The Week On-chain (Week 37, 2021)

We assess the market response of Bitcoin traders and investors following a week of volatility lead by derivatives markets.

The Bitcoin market experienced a high volatility sell-off early in the week, with prices initially breaking up to a new local high of $52,849, before selling down to a low of $44,196. What appeared to be the main driver on the sell-side, was a flushing out of excessive leverage in futures markets.

Meanwhile, in spot and on-chain markets, the historically significant trend of investor accumulation and long term holding remains well and truly intact. Despite a 50%+ sell-off experienced in May, a strong rally from the $29k lows, and now another sharp sell-off this week, HODLers appear unphased.

This week, we will explore both the leverage flush that initiated the price mark down, and deep dive into the observable dynamics in the on-chain Bitcoin supply.

Derivatives Lead Downside Volatility

In last weeks newsletter and video report, we covered how the growth in futures contracts open interest, and increasingly positive perpetual swap funding rates in Bitcoin and Ethereum markets.

This highlighted a growing risk that excess leverage, with a long directional bias, could create a downside price squeeze. On Tuesday, both markets indeed saw a significant sell-off, with Bitcoin trading down more than $10k in one hour. This event acted to clear out much of the accumulated leverage, with the market consolidating for the rest of the week.

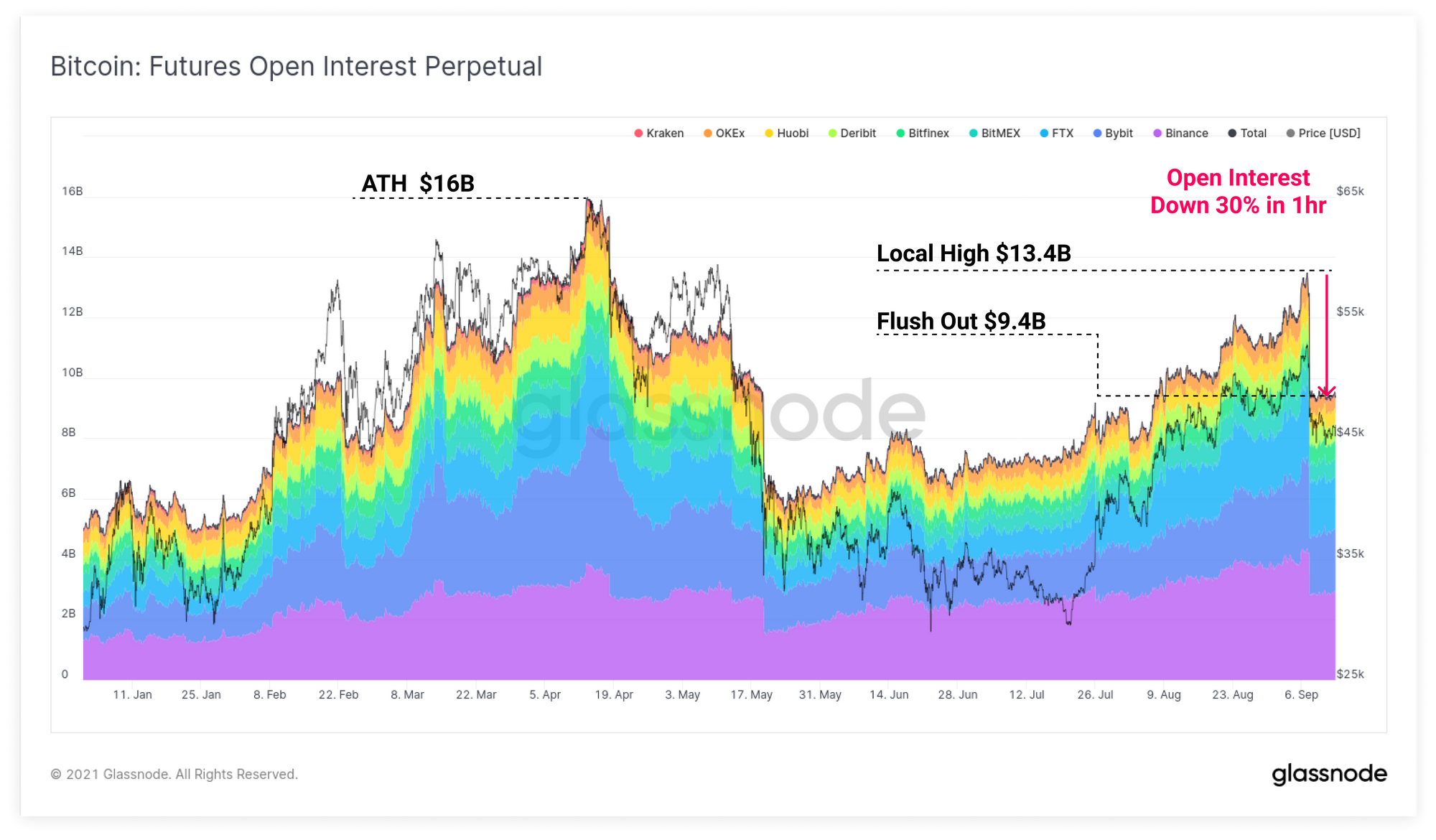

From the local high of $13.4B in open perpetual futures interest, a total of $4B worth of contracts (30%) were closed out and cleared within the hour. Leverage has remained fairly steady at around $9.4B for the remainder of the week.

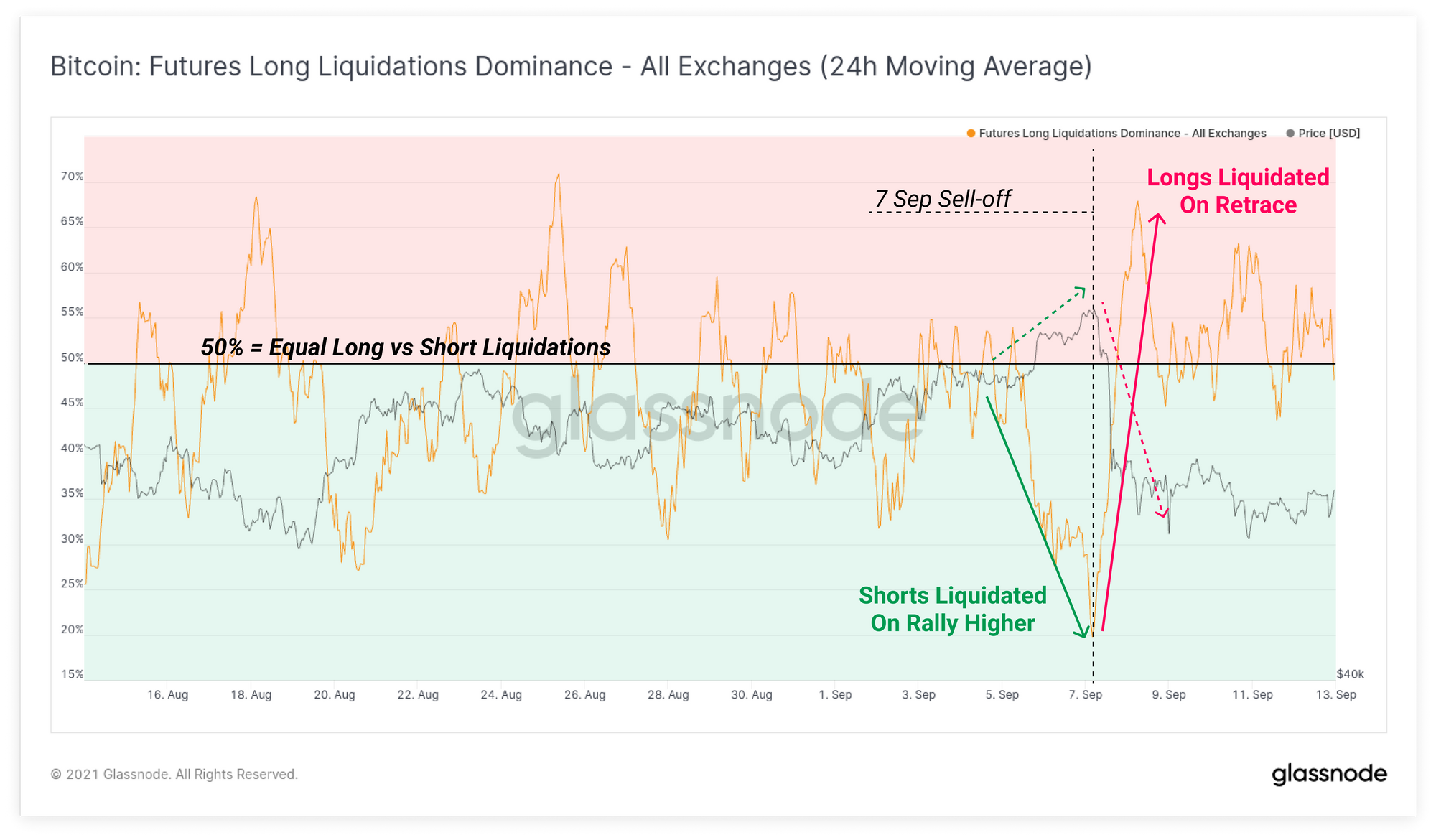

Using the Long Liquidation Dominance metric, we can see that just prior to this sell-off, futures markets actually experienced a brief short liquidation squeeze, that aided in pushing prices up to the local high of $52.8k. Short liquidations represented 80% of all liquidations during this time.

Immediately following this peak, the opposite occurred, with the proportion of long contract liquidations spiking to 68%, as BTC prices fell over $10k from the highs.

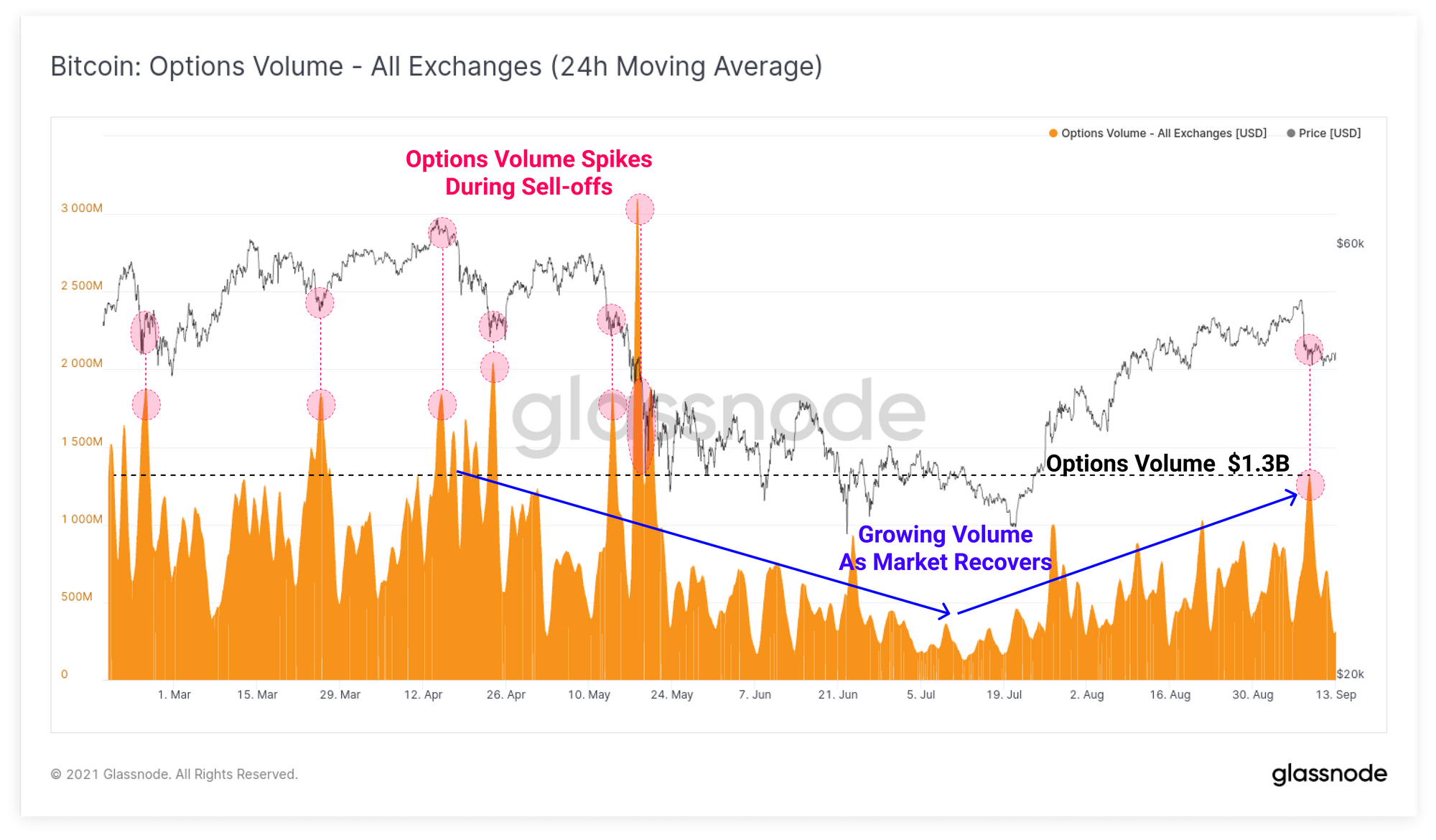

Options markets also saw a spike in volume, as traders rushed to hedge their positions, and capture volatility premium. This has become fairly typical behaviour this year where options markets consistently see elevated activity during market sell-offs.

The total volume traded in options markets has been in recovery mode since a relative lull in activity through May to July. During the hours around Tuesday's sell-off, traded option volumes reached a multi-month high of $1.3B.

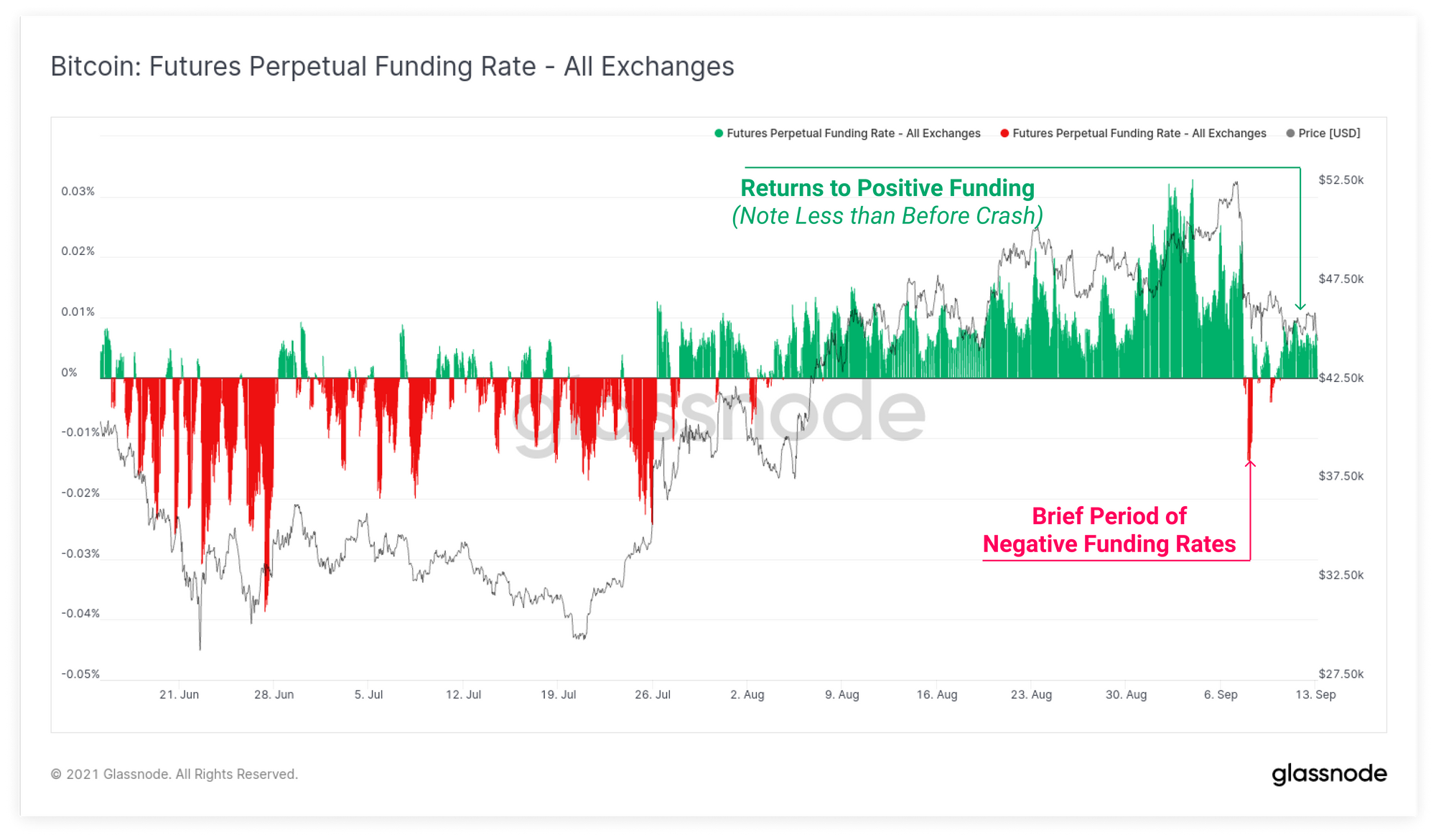

After a very brief period of negative funding rates during the sell-off, perpetual markets have returned to slightly positive funding rate suggesting that traders are still expecting upside price momentum. Note however that the magnitude of funding is much lower than it was prior to the crash, suggesting that at least a partial deleveraging has occurred.

Week On-chain Dashboard

The Week On-chain Newsletter now has a live dashboard for all featured charts here. We have also started production for