DeFi Uncovered: Exploring the Sushi Ecosystem

As the DeFi market continues to demonstrate a risk off appetite, we embark on a deep dive assessment of the fundamentals and performance of the Sushi project.

The crypto markets have caught a strong bid this week, with ETH finding its way back towards the top end of the trading range at $2,423. DeFi tokens have also traded higher, generally trading back to levels from early July.

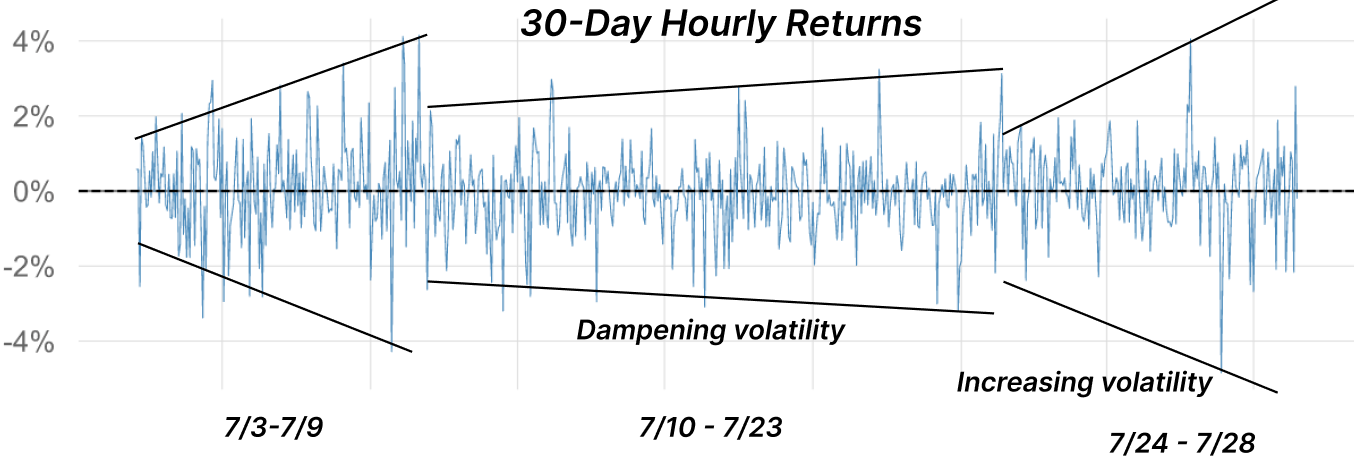

As noted in our past discussion on volatility, the extended tightening of vol created a coiled spring that has since uncoiled.

In this piece, we will explore:

- Weekly assessment of the DeFi market response to a week of positive price action.

- Feature piece on the adoption and growth of the Sushi ecosystem to assess the standing of the project to date.

Overview of DeFi Performance

Despite the uptick in prices across the ecosystem, fundamentals for most major DeFi projects remain well below the highs. We are yet to see a renewed positive correlation between price volatility and DeFi application usage. Instead, fundamentals are flat while prices have ticked up since the selloff back in May.

Some summary examples:

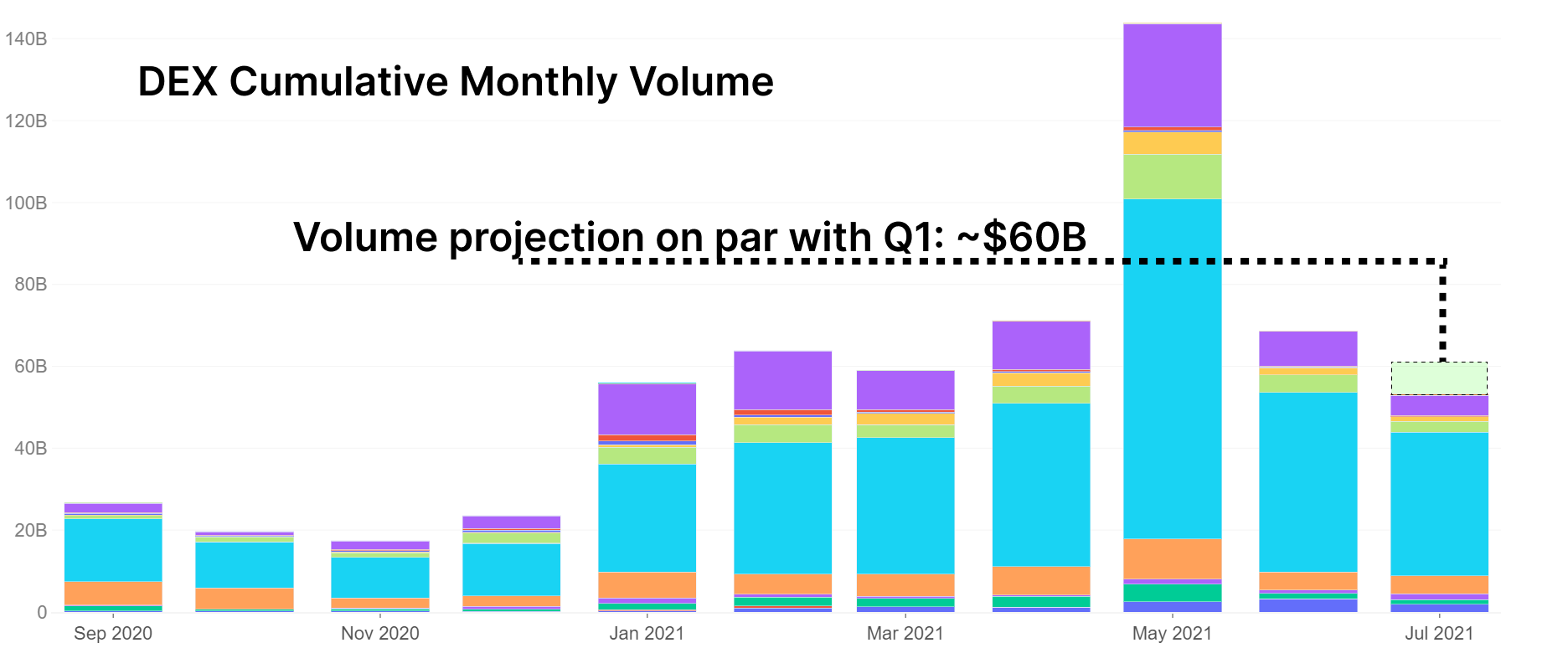

- DEX volumes have returned to early 2021 levels

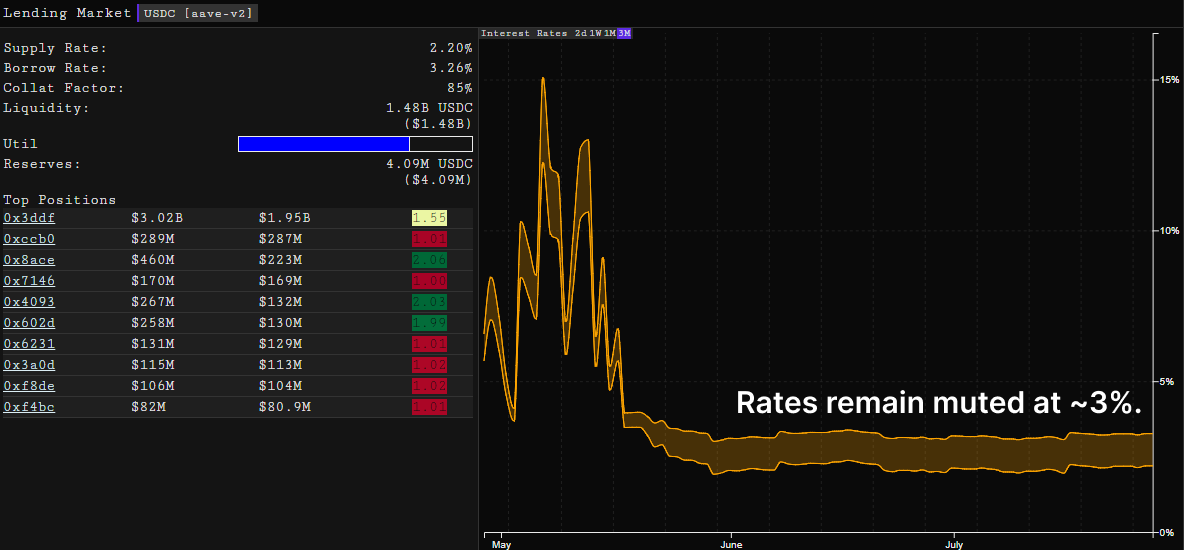

- Borrow utilization remains low with interest rates continuing to compress

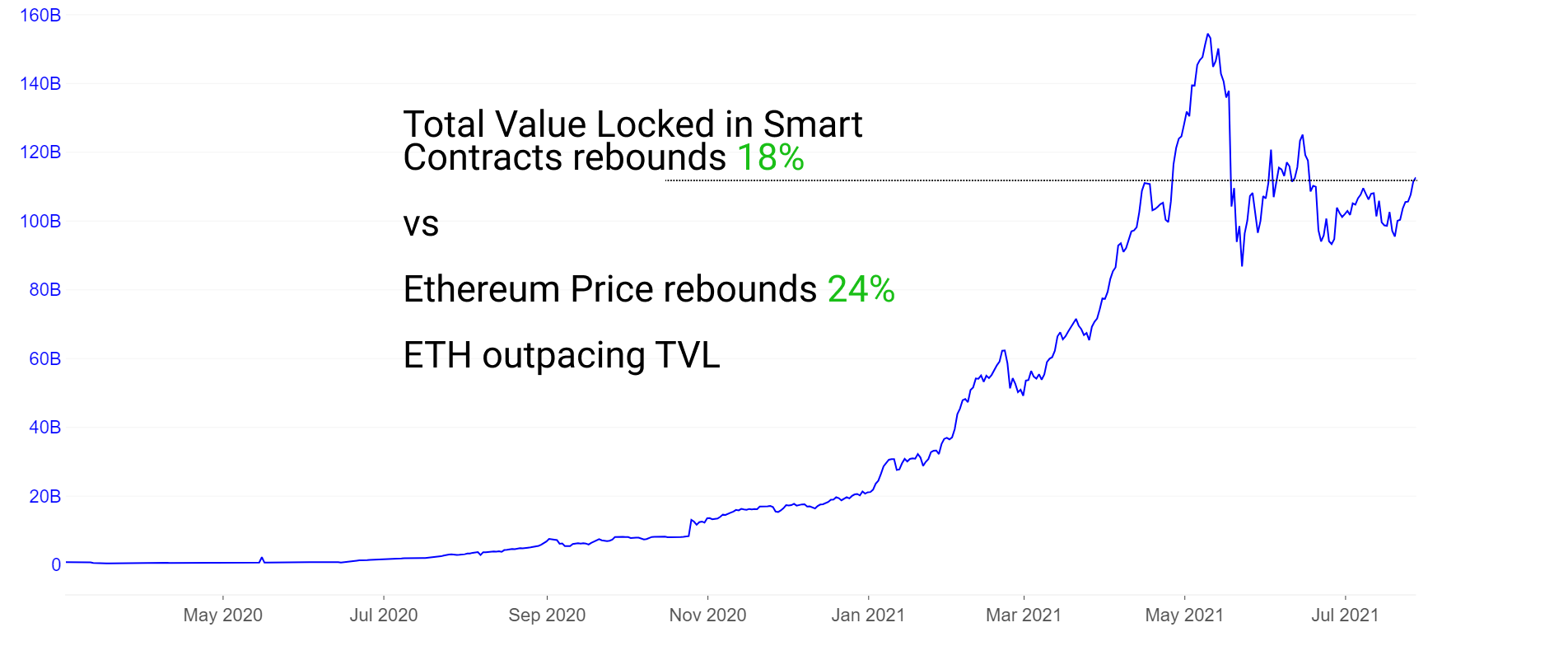

- Total Value Locked is rising, but is being outpaced by the change in ETH price

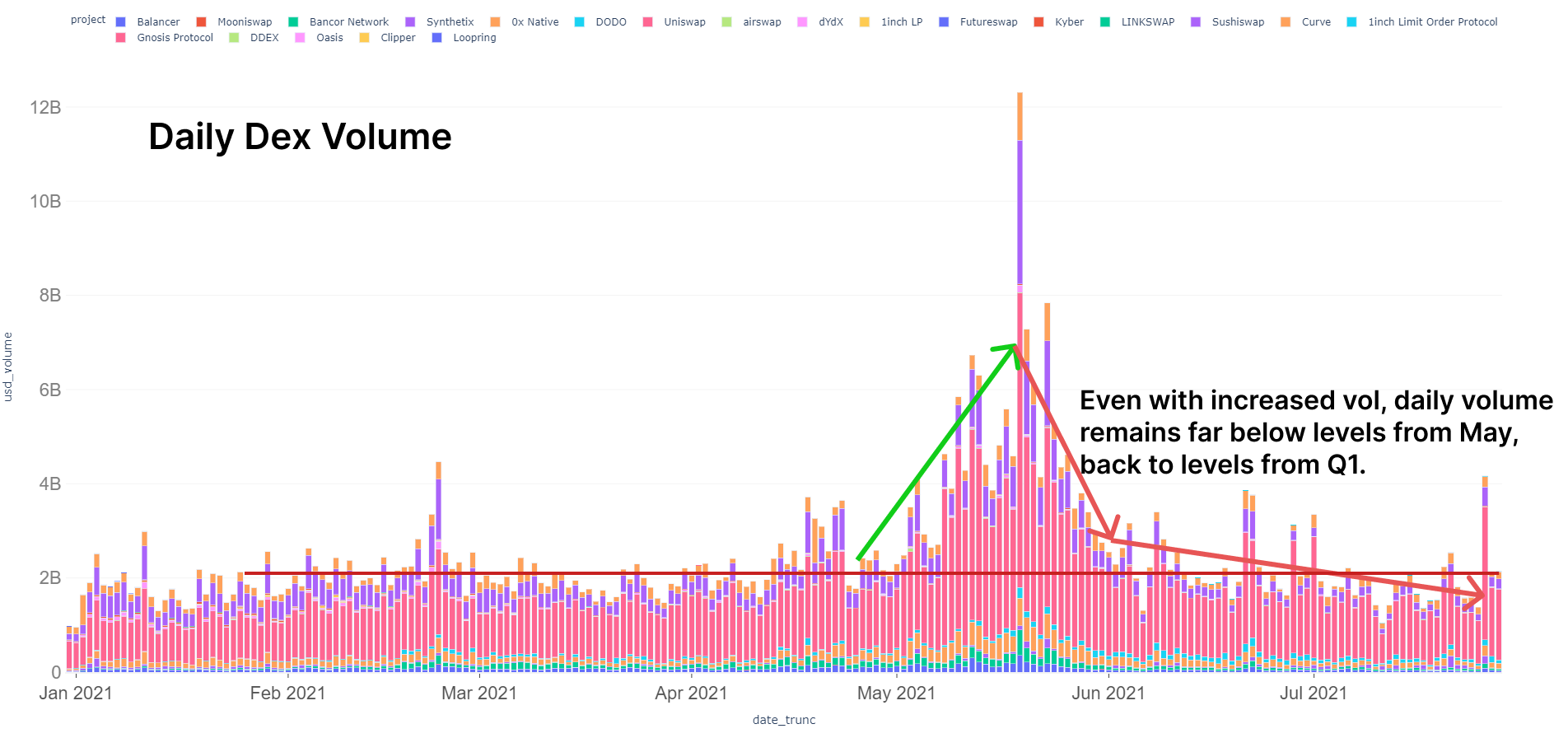

Price volatility usually has a direct correlation with increased DEX volumes. Daily trading volumes this week ranged between $1.5B and a high reaching over $4B on the 26th across all Ethereum DEXs. This level remains firmly below May/June highs.

The day after the peak on July 26th, cumulative DEX volume in this volatile period has barely reclaimed levels from earlier this month during dampened volatility. Even with this temporary uptick the last week, cumulative volume for the month remains firmly below levels from Q1, competing against volume from January.

When there is significant demand for speculation and trading of tokens, DeFi interest rates tend to increase as the demand for leverage increases. As a sign of general market hesitancy, the demand for leverage remains muted, leading to compression of rates. This is a piece of strong evidence that the market holds a risk-off appetite, largely unphased by the move up of the last few days.

Total Value Locked (TVL) has risen, but only in direct relation to the price of ETH. In a risk-on environment it is expected that TVL would spike as fresh money rushes into DeFi farming opportunities and governance tokens for Pool 2. Instead, the price of ETH has outpaced the rise in TVL which speaks to a lack of new capital inflows and instead a repricing of existing collateral already in the system.

Weekly Feature: Exploring the Sushi Ecosystem

Across the DeFi ecosystem, one project that has been high in the conversation of late is Sushi. Once simply referred to as Sushiswap for its flagship Sushiswap product, Sushi has since expanded to become an ecosystem of DeFi applications, focusing on tight integration with various partner projects in the space. The project aims to distinguish itself via commitment to community ownership, consistent shipping of products, and a bold approach to innovation and experimentation.

A quick overview of the products and core features Sushi has shipped since inception in August 2020:

- Sushiswap AMM: boasting strong liquidity, volume, and holding the position as the primary source of liquidity for numerous projects in the space. The AMM also provides some of the highest rewards for liquidity providers and token stakers via the minting of new SUSHI tokens alongside trading fees.

- Trader Tooling: features and tooling in the AMM designed to improve the experience of traders such as private transactions via ArcherDAO to dodge MEV, limit orders (Polygon only for now), and more parameters for traders to adjust.

- Kashi Lending: small isolated lending markets that fit a variety of niche borrowing demands. Their long tail borrowing market remains relatively underutilized but supports a wide variety of assets with varying levels of liquidity.

- Miso: fair launch platform designed for launching new projects, NFTs, and other sales via custom designed auctions - crowd, batch, and dutch style.

- xSUSHI: undeterred by the lack of regulatory clarity, Sushi was very early in returning a portion of protocol fees to token holders. Stakers of SUSHI receive xSUSHI, a token that has earned a typical ~5-7% APY sourced from 0.05% of AMM trading fees. As the ecosystem expands into lending and more products, the potential for additional sources of revenue for xSUSHI holders come to light.

- Multichain support: with support for 10+ blockchains. Whilst adoption remains dominant on the Ethereum mainchain, Polygon now makes up ~20% of Sushi's DEX volume. Sushi deployments on other chains are fairly underutilized for now.

Core to the Sushi ecosystem is their Onsen program, which is an incentive system built on top of Sushiswap to encourage projects to bring liquidity to Sushi, rather than competitors. Stakers of Sushi liquidity positions earn SUSHI tokens on top of trading fees on the DEX. These Onsen rewards have precipitated numerous partnerships between DeFi projects and Sushi, making Sushiswap a primary liquidity provider, especially for early phase projects.

Projects are able to incentivize liquidity with SUSHI instead of diluting their own tokens. That said, select projects have accessed the new Masterchef v2 contract, allowing rewarding both SUSHI and their native tokens as rewards (ALCX, MPH, PICKLE, CVX).

Sushi By the Numbers

At the core of Sushi is its exchange product Sushiswap AMM. From a high level view we can measure its usage by volume, liquidity, and number of users interacting with the protocol.

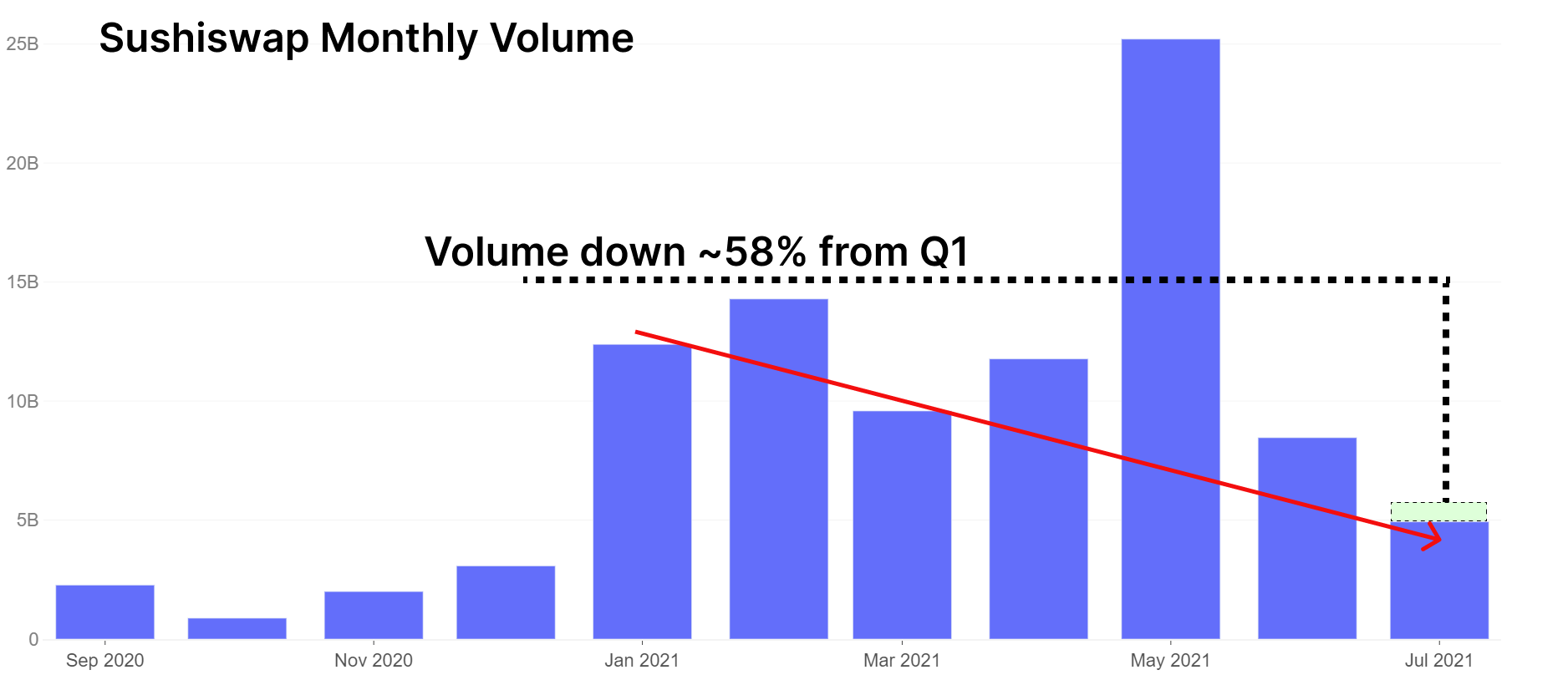

Monthly Sushiswap volume has declined quite significantly relative to performance in Q1, with expectations for July hovering around $5B in trading volume, down around 58% relative to the average of $8.6B in Q1 of this year.

It's important to note that the above chart is Sushsiwap volume on Ethereum mainchain. If we factor in the additional volume occurring on Polygon, this adds an additional ~$1.1B in the month of July, representing nearly 20% of the total monthly volume.

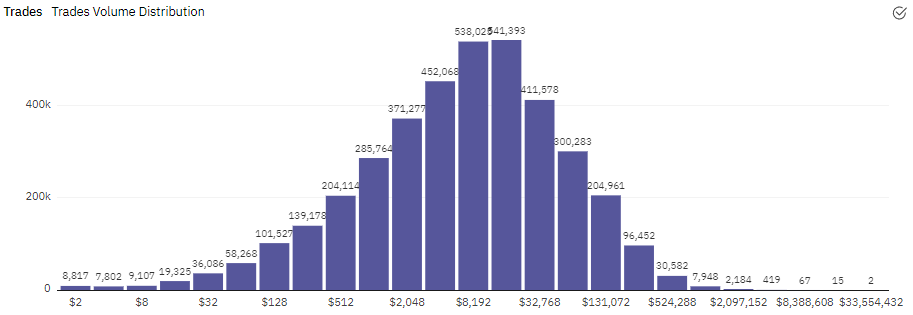

Sushiswap trade sizes see the bulk of transactions falling between $500 and $50,000. The chart below presents the distribution of trade sizes showing the mean size is between $8.2k and $32.8k. Sushiswap benefits from trades sourced via aggregators which route liquidity through the AMM, especially for pairs with deeper liquidity such as WBTC-ETH and USDC-ETH.

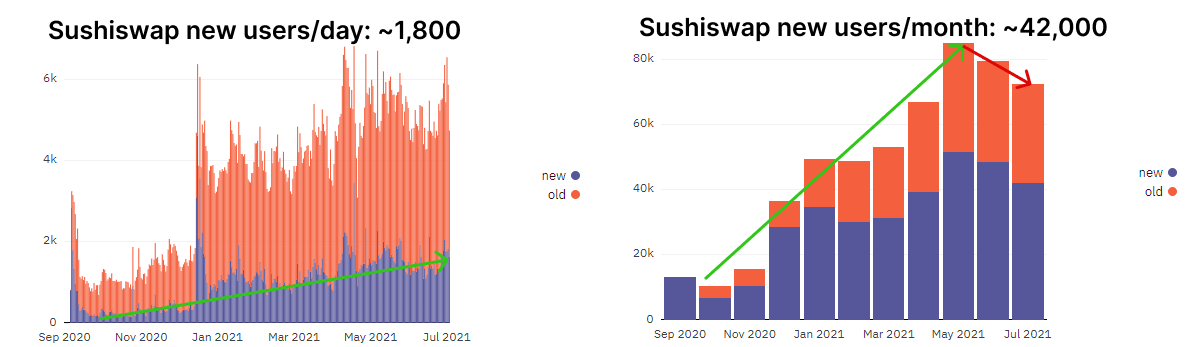

By users, Sushiswap has relatively low penetration comparative to its peers.

For comparison, 2.4 million addresses have interacted with Uniswap. Uniswap is adding about 40,000 users/week and 6,000 per day. Keep in mind, this is unique addresses, users often have more than one address. True user counts are lower. See below the daily and monthly address additions for Sushiswap. User growth has flattened across the space, and in this regard Sushi is no exception. Note Uniswap growing at 3x the pace of Sushiswap despite heightened penetration.

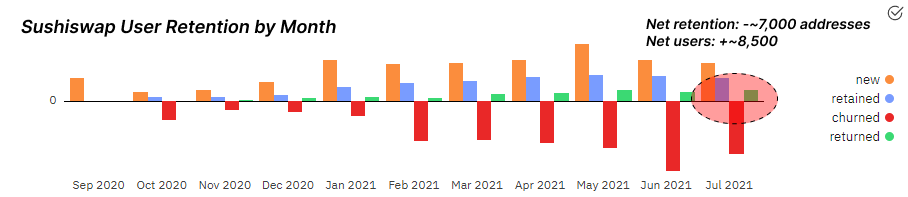

Perhaps more interesting are Sushi's user retention numbers. Retention measures the number of traders that continue to come back and use the protocol again. Measuring monthly retention we see Sushi is churning more users than are returning, suggesting more users are not returning than are new and coming to the platform. Total user numbers have increased but this is specifically due to new addresses coming to the protocol.

With constantly awarded SUSHI to liquidity providers, liquidity has remained strong since the protocol's launch in August. Note the volume/liquidity ratios for Sushiswap on Ethereum vs Sushiswap on Polygon this month.

For every $1 of liquidity on Ethereum, Sushi saw $2 of trading volume. For every every $1 of liquidity on Polygon, Sushi saw $2 in volume on Polygon. With increased efficiency, Uniswap v3 is expected to do in excess of $20B in volume this month on $2B in liquidity. This is 1$ of liquidity for every $10 in volume, showcasing the increased efficiency and usage per dollar on Uniswap v3 versus Sushiswap.

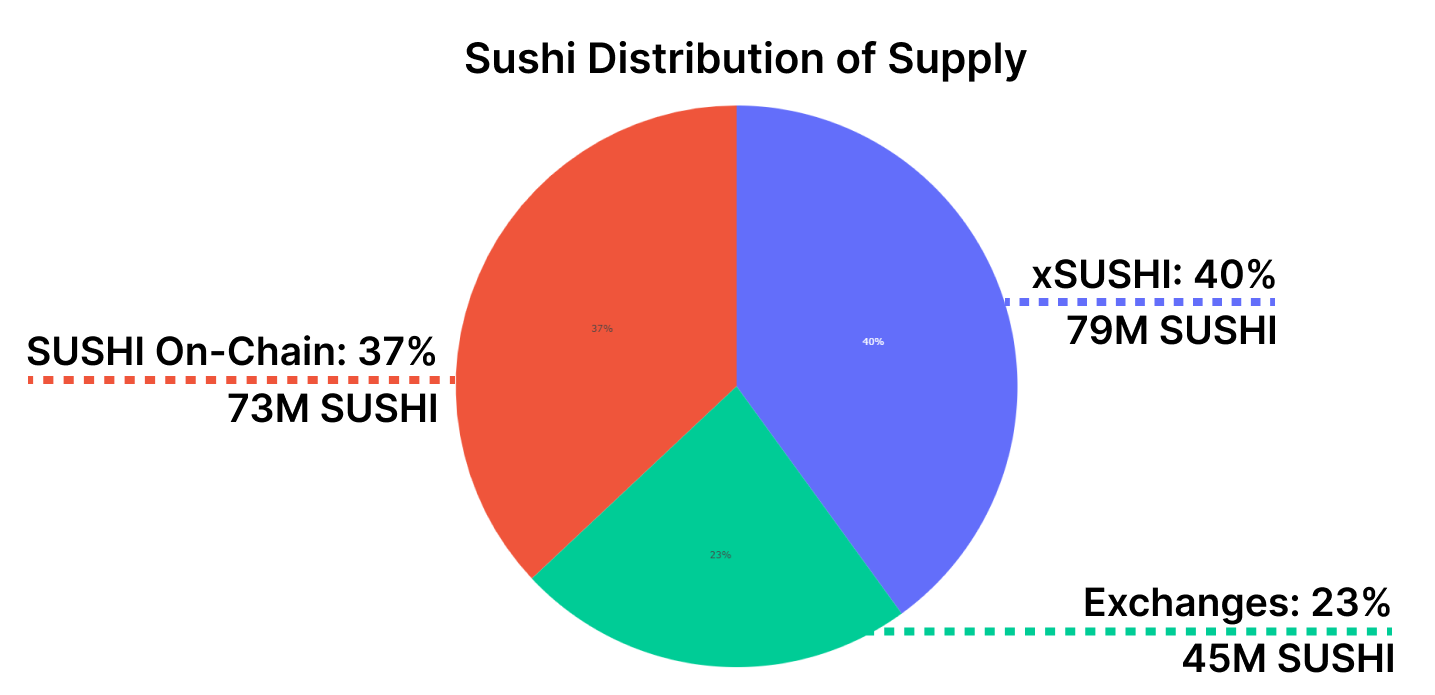

SUSHI Supply Dynamics

Of circulating SUSHI, roughly 40% is staked as xSUSHI, earning revenue from trading fees. The remaining Sushi is held either in on-chain in wallets (37%) or on centralised exchanges (23%).

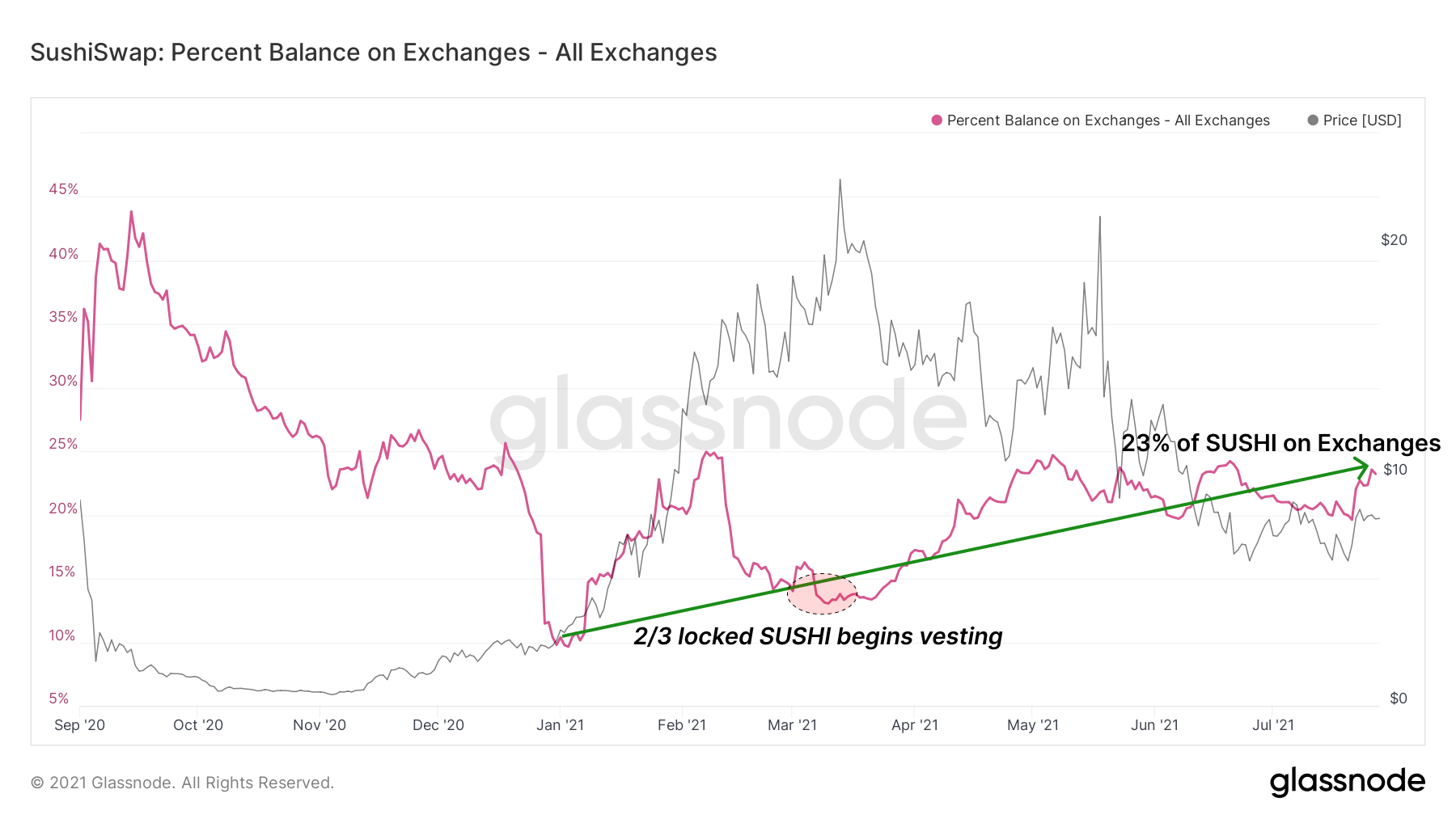

SUSHI tokens awarded to liquidity providers since inception of the project were given vesting periods. 1/3 were automatically vested, the other 2/3 continuously vesting after 6 months. As of April 2021 this vesting schedule was removed in favor of immediate vesting of all rewards. We can see an uptick in exchange balances starting at the period in which vesting of those 2/3 rewards begins.

The vesting rewards from 2020 and Q1 2021 are still actively vesting until October of this year. Once October/November has passed, these extra SUSHI rewards will have fully vested. Until then, there remains additional sell-side pressure as these rewards become liquid for early liquidity providers.

In other Sushi products, we've seen relatively muted adoption. Kashi lending supports primarily long-tail lending markets. Their chief competition continues to be Rari Capital's Fuse, Cream, and alternative markets on Aave. Of the three, Cream and Aave's long-tail products remain with fairly low adoption rates, while Fuse has found some success partnering with smaller communities.

Kashi success has been similar to both Cream and Aave, with long-tail markets remaining a generally low demand product. It's important to note that their partnering with small projects on AMM liquidity has managed to garner adoption with smaller project token pairs.

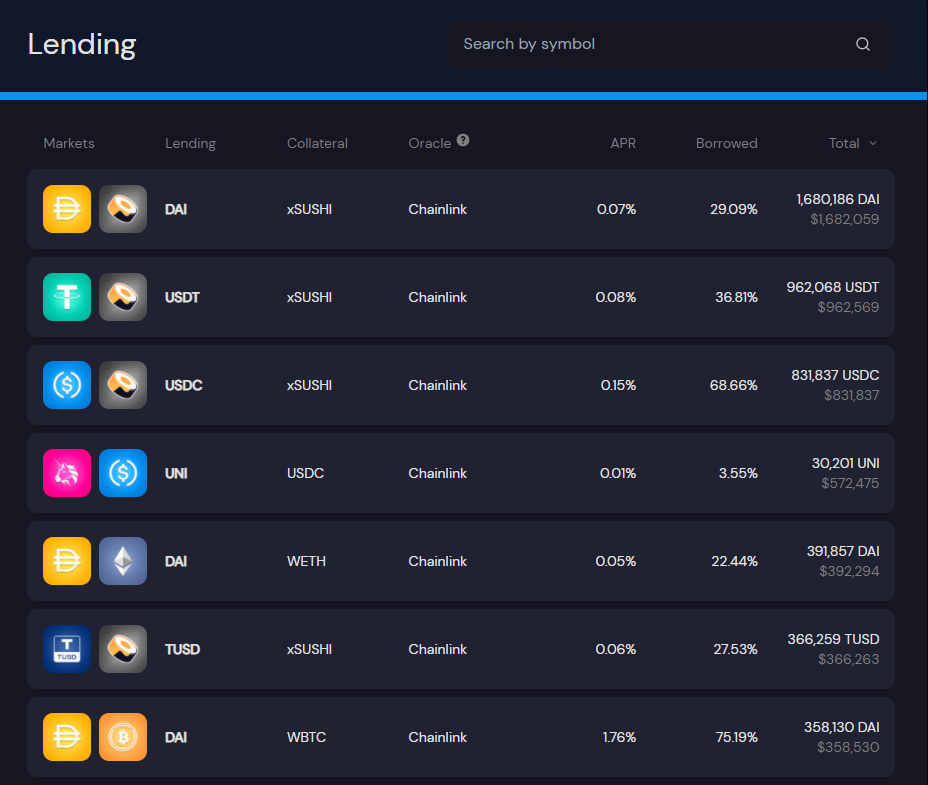

The largest Kashi liquidity pairs are for the protocol native xSUSHI.

xSUSHI can additionally be lent and borrowed on the Aave platform. In Aave's xSUSHI markets there is around $175M in supply with about 6% borrow utilization. Lenders continue to earn rewards for holding xSUSHI all while using their xSUSHI as collateral to borrow other assets.

Sushi's MISO product has hosted a handful of interesting auctions, starting out with the sale of Sake via a dutch auction mechanism. They've since followed that up with an additional 9 auctions, one which included the hotly anticipated YGG token of Yield Guild, the creators of Axie Infinity and other upcoming crypto games. The sale ended in 30 seconds with 32 large participants claiming $12.5M worth of YGG tokens.

Future of Sushiswap - Trident

In this competitive space, building products of the highest quality with continued dev momentum is critical for adoption. Last week Sushi announced their next generation AMM product, code name Trident.

The upcoming launch features three new types of pools:

- Hybrid pools: up to 32 tokens in a single pool. Trade like-kind assets. Can think of this pool similar to Curve's like-kind pools for stablecoins.

- Concentrated liquidity pools: add liquidity in ranges. These function just like pools from Uniswap V3. Undoubtedly Sushi has seen the success of increased capital efficiency and gone after their own design.

- Weighted pools: add liquidity with varying weights. These function similar to Balancer - for example, create a pool with an 80/20 weight of ETH/USDC instead of traditional 50/50 design.

Note that Sushi is basically taking what they see as the best of various DEX designs and building it into their own product. They appear unafraid by the challenge of making Sushi the one-stop shop for all DeFi needs.

Routing engine: In addition to these pool types, Sushi is building their own routing engine on top. This essentially will act as an aggregator, distributing trades among their various pools to route trades and minimize price impact for traders. They expect their various pool types to fragment liquidity, so the best possible Sushi trades will most likely require efficient routing and division of price impact.

Franchised pools: an attempt at onboarding centralized exchange (CEX) liquidity to their platform. Franchised pools will allow deposits from CEX users so orders can additionally route against CEX liquidity pools franchised by the protocol. These pools will include whitelisting capabilities so CEXs can remain compliant. Details on how this product will be implemented remain sparse.

Closing Remarks

With volatility returning to crypto token prices, fundamentals driven by usage remain relatively lackluster. However, DeFi usage even during a risk off environment demonstrates product fit with the market expressing a preference for lower yields, but with higher stability assets. DEX volumes remain down, borrow remains underutilized, and user growth continues to flatten.

Regardless of fundamentals, corners of the ecosystem like Sushi continue to build products and features by pushing the scope and potential of DeFi innovation. Of note for Sushi:

- Sushiswap volume, liquidity, and users remain quiet and declining, but year over year growth and product momentum remain strong.

- Expansion into the Polygon ecosystem has seen trading volumes on the sidechain represent 20% of the protocol's total volume.

- Kashi lending for long tail assets sees limited adoption, although xSUSHI's use as a collateral pair across the DeFi ecosystem is very strong.

- xSUSHI as a percentage of outstanding $SUSHI shows reasonable adoption, capturing 40% of the circulating supply.

- High percentage of vesting $SUSHI rewards continue to be sent to exchanges over time, potentially increasing the sell-side pressure on the token through to October.

Uncovering Alpha

This is our weekly segment that briefly discusses some of the most important developments of the prior and upcoming week.

Enthusiasm for building continues, regardless of price or fundamentals.

- YGG token launches in a Miso crowd sale. The controversial sale ended in 30 seconds with only 32 participants.

- Tokemak degensis event kicks off. The sale of their project's token TOKE has commenced, with $19M already committed for their token. The project goes after automated liquidity positions across DeFi.

- MakerDAO decentralizes. The DAO is becoming fully decentralized as it hands control of the protocol to the community/DAO and CEO Rune Christensen plans to step aside.

- Opyn launches Ziku, a point and click options setup. Ziku allows traders to point and click their way to a sophisticated options position, without needing to know the intricacies of how to put on such positions. Note that the options are still limited with very few contracts available.

- Thorchain sees second exploit for $8M. Thorchain has previously expressed its interest in building fast and in a hostile environment, creates risks inherent to such innovation. Teams that push past controversy like this and keep building often cement themselves in the space.

- Uniswap restricts a list of tokens, citing risks for their users. The list of tokens removed from the Uniswap front-end includes a number of derivatives products, showing Uniswap's likely alignment with regulators. The move marks an interesting point in DeFi where participants wrestle with the trustless nature of smart contracts vs often trusted nature of front-end products.

- KeeperDAO launches their much anticipated vaults. Liquidation protection from KeeperDAO with support for positions in Compound. Users additionally receive ROOK rewards in the process. A novel product idea with novel incentives built on top.

- Crypto researcher Hasu held a discussion with @MEVIntern on the subject of MEV. This is one of the better and more transparent discussions on this nuanced topic from an experienced MEV searcher. (LINK).

- Follow us and reach out on Twitter

- Join our Telegram channel

- For on–chain metrics and activity graphs, visit Glassnode Studio

- For automated alerts on core on–chain metrics and activity on exchanges, visit our Glassnode Alerts Twitter

Disclaimer: This report does not provide any investment advice. All data is provided for information purposes only. No investment decision shall be based on the information provided here and you are solely responsible for your own investment decisions.