Weakness in the Recovery

The Bitcoin market pulled back this week after a break-out from the multi-month consolidation range. Prices have thus far struggled to find sustained upside momentum, and there are indications of a modest volume of profit taking by investors.

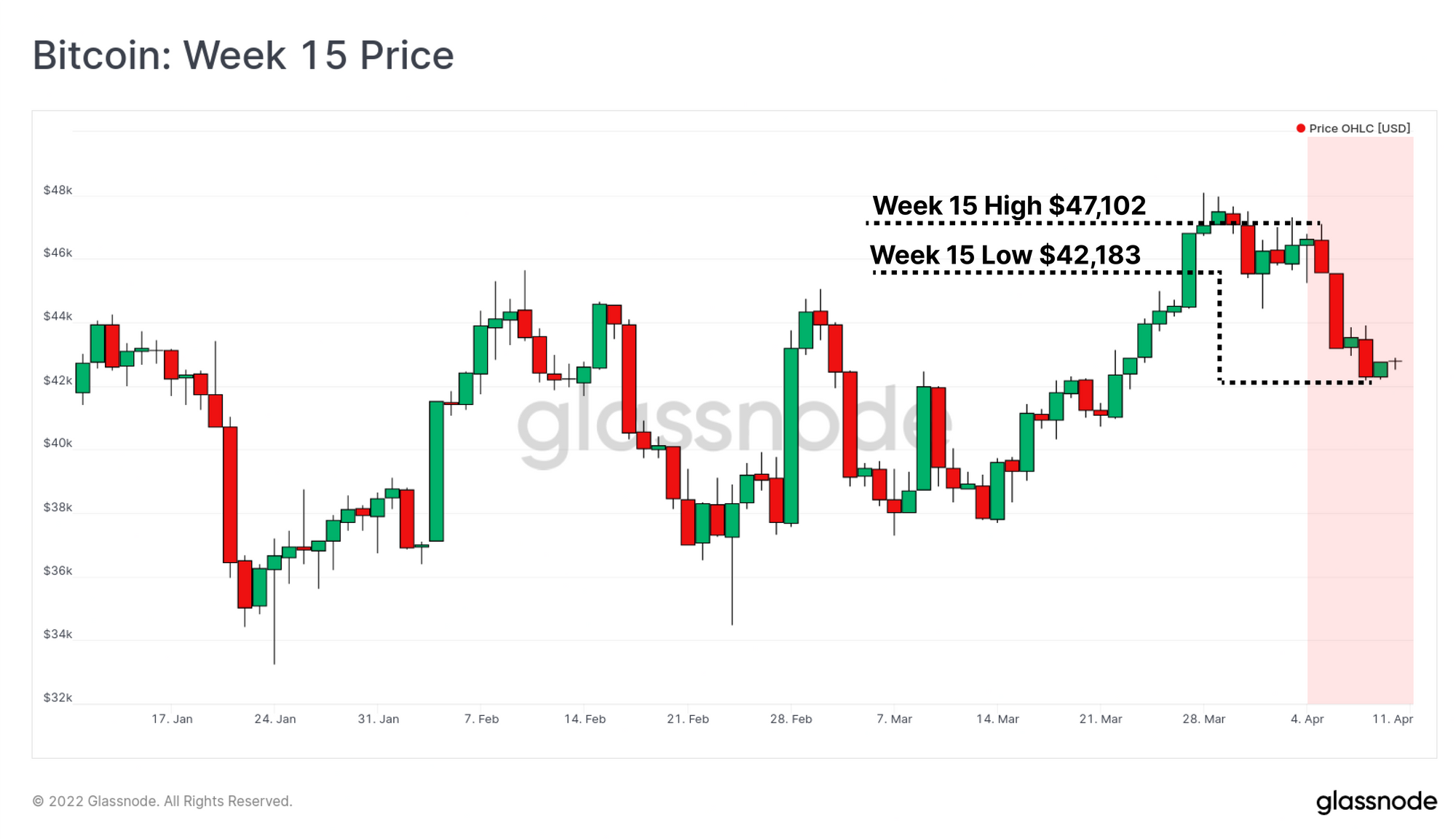

The Bitcoin market traded lower this week, coming off an opening high of $47,102, and slipping to a low of $42,183. This market weakness follows a relatively modest price break-out from the multi-month consolidation range that has been established since mid-January. On-chain activity and spending behaviours suggest that investors have been taking profits during the recent rally, and that we are yet to see a convincing influx of new users or demand.

In this edition we will explore the nature of the market recovery across on-chain activity and network profitability as a measure for growth and health of the Bitcoin user-base. We will also explore some of the mechanisms that enable the interesting dichotomy of BTC denominated transaction fees and block subsidy being near all-time-lows, whilst competition in the mining industry sets new all-time-highs.

Executive Summary

- The Bitcoin market pulled back this week as it struggles to establish upside price momentum.

- On-chain activity remains fairly muted, suggesting that there is little growth in the user-base, minimal inflows of new demand, and that the market remains largely HODLer dominated.

- Investor spending behaviour appears to be switching from dominance of loss realization, towards a modest amount of profit taking. 58% of transaction volume is currently realizing a profit.

- Aggregate Bitcoin transaction fees are currently near all-time-lows, a result of a confluence of factors including SegWit adoption, transaction batching, and the aforementioned lack of demand for Bitcoin block-space.

- Despite this, USD denominated miner revenue is up 150% compared to after the last halving event, and both hash-rate and protocol difficulty are setting consistent all-time-highs.