Structural Weakness

Bitcoin remains defensive between $60k–$72k zone while the $82k–$97k overhead supply caps rallies. Treasury outflows, reactive spot volume, and cooling futures signal shallow demand, keeping price reactive rather than expansionary.

Executive Summary

- Bitcoin remains confined between the True Market Mean (~$79.2k) and the Realized Price (~$55k), reflecting a defensive regime following the structural breakdown, with sell-side pressure continuing to be absorbed in the $60k–$72k demand corridor.

- Large supply clusters at $82k–$97k and $100k–$117k sit in unrealized loss, creating overhead resistance potential during relief rallies.

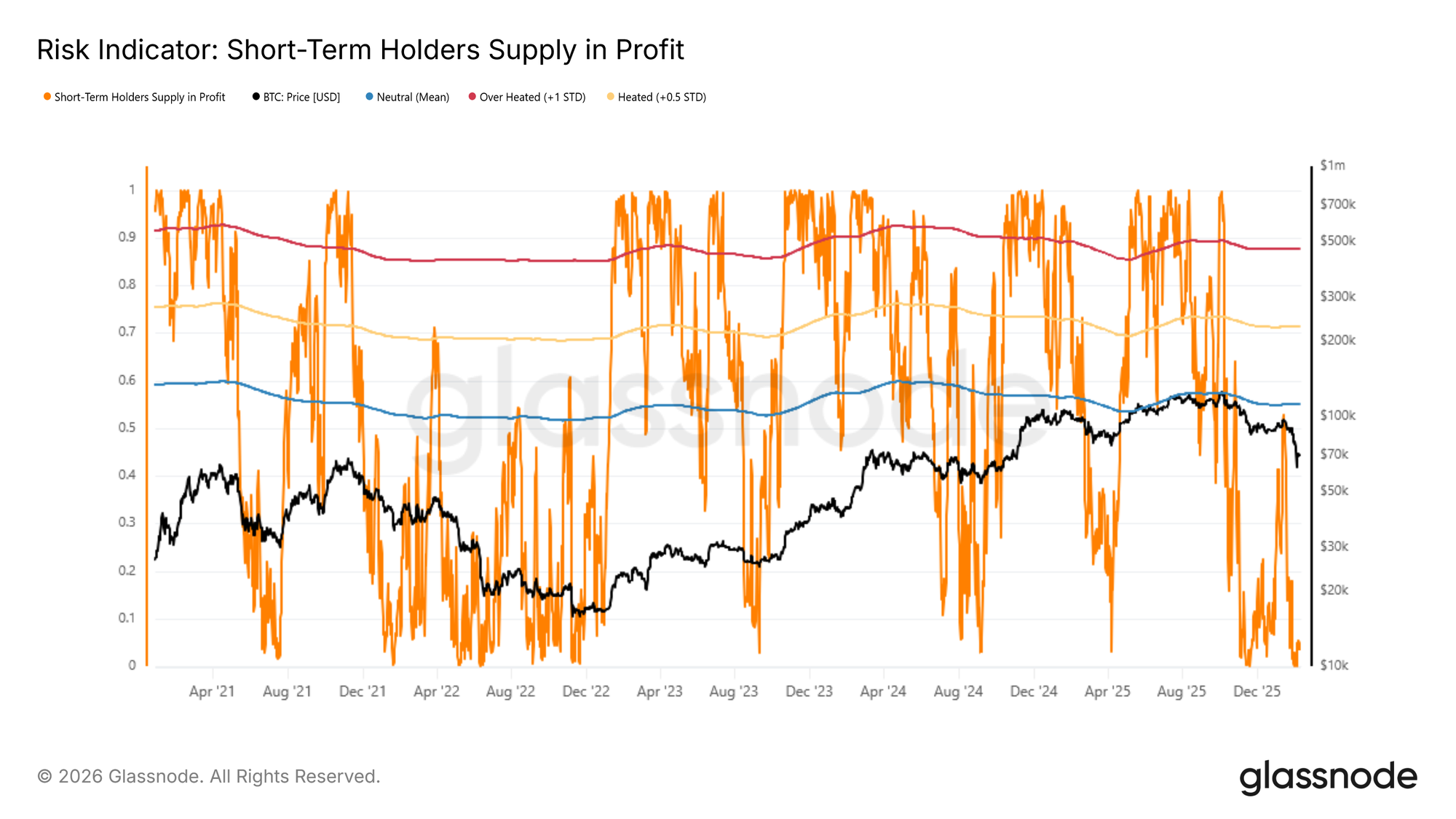

- Short-Term Holder profitability remains negative, underscoring fragile conviction among recent buyers and limiting upside follow-through.

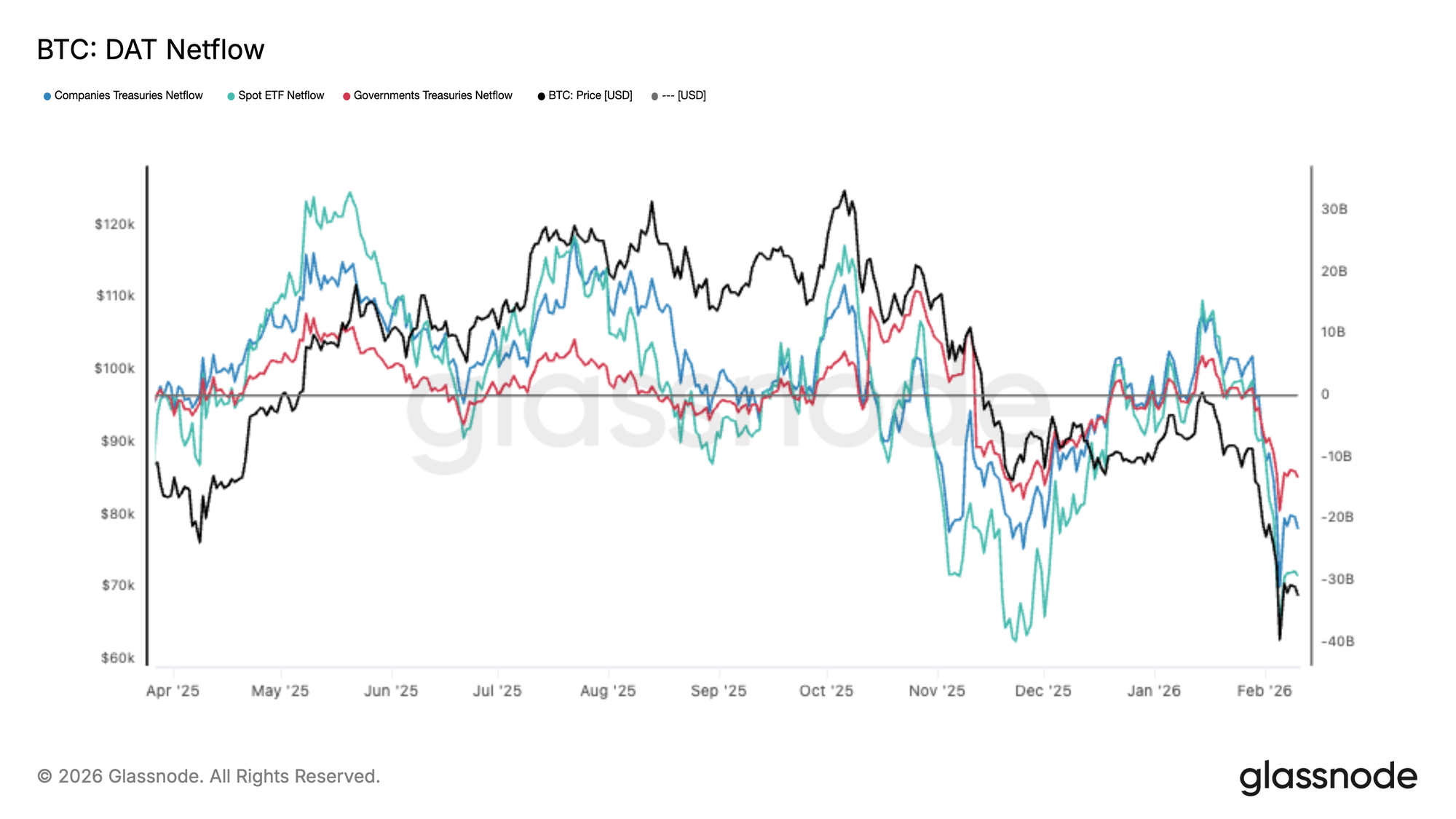

- Digital Asset Treasury flows have flipped into synchronized net outflows, signalling broad institutional de-risking and shallow spot absorption.

- Spot volume spiked during the selloff but failed to sustain, indicating reactive participation rather than constructive accumulation.

- Perpetual futures positioning has cooled, with directional premiums compressing as leveraged traders step back and speculative momentum fades.

- Implied volatility and skew reflect persistent downside hedging demand, consistent with a defensive market posture.

- Dealer gamma and options positioning are reinforcing reactive price behaviour, keeping moves short-lived amid fragile liquidity conditions.

This report is also available for download in PDF format.

On-chain Insights

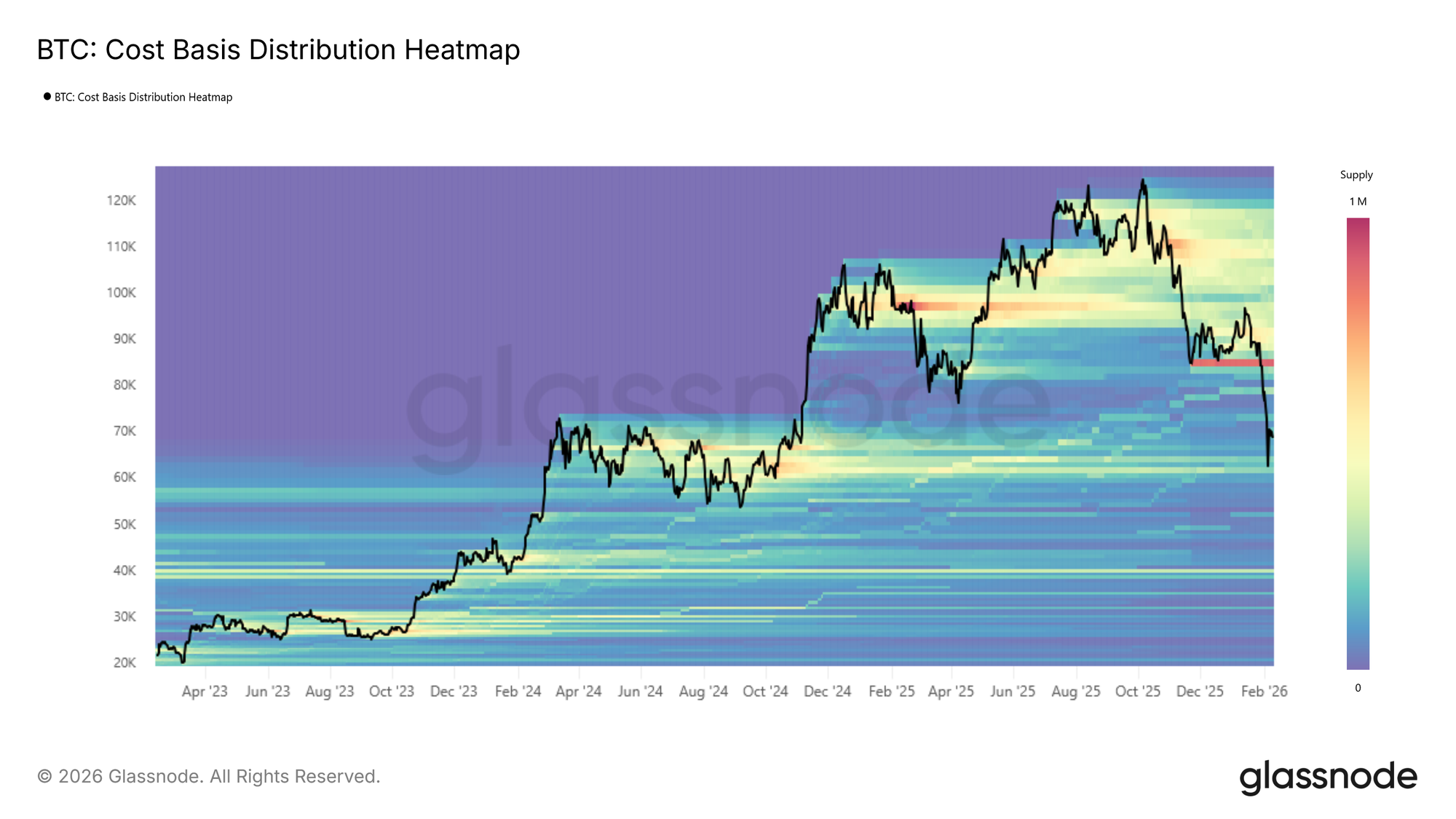

Since recording a new all-time high in early October, Bitcoin has progressed through three distinct structural phases. The first was a sharp contraction, with price rapidly declining toward the True Market Mean, a level repeatedly tested through late November 2025. This was followed by an extended consolidation period, where the price held marginally above this threshold into late January 2026. Most recently, the market entered a third phase, defined by a decisive breakdown below the True Market Mean, accelerating the move toward the $60k region.

New Trading Range

The prevailing range in the cited third phase, currently bounded by the True Market Mean near $79.2k and the Realized Price around $55k, closely resembles the structural environment observed during the first half of 2022.

Similar to Q2 2022, the price is expected to continue oscillating within the Realized Price and True Market Mean corridor, as time and further compression are required for new buyers to emerge and gradually accumulate supply.

A meaningful regime shift, in the short-term, would likely require an out-of-ordinary catalyst, either a decisive reclaim of the True Market Mean near $79.2k, signaling renewed structural strength, or a systemic dislocation similar to LUNA or FTX that forces price below the Realized Price around $55k. In the absence of such extremes, a prolonged phase of range-bound absorption remains the most probable path for the mid-term market.

Defending An Old Accumulation Range

Thus far, sell-side pressure has largely been absorbed within the same oscillatory band that defined much of H1 2024, between $60k and $72k. This repeated defense suggests emerging conviction among buyers willing to accumulate within this corridor. In a constructive scenario, sustained absorption across this range could mirror prior strong accumulation phases, laying a durable foundation for the next impulsive advance.

However, the durability of this structure ultimately depends on the intensity and persistence of demand. The extent to which buyers step in aggressively across the $60k–$72k zone will determine whether the market remains range-bound and stabilizes, or whether weakening absorption opens the door to deeper downside exploration.

Overhead Supply Risk

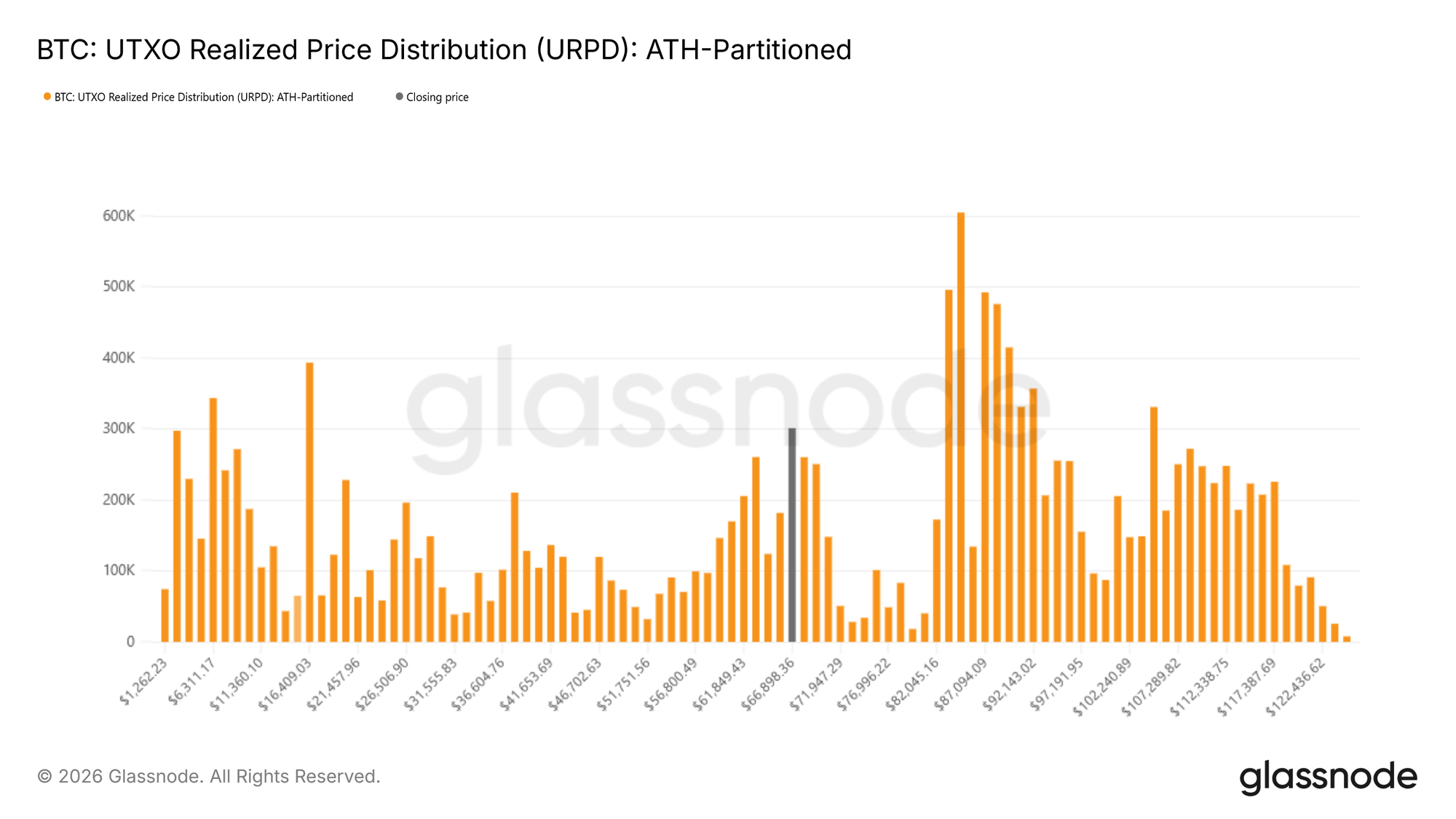

To evaluate whether demand within the $60k–$72k corridor is strengthening, we turn to cost-basis distribution data. The UTXO Realized Price Distribution (URPD) provides a granular view of supply based on the price at which coins last moved, allowing us to identify discrete accumulation clusters. Current readings show that price has so far found support within a dense supply band formed during H1 2024, concentrated between $60k and $72k. This suggests that prior buyers in this range are actively defending their positions.

However, overhead supply remains structurally heavy. Significant clusters are positioned between $82k–$97k and $100k–$117k, representing cohorts now holding substantial unrealized losses. These zones may act as latent sell-side overhang, particularly if prolonged time under water or renewed downside volatility triggers further capitulation.

Tracking Bear Market Tops

Within this range-bound structure, identifying tactical inflection points becomes critical. Assuming the mid-term corridor remains defined by the Realized Price on the downside and the True Market Mean overhead, monitoring local rally dynamics becomes particularly important in a bear regime. Historically, early-stage bear markets tend to see counter-trend rallies capped by recent buyers distributing into strength. As such, sharp expansions in their unrealized profit often precede local top formation.

The Short-Term Holders Supply in Profit metric provides a useful gauge of this oscillation. When positioned within its statistically derived “mean-heated” band, spanning from the historical average to +0.5 standard deviations, prior bear market rebounds have frequently stalled. At present, this metric sits near 4.9%, indicating that the majority of recent buyers remain underwater. This subdued profitability underscores a structurally fragile environment, where upside momentum may struggle to sustain without meaningful demand expansion.

Off-Chain Insights

Digital Asset Treasury Flows

Digital Asset Treasury (DAT) flows have turned sharply negative, with spot ETF, corporate, and government treasuries all registering simultaneous net outflows as Bitcoin trades into fresh local lows. ETF treasuries are driving the majority of the move, while corporate and sovereign flows reinforce that selling pressure is broad rather than isolated. This alignment signals a clear shift toward de-risking, where marginal institutional demand has stepped back, and supply is dominating near-term order flow.

The scale of these outflows highlights ‘heavy’ spot conditions, with absorption struggling to keep pace with distribution. Rather than reflecting tactical rotation within a single cohort, the synchronized nature of the move suggests a market-wide pullback in treasury exposure. Until DAT flows stabilize, price action remains sensitive to continued selling pressure, with volatility likely dictated by how quickly new buyers step in to counterbalance the current wave of institutional distribution.

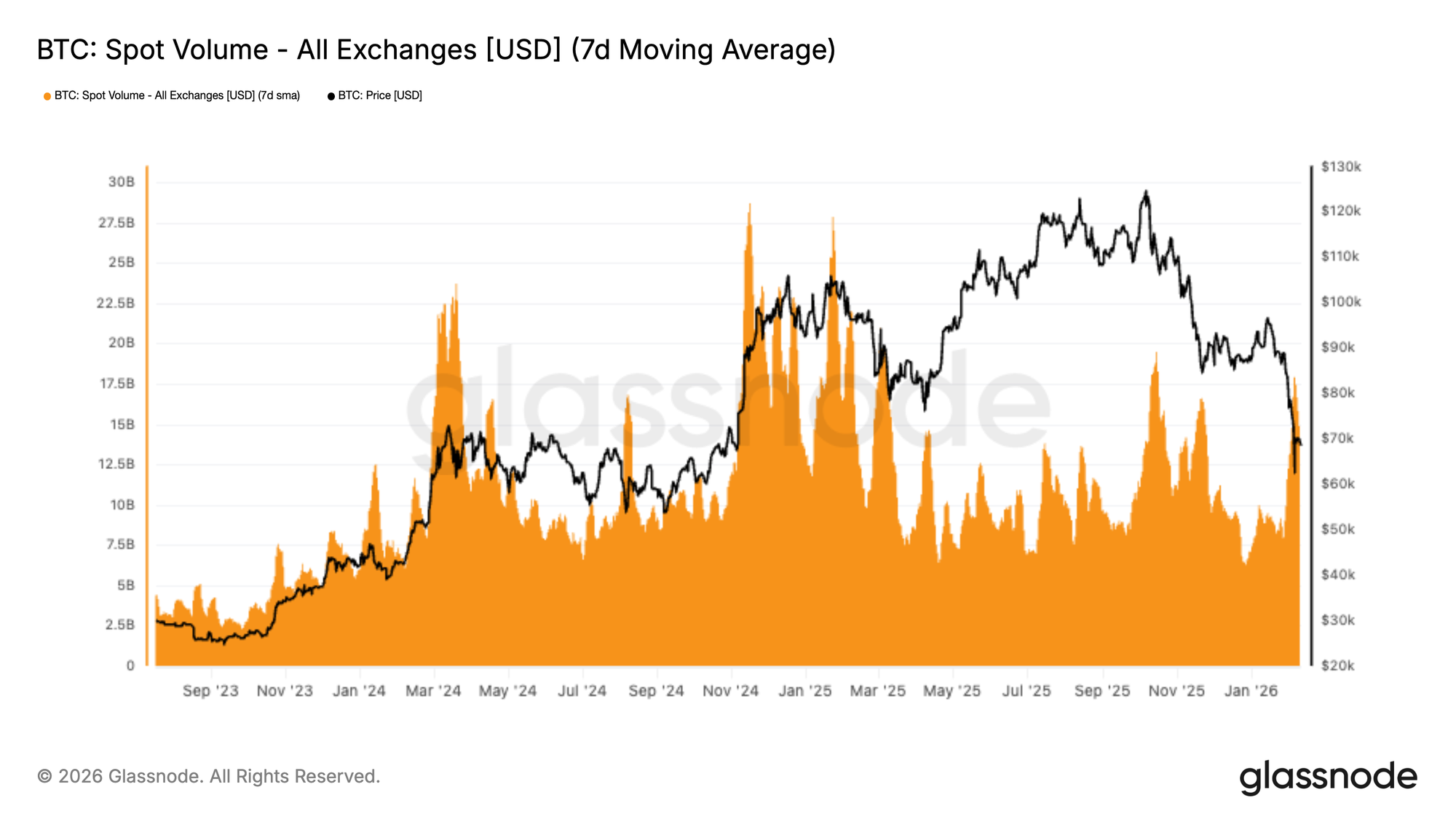

Lackluster Spot Volume

Spot trading volume expanded sharply during Bitcoin’s selloff into the low-$70Ks, with the 7-day average registering a clear spike as volatility accelerated. This increase reflects reactive participation as traders responded to rapid downside movement, rather than a broad wave of fresh conviction buying. Notably, the volume expansion faded quickly after the initial surge, suggesting that while the move drew attention, it did not translate into sustained spot demand.

The lack of follow-through indicates that absorption remains shallow relative to the scale of selling pressure. Instead of signalling accumulation, current activity appears driven by short-term repositioning and liquidation-related churn. Without continued participation on the bid side, price remains sensitive to further volatility, as the market has yet to demonstrate the kind of persistent volume support typically associated with stabilization. For now, spot flows reflect engagement during stress, not a decisive shift toward constructive demand.

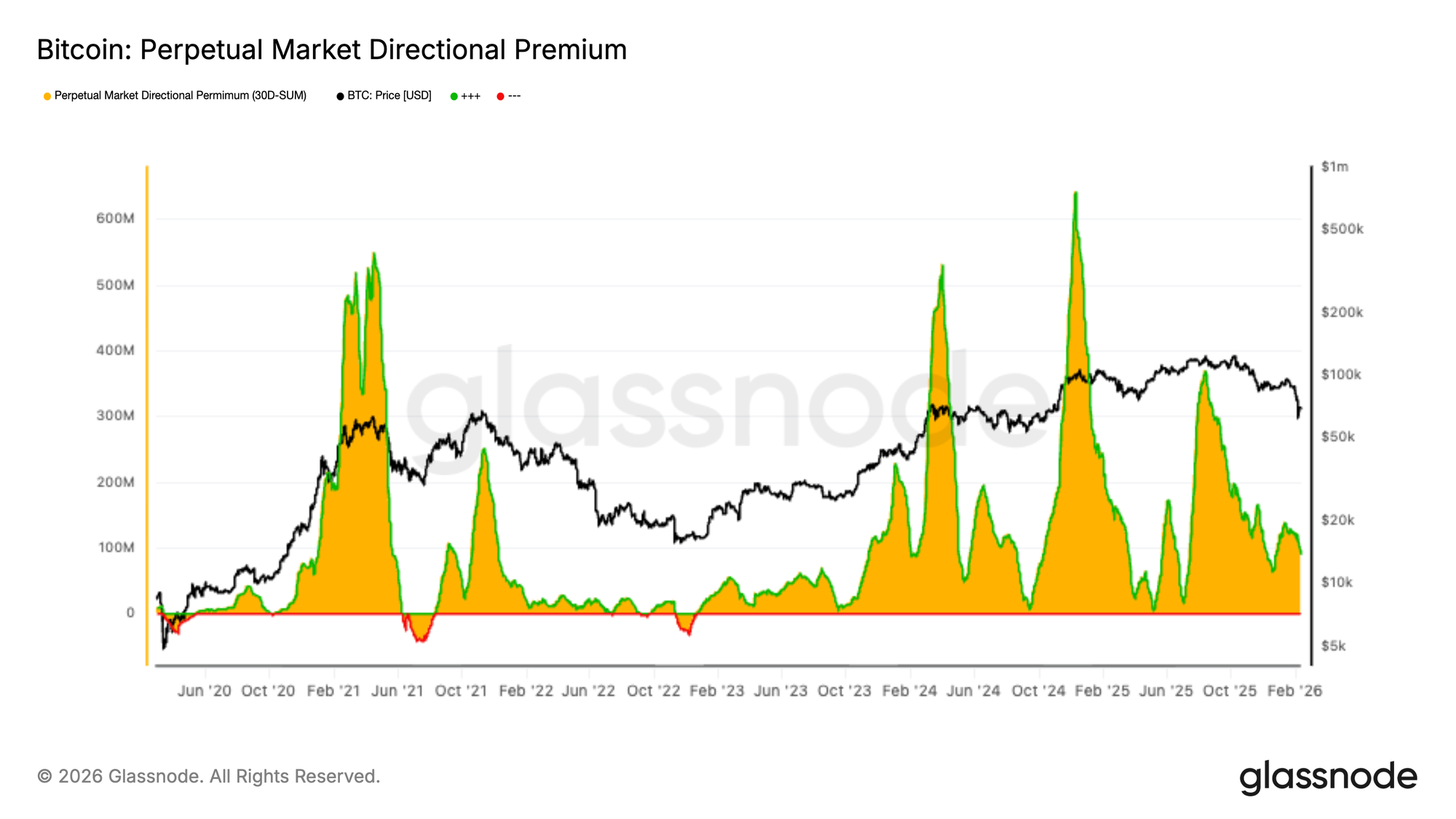

Futures Premium Cools Off

Perpetual futures positioning has cooled notably, with the directional premium compressing toward neutral territory following the recent pullback. This reflects a clear reduction in speculative activity, as leveraged traders step back rather than aggressively positioning for continuation in either direction. Earlier in the cycle, elevated premiums coincided with strong directional conviction, but the current regime suggests a market lacking appetite for leveraged exposure.

The contraction highlights a broader decline in futures participation, where risk appetite has faded alongside volatility. Instead of seeing aggressive short positioning or renewed long speculation, traders appear hesitant, resulting in thinner directional flows. This subdued derivatives activity removes a key source of momentum that often amplifies price swings, leaving spot markets to dictate near-term direction. For now, the futures complex signals caution and reduced conviction, consistent with a market transitioning into a lower-energy phase following the recent selloff.

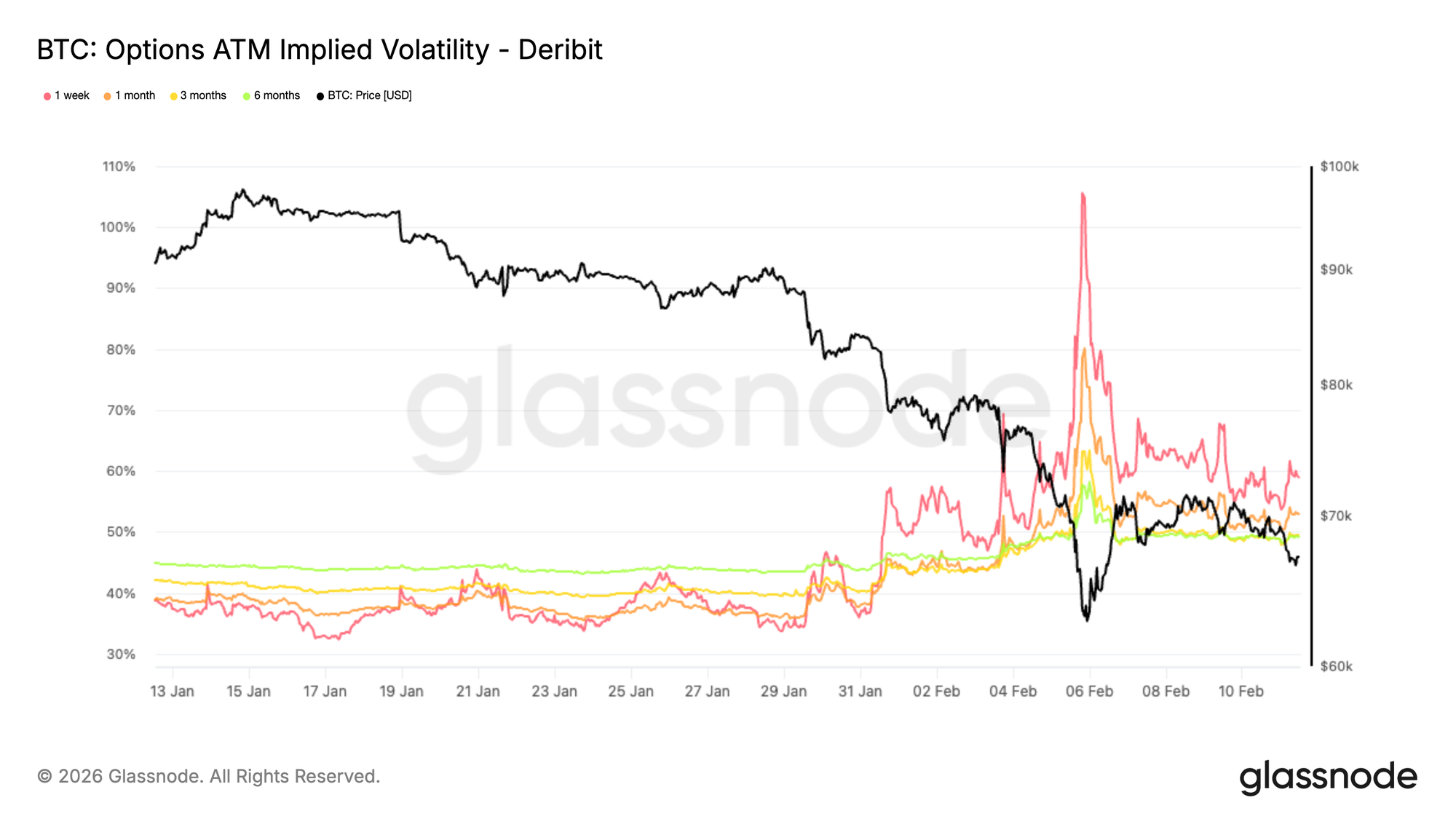

Implied Volatility Signals a Higher Risk Regime

The first structural shift after the capitulation event is visible in the implied volatility regime. Looking at the 1 month ATM implied volatility chart, the distinction is clear. Longer dated maturities repriced higher, with 6-month implied volatility gaining more than 5 volatility points since the beginning of the month, and 3 month rising by roughly 9 points.

The most significant jump occurred in the front end, where 1-week implied volatility surged by more than 20 points. Implied volatility reflects how much movement the market expects going forward. Moves of this magnitude rarely represent a temporary spike. They signal a repricing of forward risk across the surface.

Although volatility has eased from its peak, it remains elevated across maturities, indicating that traders continue to price sustained uncertainty rather than a quick return to calm conditions.

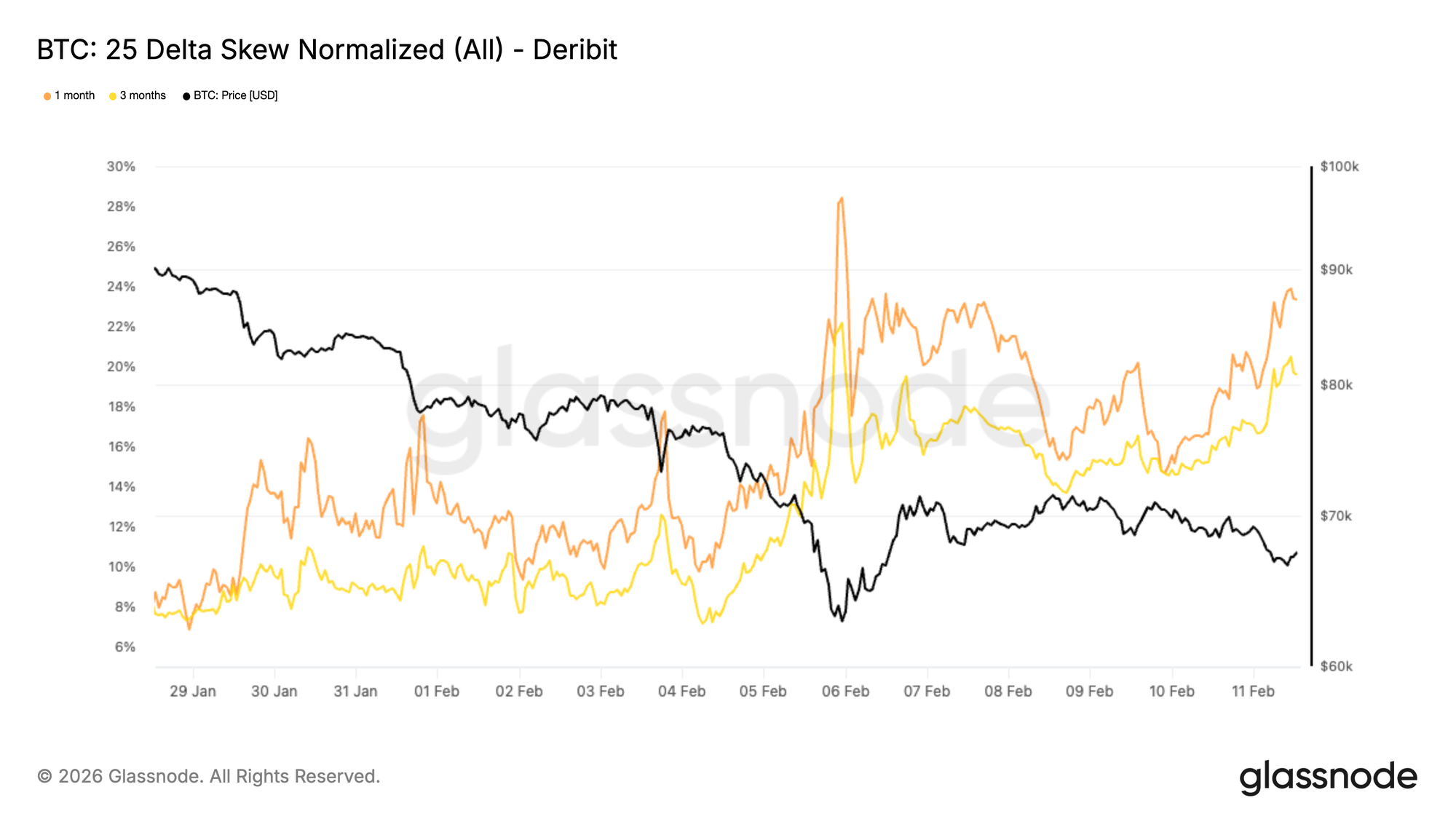

25 Delta Skew Shows Persistent Downside Demand

While overall volatility repriced higher, skew reveals how that demand is distributed across strikes. Looking at the 1-month and 3-month 25 delta skew, both moved sharply negative during the crash as traders aggressively bought puts.

Even after Friday’s relief rally, downside protection continues to trade at a significant premium and is now near the most extreme levels reached during the selloff. The 25 delta skew compares the implied volatility of out-of-the-money puts versus calls. When negative, it signals a stronger demand for downside protection than for upside exposure. On January 28, the 1-month and 3-month skew were around 8 percent put premium. They now stand near 23 percent and 19 percent, respectively.

The surface remains clearly tilted toward downside insurance, showing that caution and fear persist despite the bounce.

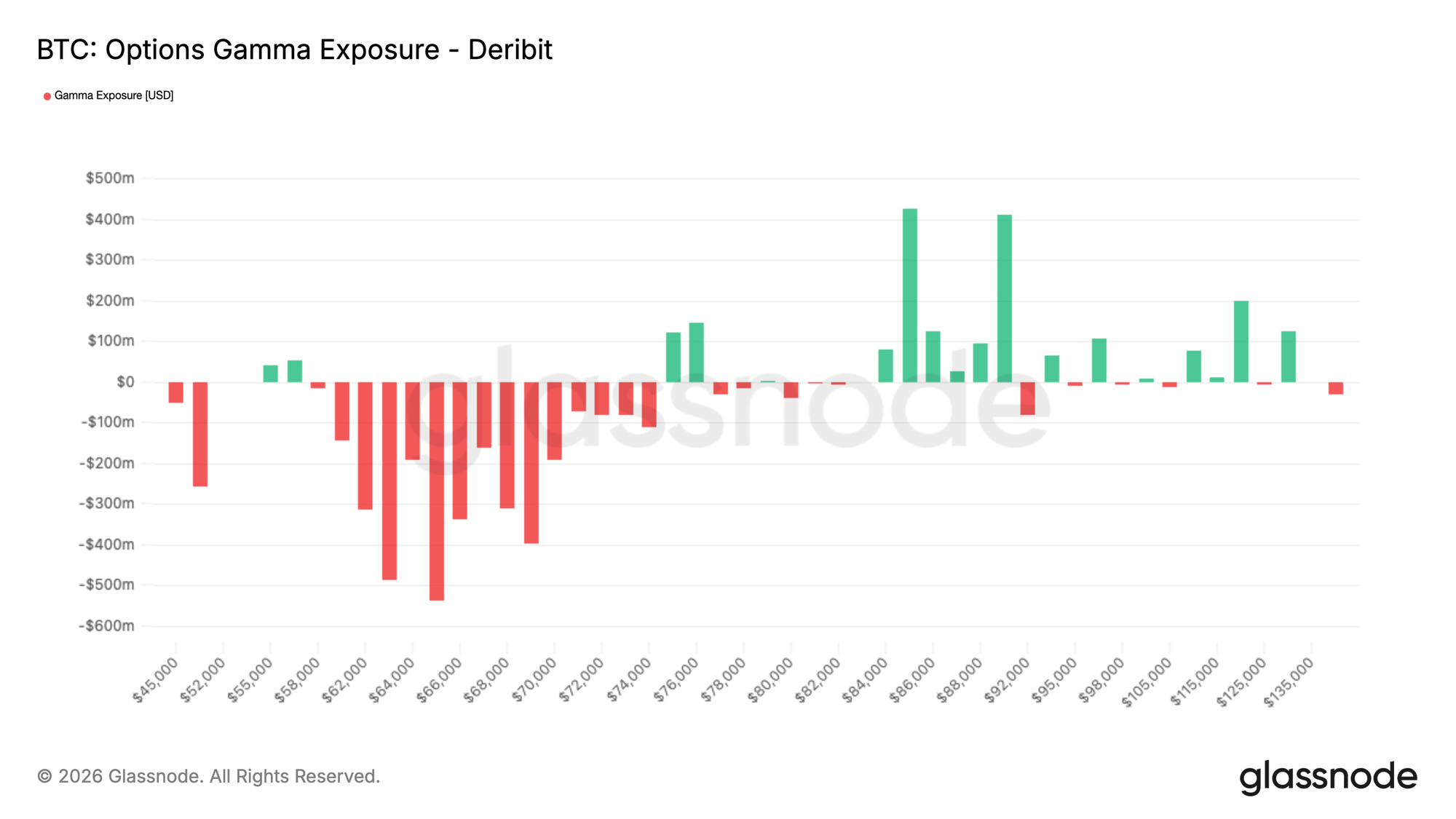

Dealer Gamma Positioning Keeps Price Reactive

With BTC at 68K at the time of writing, spot sits in the middle of a pronounced short gamma corridor, with even larger gamma exposure stacked below.

This defensive options flow leaves a mechanical footprint in dealer positioning. When dealers are short gamma, they must buy into strength and sell into weakness to remain hedged. This behavior reinforces price moves rather than dampening them, particularly in elevated volatility conditions such as the current regime.

Following aggressive put buying during the crash, dealers remain structurally exposed in a way that can amplify swings. The recent rally has not fully neutralized that sensitivity. The result is a mechanically fragile market structure, where hedging flows can accelerate moves in either direction, with a skewed risk toward sharper downside extensions.

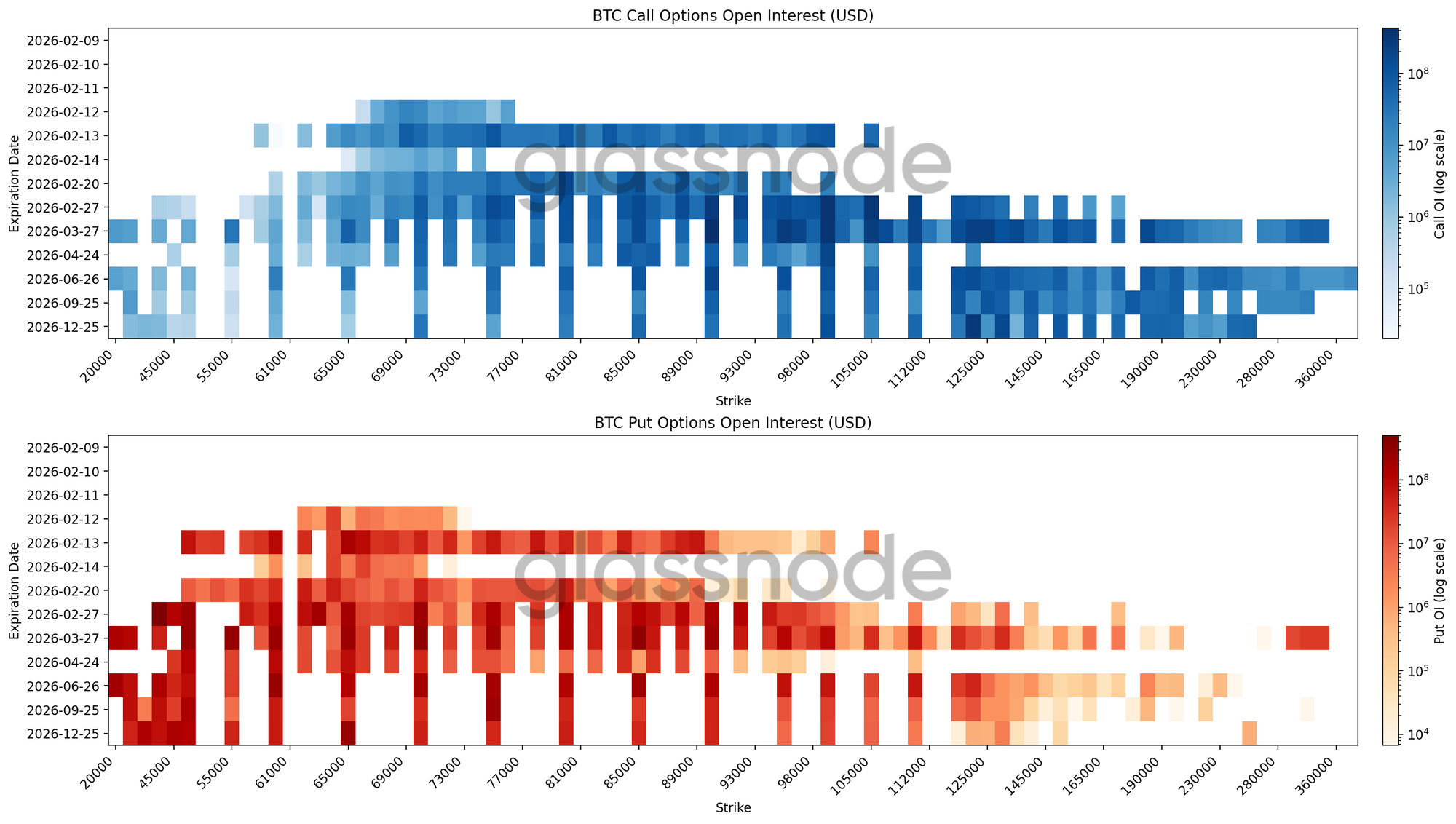

Open Interest Heatmap Reveals Broad Hedging Zones

Our latest heatmap visualizes BTC options open interest across strikes and expiries in a single view, highlighting where positioning is concentrated and where structural price sensitivity may emerge. Put open interest is heavily stacked below spot. For the February expiry, the largest cluster sits between 70K and 60K. Further out on the curve, a broader concentration builds between 50K and 30K across longer dated maturities into year end.

This structure spans multiple expiries, indicating persistent hedging demand rather than protection tied to a single event. Exposure is distributed across adjacent strikes, suggesting range-based insurance rather than targeting a precise crash level. On the call side, open interest clusters above 120K into the second half of the year. Near term upside is being monetized, while longer dated downside remains owned as tail risk protection, reinforcing the deeply negative skew.

Positioning remains defensive and is not consistent with a market preparing for a snapback rally.

Conclusion

Bitcoin continues to trade within a structurally defensive regime, where price remains anchored between key cost-basis levels and absorption zones that are actively being tested. Sell-side pressure is still being met with demand in the $60k–$72k corridor, but overhead supply and negative short-term holder profitability suggest conviction remains fragile. This leaves rallies vulnerable to resistance while stabilization depends on sustained buyer participation.

Off-chain flows reinforce this cautious backdrop. Institutional treasury outflows point to ongoing de-risking, while spot activity has been reactive rather than accumulation-driven. At the same time, derivatives markets reflect a cooling in speculative appetite, with elevated hedging demand and dealer positioning keeping price action reactive rather than directional.

Taken together, the market appears to be navigating a period of balance under stress. Liquidity remains thin, participation is selective, and positioning is defensive. For conditions to improve, the market will likely require both renewed spot absorption and a shift in risk appetite. Until then, volatility is expected to remain driven by short-term positioning dynamics rather than broad-based expansion.

Disclaimer: This report does not provide any investment advice. All data is provided for informational and educational purposes only. No investment decision shall be based on the information provided here, and you are solely responsible for your own investment decisions.

Exchange balances presented are derived from Glassnode’s comprehensive database of address labels, which are amassed through both officially published exchange information and proprietary clustering algorithms. While we strive to ensure the utmost accuracy in representing exchange balances, it is important to note that these figures might not always encapsulate the entirety of an exchange’s reserves, particularly when exchanges refrain from disclosing their official addresses. We urge users to exercise caution and discretion when utilizing these metrics. Glassnode shall not be held responsible for any discrepancies or potential inaccuracies.

Please read our Transparency Notice when using exchange data.