The UNI Token: Is Uniswap Really Decentralized?

The UNI token aims to transition Uniswap into a decentralized, community-owned protocol - but the team hasn't been fully transparent about the path to decentralization.

After becoming the world's highest-volume DEX within less than 18 months of launching, Uniswap recently faced an existential threat with the launch of SushiSwap, a Uniswap fork which introduced decentralized community ownership via its governance token, SUSHI.

Liesl Eichholz

Liesl Eichholz

Despite losing a large portion of its liquidity, Uniswap weathered this storm, and has emerged stronger than ever.

What's more, as a response to the likes of SushiSwap and the community's calls for decentralization, Uniswap launched its own native protocol token, UNI. According to the launch post:

"UNI officially enshrines Uniswap as publicly-owned and self-sustainable infrastructure while continuing to carefully protect its indestructible and autonomous qualities."

With this announcement and its returned dominance over SushiSwap, Uniswap has firmly re-established itself as the world's most popular DEX. But the transition toward token-based governance via the UNI token falls far short of true decentralization, at least for the foreseeable future.

UNI Token Basics

Token Utility

The primary function of the UNI token is governance over the Uniswap protocol and the funds in the governance treasury.

Another aspect of UNI's utility is a potential revenue share. The governance contract contains a fee switch which, if activated, will enable UNI holders to earn a portion of the protocol's fees (similar to the SUSHI fee model). This switch is subject to a 180 day timelock, giving investors and liquidity providers (LPs) half a year to prepare for the shift to this new revenue sharing model if it occurs.

Token Launch

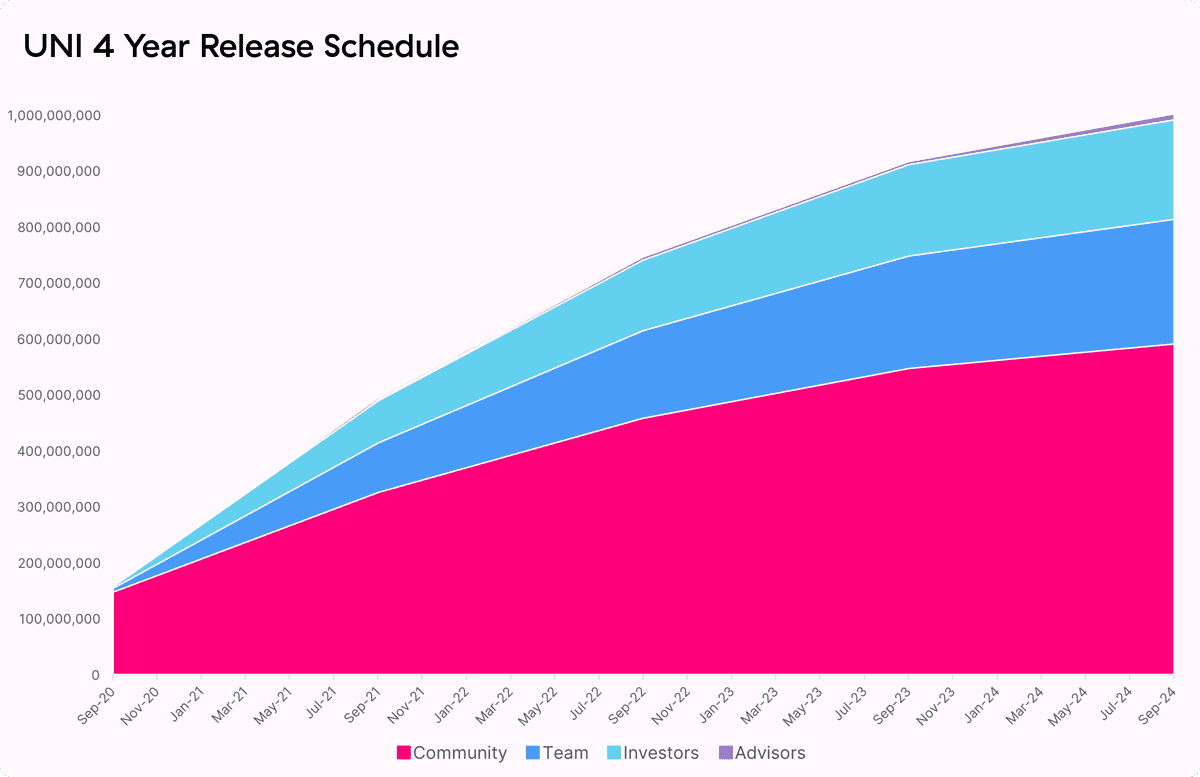

The UNI token is initially launching via a community airdrop and liquidity mine, which started on 18 September 2020. The genesis supply of UNI is 1 billion, which will gradually enter into circulation as outlined below.

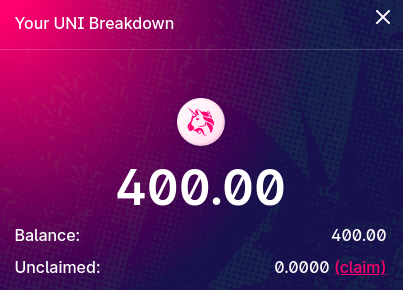

Community Airdrop - 15% of the genesis UNI supply is currently being distributed to the Uniswap community via an airdrop. 10.06% of the supply is going to historical users; any wallet that interacted with Uniswap's contracts before 1 September 2020 can claim 400 UNI tokens. In addition, 4.92% has been allocated to historical liquidity providers (pro-rated based on how much liquidity they provided in the past) and 0.02% is claimable by historical SOCKS users.

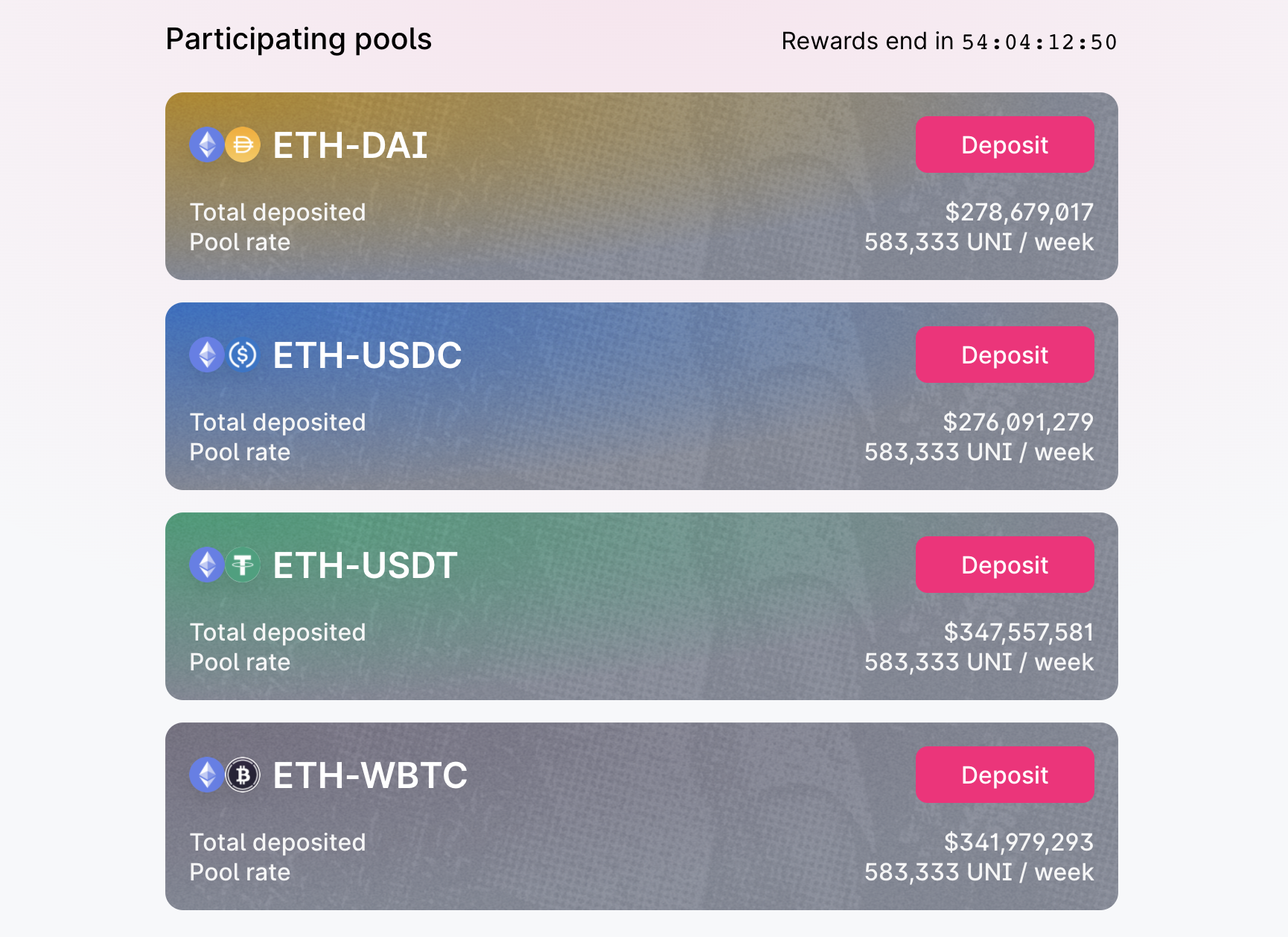

Liquidity Mining - Via the liquidity mine, an additional 2% of UNI will be distributed to the community. Anyone can farm UNI by providing liquidity to one or more of four pools, USDT/ETH, USDC/ETH, DAI/ETH, and WBTC/ETH, with the potential for more pools to be added after 30 days. Between 18 September and 17 November 2020, 5 million UNI will be allocated to each pool and distributed to LPs proportional to liquidity provided.

Token Distribution

The circulating supply of UNI tokens theoretically started at 150 million as a result of the community airdrop. However, because not all airdropped tokens have been claimed yet, the current circulating supply is only ~130 million.

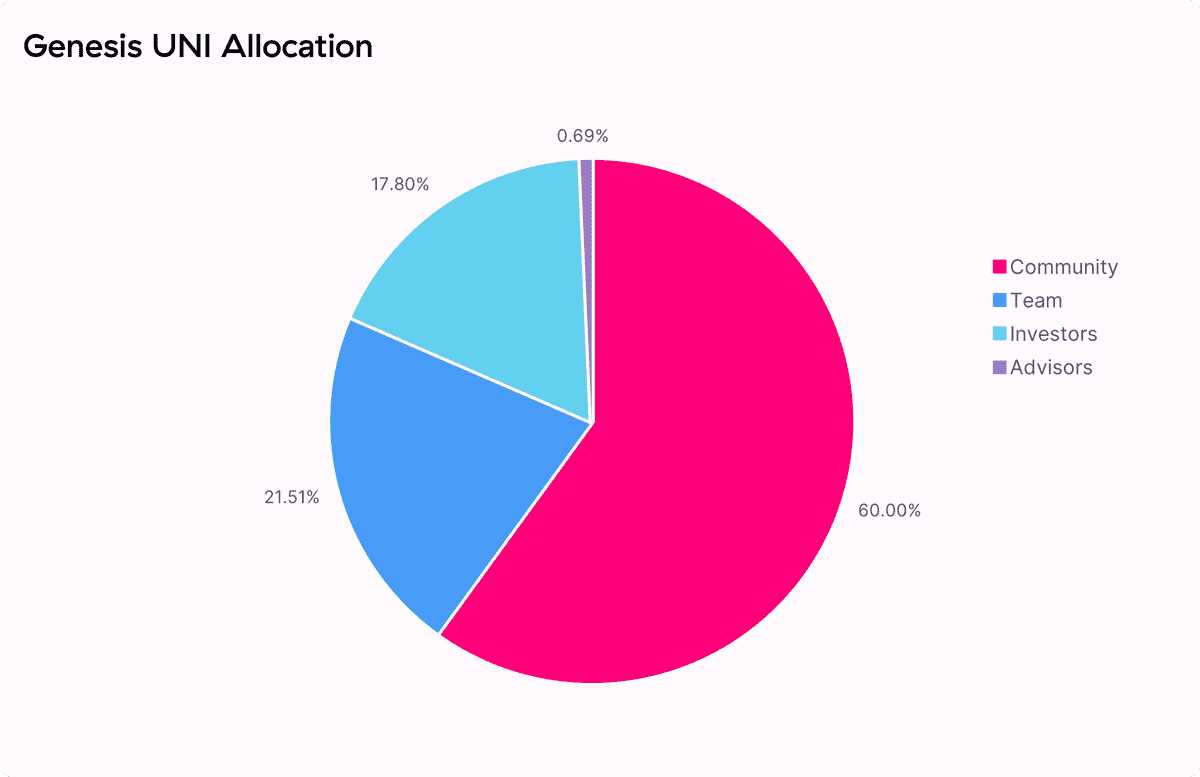

In total, 60% of the genesis supply will go to the community, while the remaining 40% have been allocated to Uniswap team members, investors, and advisors. These tokens will vest over 4 years, to minimize the potential for manipulation of the protocol and UNI markets.

Initial release:

- 15% to the community airdrop.

- 2% to liquidity mining (over the course of 3 months).

Vesting over 4 years:

- 43% to the governance treasury (explained in more detail below).

- 21.51% to team members and future employees.

- 17.80% to investors (i.e. early VCs who funded Uniswap).

- 0.69% to advisors.

As the above image shows, the Uniswap team and investors have allocated themselves an immense proportion of the total supply of UNI tokens. The pie chart feels more reminiscent of a 2017-style ICO than a 2020-style fair launch, which is one of several reasons why the narrative of a shift toward decentralized community ownership feels somewhat disingenuous.

Token Supply

The number of UNI tokens currently in existence is 1 billion, with Uniswap claiming that these will become accessible over 4 years:

After the first 4 years, a perpetual inflation rate of 2% per year will start, in order to encourage active participation rather than passive holding. The Uniswap team have not specified how these new tokens will be distributed, or to whom, but they will likely go into the governance treasury to be allocated to liquidity providers and development efforts.

Token Vesting: A Black Box

Although Uniswap has claimed that the team and investor allocation will vest over 4 years, the exact vesting schedule has not been publicly announced. Even more worryingly, these tokens currently appear to be fully liquid.

While the distribution schedule pictured above shows them vesting gradually, the tokens allocated to the Uniswap team and investors are currently held in regular Ethereum addresses (i.e. externally owned addresses, or EOAs) with no transfer restrictions. In contrast, the governance treasury tokens are locked up in smart contracts and will be released programatically over time.

It remains unknown who controls the keys to these addresses, but unless there is some other explanation, these tokens are apparently not locked up. It appears that the term "vesting" has been used very loosely by the Uniswap team, perhaps with the express goal of misleading community members into thinking the team/investor tokens will not be accessible until they vest.

The 400mm $UNI that is 4 year vesting for employees and advisors - Do we know the vesting schedule, unclear.. Are those account under timelock now... no?

— DK (@dkryptd) September 17, 2020

Am I missing something? Or is it if we violate your trust its mutually assured destruction? Ex here:https://t.co/UXgLKl4Q3w

This method of storing the tokens gives the Uniswap team and investors what essentially amounts to admin rights over the protocol.

There is probably a defensible explanation for this; it was likely implemented as a sort of "emergency override" in the event of a coordinated attack (as described below). In addition, perhaps in an attempt to inspire confidence, Uniswap has pledged that "team members will not participate directly in governance for the foreseeable future, although they may delegate votes to protocol delegates without seeking to influence their voting decisions."

But regardless of any security-related justifications or vague promises not to participate in governance, the decision not to lock up vesting tokens still raises concerns. Even if there is valid justification, the Uniswap team should have been transparent about the structure of these tokens, the reasoning behind keeping them unlocked, and the precautions being taken to prevent manipulation.

NOTE: The remainder of this analysis is predicated on the assumption that the team, investor, and advisor tokens are in fact immediately accessible and not locked up or restricted in any way. If anyone has another explanation or evidence to the contrary, please let me know.

UNI Governance

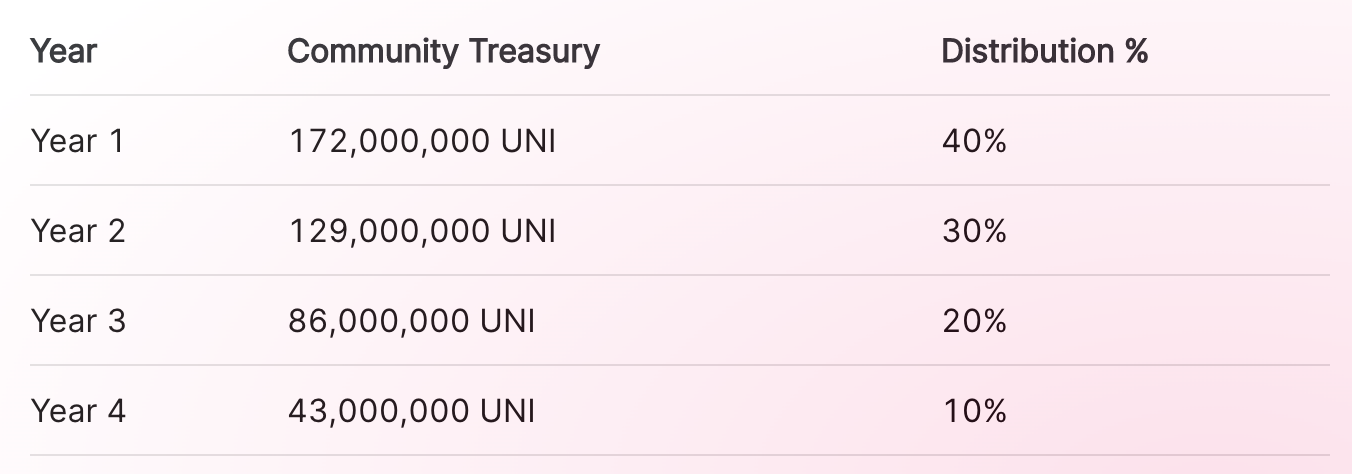

As mentioned above, the main function of the UNI token is that it grants holders the right to make decisions about the protocol. This includes updating and modifying the protocol's logic, as well as the ability to allocate funds from the governance treasury, which has been allocated 43% of the total supply (currently valued at over $2 billion).

Governance Treasury

The token's governance functionality went live on day one of the UNI token launch, but the treasury only unlocks after 30 days. Once it unlocks, UNI holders will be able to decide what to do with the funds in the treasury.

However, not all funds will be available at once; the tokens held in the governance treasury smart contracts will be released on an ongoing basis, with a gradually decreasing amount vesting over 4 years.

These tokens can be allocated toward contributor grants, community initiatives, liquidity mining, and other programs to further the development of the Uniswap protocol and ecosystem.

Controversy Around Governance Proposals

While the governance treasury appears on the surface to be an excellent way to decentralize protocol ownership, the community has raised concerns about the degree of decentralization and flexibility granted by Uniswap's particular governance model.

The main criticism: a minimum threshold of 1% of the total UNI supply is required in order to submit governance proposals.

Uniswap's DAO uses a delegate system via which UNI holders may delegate their voting power to a representative. As such, in order to reach 1% of the total supply, a potential representative would need to have 10 million UNI (currently worth almost $50 million) delegated to them.

The core problem with this system is that right now, only 130 million UNI tokens are in circulation - meaning that for a representative to acquire enough voting power to make a proposal, they would need to control almost 8% of all currently circulating UNI (either by holding the tokens themselves or having votes delegated to them).

As a result, despite the UNI token having been launched a week ago, not a single governance proposal has been made, standing in stark contrast with the vibrant and active communities participating in other DeFi protocols.

A further issue is that 4% of the total UNI supply (40 million tokens) is required to reach quorum (i.e. the minimum number of "yes" votes required for a proposal to pass). This represents almost 31% of all currently circulating UNI, meaning that a community-driven governance vote would be extremely difficult to pass, even if the 1% proposal threshold were met.

Potential Governance Whales

Currently, only 15 addresses control at least 10 million UNI. Of these, we can exclude several when considering the potential to create governance proposals:

- 4 addresses contain (currently locked, but gradually vesting) tokens reserved for the governance treasury.

- 1 address is the UNI token distributor contract, which contain tokens earmarked for the 400 UNI airdrop.

- 9 addresses contain part of the team and investor token allocation. As we have already noted, these tokens are technically liquid - but for reputation reasons, the Uniswap team and VCs will likely refrain from making governance proposals at this stage.

Assuming that the team and investor tokens will not be touched at this stage, only one address currently has enough liquid UNI to submit a governance proposal; the address is owned by Binance, and holds around 26 million UNI.

This means that even though the governance treasury will be unlocked in less than a month, currently only Binance - a centralized exchange in direct competition with Uniswap - has the power to propose uses for these funds. Of course, if it decided to participate at all, Binance couldn't be expected to create proposals that benefit Uniswap.

As a result, unless someone can lobby 10 million UNI worth of delegated voting power and at least 40 million votes, community-led governance is essentially impossible for the time being.

Community Governance Efforts

So how realistic is it to expect a community-led governance proposal in the near future?

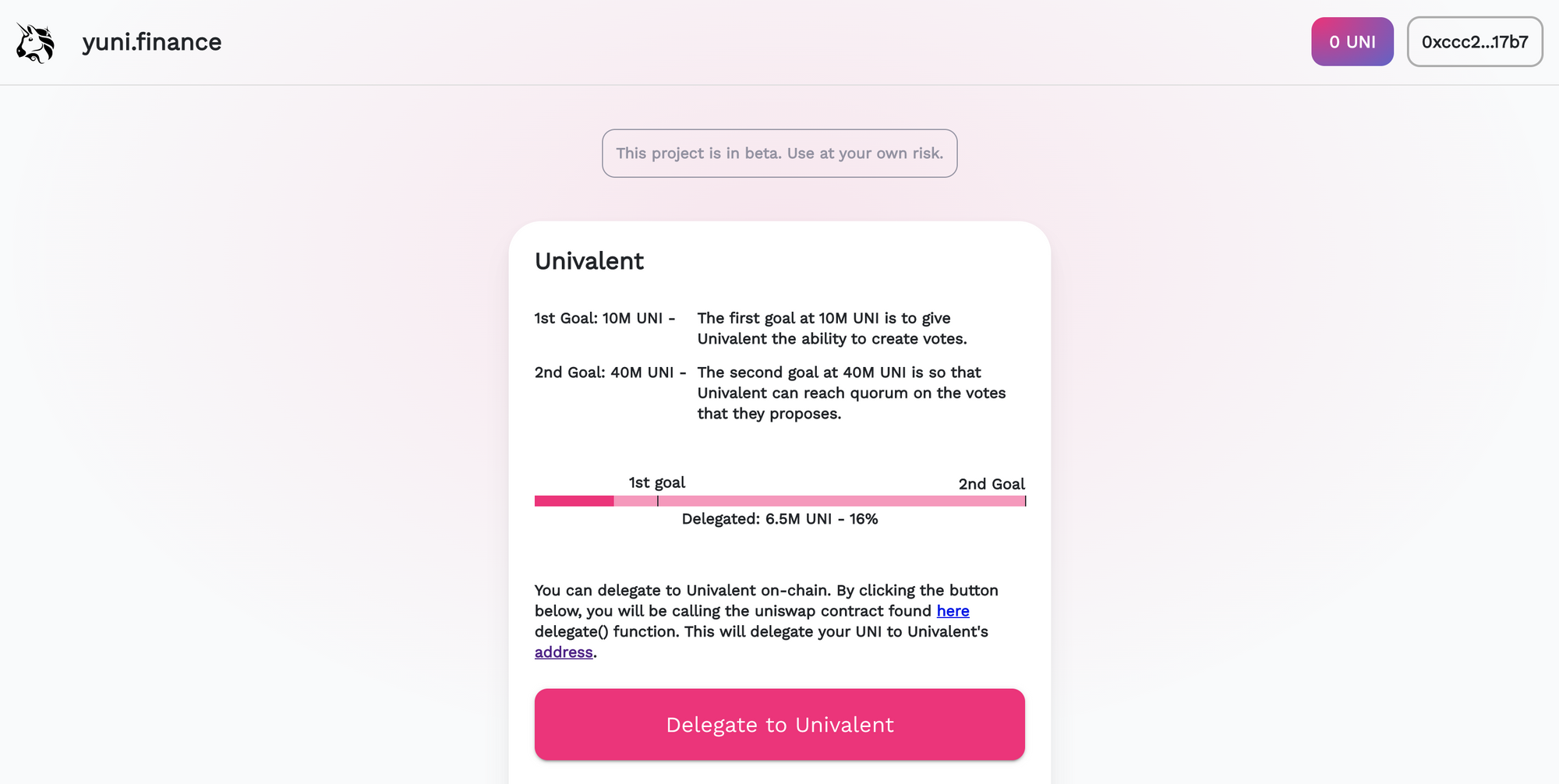

Andre Cronje, one of DeFi's most trusted buidlers and the creator of yearn.finance, is attempting to collect delegate votes through an interface called Univalent. Initially, he was not optimistic, but after five days and plenty of lobbying, he has managed to collect 6.5 million UNI worth of delegated votes.

Although Cronje appears to be making headway, the emergence of other delegate voting pools is making the goal of 10 million UNI look even more difficult, as votes are spread across multiple potential delegates.

Now I see other delegates popping up, this means even less of a chance to be able to make any proposals. So after this day, please refer to my original point.

— Andre Cronje (@AndreCronjeTech) September 19, 2020

Team and Investors can make proposals. Everyone else. Sorry.

Not only do individual UNI holders have very little voting power in comparison with Uniswap's team and investors, but community governance is made even more difficult by the issue of low voter turnout. Inevitably, many UNI holders will simply sit on their tokens rather than participating in governance. As highlighted by Vault Research:

In the case of Compound and Yearn, the voter turnout is lower than 40%. And this 40% is including the VCs’ votes. These projects are one of the most active products so expecting the same level of the voter turnout for Uniswap would be a reasonable and very conservative assumption.

Because of probable low voter turnout and the 4% quorum requirement, for the smaller community members who do participate in governance, coordinating to implement changes that meet their best interests will be orders of magnitude more difficult than it will be for the Uniswap team and VCs.

Game-Theoretic Governance Protections

This brings us to yet another issue with the UNI governance model; even if we assume that the team and investors will not use tokens that have not vested, Uniswap's team and VC investors will have a disproportionate amount of power in the early stages of governance. As such, they could vote for treasury funds to be distributed in ways that further increase their UNI token holdings, giving them even more voting power.

But while the seemingly unattainable 1% proposal threshold may seem like a power grab on the part of the Uniswap team, it is more likely that this model was implemented with benevolent intent, in order to protect the protocol from radical changes in the early stages of its transition to decentralized governance - even at the cost of community disenfranchisement.

I think it’s by design that no one can collect 10M votes and get to make proposals this early on. Presumably once the circulating supply increases further, it will be much likelier that some regular person gets enough votes. However, I agree with you it’s heavily skewed

— Larry Cermak (@lawmaster) September 20, 2020

In addition, the power wielded by the Uniswap team and investors does come with limitations. Unlike many recent DeFi protocols whose whales are anonymous profit-seeking yield farmers with no stake in the future of the project, the predominant UNI whales - specifically, the Uniswap team and investors - are publicly known and have their reputations and the protocol's success at stake.

As such, there is some protection for the wider Uniswap community, even if these entities act purely out of self-interest. While the team and investors wield immense power, they will have to balance potential gains in profit and power with the need for positive reputation and community support, especially with the potential for forks and the existence of viable competitors such as SushiSwap.

These incentives mean that the Uniswap team and VCs have an inbuilt limitation in their ability to manipulate the protocol if they wish to maintain their reputation and the value of UNI.

Protection against Governance Attack Vectors

As mentioned above, the only external address with enough tokens to unilaterally make a governance proposal is controlled by Binance, which holds almost 26 million UNI (worth over $120m) of user funds deposited on the exchange.

In theory, these funds could be used to launch an attack against Uniswap. While Binance does not currently control enough UNI tokens to meet the 4% quorum, a coordinated attack by several centralized exchanges (CEXs) is a theoretical possibility.

The current balance of UNI on exchanges is coming close to the 40 million UNI required to reach a quorum, currently standing at over 36.9 million (26 million on Binance, 9.4 million on Huobi, 1.5 million on OKEx). If these exchanges were to collude and execute an attack via a malicious governance proposal, benevolent actors would need to counteract this with a greater number of "no" votes.

As we examined above, mobilizing the community to acquire this many votes would be difficult, but Uniswap has prepared for this eventuality by keeping the team/investor token allocations liquid, despite the vesting schedule. The choice to keep these tokens fully accessible before they vest was almost certainly made in order to protect against an attack by CEXs.

2/ Tagged top 200 addresses. Most of the UNI tokens are held by the team/VC/advisors (fig 1). Even with the vesting, they have major voting power (fig 2). It means CEXs cannot attack the governance, but also means it's not governed by the community, at least for a while. pic.twitter.com/ThLfydh0K4

— Vault Research (@Vault_Research) September 21, 2020

Alternative Security Methods

While many would consider this a necessary sacrifice to protect Uniswap against these kinds of attacks, allowing the team to have de facto admin rights over the protocol could also be seen as an unnecessarily strong approach which fundamentally opposes the protocol's ethos. It is especially problematic given the existence of other strategies to prevent attacks:

- Quadratic voting - This approach is well-tested in production and has been successfully implemented by many other protocols. If correctly applied, it would minimize the power of whales, and would be a much more reasonable approach than giving the Uniswap team a unilateral governing stake. To integrate sybil resistance (i.e. to avoid a situation where exchanges split their holdings across many wallets) and give the community time to mobilize against an attack, the protocol could bar users from voting if their UNI tokens were held in a known CEX address within the past week.

- Emergency migration contract - A potential backup plan could be a mechanism allowing stakeholders to vote to move all liquidity to a new Uniswap fork in the event of a malicious governance proposal. To avoid misuse, it could require a quorum of both UNI holders and Uniswap LPs, such that it would only be used if it benefitted a broad representation of the protocol's stakeholders.

The existence of these and other potential security solutions makes the Uniswap team's decision to maintain a controlling stake concerning. Even though it would be against the team and investors' best interests to make unilateral changes to the protocol using their disproportionate voting power, the fact that it is technically feasible is still worrisome.

Is Uniswap's Decision Justifiable?

Despite concerns, there are definitely some valid justifications for the Uniswap team's decision to maintain control over non-vested tokens.

First, although there are alternative security solutions, these would require time to implement and would need to be tested and audited. Uniswap was working with a short timeline in the wake of the SushiSwap saga, and would have wanted to launch the UNI token as quickly as possible. Now that it has been released and Uniswap is dominating the market once again, the team has the opportunity to spend more time preparing the network for full decentralization.

Second, as Vitalik has previously noted, a gradual path to decentralization is often the safest and most pragmatic one for early-stage projects.

The optimal governance structure for early-stage projects is founder dictatorship.

— vitalik.eth (@VitalikButerin) August 22, 2020

The optimal governance structure for mature projects has large user/stakeholder involvement.

"Exit to community" continues to be underrated as a way to get both.https://t.co/8bnTvyytDX

While Uniswap is not necessarily "early-stage" anymore, its decentralized governance model is. As such, even though the goal should be to transcend the need for "founder dictatorship", the team likely decided that it was too early to transition to full decentralization. The protocol does seem to be moving forward on the "exit to community" path, but it is still in the earlier stages, hence the decision to maintain founder control.

Third, the Uniswap team is trusted and well-regarded within the community. Unlike SushiSwap's Chef Nomi, they are unlikely to rug-pull or panic sell. While the vesting tokens have been kept liquid as a safety precaution, the chances of these being misused (or even used at all before they vest) are extremely low. However, while the Uniswap team is highly trustworthy, the whole point of decentralized protocols is that the community shouldn't have to rely on trust.

On this note, while their decision to maintain control over non-vested tokens is justifiable, the Uniswap team did make one huge mistake: they should have been transparent about it. If they had explained their reasoning and outlined a detailed vesting schedule, the community would have accepted this. Instead, they were vague and unclear about the status of pre-vested tokens when they didn't need to be.

In an ecosystem driven by transparency and trustlessness, the team's failure to disclose the true nature of these tokens should be called into question.

Conclusions

With the launch of its UNI token, Uniswap has branded itself as "decentralized", but it still has a long way to go to reach this point. By giving itself a skeleton key to the protocol, Uniswap has (at least in the near term) sacrificed decentralization for the sake of control.

However, even though the team and investors chose to retain a controlling stake in UNI, this decision was almost certainly made with the protocol's best interests at heart, and they are unlikely to access these tokens before they vest unless the protocol is at risk of an attack. Eventually, they will be diluted by the funds from the governance treasury, and control over the protocol will gradually transition to the community.

Overall, despite the team's lack of transparency and somewhat deceptive marketing, the UNI token remains a strong and likely extremely valuable asset. Its fundamental mechanism design was clearly well thought out given the short timeline in which it was probably devised and the challenge of creating a model that the protocol's investors would approve of.

With Uniswap's impressive growth and the development of V3 in the pipeline, it is likely to continue moving ahead as one of the most valuable platforms in crypto. If the protocol's fee switch (which will enable UNI holders to earn a portion of trading fees) is activated - which it almost certainly will be - the potential for sizeable ongoing returns for UNI holders is very real.

Whether you think the protocol's approach to decentralization is pragmatic or misleading, the UNI token stands to benefit hugely from Uniswap's unceasing growth, and the protocol has a large community with a now-tangible stake in its continued success.

- Follow us and reach out on Twitter

- Join our Telegram channel

- For on–chain metrics and activity graphs, visit Glassnode Studio

- For automated alerts on core on–chain metrics and activity on exchanges, visit our Glassnode Alerts Twitter