New Year Opens Sideways

Bitcoin has opened the new year quietly, with lacklustre demand for blockspace, despite bullish undertones in macro supply dynamics.

The Week Onchain Newsletter (Week 1, 2022)

Happy New Year to all of our readers, the Glassnode Team hopes you had a safe and happy break over the holiday season. Also, Happy Birthday to Bitcoin. Thirteen years ago, Satoshi Nakamoto mined the first Bitcoin block, with the following message encoded into the coinbase transaction as a timestamp:

The Times 03/Jan/2009 Chancellor on brink of second bailout for banks

As 2021 wound down, so too did activity in the Bitcoin market, with trading volumes softening, and prices trading more or less sideways. Price has continued to trade in the same range since late November, bouncing between a high of $51,654, and a low of $46,197 this week.

Across many on-chain metrics, there is a general lack of activity, despite a modestly bullish undertone in supply dynamics. Coins continue to migrate to increasingly illiquid, and dormant wallets, whilst investor profitability and cyclical metrics paint a more bearish picture. With a balance of both bull and bear signals at hand, our expectations into the start of 2022 are likely continued sideways consolidation.

The Week Onchain Dashboard

The Week Onchain Newsletter has a live dashboard with all featured charts available here. This dashboard and all covered metrics are explored further in our Video Report which is released on Tuesdays each week. Visit and subscribe to our Youtube Channel, and visit our Video Portal for more video content and metric tutorials.

Onchain Activity Remains Lacklustre

The first suite of metrics we will asses in this newsletter are associated with activity occurring onchain. Generally speaking, bullish momentum is usually accompanied by increased demand for blockspace, as coins are purchased, sold, and transferred to new owners. Conversely, bearish trends typically see fewer new wallets, reduced transaction demand, and lower network utilisation.

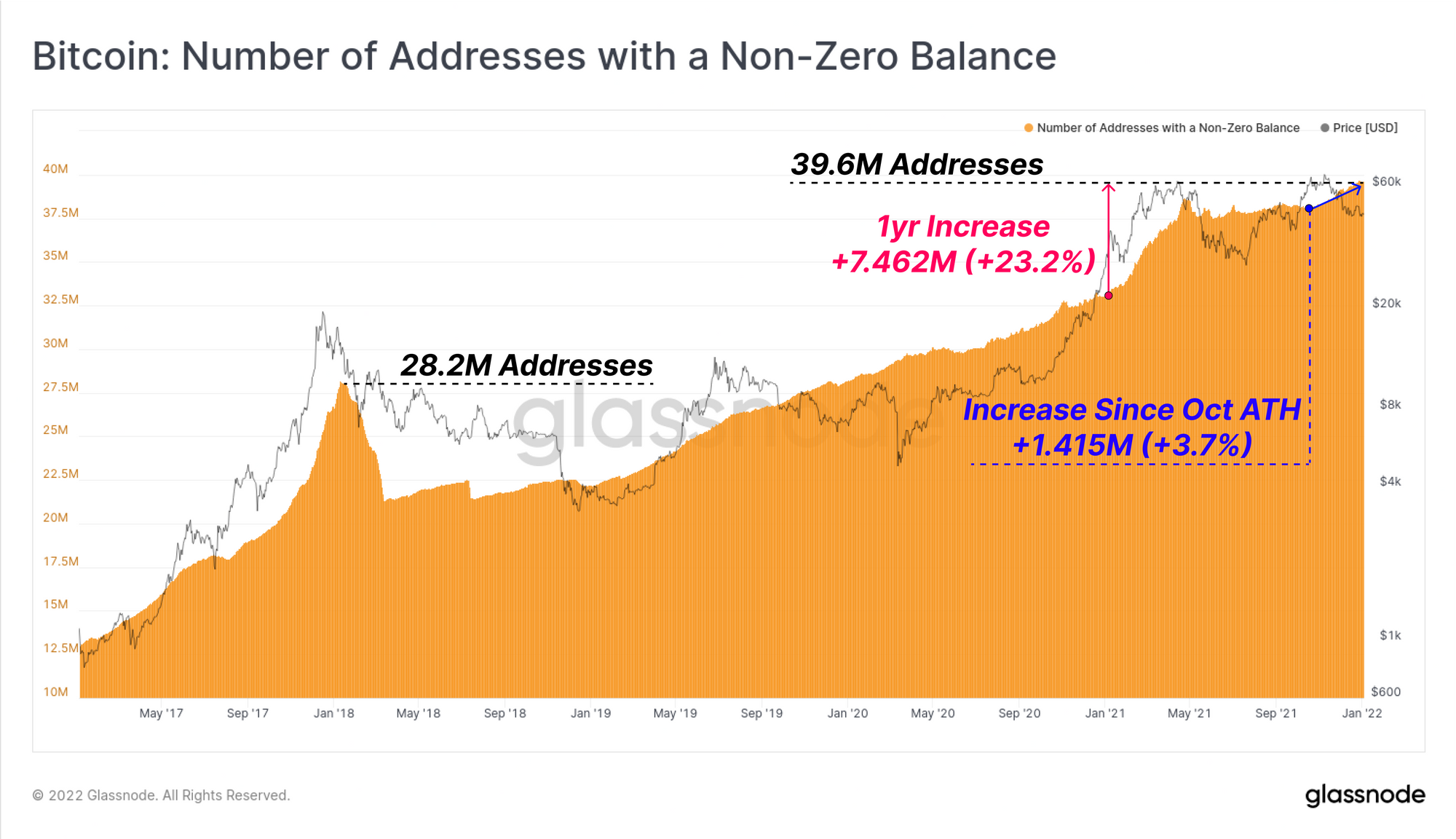

The number of wallet addresses with a non-zero balance is a metric that can be used to assess the longer-term demand for Bitcoin. Over the last year, a net total of 7.462M non-zero balance wallets have been added to the network a 23.2% YoY growth. 1.415M of these were added since the October ATH, 18.9% of the yearly total.

The current ATH of 39.6M of non-zero addresses is 40% higher than the peak set at the end of the 2017 bull market, indicating that user-base growth has been sustained over the last five years.

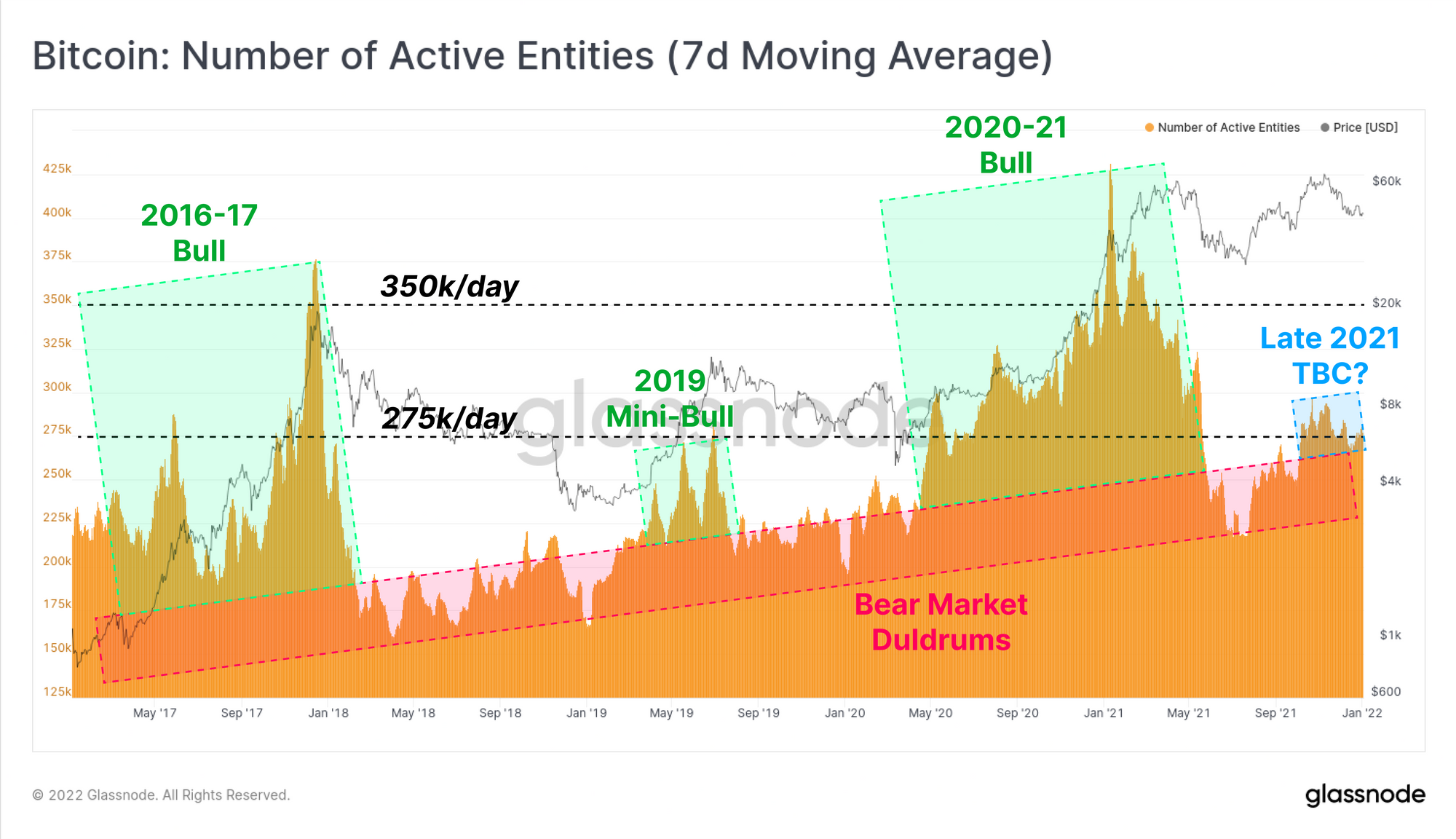

With respect to daily activity, we can see that the number of active onchain entities has finally managed to break above 275k/day. The chart below highlights in red an observable and rising 'bear market channel'. This shows that during periods of depressed prices, and lower relative interest, there remains a persistent growth in network users.

Both 2017 and 2020-21 bull markets stand out as having markedly more onchain activity relative to this channel. However, the current regime appears to more closely resemble the 'mini-bull' that occurred from April to August 2019. These two periods are similar in that they followed a deep correction and broad capitulation event, but the subsequent rallies could not generate sufficient momentum for a full scale bull market.

The rally in 2019 eventually culminated into a nine month long sideways-to-down trading range, until the final capitulation occurred in March 2020.

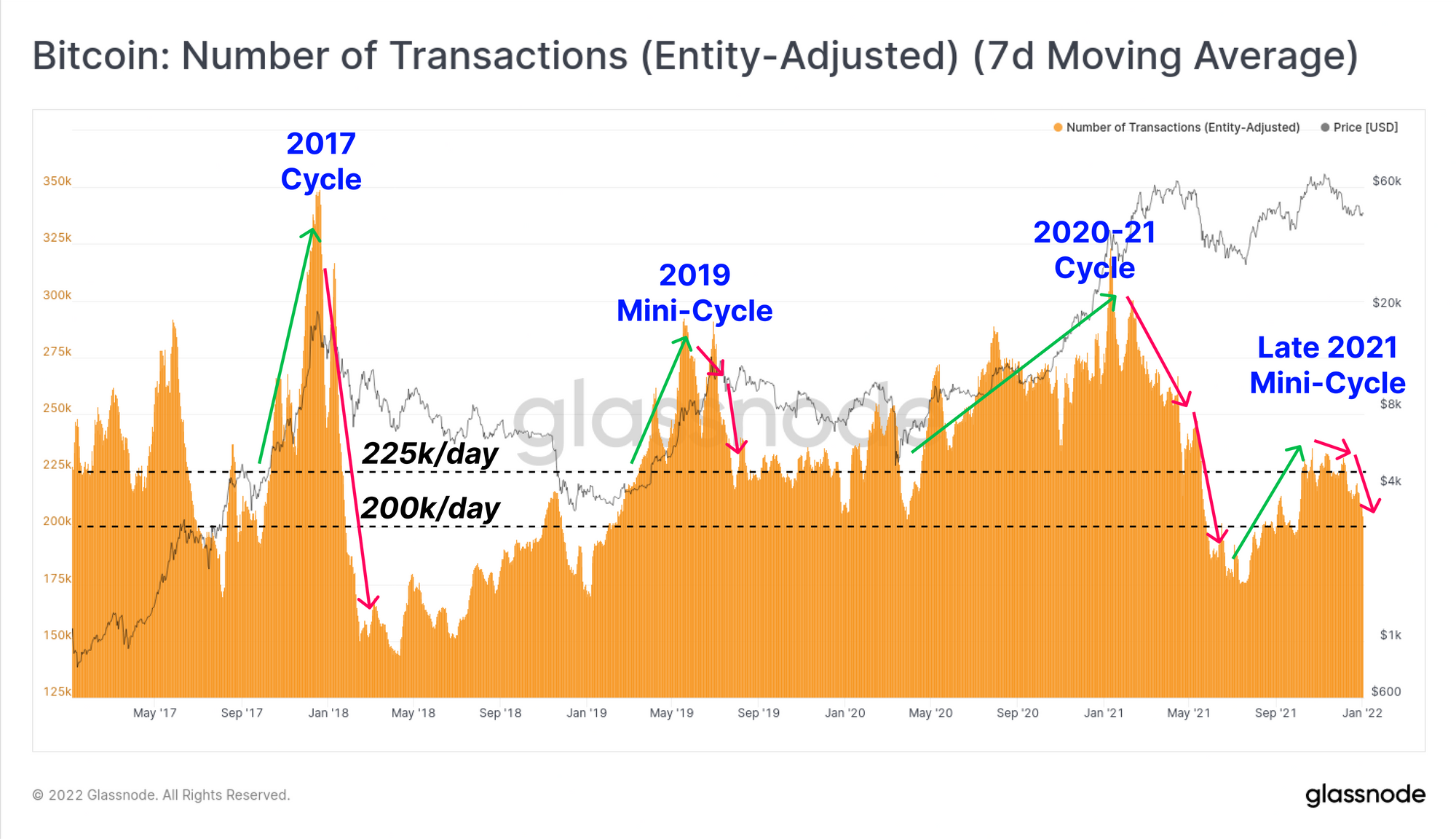

Transaction counts paint a similar picture, where the bull markets of 2017 and 2020-21 stand out clearly, hitting over 300k transactions per day at the peaks. Again similarities can be found between April-August 2019 and the current market since September 2021. In both cases, an initial burst of activity supported rallying prices, but failed to sustain any meaningful momentum, with both transaction counts and prices rolling over.

Until there is further expansion in demand for Bitcoin blockspace, it can be reasonably expected that price action will be somewhat uneventful, and likely sideways at a macro scale.

It is worth noting the underlying differences in market structures between the 2019 and 2021-22 periods. The Apr-Aug 2019 rally was largely associated with heavy spot BTC demand due to the PlusToken ponzi scheme, coupled with multiple short squeezes as trades faded the move in futures markets. The current market is best described as strong rally off the July and September lows following heavy accumulation. This rally was sold into after a very strong October, as both macroeconomic uncertainty and inflation concerns crept into markets, and trading firms sought to lock in end of year profits.

Underlying Supply Remains Constructive

One of the hallmarks of bearish markets is actually a constructive undertone in supply dynamics. Whilst the onchain activity above points to a fairly anaemic demand from retail and market tourists, coin dormancy remains impressive, and signs of smarter, more patient money accumulating remain in tact.

December 2020 was the launching point for very strong price performance in Q1 2021, as Bitcoin broke the previous cycle $20k ATH, and pushed on reach over $64k in April.

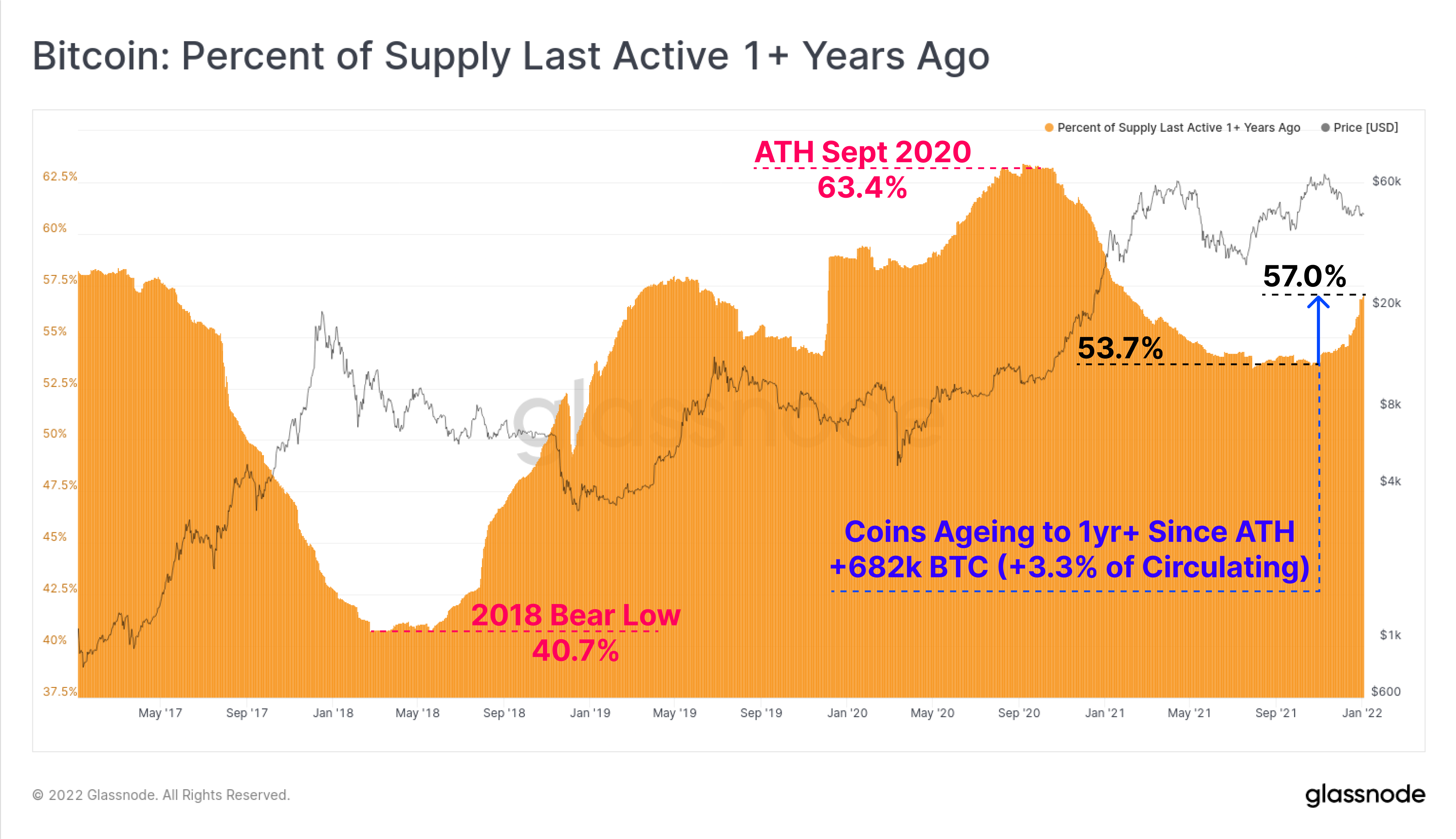

If we look at the supply last active 1y+ metric, we can see that a great proportion of coins accumulated in late 2020 remain unspent to this day. Since October 2021, over 682k BTC have migrated into the 1yr+ age band, representing 3.3% of the circulating coin supply. Over 57% of the coin supply is now older than 1yr, equivalent to the 51.5% seen at the time of the April 2019 bullish impulse.

Given how volatile 2021 was, seeing such an acceleration and large proportion of coins held throughout is quite remarkable.

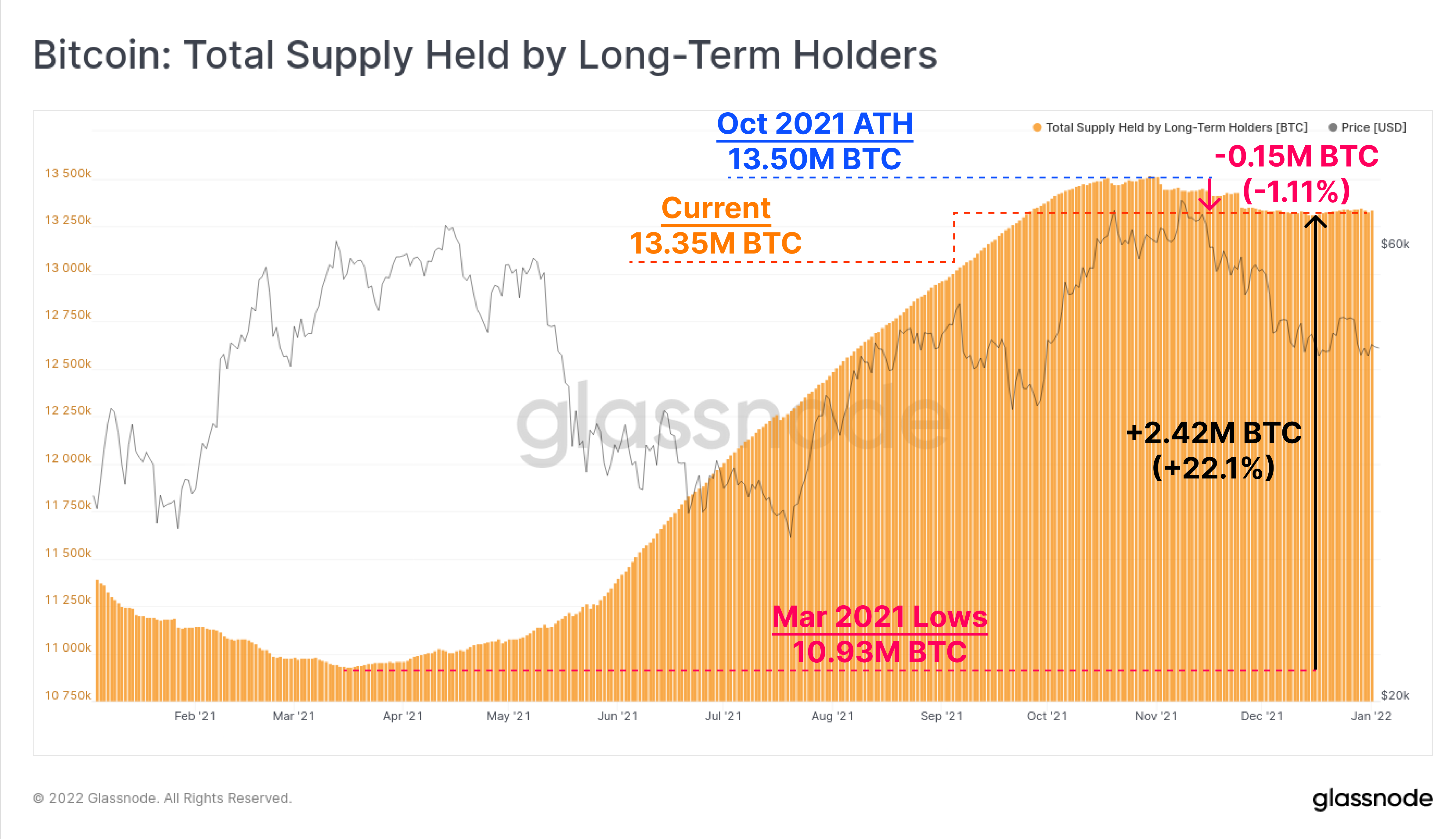

Long-Term Holder (LTH) supply has also plateaued after a very modest period of distribution following the twin ATHs in October and November. This signifies that LTHs have slowed their spending, and are more likely to be HODLers, or even buyers at these prices. This provides another constructive view of market conviction.

LTHs have spent around 150k BTC since October which is just 1.11% of their total held balance. The slow-down in spending is notable given the sharp and sustained correction during this time. Note that this also follows a massive accumulation phase in 2021, where on net, over 2.42M BTC migrated to LTH wallets after March, a balance growth of 22.1%.

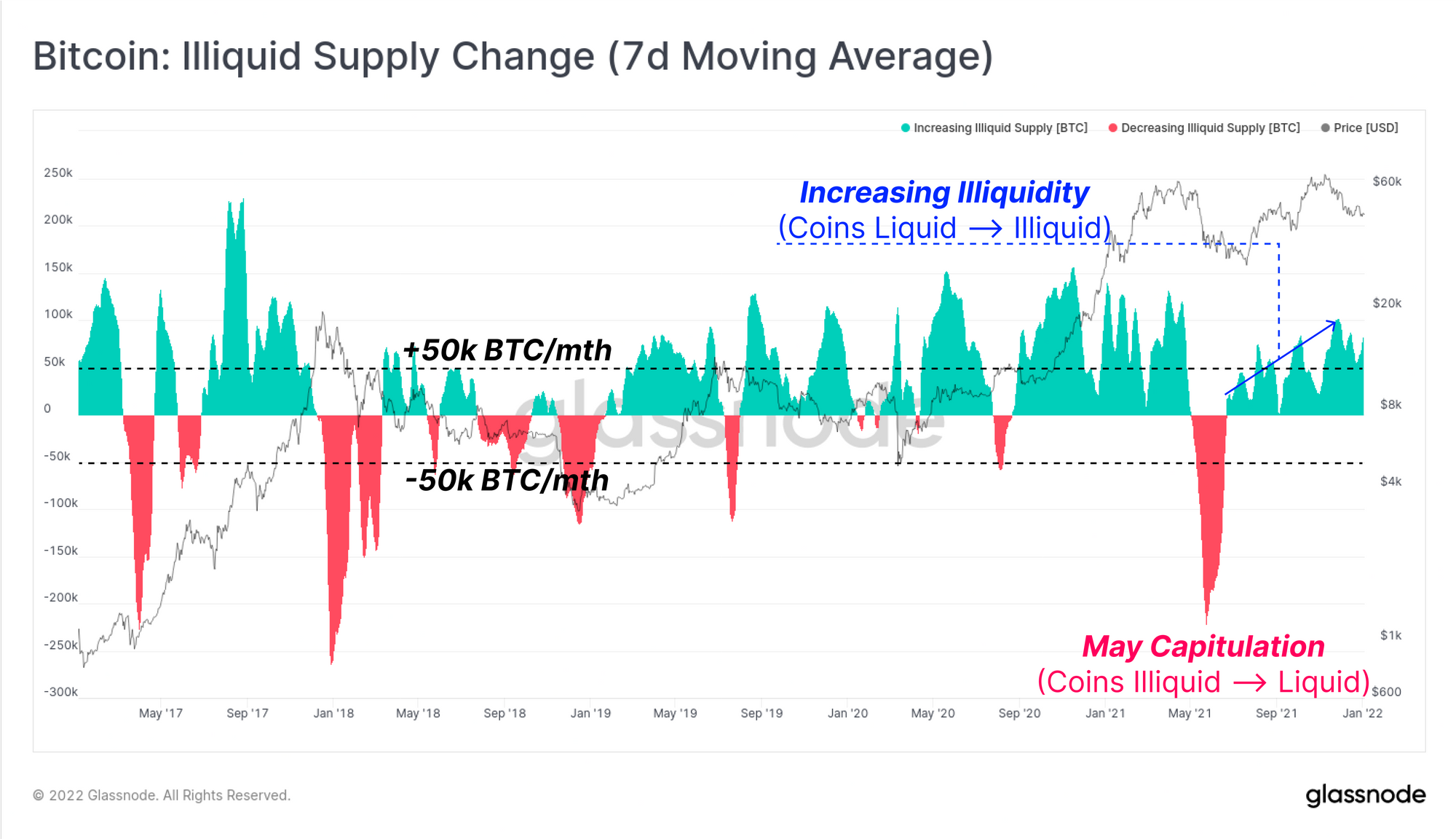

We can also assess coin liquidity as a more immediate measure of current coin supply dynamics, such as whether the market is in accumulation (more illiquid) or distribution (more liquid).

Where the Supply Last Active, and Long-Term Holder Supply metrics use time as the primary input (coin-age, or lifespan), our Liquid and Illiquid metrics uses wallet spending heuristics (see our methodology here). When a coin is moved to a wallet with no history of spending, it will be classified as illiquid (eg. a HODLer executing a dollar cost averaging strategy). Conversely, a wallet that spends very regularly (eg. day-trader or an exchange hot wallet) will be classified as either Liquid or Highly Liquid.

We can see below that over the final months of 2021, even as prices corrected, there has been an acceleration of coins from Liquid, into Illiquid wallets. Through December, coins moved to increasingly illiquid wallets at a rate of between 50k and 100k BTC/month reflecting a higher likelihood of broader accumulation.

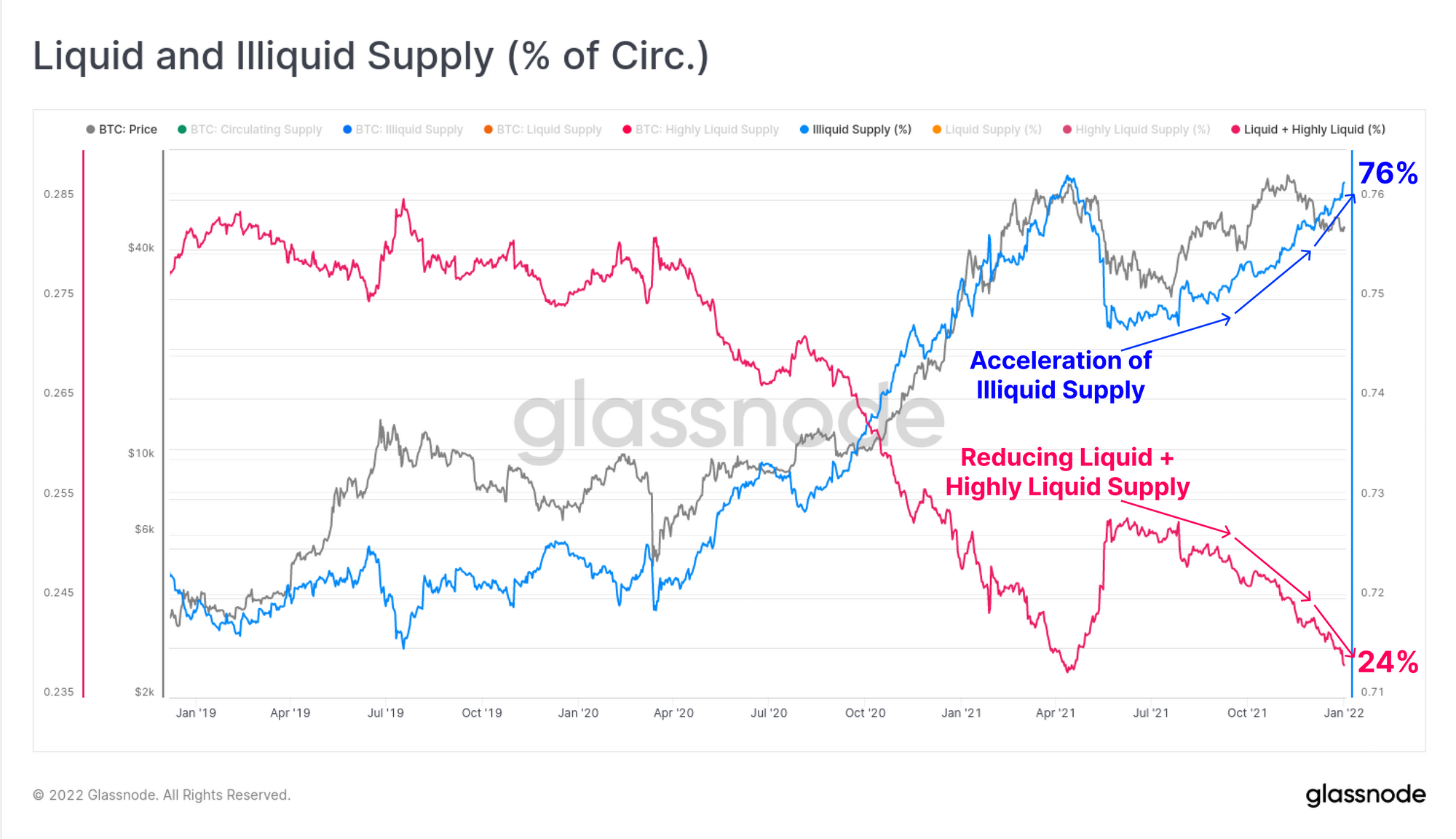

On net, we can see that Illiquid supply (blue) has accelerated higher, at the expense of the combined Liquid and Highly Liquid supply (pink). Illiquid coins now represent 76% of the total supply, and can be seen to have a visible correlation with price. The current conditions do speak to a divergence between what appears to be constructive onchain supply dynamics, compared to bearish-to-neutral price action.

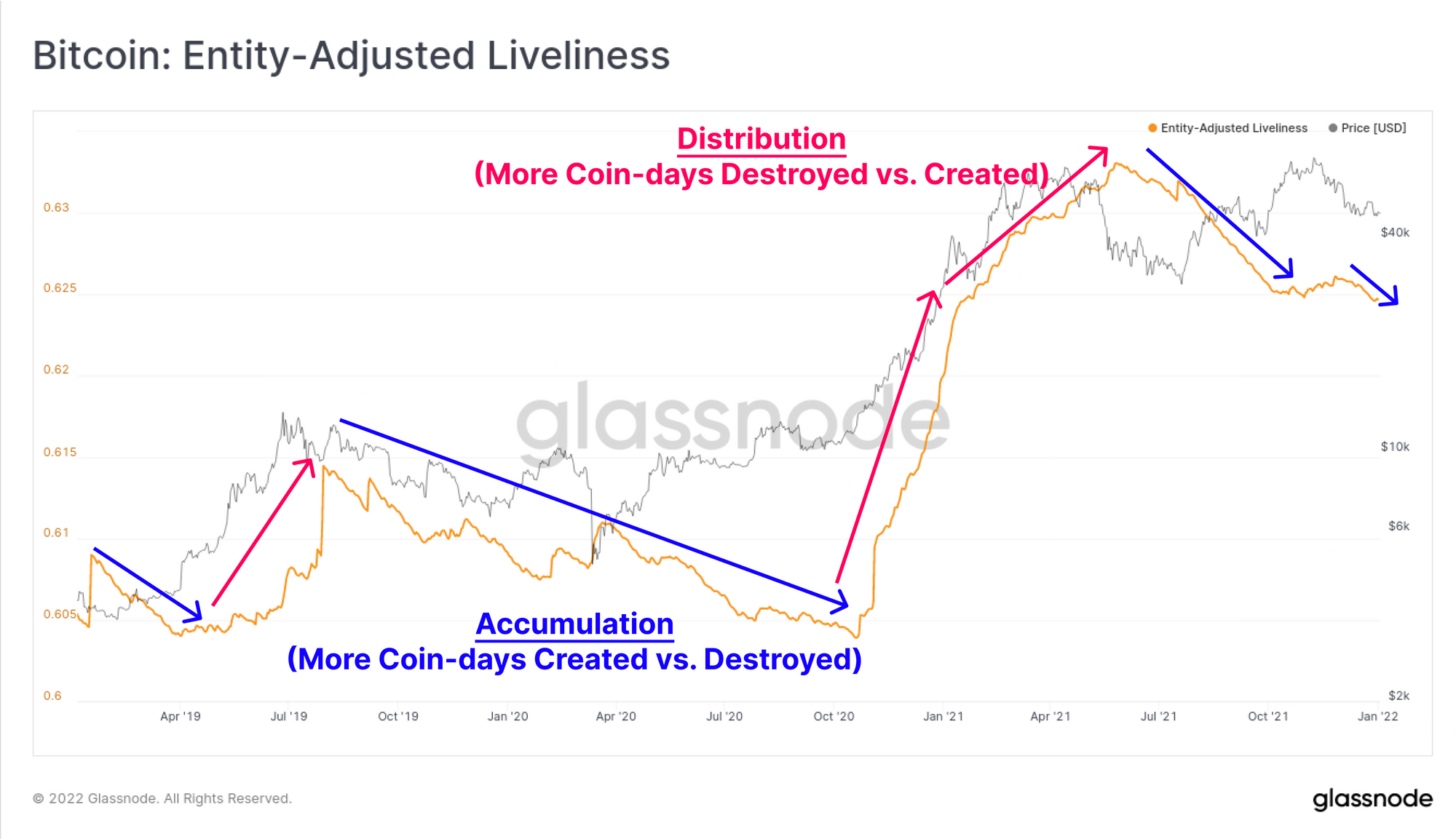

Lastly on the longer-term macro trends, we can see confluence within the Liveliness metric. Liveliness reflects the relative growth of coin-day creation, and coin-days destroyed in the circulating coin supply. Where more coin-days are created, there is more dormancy and HODLing, and Liveliness will trend lower (blue). Conversely, distribution, particularly by older hands, will see more coin-days destroyed than created and Liveliness will trend higher (pink).

Liveliness appears to be in a strong downtrend even as prices correct. This is typical of bearish markets and periods of accumulation, which further adds to the assessment of bearish with bullish undertones.

Short Term Holder Pain

Whilst supply dynamics for the more patient smart money appear constructive, there remains a large sector of the market whom are currently underwater on their holdings. Whilst Long-Term Holders appear to have growing conviction, prices are trading below the onchain cost basis of their counterparts, the Short-Term Holders. These are the most likely coins to create sell-side pressure and weigh on a market recovery.

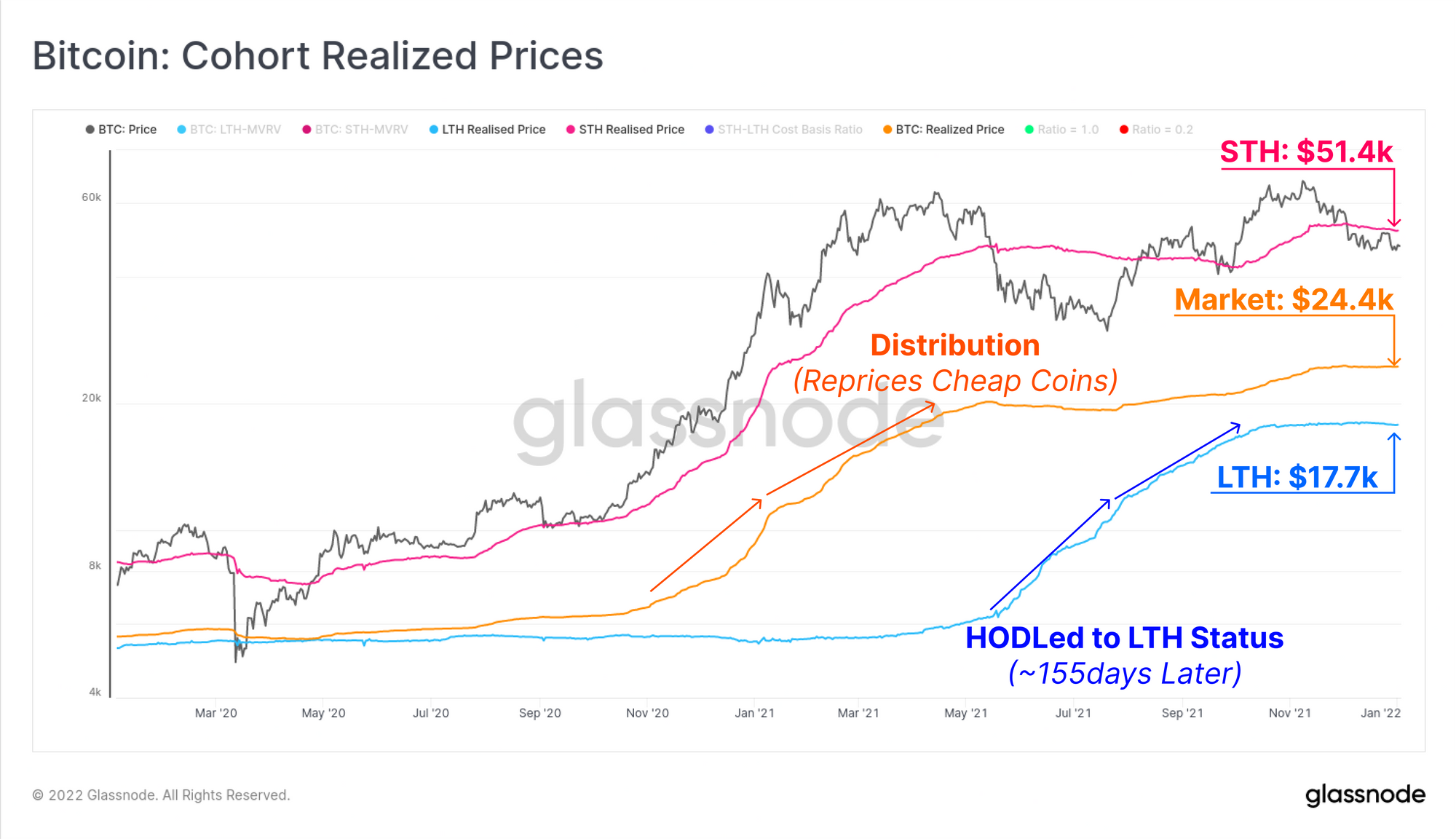

The Realised Price is a metric that values each coin at the time when it was last spent onchain, reflecting the 'valued stored' in Bitcoin, and an estimate of cost basis. The chart below shows the realised price for three cohorts:

- Short-Term Holders (pink): currently trading at $51.4k, meaning this cohort on aggregate is underwater on their investment, and are the most likely to create sell-side resistance.

- Aggregate Market (orange): The realised price for the whole market is currently trading at $24.4k. Generally, the Realised Price provides reliable price support and bear market floors, although it is obviously not ideal to see prices reach this level.

- Long-Term Holders (blue): currently trading at $17.7k, after a steep rise as coins accumulated in H1 2021 at higher prices remain unspent. This metric can be considered a visual observation of LTHs valuing Bitcoin at a higher floor value over time.

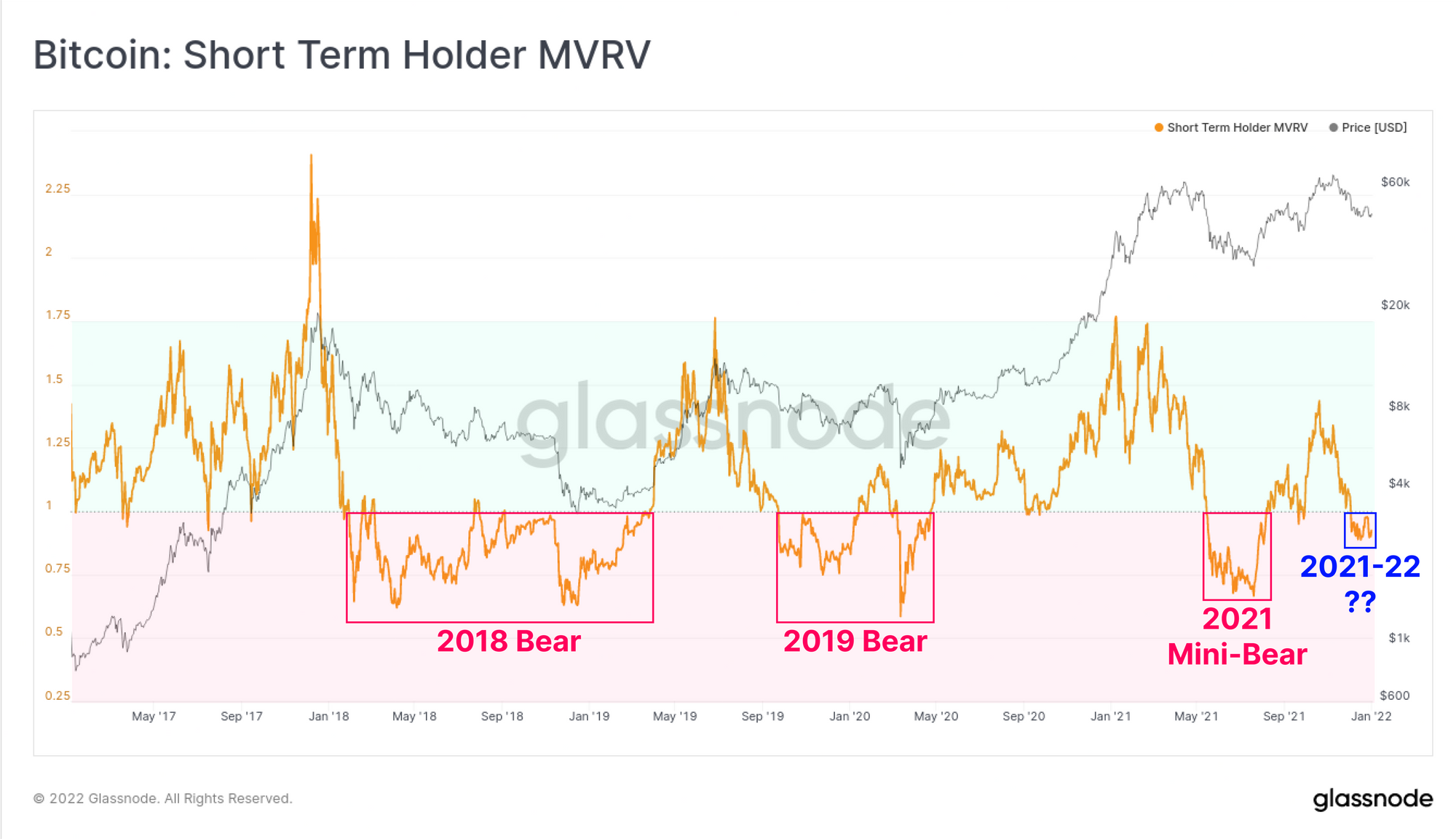

For the Short-Term Holder cohort, the STH-MVRV metric shows the magnitude of current underwater pain relative to past bearish periods. The STH-MVRV is currently trading below 1.0, an event which unfortunately has very few periods since 2017 of being a short lived event. The bearish periods in 2018, 2019 and mid-2021 all saw STHs persistently underwater, with STH-MVRV values of 1 acting as resistance.

Psychologically, this represents new buyers 'getting their money back', which puts $51.4k as a key level to watch.