Time is Money: How Coin Age Shapes Bitcoin’s Spending Patterns

We examine the relationship between a coin's age and its spending likelihood. We discover a power-law dynamic that governs this likelihood, highlighting a smooth and mathematically elegant decay in spending behavior as coins grow older.

In this article, we reveal a fascinating power-law relationship between coin age and spending probability, offering a predictive framework for understanding investor behavior and coin dormancy. Read on to learn how these insights can help refine your on-chain analysis and inform better trading strategies.

Introduction

Bitcoin's transparent blockchain allows for detailed analysis of coin movements and holder behaviors. By examining the age of Unspent Transaction Outputs (UTXOs) and their spending probabilities, we can gain deep insights into the dynamics of Bitcoin's ecosystem. This article explores the power-law relationship between UTXO age and spending probability, revealing a predictable pattern in how coins are held and spent over time.

Why This Analysis Matters

Understanding Bitcoin's UTXO spending behavior offers powerful insights for traders, investors, and analysts alike. By uncovering the predictable patterns governing coin dormancy, you can:

- Enhance Investment Strategies: Predict potential liquidity shifts and better gauge market sentiment.

- Improve On-Chain Analysis: Leverage a mathematical framework to complement traditional LTH/STH metrics.

- Anticipate Holder Behavior: Identify when coins are likely to re-enter circulation, informing timing for trades or decisions.

Whether you're optimizing trading algorithms, analyzing market trends, or refining investment approaches, this framework provides a clear, data-driven edge in navigating Bitcoin's ecosystem.

What Are UTXOs and Spending Probabilities?

At the heart of Bitcoin's blockchain lies the UTXO model. UTXOs represent Unspent Transaction Outputs — essentially, chunks of Bitcoin that have been received but not yet spent. Every Bitcoin transaction consumes existing UTXOs as inputs and creates new UTXOs as outputs. These UTXOs can be thought of as coins held at specific addresses, waiting to be spent in future transactions.

By analyzing the age of these UTXOs — the number of days since they were created— we can infer behavioral patterns of holders across the network. A fundamental concept in this analysis is the spending probability, which measures the likelihood that a UTXO of a given age will be spent on any given day. This measure quantifies how Bitcoin moves within the ecosystem and how holder behavior evolves.

Methodology

Dataset and UTXO Counts

Our analysis is based on Bitcoin UTXO data spanning from 2015 to November 2024. For each day within this period, we count the number of UTXOs of every possible age, from one day up to 10 years (approximately 3,650 days). We limit the maximum age to 10 years to avoid noise inherent in the data for extremely old UTXOs.

Calculating the Spending Rate

To determine the spending probability, we compare the number of UTXOs of a specific age on one day with the number of UTXOs of the next higher age on the following day. The spent fraction is calculated as:

Spent Fraction = 1 - (Number of UTXOs of age N on day T) / (Number of UTXOs of age N-1 on day T-1)

This formula represents the fraction of UTXOs of age N-1 that were not present as UTXOs of age N on the next day, implying they were spent.

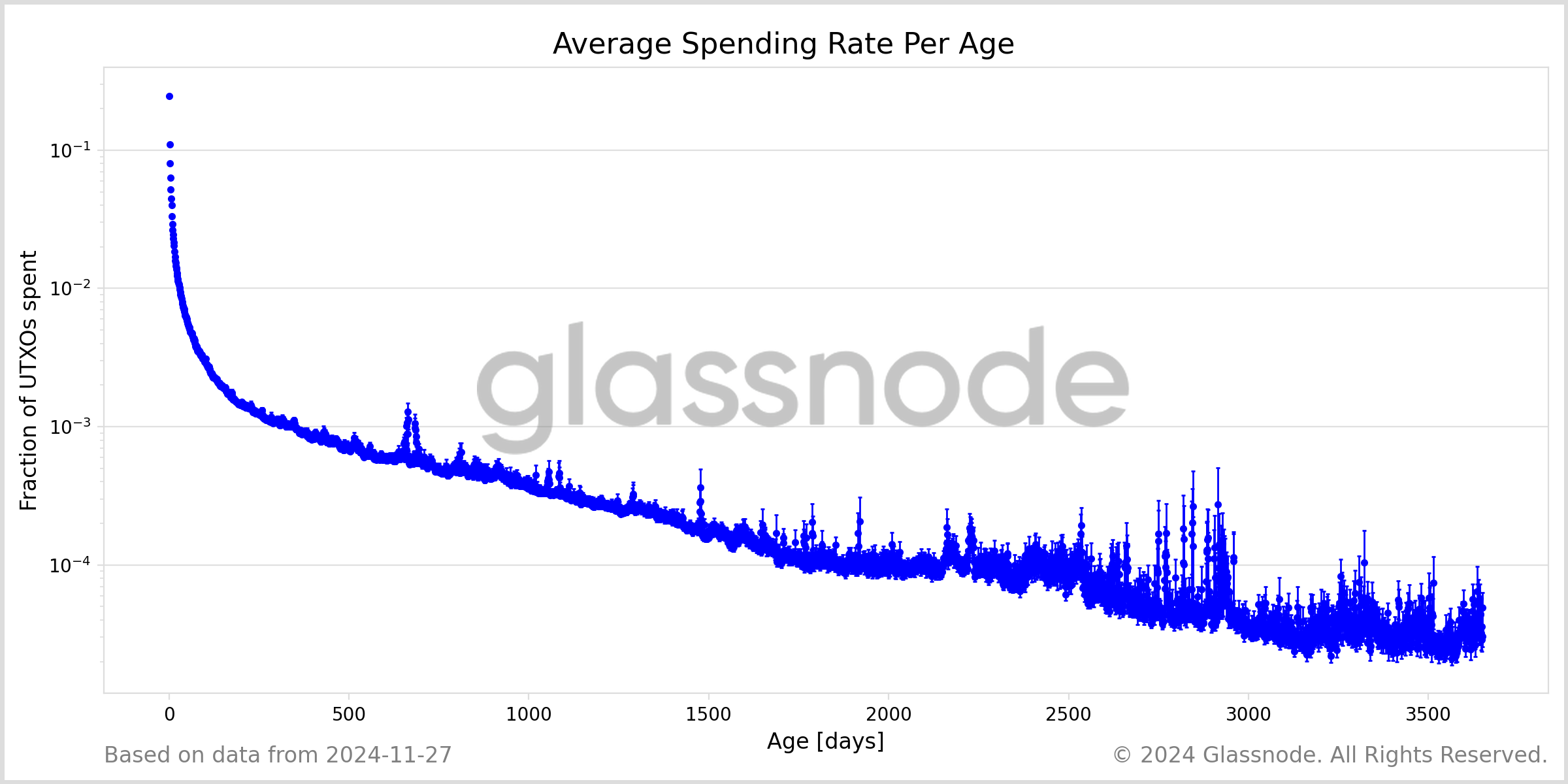

We then calculate the average spending rate for each age across the entire dataset, along with the standard errors of the mean. Figure 1 visualizes the average spending rate by age.

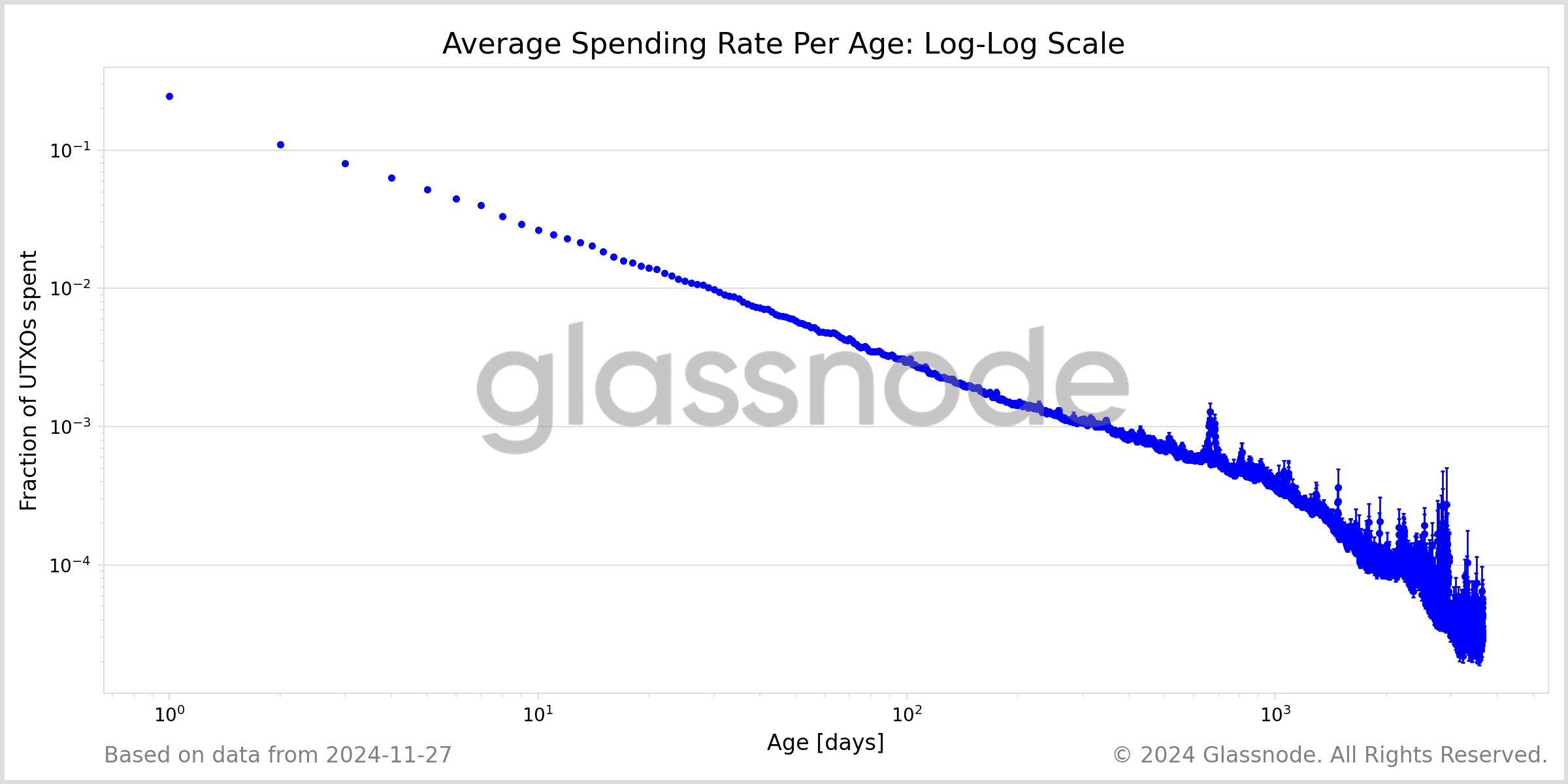

Power-Law Dynamics in Log-Log Space

To better understand the relationship between UTXO age and spending rate, we plot the data in log-log space. This transformation is beneficial because a power-law relationship appears as a straight line in log-log space, making it easier to identify and analyze. Figure 2 shows the log-log plot of spending rates.

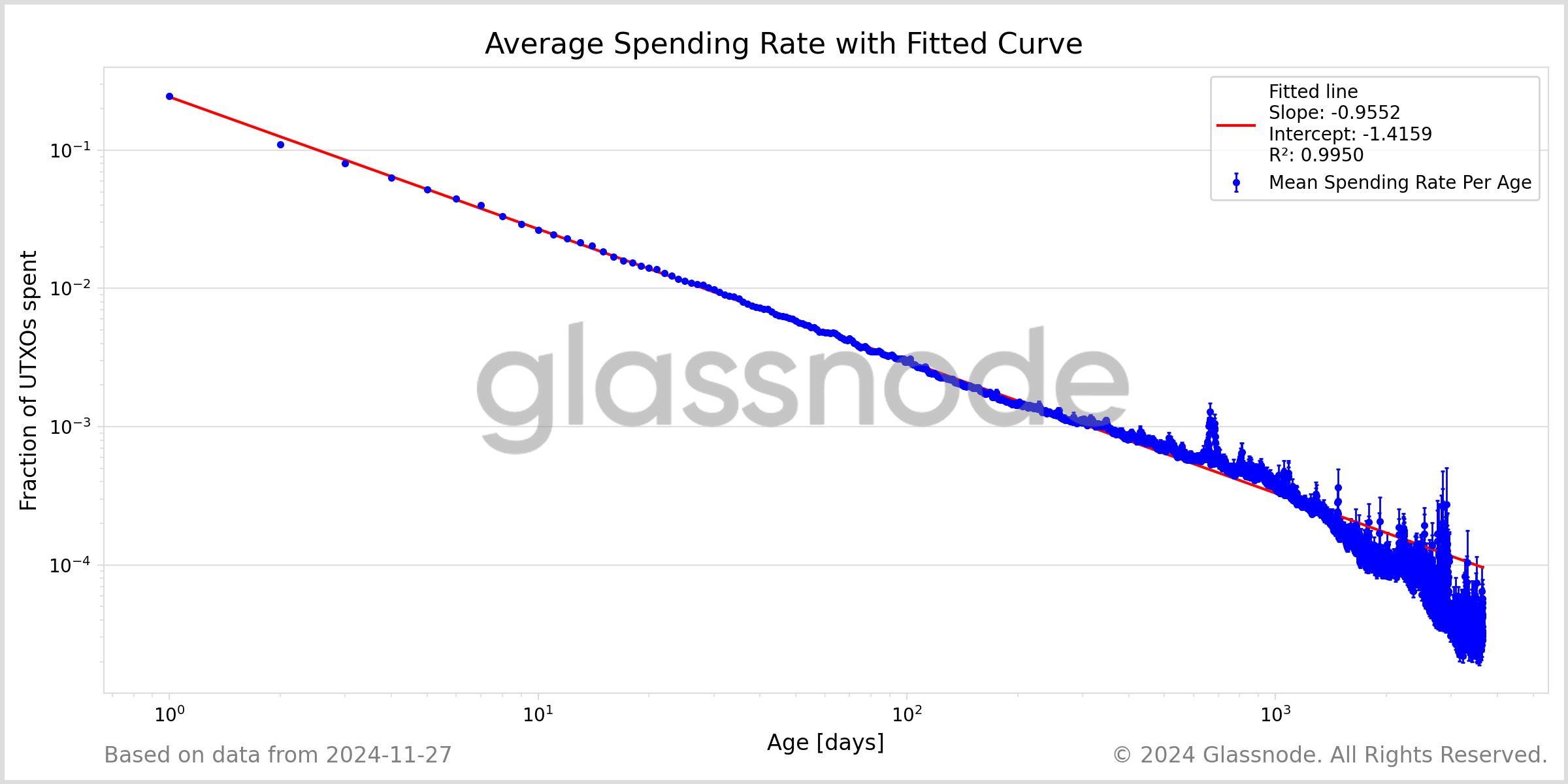

Fitting the Power Law

We perform a linear regression on the log-log data to quantify the power-law relationship. We use weighted least squares for the regression, with weights proportional to the square of the UTXO counts divided by the square of the standard errors of the mean. This weighting accounts for the varying reliability of data points due to differing sample sizes and variances.

The slope of the regression line corresponds to the power-law exponent, indicating how rapidly the spending probability decreases with age. Figure 3 presents the fitted regression.

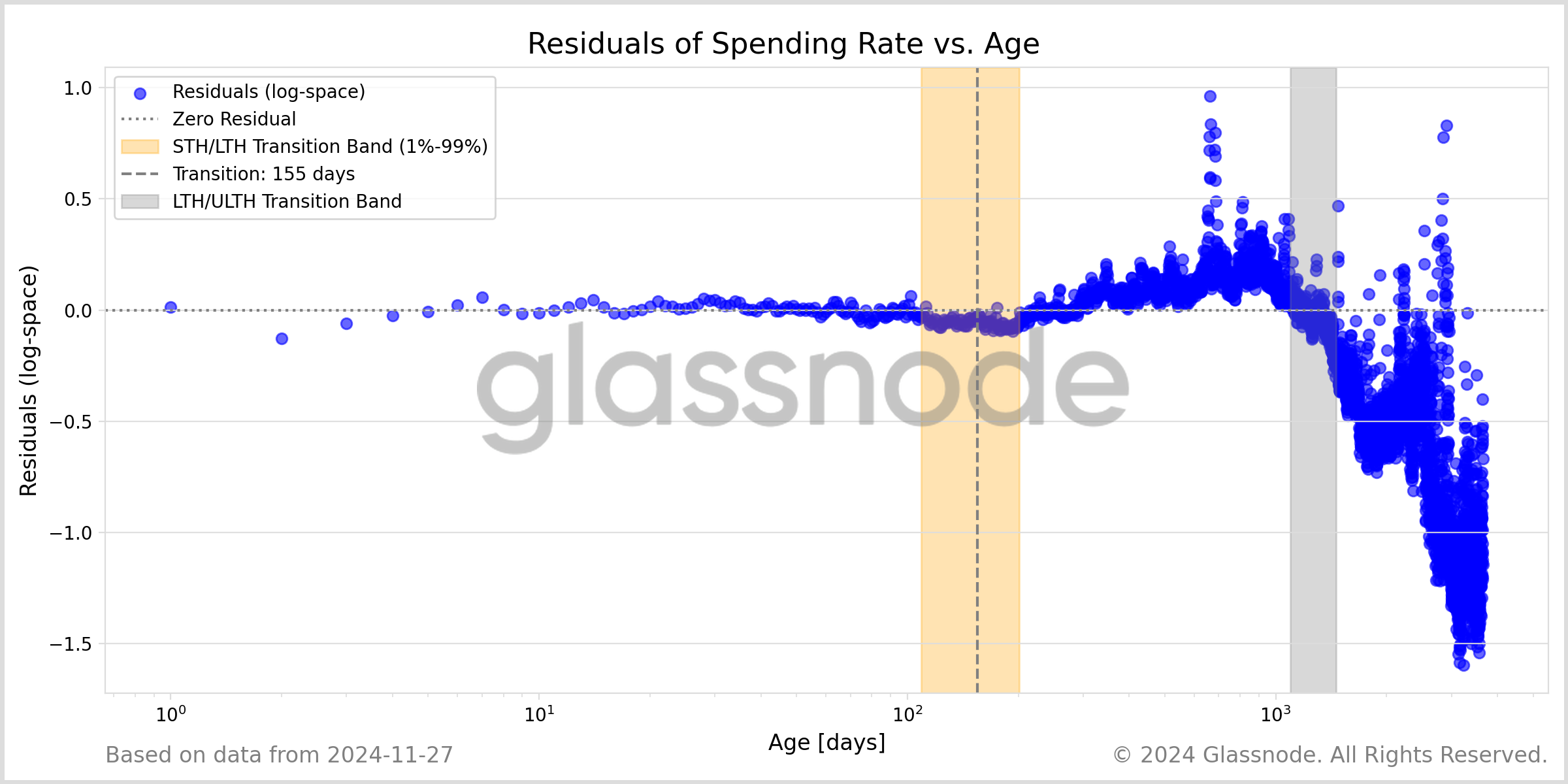

Analyzing Residuals to Assess Fit Quality

To evaluate the quality of the power-law fit across different age cohorts, we analyze the residuals, which are the differences between the observed mean spending rates and the values predicted by our model. Plotting residuals helps us identify patterns or systematic deviations from the model. Figure 4 shows the residuals as a function of UTXO age.

We observe minimal residuals for UTXOs up to around 200 days old, indicating a high predictability within this cohort. This aligns with the gradual transition from Short-Term Holders (STH) to Long-Term Holders (LTH). A sigmoid function models this transition to obtain a smooth shift in holder behavior. The central point of this transition is at the 155-day mark, representing a 50-50 split between STH and LTH classifications. At around 200 days, the transition from STH to LTH is completed at 99%.

Our analysis demonstrates that the power-law model fits nearly perfectly for STH coins until they fully transition into LTH. The model continues to hold well — with small deviations —f or LTH coins aged up to 3-4 years (the second transition band). These deviations suggest a slightly higher spending probability than the model predicts for the mid-term LTH cohort.

However, for ultra-long-term holders (ULTH) — coins aged beyond approximately one halving cycle — we observe more significant deviations from the model. Specifically, the observed spending probabilities are lower than those predicted by the power law. This indicates an even greater tendency to hold these coins, possibly due to strong hodling convictions or the possibility that some of these coins are lost.

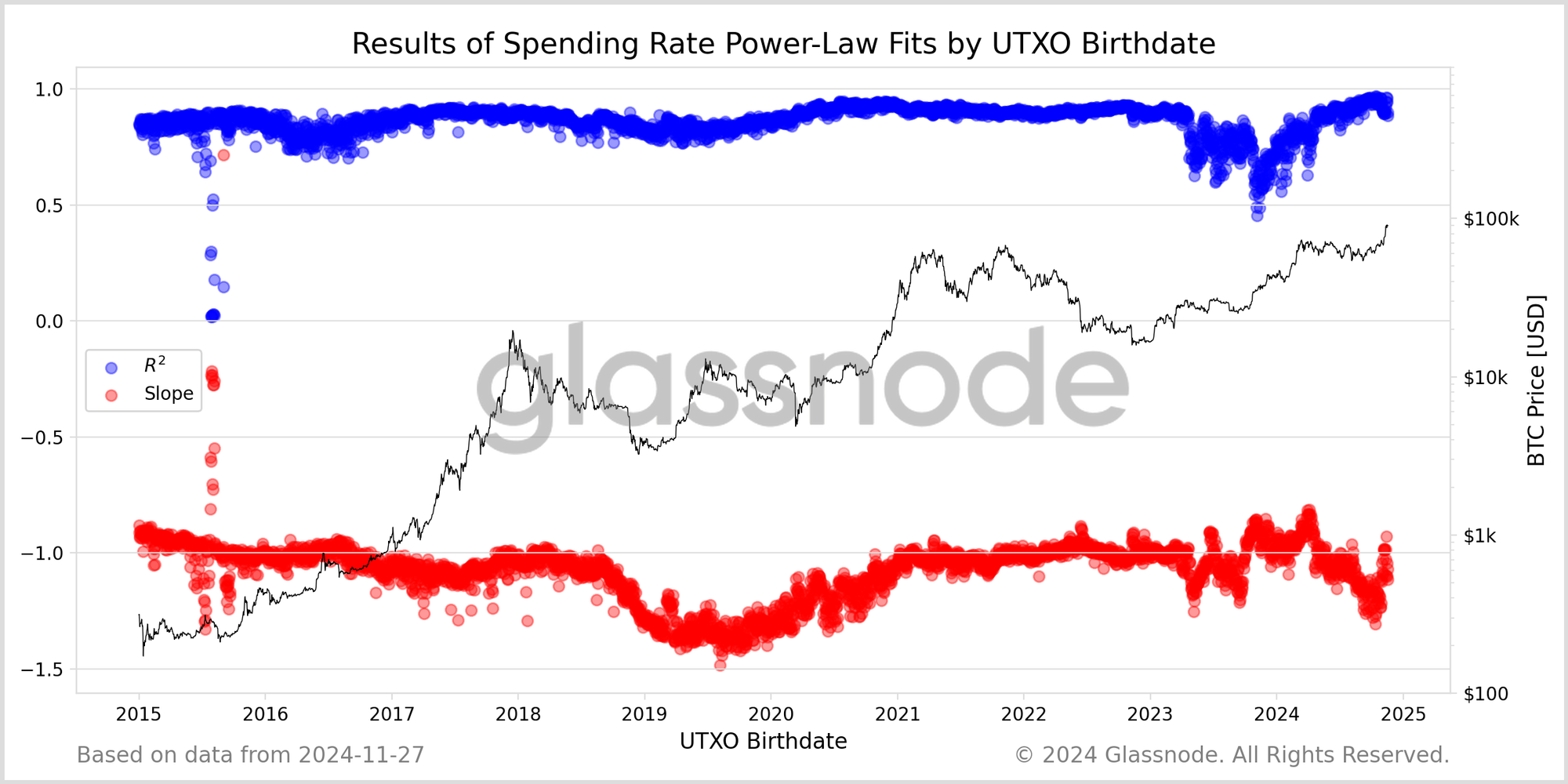

Power-Laws by Birthdate

We take another perspective to investigate whether the power-law dynamic of coin spending probabilities changes over time. Instead of averaging UTXO counts per age over all dates, we track groups of UTXOs born on the same day throughout their lifetime. Following these birthdate groups, we can analyze how spending rates evolve for coins originating at different points in Bitcoin's history.

For each birthdate group, we calculate the spending rates day by day as the cohort ages. We then perform a linear regression on the log-log spending probabilities for each group individually. Neglecting the most recent birthday groups with a recorded live of less than 10 days results in about 3600 remaining groups and corresponding linear regressions.

The coefficient of determination (R²) of each regression indicates how well the power-law model fits the data for that cohort. The slope of each line gives insights into how rapidly the spending rates decline with coin age. Figure 5 plots the R² values and line slopes for each birthdate group over time.

Overall, the power law holds remarkably well across different birthdates, confirming the consistency of this dynamic over time. However, specific periods exhibit lower fit quality, although there is no apparent correlation to price movements during these times. We observe a pre-longed period of steeper spending probabilities (smaller slope values) throughout 2019. One possible interpretation is that investors who bought at that time amidst the -80% drawdown from the 2017 ATH did so for the long term, and consequently, their spending rate is steeper than typical.

Implications for On-Chain Analytics

These findings provide a continuous perspective on coin age and spending probability, complementing the existing LTH/STH framework. The power-law relationship captures the gradual transition from active trading to long-term holding.

Notably, the model fits nearly perfectly for younger coins and continues to hold well — with only minor deviations— for coins aged up to about four years. Beyond this age, deviations from the model become more significant, indicating that additional factors may influence the spending behavior of ultra-long-term holders.

The power law with a slope close to one offers a clear and intuitive rule of thumb: for every tenfold increase in a coin's age, its probability of being spent decreases by approximately a factor of ten. This is illustrated in the following table of approximate model values:

| Age (days) | Spending Rate |

|---|---|

| 3 | 10% |

| 30 | 1% |

| 300 | 0.1% |

| 3,000 | 0.01% |

This predictable decay in spending probability underscores the behavioral pattern where younger coins are actively traded or speculated upon while older coins become increasingly dormant over time. By embracing this continuous perspective, analysts and investors gain a richer understanding of the gradual decline in spending activity as coins age, enhancing the interpretation of on-chain data and investor behavior.

Quantifying the Hot Supply Assumption

Our analysis also allows us to quantify the hot supply assumption, which posits that coins younger than one week are highly likely to be spent and thus are considered part of the "hot" supply. Based on our data, we evaluated a simple predictive heuristic:

- If a UTXO is younger than 7 days, assume it will be spent that day. Otherwise, assume it will not be spent.

Using historical data, this heuristic achieves an impressive accuracy of 98%, indicating that it correctly predicts whether a UTXO will be spent in the vast majority of cases. However, the high accuracy figure can be somewhat misleading due to the imbalance in the dataset—where there are significantly more UTXOs that remain unspent on any given day.

Conclusion

Our analysis reveals that Bitcoin UTXO spending behavior is governed by a robust power-law dynamic, with older coins being progressively less likely to be spent. The power-law relationship fits nearly perfectly for younger coins and continues to hold well—with only minor deviations—for coins aged up to four years (aka. one cycle). Deviations from the model become more pronounced for ultra-long-term holders beyond this age, indicating even lower spending probabilities than the model predicts. This suggests that additional factors, such as strong holding convictions or lost coins, influence the spending behavior of these oldest UTXOs.

This finding enhances the existing LTH/STH framework by providing a continuous mathematical perspective on the gradual shift from active trading to long-term holding. The power law offers a precise rule of thumb: for every tenfold increase in a coin's age, its probability of being spent decreases by approximately a factor of ten. This predictable decay in spending probability provides valuable insights into investor behavior and coin dormancy over time.

As Bitcoin continues to evolve, the power-law model provides a mathematically grounded framework for on-chain analysis, enabling a deeper understanding of the lifecycle dynamics of UTXOs.

Disclaimer: This report does not provide any investment advice. All data is provided for information and educational purposes only. No investment decision shall be based on the information provided here and you are solely responsible for your own investment decisions.

Exchange balances presented are derived from Glassnode’s comprehensive database of address labels, which are amassed through both officially published exchange information and proprietary clustering algorithms. While we strive to ensure the utmost accuracy in representing exchange balances, it is important to note that these figures might not always encapsulate the entirety of an exchange’s reserves, particularly when exchanges refrain from disclosing their official addresses.

We urge users to exercise caution and discretion when utilizing these metrics. Glassnode shall not be held responsible for any discrepancies or potential inaccuracies.

Please read our Transparency Notice when using exchange data.

- Join our Telegram channel.

- For on-chain metrics, dashboards, and alerts, visit Glassnode Studio