The Week On-chain (Week 24, 2021)

Bitcoin becomes legal tender in El Salvador, whilst the market remains uncertain over macro direction. On-chain, Long and Short term investors are taking opposing sides of the trade.

Bitcoin has, once again, stepped into uncharted territory. This week, Bitcoin was officially voted in as legal tender in El Salvador, a truly historic moment for the industry. It also appears likely that the next major source of mining energy will be sourced from volcanoes. Was this on your 2021 bingo card?

Our engineers just informed me that they dug a new well, that will provide approximately 95MW of 100% clean, 0 emissions geothermal energy from our volcanos 🌋

— Nayib Bukele 🇸🇻 (@nayibbukele) June 9, 2021

Starting to design a full #Bitcoin mining hub around it.

What you see coming out of the well is pure water vapor 🇸🇻 pic.twitter.com/SVph4BEW1L

The week opened to relatively soft price performance, selling-off to a weekly low of $31,185. However, the market responded to the rapid passing of the bill in El Salvador with a rally back into the recent consolidation range, hitting an intra-day high of $39,269.

After becoming a distinguished macro-economic asset in 2020, it appears Bitcoin is transitioning out of the 'gradually' and into the 'suddenly' phase. This week, we investigate the on-chain behaviour of both short-term traders and long-term hodlers to the weekly events.

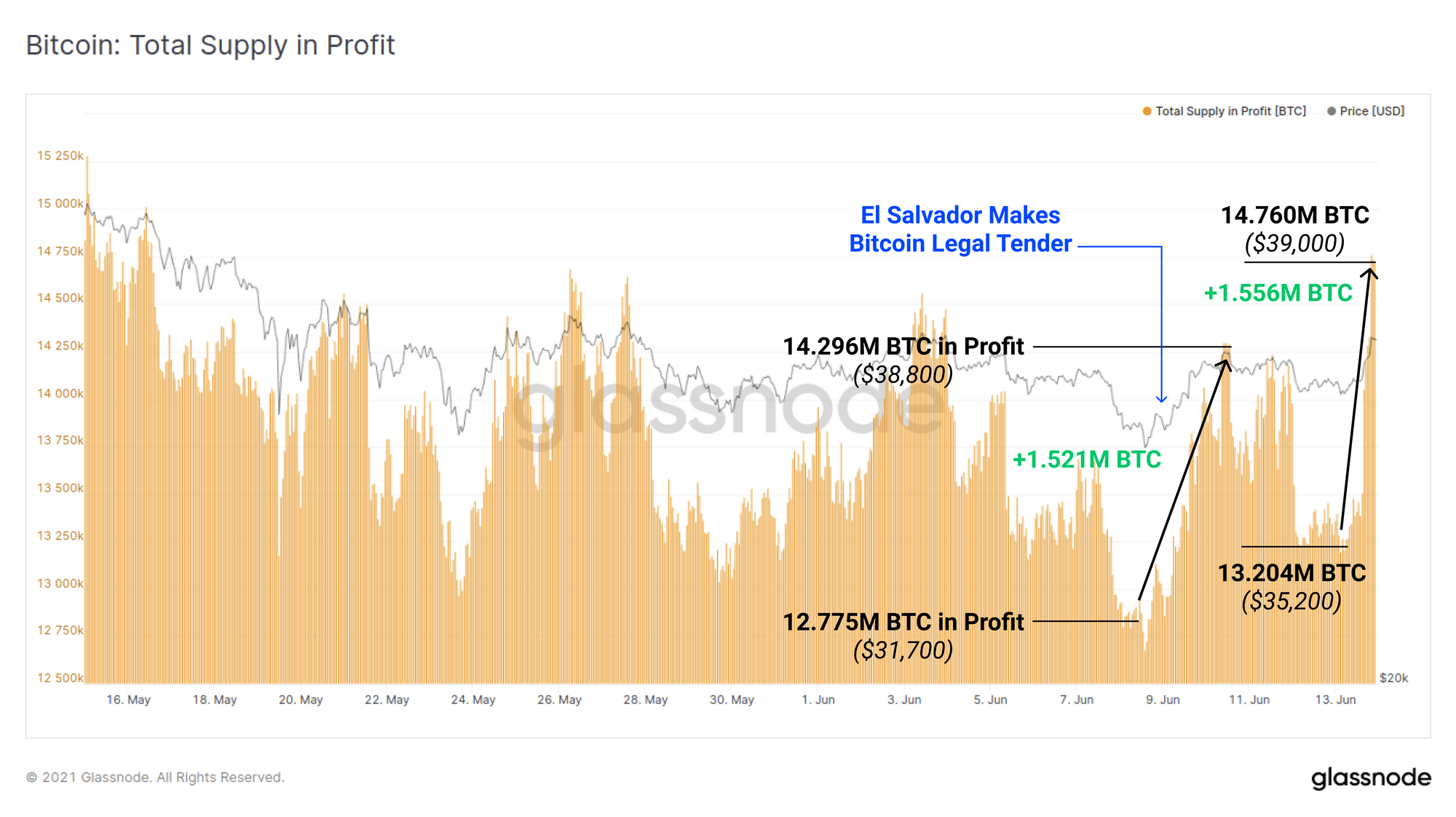

Profitable Supply Swings

The high volatility of Bitcoin markets makes it a magnet for traders, who are able to monetise price swings in both directions. Simultaneously, the powerful fundamental properties of Bitcoin make it a desirable store of value asset for long-term investors. During choppy and consolidating market structure, we can gain insight into the balance of supply and demand, and degree of accumulation by short and long-term holders, by observing changes in profitable supply during price swings.

Price rallied twice this week, first after El Salvador voted in the legal tender bill, and then again on Sunday afternoon. During both of these swings, the value held in profitable UTXOs jumped by around 1.5M BTC. Between both of these upswings, the weekly low of $31.7k to Sunday's high of $39.2k, a total of 1.985M BTC returned to an unrealised profit.

Whilst some of these coins are likely to those purchased back in January (similar price range) and remain unspent, we can estimate that at least 1.985M BTC (~10.5% of circ. supply) has an on-chain cost basis between $31.7k and $39.2k.

We can reasonably assume that this newly profitable supply is broadly held by three different cohorts:

- HODLers who purchased coins in early Jan 2021 and have not spent them. These coins are currently maturing across the 155-day Long-Term Holder (LTH) threshold.

- New HODLers who are buying the dip in the current range and likely to hold throughout whatever volatility lies ahead (hard to isolate in the data for now).

- Traders and Short-Term Holders (STH) who are trading price swings and are more likely to liquidate at price targets or in downside volatility. They are also more likely to utilise derivative markets and leverage.

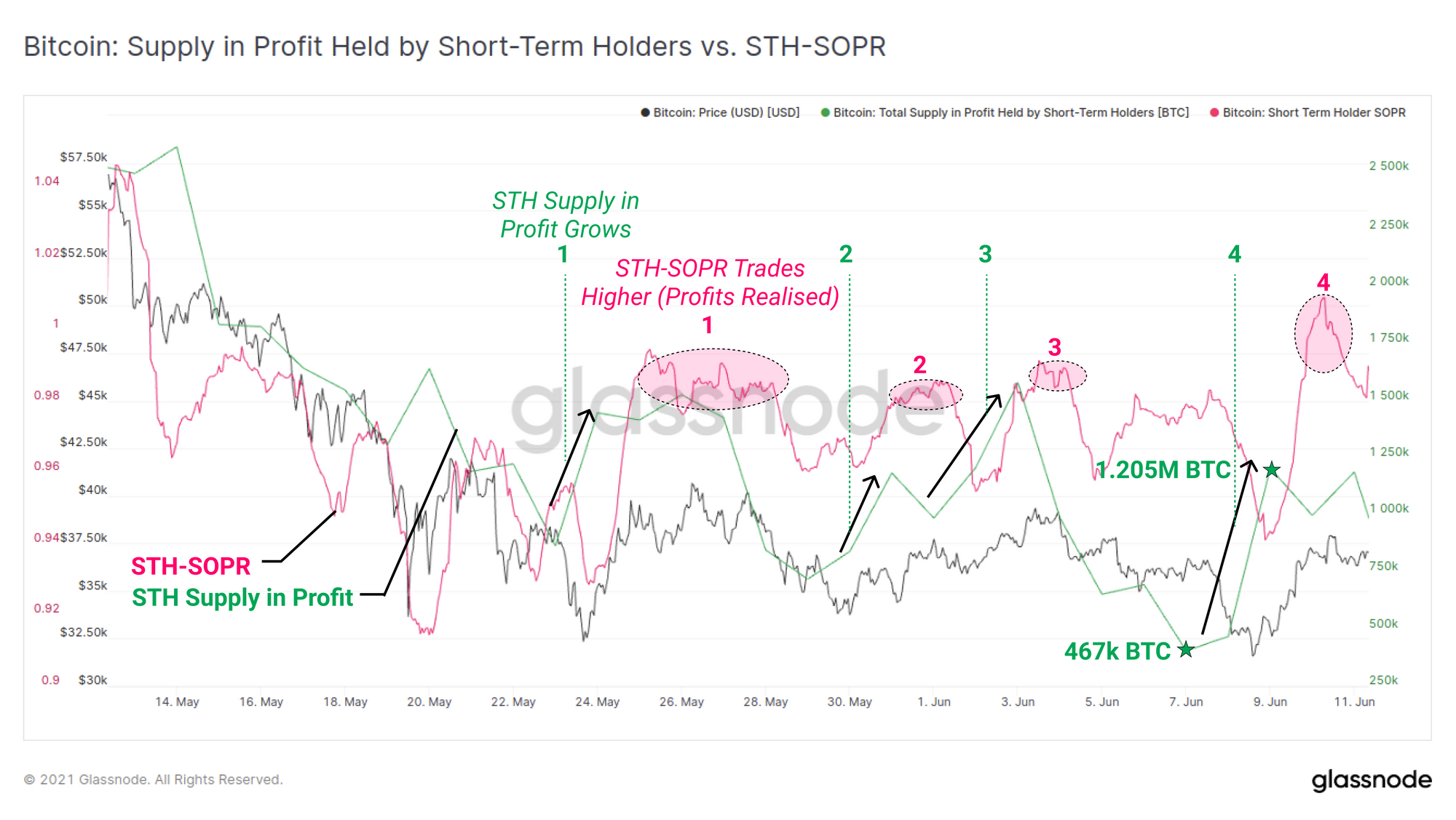

Traders Take Profits and Short Positions

Let's start with the last cohort, the Traders and STHs who are the most likely to generate overhead supply (sell pressure).

The chart below shows the amount of STH held supply in profit (green) and the STH-SOPR as a metric for the degree of profit taking (pink). There are two key observations here:

- Following each spike in STH profitable supply during price rallies (green 1, 2, 3, 4), the STH-SOPR spikes and holds an elevated level soon after (matching pink 1, 2, 3, 4). This indicates that some portion of this STH cohort are likely taking profits on swing trades or being shaken out by intra-day price volatility.

- During the price rally after the vote in El Salvador, around 737k BTC owned by STHs returned to profit (representing around 37% of the 1.985M from the last chart). As such, we can estimate that around 63% of coins with a cost basis in this price range are actually LTH owned coins purchased in January 2021, and 37% are recently accumulated.

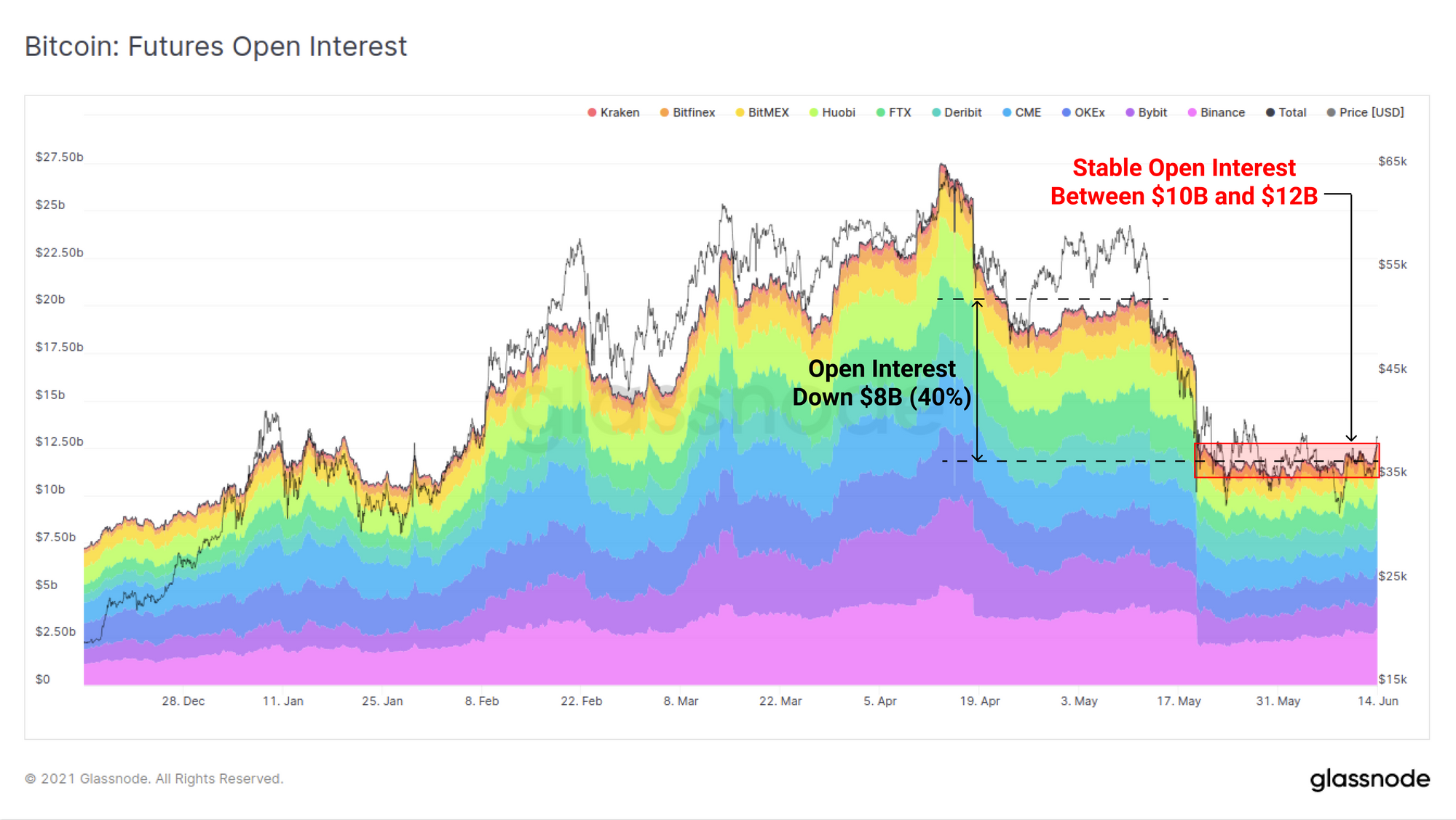

Staying with analysis of short-term traders, we can see that futures open interest is climbing, albeit slowly, especially compared to Q1 2021. Total open interest has fluctuated between $10B and $12B for the last month and remains down around $8B (40%) from the previous peak in mid-May.

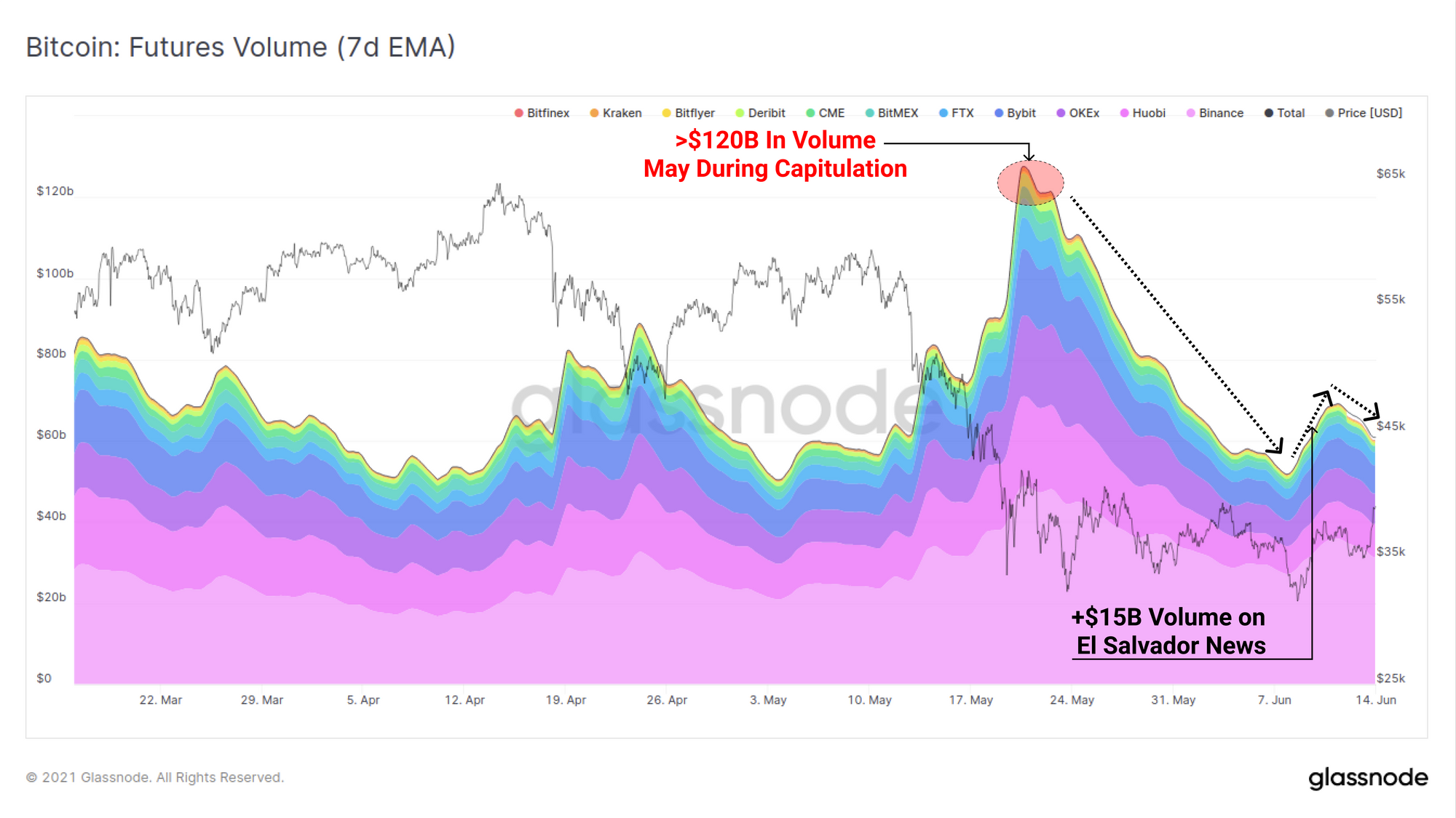

Trading volume on futures has been similarly muted, particularly relative to the $120B in volume that occurred during the capitulation event in May. Around $15B in additional volume was traded in the days immediately following the vote in El Salvador. Trading volume is starting to trail off again over the second half of this week.

It certainly appears that traders in derivatives markets are unsure about the macro market direction and thus keeping leverage levels and volume relatively low.

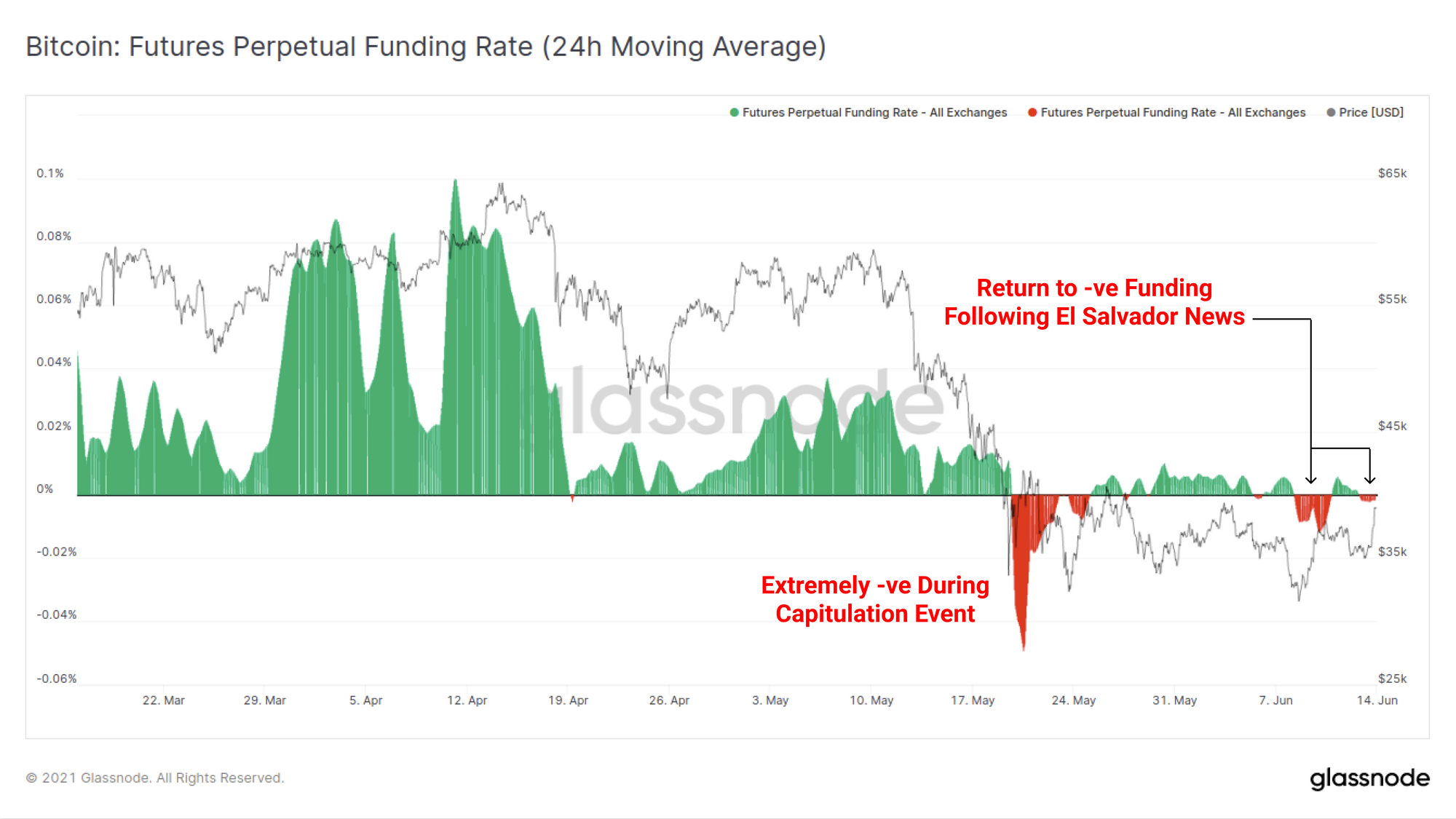

On the perpetual futures funding rate, after turning extremely negative during the capitulation event, it has remained fairly neutral over the past month. Funding rates have oscillated between +0.005% and -0.010%.

Interestingly, on the two aforementioned price rallies, funding rates turned negative indicating that a more bearish bias exists with traders preferring to sell into the rallies.

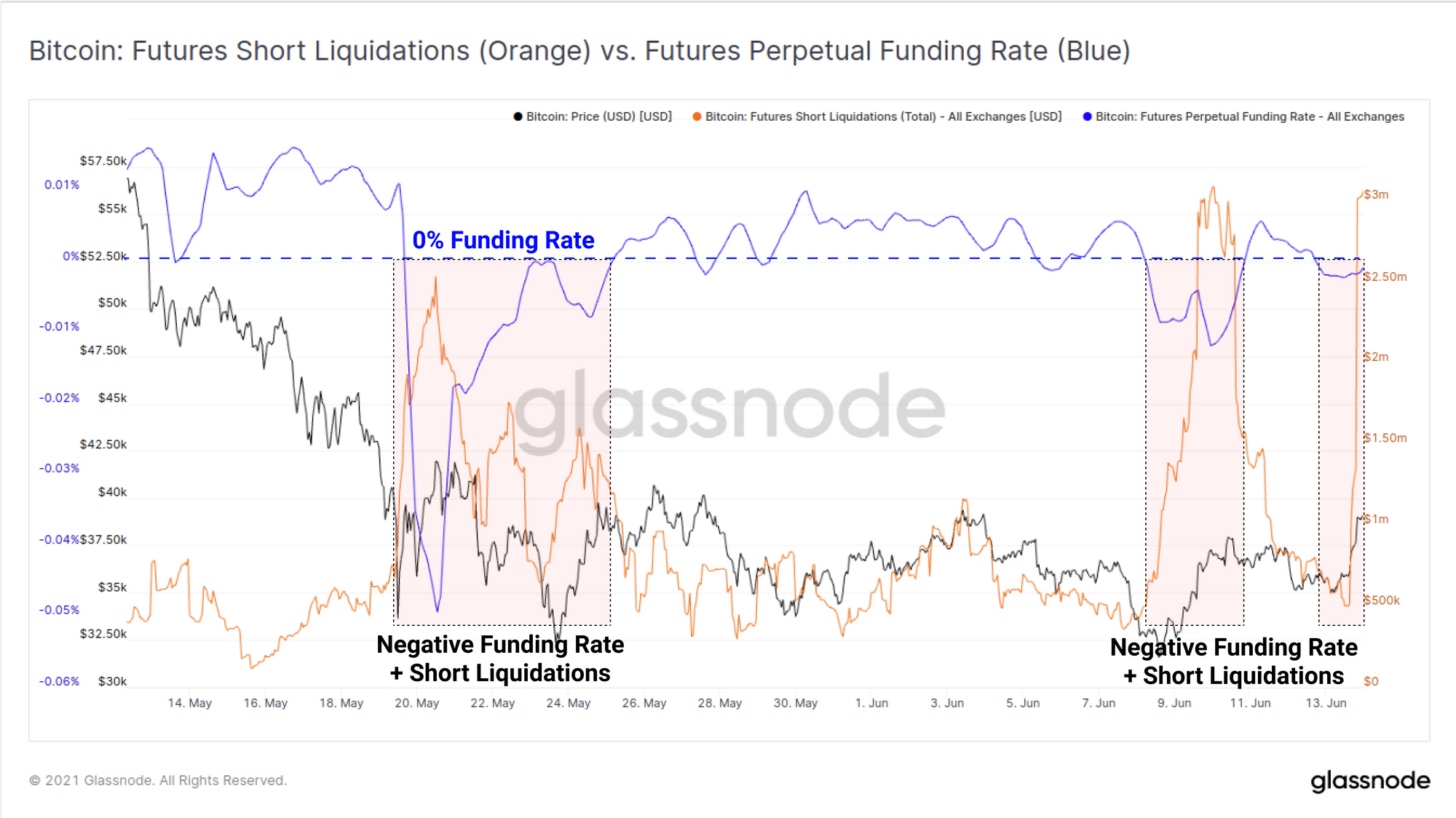

However, it is often the case that large funding rates provide a contrarian indicator, as it suggests many leveraged traders are leaning in the same direction. Whilst the above negative rates are not particularly large, there has been an outsized volume of short liquidations on all three instances.

Each time the funding rate (blue) has turned negative during the last months consolidation, price has rallied, and an increasing number of short positions are being liquidated (orange).

HODLers keep on HODLing

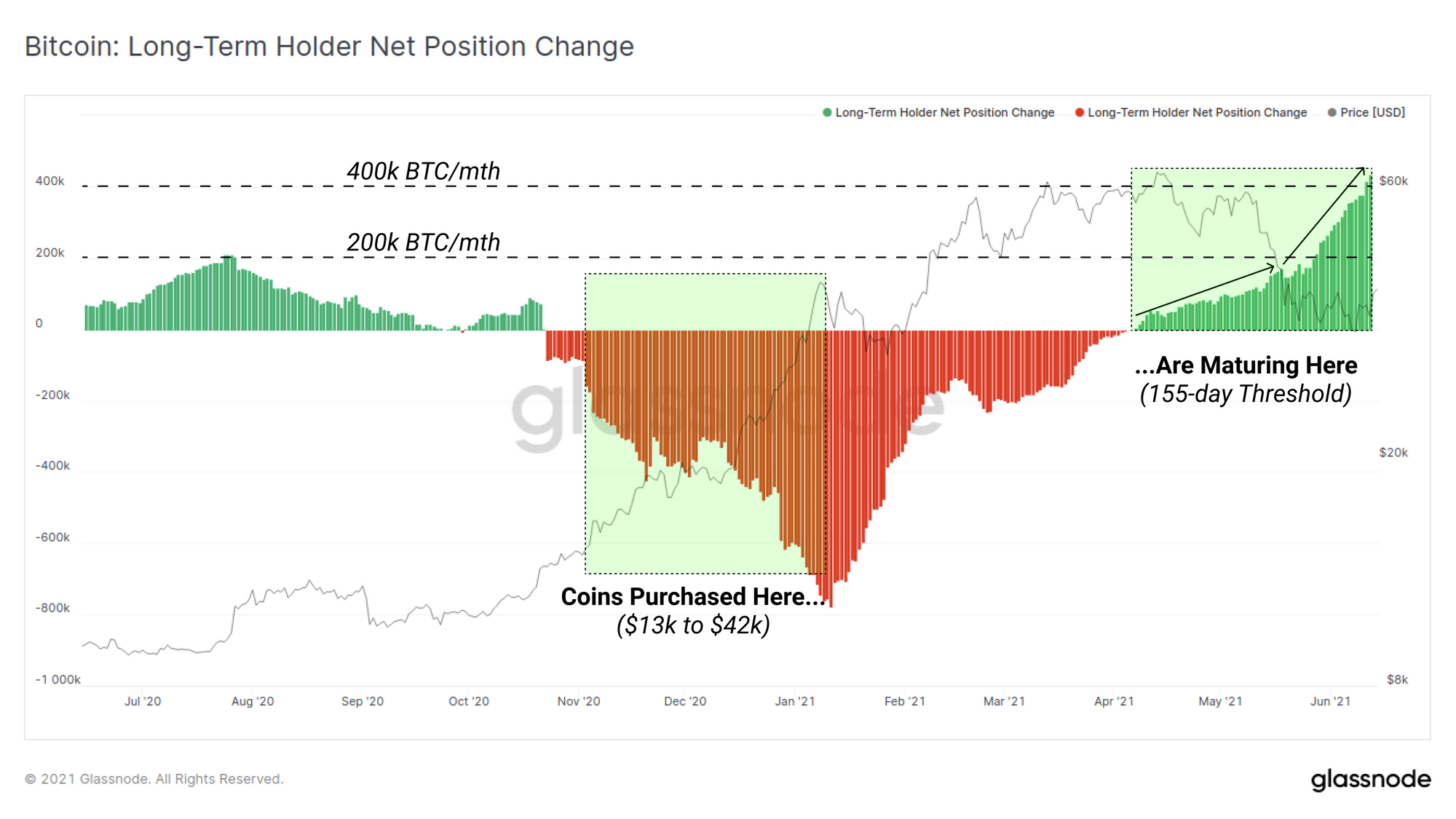

Let's turn our attention now to the long-term holder (LTHs) cohort who include all buyers of coins prior to 10 January 2021. The LTH net position change shows the net monthly rate of coins maturing across the 155-day threshold, accounting for any coins spent.

The chart below is marked up with the price range from 155-days ago ($13k to $42k) mapped onto the accelerating rate of those coins maturing today. What this indicates is that a very large volume of coins were purchased in the early bull market, and have remained largely unspent. The current rate of maturation is over 400k BTC/month which is much larger than the ~160k BTC we estimated were sold, mostly by STHs, during the May capitulation event.

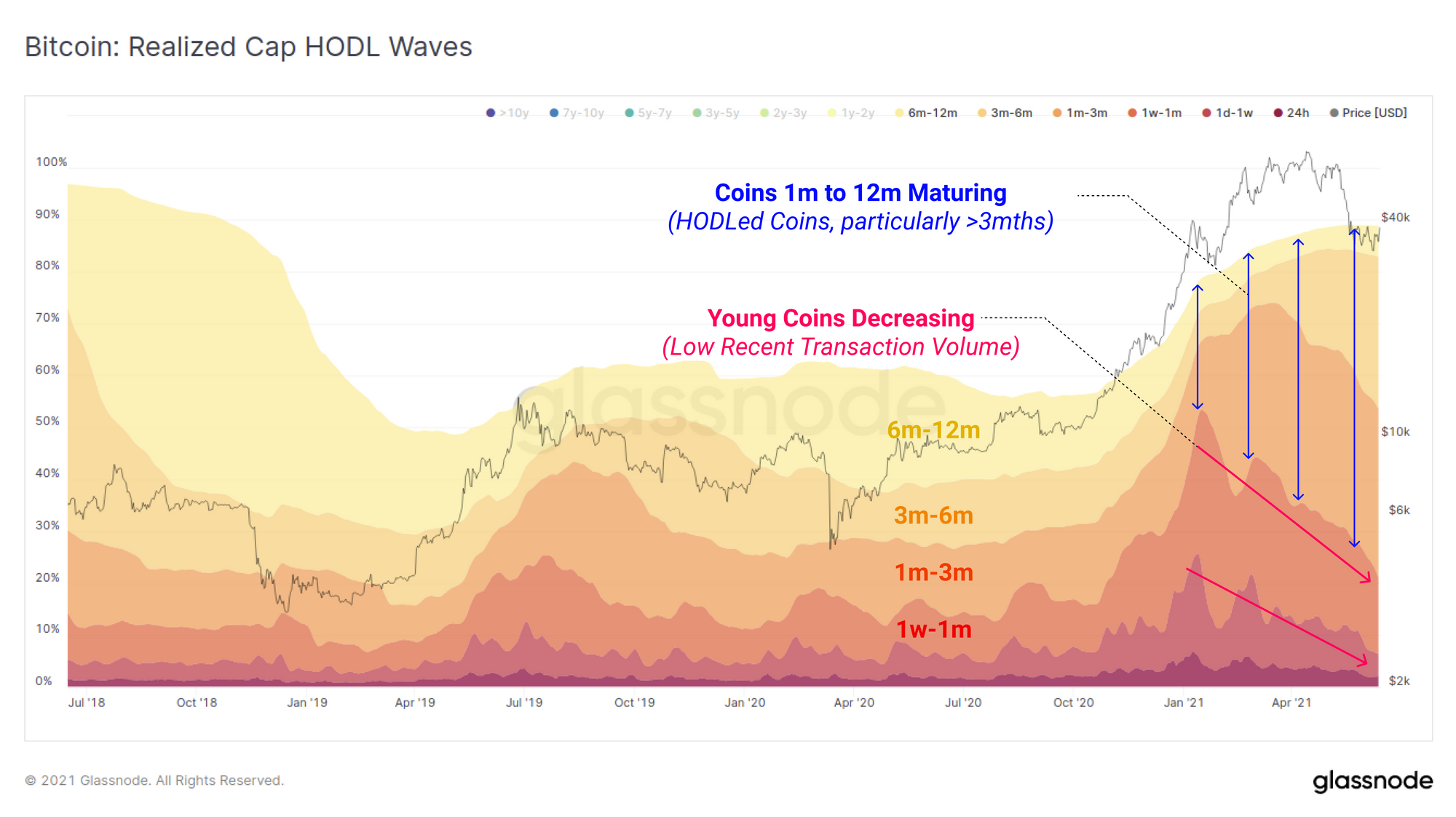

We can also see this coin maturation in the Realised Cap HODL waves, which present the relative proportion of coin supply that makes up the Realised Cap. Not only are we seeing a decline in very young coins (<1-month old) due to the recent low on-chain volume, we are also seeing an expanding share of coins aged between 3-months and 12-months old. These are those same HODLed coins that were accumulated throughout the 2020 to Jan 2021 bull market.

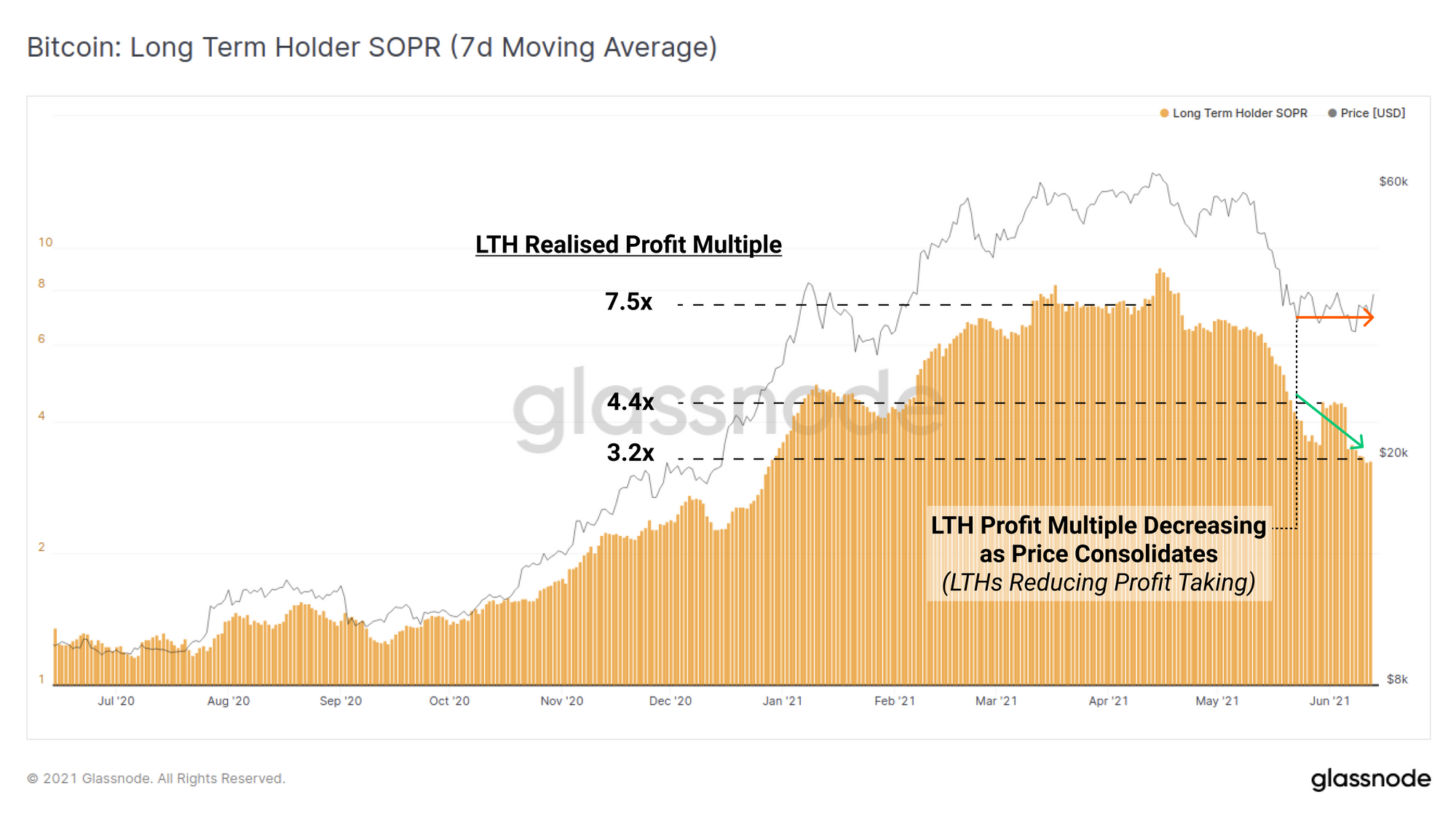

Some LTHs have and will take profits on their coins. What is common in all Bitcoin cycles is that LTHs spend a larger majority of their coins into the strength of bull rallies, and slow their spending on pull-backs as conviction returns. This behaviour can be seen in the LTH-SOPR which tracks the aggregate profit multiple realised by LTHs.

After peaking around 7.5x (LTHs realising 750% profits) in Mar-Apr, it can be seen that LTH's are realising declining profits during this price correction, even as price trades sideways. LTHs are currently realising profits with a multiple of 3.2x which suggests an aggregate cost basis of around $11.3k for their spent coins (7-day avg price $36.2k / 3.2 = $11.3k).

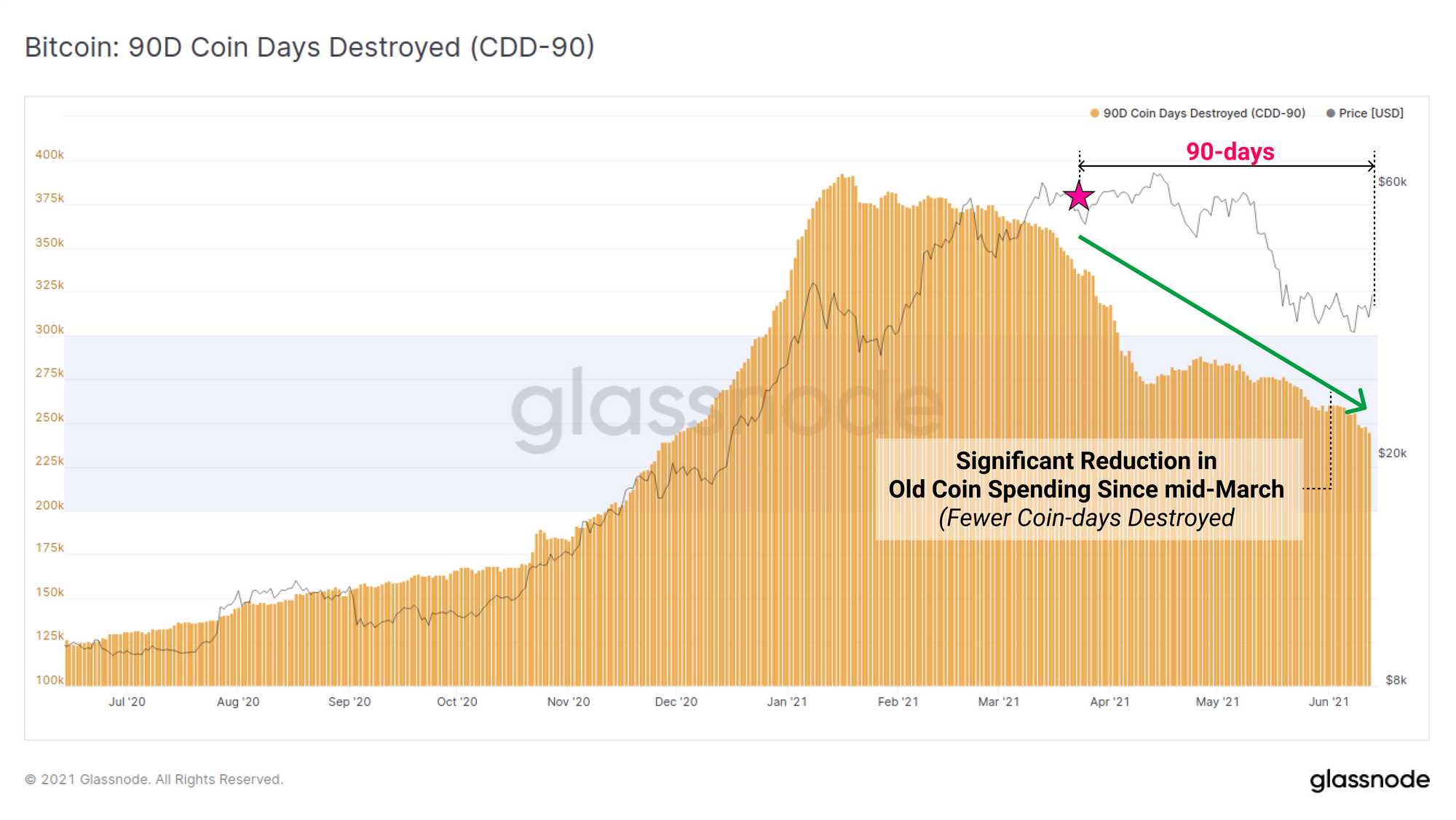

A similar observation can be seen in the CDD-90 metric which plots the aggregate sum of coin-day destruction over the last 90-days. A decline in CDD-90 suggests that older coins (with large accumulated lifespans) are remaining unspent. This suggests that LTHs are not panic selling during this volatility and are therefore more likely to be re-accumulating than cashing out.

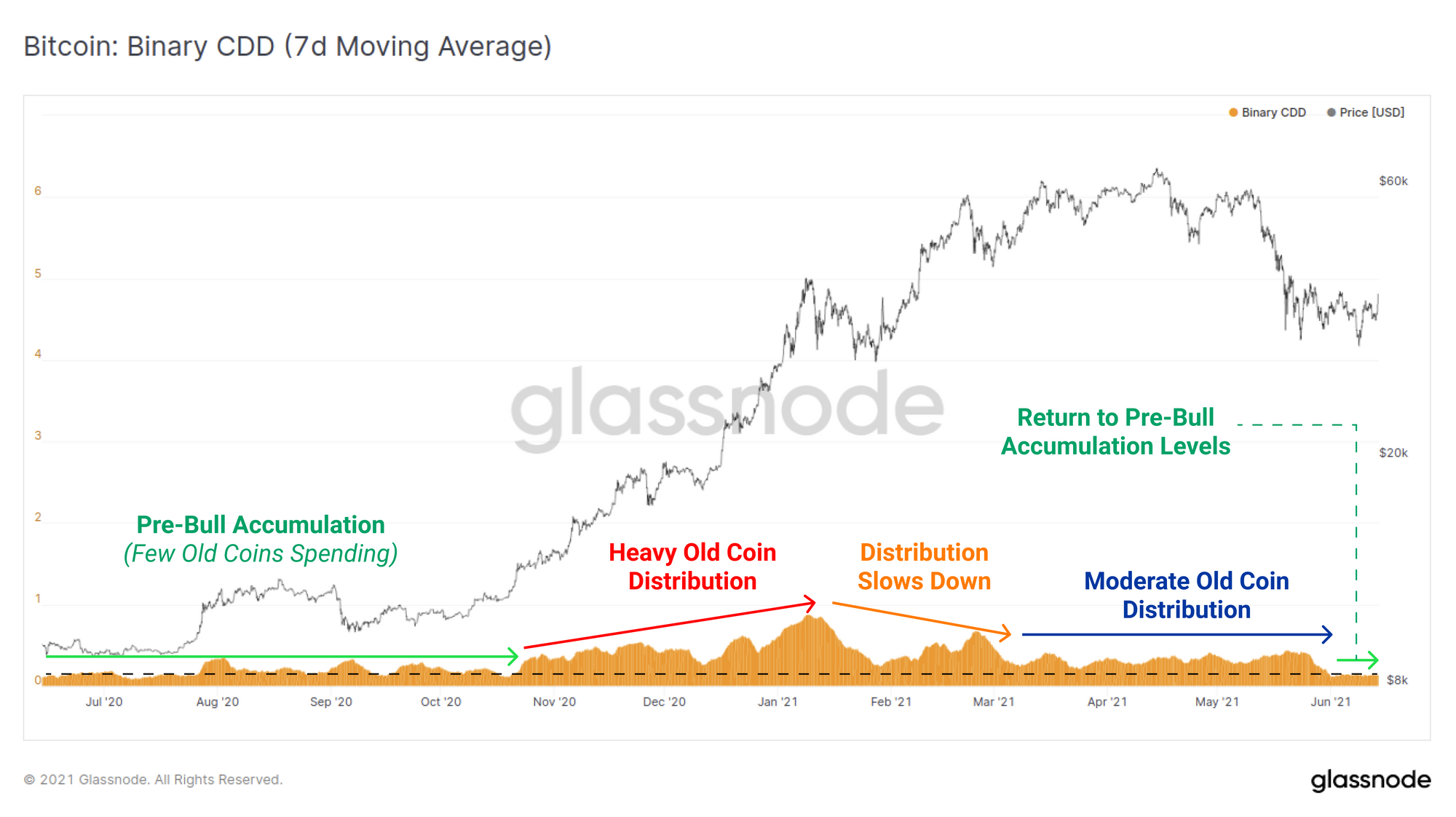

To confirm this even further, we inspect the Binary CDD metric with a 7-day moving average applied. The base Binary CDD metric will return a 1 or a 0 when the volume of coin-days destroyed is greater, or less than the long term average. With a moving average, we can see when trends develop of old coins being spent (uptrend/high values), or remaining dormant (downtrend/low values).

The Binary CDD metric has reached an extremely low value throughout June, coincident with the early 2020 start of the bullish trend. This indicates that Long term holders are simply not spending their coins.

Week On-chain Dashboard

The Week On-chain Newsletter now has a live dashboard for all featured charts