Post-ATH Indecisiveness

Bitcoin has slipped below $116k, entering a low‑liquidity “air gap”, a zone where few coins have changed hands. Short-Term Holder profitability has hit the bull market mid-line, ETF flows have turned negative, and funding rates are cooling off as the market is trying to find support.

Executive Summary

- After peaking above $123k in mid‑July, BTC has since entered a phase of indecision, with the price trading below the supply cluster with a base at $116k.

- On July 31, price broke below the lower boundary of this cluster, slipping into a relatively low‑liquidity “air gap”, which persists down to $110k. Opportunistic buying has emerged, but the market is yet to reclaim key resistance levels.

- Short‑term holder profitability has dropped, although around 70% of their supply is still held in profit. Without a quick rebound in demand, confidence amongst these new investors may start to weaken, prompting further sell pressure.

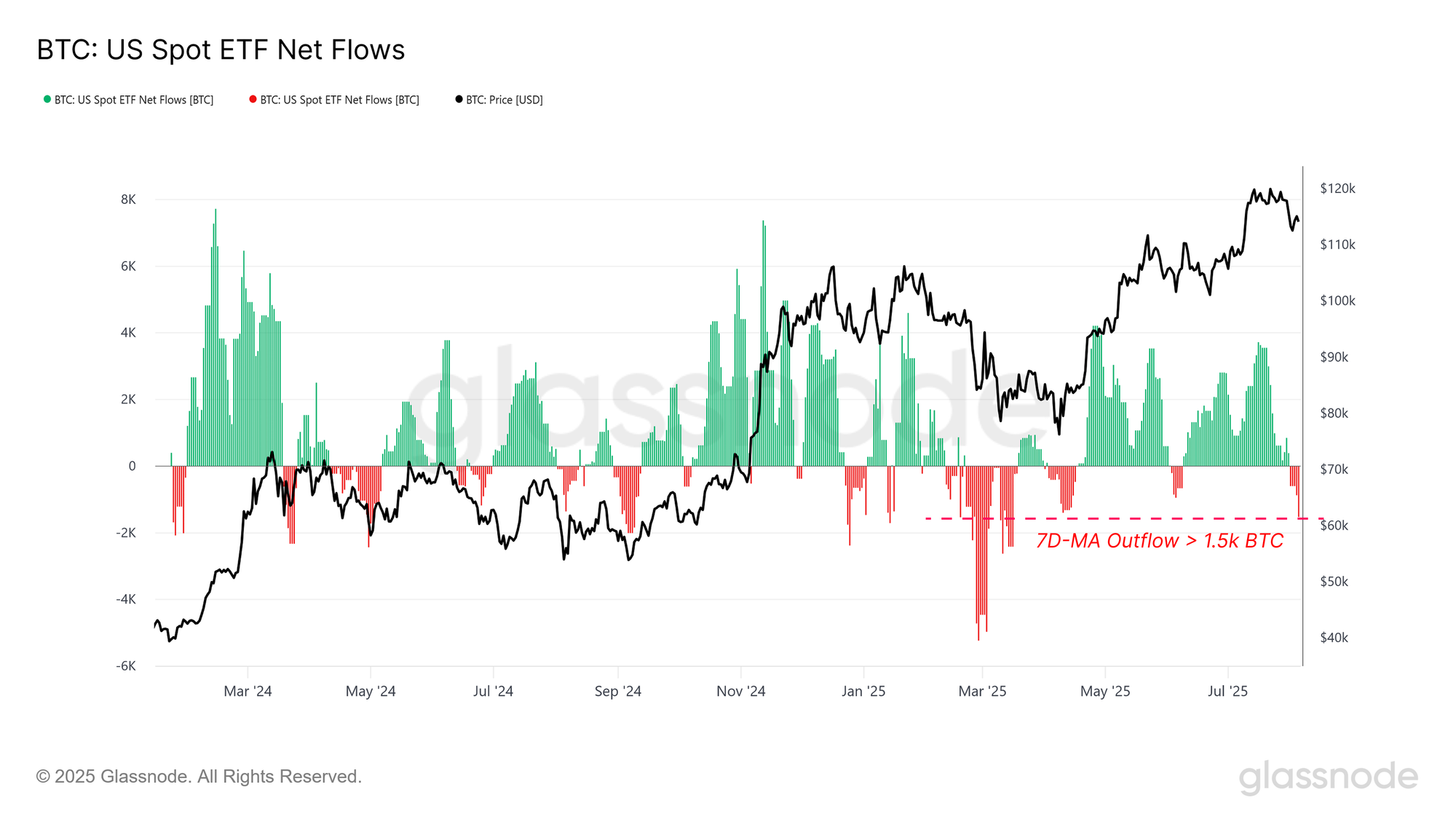

- The ETFs experienced an outflow of ‑1.5k BTC, which was the largest since April 2025.

- Funding rates across major perpetual swap markets have slid lower, signalling a reduction in excess leverage and a reluctance to pay high premiums for opening new leveraged long positions.

Drifting Into An Air Gap

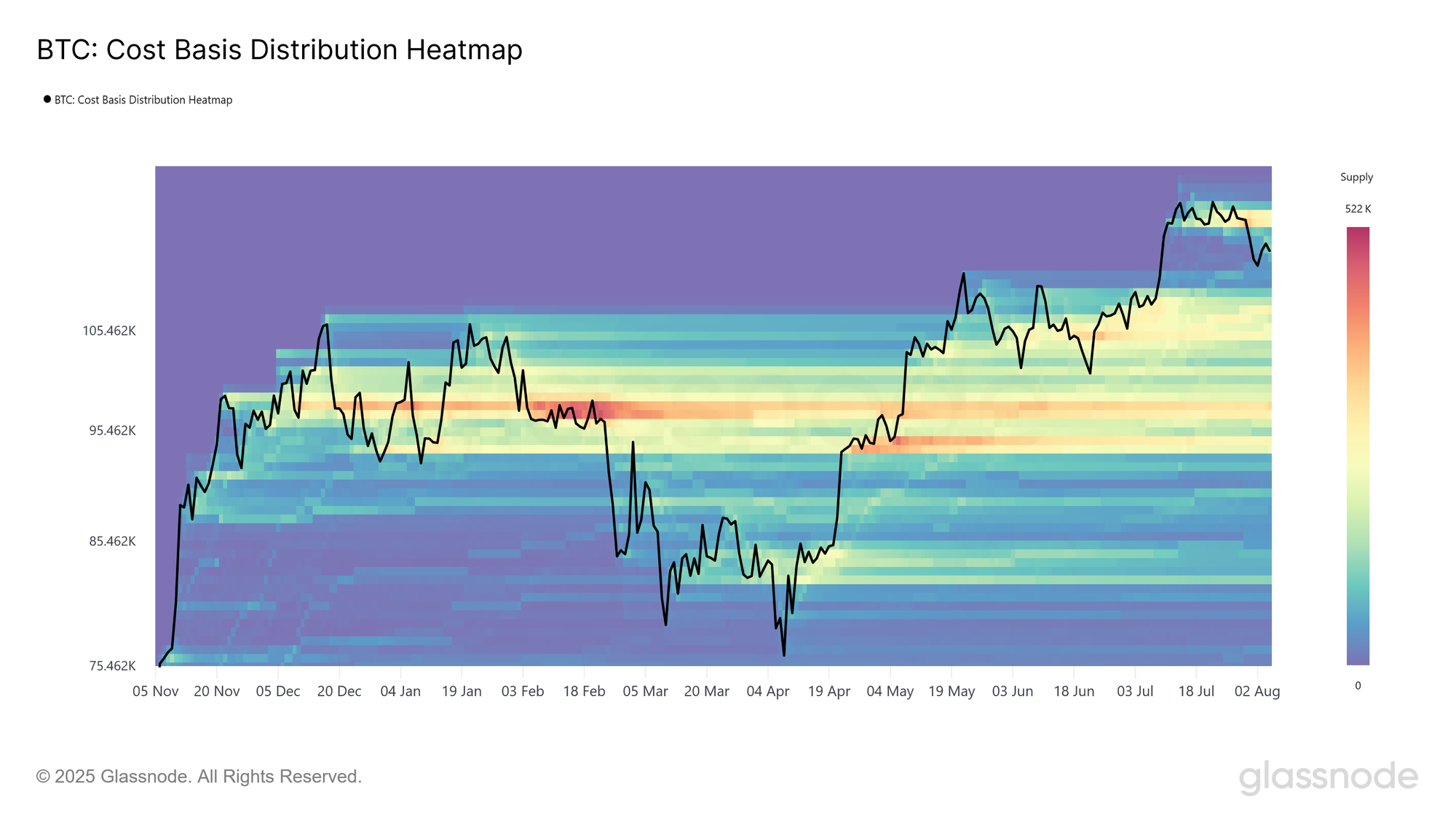

After reaching a new all-time high of $123k in mid-July, the market has since pulled back to $113k, putting many new investors underwater on their recent buys. This has formed a large supply cluster with a cost basis above $116k.

The lower bound of this cluster was tested multiple times prior to the market breaking lower, with each retest prompting a price rebound and finding support. However, on 31 July, the price broke decisively below this support level, entering the “air gap” highlighted in WoC 30.

Historically, such low-liquidity price ranges often evolve into new accumulation zones, as opportunistic buyers step in to acquire BTC at a perceived discount to the latest ATH.

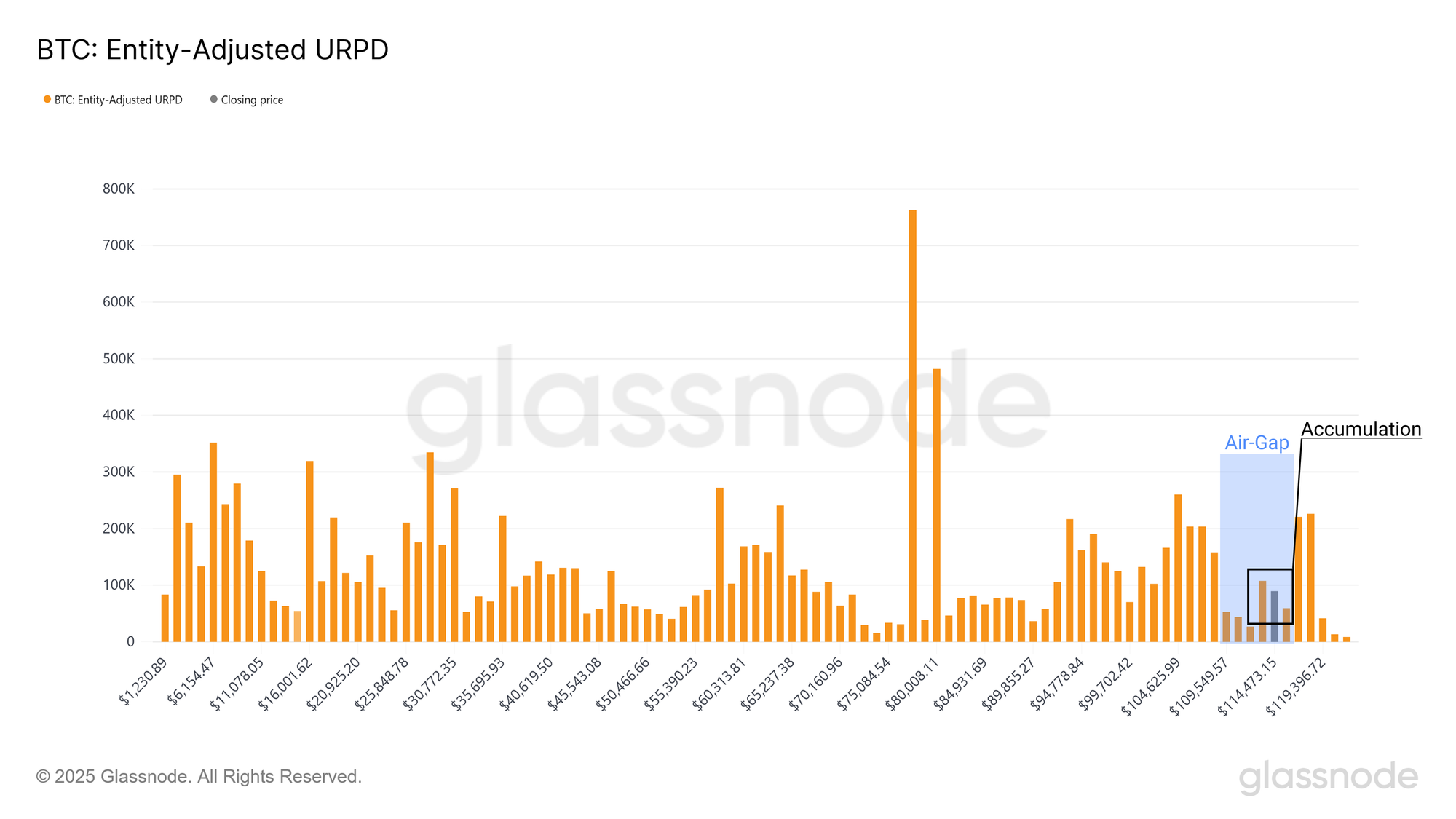

To evaluate how aggressively opportunistic buyers stepped in after the price slipped lower, we can compare the Entity-Adjusted URPD as of 31 July to that of 4 August.

The UTXO Realized Price Distribution (URPD) maps out where the set of Bitcoin UTXOs were created as of that date, with each bar showing the volume of supply which last moved within each specific price bucket.

This comparison shows that after rebounding from a low of ~$112k, roughly ~120k BTC was acquired by investors, suggesting buy-the-dip behaviour by investors, and pushing the price back above $114k.

However, this air gap between $110k and $116k remains relatively light in terms of aggregate supply, and a period of accumulation within this zone could, over time, establish a sufficiently strong base to support the next move higher.

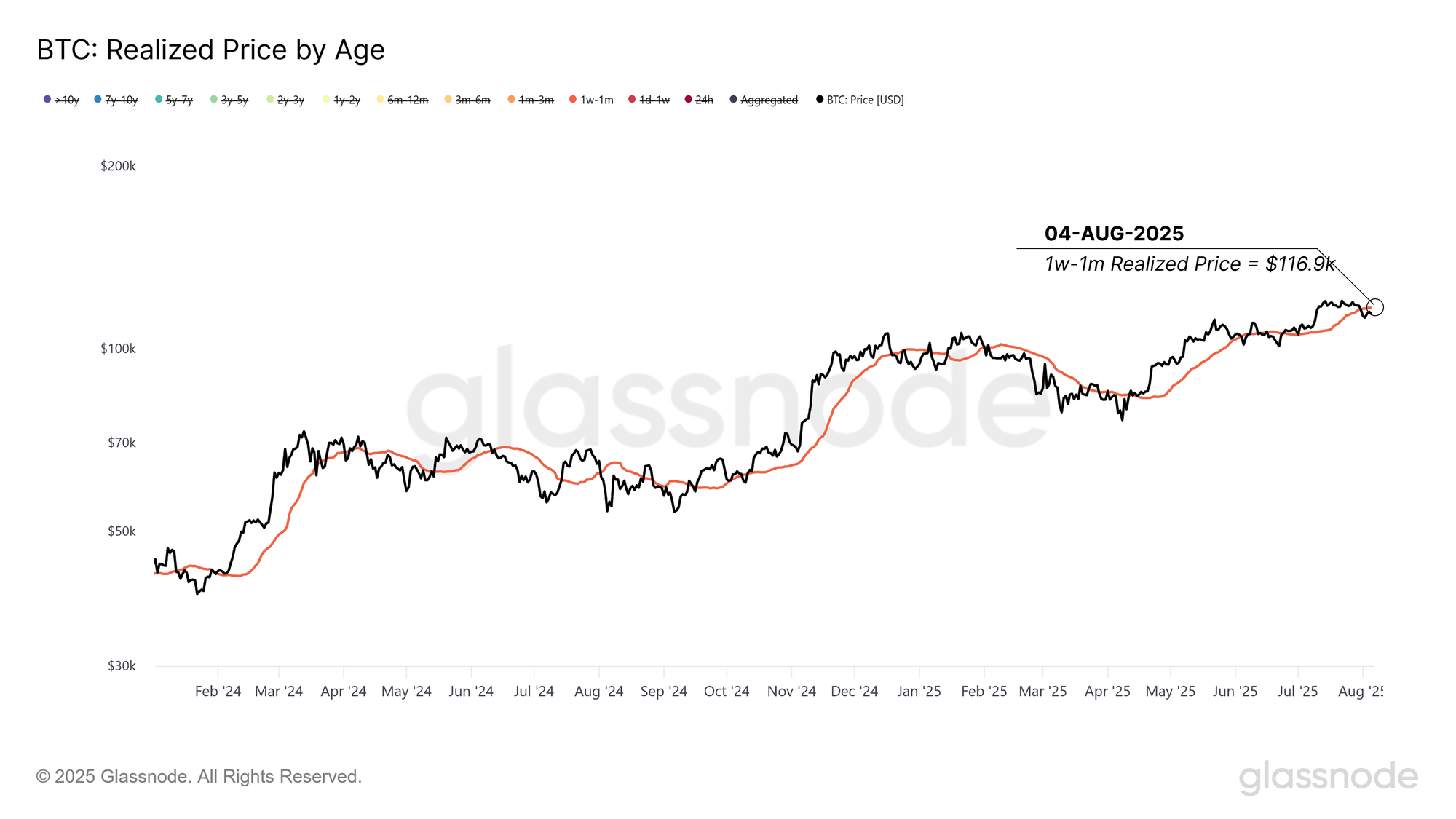

A Decisive New Resistance

Despite the accumulation which has occurred over the last week, the market rebound has thus far lacked sufficient strength to reclaim the cost basis of local top buyers who entered over the past month. For this 1w–1m holder cohort, their cost basis now acts as a resistance level, and is located around 116.9k.

A sustained price move above this threshold would signal that the demand side is regaining control and offer early confirmation that the market has found its footing. Conversely, if the price remains below this level for a longer period, it increases the risk of a deeper correction, likely toward the lower bound of the air gap near $110k.

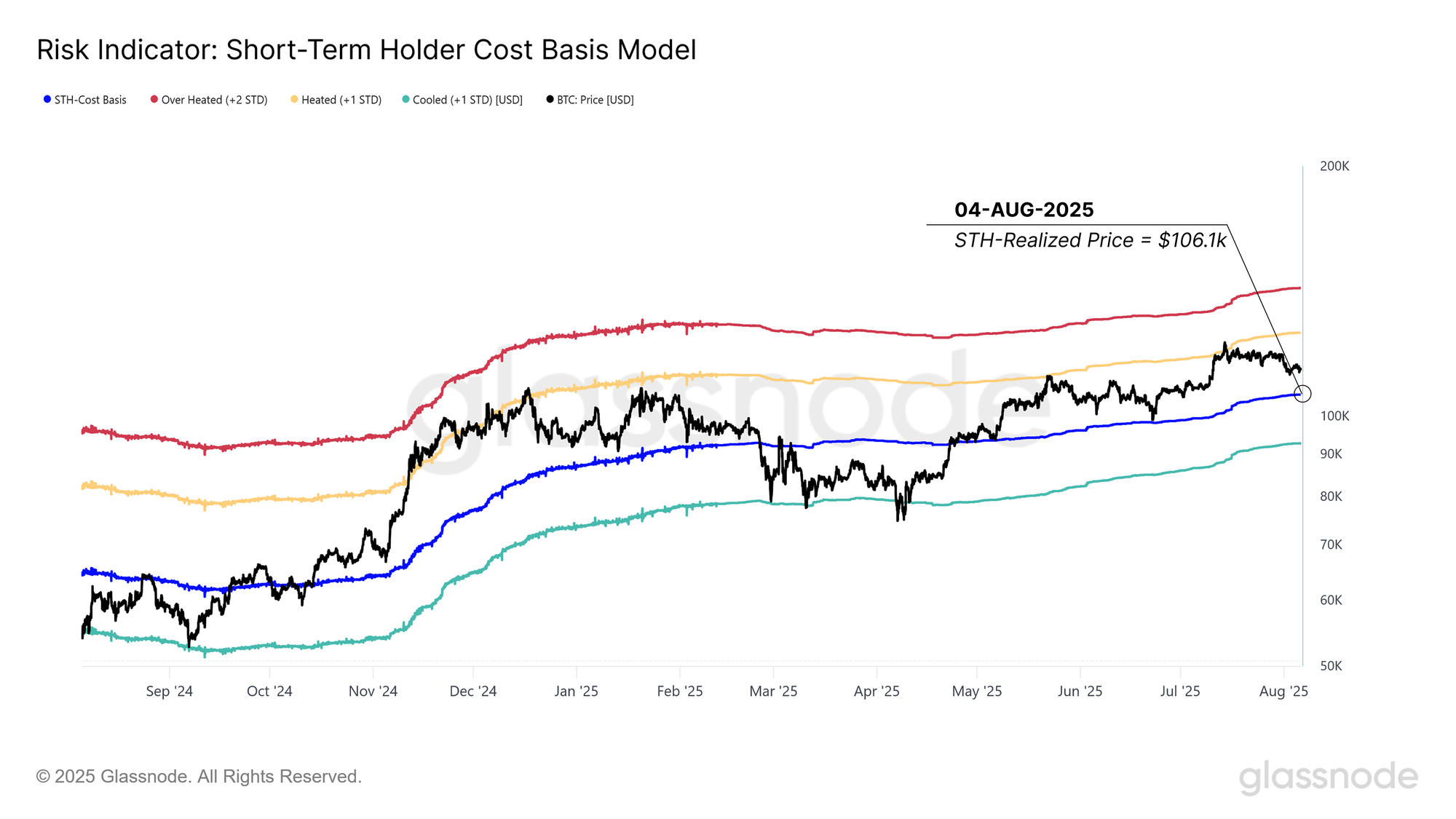

Bull/Bear Frontline

Zooming out, we can construct a set of statistical bands derived from the short-term holder cost basis, which can provide a compass for navigating the current market structure.

The Bitcoin price is currently trading within the warm, but not overheated zone, and is still above the short-term holder cost basis located at $106k. This setup is quite normal for a Bitcoin bull market, and the STH cost basis historically serves as an important threshold separating near-term bullish and bearish trends.

Profitability Around The Mid-line

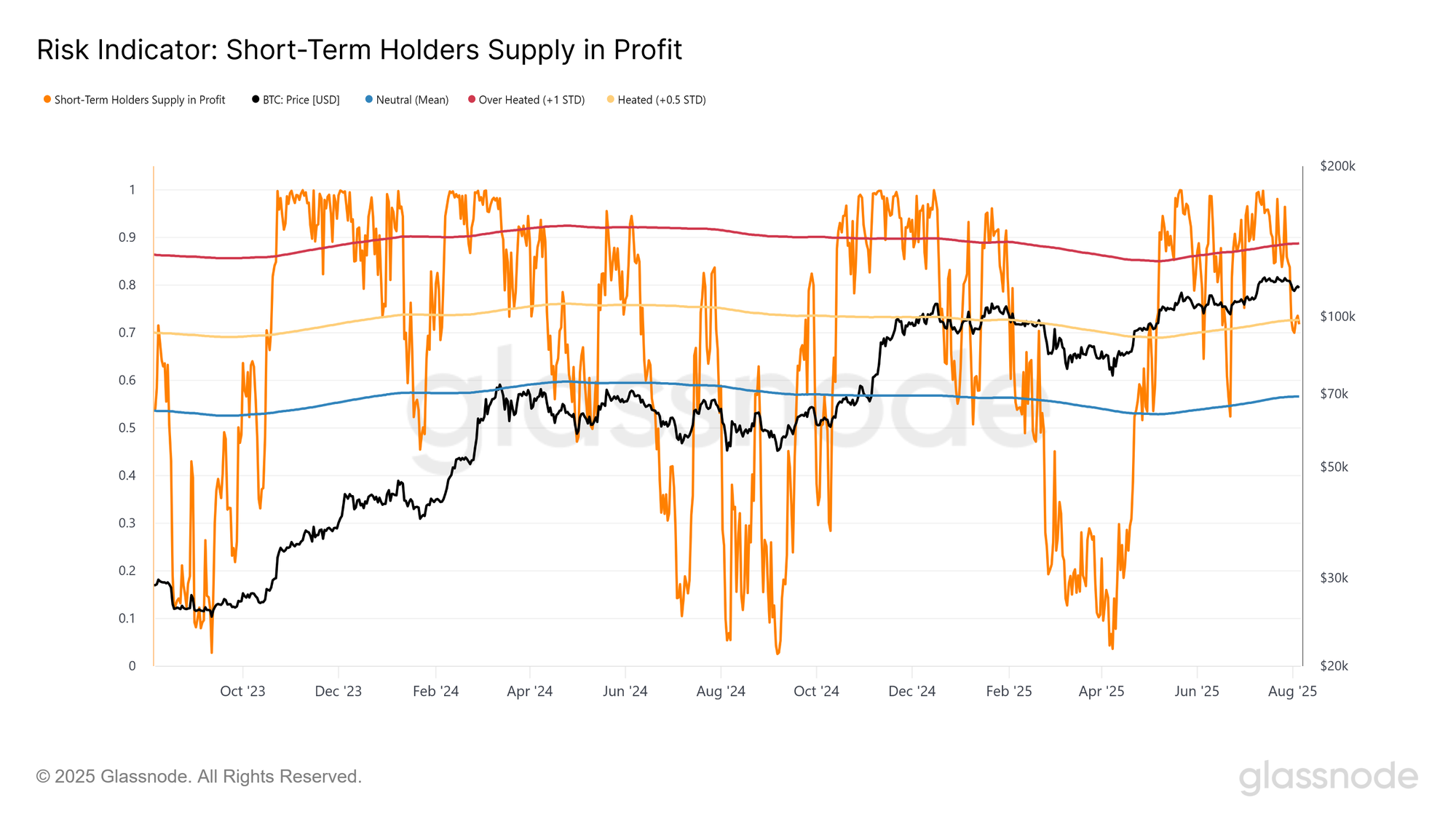

Given the market is currently within a typical post-ATH corrective phase, we can utilize indicators of on-chain investor behaviour to gauge where short-term biases may be leaning. First, we examine how the profitability of new investors has changed, as this reflects a primary driver of their confidence in the trend and a key determinant of their next decision.

For short-term holders, the percent of their supply held in profit has declined from 100% to 70% during this price pull-back. This is a level which aligns with the midline of prior bull phases, and is again not an atypical condition.

The deeper the correction, the more supply is likely to fall into loss, which can slowly erode investor confidence. However, given the market is trading within a relatively thin air-gap, the most likely source of this additional supply would be from late-stage profit-taking, should it occur.

A Need for New Demand

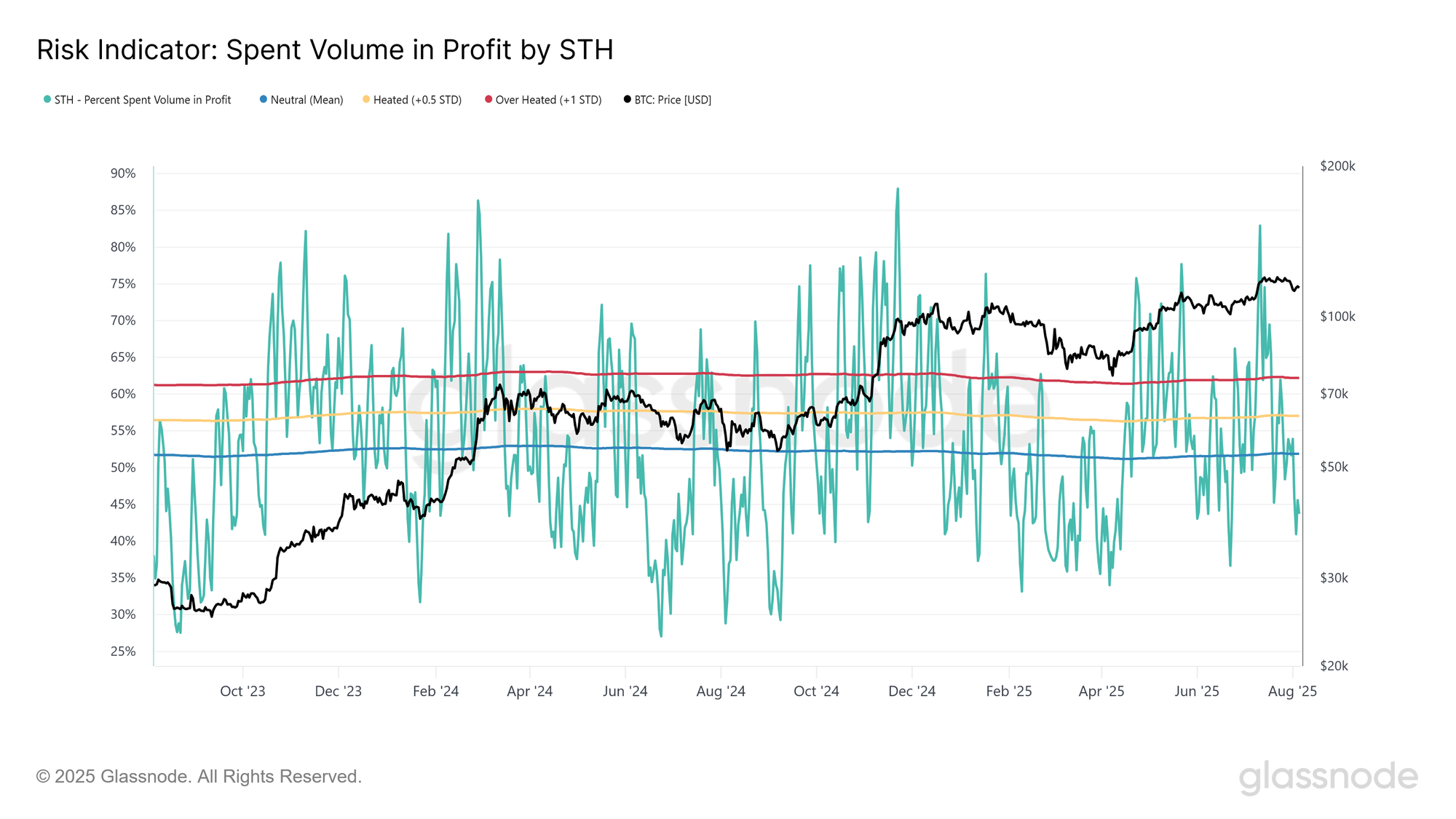

To assess how this pullback has influenced investor behaviour, we turn to the percent of spent volume originating from short-term holders who were in profit. This metric directly measures the number of recently acquired coins that are taking profit.

The proportion of STH spent coins which are taking profit has cooled off, and trading at 45%, which is below the neutral threshold.

Overall, this suggests the market is in a relatively balanced position, with 70% of STH supply still held in profit, and an almost even split of profit and loss taking in coins which are on the move.

ETF Outflows Create Sell-side Pressure

To bolster our on-chain dominant analysis thus far, we can view these metrics alongside demand from traditional vehicles via the ETFs. On August 5, the ETFs experienced a fairly sizeable outflow of -1.5k BTC, marking the largest wave of sell-side pressure from these vehicles since April 2025.

To date, outflows from the ETFs have been relatively brief events, with few instances of sustained sell-side pressure. Keeping an eye on these flows will help to identify whether this outflow is just another example of this dynamic or perhaps a more structural shift in sentiment.

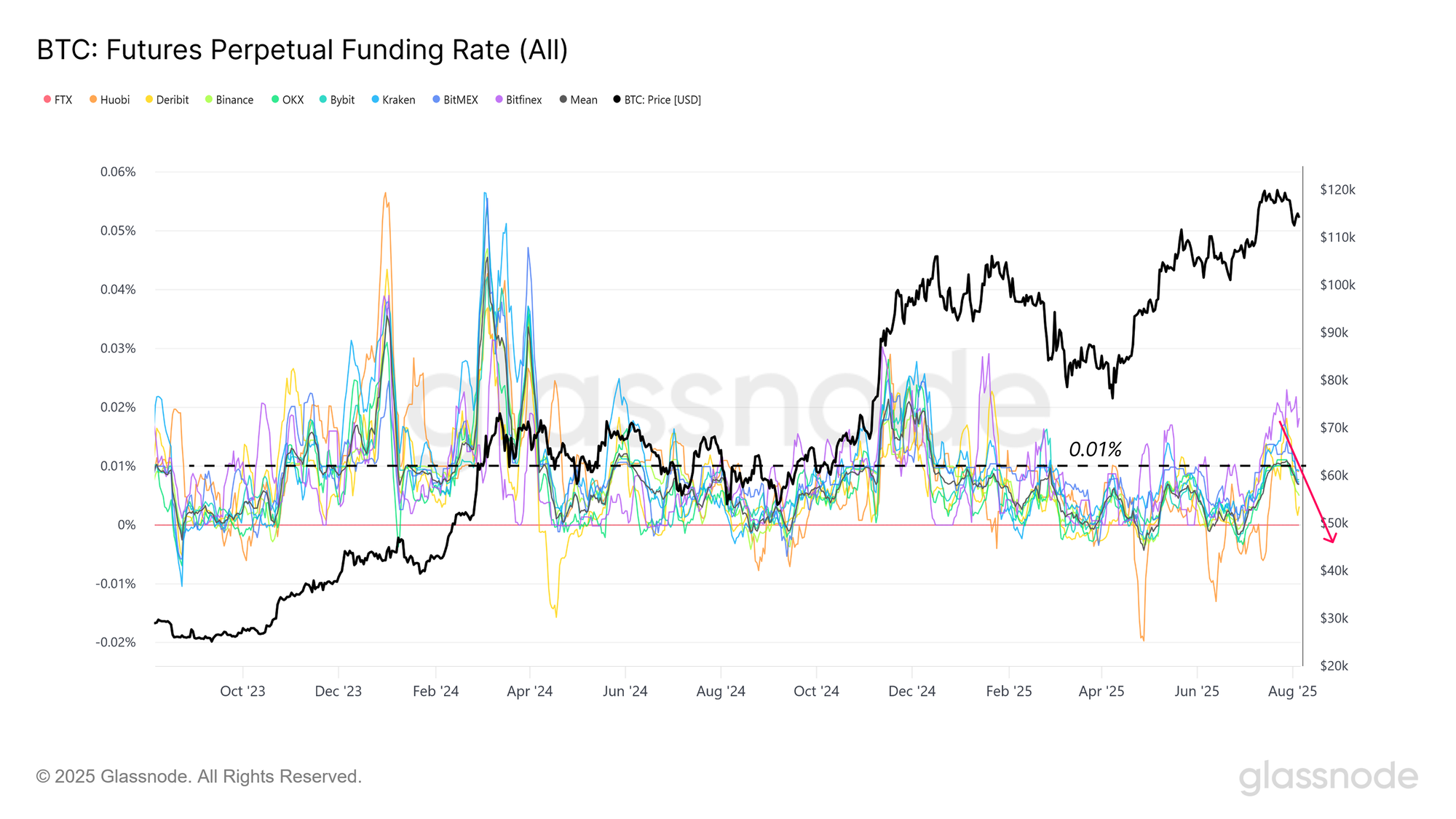

Funding Rates Pull Back

Looking beyond the spot market, sentiment in perpetual futures is also moving away from a brief dance with euphoric levels. Both the aggregated and individual component funding rates across all perpetual swap markets for Bitcoin have come off the recent highs and are now trading back below the 0.1% range.

This territory is often considered to be fairly neutral, reflecting a lack of appetite amongst the bulls to pay a large premium for leveraged long positions. Such a shift suggests a marked cooling down of speculative interest and reduced upside conviction in the near term.

Conclusion

The Bitcoin market is navigating a post‑ATH correction. The Bitcoin price has slipped below the $116k accumulation range low and entered a low‑liquidity “air gap”, first highlighted in earlier reports. Opportunistic buying has emerged, but demand has not yet been strong enough to reclaim the cost basis of recent buyers, leaving this level as a critical pivot for near‑term direction.

Investor behaviour signals a relatively balanced environment, with several Short-Term Holder-based metrics trading at levels which are quite consistent with a typical bull market trend. The ETFs have experienced a large outflow; however, to date, these have been brief events, and there isn’t sufficient evidence to suggest a more structural trend of outflows is in play.

The market is effectively re-finding its footing, bounded by the previous cycle ATH of $110k below, and the base of the most recent accumulation range near $116k.

Disclaimer: This report does not provide any investment advice. All data is provided for informational, and educational purposes only. No investment decision shall be based on the information provided here and you are solely responsible for your own investment decisions.

Exchange balances presented are derived from Glassnode’s comprehensive database of address labels, which are amassed through both officially published exchange information and proprietary clustering algorithms. While we strive to ensure the utmost accuracy in representing exchange balances, it is important to note that these figures might not always encapsulate the entirety of an exchange’s reserves, particularly when exchanges refrain from disclosing their official addresses. We urge users to exercise caution and discretion when utilizing these metrics. Glassnode shall not be held responsible for any discrepancies or potential inaccuracies.

Please read our Transparency Notice when using exchange data.

- Join our Telegram channel.

- For on-chain metrics, dashboards, and alerts, visit Glassnode Studio.