An Opportunity, or a Trap?

The recent market rally has pushed BTC prices above $23k, and has surprised many investors. However, alongside higher prices, comes an increased motivation for holders and miners to take exit liquidity, especially after the prolonged and painful bear of 2022.

The recent market bounce from the FTX fall-out trading range to levels above the Realized Price ($19.7k) has surprised many investors, inspiring them to respond accordingly.

As this article will discuss the noteworthy shifts in behavior for new investors (Short-term Holders), Long-Term Holders, and miners. For new investors and miners, the recent rally has motivated spending, taking the opportunity to exit and secure some profit. On the other hand, we have seen more resilience for long-term holders, with coins crossing the 6-month age threshold and pushing to new highs.

Exploring the response of both long and short-term cohorts, this report aims to inspect how the recent shift in profitability plays a role in changing the behavior patterns of market participants.

🪟 View all charts covered in this report in The Week On-chain Dashboard

🔔 Alert Ideas presented in this edition can be set within Glassnode Studio.

️🏴☠️ The Week On-chain is translated into Spanish, Italian, Chinese, Japanese, Turkish, French, Portuguese, Farsi, Polish, Arabic, Russian, Vietnamese and Greek.

📽️ Visit and subscribe to our Youtube Channel, or visit our Video Portal for more video content and metric tutorials.

Almost Out of The Woods

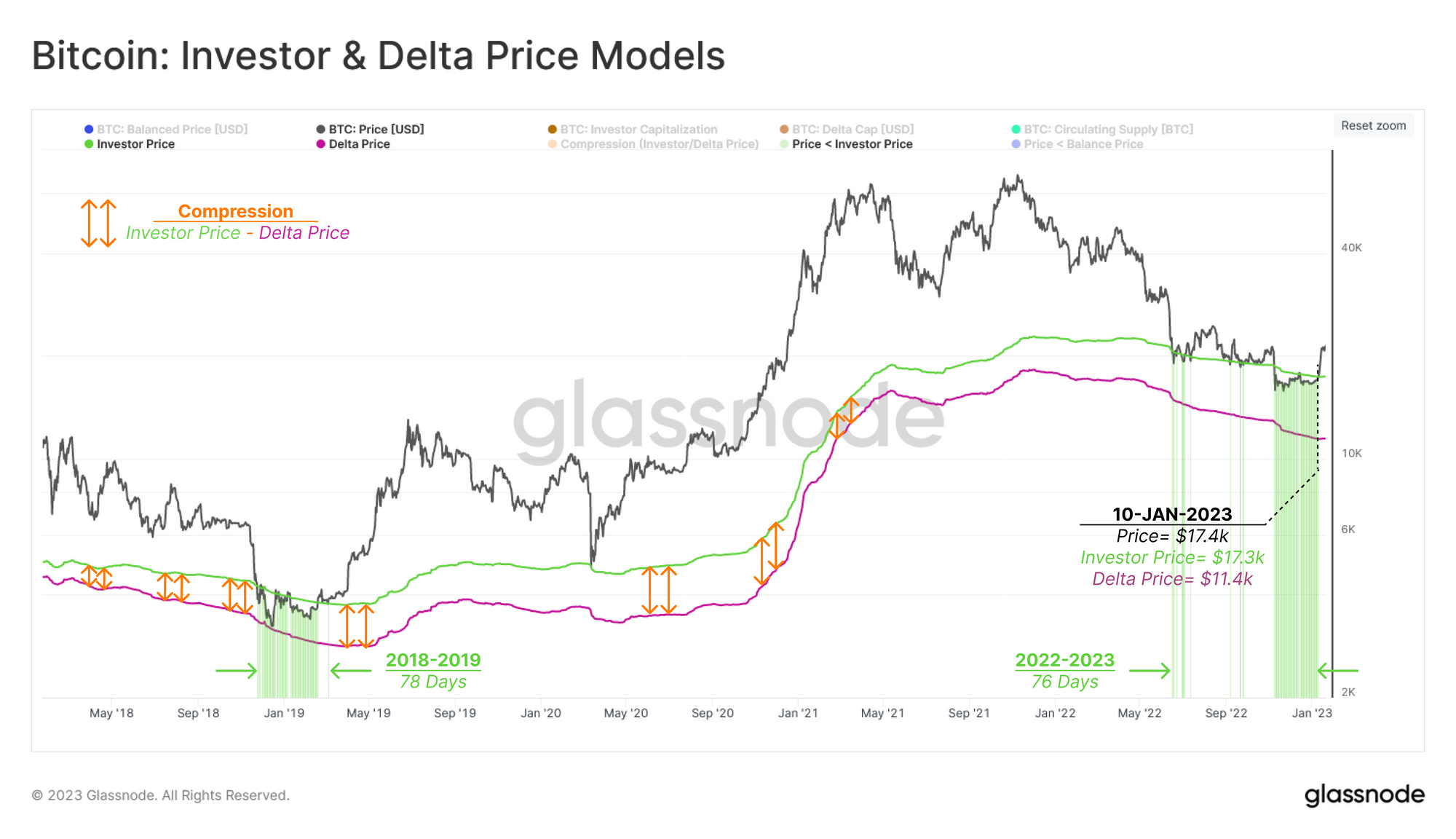

The recent surge in price action to the $21k to $23k region involved reclaiming multiple on-chain pricing models, which has historically signified a psychological shift in holder behavior patterns.

The chart below presents two specific models from our Pricing Model Dashboard where:

- 🟢 Investor Price ($17.4k) is derived from the difference between the Realized Cap and the Thermocap. It reflects the average acquisition price for all coins which have been spent and distributed by miners.

- 🟣 Delta Price ($11.4k) is calculated from the difference between Realized Cap and the all-time Average Cap. This produces a combined on-chain and technical pricing concept.

Surprisingly, price action across the 2018-2019 and the current bear market bottom discovery phase have spent a similar amount of time within the bounds of the Investor-Delta price band. This suggests an equivalency in durational pain across the darkest phase of both bear markets.

🪟 Related Dashboard: A diverse suite of models tracking cohort cost basis, fair value estimates, and mining cost of production are available in the BTC: Pricing Models dashboard for Advanced members.

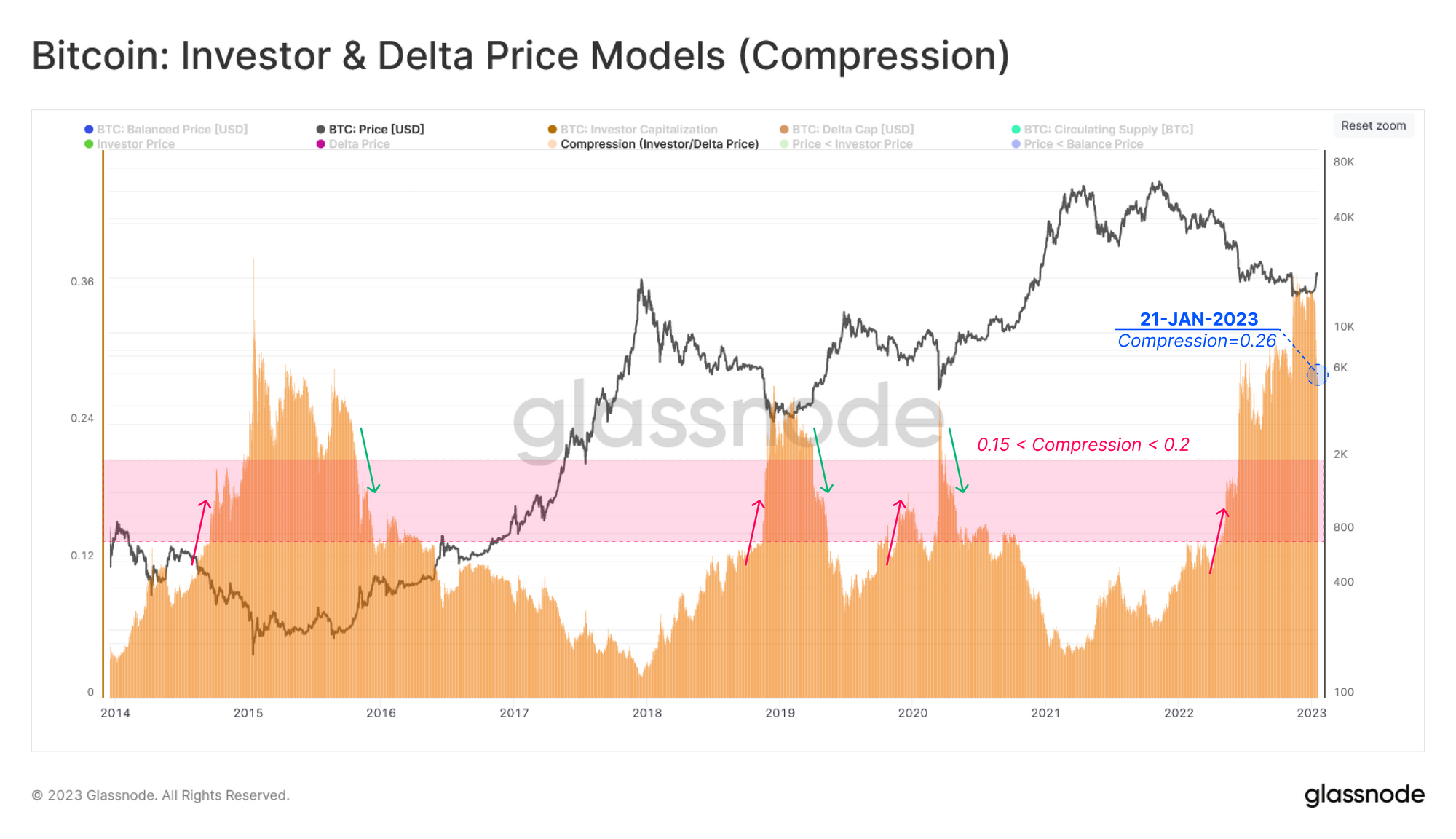

In addition to the duration component of the bottom discovery phase, we can measure the compression of the Investor-Delta Price range as a proxy for the intensity of market undervaluation. As displayed above ↕️, the compression of this range is correlated with the magnitude of change in the Realized Cap or volume of capital inflow into the market.

Compression = (Investor Price - Delta Price)/Spot Price

Assessing the historical trend of this Delta-to-Investor compression concept indicates a threshold zone (0.15-0.2 🟥) that can be employed for seeking confirmation for the beginning ↗️ and end ↘️ of the Bottom Discovery phase.

Considering the current price and compression value, a similar confirmation signal will be triggered when the market price reclaims $28.3k.

Light at The End of The Tunnel

Alongside the assessment of pricing models, we can investigate other on-chain measures to estimate the sustainability and strength of current market momentum.

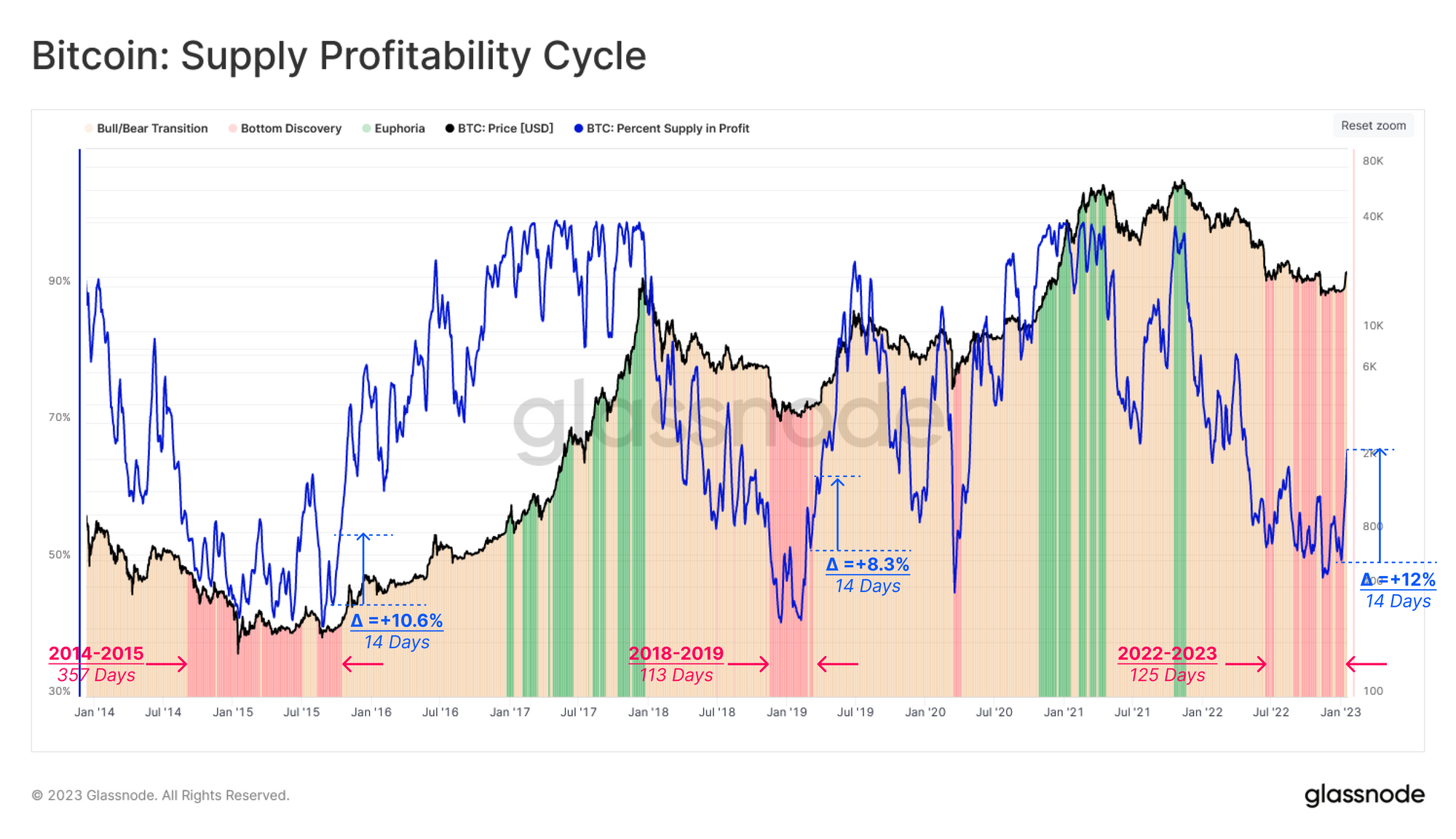

Percent Supply in Profit is an insightful metric to track when a market recovery may be underway, transitioning out of a bottom discovery phase (a loss-dominant regime) 🟥 back towards a healthier equilibrium between profit and loss 🟧. This transitional period can be considered active whilst the weekly average of the Percent Supply in Profit resides between 55% and 80%.

The recent rally from $16.9k to $23.1k has shown confluence with the Percent of Supply in Profit abruptly surging from 55% to over 67%. This 12% surge over 14 days has been one of the sharpest spikes in profitability compared to prior bear markets. This provides an indication of how much coin volume transacted and changed hands below $23.3k.

🗜️ Workbench Tip: These colored areas are established using the if-then statement, which highlights prices when a particular Percent Supply in Profit value is reached.

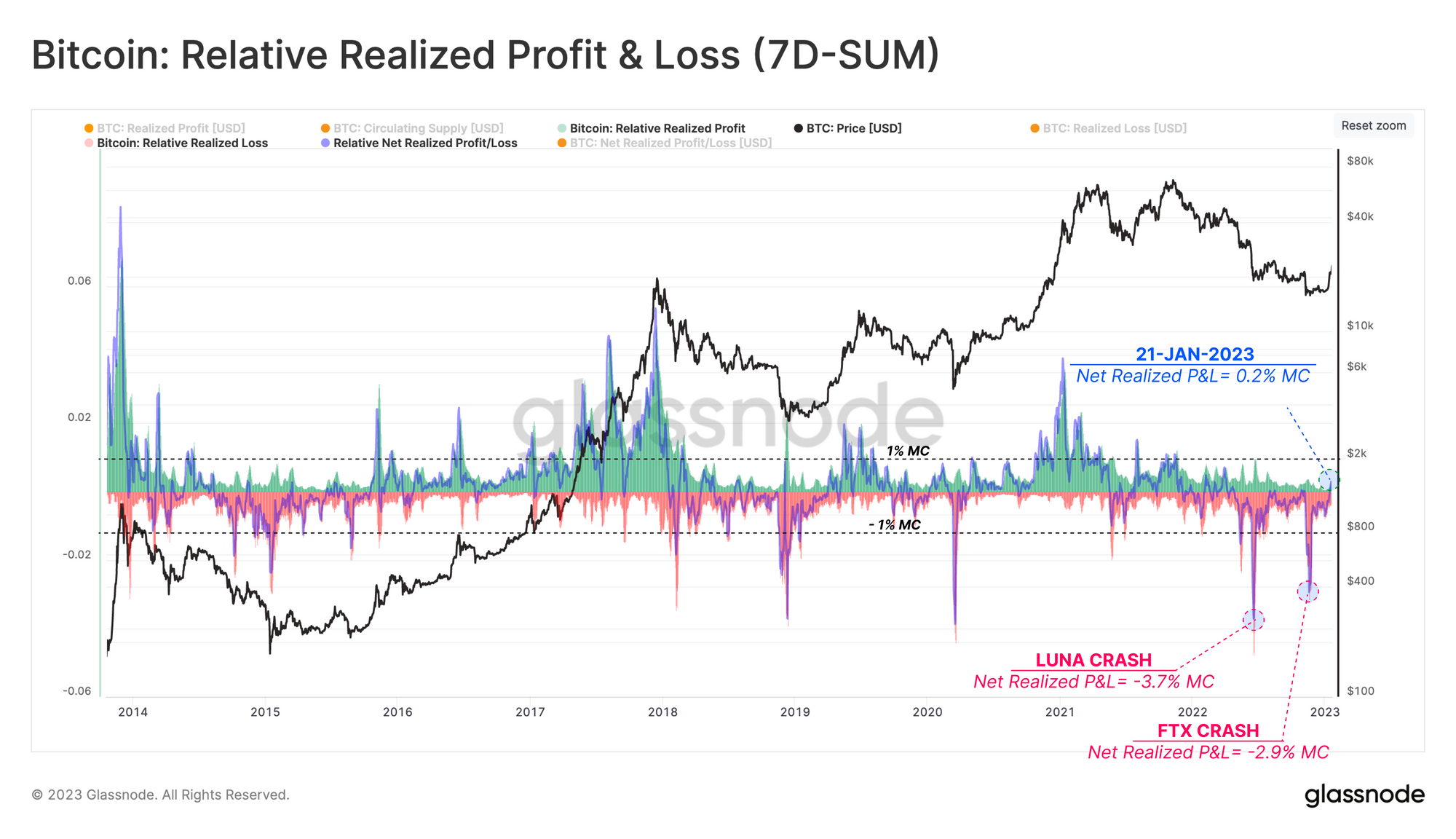

Historically, any abrupt change in supply (unrealized) profitability has motivated investors to react, which can be measured using metrics that describe Realized Profit and Loss.

The Realized Profit and Loss metrics measures the difference between the value of coins at the time of disposal and the time of acquisition. The chart below displays the weekly aggregated volume of Realized Profit and Loss alongside the Net Realized Profit and Loss. To compare magnitude across cycles, each trace is normalized by Market Cap.

- 🟩 The 7-day sum Realized Profit [USD].

- 🟥 The 7-day sum Realized Loss [USD].

- 🔵 The net 7-day sub of Realized Profit minus Loss.

The current bear, which started in November 2021, has undergone two remarkably large capitulation events, realizing a net loss of -2.9% and -3.7% of market cap per week, respectively. This regime has now shifted to one of Profit-Dominance, a promising sign of healing after the heavy deleveraging pressures inflicted in the second half of 2022.

An Opportunity For New Investors

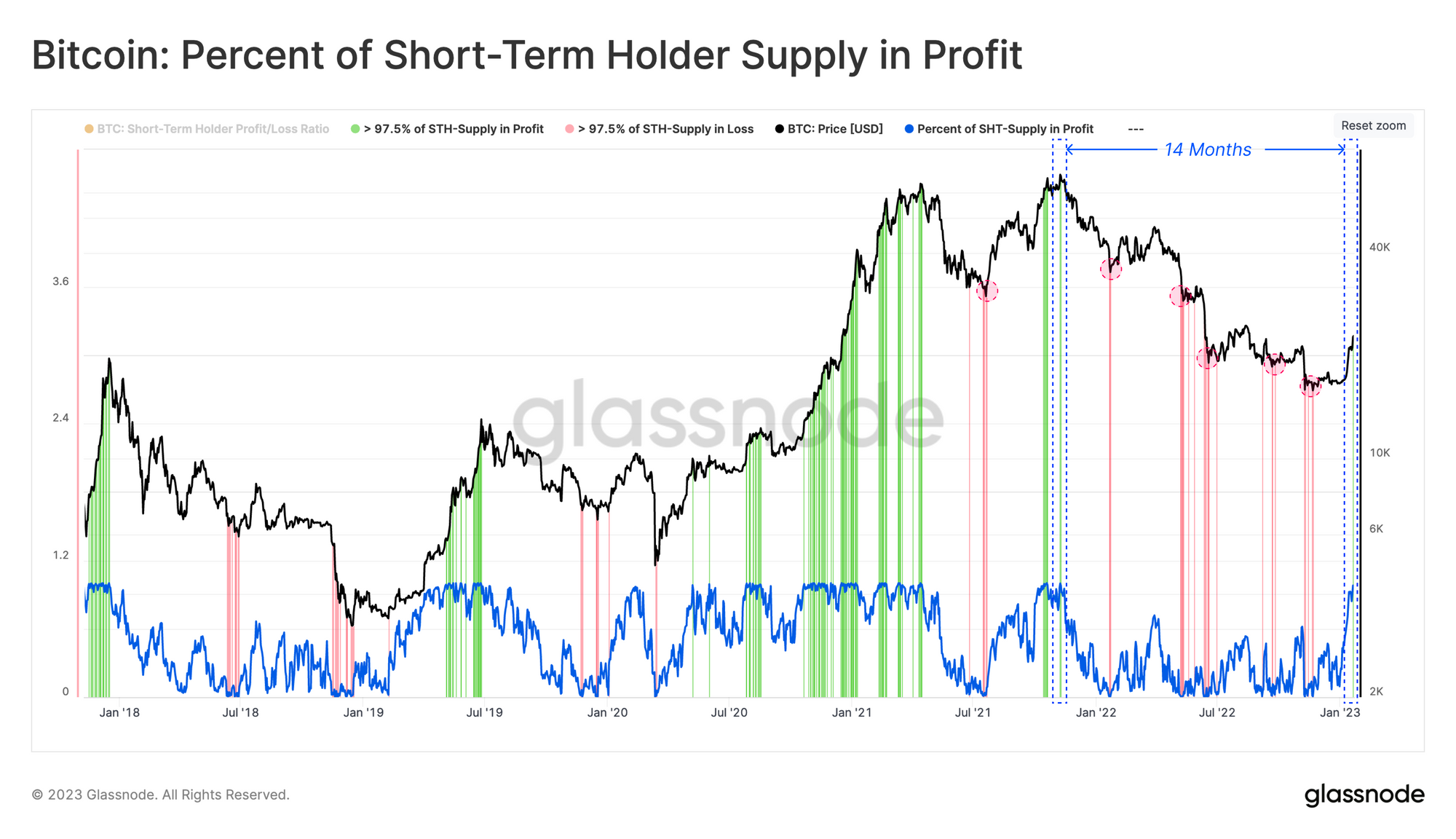

When the market is in a prolonged bottom (or top) discovery stage, new investor behavior becomes an influential factor in forming local recovery (or correction) pivot points. We can assess this behavior via the Percentage of Short-Term Holder Supply in Profit 🔵.

Interestingly, during bear markets, when > 97.5% of the acquired supply by new investors is in loss 🟥 the chance of seller exhaustion rises exponentially. Conversely, when > 97.5% of short-term holder supply is in profit, these players tend to seize the opportunity and exit at break-even or profit 🟩.

The recent surge to $23K has pushed this metric to > 97.5% in profit for the first time since the ATH in November 2021. Given this substantial spike in profitability, the probability of sell pressure sourced from STHs is likely to grow accordingly.

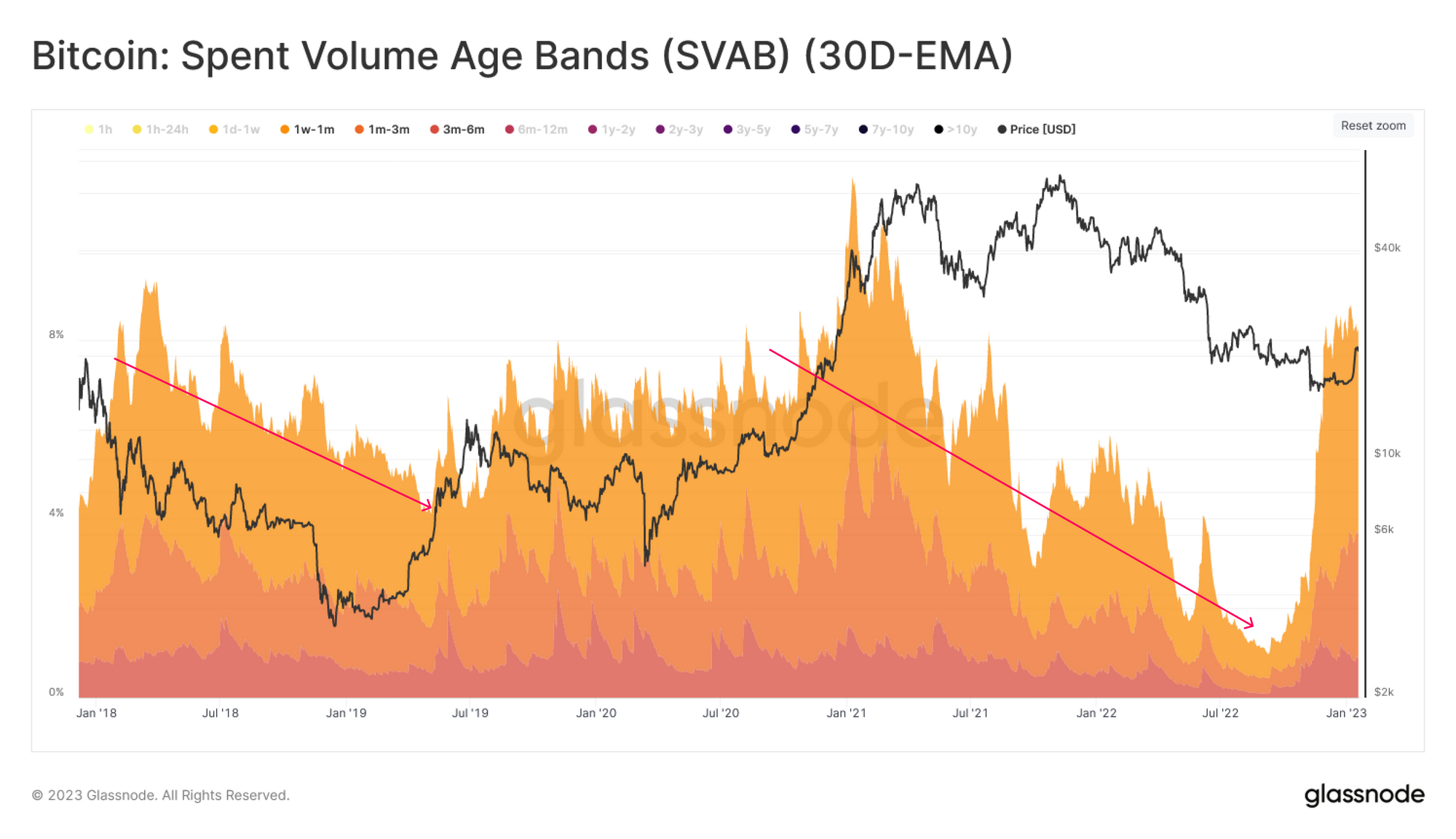

Looking at the spending volume of these newer holders through the Spent Volume Age Bands (SVAB) (30D-EMA) metric, we can see how this spike in profitability has driven the cohort’s spending volume well above the long-term declining trend.

Therefore, the sustainability of the current rally can be considered a balance between inflowing and newly deployed demand, meeting the supply drawn out of investor wallets by these higher prices.

Persistent Conviction

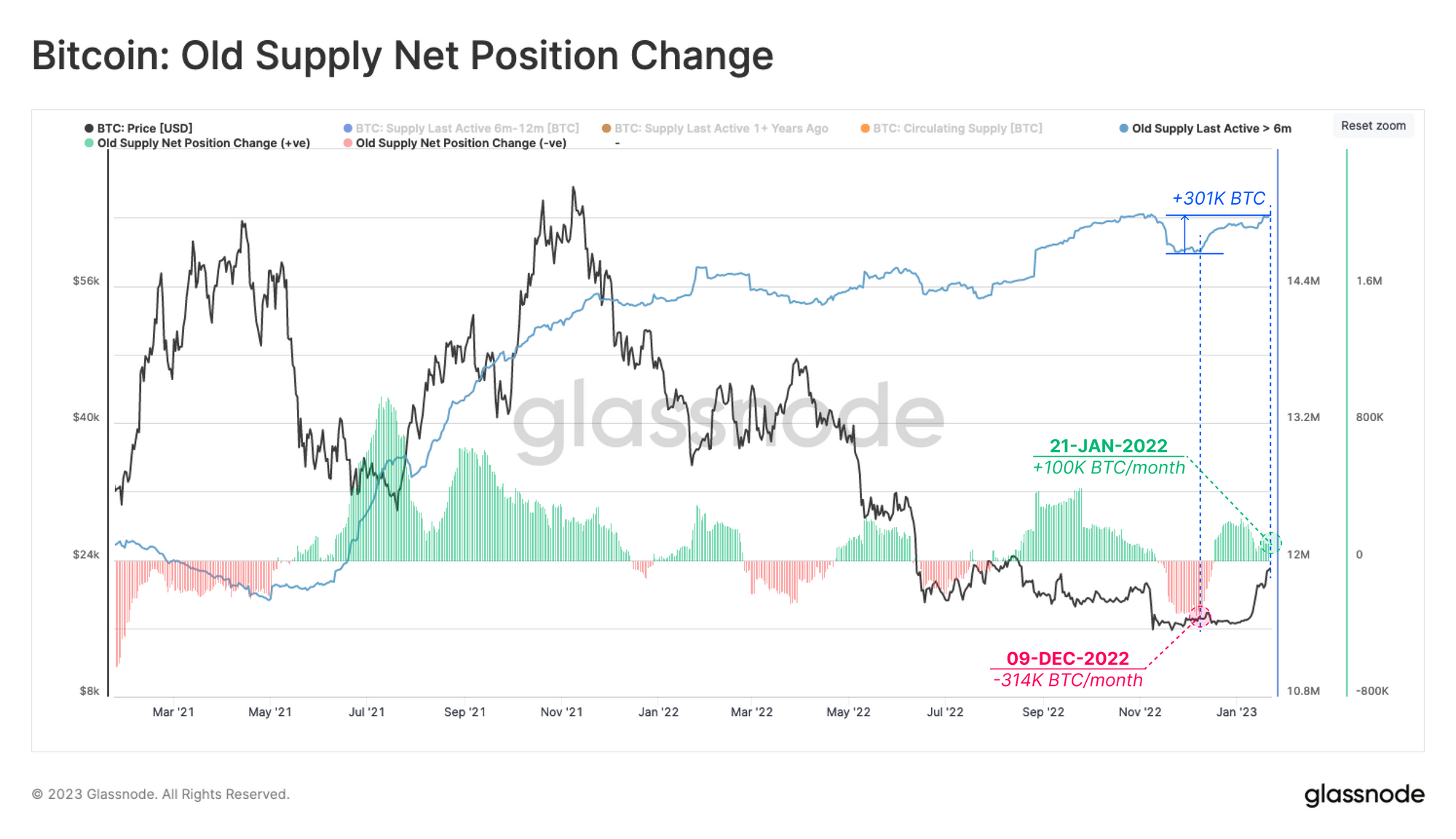

Assessing the profitability and behavior of short-term holders in isolation does not provide a full-scope assessment of the market. Therefore we shall perform the same study but focus on the long-term holder cohort, many of which are 2021-22 investors that remain overwhelmingly underwater on their holdings.

The LTH-MVRV 🟠 compares the cost-basis of the long-term holder cohort against spot prices, providing insight into the unrealized profit or loss held.

Tracing this metric shows that after 6.5 months, the market price has finally recovered above the long-term holders' cost basis at $22.6k. This denotes that the average LTH is only just above their break-even basis.

Considering the time length of LTH-MVRV traded below 1 🟩 and the lowest printed value, the ongoing bear market has been very comparable with 2018-2019 so far.

Despite the recovery from a historically undervalued condition, remarkably, the volume of coins aged more than 6 months (Old-Supply) 🔵 has increased by 301k BTC since early December. This divergence highlights the strength of the HODLing conviction via the recent market rally.

In other words, the supply held by HODLers has shifted from a contraction of -314k BTC/month following FTX collapsing, to an expansion at a rate of +100k BTC/month.

🪟 Related Dashboard: More information on the behavior of long and short-term holders can be found on our BTC: HODL Wave Dynamics dashboard for Advanced members.

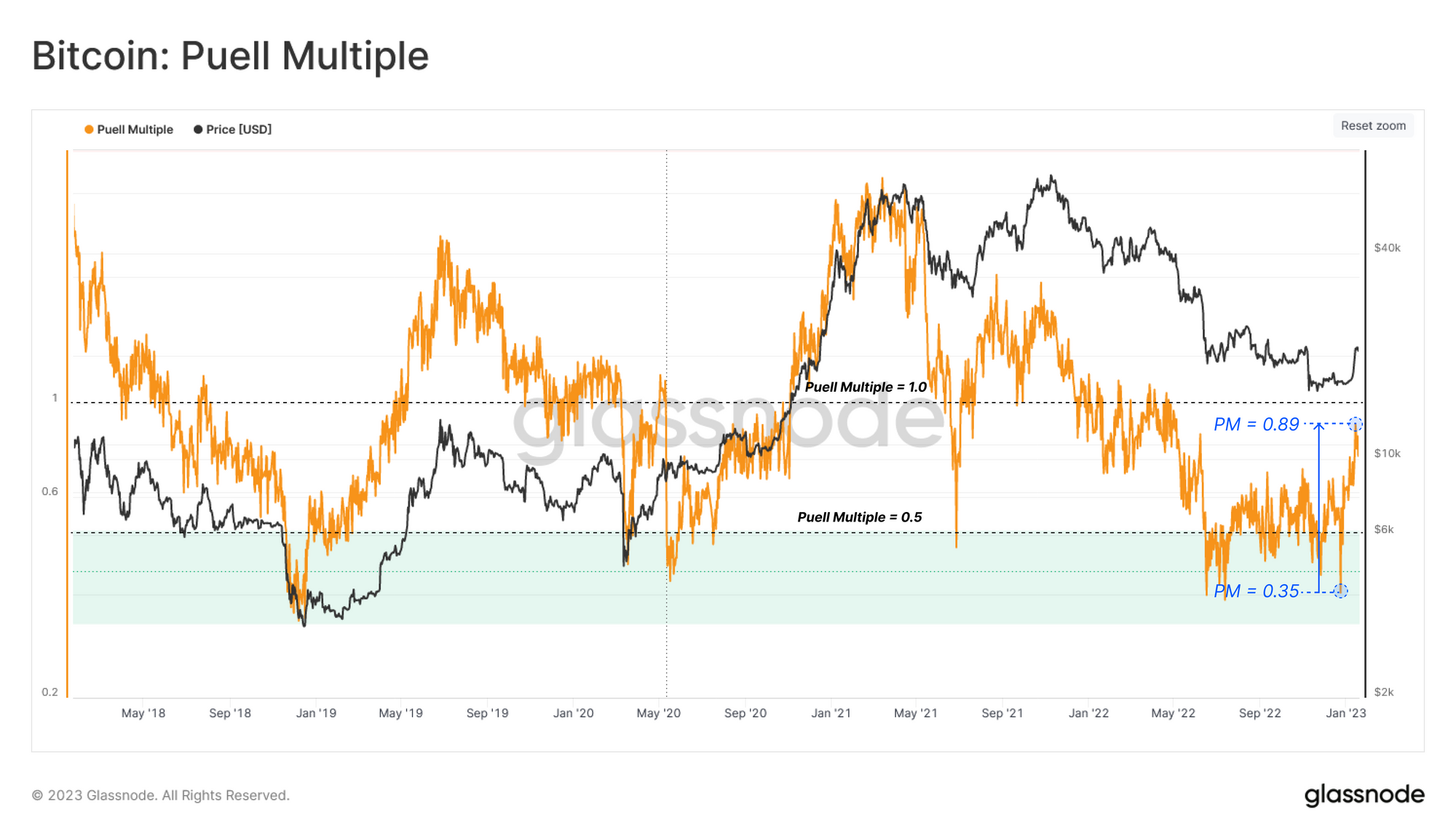

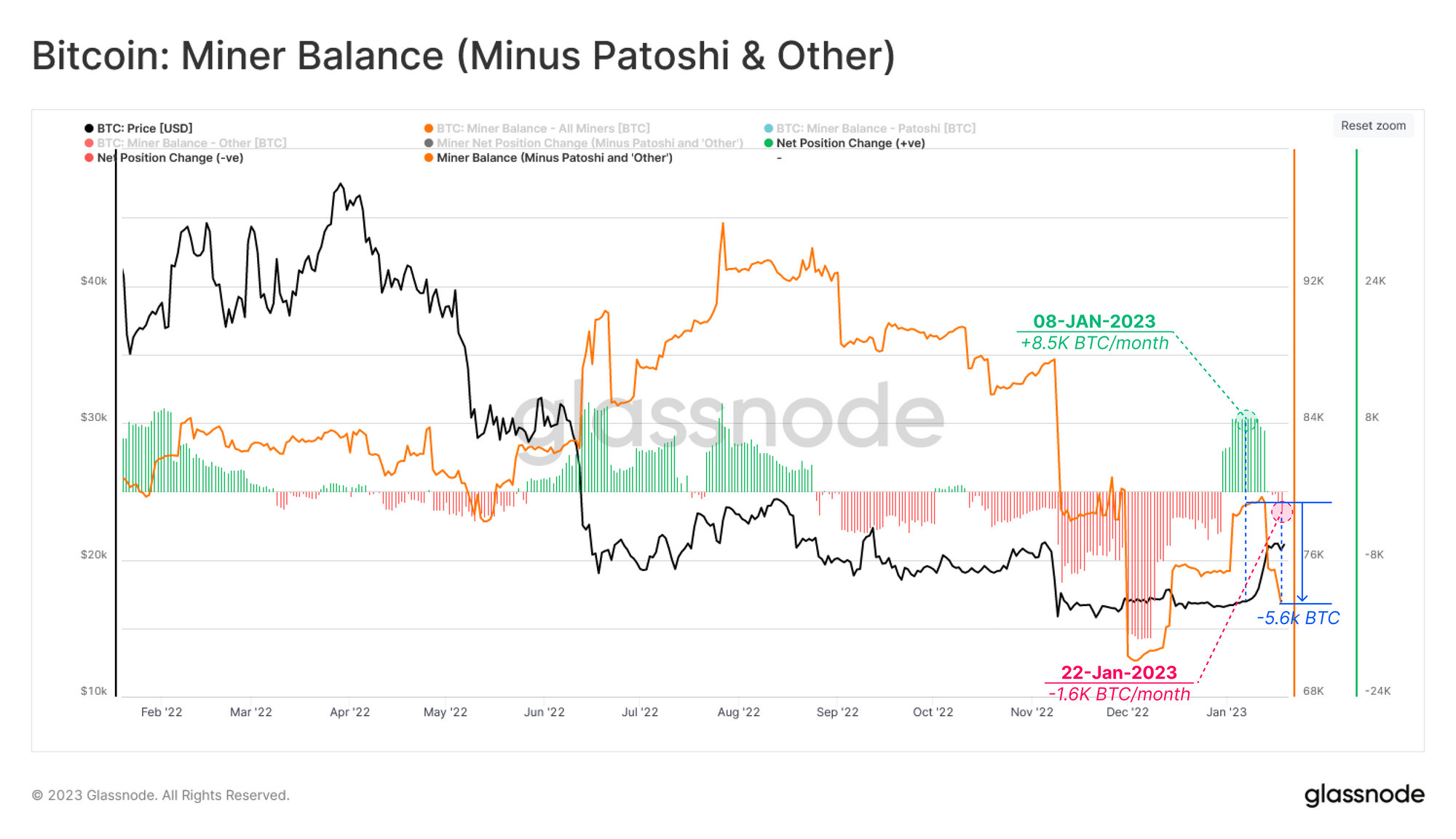

Miners Selling into Rally

Similar to the short-term holders, Miners have also taken advantage of the recent price appreciation to shore up their balance sheets.

The Puell Multiple 🟠 is the ratio between the aggregate miners' daily income (USD-denominated) to their yearly average. It shows that the relative miner revenue has increased by 254% compared to early January, highlighting how immense the financial stress experienced by the industry has been throughout the bear market.

With a notable recovery in miner USD-denominated revenues, the resulting behavior shift has switched from accumulation of +8.5k BTC/month, to distribution of -1.6k BTC/month. Miners have spent some -5.6k BTC since 8-Jan and have experienced a net balance decline YTD.

Conclusion

The recent price recovery from the December lows to over $23.2k has significantly improved investor profitability across the board. Consulting the price models, we can see that the recent rally has reclaimed several cost-basis models and pushed the proposition of supply held at a profit into the more favourable territory.

However, higher prices and the allure of profits after an extended bear market tend to motivate supply to re-enter liquid circulation. Analysis of cohort behavior shows that short-term holders and miners have been motivated by the opportunity to liquidate a portion of their holdings.

On the contrary, the supply held by long-term holders continues to grow, which can be argued to be a signal of strength and conviction across this cohort. Given the effect of long-term holders on the macro trend, watching their spending is likely a key toolset to track over the coming weeks.

Disclaimer: This report does not provide any investment advice. All data is provided for information and educational purposes only. No investment decision shall be based on the information provided here and you are solely responsible for your own investment decisions.

Product Updates

December was a relatively quiet month for the markets, but the Glassnode team was still hard at work shipping our new Discovery Page feature, 4x new dashboards, and 23x Workbench constructions. See our latest Product Update for December for a full overview.

Translated channels

We are proud to have launched new social channels for:

- Spanish (Analyst: @ElCableR, Telegram, Twitter)

- Portuguese (Analyst: @pins_cripto, Telegram, Twitter)

- Turkish (Analyst: @wkriptoofficial, Telegram, Twitter)

- Farsi (Analyst: @CryptoVizArt, Telegram, Twitter)

- Follow us and reach out on Twitter

- Join our Telegram channel

- Visit Glassnode Forum for long-form discussions and analysis.

- For on-chain metrics, dashboards, and alerts, visit Glassnode Studio

- For automated alerts on core on-chain metrics and activity on exchanges, visit our Glassnode Alerts Twitter