Waiting for Conviction

BTC is stuck between key valuation anchors, with $60k to $69k as the main demand zone. Profitability and breadth are fading, spot and ETF flows stay negative, and leverage has reset. The market is stabilizing, not yet recovering.

Executive Summary

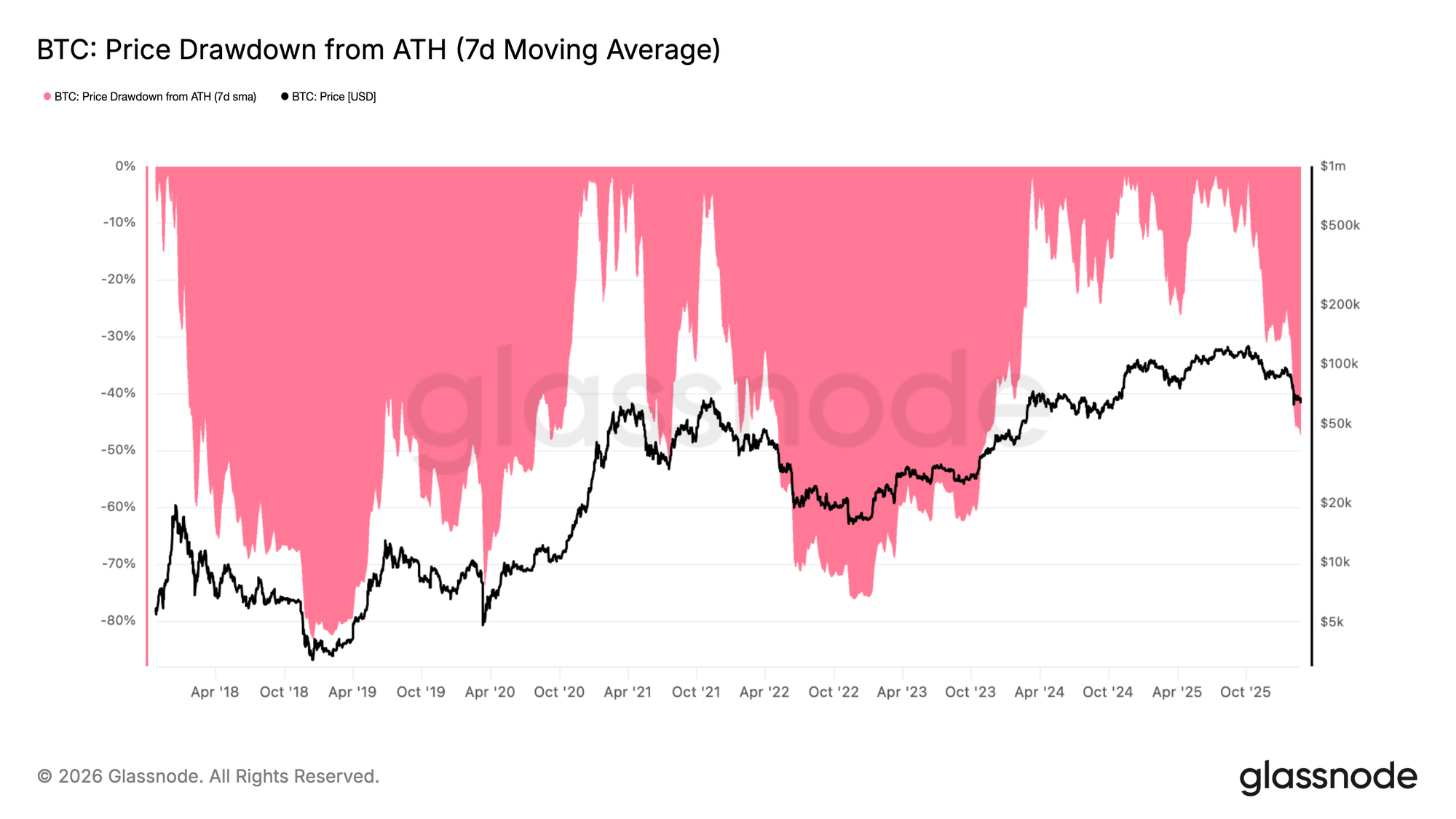

- Bitcoin remains range-bound between $60k–$70k at a 47% drawdown from ATH, a depth historically aligned with mid-to-late bear market phases.

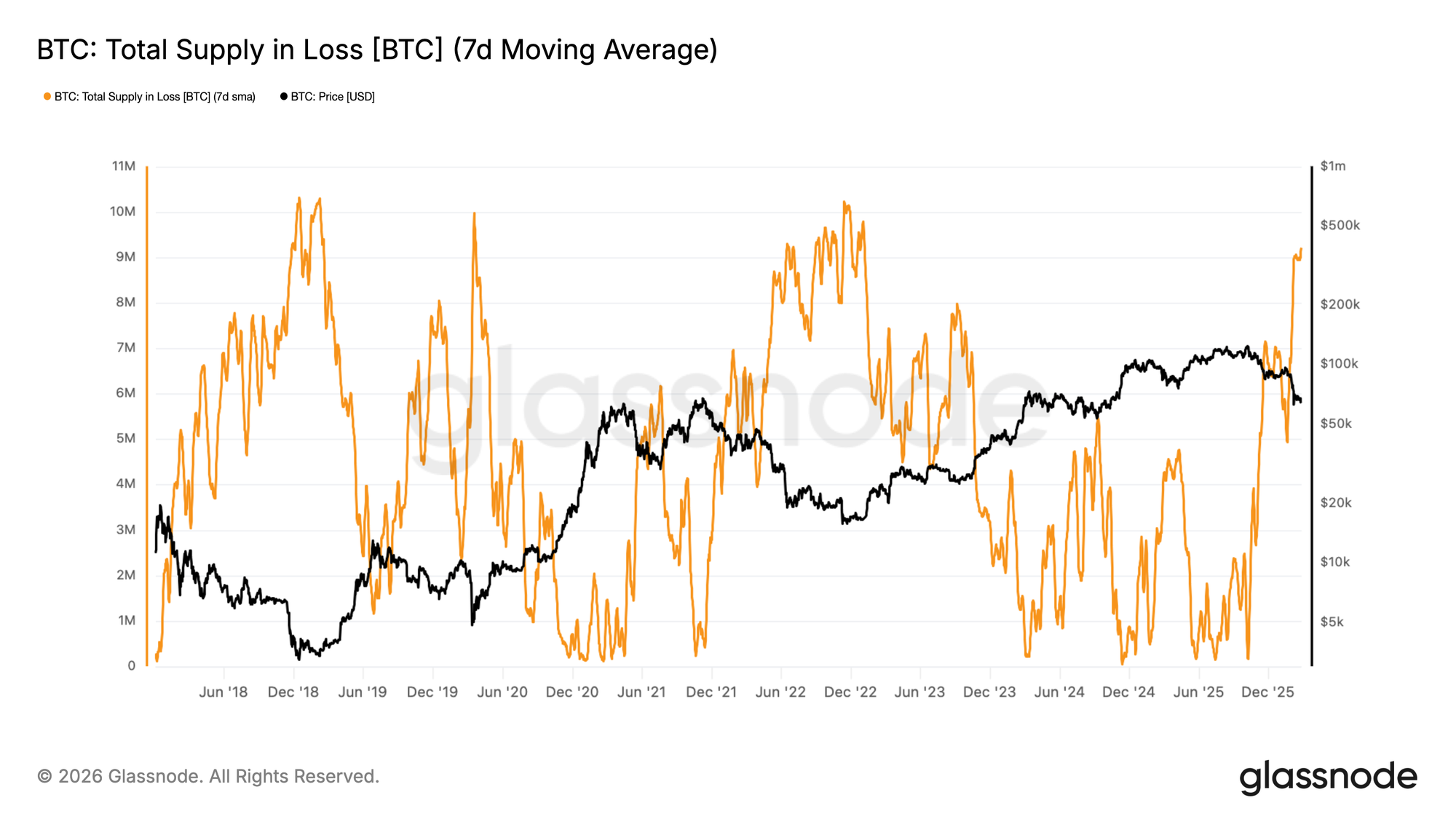

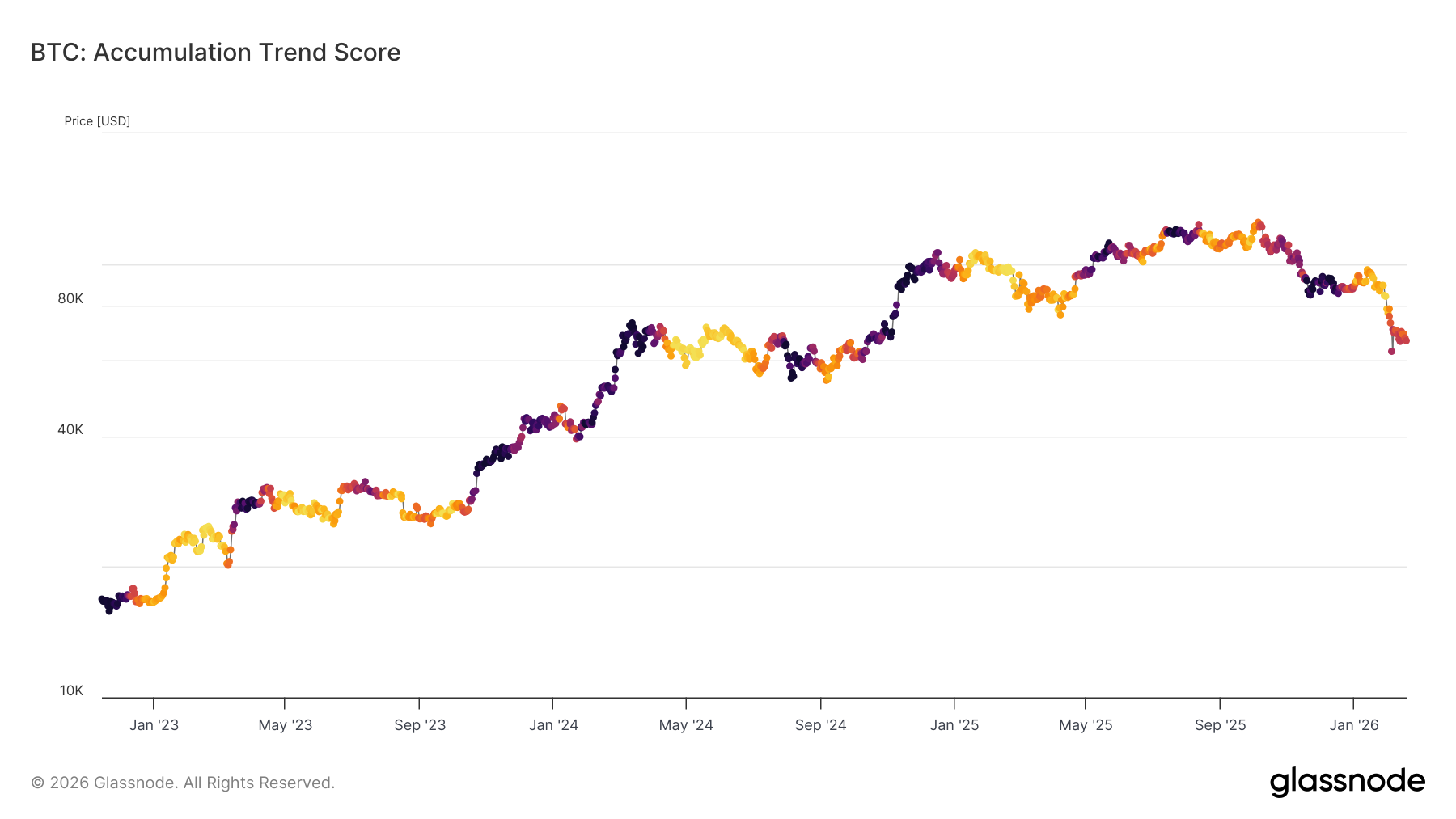

- Nearly 9.2M BTC are now held at a loss, yet accumulation remains weak, with the Accumulation Trend Score below 0.5, signaling limited conviction from larger entities.

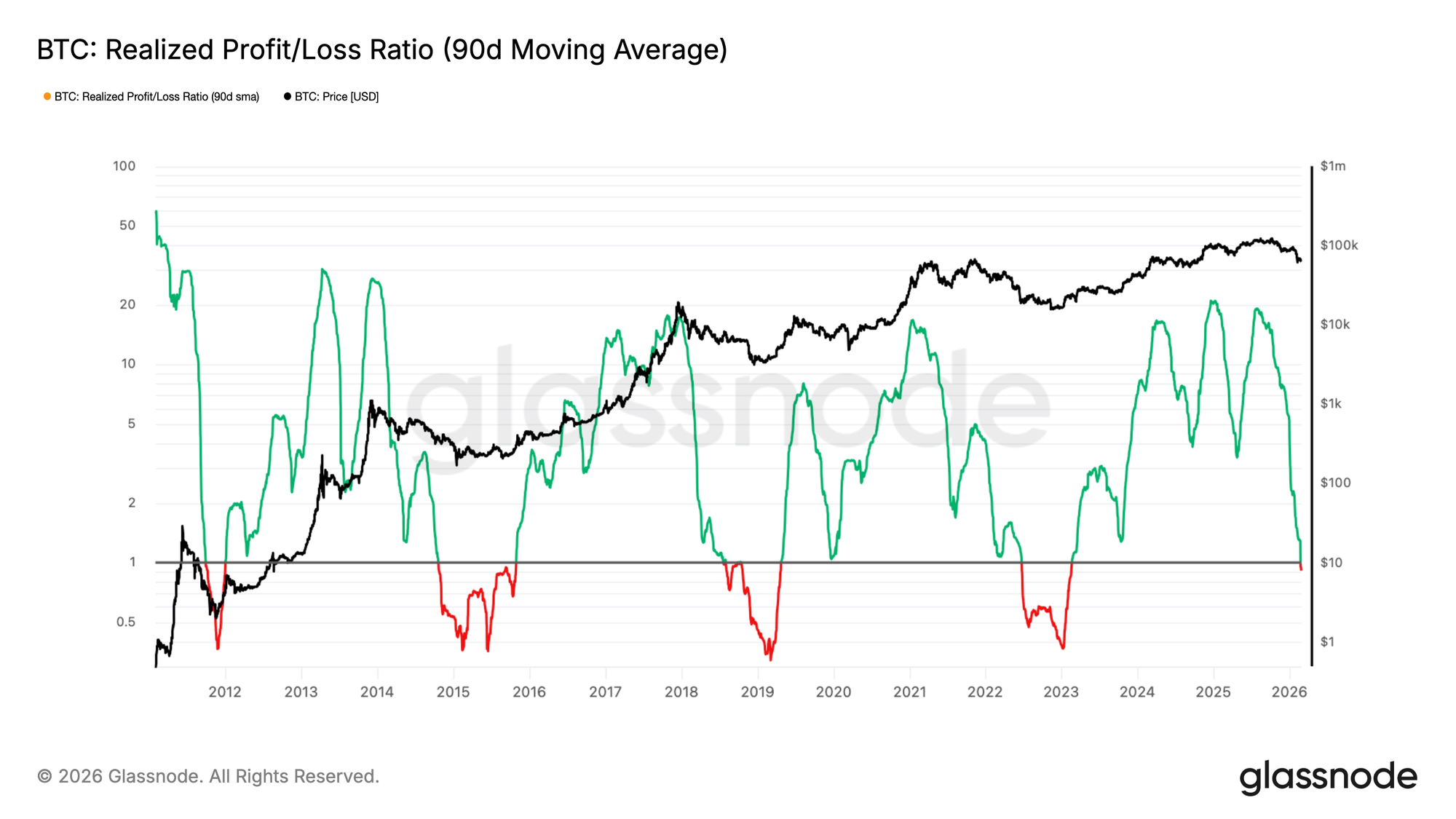

- The 90D Realized Profit/Loss Ratio has fallen below 1.0, confirming an excess loss regime and structurally impaired liquidity, keeping downside risk elevated.

- Market breadth remains weak, as fewer assets sustain positioning above long-term trend baselines, confirming underlying structural softness.

- Large entity accumulation remains constructive in structure but has slowed in pace, reducing a key source of marginal upside support.

- Spot CVD has turned decisively negative across major venues, signaling active distribution. ETF flows remain in persistent outflow, confirming institutional demand is not providing a structural bid.

- Perpetual funding rates have normalized toward neutral, indicating leverage has reset. However, the absence of sustained positive funding reflects muted speculative appetite rather than renewed bullish conviction.

- Implied volatility has reacted to downside moves but failed to expand meaningfully, suggesting options markets are stabilizing rather than pricing systemic stress.

- Dealer gamma positioning and skew dynamics point to fragile liquidity conditions, with price increasingly sensitive to incremental order flow in a lower-volatility regime.

This report is also available for download in PDF format.

On-Chain Insights

Time Becomes the Risk

Since rebounding from the $60k region in early February, Bitcoin has entered a sideways consolidation phase. As outlined in Week 06 – Structural Weakness, this fragile range reflects a temporary equilibrium between seller exhaustion and localized support from long-term holders who accumulated within the same price band during H1 2024.

From a broader cyclical perspective, the 7-day moving average drawdown from the ATH currently sits at 47.3%, comparable to the early May 2022 range-bound phase that preceded further downside expansion. Historical analogues suggest that, at similar drawdown depths, time typically acts as a headwind rather than a tailwind for bullish continuation. Prolonged compression at these levels increases the probability that leveraged or structurally weak entities face mounting balance sheet stress.

Absent a decisive reclaim of higher price levels (>$70k) in the coming weeks, the risk of renewed contraction remains elevated.

Deep into Bear Market Territory

Extending this assessment of structural pressure, supply-side pain provides an additional lens into bear market depth. Total Supply in Loss measures the volume of coins whose acquisition price exceeds the current spot price, serving as a proxy for how widespread unrealized losses have become.

The 7-day moving average of this metric has risen to approximately 9.2M BTC underwater, indicating that nearly half of the circulating supply is now held at a loss. This aligns with prior bear market environments where drawdowns approached the 50% threshold and broad investor cohorts were under pressure.

While downside risk has not fully dissipated, such elevated levels of supply in loss historically characterize the latter stages of bear cycles rather than their early phase. In structural terms, the market appears closer to a potential bottoming range than to the initial onset of contraction, even as volatility and fragility persist.

Large Holders Remain Passive

Against this backdrop of widespread unrealized losses, the sustainability of the current range hinges on renewed accumulation. Having traded largely between $60k and $70k throughout February, the direction of the eventual breakout will depend on the intensity of demand from new buyers.

The Accumulation Trend Score offers a useful gauge of this behavior, measuring relative balance changes across wallet cohorts while assigning greater weight to larger entities. Since February 5th, Accumulation Trend Score has remained capped below 0.5, signaling a lack of aggressive accumulation, particularly among large holders.

This subdued participation suggests that, despite elevated supply in loss, conviction-driven buying has yet to materialize. Until larger wallets shift toward sustained accumulation, the probability of further downside contraction remains elevated before a more durable bottoming structure can form.

Transition to Excess Loss

Reinforcing this muted accumulation backdrop, liquidity conditions have deteriorated further. The 90-day moving average of the Realized Profit/Loss Ratio, which compares the USD value of realized profits to realized losses, has now fallen below 1.0. This threshold is critical, as it marks the point where loss realization begins to dominate profit-taking, signaling a transition into an excess loss regime.

Historically, sustained breaks below 1.0 have persisted for six months or longer, reflecting prolonged periods of weak buy-side liquidity and constrained capital rotation. Only after a decisive reclaim of this level has the market typically entered a more constructive phase, characterized by renewed profitability and improving demand conditions.

Until the ratio stabilizes and trends back above 1, liquidity remains structurally impaired, limiting the probability of a durable recovery in the near term.

Off-Chain Insights

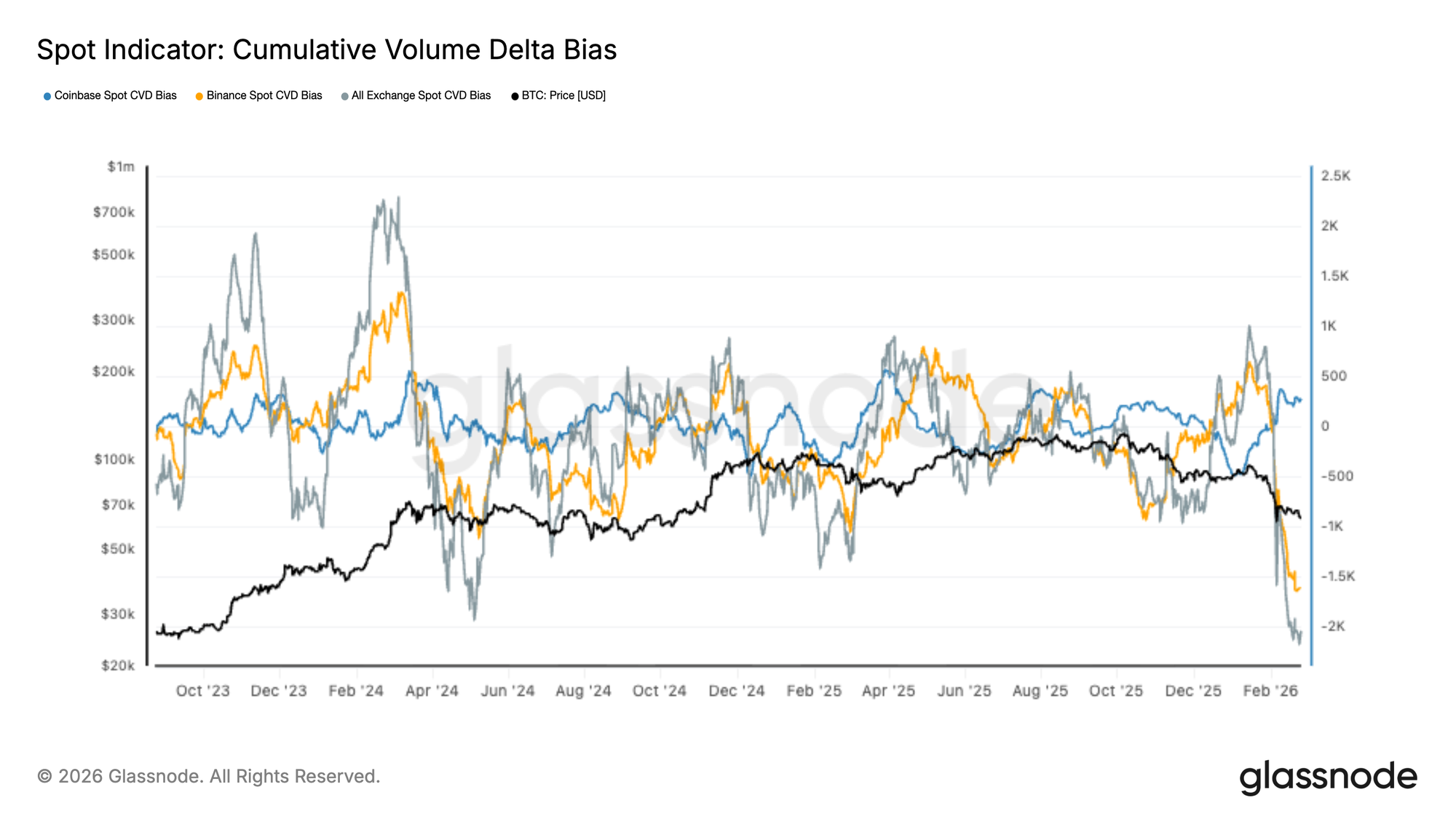

Spot CVD Bias Turns Sharply Negative

Spot markets have flipped decisively into sell-side dominance, with Cumulative Volume Delta (CVD) across all exchanges plunging to fresh cycle lows. Both Binance and aggregate spot flows show an aggressive wave of market sell orders, while Coinbase activity remains comparatively muted but unable to offset broader weakness.

The recent drawdown in price has coincided with one of the steepest negative CVD impulses of the past two years, suggesting the move lower is being driven by active distribution rather than passive liquidity gaps. Similar extremes in late 2023 and mid 2024 marked local exhaustion events, though follow-through depended on derivatives positioning and broader liquidity conditions.

With spot flows now deeply skewed to the sell side, the market appears reactive and fragile. Sustained recovery will likely require a clear shift back toward spot bid absorption, particularly across Binance and aggregate exchange flows, before constructive accumulation can be confirmed.

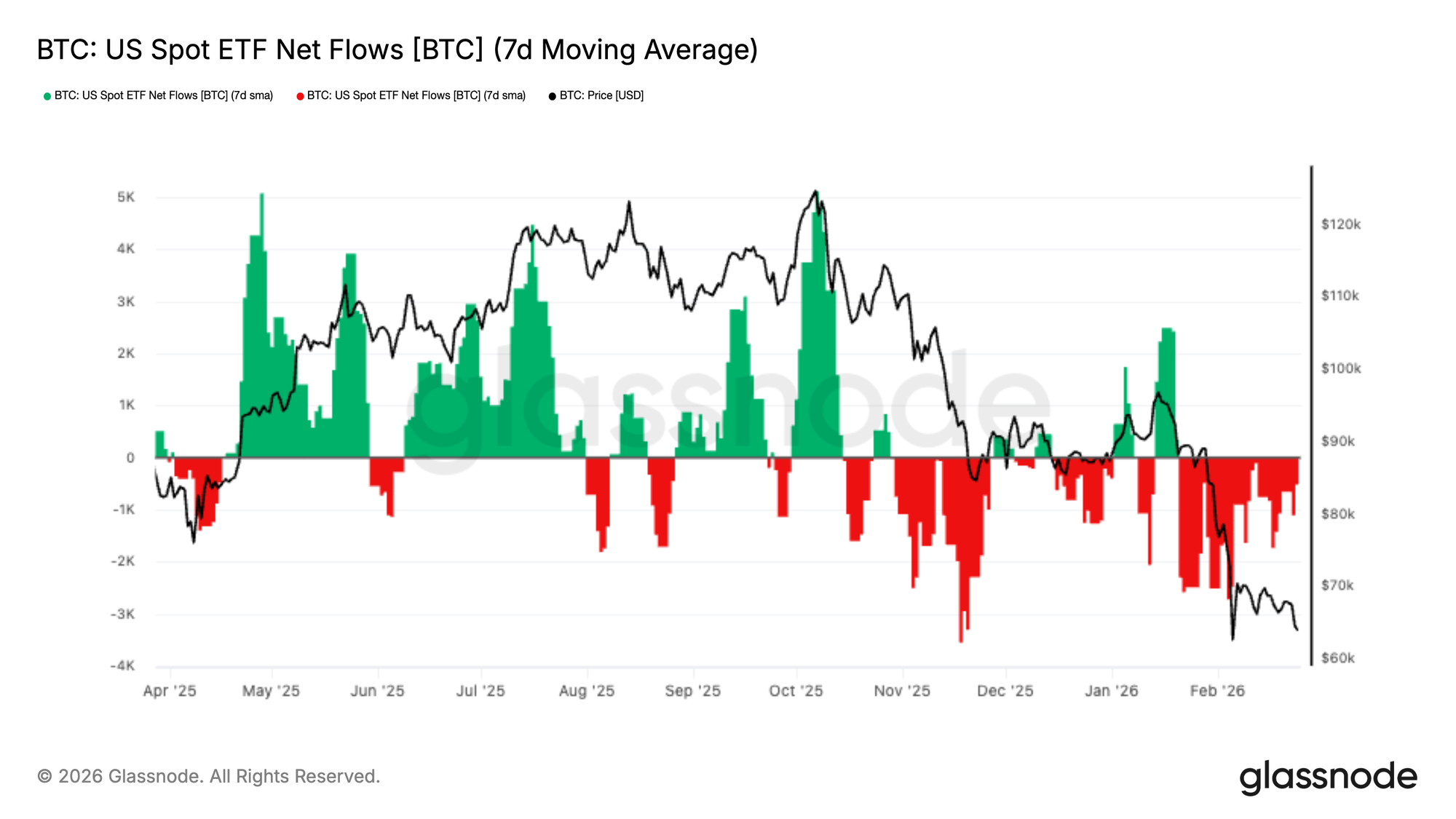

US Spot ETF Flows Extend Distribution Phase

US Spot ETF flows have remained firmly in net outflow territory, with the 7-day moving average printing a persistent series of red bars since late November. Recent weeks have seen renewed acceleration in outflows, coinciding with BTC’s breakdown toward the $60k–$70k range.

Earlier in the cycle, strong inflow impulses consistently aligned with price expansions, particularly through May and October. In contrast, the current regime is characterized by sustained redemption pressure and a lack of meaningful bid support from ETF allocators.

This shift suggests institutional demand has cooled materially, removing a key structural tailwind that supported prior rallies. Until flows stabilize or return to sustained net inflows, price action is likely to remain reactive and vulnerable to further downside pressure.

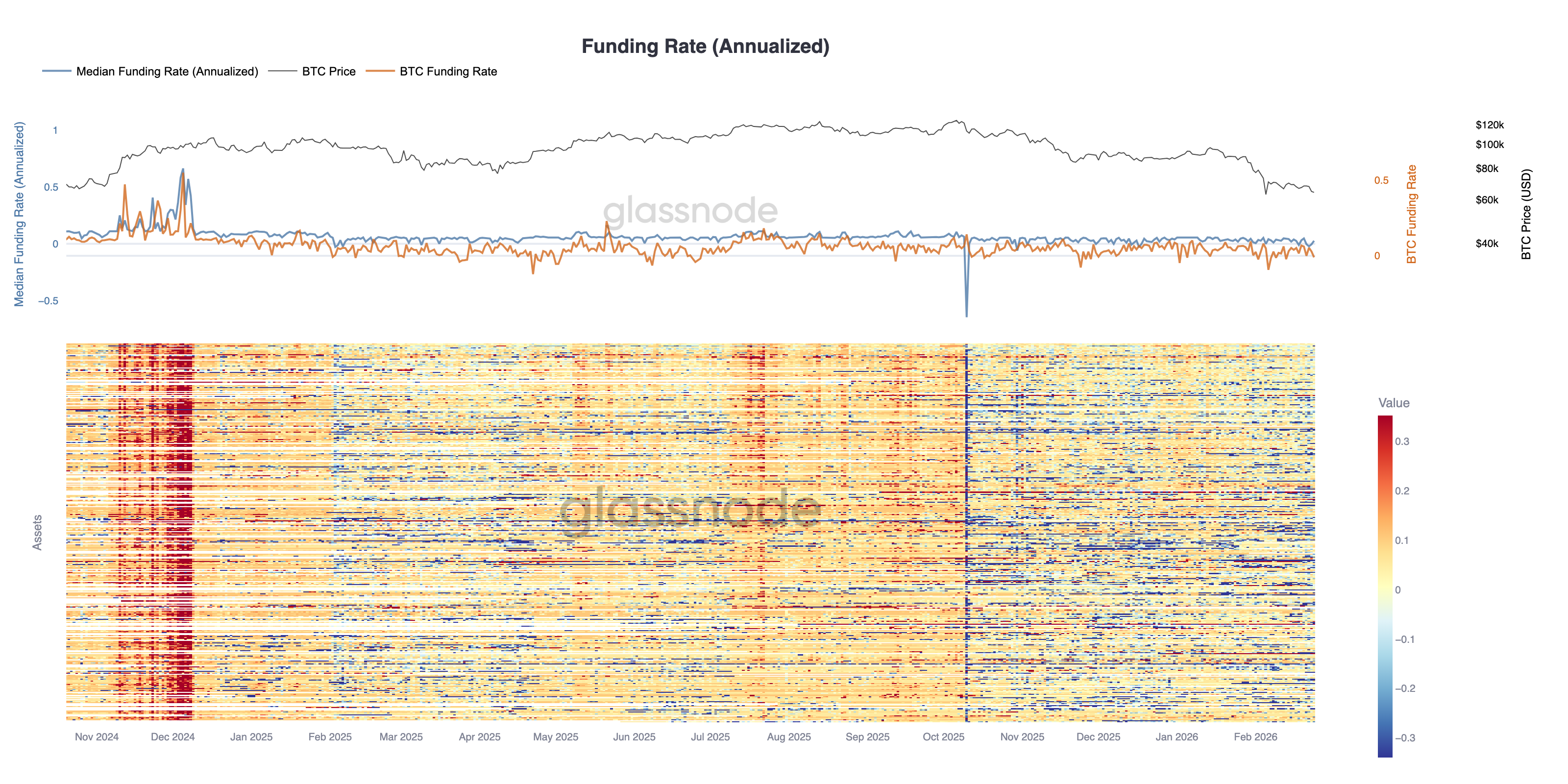

Funding Rates Remain Neutral

Perpetual futures funding has normalized materially, with the median annualized rate compressing back toward neutral after sustained positive readings through much of the prior rally. The recent price drawdown has coincided with a cooling in speculative positioning, as leveraged long exposure is gradually unwound.

The cross-asset heatmap highlights broad-based funding softness, with many instruments shifting from persistent positive prints to mixed or slightly negative territory. This stands in sharp contrast to late 2024, when elevated funding reflected crowded long positioning and aggressive directional conviction.

While the absence of extreme negative funding suggests limited panic-driven shorting, the lack of sustained positive prints also indicates muted risk appetite. Derivatives markets now appear more balanced, with leverage reduced and positioning less extended, leaving spot flows and structural demand as the key drivers for the next directional move.

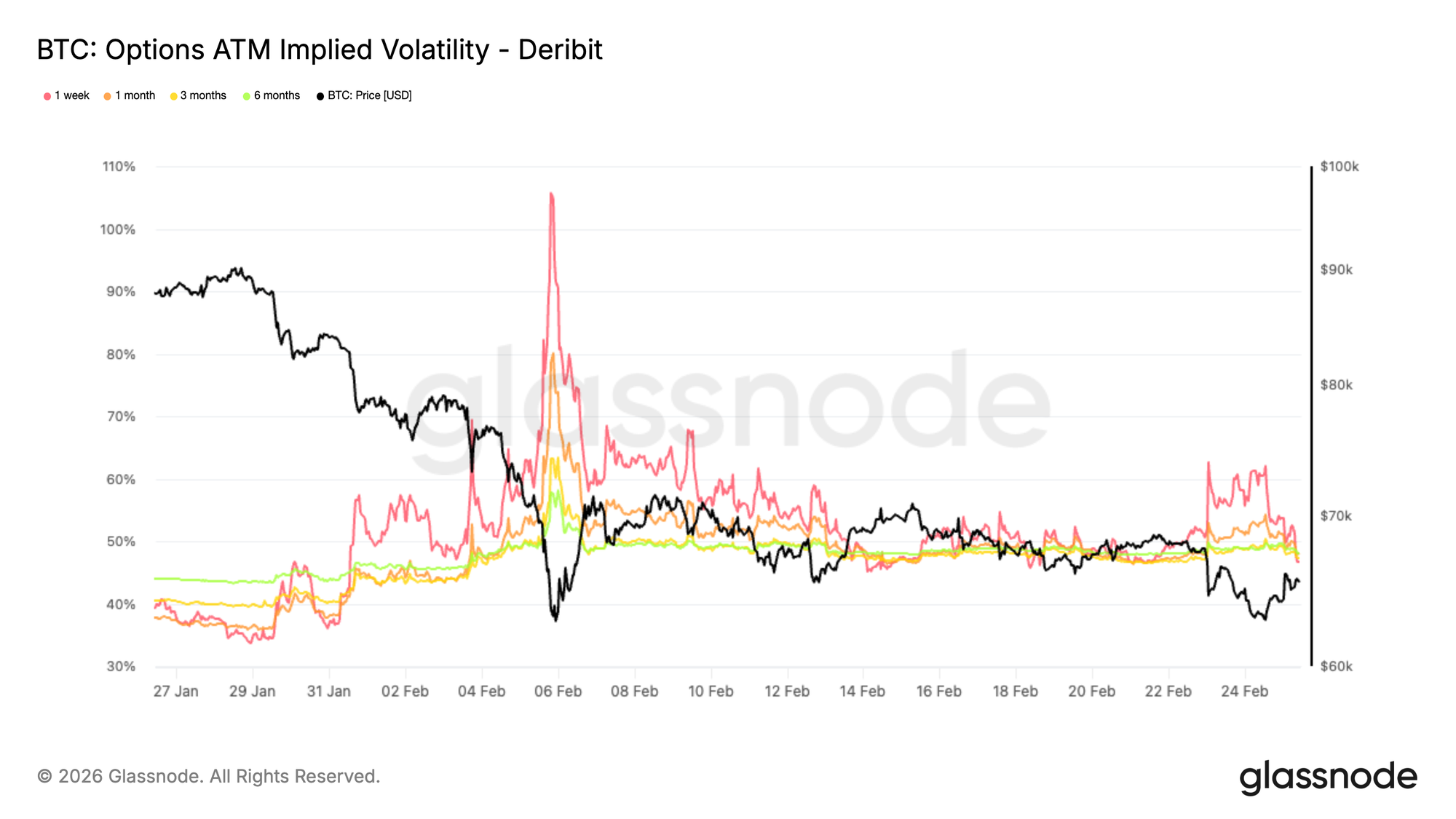

Implied Volatility Reacts but Fails to Expand

At the money implied volatility is elevated versus a month ago but not extreme, sitting around 47 percent across maturities.

In recent sessions, volatility briefly spiked as $BTC approached the 62K level, a zone that could have opened a move toward the high 50s if broken. One week ATM volatility jumped from 47 percent to 62 percent as traders rushed to hedge, recalling the sharp selloff earlier this month.

That repricing proved short lived. As price reclaimed 65K, one week volatility compressed back to 47 percent.

This rapid expansion and equally rapid compression highlights a highly reactive options market. Participants are quick to pay for short term protection near key levels, but just as quick to unwind it when the immediate threat fades.

The result is a mean reverting volatility backdrop, where fear spikes are not yet translating into sustained volatility expansion.

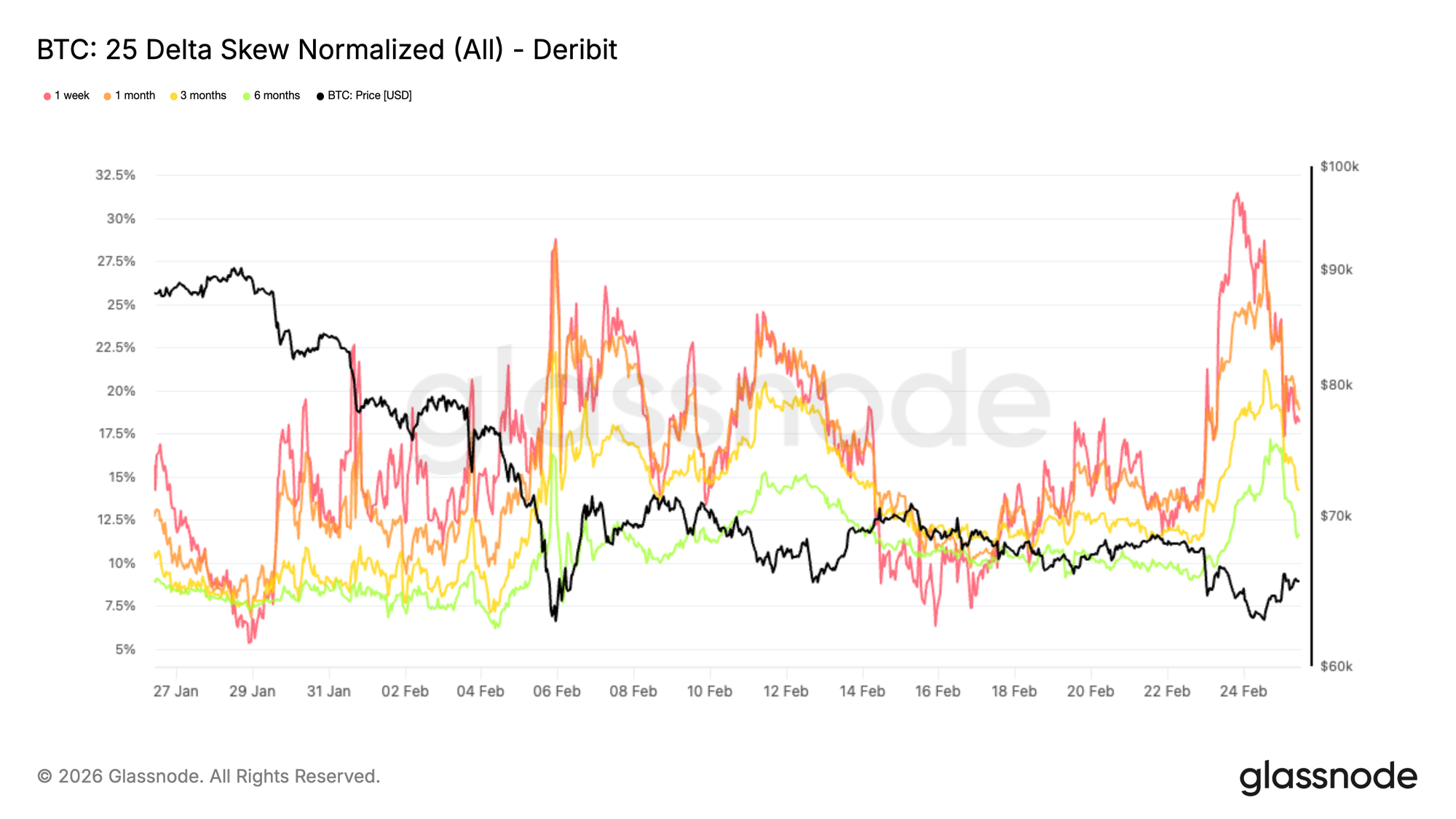

25 Delta Skew Signals Renewed Downside Fear

While implied volatility has remained contained overall, 25 delta skew tells a more defensive story. This metric measures the price difference between downside puts and upside calls, highlighting whether protection or upside exposure is in greater demand.

Skew has once again reached extreme asymmetry, approaching levels last seen on February 5 during the sharp drop toward 60K. At that time, the speed and amplitude of the move caught traders off guard, triggering late stage hedging and pushing puts to trade at a 28 percent premium over calls.

In recent sessions, put skew has climbed toward 30 percent. Each test of the lower end of the range has revived demand for protection, with participants using rebounds to rebuild downside hedges.

This persistent richness in puts reflects a market willing to pay up for insurance, reinforcing a clearly defensive positioning bias.

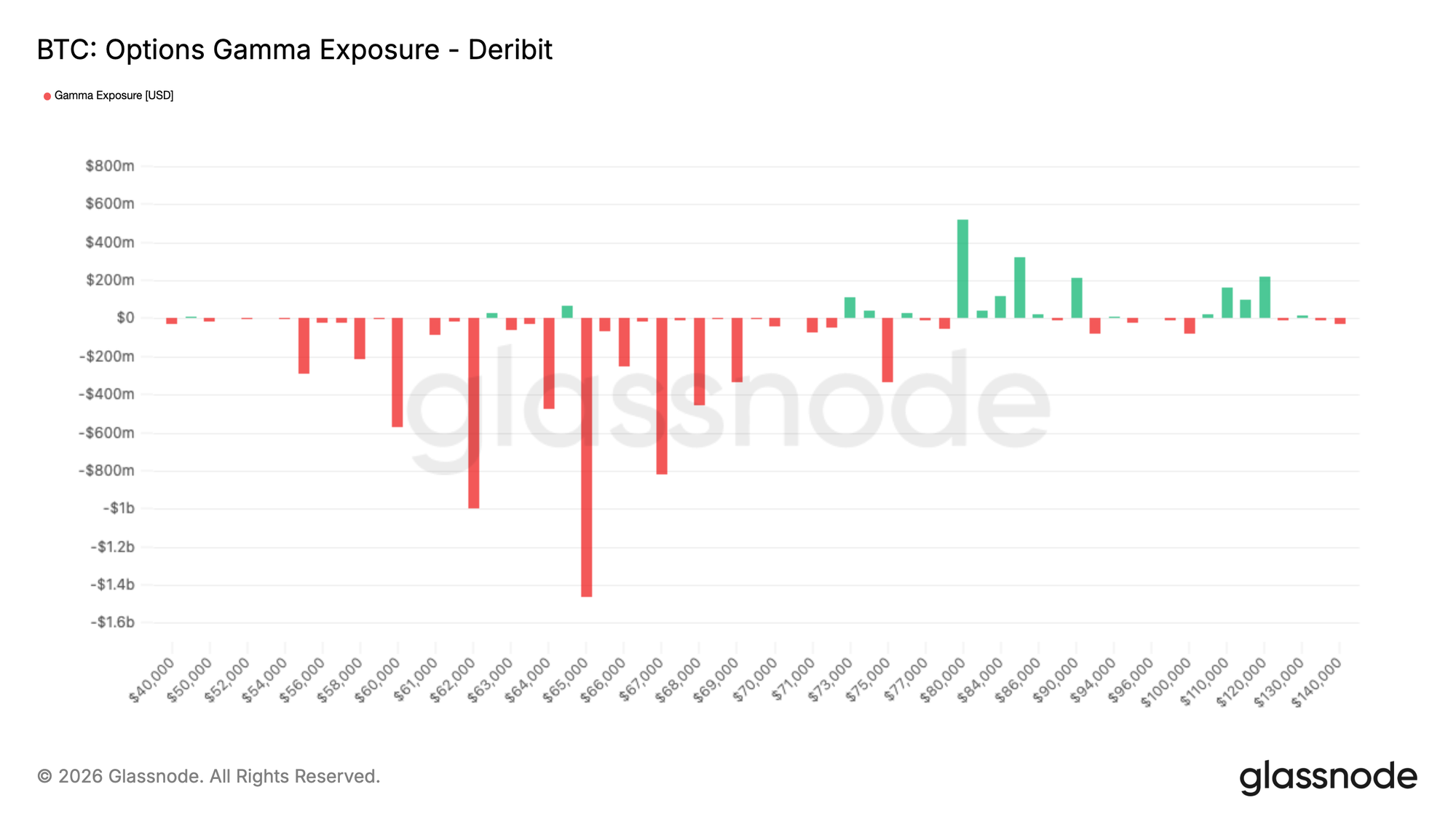

Options Gamma Exposure Remains Net Short

That persistent demand for protection is mirrored in current gamma positioning. Across expiries, the market sits inside a broad short gamma corridor between 70K and 55K, leaving the structure inherently fragile within this range.

The 65K strike stands out, with roughly 1.5 billion dollars of negative dealer gamma concentrated there. This pocket expires entirely this Friday, making it especially relevant in the short term. A move lower into expiry could trigger accelerated hedging flows as dealers sell futures to remain delta neutral. At the same time, once expiry passes, those hedges are unwound. Dealers would buy back futures, which can mechanically ease pressure and create temporary relief.

Further out, end of March expiries carry roughly 650 million dollars of negative gamma at 62K and 830 million dollars at 60K, extending structural sensitivity over the coming weeks.

Short gamma does not determine direction, but it increases the likelihood that moves, once underway, become sharper and more self reinforcing.

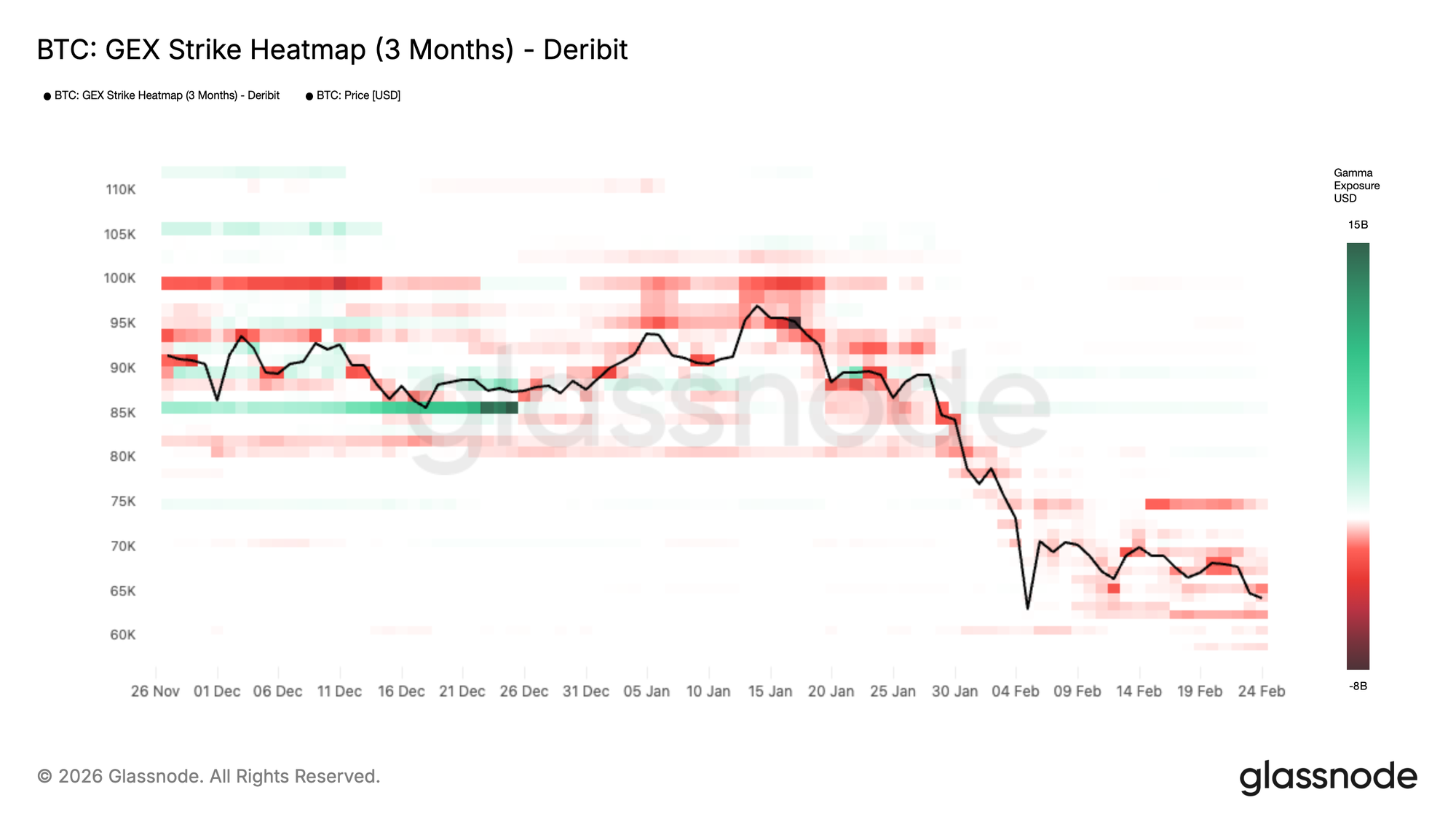

GEX Heatmap Highlights Structural Regime Shifts

While current positioning shows a net short gamma environment, the GEX Heatmap helps place this in a broader structural context.

This chart tracks how dealer gamma exposure has evolved over the past three months, highlighting zones where volatility is mechanically suppressed or amplified.

In December, clear positive gamma bands appeared around 85K, shown in green. These acted as classic gamma walls. Dealers were structurally long gamma, incentivized to sell strength and buy weakness. That flow dampened volatility and helped anchor price within a tight range. The wall did not break. It simply rolled off as year end options expired, removing the stabilizing effect and allowing the structure to reset.

More recently, the heatmap shifted toward deeper red bands during the January to February decline. Expanding negative gamma around and below spot signaled a regime where dealer hedging reinforced the move, allowing volatility to expand and momentum to accelerate.

Conclusion

Bitcoin remains in a structurally defensive consolidation phase. While price continues to find support within the $60k–$69k demand zone, on-chain profit compression, weak breadth, and moderated large-holder accumulation highlight fragile conviction beneath the surface.

Spot sell pressure and sustained ETF outflows confirm that structural demand remains constrained, even as derivatives positioning has reset and panic hedging has faded. The market is stabilizing, but not yet strengthening.

For a durable upside recovery to emerge, renewed spot absorption, sustained large-entity accumulation, and a clear shift in institutional flows will be required. Until then, range-bound price action between key valuation anchors remains the dominant structural theme.

Disclaimer: This report does not provide any investment advice. All data is provided for informational and educational purposes only. No investment decision shall be based on the information provided here, and you are solely responsible for your own investment decisions.

Exchange balances presented are derived from Glassnode’s comprehensive database of address labels, which are amassed through both officially published exchange information and proprietary clustering algorithms. While we strive to ensure the utmost accuracy in representing exchange balances, it is important to note that these figures might not always encapsulate the entirety of an exchange’s reserves, particularly when exchanges refrain from disclosing their official addresses. We urge users to exercise caution and discretion when utilizing these metrics. Glassnode shall not be held responsible for any discrepancies or potential inaccuracies.

Please read our Transparency Notice when using exchange data.