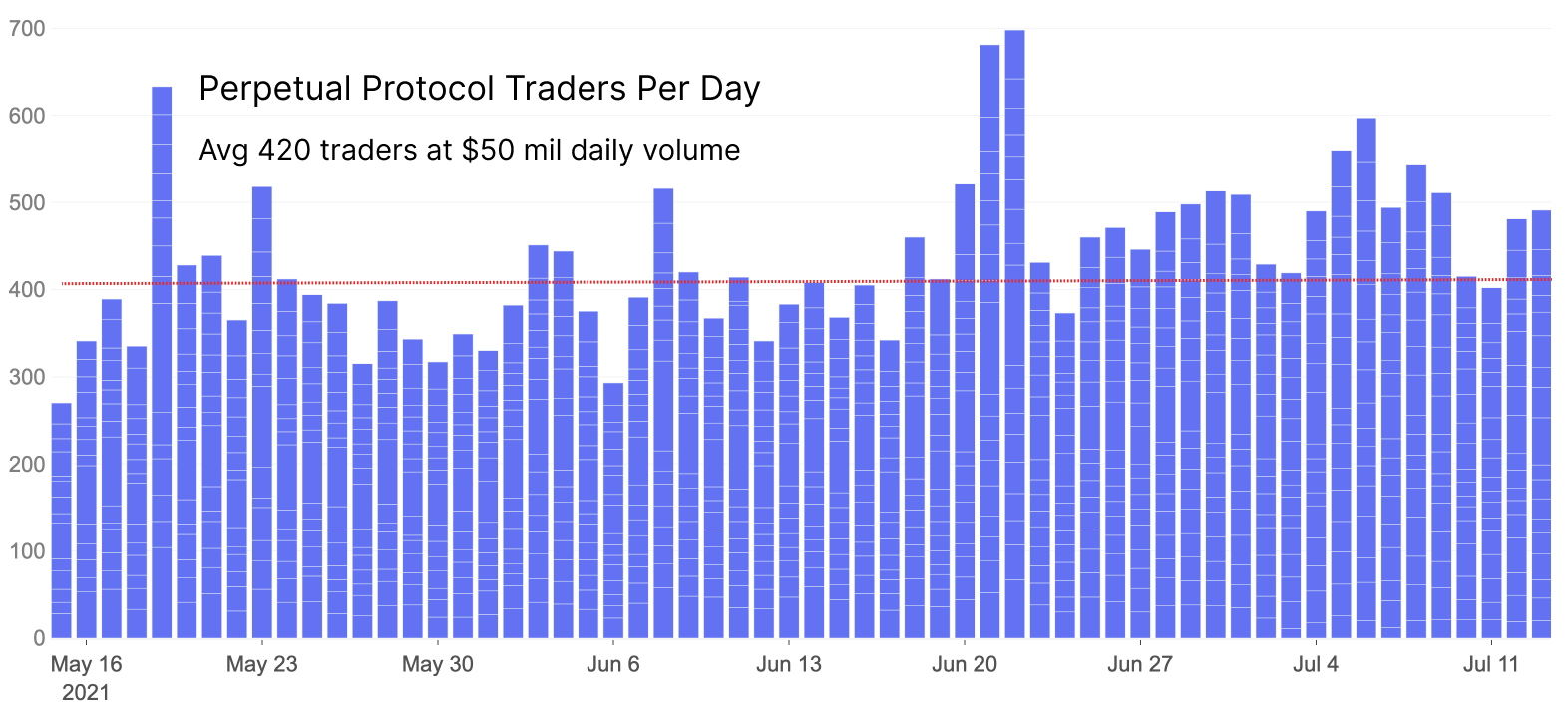

We mentioned that a decreasing user activity means decreasing returns for liquidity providers. Perpetual contracts have been one shining corner of DeFi derivatives with a growing pie over the last few months. Volumes on Perpetual Protocol and DyDx remain strong and growing month over month.

Token holders get a slice of both trading fees and liquidity mining rewards, currently yielding ~40% APY for Perpetual Protocol (PERP) stakers. This number is set to increase as fees for token holders go into play for the upcoming V2 of Perpetual Protocol.

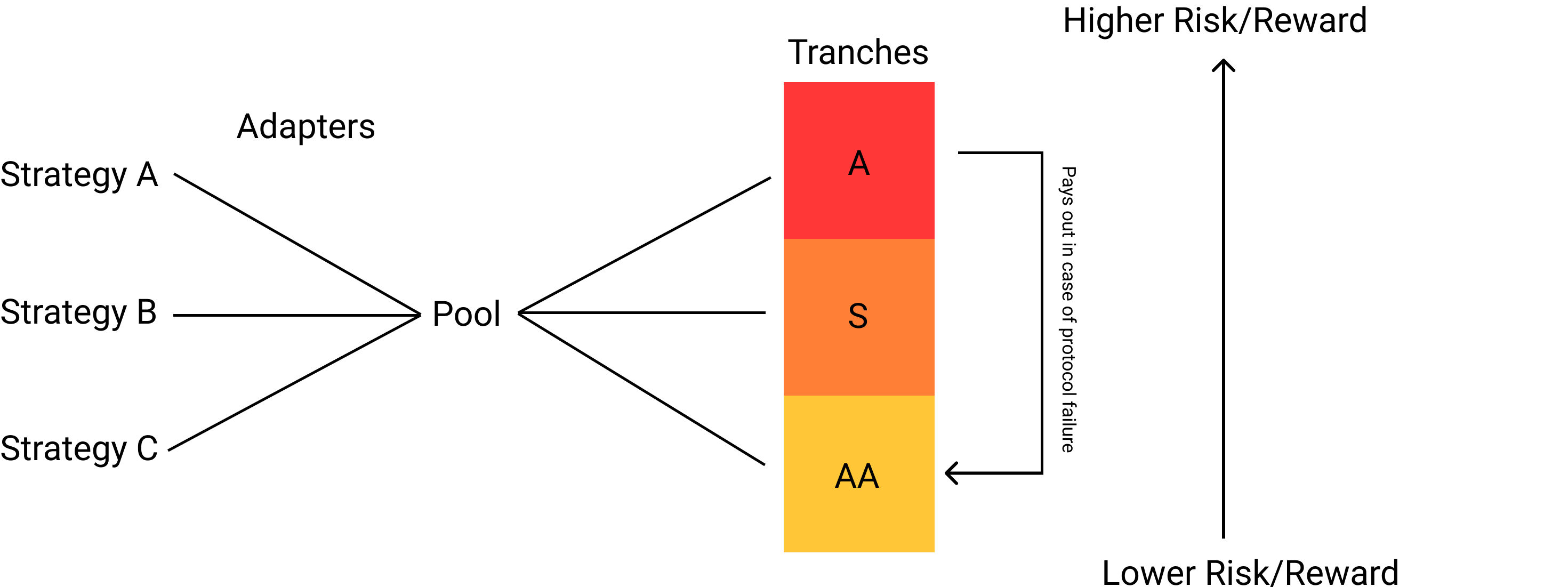

Tranches

Tranches are a relatively new primitive in DeFi, with only $100M TVL in DeFi's largest tranche product Barnbridge. Tranches are largely unknown products because of their relative complexity, however are a more familiar concept in legacy finance.

Tranches are an instrument that enables varied levels of risk exposure to the same underlying. In this way, investors can get exposure to a protocol, without needing to take on the full risk profile of the protocol. It enables participants to opt for varying levels of defined risk that may be attractive to the next wave of DeFi adoption.

The following visualization is what a traditional tranche setup might look like in a DeFi setup, with a series of strategies being divided into 3 tranches. AA is the most senior, and thus takes on the least risk, but at the lowest return.

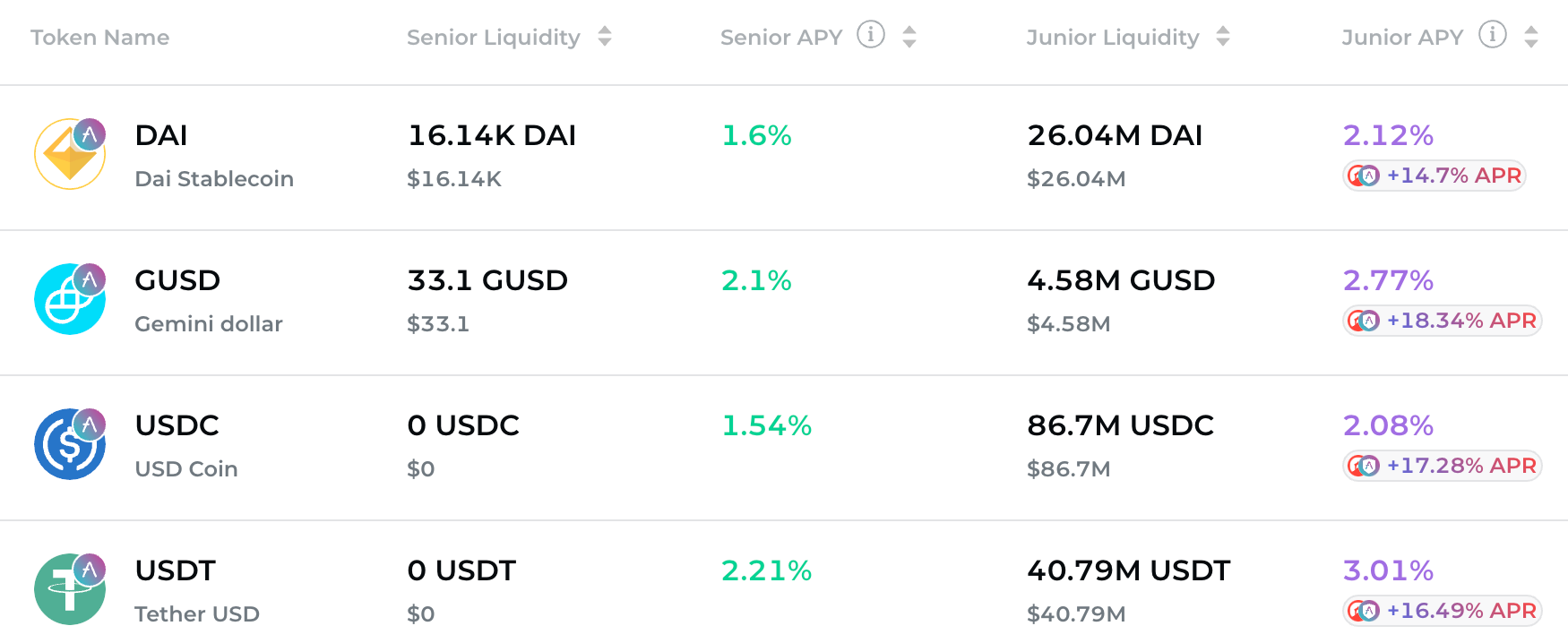

Barnbridge's tranches simplify this structure, having only two levels, offloading risk to the junior tranche, making the senior tranche yield less but take on less risk. Junior tranches in Barnbridge currently yield up to 20% APY after liquidity incentives from BOND, AAVE, and COMP.

Airdrops & Competitions

Many DeFi projects will airdrop tokens onto holders of certain tokens, participants in testnets, and other activities.

As an example, Thales, a binary options platform is set to launch soon and airdrop 35% of its governance token onto Synthetix stakers. This is one of many examples of airdrops that can be claimed.

In a similar vein, projects often hold competitions to incentivize early participants in their test networks. Cosmos recently held a trading competition on their new Gravity DEX, with a wide range of prizes for winners.

Currently, Lyra, a new options platform on Optimism is holding an options trading competition. This is a testnet competition so all positions and testing are completely free. Prizes include up to $30k+ in NFTs and tokens for the most profitable (play money) options traders over the next few weeks of trading.

Uncovering Alpha

This is our weekly segment that briefly discusses some of the most significant developments of the prior and upcoming week.

Big scaling news from across the space this week! Expect more and more announcements to be centered around product launches on L2.

- Uniswap V3 launches on Optimism. Long awaited, the Optimism launch of Uniswap V3 marks a new era for scaling as Optimism's marquee partnership finds its way to an alpha release, this soon after their launch on Arbitrum. It will be fascinating to see where they try to direct liquidity and volume. Also to see if/when liquidity fragments across V2, V3, L2, etc. Lots at stake here for the space's DEX darling by users/volume.

- Synthetix set to launch trading pairs on July 26th. July 26 marks the transition to Optimism for Synthetix. They will launch with 4 pairs as they work to transition liquidity over to L2.

- Ethereum's London update is slated for August 4th. General dev agreement has pointed to an August 4th release date after months of July as the planned date. This is the upgrade that will include EIP-1559, the hotly contested fee burn upgrade that looks to reduce ETH inflation.

- Sushi announces an NFT exchange. Sushi continues to experiment, offering product after product to try and bring value to token holders. This time they have announced an August launch for an NFT exchange.

- Harvest Finance launches V2. More of an aesthetic update, the V2 launch marked another milestone for this popular yield aggregator. New pairs were added, but overall it was more of a user-friendly refresh of the UX.

- Lyra launches an options trading competition. Lyra is built on top of Synthetix, one of a handful of Synthetix offshoots expected to launch within the next few months. This is a fun free competition for anyone to join. It runs through the 26th on Optimism's Kovan testnet. GLHF. This is one of many new products expected to first launch on L2. Options are notoriously expensive positions to put on within L1; the gas costs are high and limited liquidity makes pricing these options difficult.

- Follow us and reach out on Twitter

- Join our Telegram channel

- For on–chain metrics and activity graphs, visit Glassnode Studio

- For automated alerts on core on–chain metrics and activity on exchanges, visit our Glassnode Alerts Twitter

Disclaimer: This report does not provide any investment advice. All data is provided for information purposes only. No investment decision shall be based on the information provided here and you are solely responsible for your own investment decisions.

To keep up to date with the latest Glassnode analysis of the DeFi ecosystem, be sure to subscribe to this DeFi specific content series here.