Sushi vs. Unicorn: The Rise (And Fall?) of Uniswap

Uniswap has long been one of Ethereum's favorite projects. But the emergence of SushiSwap may be threatening its very existence.

Uniswap is in the battle of its life against a new competitor: SushiSwap. But is this a case of fair game, healthy competition, or daylight robbery?

What is Uniswap? 🦄

In short, Uniswap is a decentralized exchange (DEX) on Ethereum. More specifically, it is an automatic market maker for liquidity provision, allowing anyone to provide liquidity and/or make trades ("swaps") between tokens on Ethereum.

It is also the world's largest DEX by volume.

Uniswap was founded by Hayden Adams in 2017, after he was laid off from his job as a mechanical engineer. Inspired by Vitalik Buterin's ideas on automatic market makers, he learned to code and started building a decentralized liquidity market. The project officially launched on 2 November 2018 at Devcon 4 in Prague. It has subsequently received a $100k grant from the Ethereum Foundation, followed by over $11 million in VC funding from the likes of Paradigm and Andreessen Horowitz.

But, thanks to the very principles it claims to hold dear - decentralization - its very existence is under threat.

Uniswap: The Rise 🌈

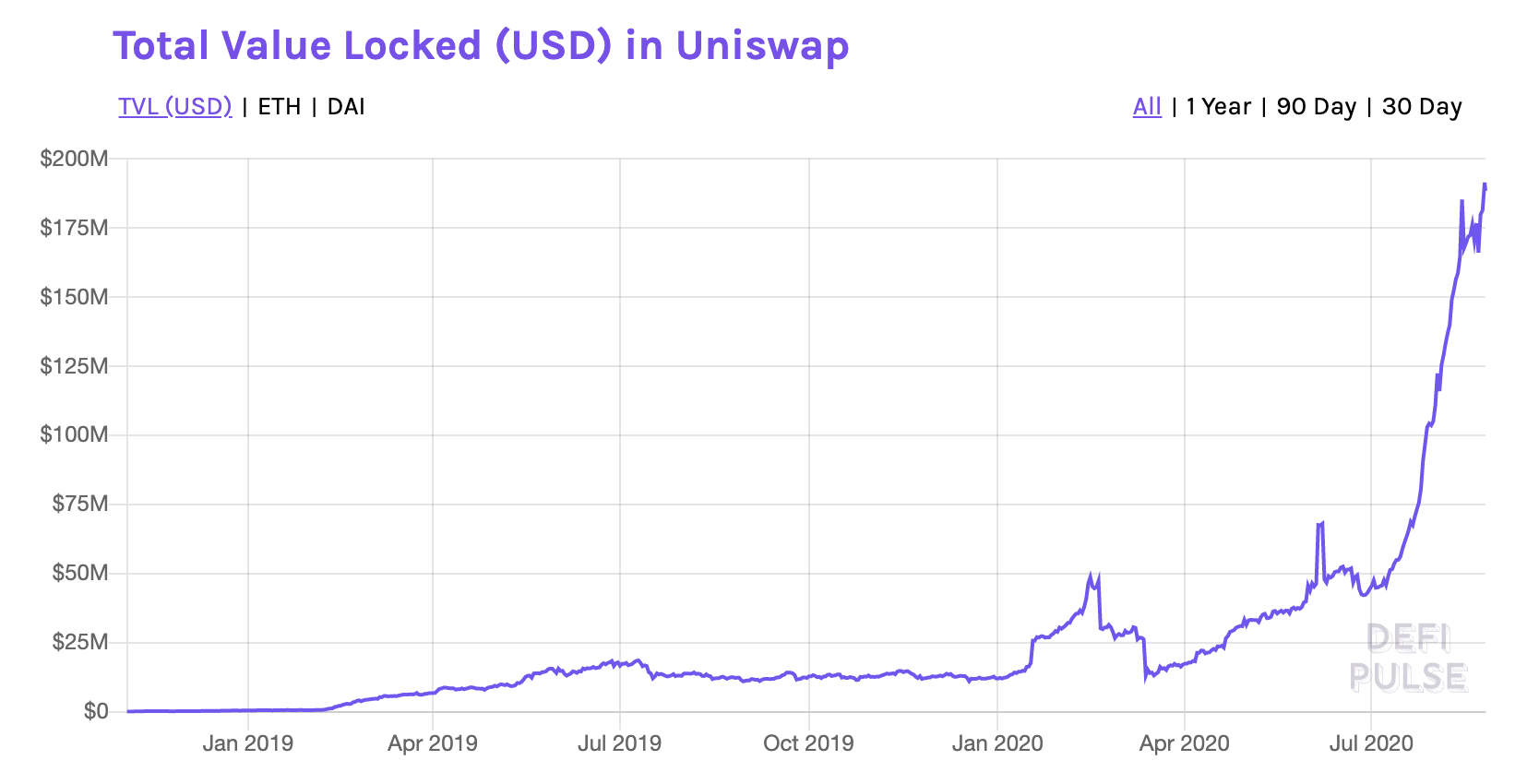

After growing slowly but steadily for the first year of its existence, Uniswap started seeing much more rapid growth in 2020. Then, in July, its growth rate took off, taking total capital locked up in Uniswap from $50 million to over $150 million by mid-August.

By late August - before SushiSwap emerged - Uniswap had $200 million in liquidity locked in its smart contracts.

So before we look at the post-SushiSwap figures - how did a small project with a tiny team grow from obscurity into the world's largest decentralized exchange with millions of dollars in funding?

If you're already familiar with Uniswap's history, skip to where SushiSwap comes in. Otherwise, let's look at some factor's of Uniswap's success:

- Decentralization - Uniswap's guiding principle is that it is decentralized, and its contracts are open source. Users can interact trustlessly with the platform without the risks or identity checks of centralized exchanges.

- Great smart contracts - Throughout Uniswap's existence, it has never experienced a hack or major bug, leading to trust in the protocol that keeps people using and recommending it.

- Support for all ERC-20 tokens - Anyone can create a market for a token on Uniswap simply by providing liquidity. There are no centralized approval processes or waiting times, drawing in supporters from many smaller token communities.

Building on these strong foundations, in May 2020, Uniswap V2 was launched. This coincided with the beginning of the recent DeFi boom, which helped with Uniswap's further growth, along with its new features:

- Direct token swaps - While Uniswap V1 only enabled swaps between ERC-20 tokens via ETH (a process called "ETH bridging"), V2 supports direct ERC-20 to ERC-20 swaps, essentially halving gas fees.

- Lower gas fees - When rewriting the contracts, Uniswap switched from Vyper to Solidity, optimizing contract execution and thereby reducing gas fees even further.

- Greater token support - V2 added support for non-standard ERC-20 tokens such as USDT and BNB, opening up more potential liquidity pools for popular tokens.

- Flash swaps - Similar to flash loans, this functionality allows users to "borrow" tokens from a Uniswap pool, perform some transaction with external services, and then pay back the borrowed tokens to the pool - all in a single transaction. This has increased arbitrage opportunities and led to wider adoption.

- Extensive auditing - Uniswap retained its excellent reputation by extensively testing its V2 contracts and having them audited, including an audit by ConsenSys Diligence. It also has a bug bounty program, but so far, no exploits have been found, adding to confidence in the platform.

Uniswap managed to beat out much larger and more well-funded competitors (such as Bancor and 0x) by creating an image of a lean, quickly-evolving, user-friendly platform that stayed true to the Ethereum community's core principle of decentralization.

As of barely a week ago, Uniswap seemed unstoppable. Its market share far outstripped that of any of its competitors, and its standing within the community was generally positive.

But not everyone was happy.

Uniswap: The Peak 📈

Despite all the hype around Uniswap and the added features introduced in V2, there was some discontent in the community. Some members were growing skeptical of the lack of decentralization in Uniswap's governance, and of the involvement of venture capitalists in what is supposed to be a platform build by the community, for the community.

At the same time, while its end users generally report a positive user experience, the platform's lifeblood - liquidity providers (LPs) - have not been as highly rewarded as many of them would have liked.

Refresher: When someone provides liquidity to a pool (for example, ETH/DAI) on Uniswap, they receive LP tokens which represent their stake in that pool. Uniswap takes a 0.3% fee on each trade, which is proportionally distributed among that pool's LP token holders (i.e. active liquidity providers).

With the rise of highly-profitable yield farming protocols, people are expecting higher returns on staked funds, and Uniswap is struggling to compete for liquidity while there are more lucrative opportunities elsewhere.

Enter: SushiSwap 🍣

Amidst these concerns, SushiSwap appeared seemingly out of the blue, spearheaded by a figure going by the name of Chef Nomi and sporting the eponymous Hearthstone character's image as their avatar.

1/ Introducing #SushiSwap🍣, an evolution of #Uniswap with $SUSHI tokenomics. SushiSwap protocol better aligns incentives for network participants by introducing revenue-sharing & network effects to the existing AMM model.https://t.co/Ywe9Gs8Pjx

— Chef Nomi #SushiSwap (@NomiChef) August 26, 2020

Put simply, SushiSwap is a fork of Uniswap. It is also stroke of genius, taking advantage of a few key elements of the zeitgeist to break into mainstream success.

Liquidity Mine Token Launch

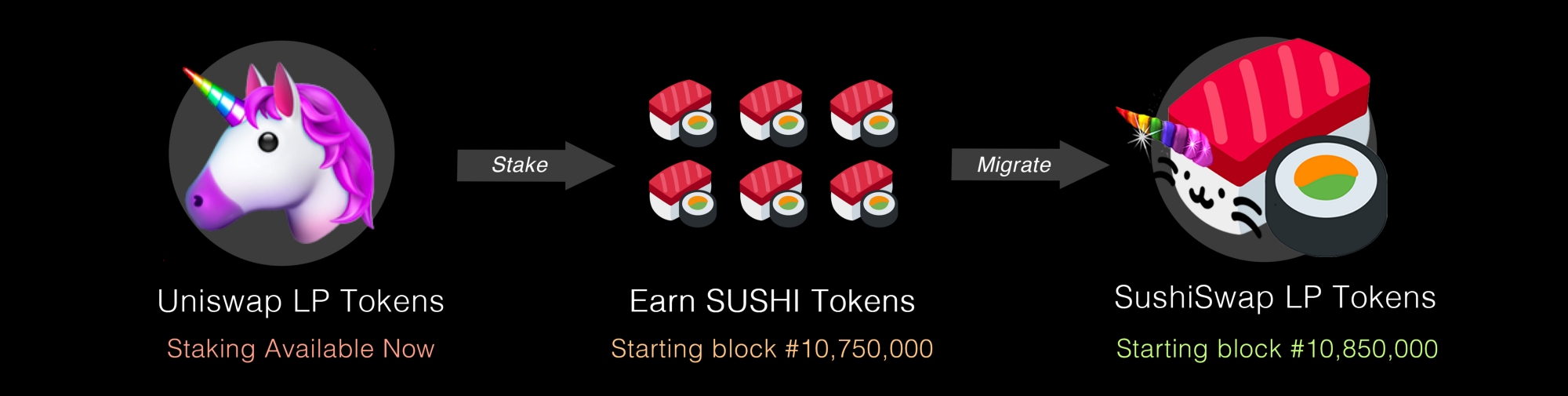

SushiSwap is riding the current hype wave of liquidity mining by launching the SUSHI token, helping the platform to gain more attention and poach liquidity providers. Anyone can mine SUSHI by staking Uniswap LP tokens on SushiSwap. For the first 2 weeks, 1000 SUSHI tokens will be minted each block and divided among stakers.

Not only does the liquidity mine help with marketing and bootstrapping adoption, but the SUSHI token also aims to solve Uniswap's decentralization problem by allowing liquidity providers to govern the platform themselves. In addition to this, in the spirit of decentralization, the platform has adopted the trending "fair launch" distribution approach; no VC allocation, a small (10%) development fund allocation, and an open pre-mine that rewards early community members.

Incentives for LPs

SushiSwap claims that under its model, LPs (especially smaller and earlier ones) get a better deal than under Uniswap's model. As outlined in the platform's launch announcement post:

With Uniswap, liquidity providers only earn the pool’s trading fees when they are actively providing said liquidity. Once they have withdrawn their portion of the pool, they no longer receive that passive income...

With SushiSwap, one can also provide some liquidity into a pool and earn rewards in the form of SUSHI tokens. However, unlike Uniswap, those SUSHI tokens will also entitle you to continue to earn a portion of the protocol’s fee, accumulated in SUSHI, even if you decide to no longer participate in the liquidity provision. As an early adopter to help provider liquidity, you become a significant stakeholder of the protocol.

As elaborated upon in its initial Twitter post:

3/ With SushiSwap, 0.25% goes directly to the LP, and another 0.05% goes to $SUSHI token holders. Because $SUSHI tokens can only be minted by supplying liquidity to #SushiSwap🍣 pools, each LP gets roughly the same 0.3% fees in the long run with better-aligned incentives.

— 🍣 SushiSwap | sushiswap.eth (@SushiSwap) August 26, 2020

As an additional incentive to actively provide liquidity, 100 SUSHI tokens will be minted each block and divided proportionally among all SushiSwap LP token holders. As such, unless LPs continue to provide liquidity, their SUSHI holdings (and corresponding reward earnings) will be gradually diluted.

But in reality, these changes won't make a huge difference in the returns LPs can expect to make. For Uniswap, the nail in the coffin doesn't come from being outcompeted by a protocol fork with better LP incentives, a native token, or effective marketing. Ultimately, it comes down to one simple factor:

SushiSwap is going to steal all of Uniswap's liquidity.

Uniswap: The Fall? 📉

The above statement might seem alarmist - and SushiSwap certainly denies that this is the project's intention - but regardless of intent, it is a very real possibility.

Uniswap must have felt safe in the notion that it was by far the largest and most popular DEX. The team probably never took the threat of a fork seriously, because despite their code being open source, their liquidity was, in a sense, proprietary - restricted to their own smart contracts.

Secure in their position, the team failed to innovate. They allegedly delayed the implementation of decentralized protocol ownership - which V2 technically has the capability to do - in order to focus on building their brand and implementing features that users didn't really care about or even actively disliked.

#Uniswap token lists are the worst kind of handholding, the kind that gets in the way of people who know what they're doing. Not a fan. #DeFi

— Gam (@gammichan) August 30, 2020

After all, surely they could rely on the network effect generated by the huge amounts of liquidity locked up inside their liquidity pools - couldn't they?

But the liquidity mining craze highlighted a vulnerability in Uniswap's liquidity pooling model which doesn't exist under orderbook models: liquidity is only as sticky as the LP tokens which represent it. Gain control of the Uniswap LP tokens, and you gain control of all of Uniswap's liquidity.

And that's exactly what SushiSwap has done. By making its SUSHI liquidity mine contingent on staking Uniswap LP tokens, it has gained control of a staggering proportion of Uniswap's liquidity.

The Numbers: How Bad Could it Be?

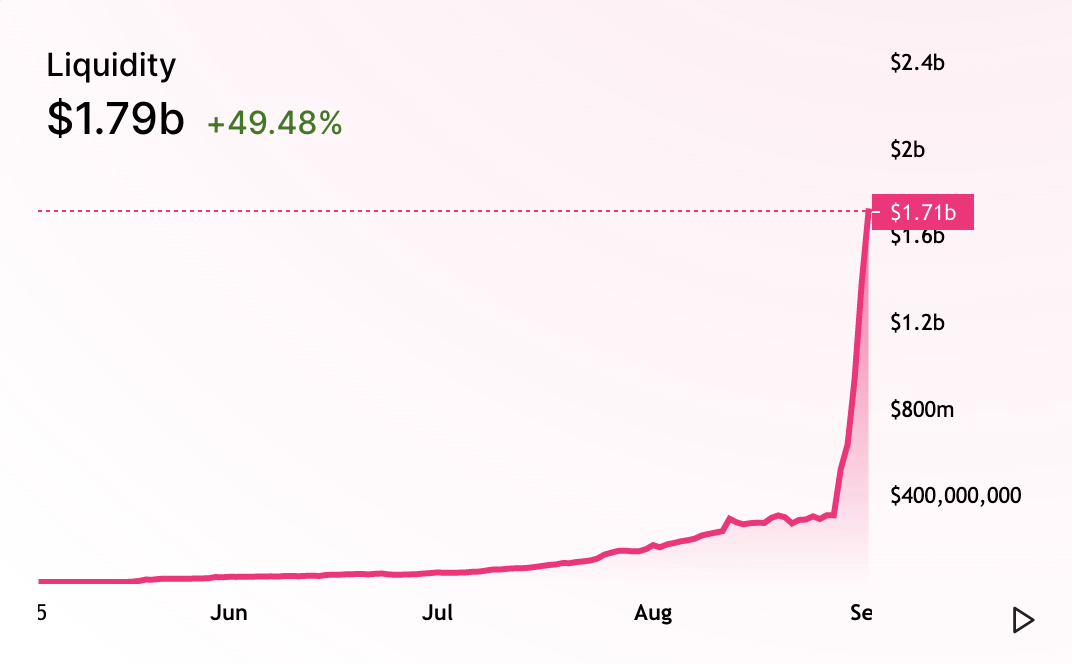

Since the SushiSwap liquidity mining phase launched, total liquidity on Uniswap has skyrocketed from $300 million to $1.8 billion, and is still climbing as opportunists scramble to accrue LP tokens and stake them on SushiSwap.

Of the liquidity now locked in Uniswap contracts, 71% is currently staked on SushiSwap in the form of LP tokens, generating SUSHI for their owners.

In less than 2 weeks, when we reach block 10,850,000, SushiSwap will use these staked LP tokens to withdraw liquidity from Uniswap and port it over to their own smart contracts.

In other words, if liquidity providers do not withdraw their LP tokens from the SushiSwap contract before the migration takes place, 71% of all liquidity on Uniswap will be migrated to SushiSwap in a matter of seconds.

Uniswap will be bled dry in an instant... Or will it?

The Future 🔮

In reality, Uniswap will almost certainly not be stripped of all its liquidity. Based on the current figures, it would still be left with over $500 million of liquidity - twice as much as it had before this all started a few days ago.

On top of this, the past week's massive increase in liquidity providers will likely correct itself once the SUSHI liquidity mine phase is over. Many new LPs who only provided liquidity in order to farm SUSHI will likely choose to withdraw their liquidity from SushiSwap, seeking out the next big yield farming opportunity.

Of course, many will stay, keen to farm SUSHI even at 10% of the previous rate. SushiSwap will still be left with a lot of liquidity, and may even succeed in capturing more volume than Uniswap once they launch trading capabilities after the liquidity migration.

But Uniswap still has widespread brand recognition, an intuitive (for crypto) user interface, and integrations with plenty of third-party apps. It will almost certainly have enough liquidity and volume to compete against SushiSwap, and the disparity between both platforms' APYs will be arbitraged by liquidity providers until they reach an approximately even footing.

Uniswap will live on. And as long as nothing goes wrong with SushiSwap's migration contracts, it will likely live on too, giving Uniswap some healthy competition and an incentive to innovate.

The Wild Card 🃏

One remaining wild card is the SUSHI token. It has traded for as high as $14 a piece, a price which would give it a $4.5 billion market cap based on the projected supply after a year. This market cap does not seem crazy among the token valuations of the day - and a $4.5 billion valuation for an exchange that does volumes in the hundreds of millions a day doesn't seem so outrageous.

But the token economics of SUSHI are as yet untested and barely examined.

- Does its incentive model hold up to scrutiny?

- Can its unit price withstand an inflation rate of 650,000 SUSHI per day?

- Will the value accruing to SUSHI holders be enough to justify its valuation, and if so, at what price?

- How much value should potential investors place on the token's governance functionality?

Read our SUSHI token valuation analysis to learn more:

Liesl Eichholz

Liesl Eichholz

- Follow us and reach out on Twitter

- Join our Telegram channel

- For on–chain metrics and activity graphs, visit Glassnode Studio

- For automated alerts on core on–chain metrics and activity on exchanges, visit our Glassnode Alerts Twitter