Supply Cleared, Conviction Pending

Bitcoin has rebounded toward ~$74k as ETF inflows and spot demand recover. Shorts remain crowded with negative funding, while easing options stress suggests improving conditions but still early conviction.

Executive Summary

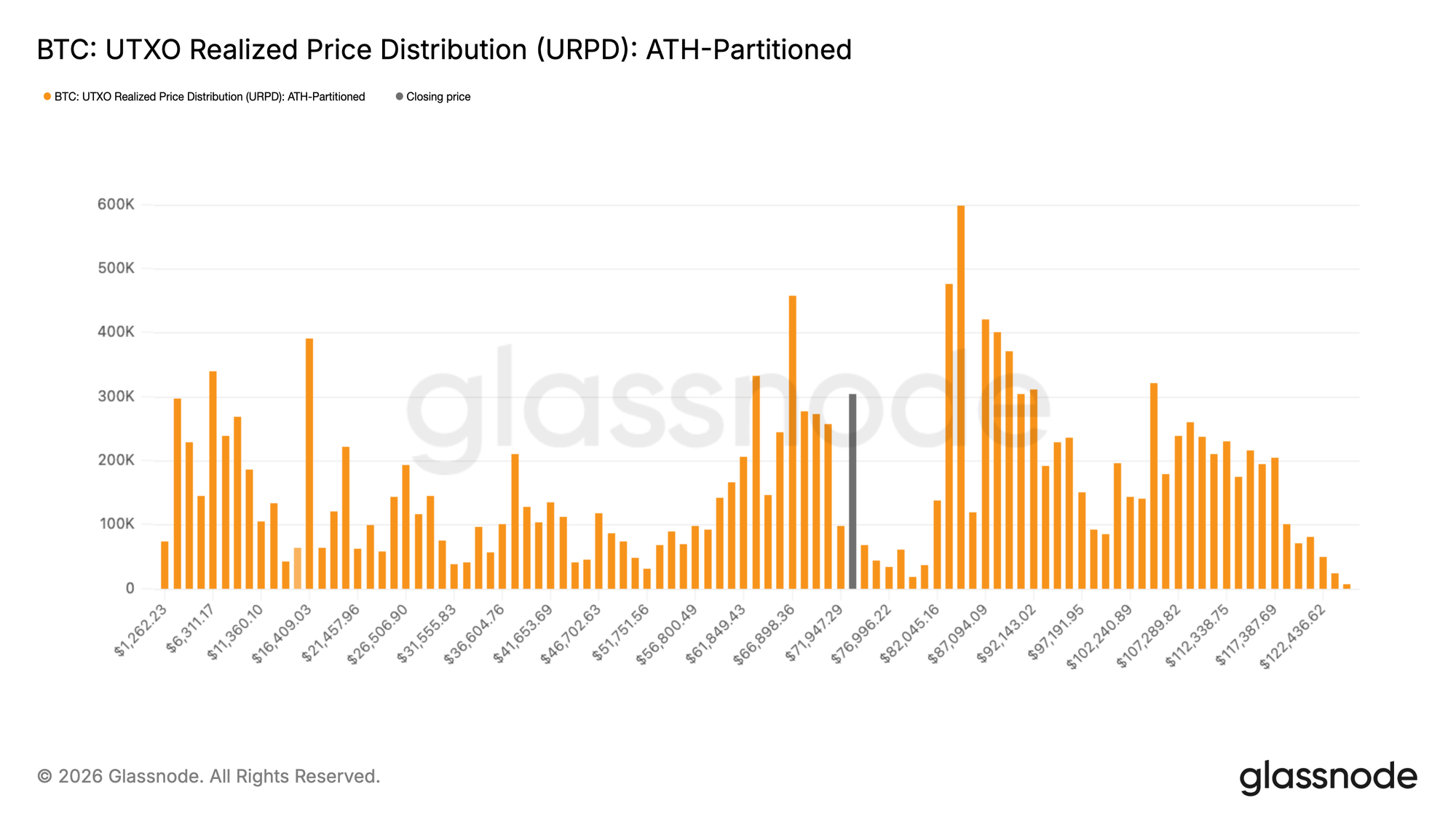

- Bitcoin has broken above $70k and entered a thinly accumulated air gap between $72k and $82k, with URPD confirming limited on-chain resistance until the upper band near $82k.

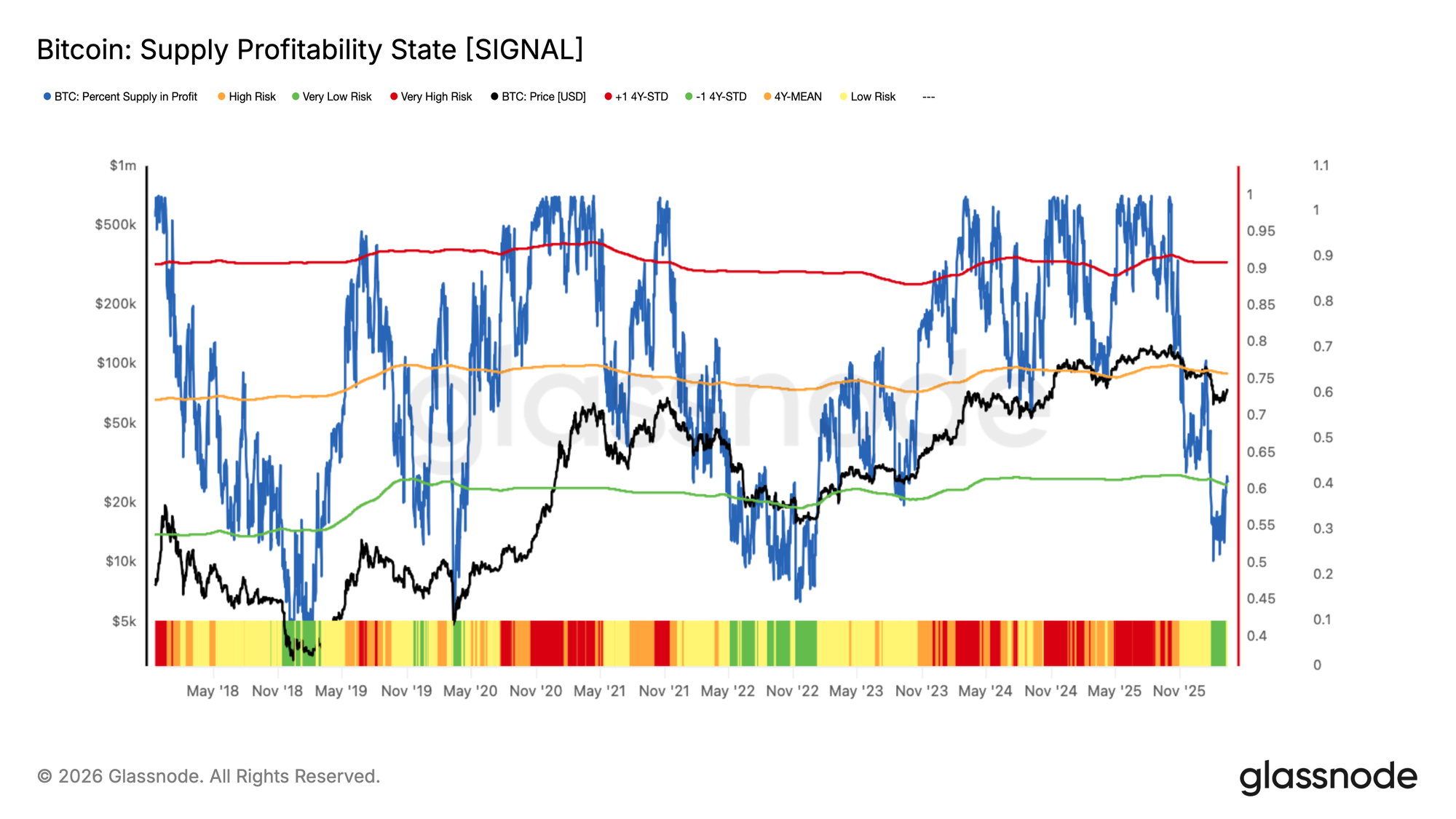

- The Percent of Supply in Profit has recovered to approximately 60%, a level historically associated with first-bounce exhaustion at prior cycle bottoms, with a sustained move above 75% required to confirm a genuine bull market transition.

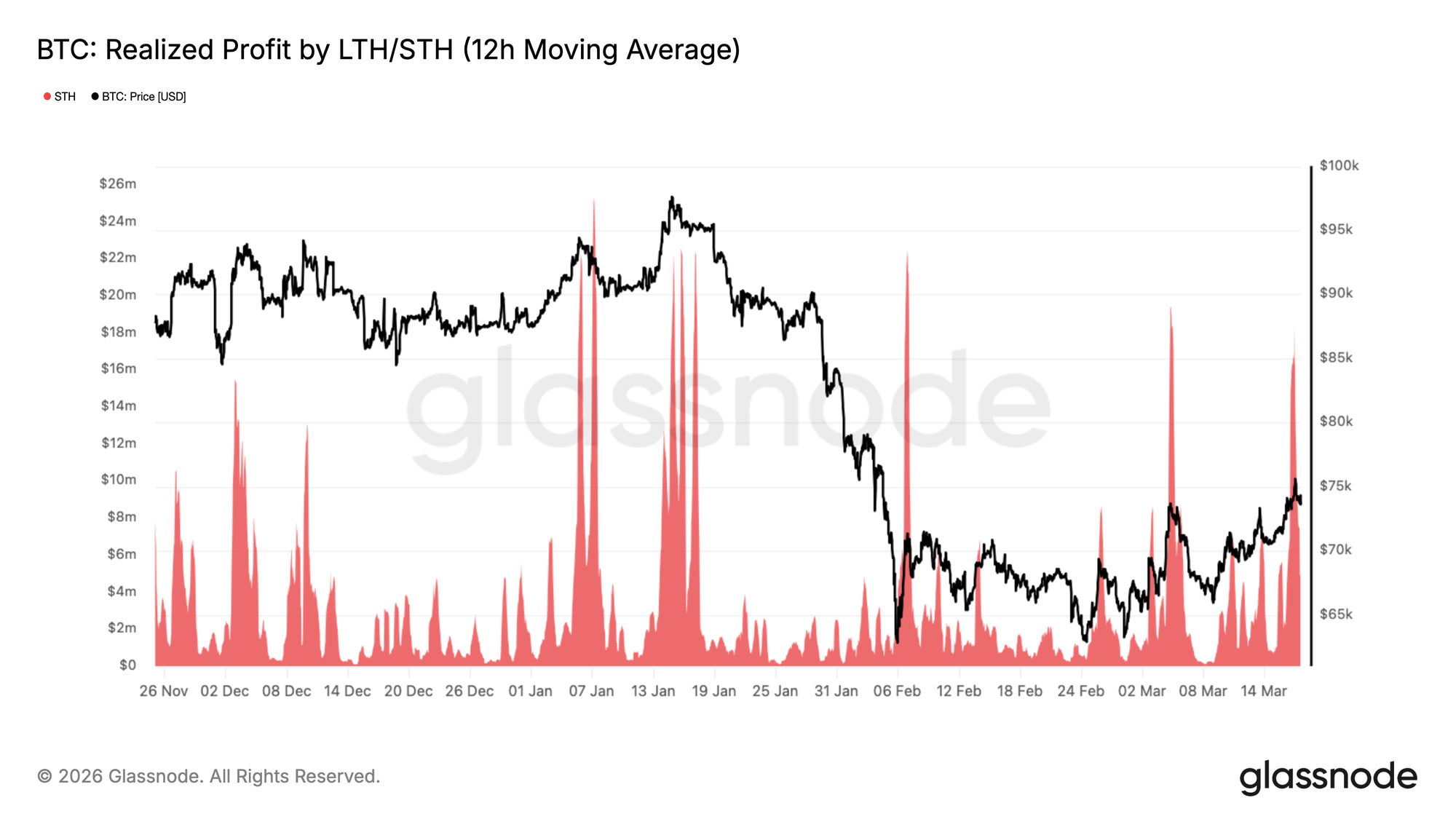

- STH Realized Profit spiked to $18.4M per hour as price approached $74k, echoing February's pattern of short-term holders selling into strength. Digesting this pressure above $70k is the key condition for extending toward $78k–$82k.

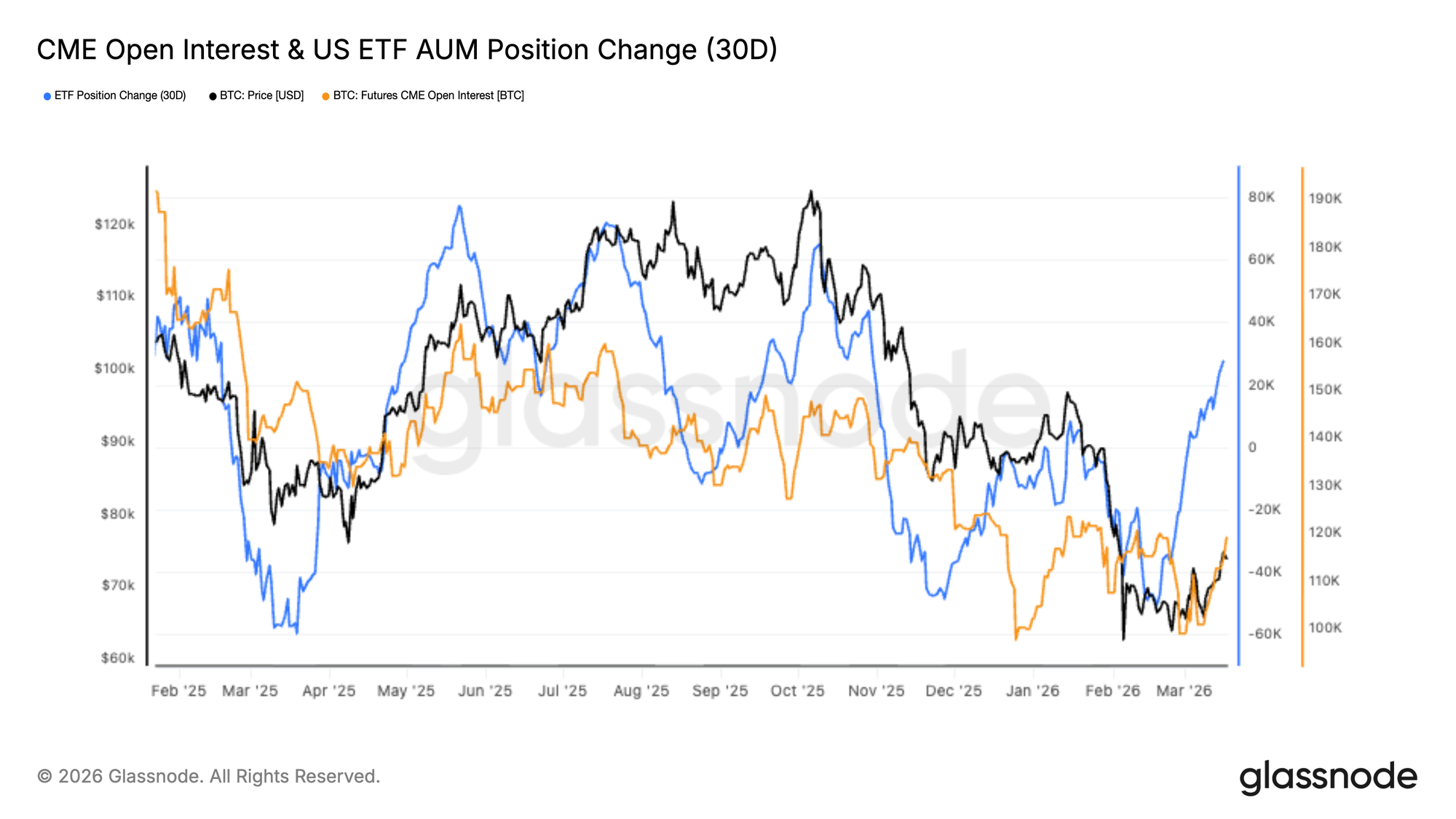

- ETF inflows have rebounded over the past month, marking a renewed wave of institutional demand and supporting the shift back toward spot-led market strength.

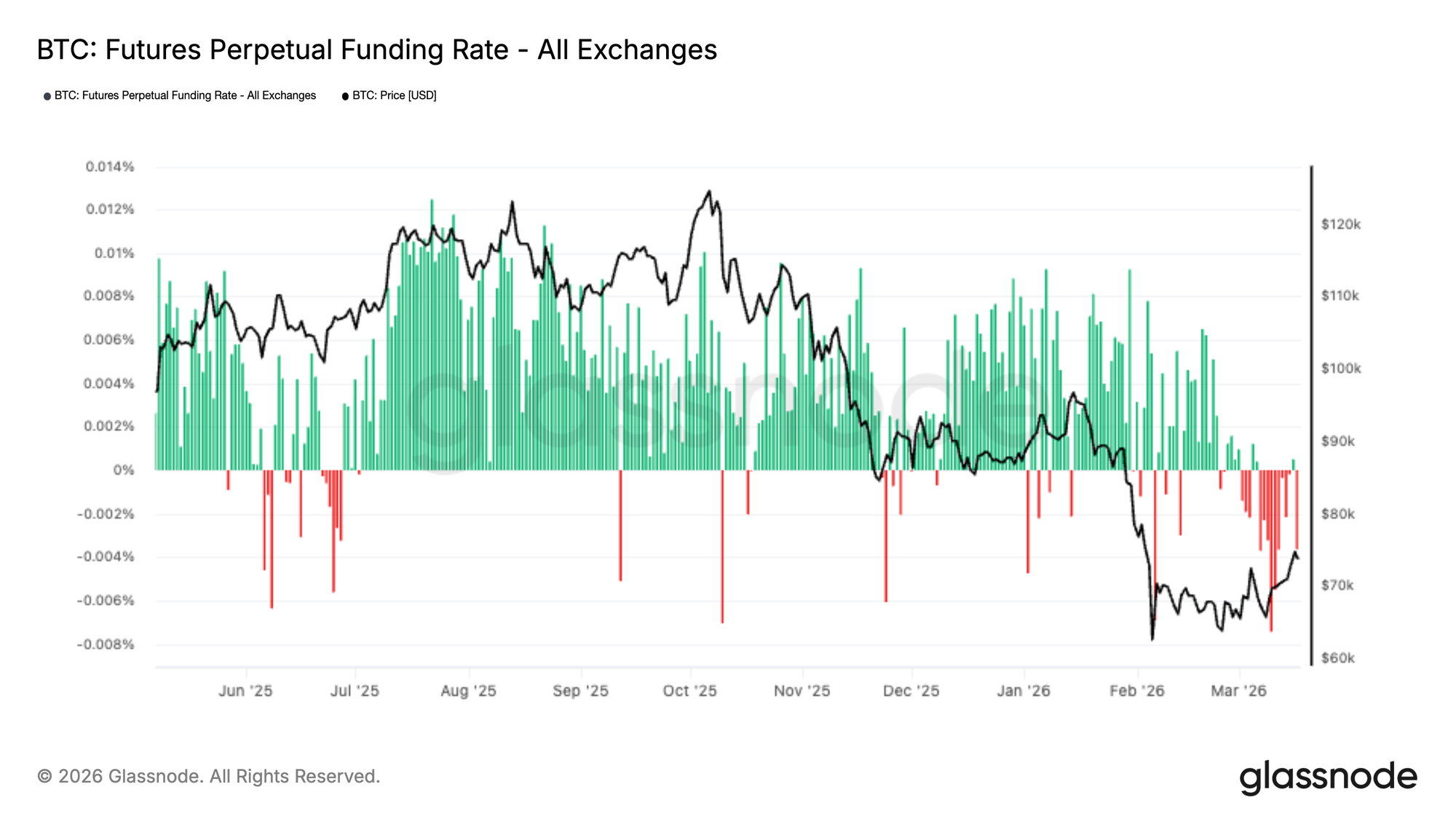

- CME futures positioning remains subdued, indicating the recovery is being driven primarily by spot flows rather than leveraged speculation.

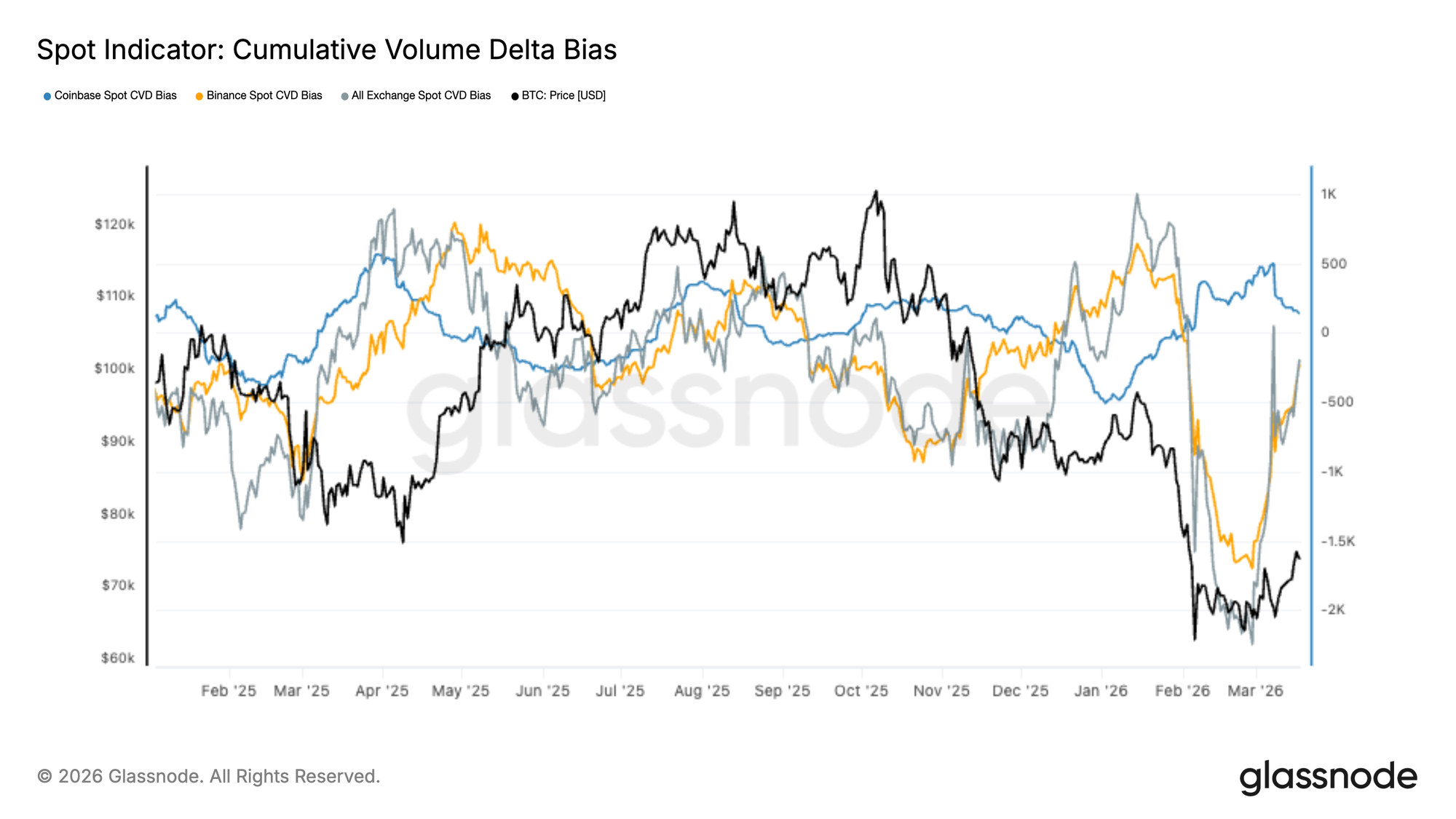

- Spot CVD has reversed higher across major exchanges, signalling a transition from sustained sell pressure toward renewed accumulation.

- Coinbase spot activity has stabilised and turned positive, pointing to early-stage institutional re-engagement. Binance-led sell pressure has eased materially, removing a key source of downside momentum observed during the recent drawdown.

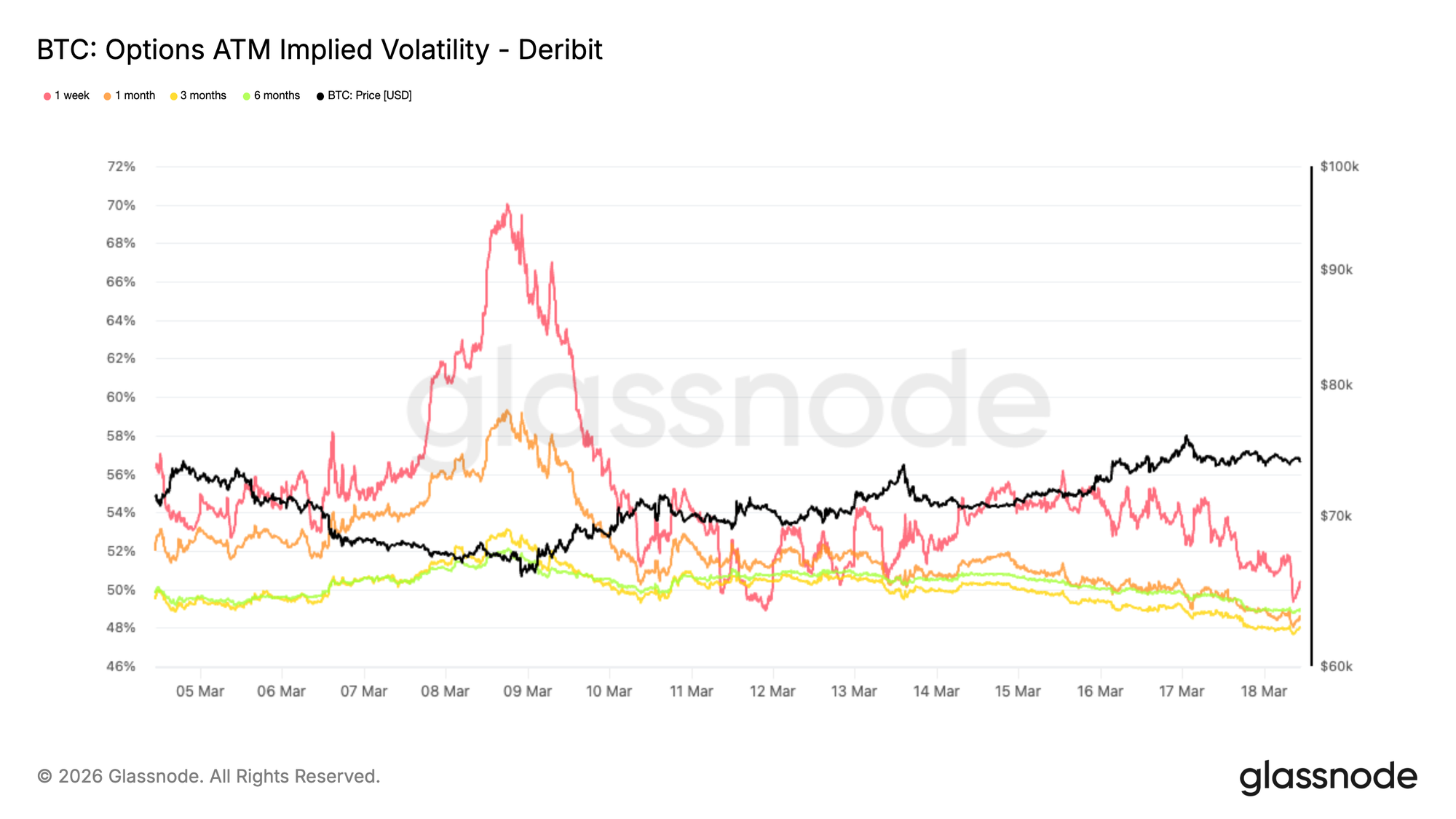

- Implied volatility has declined across tenors, reflecting a reduction in hedging demand and a normalisation in market conditions.

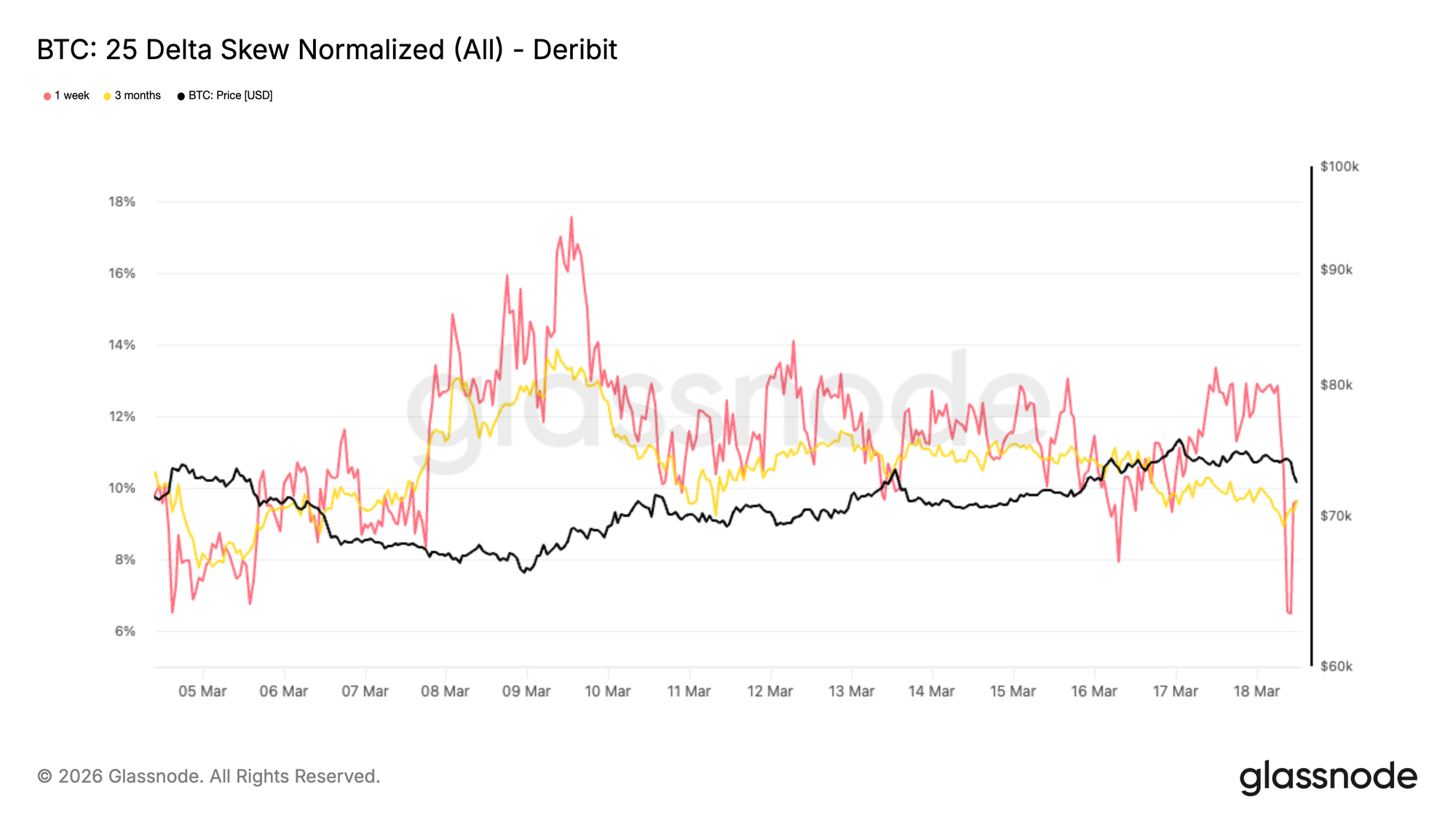

- Options skew has turned slightly positive, suggesting a modest shift toward upside positioning and improving sentiment.

- Dealer gamma positioning remains near neutral, indicating limited options-driven volatility amplification in the near term.

This report is also available for download in PDF format.

On-Chain Insights

Breaking Out of the Cluster

After weeks of failed attempts to reclaim the $70k level, Bitcoin has pushed above the upper bound of its February-March range, now trading near $74k. This move is contextualized by the UTXO Realized Price Distribution (URPD), which maps the volume of circulating supply against its on-chain acquisition cost, effectively revealing where coins were accumulated and at what price.

The current distribution shows a dense supply cluster between $59k and $72k, built predominantly across February and March 2026, which price has now cleared. Bitcoin has edged into a relative air gap between $72k and $82k, a zone thinly populated by prior accumulation and therefore offering limited technical resistance. This breakout, occurring against a backdrop of ongoing geopolitical uncertainty and broader market resilience, suggests investors are provisionally treating macro headwinds as temporary. Regardless of longer-term resolution, the $72k–$82k air gap defines the most probable trading range in the short-term.

One Bounce Does Not Make a Bull

While the breakout above $70k and the subsequent move into the $72k–$82k air gap are encouraging, a single constructive price push falls short of confirming a decisive structural shift. A broader assessment of market health requires examining investor profitability, a dimension best captured by the Percent of Supply in Profit, which measures the share of circulating Bitcoin supply currently held at an unrealized gain.

Historically, recoveries from deep bear markets into early bull market conditions have been validated by this indicator climbing from below its -1 standard deviation threshold near 60% toward its long-run mean of approximately 75%. The recent price move has lifted this metric to around 60%, a level consistent with comparable early bounces in prior cycle bottoms, where market exhaustion at first recovery attempts was a common feature. A sustained push above 75% would carry considerably more weight as a confirmation of early bull market conditions, whereas continued rejection near current levels would reinforce the bear market recovery narrative.

Watching the Market Digest Sell Pressure

Beyond the breadth of unrealized profitability, a complementary lens is how the market absorbs the wave of profit-taking that typically accompanies price recovery. If sell pressure from recent buyers is digested without a structural breakdown back into the $59k–$72k accumulation cluster, the probability of extending toward higher levels strengthens considerably. As price edged above $74k this week, the 12HR-SMA of STH Realized Profit spiked to $18.4M per hour, echoing the pattern observed throughout February where short-term holders consistently exhausted rallies above $70k, selling into strength before any sustainable breakout could develop.

This dynamic is a natural feature of early recoveries in bear market regimes, where recent buyers prioritize exit over conviction. Should the market successfully digest this sell pressure and hold above $70k in the coming weeks, higher targets, including the True Market Mean at $78k and the upper band of the current air gap near $82k, would become increasingly probable objectives.

Off-Chain Insights

Early Signs of Institutional Re-Entry

Bitcoin’s recent recovery has been accompanied by a sharp rebound in US spot ETF allocations, with 30-day position change accelerating higher after a prolonged period of outflows. This marks a clear shift in institutional demand, with capital rotating back into spot exposure as price reclaims higher levels.

At the same time, CME futures open interest remains relatively subdued, only beginning to stabilise after a sustained decline. This divergence suggests that the current move is being driven more by real spot demand rather than leveraged positioning. Historically, this type of structure reflects healthier market conditions, where price appreciation is supported by capital inflows rather than speculative excess.

The combination of rising ETF AUM and still-muted futures positioning indicates early-stage re-engagement from institutional investors. Should CME open interest begin to expand alongside ETF inflows, it would signal growing conviction and potentially reinforce the strength of the current uptrend.

Spot Demand Returns

Spot Cumulative Volume Delta (CVD) has staged a notable recovery across major exchanges, following an extended period of aggressive sell-side pressure. The sharp negative imbalance observed during the recent drawdown, particularly on Binance, has begun to reverse, signalling a shift back toward net buyer dominance.

This inflection aligns with Bitcoin’s rebound from the ~$60k lows, suggesting that the move higher is being supported by genuine spot demand rather than purely derivatives-driven flows. Coinbase CVD, often used as a proxy for institutional activity, has stabilised and is trending higher, reinforcing the case for renewed accumulation.

The broad-based recovery across exchanges indicates improving market depth and buyer conviction. While not yet at euphoric levels, this transition from distribution to accumulation suggests that spot markets are once again providing structural support for price, a key ingredient for a more sustainable recovery phase.

Perp Funding Shows Short Bias

Perpetual futures funding rates have shifted decisively into negative territory in recent weeks, reflecting a growing dominance of short positioning across derivatives markets. This build-up in bearish exposure occurred as Bitcoin traded within the ~$60k–$70k range, reinforcing downside expectations among leveraged traders.

However, the most recent price breakout toward ~$74k has occurred against this backdrop of persistent negative funding, highlighting a key divergence. This suggests that the move higher is being driven, at least in part, by short covering rather than aggressive long positioning.

Such conditions typically indicate a crowded short trade, where positioning becomes vulnerable to squeezes. As price pushes higher, forced liquidations can act as fuel for continuation. While this dynamic supports near-term upside, a sustained trend will likely require funding to normalize and a more balanced positioning structure to emerge.

ATM Implied Volatility Normalizing

Bitcoin's volatility shock is fading. One week implied volatility has dropped sharply over the past week, falling from around 56% earlier in the week to roughly 50% at the time of writing, while longer maturities have declined by about three volatility points across the curve.

This shift signals that traders are no longer pricing the same level of immediate uncertainty, and the earlier spike in volatility that accompanied recent market stress has now eased. Lower implied volatility typically reflects a market transitioning from a reactive phase into a more stable regime.

The current structure suggests traders are gradually moving away from panic hedging. We have seen significant unwinding of downside protection, which has participated in easing implied volatility levels and helped shape the current relief rally. The market is now moving toward a more balanced near-term outlook where the most favorable path may be higher, as price action becomes increasingly shaped by options hedging dynamics in an environment of low liquidity across both spot and derivatives markets.

25 Delta Skew Moving Toward Neutral

Following the normalization in implied volatility, skew has also started to adjust. The 25 delta skew remains negative, currently around 10% across expiries, down 7 to 4 vol points from recent highs.

Negative skew means downside protection remains relatively expensive compared with calls, reflecting persistent demand for protection and the reluctance of market makers to sell downside volatility too cheaply.

However, skew is gradually moving into less negative territory. This shift indicates that demand for downside hedging is starting to ease as traders reduce defensive positioning.

In practical terms, puts are becoming less expensive relative to calls. This type of adjustment typically appears when markets begin reopening the door to upside positioning while the broader macro backdrop remains uncertain and sentiment still cautious.

Current skew dynamics suggest the market is moving away from panic protection toward a more balanced options structure while positioning for a potential tactical rally.

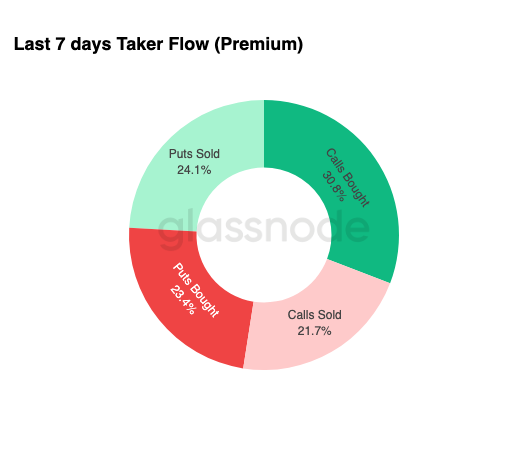

Options Flow Turning Gradually Positive

This shift in sentiment is also visible in recent options flow. Delta positive trades accounted for 54.9% of activity, with call buying leading the charge at 30.8% of total flow.

Trading activity over the past sessions shows increasing demand for call options, instruments typically used to gain exposure to upside moves while limiting downside risk.

At the same time, the market has registered substantial unwinding of downside protection. As traders close hedges, market makers often need to buy back exposure, creating buyback flows that have helped support the recent price move higher.

Such dynamics often characterize transitional phases. Participants begin positioning for recovery while still keeping some defensive structures in place, producing a cautious but increasingly constructive options flow profile.

Whether this shift reflects a structural change in positioning or simply short-term opportunistic activity remains to be seen.

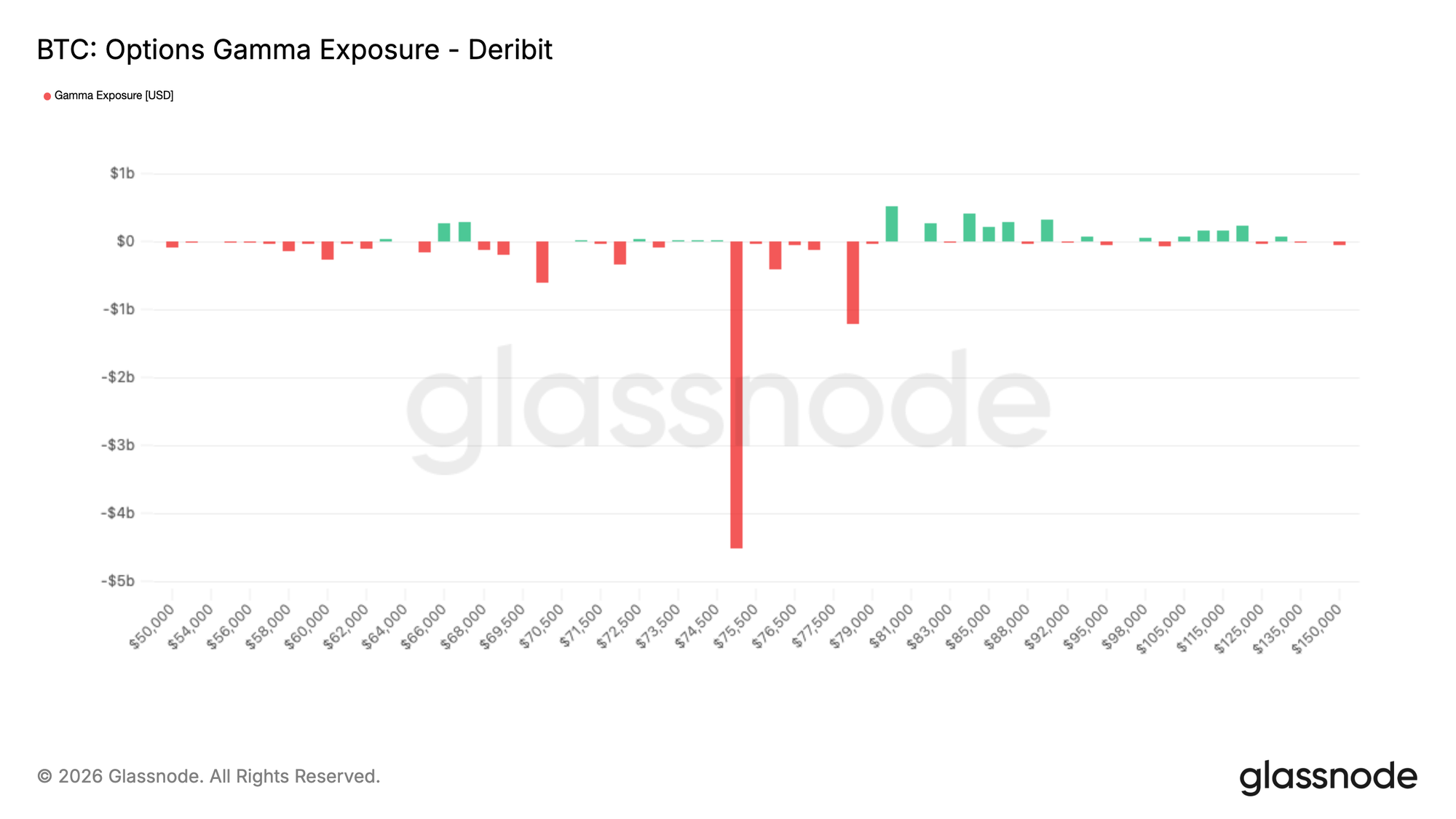

Negative Gamma Concentrated at $75K

Zooming in on one of the most important metrics to watch: dealer gamma exposure. With the market operating on low volumes, dealer hedging flows can move price toward strikes that act as magnets.

The only meaningful strike at the moment is $75K, where roughly $4.5B of negative gamma is concentrated. As Bitcoin consolidates just below this level, a small move higher could trigger dealer buying flows as they hedge positions moving in the money, potentially fueling a move toward the high $70s.

The $75K level remains key into the March options expiry, where $3.9B of the $4.5B negative gamma is set to expire. Once the end of Q1 expiry passes, the unwinding of dealer hedges could create headwinds for further upside and contribute to consolidation or a pullback as the market shifts from a hedging driven dynamic back toward a broader macro narrative.

Conclusion

Bitcoin’s recovery toward the mid-$70k range is increasingly underpinned by improving spot market conditions, with ETF inflows and positive CVD trends signalling renewed accumulation across both institutional and retail participants. This shift marks a transition away from the distribution-heavy environment that defined the recent drawdown, providing a more constructive foundation for price.

At the same time, derivatives markets remain defensively positioned. Persistent negative funding rates point to crowded short exposure, which has likely contributed to the recent upside via short covering. Meanwhile, options markets show signs of stabilisation, with declining volatility and a modest positive skew reflecting improving sentiment without excessive risk-taking. Together, this positioning backdrop suggests further upside may be supported in the near term, though a sustained trend will likely require continued capital inflows and a broader expansion in leverage and conviction.

Disclaimer: This report does not provide any investment advice. All data is provided for informational and educational purposes only. No investment decision shall be based on the information provided here, and you are solely responsible for your own investment decisions.

Exchange balances presented are derived from Glassnode’s comprehensive database of address labels, which are amassed through both officially published exchange information and proprietary clustering algorithms. While we strive to ensure the utmost accuracy in representing exchange balances, it is important to note that these figures might not always encapsulate the entirety of an exchange’s reserves, particularly when exchanges refrain from disclosing their official addresses. We urge users to exercise caution and discretion when utilizing these metrics. Glassnode shall not be held responsible for any discrepancies or potential inaccuracies.