Bitcoin Faces Sell-Side Headwinds

Bitcoin bulls face a number of headwinds, ranging from dwindling demand on-chain, to over 4.7M BTC held at an unrealized loss. In this edition, we explore this potential sell-side energy carried by underwater investors.

Bitcoin markets have continued to struggle, with prices trading down from the weekly high of $44,659, and closing below the psychological $40k support level at $38,144. Weakness in both Bitcoin, and traditional markets, reflects the persistent risk and uncertainty associated with Fed rate hikes expected in March, fears of conflict in Ukraine, as well as growing civil unrest in Canada and elsewhere.

As the prevailing downtrend deepens, the probability of a more sustained bear market can also be expected to increase, as recency bias and the magnitude of investor losses weighs on sentiment. The longer that investors are underwater on their position, and the further they fall into an unrealized loss, the more likely those held coins will be spent and sold.

As such, we will focus this newsletter on the 'potential sell-side energy' that remains within the coin supply, primarily the volume of supply held at an unrealized loss, and whom it is held by.

Translations

This Week On-chain is now being translated into Spanish, Italian, Chinese, Japanese, and Turkish.

The Week Onchain Dashboard

The Week Onchain Newsletter has a live dashboard with all featured charts available here. This dashboard and all covered metrics are explored further in our Video Report which is released on Tuesdays each week. Visit and subscribe to our Youtube Channel, and visit our Video Portal for more video content and metric tutorials.

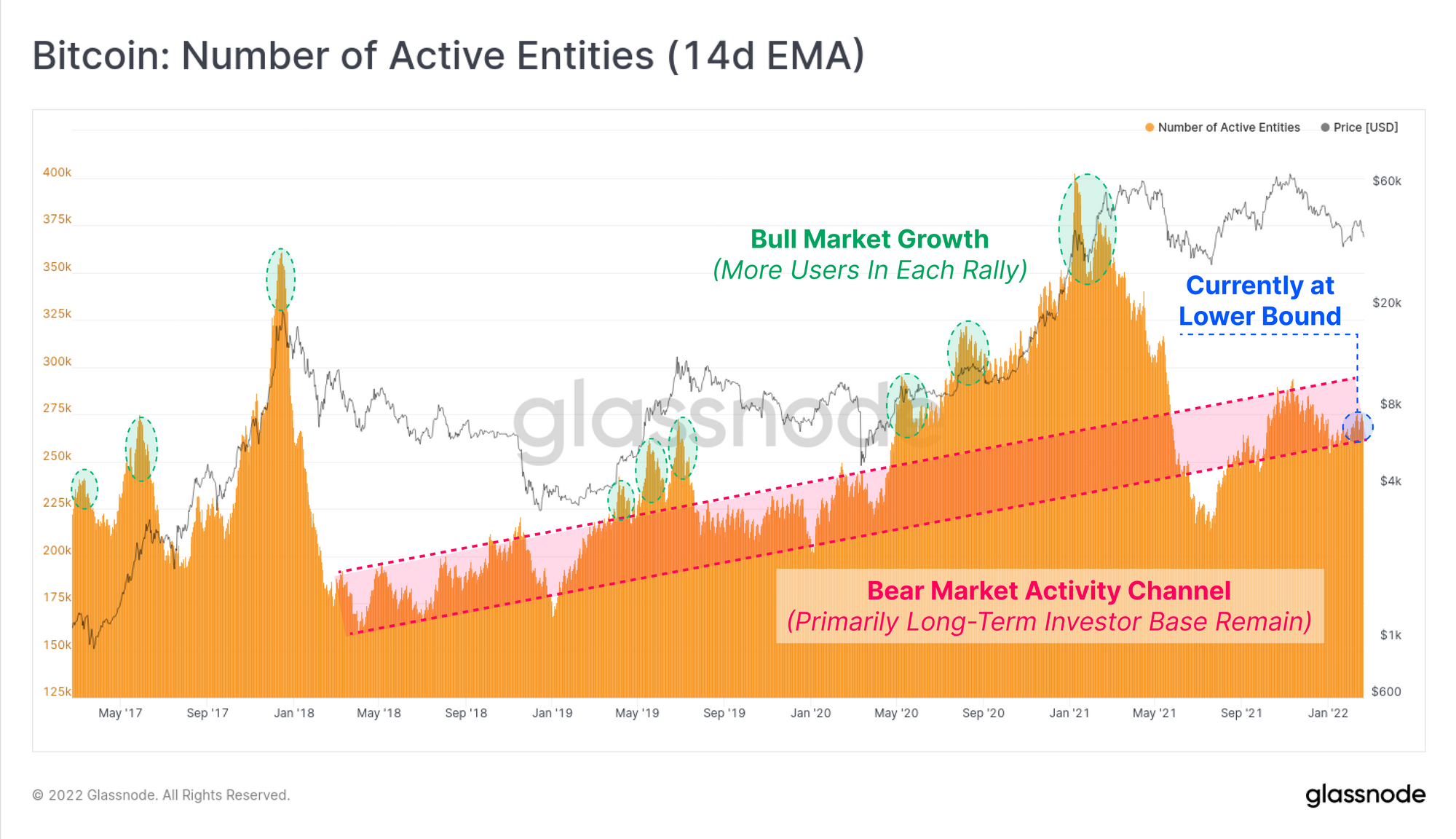

The Bear Market Channel

One of the distinct signals of bearish Bitcoin markets is a lack of on-chain activity. This can be identified using tools such as Active Addresses/Entities as a proxy for users, or via blockspace demand metrics such as Transaction Counts, and On-chain Fees spent as users bid for inclusion in the next block.

The chart below presents the number of Active Entities using the Bitcoin network over the last 5yrs.

- Bull markets can be clearly identified as periods of growing demand from users, typically with an increasing number of active entities during each subsequent bullish impulse (net user growth).

- Bear markets are characterised as periods of relatively low network activity, and diminished interest from retail, marked out in the red channel below. The lower-bound of this channel has historically increased in near-linear fashion, suggesting that the pool dependable Bitcoin users (the HODLers) is still growing over the long-term.

This week however the degree of on-chain activity is languishing at the lower-bound of the bear market channel, which can hardly be interpreted as a signal of increased interest and demand for the asset.

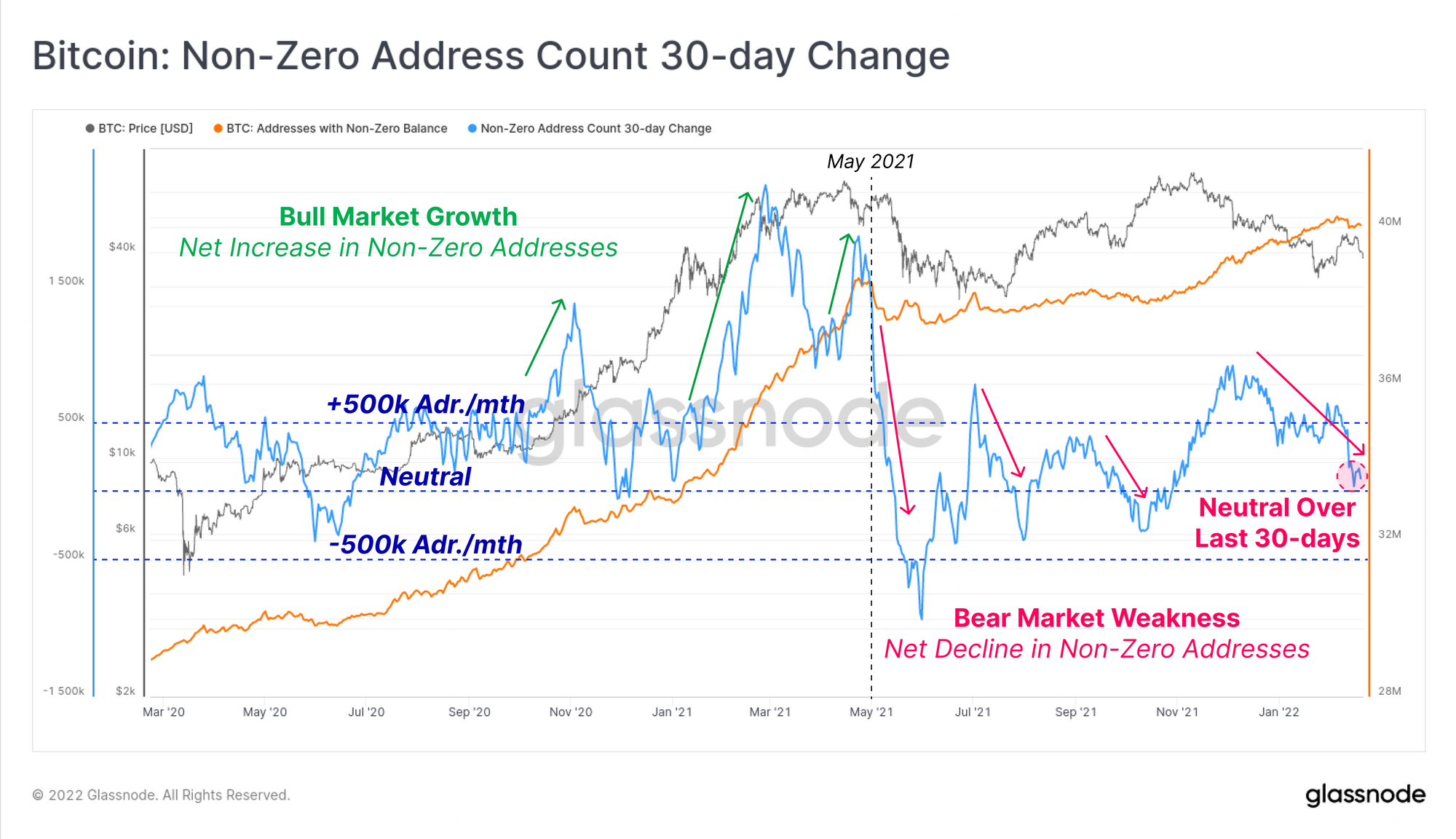

Supporting this observation is the 30-day change in non-zero balance addresses. Whilst a relatively crude measure of user-base demand, periods of high demand and supply accumulation are usually accompanied by an increase in UTXO creation, and growth in non-zero address counts (and vice-versa).

Whilst the macro trend in non-zero balance address creation is upwards, over the last 30-days, there has been a softening of the trend. This is the result of some investors emptying their address balances completely. Over the last month, around 219k addresses (0.54% of the total) have been emptied, which is a metric to watch in case this is the start of a period of net outflows of users from the network (as was seen in May 2021).

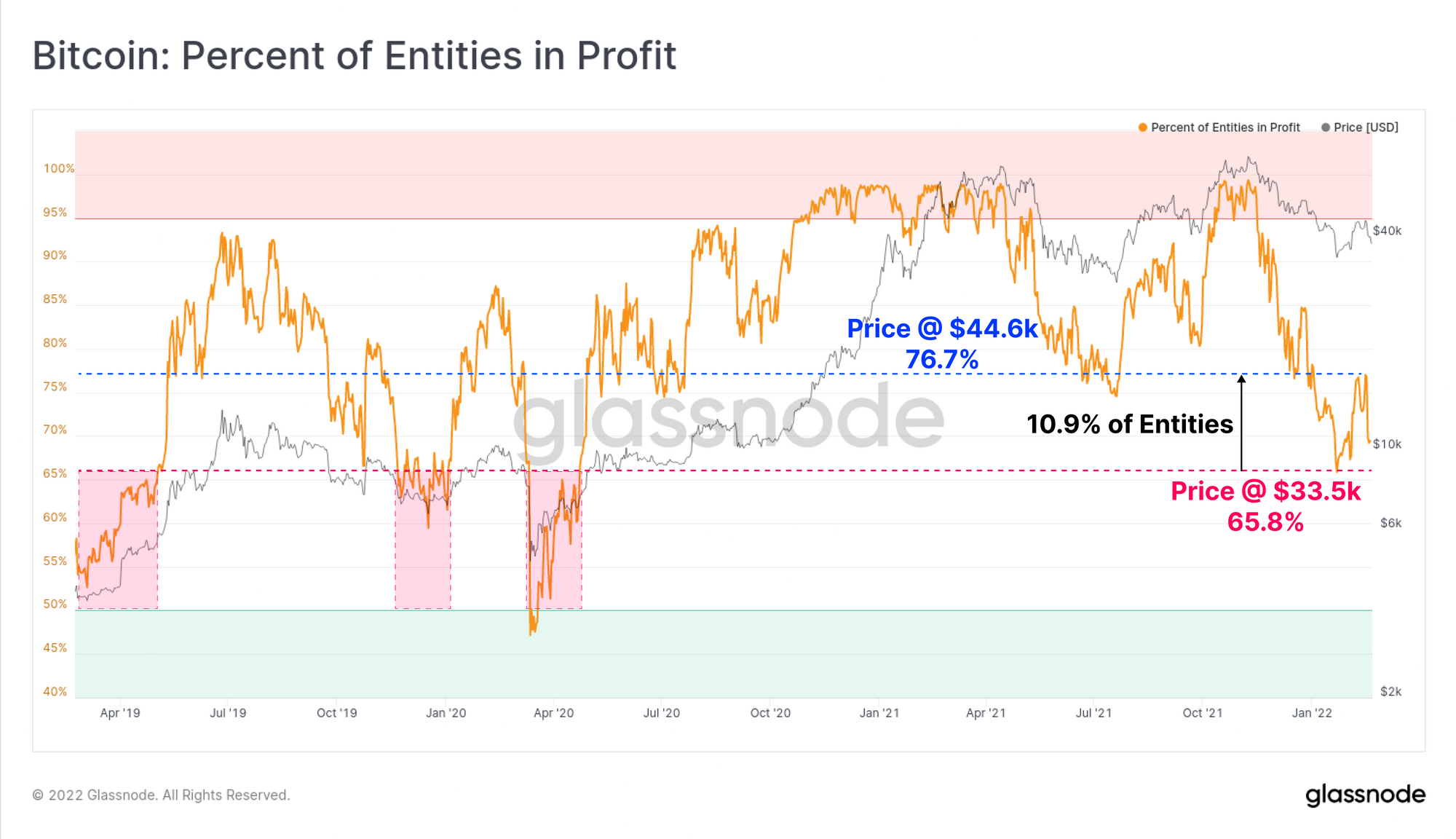

A probable cause for this spending behaviour is associated with the financial cost, and psychological pain of holding an underwater investment. We can see in the chart below that the proportion of on-chain entities in profit is oscillating between 65.78% and 76.7% of the network.

The flip side of this observation is that more than a quarter of all network entities are now underwater on their position. Furthermore, approximately 10.9% of the network has a cost basis between $33.5k and $44.6k, with many of them purchasing in recent weeks. If the market fails to establish a sustainable uptrend, these users are statistically the most likely to become yet another a source of sell-side pressure, especially if price trades below their cost basis.

Long and Short-Term Holder Losses Mount

One of the primary tools we use to assess the probability of a coin being spent (and assumed sold) is lifespan, defined as the time since the coin was last moved on-chain. On a statistical basis, the longer a coin remains dormant, the more likely it is to remain dormant.

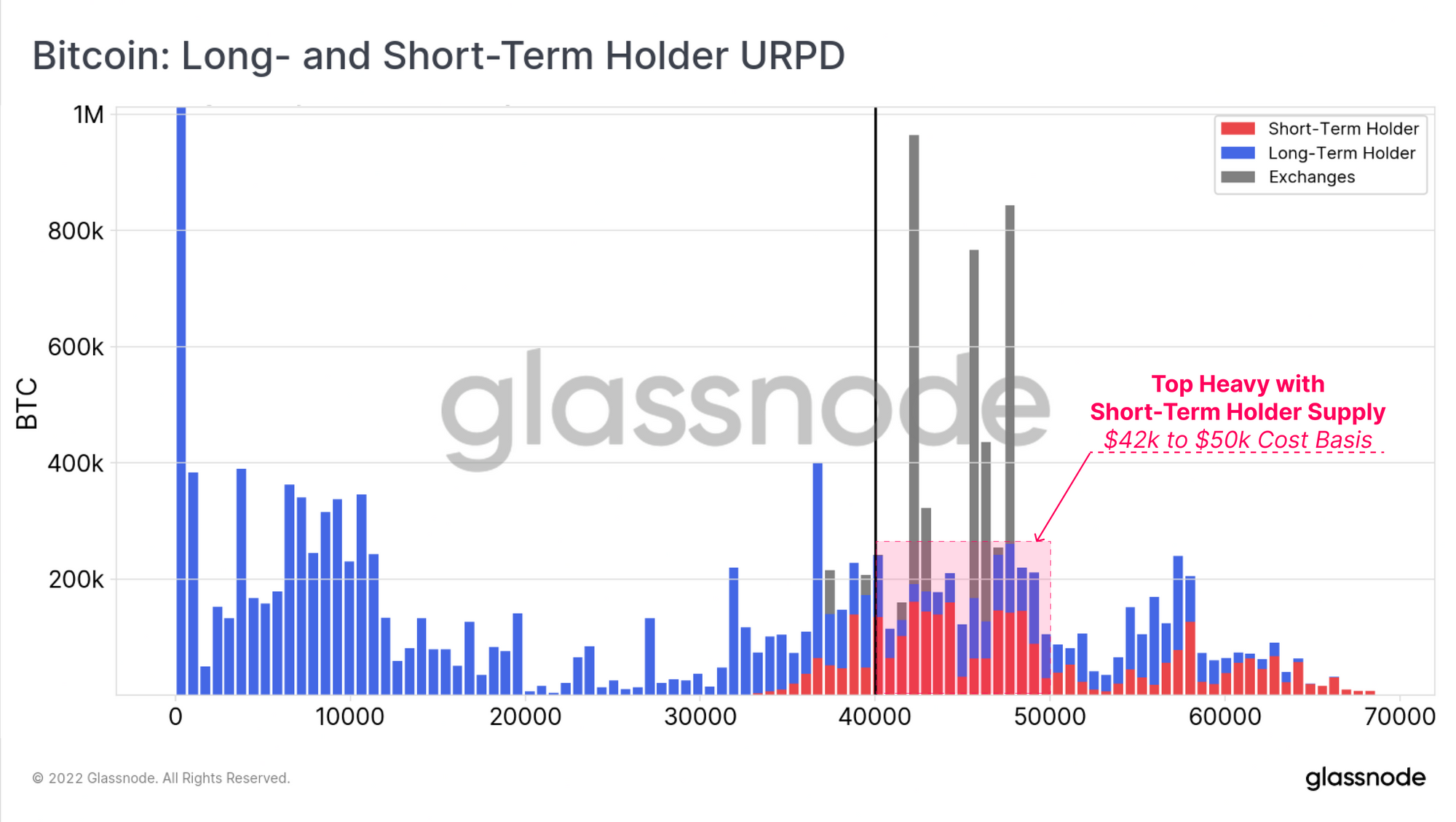

This leads into our definition of Long-Term (> 155-day, blue) and Short-Term (< 155-day, red) holders, which is a representation of coins that have a low and high probability of being spent and sold, respectively.

Using these cohorts, we can break down the distribution of prices where each coin in the supply was last moved. We do this to assess price levels associated with a large cluster of investor cost basis. What stands out is the high concentration of supply held by STHs between $42k and $50k.

With prices currently trading underneath the lower end of this range, and alongside dwindling on-chain activity, the coins held by this price sensitive cohort market represent a likely source of sell-side pressure, unless balanced by an equivalent influx of demand.

New Content: Short-Term Holder Shake-out

In case you missed it, our latest video analysis attempts to isolate which on-chain cohorts are the most likely source of sell-side pressure in the current environment. We analyse Short-Term Holders in particular using supply dynamics and spending behaviours.

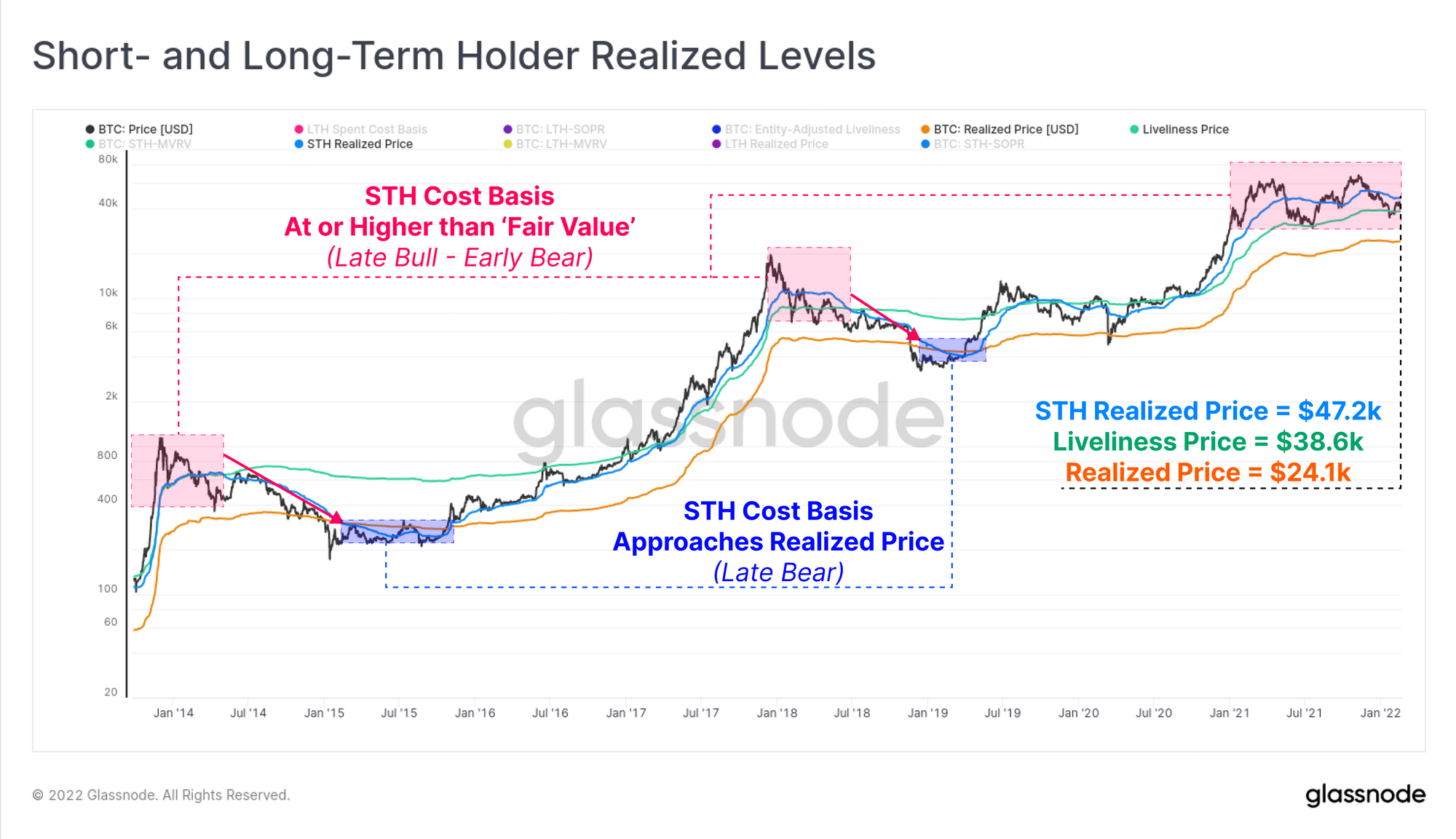

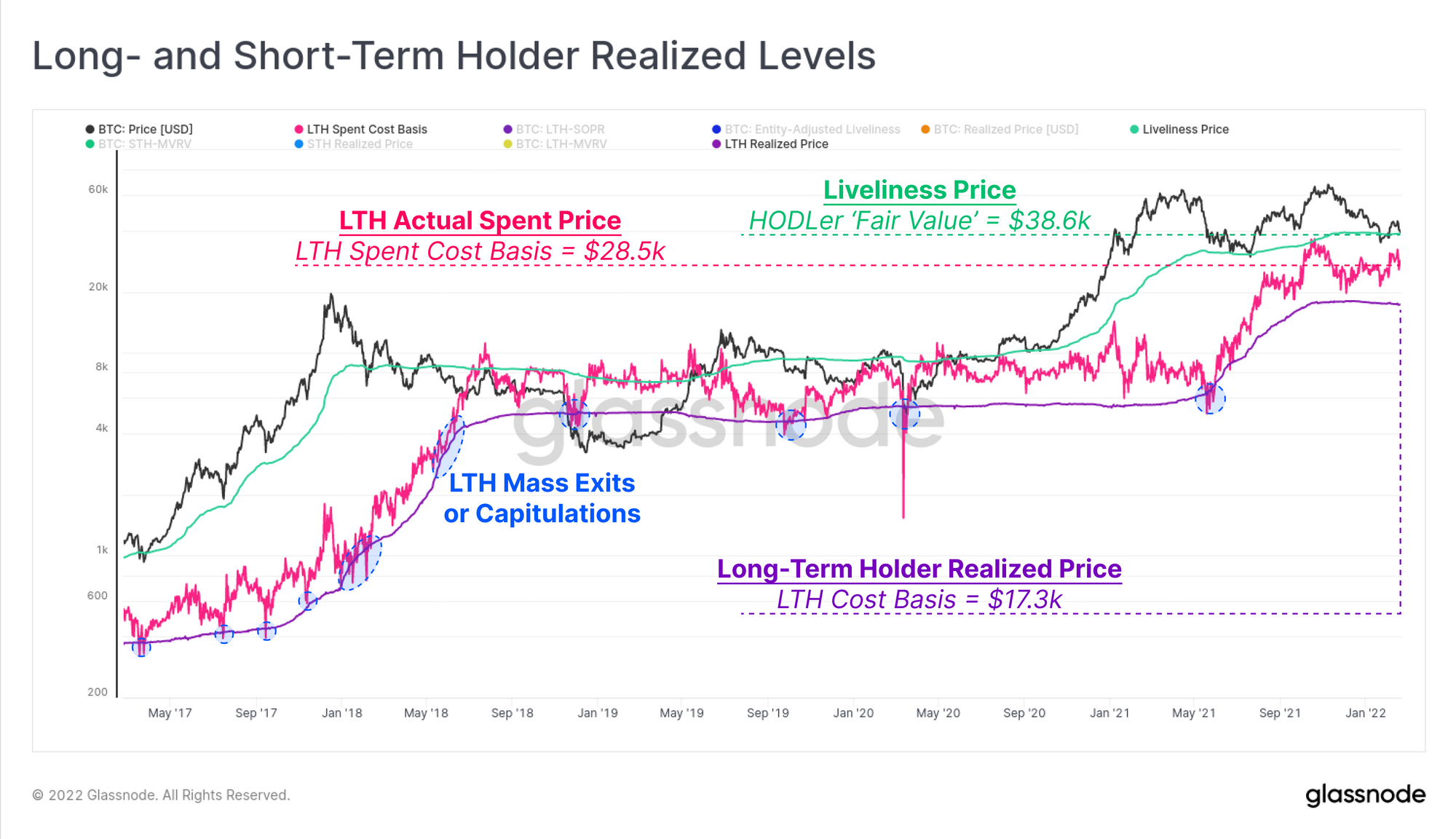

As a gauge of just how underwater Short-Term Holders are, we can calculate the STH Realized Price (aggregate cost basis) by dividing price by the STH-MVRV Ratio (result in blue). This indicates that STHs have an average on-chain cost basis of $47.2k, which at the time of writing (BTC price $38.1k) is an average unrealized loss of -19.3%.

Furthermore, the STH realised price is currently trading above the Liveliness Price ($38.6k) which reflects an estimate of 'HODLer Fair Value'. In both the 2013-14, and 2018 bear markets, when STHs hold coins well above this fair value estimate, it has signalled that the bearish trend has some time left in it to reestablish a price floor.

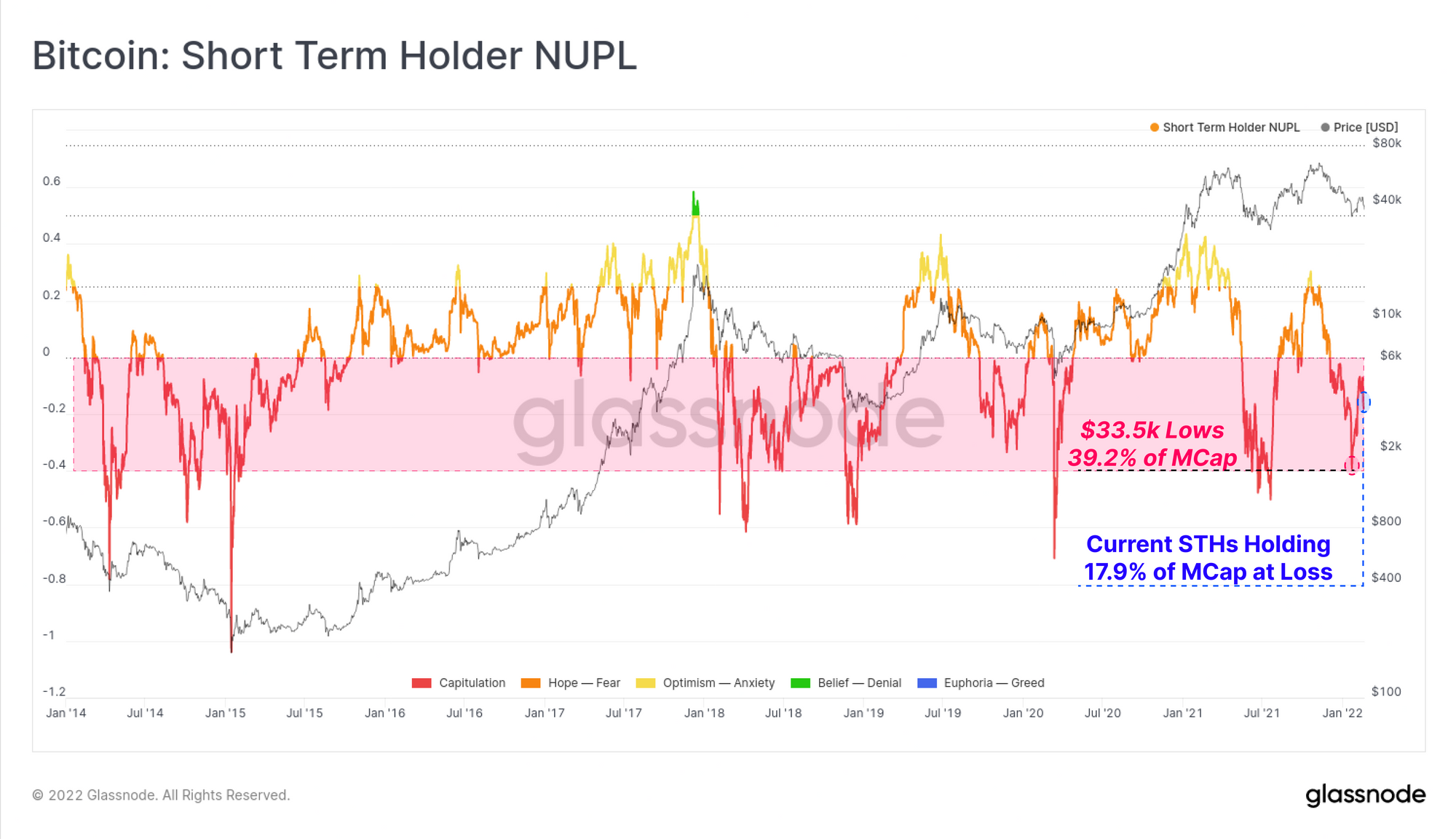

The STH-NUPL metric presents the magnitude of losses held by these Short-Term holders in proportion to the Bitcoin Market Cap. Here we can see that STHs have been underwater, in aggregate, since 4-Dec-2021. The total unrealized losses held by STHs is currently equal to 17.9% of Bitcoin's Market Cap.

At the recent price lows of $33.5k, STH-NUPL reached -39.2%, a level of extremely poor supply profitability, and a level that is rarely exceeded outside the deepest of sell-offs during bear markets. STHs have held coins at a loss for over 2 months now, which could be argued to be a sign of resilience, but should equally be considered a probable source of overhead resistance.

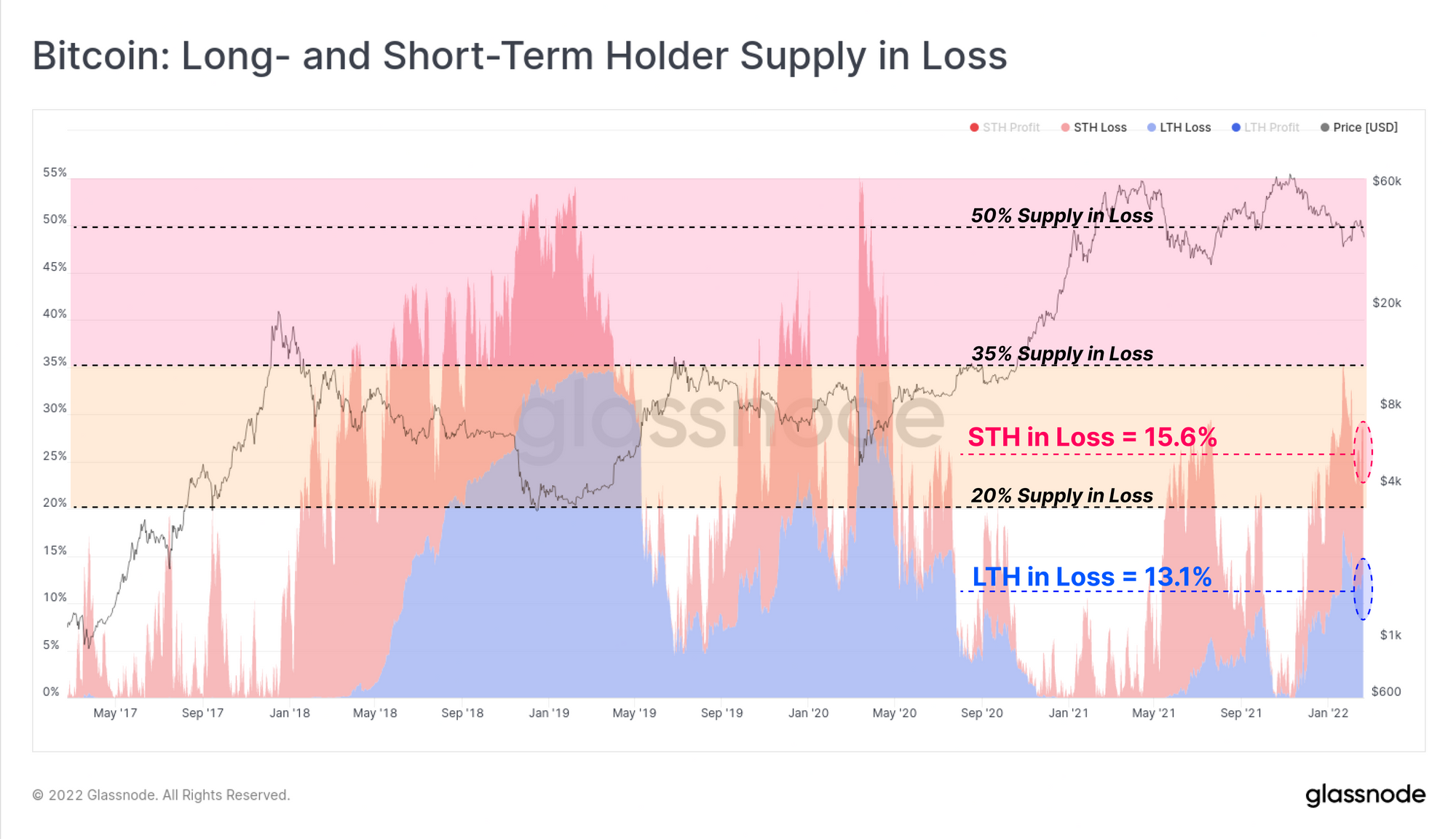

Looking at both cohorts, we can see a near even split in supply held at a loss between LTHs and STHs. Note that the supply percentages shown below are in proportion to the total supply that is not held in exchange balances (termed Sovereign Supply).

- STH supply in loss is currently 15.6% of Sovereign Supply (2.56M BTC).

- LTH supply in loss is currently 13.1% of Sovereign Supply (2.14M BTC).

The total magnitude of coin supply held in an unrealized loss is now higher than it was during the May-July 2021 period, but is only half as severe as the worst phase of the 2018 bear market, and March 2020 flush-out.

Nevertheless, with 28.7% of Sovereign Supply currently underwater (4.70M BTC), which again poses headwinds for to bulls to establish a compelling market recovery.

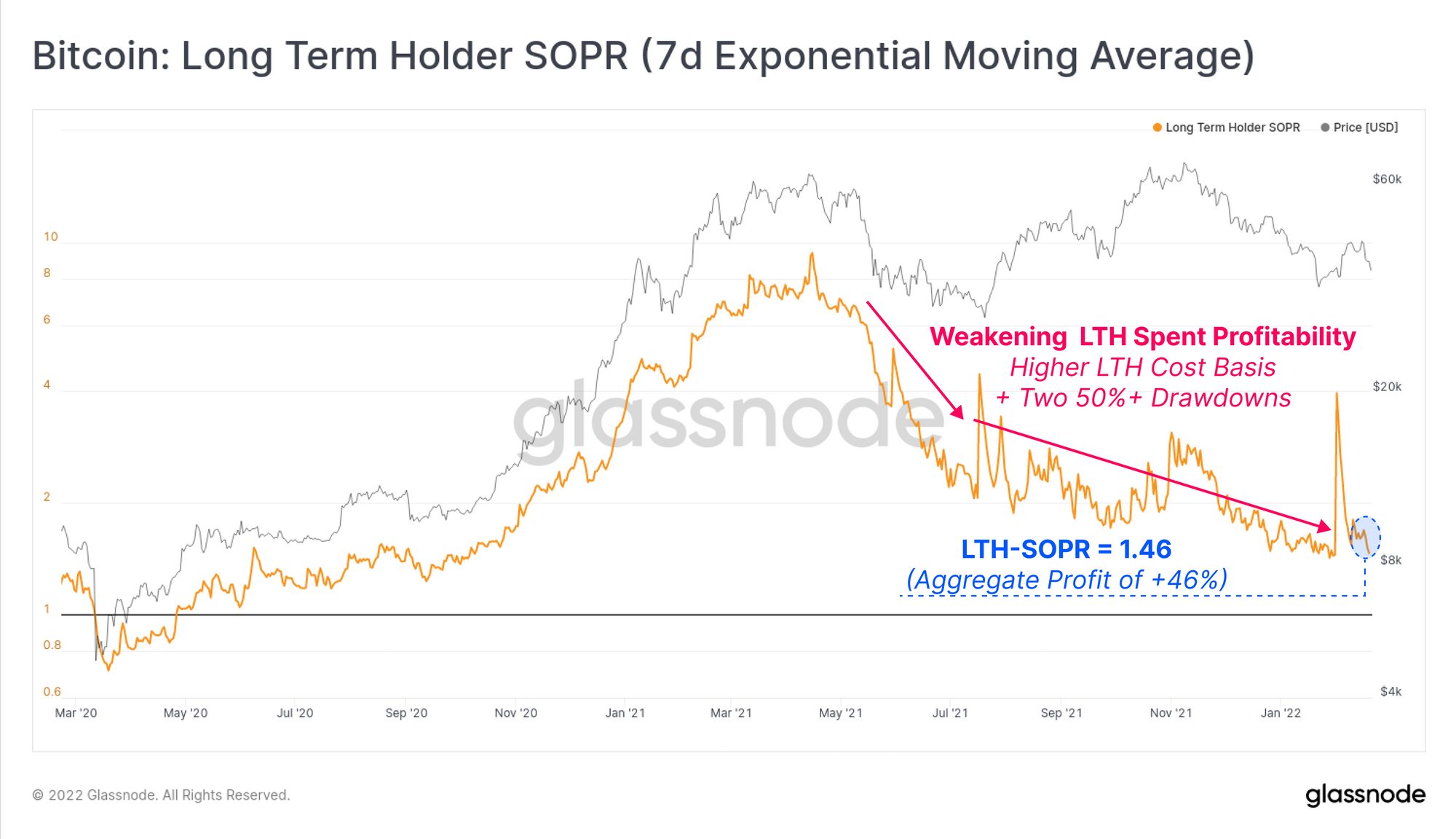

Shifting our focus to the Long-Term Holders, we can review the LTH-SOPR metric to assess the profitability of coins that are being spent on-chain by this cohort.

- Higher values of LTH-SOPR indicate greater profits realized, typically observed near bull market peaks.

- Lower values of LTH-SOPR indicate diminished profitability of spent coins, usually the combined result of bearish price action, and lower aggregate LTH cost basis (155-days ago, the market price was ~$40k)

At present, LTH-SOPR is returning a relatively low value of 1.46, suggesting that the coins that are being spent by LTHs are realizing a fairly modest 46% profit on aggregate. Historically, declining LTH-SOPR values are characteristic of macro sideways, to bearish market trends.

Using this concept of LTH-SOPR as a 'realized profit multiple', we can therefore estimate the LTH Spent Price (pink). This model reflects the average price at which today's spent LTH coins, were accumulated in the past.

This model is currently trading at $28.5k, which is very near the midpoint between the LTH Realized Price (LTH cost basis), and the Liveliness Price (HODLer 'Fair Value'). Once again, this style of behaviour is indicative of a lack of macro-direction in the market, and was seen particularly throughout the 2019-20 bear market.

Perhaps this leaves room for a final capitulation event where LTH Spent Price falls back to the LTH Realized Price. Or perhaps the general trend of LTHs holding their spot coin supply and using derivatives to hedge risk makes for a more constructive bear than we have seen in the past.

Summary and Conclusions

Overall, the Bitcoin market has numerous bearish headwinds in play, ranging from very weak on-chain activity (a proxy for demand), to large volumes of supply held at a loss (potential sell-side). With a total of 4.70M BTC currently underwater, and 54.5% of it held by STHs whom are statistically more likely to spend it, the bulls certainly have their work cut out for them.

However, despite the prevailing drawdown that has been in play for over three months, the underlying supply dynamics remain markedly more constructive that previous bears. As was covered in the last three WoC editions (weeks 5, 6 and 7), Bitcoin investors appear far more likely to hold on for dear life (HODL), and use derivatives to hedge risk, rather than selling spot to reduce exposure.

It looks like a bear market. But do keep in mind, that longer term, the bear authors the bull that follows.