How Many Bitcoin Are For Sale?

With a gold rush of applications for a Bitcoin ETF filed this week, a key question is, how many Bitcoin are active and available for sale? In this report, we try to measure the available supply, and assess how demand impacted valuations in past cycles.

Executive Summary

- Analyzing the fund flow attributed to top exchanges in the US and Asia, shows a strong accumulation during Asia trading hours, while the US markets have shown weaker demand in 2023.

- Employing a framework introduced in this article, we identify periods of demand expansion (or contraction) using the concept of ‘hot supply’, which isolates the coin volume actively participating in price discovery.

- Analysis of short-term holder behavior in 2023 suggests market psychology has shifted from the bearish environment of 2022, with the recent rally springing off their cost basis, which acted as support.

🪟 View all charts covered in this report in The Week On-chain Dashboard.

Regional Sentiment Analysis

In recent weeks, the SEC has been applying pressure to the top two cryptocurrency exchanges in the US. However, this week saw a gold rush of spot Bitcoin ETF applications lead by Blackrock, the largest global asset manager. In response, BTC has rallied from $25k to over $31k, reaching new yearly highs.

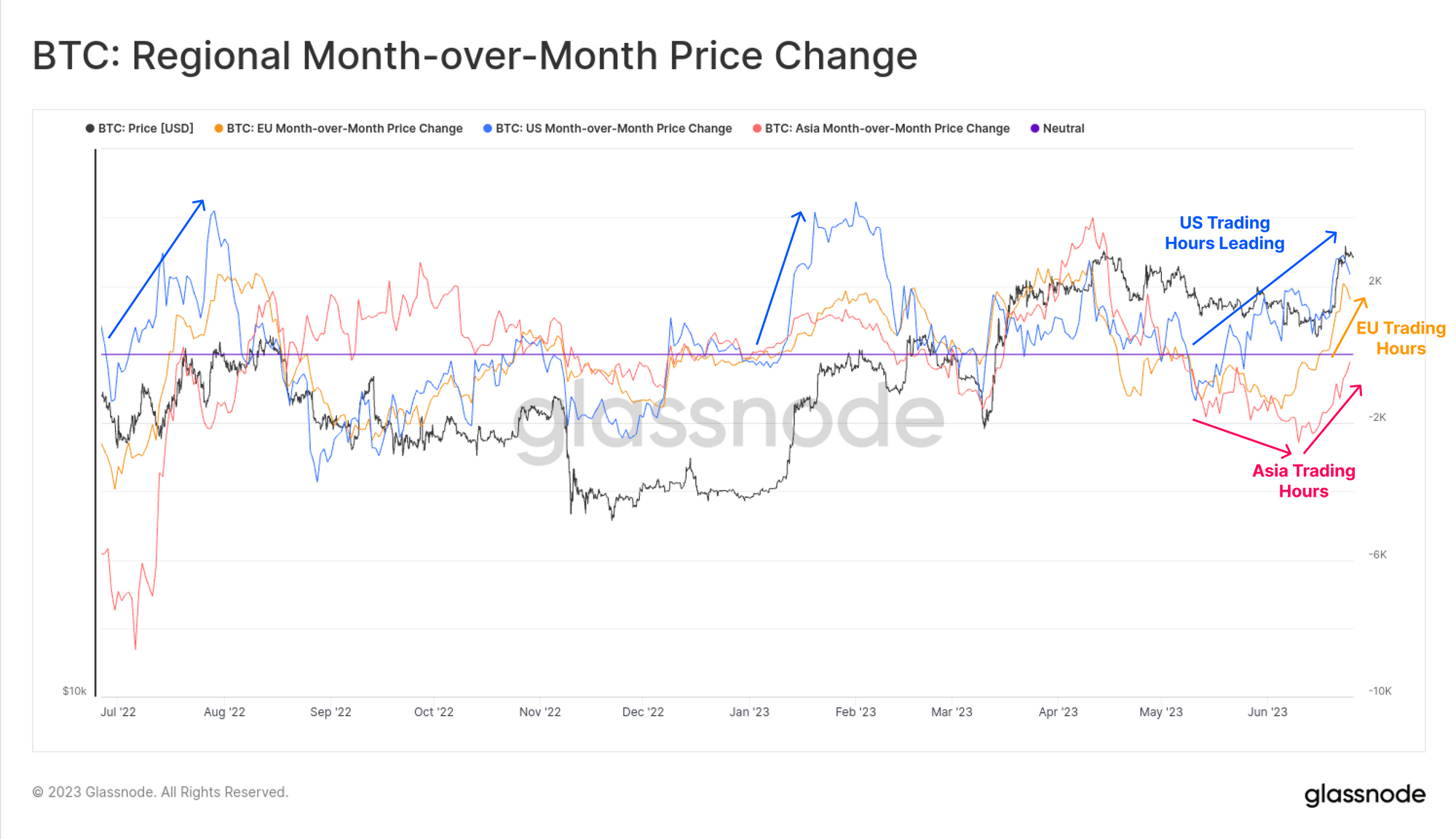

The rally was led by traders in US 🔵, followed by traders in EU 🟠, and lastly in Asia 🔴.

We can explore a framework for these regional shifts by assessing coin flows through fiat on-ramping entities (exchanges). To achieve this, we have isolated the top three exchanges from the US and Asia regions as ranked by CoinGecko.

US (On-shore): Coinbase, Kraken and Gemini

Asia (Off-shore): Binance, OKX and Houbi

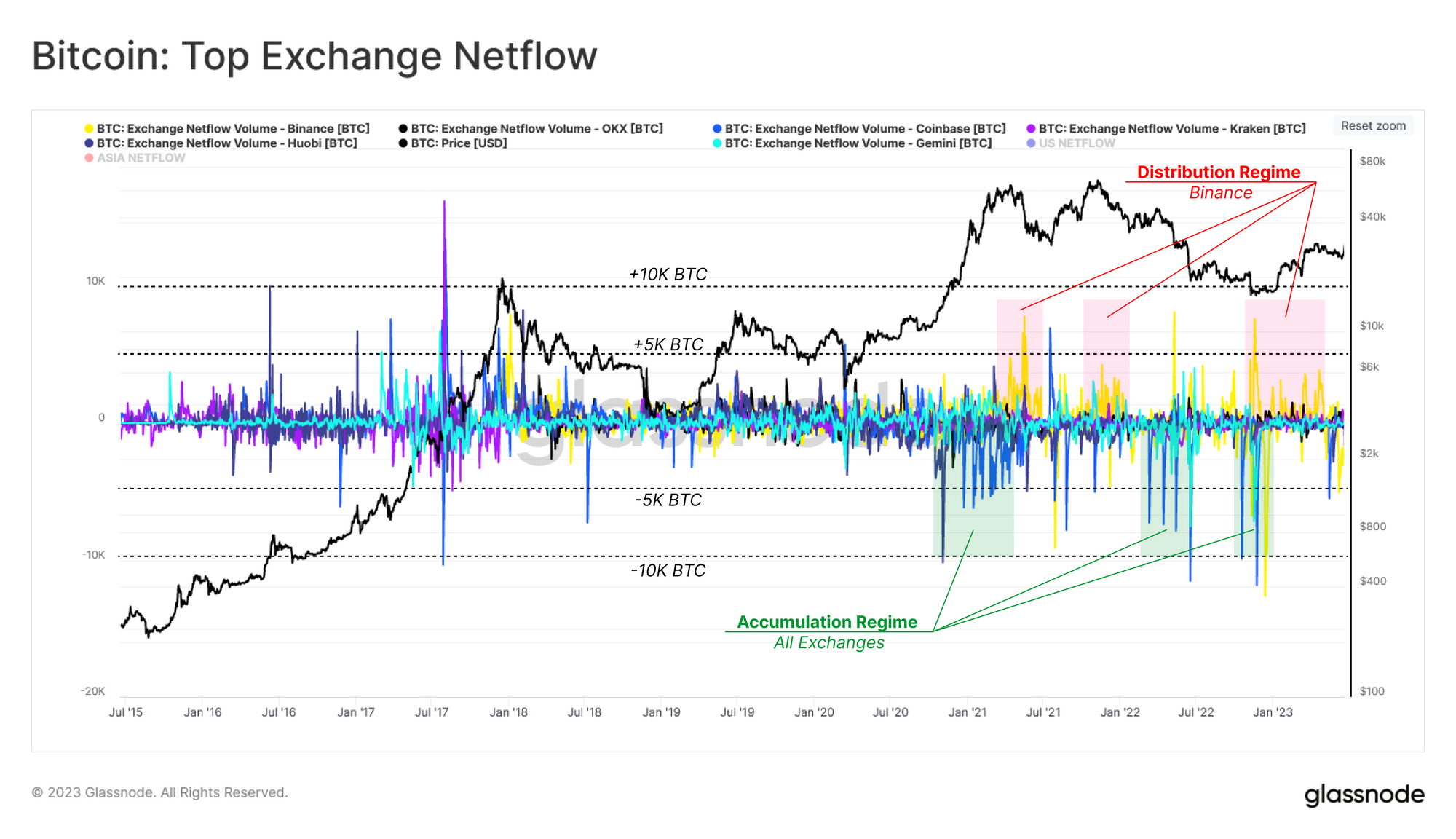

Focusing on the weekly average BTC netflow exposes some interesting patterns in their behavior. During the early stages of the 2020-2021 bull market, the LUNA debacle and FTX fallout led to a regime of strong accumulation and preference for self-custody. Most exchanges experienced 5k-10k BTC daily net outflows.

However, on multiple occasions, Binance demonstrated the opposite behavior, where large inflow volumes accompanied market sell-off events and downtrends. This may be, in part, investors moving holdings away from exchanges perceived as riskier (like FTX) and towards the largest exchange in the world.

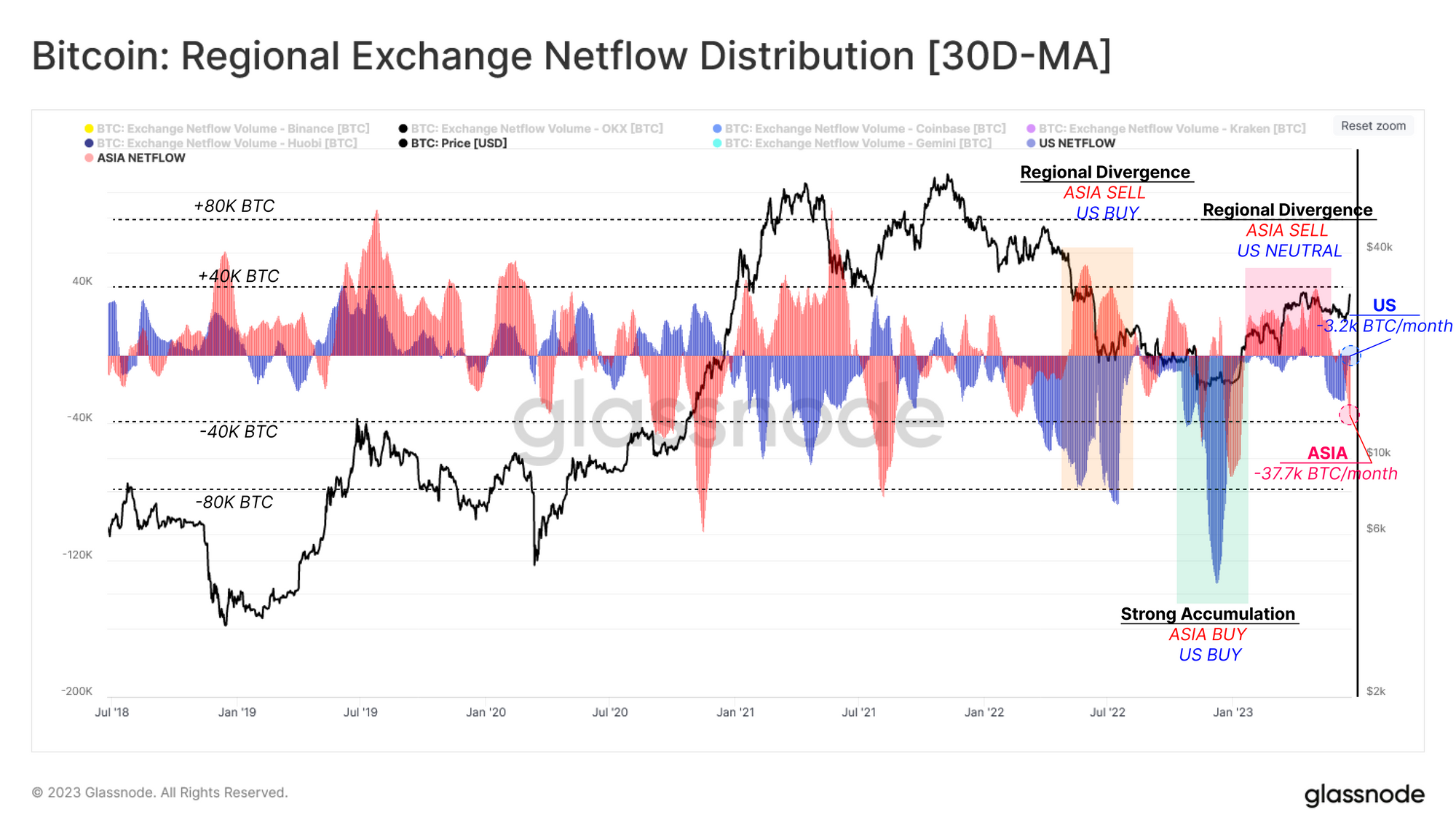

We can also categorize exchanges based on their headquarters (On- vs Off-shore) and then aggregated the total netflows for each subcategory.

The following chart displays the monthly cumulative netflow for each region. We can observe that both regions saw net outflows (accumulation) during the bottom discovery phase between Nov-2022 and Jan-2023. Conversely, after the LUNA debacle, and for much of 2023, Off-shore exchanges have seen net inflows, whilst On-shore exchanges are seeing net outflows, as US based investors accumulate or stay neutral.

Observers can use this indicator to monitor regional market sentiment shifts as they react to external factors. For instance, after the SEC lawsuit against BinanceUS and Coinbase was announced, both regions reacted to price correction via notable exchange outflows. Currently, off-shore exchanges are showing -37.7k BTC/month in net outflows, while buying pressure in on-shore exchanges has declined to -3.2k BTC/month.

Gauging Demand Via Hot Supply

Our recent newsletters highlighted the ongoing transfer of wealth from investors with high time preferences towards HODLers. This pattern of growing illiquidity is a primary component of all prior Bitcoin bull markets. However, while a ‘supply shock’ can positively affect price discovery, the sustainability of the trend still depends on the influx of new demand entering the market.

Given the demand side importance, we seek to establish a framework for tracing demand expansion (or contraction) using on-chain metrics. To achieve this goal, we will measure the momentum of supply, which is highly active as a proxy representation of demand.

💡 Quantifying capital flows can be measured from changes in the size of the highly-active region of circulating supply.

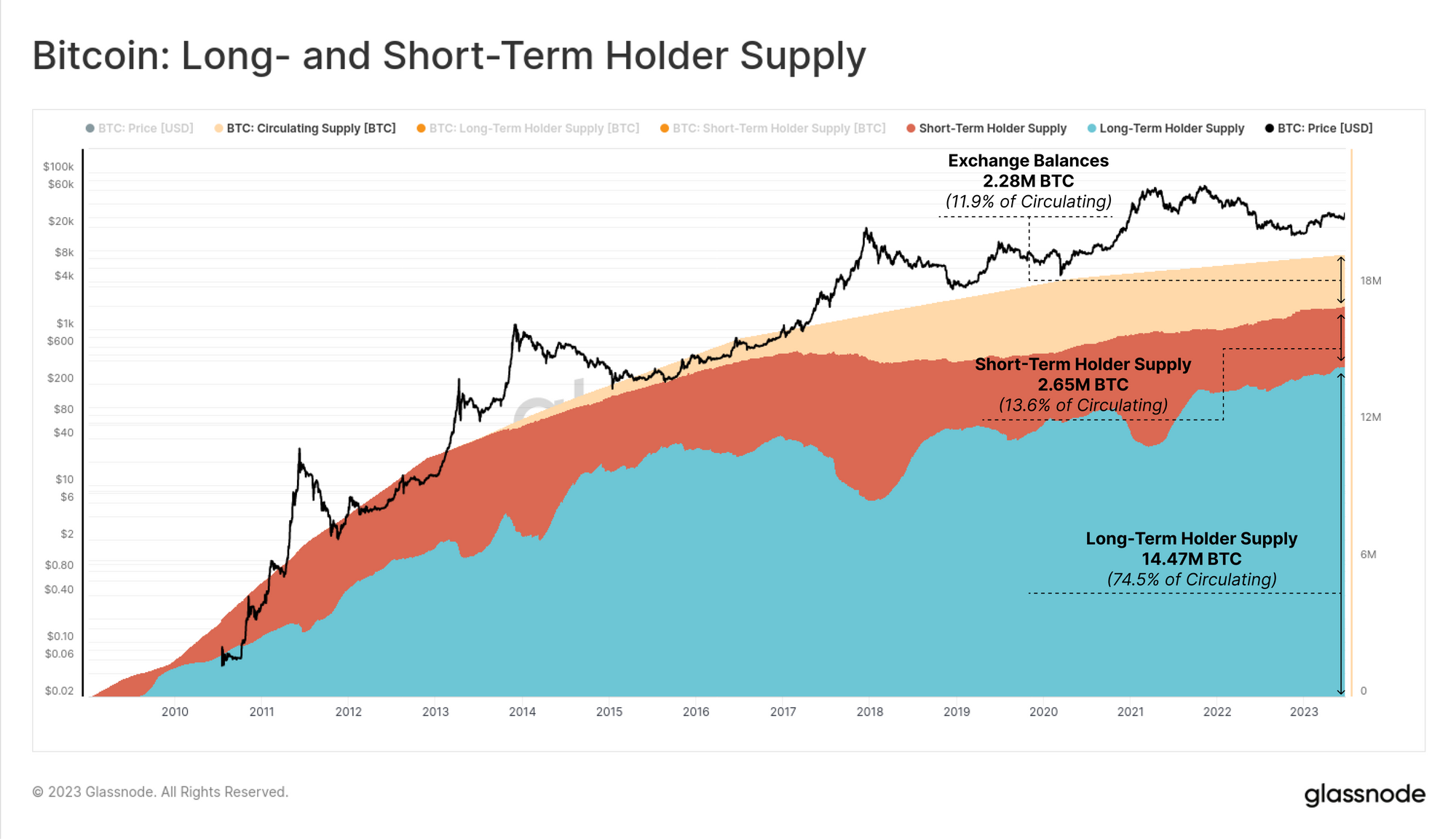

In other words, when new demand enters the market, existing investors usually react by transacting and distributing their coins at higher prices. The spending of older coins 🟦, therefore, necessitates an expansion of the younger supply 🟥 region.

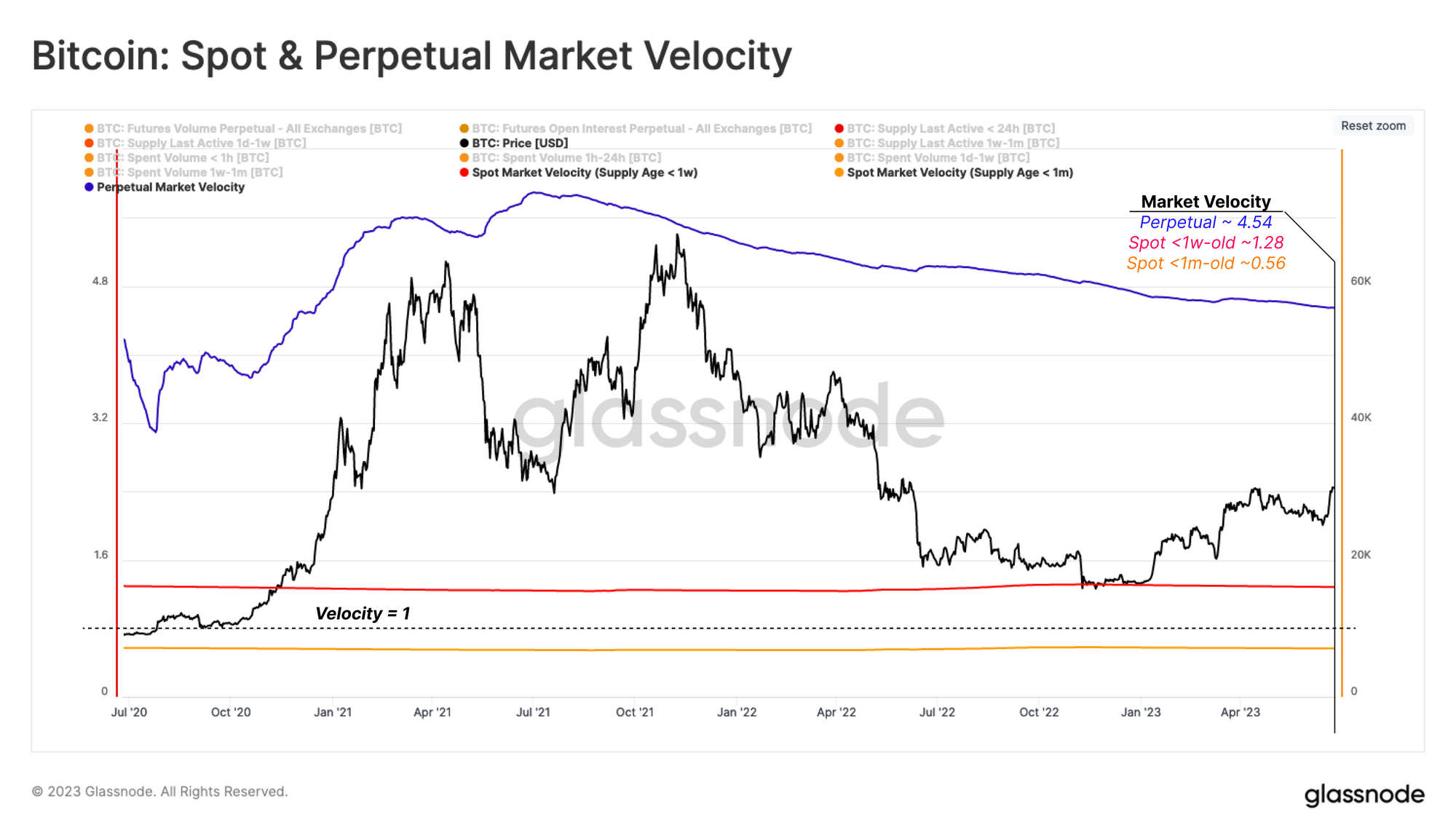

We start by defining ‘young supply’ as all coins moved within the last 155 days (Short-Term Holders), which have a high probability of being spent in the near-term. However, we can look deeper and isolate only the most liquid and highly active subset of the young supply region, which we will define as ‘Hot Supply.’

Hot Supply is a subdivision of young supply which has a Velocity of one or higher. A velocity of more than one means, on average, each coin in that region moves more than once per day.

Using the following formula, we can calculate the velocity of any arbitrary subdivision of coins i.

Velocity_i = Daily Volume_i / Supply Size_i

The chart below shows the all-time-average velocity for the following markets:

- Perpetual Futures Market 🔵 (velocity = trade volume divided by open interest).

- Spot Market (<1w coins) 🔴 (velocity = on-chain volume divided by supply < 1wk).

- Spot Market (<1m coins) 🟠 (velocity = on-chain volume divided by supply < 1m).

The velocity of both perpetual futures markets, and supply < 1wk is more than one. If we consider coins from the next age bracket (1 month), velocity drops below one, reinforcing the notion that older coins have a lower probability of spending.

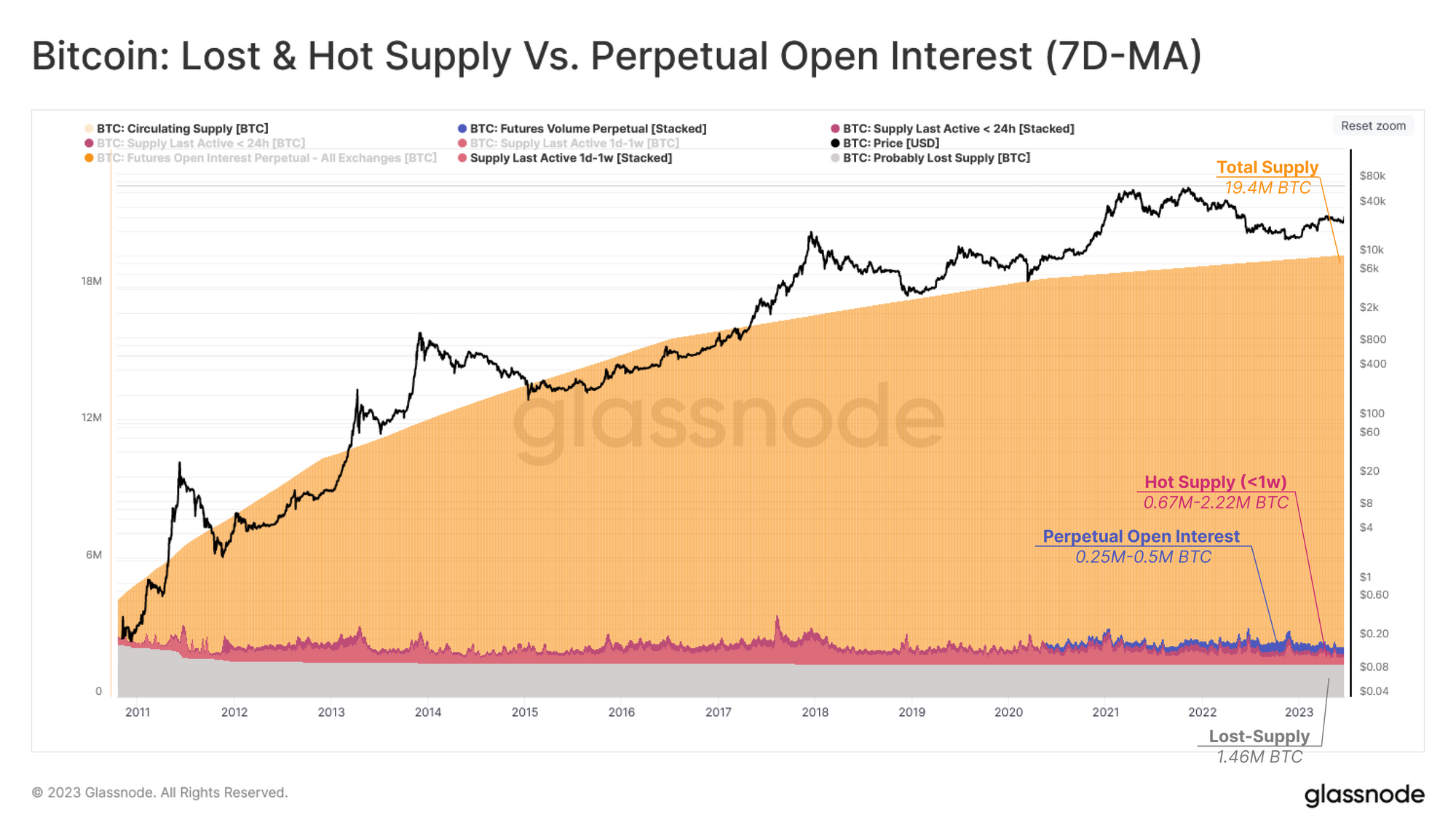

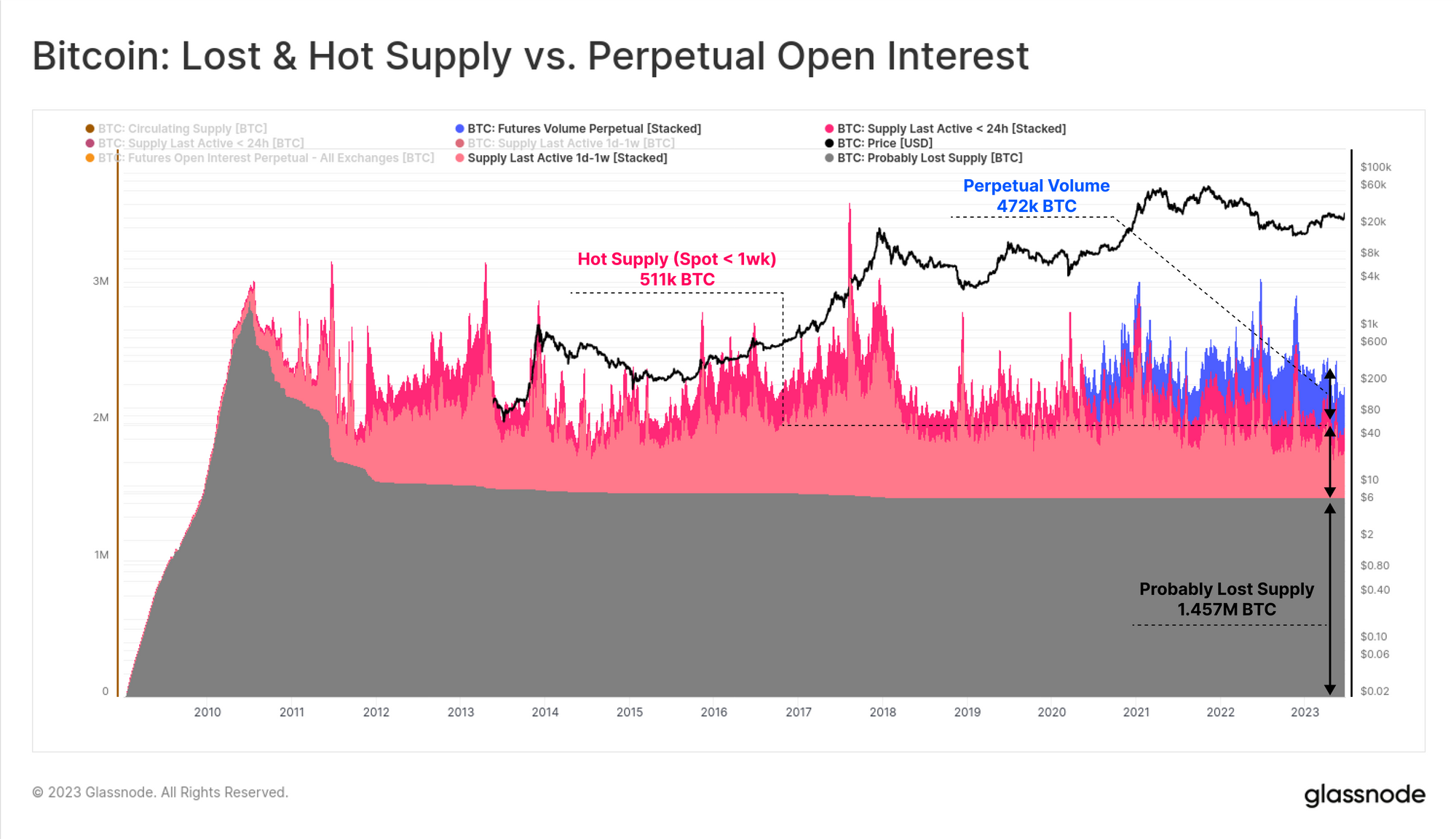

To put the magnitude of this Hot Supply 🟥 into perspective, this supply region is presented against Perpetual Open Interest 🟪, Total Circulating Supply 🟧 and (Probably) Lost Supply ⬛. The interesting takeaway is that throughout the whole history of Bitcoin, the pricing process has been driven by a relatively small fraction of the total circulating supply.

With a median size of 0.67M BTC and a maximum of 2.2M BTC, Hot Supply represents between 3.5% to 11.3% of the total supply. This is comparable to the volume of probably lost coins (1.46M BTC ~ 7.2%), being those that have not transacted since Bitcoins first traded price in July-2010.

Perpetual Futures Open Interest (472k BTC) and Hot Supply (511k BTC) are also similar in size as shown below, suggesting that a volume of around 983k BTC (~$29.5B) is currently ‘available’ for sale, with just under half of this being spot BTC.

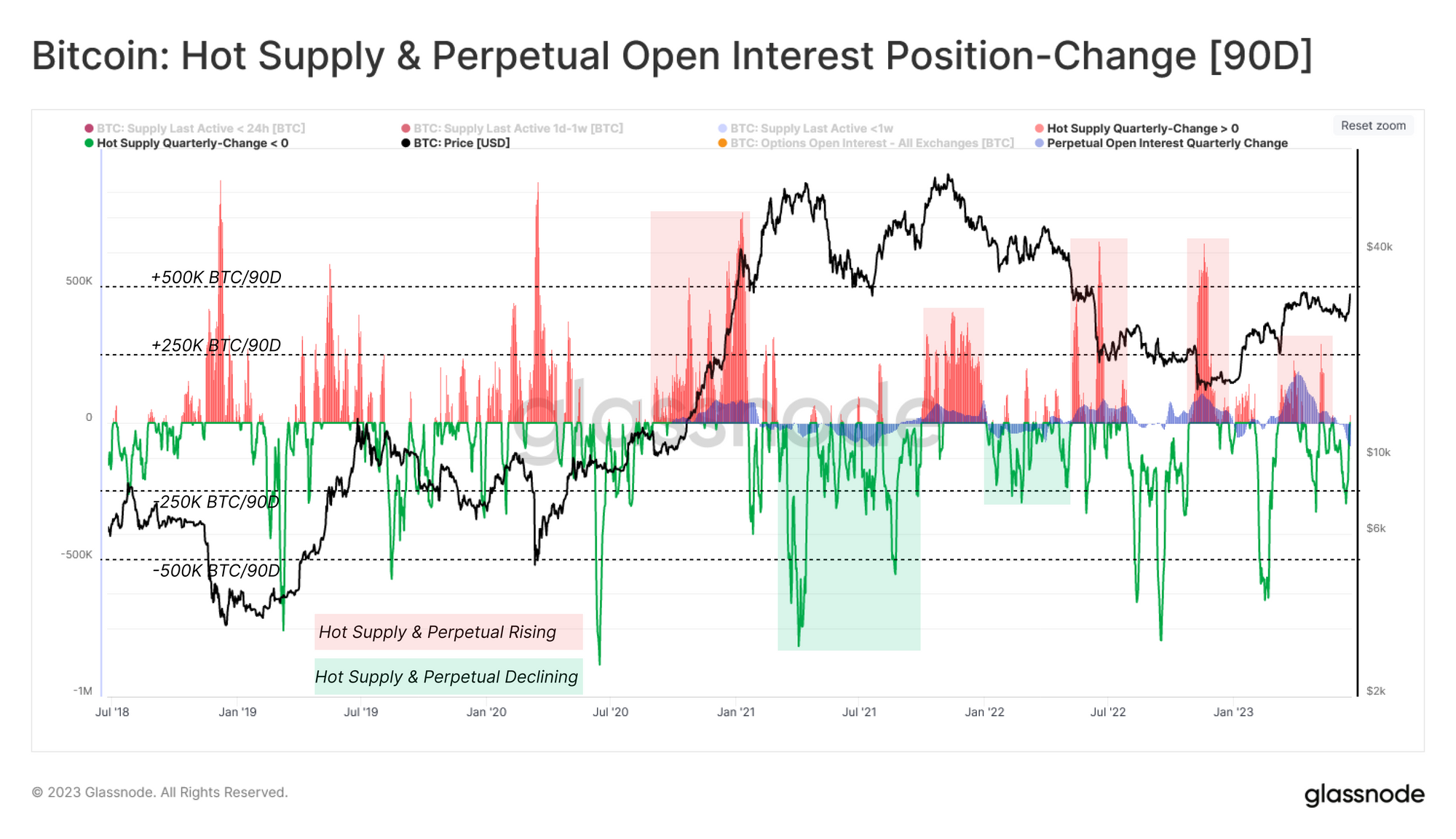

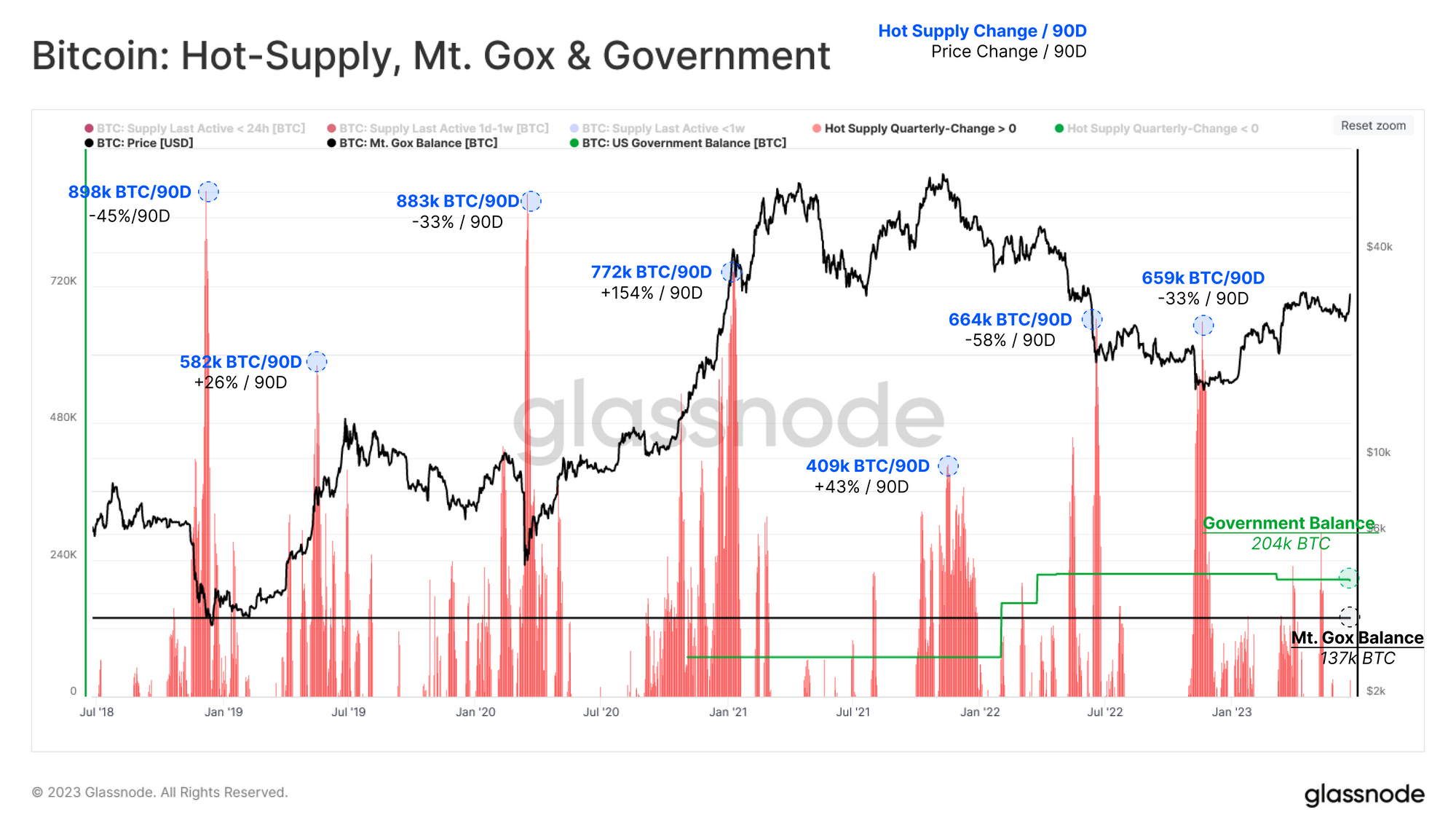

We can also demonstrate the interrelation between price action, and changes in these Hot Supply and Perpetual Open Interest components. The chart below looks at the 90-day Net Position Change in these regions, where we can identify the direction and magnitude of capital flow into 🟥 and out of 🟩 the market.

Throughout past bull markets and severe capitulation events, between 250k to 500k BTC in value is typically deployed into the market. During prolonged bear markets, a similar magnitude of volume is accumulated and taken off-market long enough to exit this Hot Supply cohort (acquired and held by HODLers).

The impact on price action arising from these expansions in hot supply is shown in the chart below. There have been seven major waves of capital inflow over the last 5yrs, ranging in magnitude from 400k BTC to 900k BTC per quarter. These were associated with market moves of between 26% to 154%.

From this chart, we can also compare the potential impact of the liquidation of major supply sources such as the Mt. Gox funds (137k BTC) and confiscated bitcoin held by US government (204k BTC). From this, we can see that a single quarter of similar demand inflows may be capable of absorbing the full distribution from both sources.

Reacting to On-Chain Cost Basis

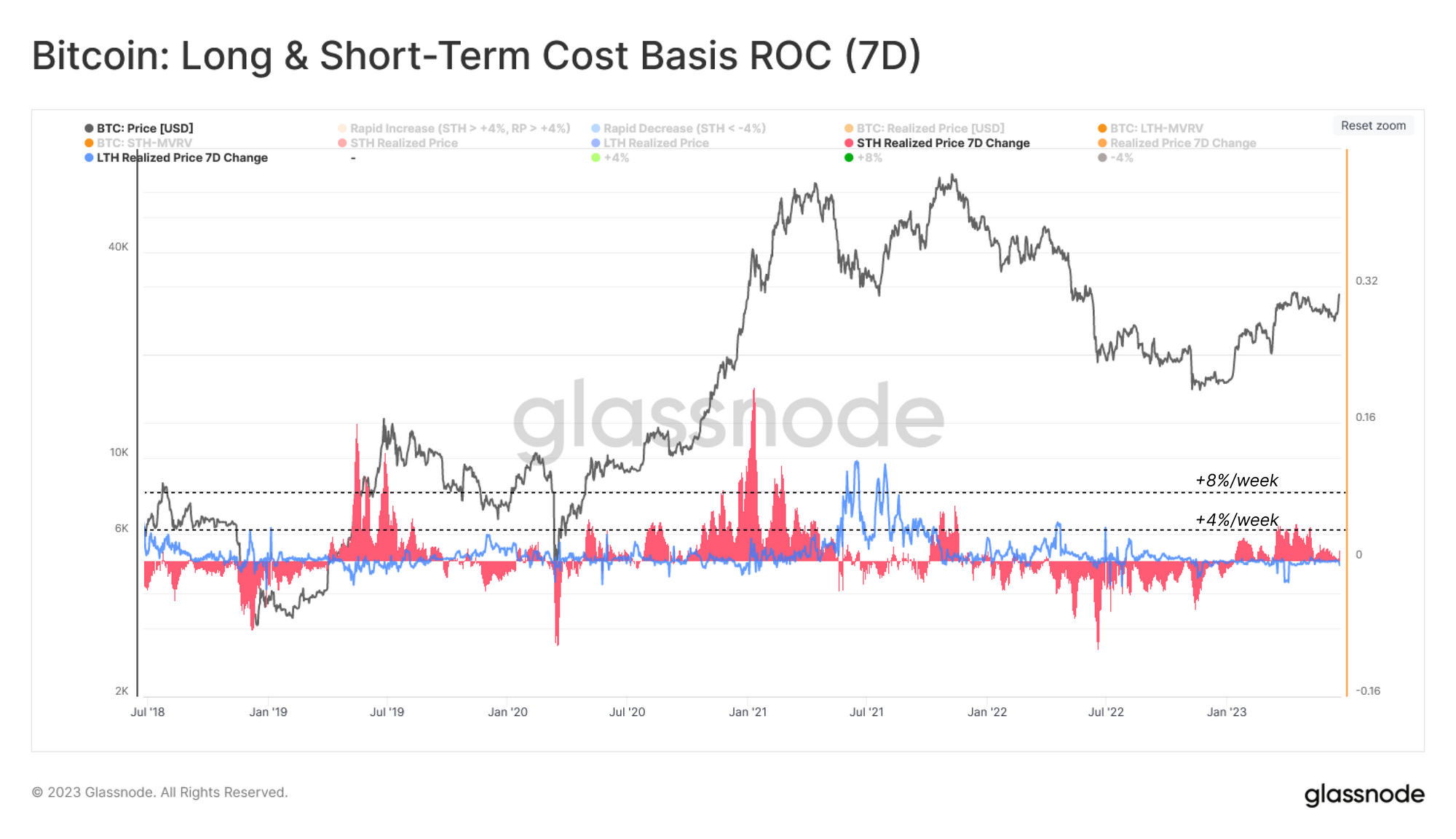

In our WoC 18 report, we illustrated the significance of short-term holder behaviour during cycle pivot points. Through 2023, there have been two major intersections between price and the Short Term Holders-Cost Basis 🔴 where it provided strong support.

The weekly rate of change for both the long-term 🟦 and short-term holder 🟥 cost-basis fell towards zero last week, reflecting a stable equilibrium being reached around $26k. This suggests that investor psychology has shifted away from the 2022 bear mindset, and towards a perception of break-even levels as an opportunity to build a position, rather than take exit liquidity.

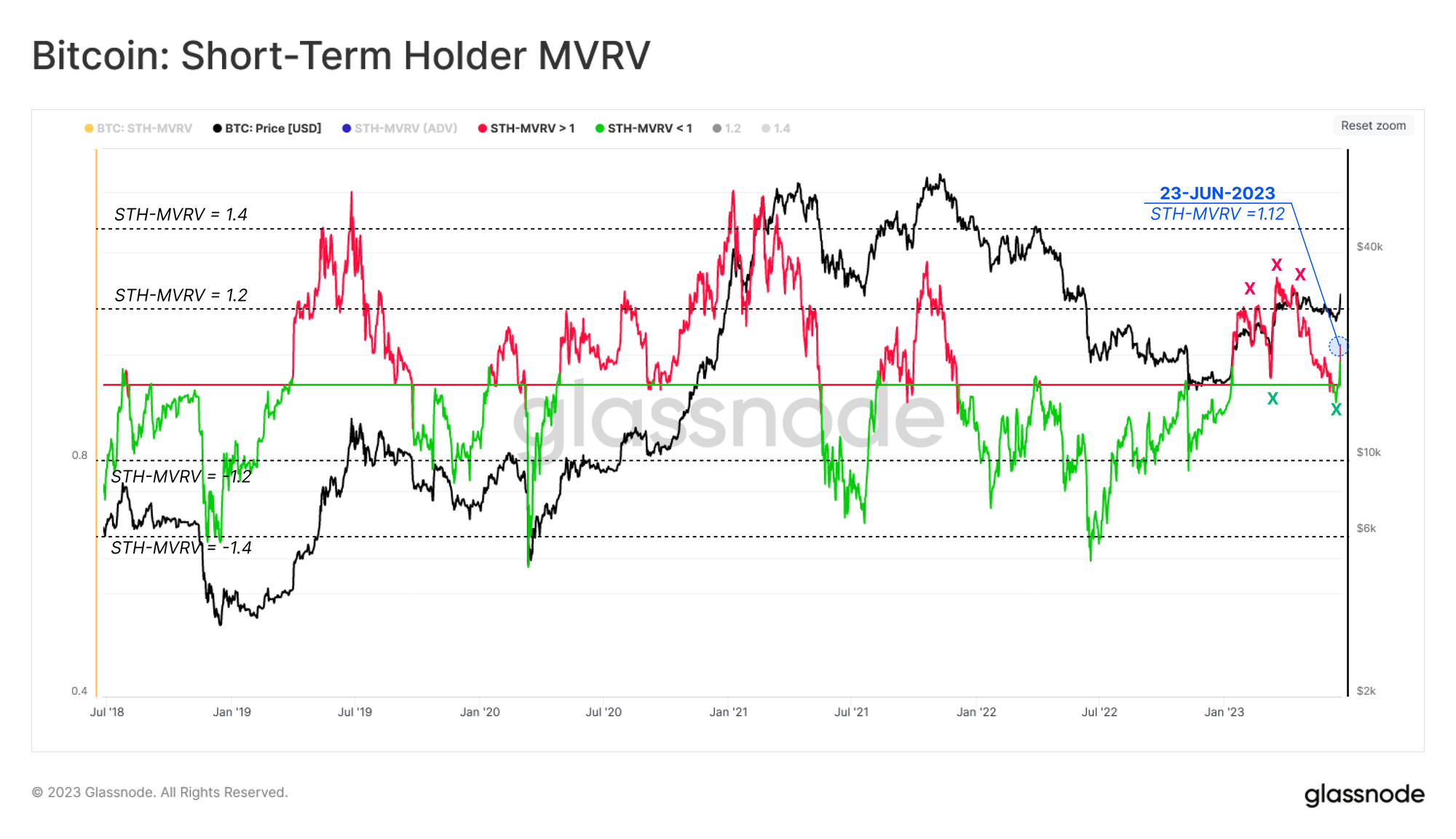

We can also see a strong reaction in the Short-Term Holder MVRV indicator, reacting strongly off the break-even level of MVRV = 1.

This ratio is currently at 1.12, suggesting that, on average, the short-term holder cohort is sitting on a 12% profit. The risk of market corrections tend to rise when this metric exceeds levels of between 1.2 (~$33.2k) and 1.4 (~$38.7k), as investors come into increasingly large unrealized profits.

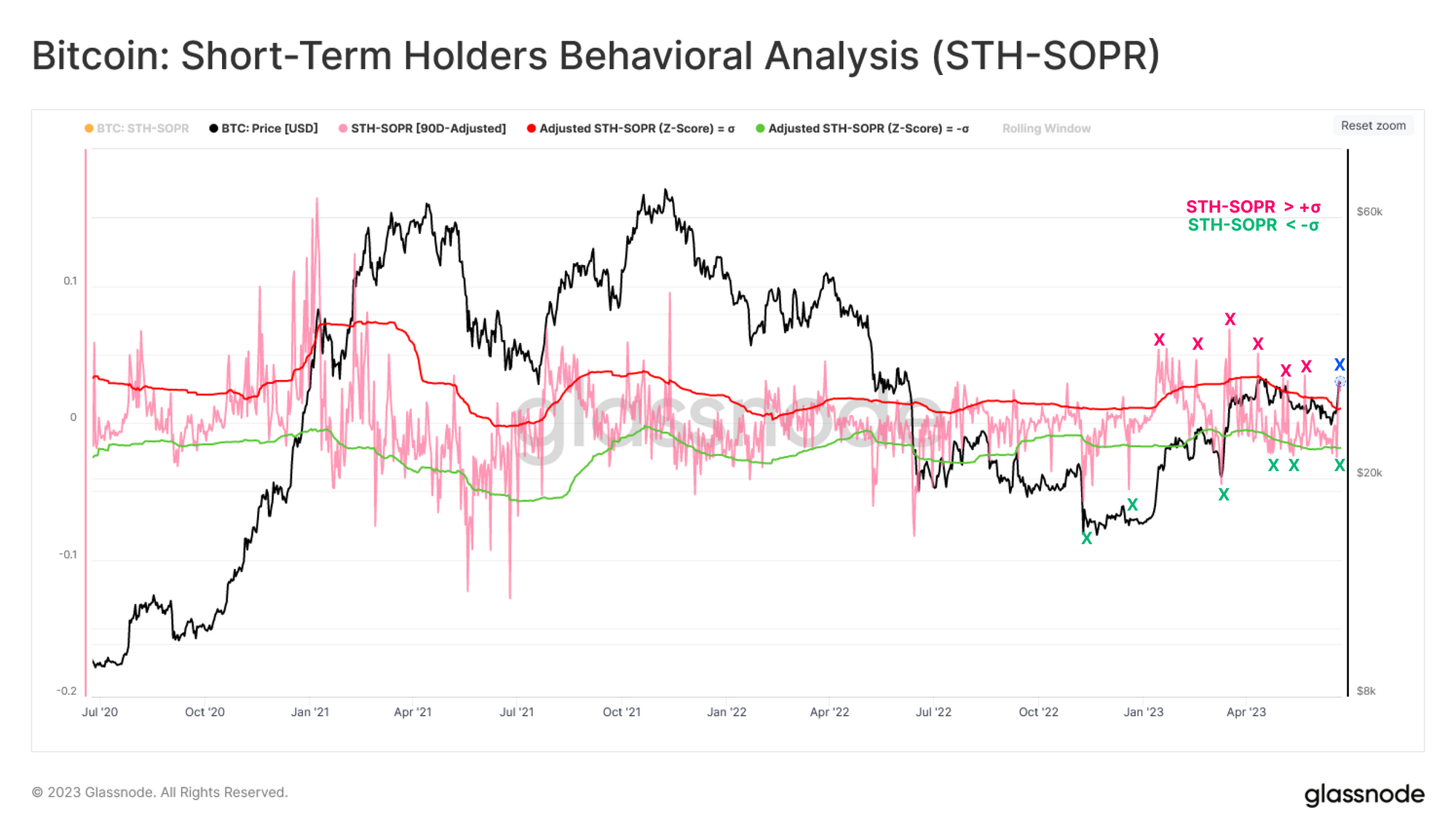

To close, we look to the Short-Term Holder spending behavior YTD, presented in the STH-SOPR indicator. We have plotted upper and lower bands using 90-day ± standard deviation bands as a tool to identify likely reaction points. On multiple occasions in recent weeks, we can identify spot seller exhaustion taking place below the lower band 🟢 including the final low set at $25.1k before the recovery back above $30k.

Summary and Conclusions

As a gold rush of institutional-grade ETF applications are filed in the US, we have seen early signs of a revival of US-led demand. This comes after a period of weaker relative US demand in 2023, with top exchanges in Asia seeing the strongest accumulation year to date.

With the prospect of a new large acquirer of spot BTC on the table, we developed a framework for assessing the available volume of BTC supply, and a toolkit to assess the expansion (or contraction) of new demand.

We close by examining the behavior of the Short-Term Holder cohort, and observe that their market psychology appears to have shifted from the bear market blues of 2022. Their actions speak to a newfound perception of ‘break-even’ levels as an opportunity to add to positions, rather than to liquidate into whatever exit liquidity is available.