Extreme Leverage at Extreme Depths

With onchain indicators hitting significantly oversold conditions, Bitcoin futures markets see all-time-high leverage, with increased chances of volatility, and a short squeeze bias.

Bitcoin investors were faced with six consecutive red daily candles this week, accompanied by a broader market sell-off following increased concerns of hawkish policy from the Federal Reserve. Following the release of the December's Federal Open Market Committee meeting minutes early in the week, markets reacted to notes related to an accelerated pace of tapering, rate hikes, and of potential quantitative tightening to lighten the central bank's balance sheet.

After opening at $47,875, Bitcoin led global declines, trading down as much as -15% year-to-date. Prices have since closed the first full week of 2022 at $40,672, putting the bulls on the back-foot to start the year. In this week's newsletter, we will unpack a number of concepts underlying the reaction of market participants including:

- The climate of older coin spending on-chain,

- Increasingly elevated levels of Open Interest in futures markets,

- The potential of a near-term short squeeze developing, as prices trade lower, and bear conviction chases the market down.

The Week Onchain Dashboard

The Week Onchain Newsletter has a live dashboard with all featured charts available here. This dashboard and all covered metrics are explored further in our Video Report which is released on Tuesdays each week. Visit and subscribe to our Youtube Channel, and visit our Video Portal for more video content and metric tutorials.

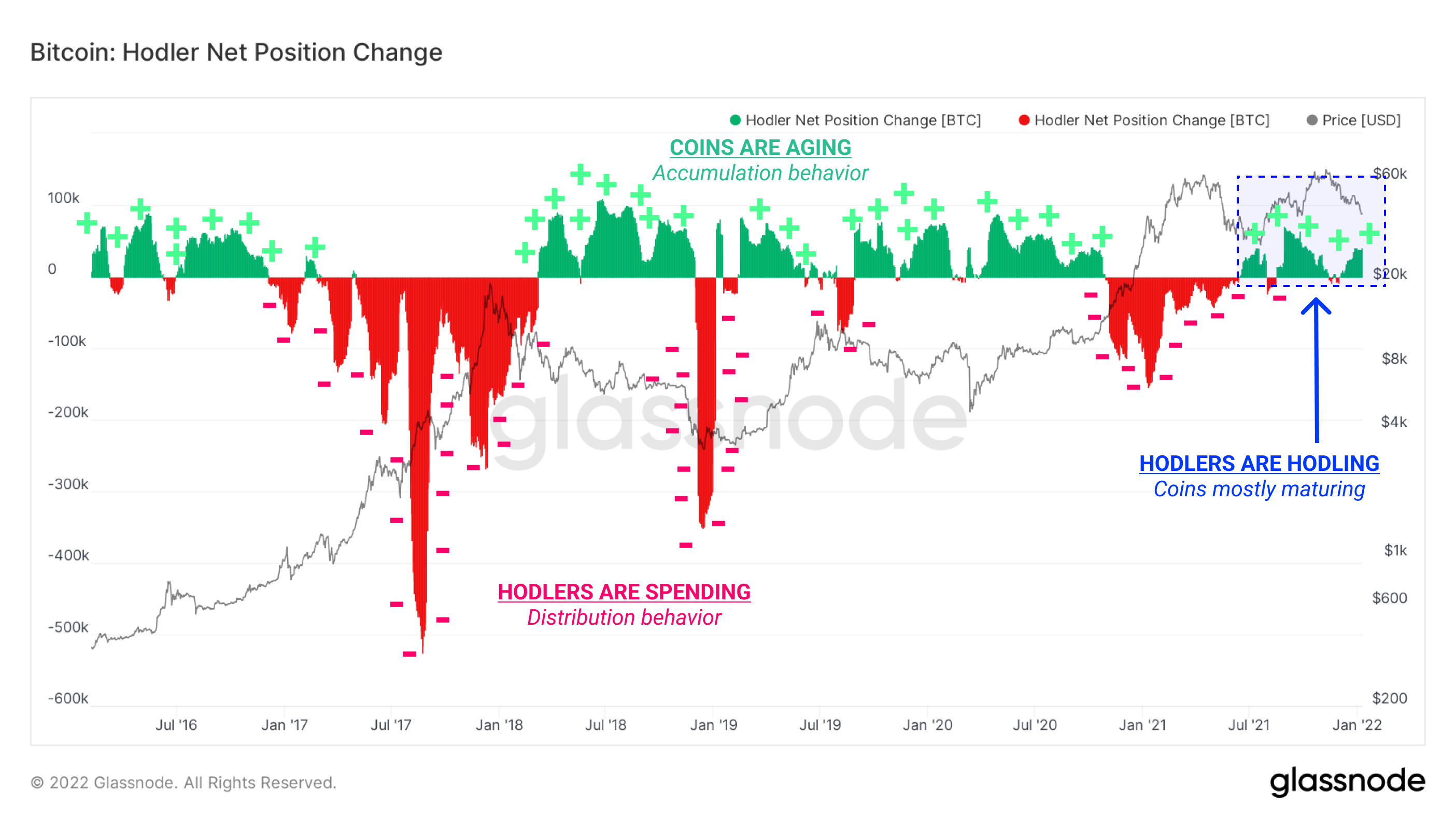

Only The HODLers Remain

A phase of heavy loss realization by top buyers has followed the December 4 flush-out, as we first reported in our Week 50 2021 newsletter. In the weeks since, onchain behavior has been more heavily dominated by the HODLer class, with little activity by newer market entrants.

One way to see this dynamic is through Hodler Net Position Change, which is the rolling 30-day change in coin maturation. As units of BTC age and mature in investor wallets, they accrue Coin Days, which are 'destroyed' upon spending and help to produce various lifespan metrics.

- Positive (green) values mean coins are ageing and maturing at a higher rate than spending. This is typically in bearish market conditions absent retail interest as long-term accumulation takes place by high conviction buyers.

- Negative (red) values occur when elevated rates of spending, particularly by older coins, outpace the present accumulation behavior. This is frequently observed in the heights of bull markets and moments of total capitulation, when older hands are more likely to relinquish their holdings.

Following a brief period of net spending after the early November price peak, maturation has again taken the mantle as price declines. It speaks to a trend typically seen when retail/tourists have left the market, HODLers remain, and generally more bearish forward price expectations.

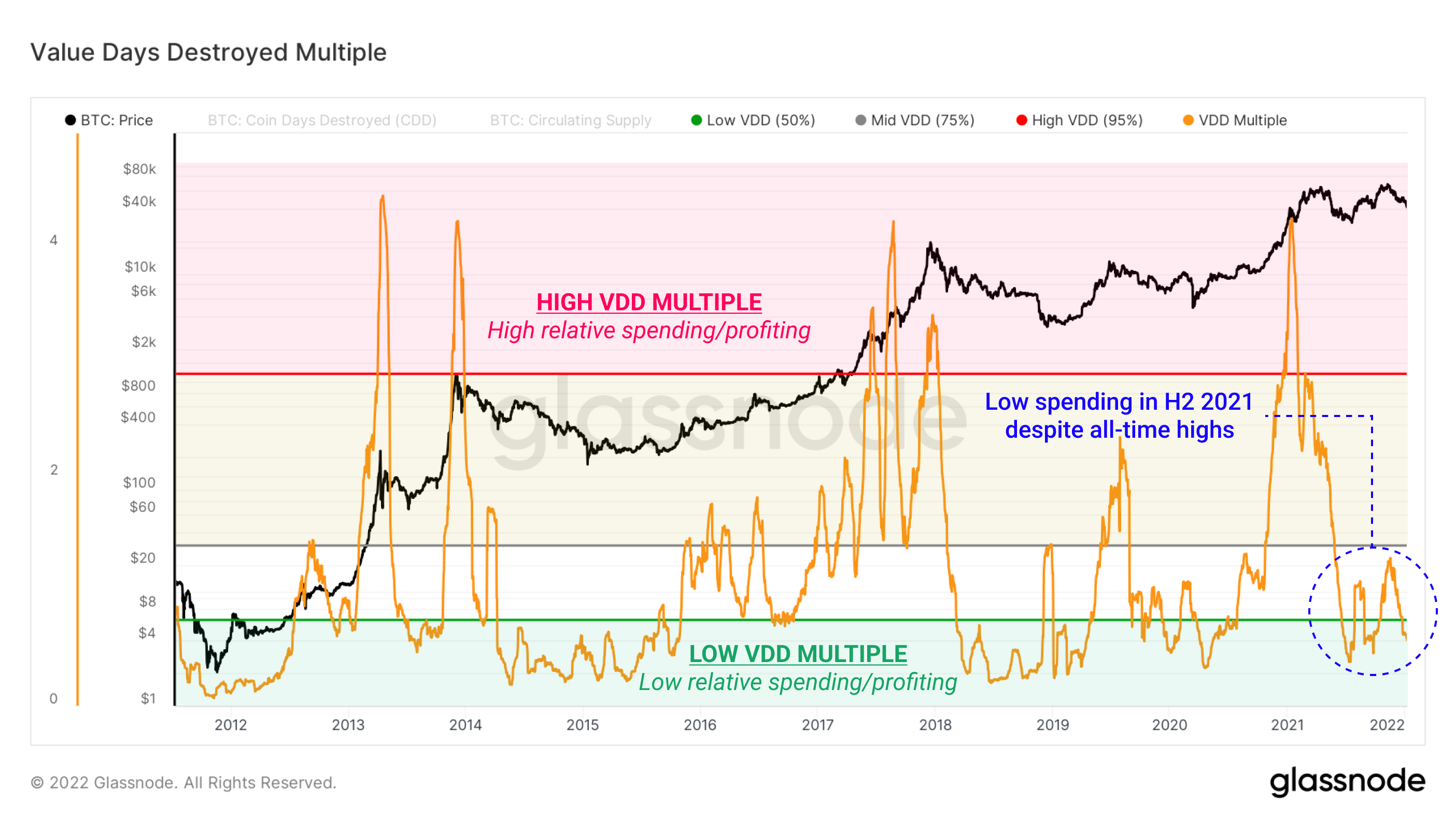

Another method for measuring spending velocity is via the Value Days Destroyed Multiple (VDD), which compares the monthly sum value of coin destruction to the yearly average.

- High VDD Multiple values signify elevated coin destruction behavior relative to the past year. This historically marks periods of peak market liquidity, large supply turnover, and rising prices.

- Low VDD Multiple values demonstrate a quiet HODLer market with calm relative coin destruction. These moments can stretch for long periods and often occupy cyclical lows.

Using the Value Days Destroyed perspective of activity, the October and November rallies saw a very mild level of spending compared to the long-term average. This is in some ways influenced by the historically high VDD values reached in early 2021, but still shows the value of spending at the recent all-time high was relatively low.

This again paints a picture of a HODLer dominated market, and low relative retail interest.

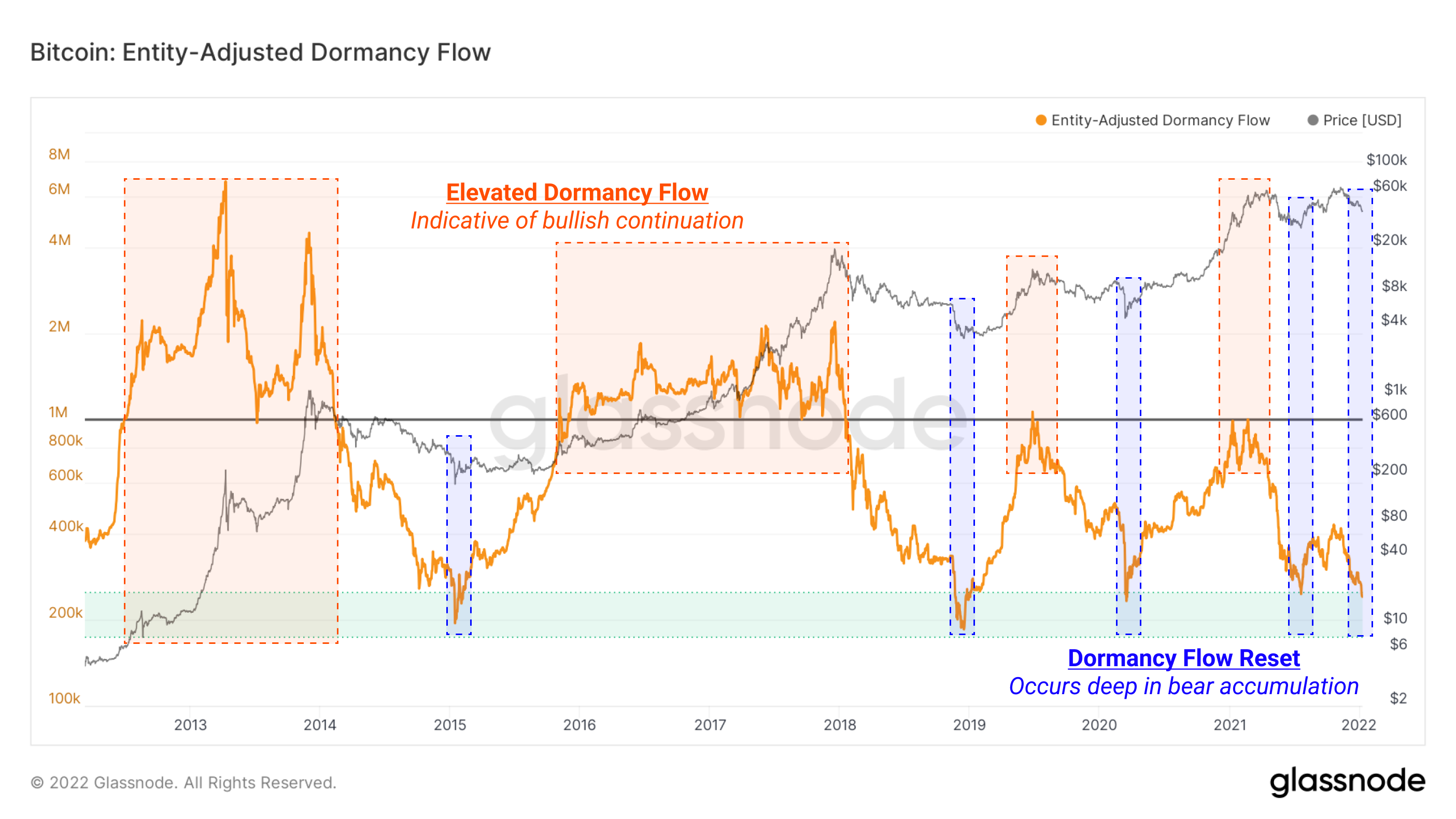

Rounding out our assessment of spending behavior is Entity-Adjusted Dormancy Flow, which compares the Bitcoin market cap (asset valuation) to the annualized dollar value of coin Dormancy (spending motive). Dormancy is the average age (in days) of spent coins per unit of BTC, which is akin to an Average Spent Output Lifespan weighted by volume.

- High values of Dormancy Flow means network value is high relative to the yearly value of realized Dormancy in USD. The interpretation is that the bull market is in "healthy" conditions (spending in concert with demand valuation).

- Low Dormancy Flow values indicate moments where market cap is undervalued relative to the yearly sum of realized Dormancy, indicating moments where Bitcoin is a value price.

Entity-Adjusted Dormancy Flow recently bottomed out, showing a full reset of the metric. These events historically print at cyclical bottoms, and confluence with Hodler Net Position Change and the VDD Multiple hint at a potential floor of spending in the near-term, barring new surprises.

With the above three charts in tow, we can largely identify market conditions typically seen in the late stages of a macro bearish trend, often around capitulation style events. It remains to be seen whether there is more pain to the downside, perhaps in response to macro/monetary headwinds, or whether the majority of the damage has already been done and a bullish relief rally is due.

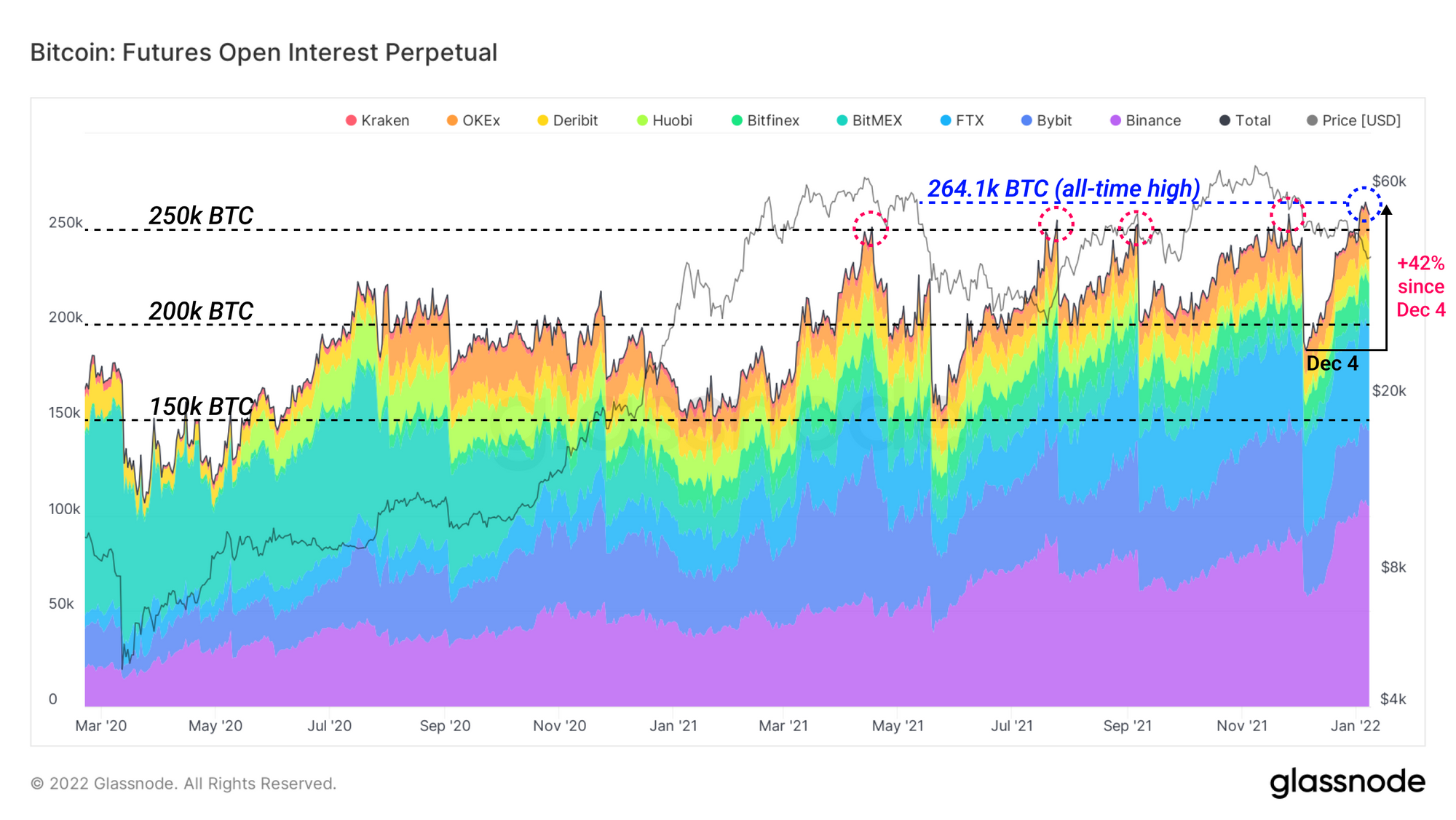

Futures Markets See New Highs in Open Interest

While on-chain has stayed quiet, the leverage in Bitcoin derivatives market has been growing at an aggressive pace This speaks to an outsized interest in Bitcoin price action as a speculative bet, rather than the relatively tepid demand for Bitcoin in spot markets.

Leading our assessment of derivatives is the growth of Futures Perpetual Open Interest, which is the sum value of all open contracts in the continuous contracts market. Shown here in BTC terms, Perpetual Open Interest has reached new all-time highs of 264k BTC in the face of recent price declines, rising +42% since December 4 and surpassing the previous high of 258k BTC set on November 26.

With the first principles understanding that price declines will inherently close out long traders, a growth in Open Interest in recent days hints at short traders layering on bets into market weakness.

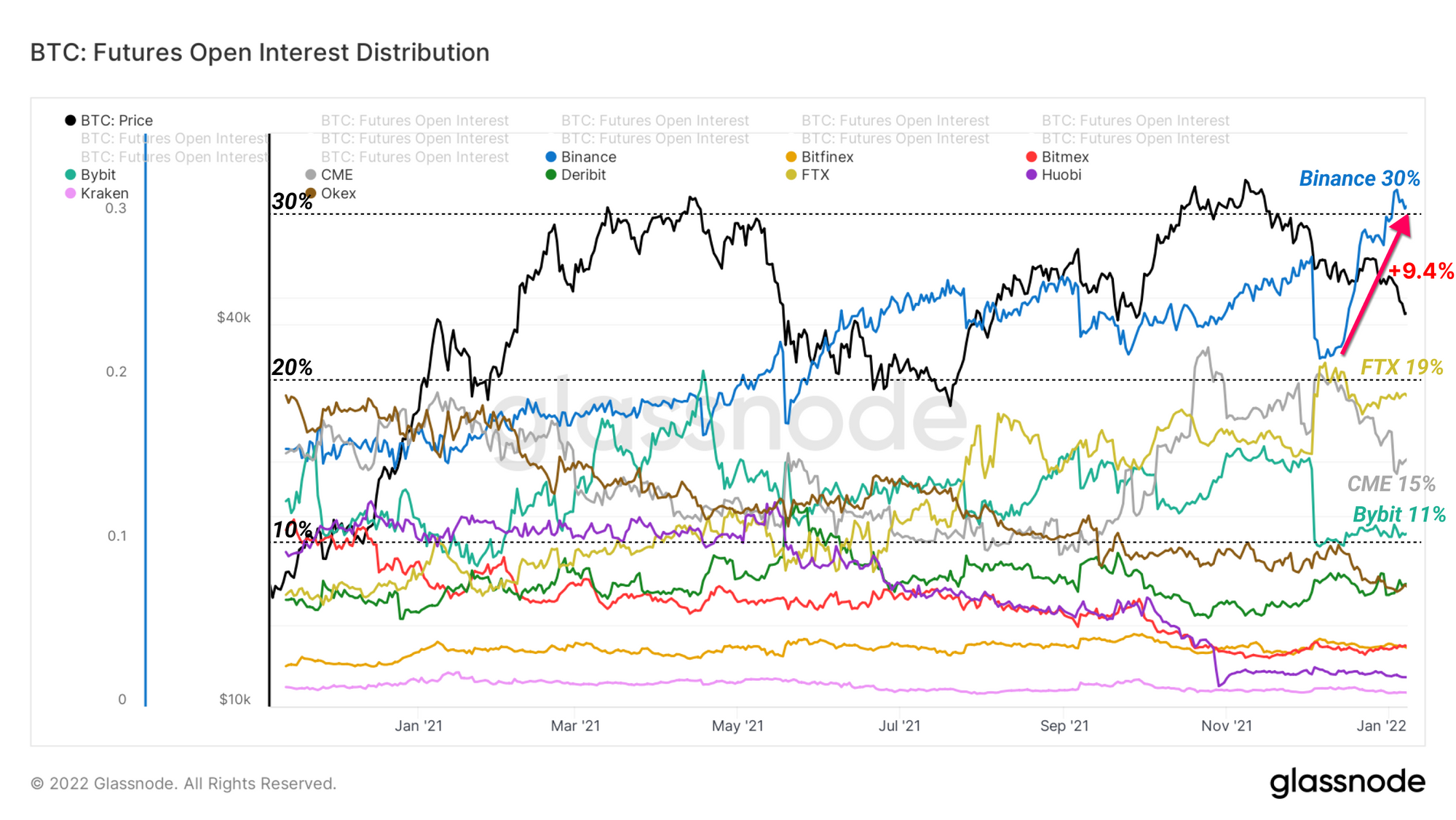

Leading the rapid growth of futures speculation are users on Binance, far and away the largest Bitcoin futures exchange by volume and size. Since May 2021, Binance has enjoyed the lion's share of Futures Open Interest among all exchanges, with a notable increase in market share during recent weeks. Since the dramatic purge on December 4th, Binance has absorbed 9.4% of Bitcoin's Futures Open Interest, and now dominates with a 30% market share.

The second largest exchange by Open Interest market share is FTX with 19%, surpassing the Chicago Mercantile Exchange (CME). CME had seen a jump in market dominance in October at the launch of the $BITO ETF, but is now the third largest at 15% of Futures Open Interest.

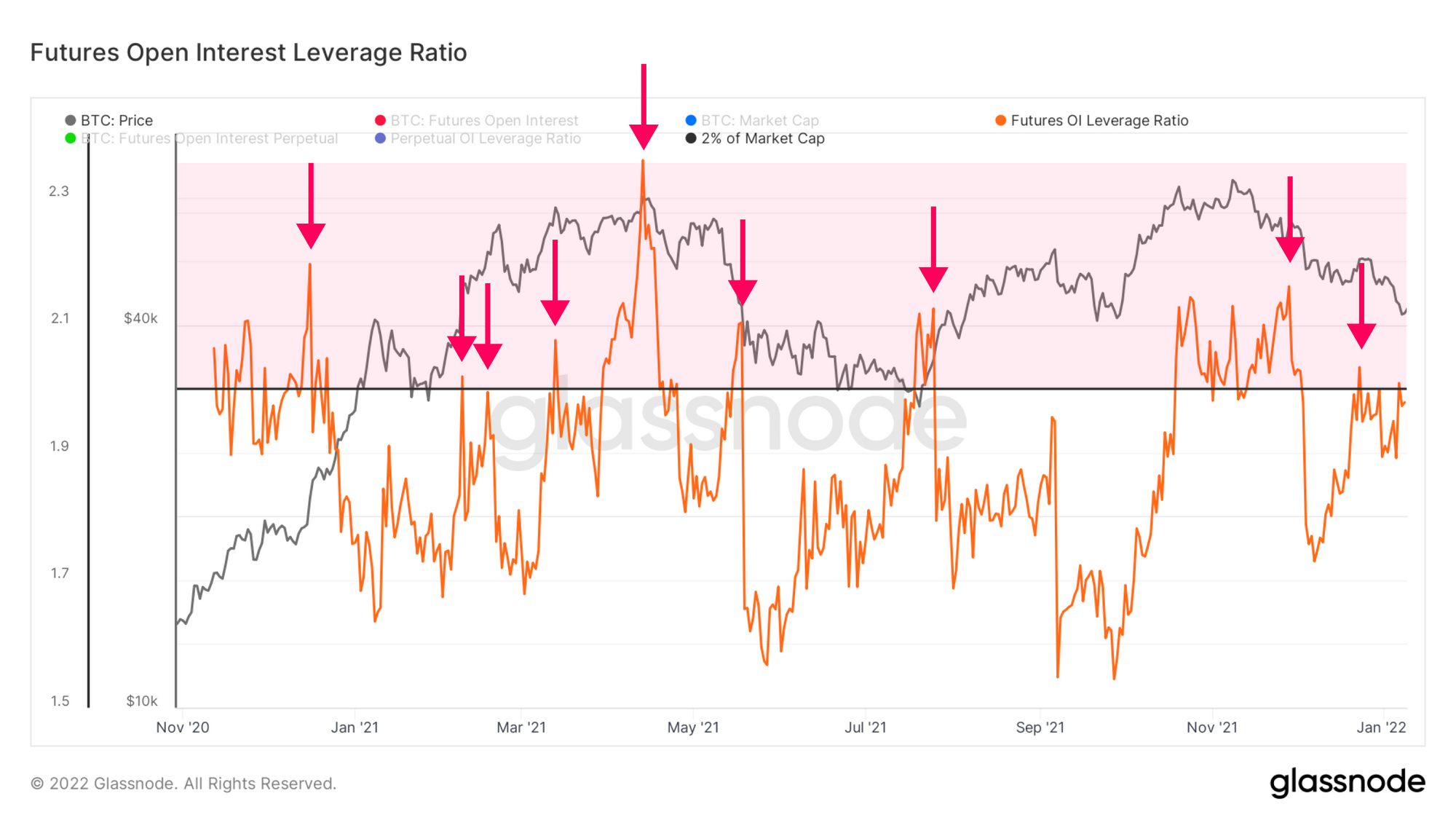

The dramatic leap in Futures Open Interest can be viewed in another way: representing itself as a leverage ratio against the Market Cap. Typically, periods where Futures Open Interest exceeds >= 2% of Market Cap are short-lived, and tend to end with a dramatic flush of margin.

De-leveraging events can occur in either direction, and at times have triggered despite an Open Interest leverage ratio below 2%, like on September 7 when El Salvador made Bitcoin legal tender. The combination of elevated Open Interest plus a big news event catalyzed a volatile move down.

However, each instance where leverage exceeded 2% in the past year ended with a swift liquidation of contracts. At time of writing, Futures Open Interest Leverage Ratio is at 1.98% so there exists a non-trivial risk of high volatility in the short term.

Short-Term Squeeze of Shorts?

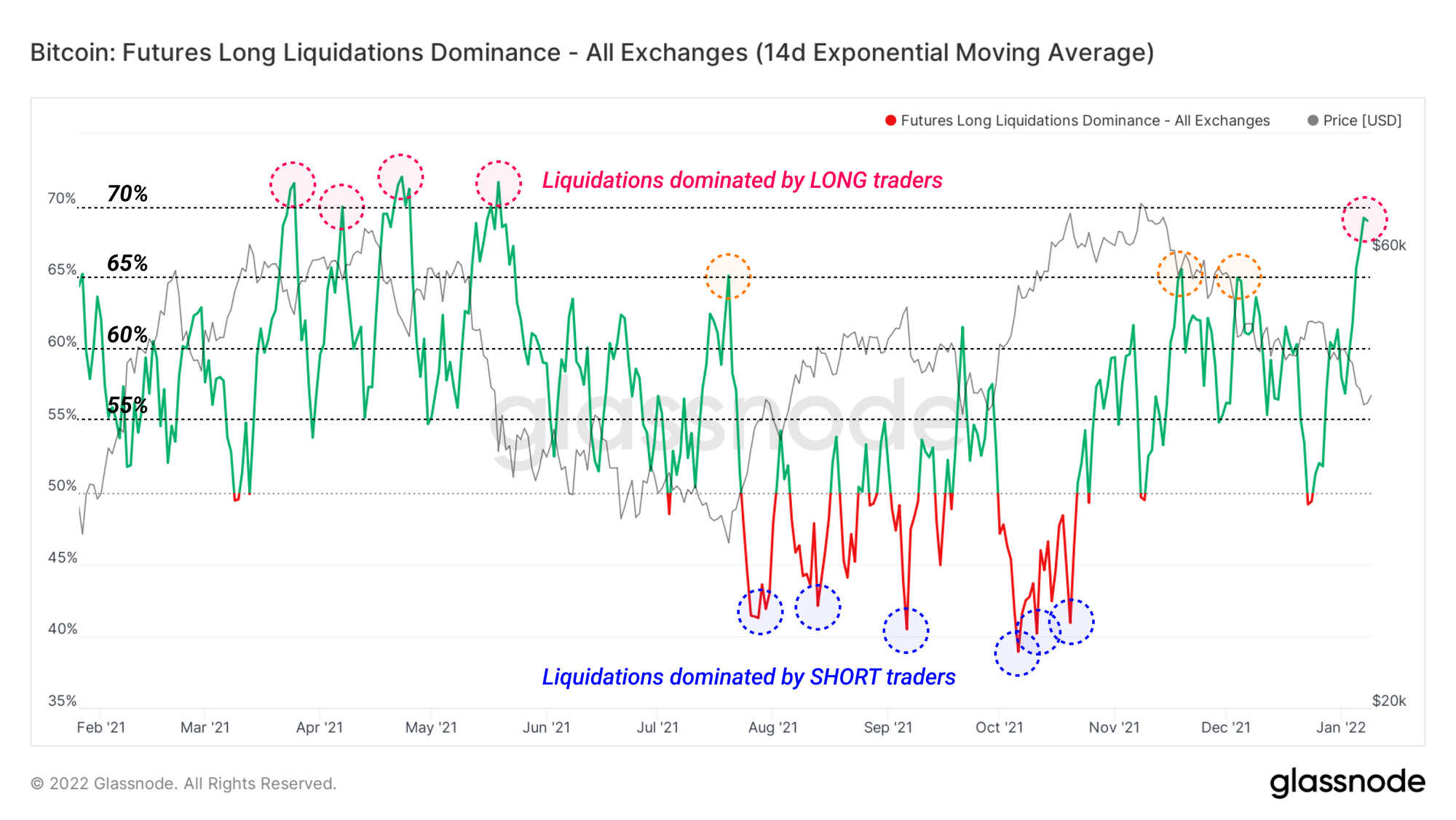

A byproduct of consistent downtrends in price are the liquidation of confident long traders trying to catch a falling knife. A great way to view the trend of liquidations is via the dominance oscillator between long and short liquidations.

Since November, Bitcoin futures has been in a regime of long liquidation dominance, where traders betting on "Number Go Up" are consistently on the losing side. This value recently spiked to a local high of 69%, its highest value since the May 2021 crash.

Factoring in this observation with the aforementioned rise of Open Interest into declining price, and the probability of a local reversal is increasing. Short traders, who have not been punished for taking on increasing risk, may find themselves candidates for a near-term squeeze.

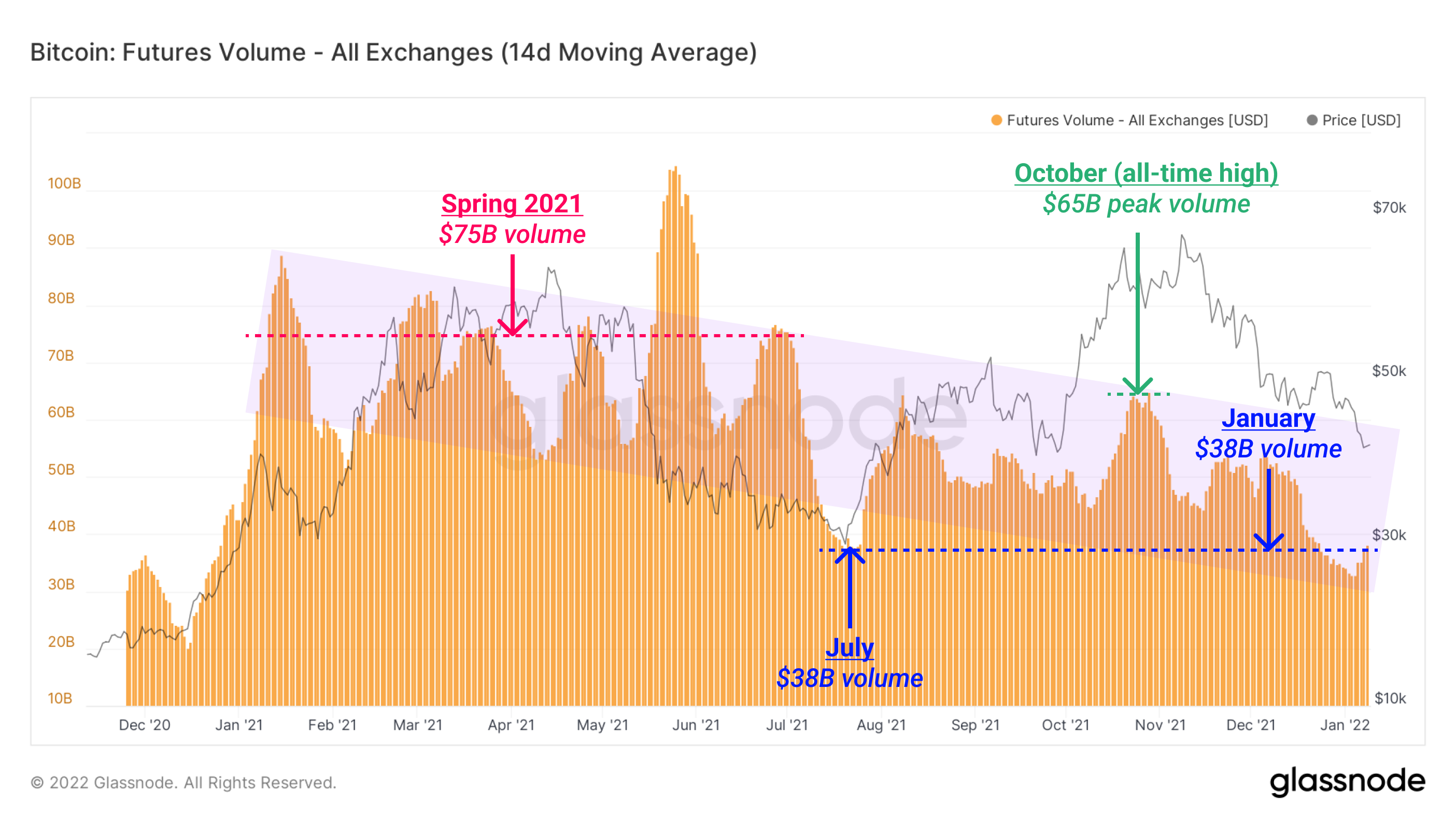

As the volume of open contracts in futures rise to new highs, the daily sum of traded volume in futures has been trending in the opposite direction. Large price movements result in contracts changing hands and stop losses being triggered. In sideways price action, traders get away with not having to close their positions, allowing volumes to decline in periods of consolidation while Open Interest can remain high.

Futures Volume saw its zenith in the first half of 2021, where daily trading exceeded $75 billion/day for weeks at a time. Following the market decline of 50% into July, the October rally to all-time highs was supported by volume back up around $65 billion/day.

In the current environment however, the 14-day average of daily Futures Volume is around $38 billion/day, the same level it was in the depths of the July lows. Low trading volumes can however create environments of reduced market depth, and limited resistance against rapid price moves. Should a deleveraging event follow, in a low liquidity environment, the magnitude of the price move may well be greatly amplified.

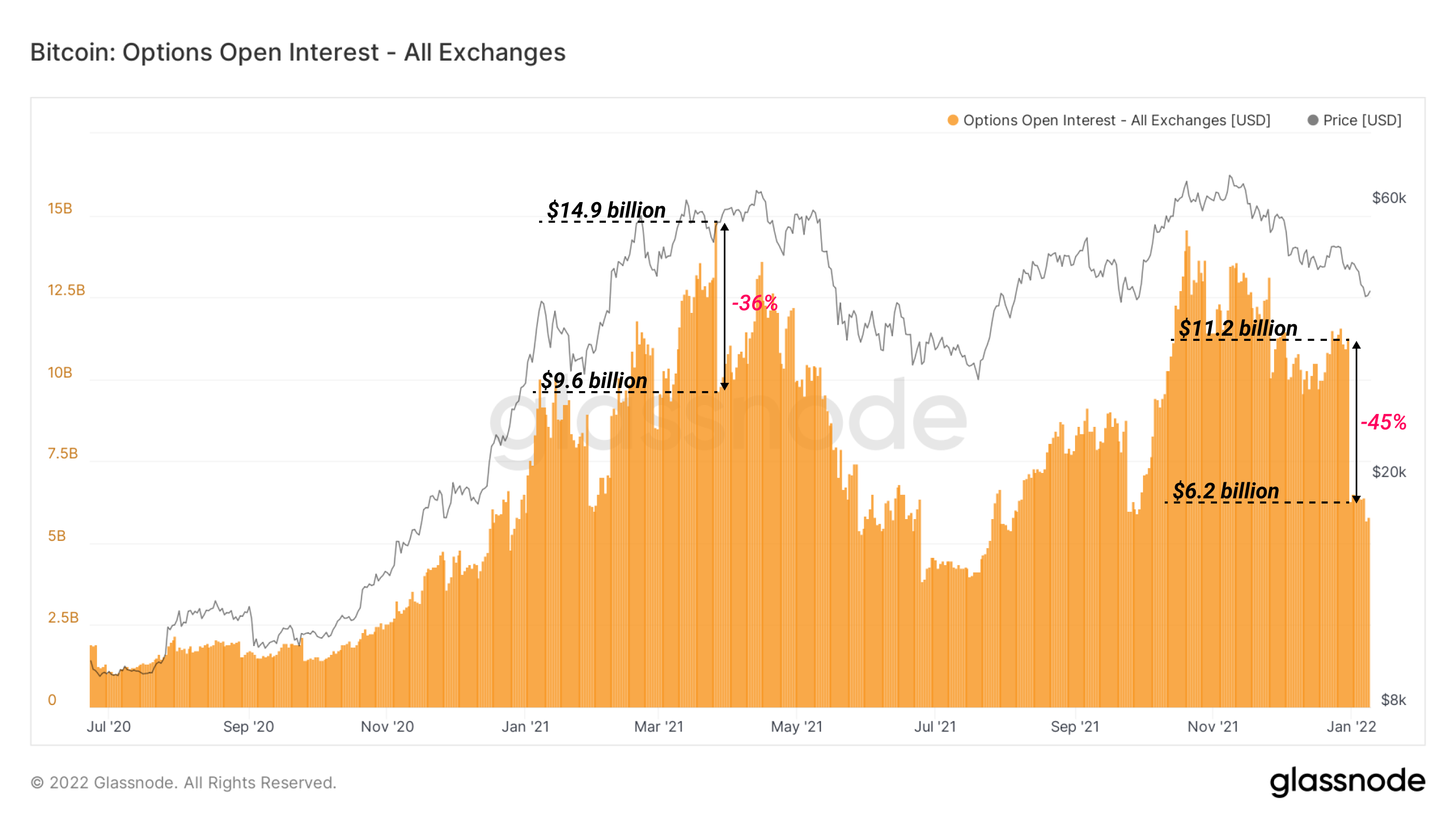

Rounding out our look at derivatives is Options Open Interest. Coming into December, all eyes were on the end-of-year strike on December 31, following months of buildup to the tune of more than $11 billion in contracts. Many of these contracts were dominated by bulls, with a particular emphasis on Bitcoin prices exceeding $100k.

By January 1, Options Open Interest was down to $6.2 billion from a December 31 value of $11.2 billion, a haircut of -45% ($5B). The end-of-year strike was the largest of 2021 in percentage closures, but only the second in total dollars. The March 26 strike saw a record $5.3 billion closed at expiration, a reduction of -36%.

In summary, the current Bitcoin market structure can be best described as having:

- Tepid demand for spot, with the majority of onchain metrics describing a dominance of HODLers in accumulation, typical of bearish markets with low retail/tourist interest.

- Derivatives market leverage is at high risk levels around 2% of the market cap. This is strongly lead by Binance markets, and open interest has increased as prices decline.

- An elevated risk of a deleveraging exists, coupled with low trading volumes, and an elevated probability of short-dominance in futures markets.

Alongside very oversold indicators in onchain spending activity, this suggests a short squeeze is actually a reasonably likely near-term resolution for the market. Whether it can overcome macro headwinds, and reestablish a convincing uptrend will be a focus for upcoming newsletters.