Expanding Glassnode: Macro and Traditional Finance Data

Glassnode is expanding its data coverage to include macro and TradFi metrics, enabling users to contextualize digital asset markets within broader financial conditions.

Our guiding principle in developing Glassnode's product offering has always been about enabling a comprehensive view of digital asset markets. This has meant delivering industry-leading on-chain and derivatives analytics, while also helping investors interpret the broader forces shaping market behavior.

As digital assets mature, these forces increasingly extend beyond on-chain data. Today, we are further expanding our product to reflect this ongoing shift. Glassnode now integrates macroeconomic and traditional finance (TradFi) data, bringing everything you need to understand Bitcoin and digital assets into a single platform.

Why Macro Now Matters More Than Ever

Digital assets are no longer a niche experiment. They are a mainstream asset class, with growing participation from institutions, ETFs, and traditional finance players. The recent approval and rapid growth of Bitcoin ETFs – now exceeding $100 billion in assets under management as of early 2026 – is a clear signal of this shift.

But with this integration comes a new dynamic: Bitcoin’s price is increasingly influenced by traditional financial forces. Geopolitical risks, monetary policy, and broader macroeconomic trends now play a critical role in shaping Bitcoin’s trajectory. For investors, traders, and institutions, this makes access to a broader set of actionable data more important than ever.

That is why Glassnode is expanding its data coverage to include TradFi and macro metrics. The goal is not to move beyond on-chain analysis, but to extend it — enabling users to connect the dots between digital asset markets, traditional financial data and the global economy.

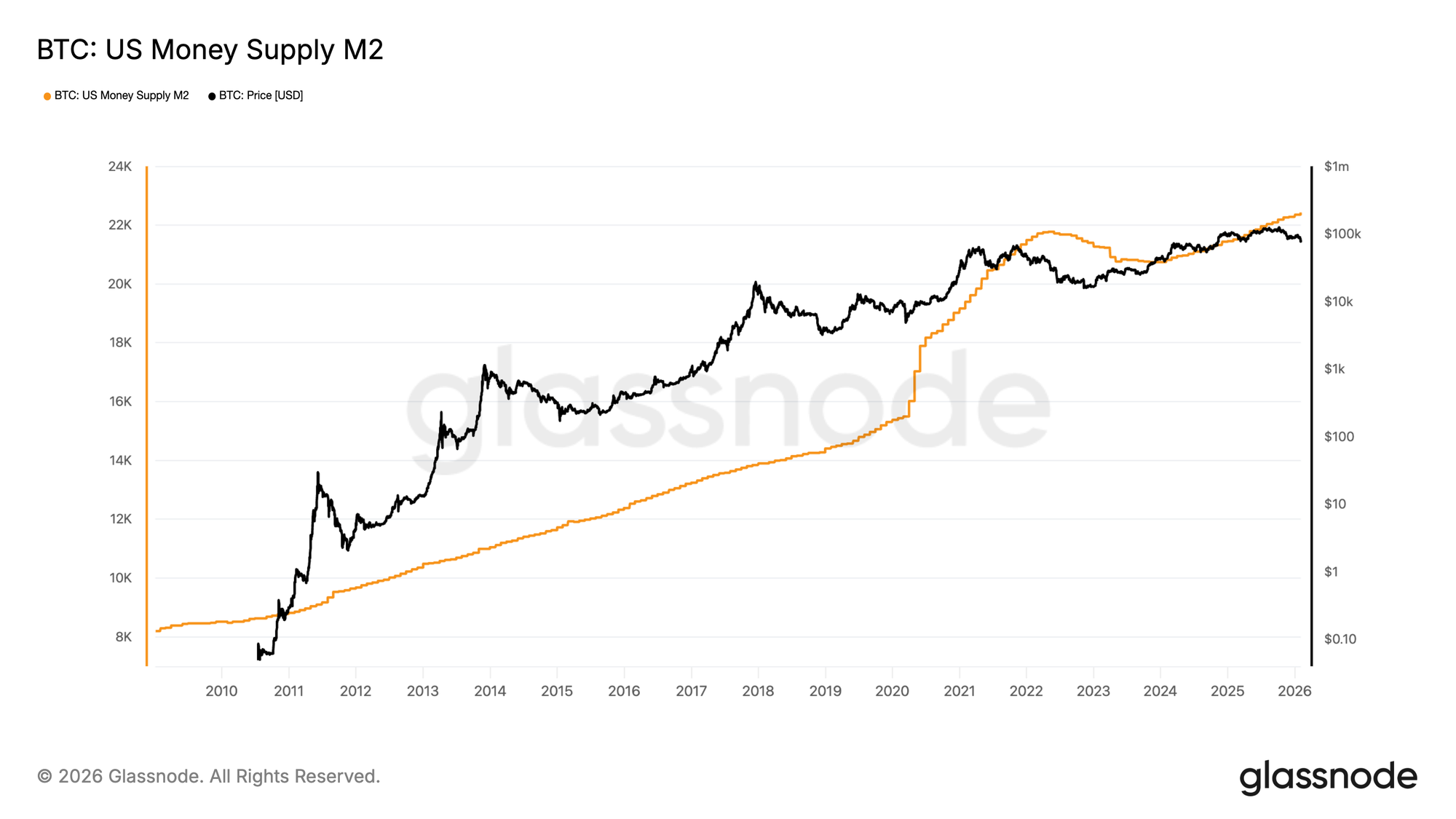

From Digital Gold to Liquidity-Sensitive Asset

Bitcoin was created in the immediate aftermath of the Global Financial Crisis in 2009, as a direct response to what its creator saw as a fundamental flaw of modern finance: the ability of central banks and governments to create money at will. Bitcoin's fixed supply of 21 million coins is not just a technical detail; it is a political statement.

This aspect becomes most relevant when central banks are most active. When central banks expand their balance sheets, money supply grows, financial conditions become more supportive, and investors generally have more capital available to allocate across risk assets. In that environment, Bitcoin has often benefited alongside other liquidity-sensitive assets.

By contrast, periods of monetary tightening tend to create a more difficult backdrop. Higher rates, shrinking central bank balance sheets, and weaker liquidity conditions typically reduce risk appetite and can weigh on digital asset markets.

This is why it is useful to monitor metrics such as:

- US Money Supply (M2)

- US Central Bank Balance Sheet

- Euro Area Money Supply (M2)

- Euro Area Central Bank Balance Sheet

They help place Bitcoin price action in the broader context of global liquidity cycles and provide a macro framework for interpreting market moves.

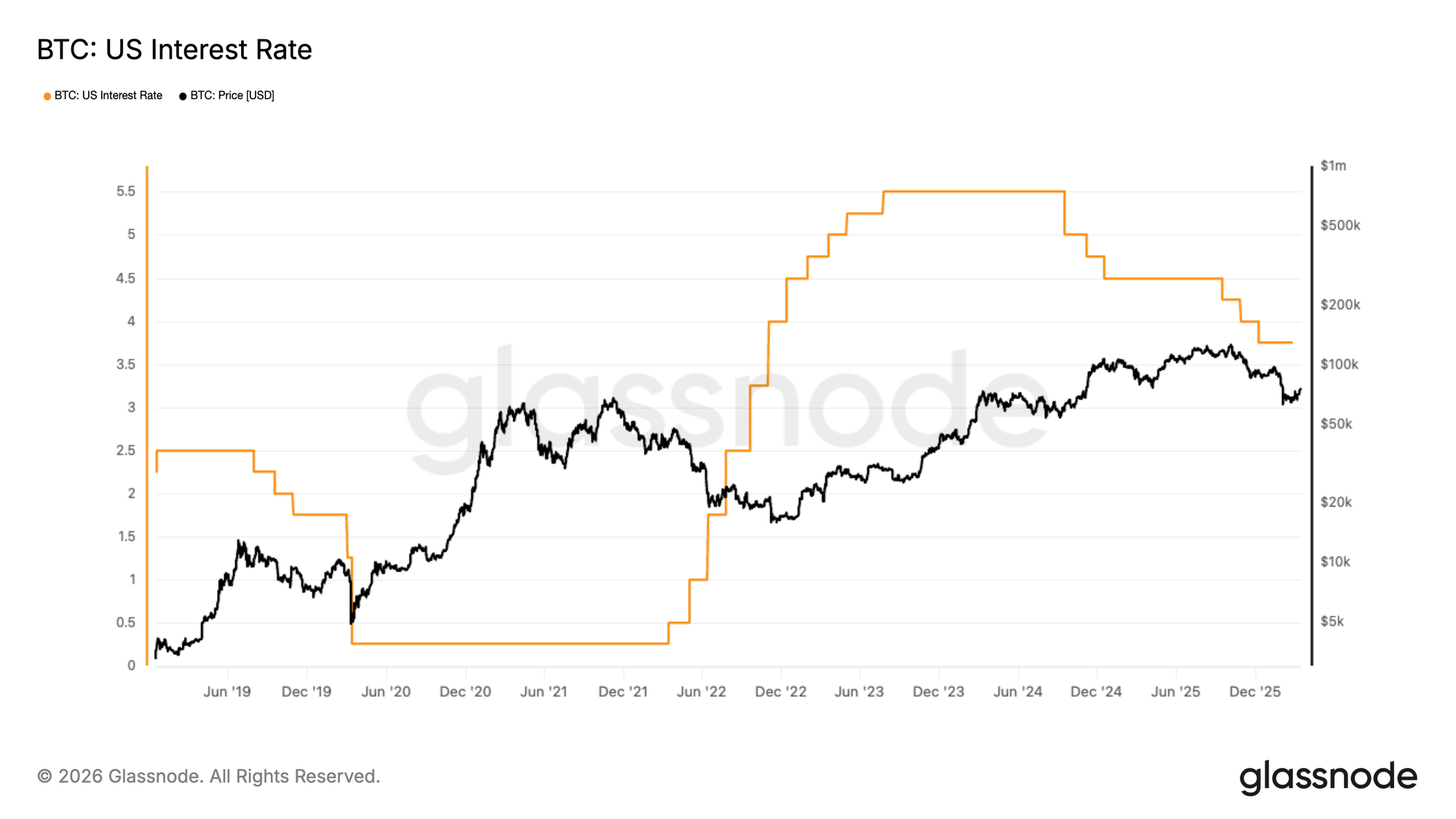

From Dovish to Hawkish: How Interest Rate Shifts Impact Bitcoin

Interest rates are another key transmission channel. Bitcoin does not generate cash flow, so the opportunity cost of holding it changes meaningfully with monetary policy. In tighter regimes, higher rates tend to support the dollar, raise real yields, and reduce appetite for speculative assets. In looser regimes, easier financial conditions can support broader risk-taking. This is why metrics such as US Interest Rate, Euro Area Interest Rate, US 10Y Yield, and Germany 10Y Yield are relevant to digital asset investors, not just bond traders.

As illustrated above, periods of low interest rates tend to support Bitcoin and other risk assets, as cheaper capital and looser financial conditions encourage risk-taking. Conversely, rising interest rates increase the cost of capital and typically reduce investor appetite for risk, creating a more challenging environment for Bitcoin price performance.

Traditional Finance Data in Digital Assets

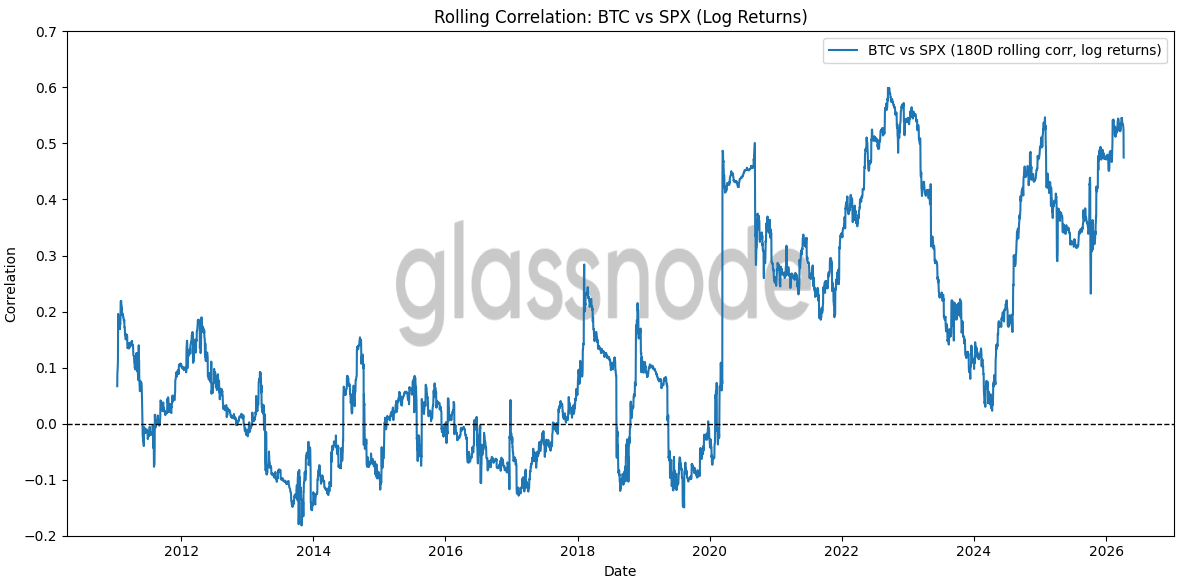

As digital asset markets mature, they are becoming increasingly connected to the same macro forces that move equities, bonds, FX, and commodities. Bitcoin now trades in an environment shaped by interest rates, liquidity conditions, dollar strength, inflation expectations, and risk sentiment.

As a result, understanding digital asset markets requires more than on-chain data alone. By adding TradFi metrics, Glassnode gives users the context needed to interpret market moves, identify regime shifts, and assess whether a move is digital asset-specific or part of a broader cross-asset trend.

The chart above plots the 180-day rolling correlation between Bitcoin and the S&P 500 using log returns. The main signal is that BTC appears to have become more sensitive to macro and broader risk-asset dynamics over time. In earlier years, the correlation hovered around zero or was occasionally negative, while in recent years it has often been meaningfully positive.

This does not appear to be a temporary dislocation, but a structural shift, driven by three forces:

- the entry of institutional capital that allocates across asset classes;

- the post-COVID liquidity cycle, which inflated and then deflated risk assets simultaneously;

- and the launch of spot Bitcoin ETFs, which embed BTC more directly into traditional portfolio flows.

This supports the view that Bitcoin is no longer solely a standalone, crypto-native asset; it now trades alongside broader liquidity and risk conditions more frequently than in the past.

Using TradFi Metrics to Contextualize Digital Asset Markets

Glassnode's TradFi market metrics suite helps users understand the external forces that increasingly influence digital asset markets.

▷ Rate and yield curve indicators provide insight into monetary policy, growth expectations, and recession risk. Relevant metrics: The US 10Y-2Y Spread, Germany 10Y-2Y Spread, US 2Y Yield, US 10Y Yield, Germany 2Y Yield, and Germany 10Y Yield.

▷ Equity benchmarks help gauge global risk appetite and market stress. Relevant metrics: The US 500 Stock Market Index and EU50 Stock Market Index, along with the US Fear Index and EU Fear Index

▷ FX measures provide context on dollar strength and liquidity conditions, both of which can materially affect digital asset performance. Relevant metrics: EUR/USD and the U.S. Dollar Index

▷ Commodity prices, including Gold, Silver, and WTI Crude Oil, add another layer by reflecting inflation expectations, safe-haven demand, and geopolitical risk.

One Platform, Full Market Context

The broader point is that digital asset markets are maturing. The arrival of spot ETFs, growing institutional participation, and stronger links to policy and geopolitics mean that digital assets increasingly sit within the same information ecosystem as equities, bonds, FX, and commodities. Glassnode’s Macro and TradFi metric categories are built for this environment.

Glassnode remains the home for deep digital asset-native intelligence. At the same time, delivering a comprehensive analytical view of the markets now requires tools to analyze the macro and traditional financial forces that shape them.

Explore the new Macro and TradFi metrics in Glassnode Studio or compare pricing plans to gain access.

- Follow us on X for timely market updates and analysis

- Join our Telegram channel for regular market insights

- For on-chain metrics, dashboards, and alerts, visit Glassnode Studio

Disclaimer: This report is for informational and educational purposes only. The analysis represents a limited case study with significant constraints and should not be interpreted as investment advice or definitive trading signals. Past performance patterns do not guarantee future results. Always conduct thorough due diligence and consider multiple factors before making investment decisions.