Keeping A Firm Grip

The volume of Bitcoin supply in profit has reached the levels last was seen 2 years ago as the market came off the Nov 2021 ATH. However, the magnitude of unrealized profit held within these coins remains modest, and thus far insufficient to motivate long-term holders to lock in profits.

Executive Summary

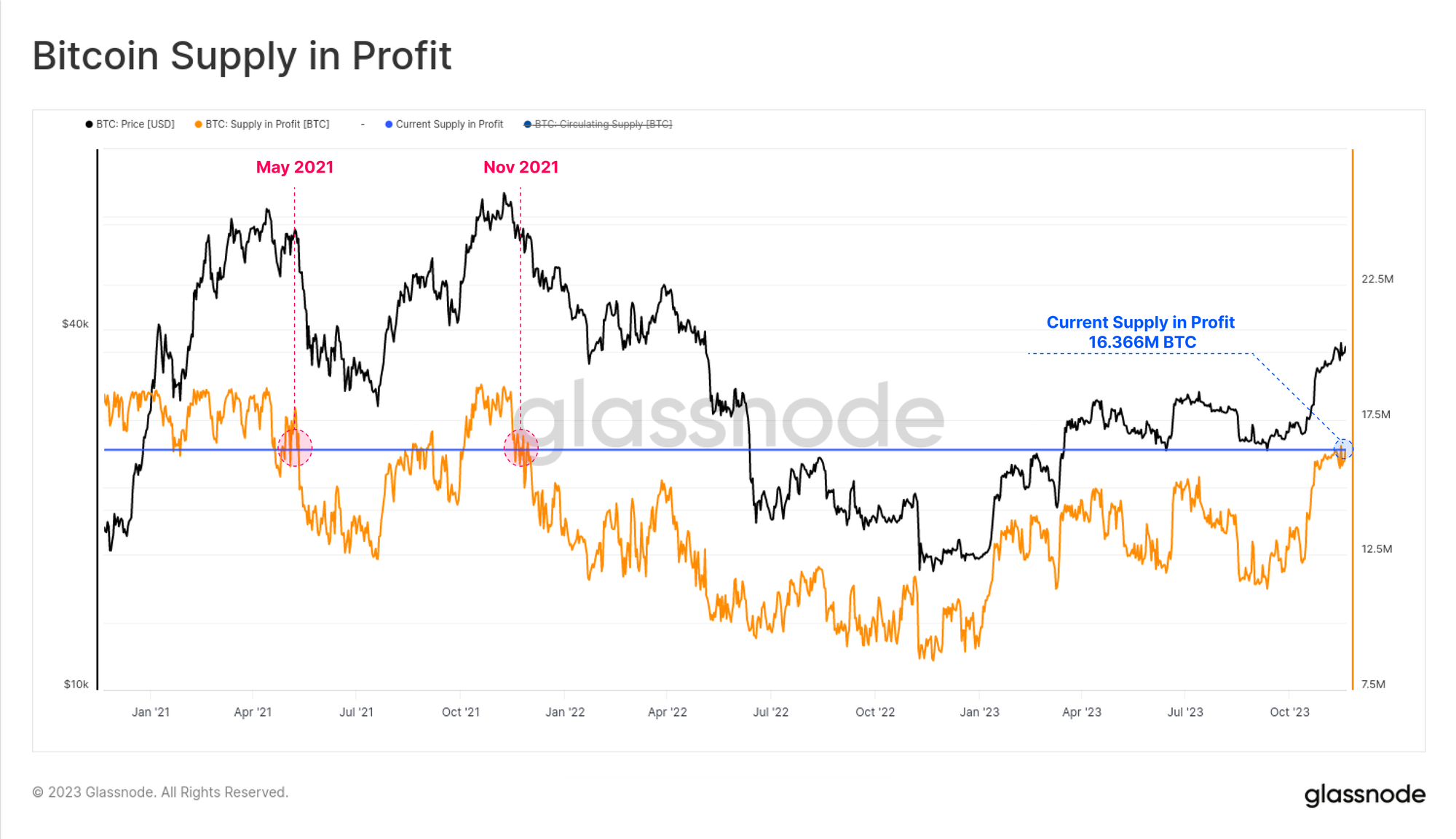

- As the market trades at yearly highs, over 83.6% of the Bitcoin coin supply are now held in profit, being the highest level since November 2021 (near the ATH).

- However, the magnitude of unrealized profit held, measured as the delta between spot price and the coins cost basis, remains modest.

- The degree of unrealized profit held by investors is thus far an insufficient incentive to motivate long-term holder to spend, keeping the overall supply relatively tight.

Bitcoin continues its strong price performance, trading near year to date highs and pushing over $37.9k this week. As a result, over 16.366M BTC are now held in profit, equivalent to 83.6% of the Circulating Supply. This puts the coin volume in profit at levels similar to the 2021 bull market highs.

In this edition, we will explore what this means for investor profitability, and how it compares to past bull market conditions.

Accumulation Across the Board

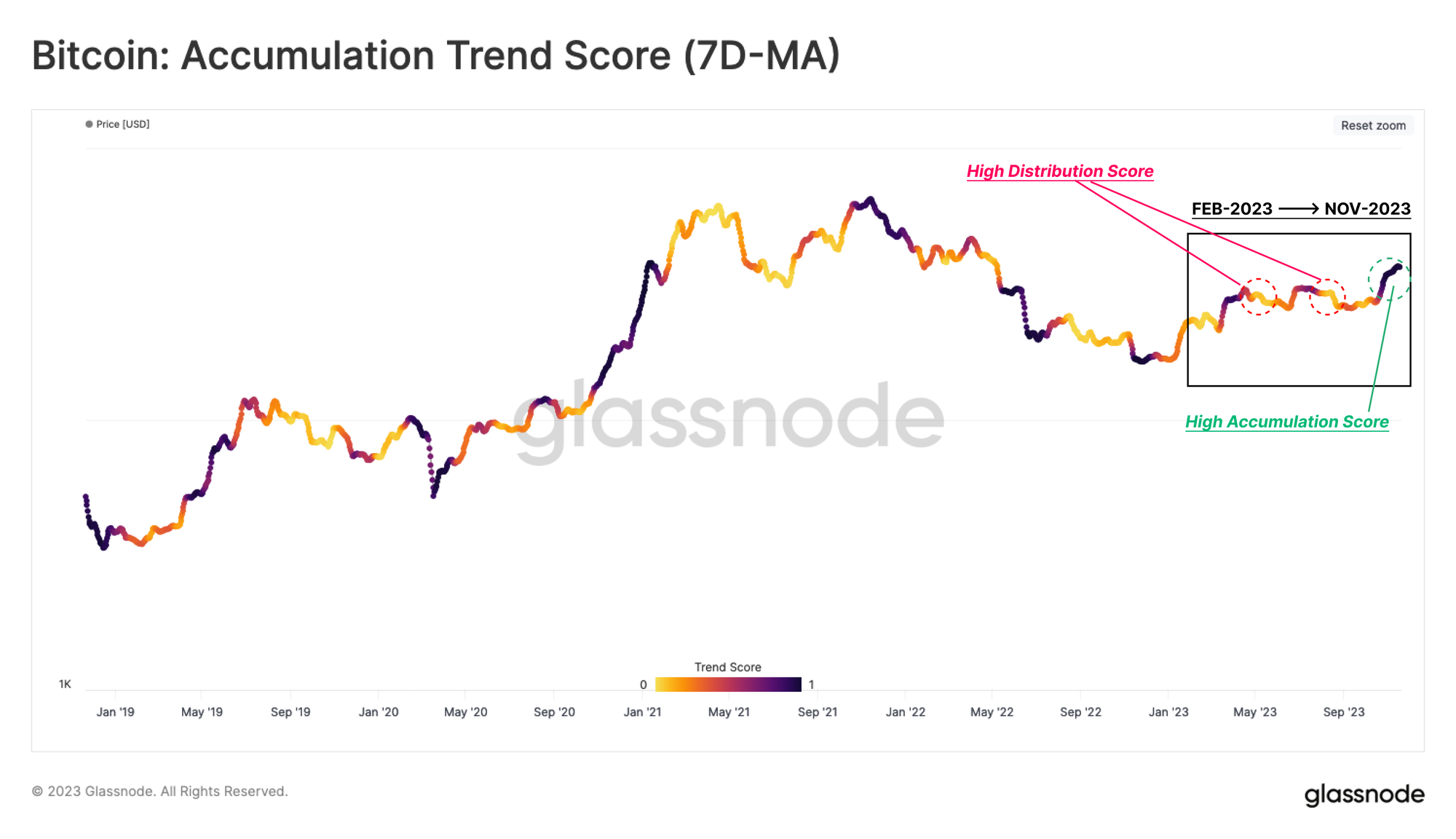

We will start with a view on investor accumulation behavior, considering the balance change of on-chain wallets. Using the Accumulation Trend Score, we can illustrate how this most recent rally is seeing greater accumulation patterns than others this year.

Unlike the first two rallies of 2023, this indicator is signalling a robust accumulation regime (dark colors) during recent price expansion, supporting the price spiking +39% over the last 30 days.

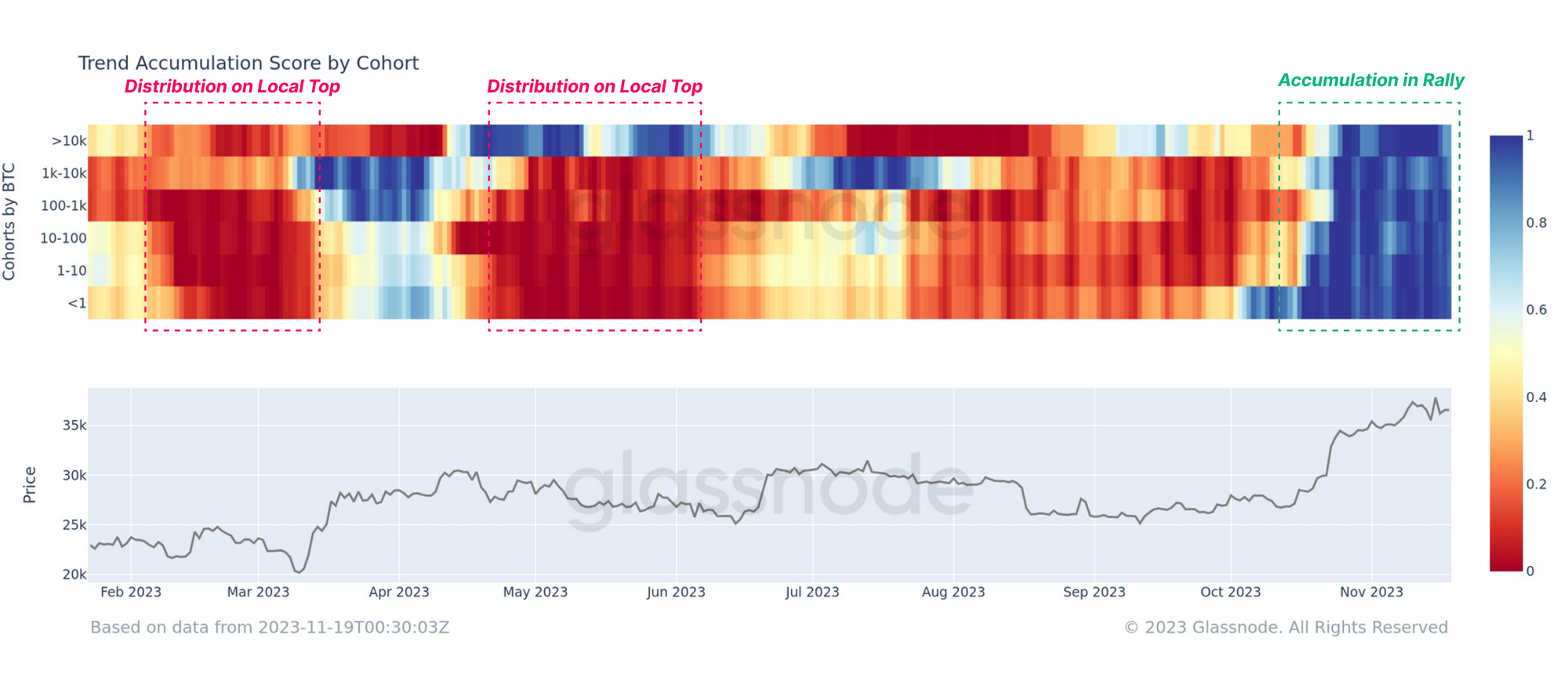

Considering different wallet sizes, a more detailed assessment can break down this accumulation score by cohorts. A distinct shift has occurred since late October, where investors of all wallet sizes have seen a substantial uptick in their holdings (denoted in 🟦).

We can see that conditions throughout 2023 have seen net outflows 🟥 across several cohorts, suggesting a non-uniform behavior by different investor cohorts. This broad uptick in accumulation means that strong market performance and increasingly optimistic hopes around a spot BTC ETF are improving investor confidence in the uptrend.

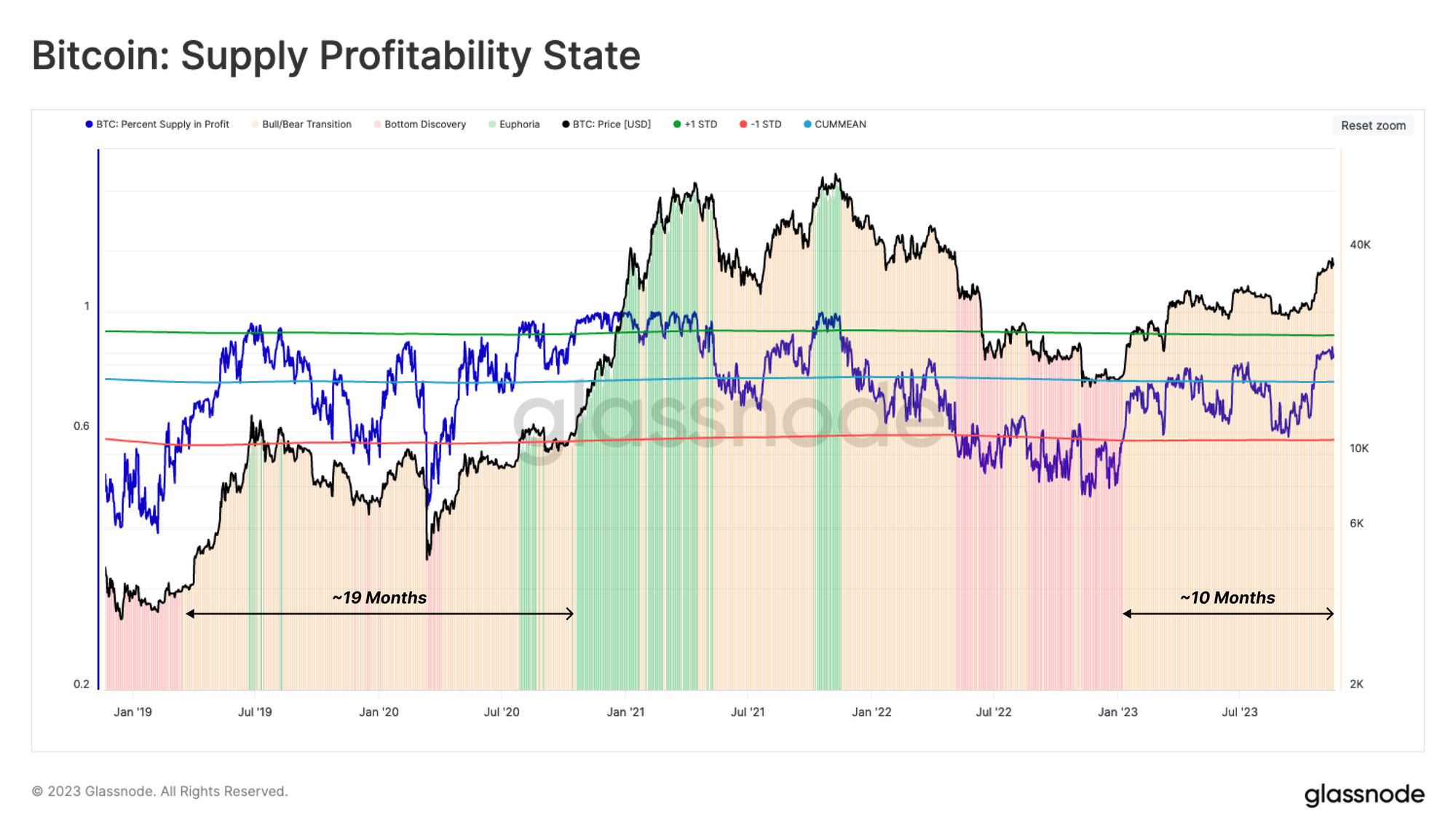

A Profitable Rally

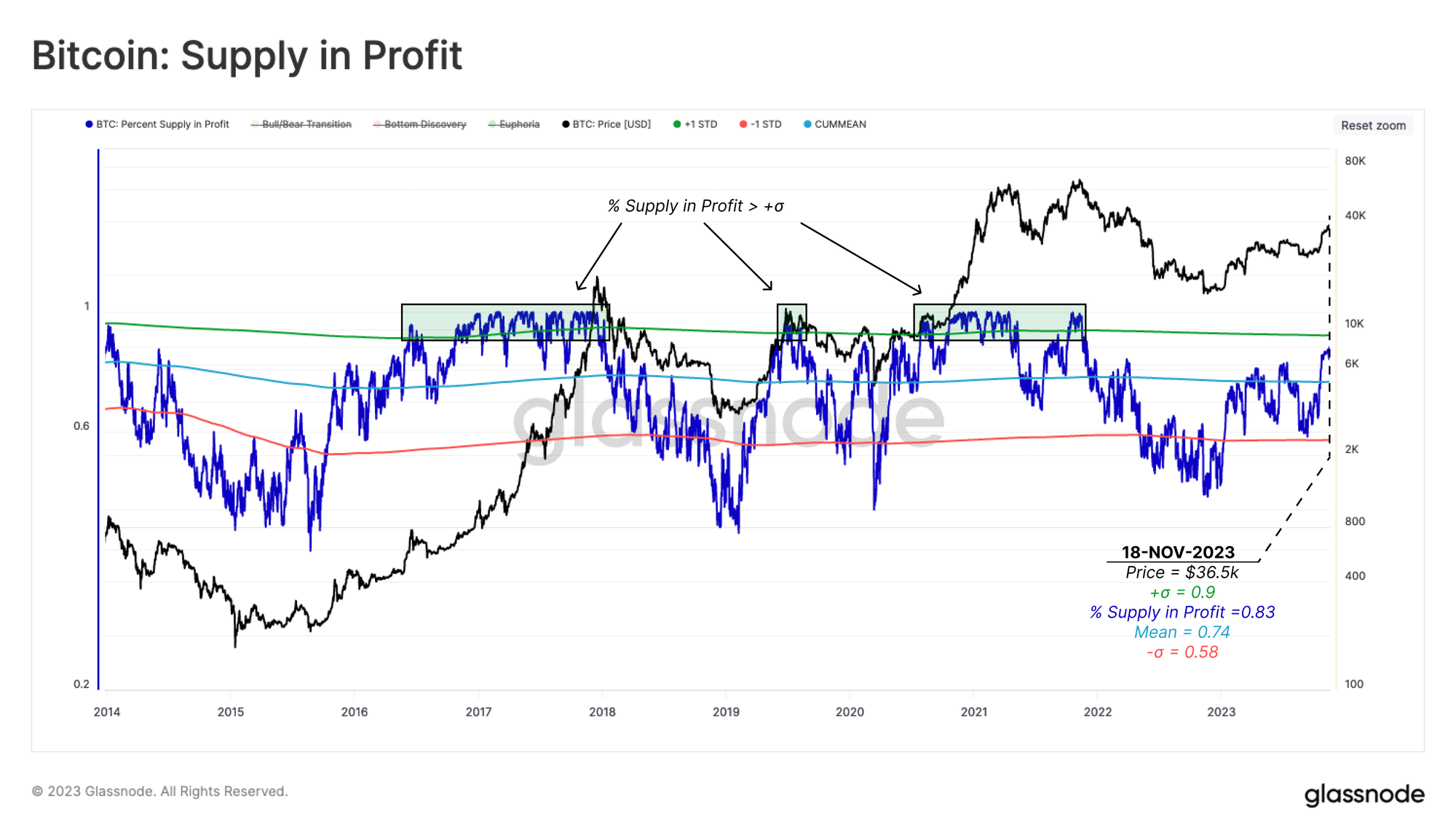

With price retesting yearly highs, the percentage of the supply held in profit has reached 83% of the total circulating supply. From a statistical standpoint, this is historically significant, being well above the all-time mean value (74%) and pushing towards the higher band of +1 standard deviation 90%.

When this indicator trades above this upper band, it has historically aligned with the market entering the early stages of a bull market's "Euphoric phase."

To put the current supply profitability into perspective, the chart below highlights three typical cycle phases over the last 5 years.

- Bottom Discovery 🟥 where less than 58% (-1 std) of circulating coins are in profit.

- Bear/Bull Transition 🟨 where the market is recovering from the Bottom Discovery phase (or falling from Euphoria) by trading within 58% of supply in profit and 90%.

- Euphoria 🟩 where most coins are in profit as the price is reaching the last ATH (+1 std).

The market has been within the Bear/Bull Transition phase for the past 10 months, as it recovered from the 2022 bear trend. The majority of 2023 has traded below the all-time average, with the October rally being the first sustained break above.

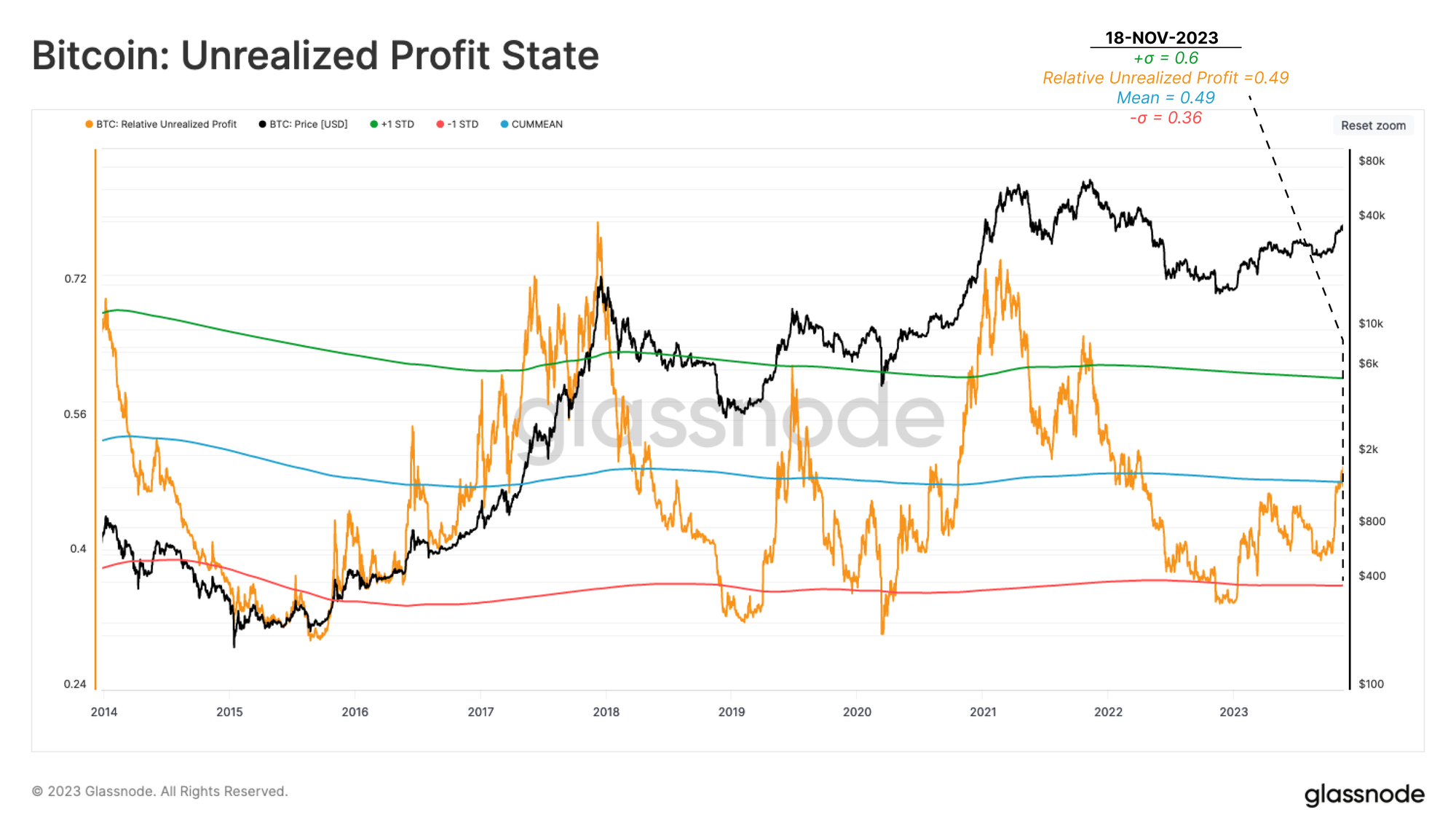

Volume vs Magnitude

It is important to note that the prior charts measured the coin volume held in profit, being coins with a cost basis lower than the spot price. This, however, is different from the magnitude of unrealized profit held, which assesses the delta between the cost basis and the current rate.

For the analysis of investor behavior, often the unrealized profit is a more critical variable as it relates back to the USD-denominated profit of investor positions.

The next chart applies the same mean and ±1 std bands to the Unrealized Profit indicator. From this, we can directly measure the magnitude of profit held by investors. This metric shows, on average, how much profit is stored in the market for every dollar worth of bitcoin.

Unlike the prior coin volume metrics, the magnitude of Unrealized Profit has not yet reached a statistically high level coincident with the heated stages of the bull market. It is currently trading at the all-time mean level of 49%, significantly lower than the extreme levels of 60%+ seen in the euphoria phase of past bull markets.

This suggests that whilst a significant volume of the supply is in profit, most have a cost basis, which is only moderately below the current spot price.

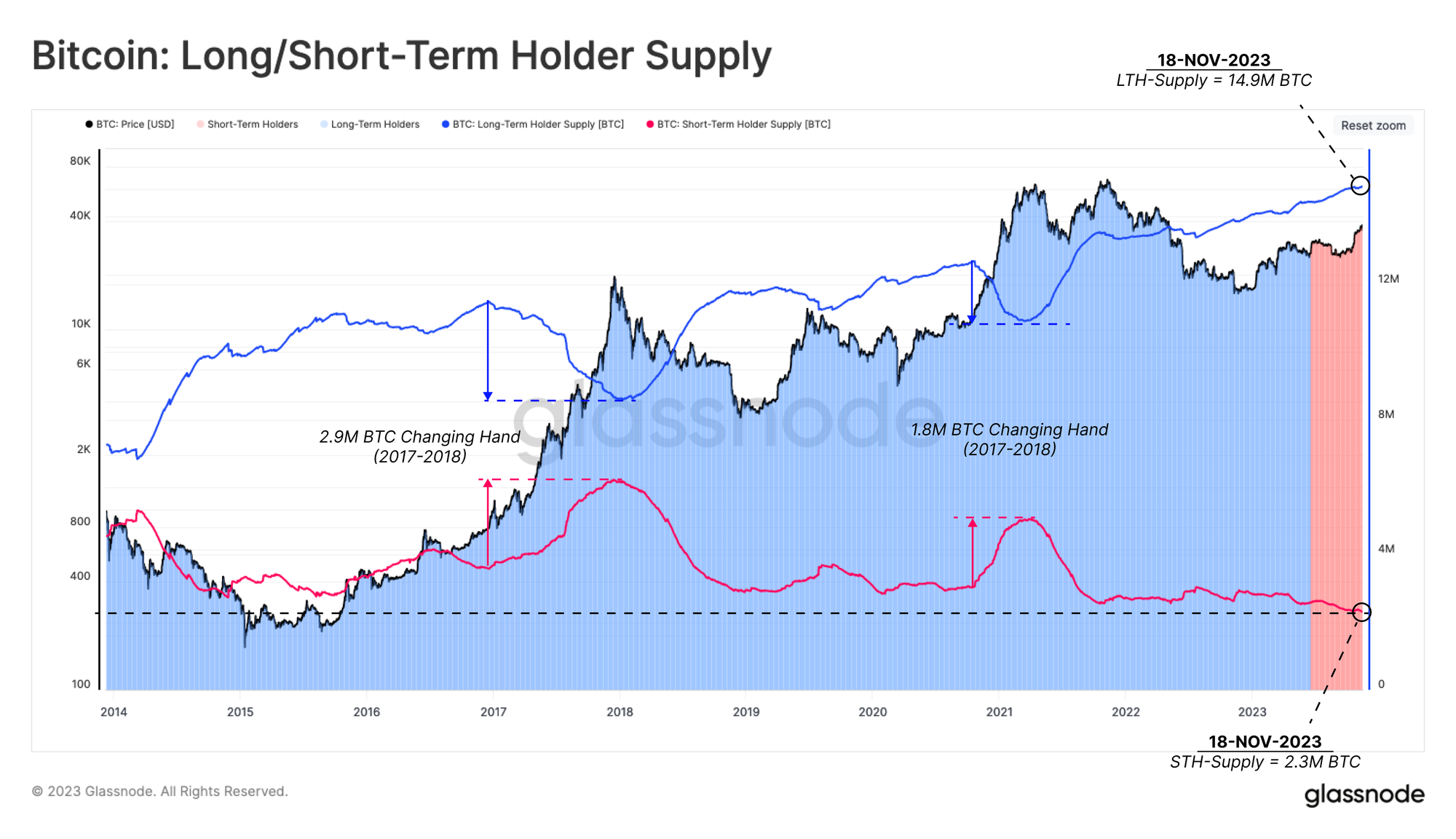

A Strong Divergence

Another remarkable phenomena is the increasing divergence between the supply held by long-term holders and short-term holders.

As discussed in WOC 45, Long-Term Holder (LTH) supply 🔵 has been continuously hitting new all-time highs since November 2022, reaching 14.9M BTC at the time of writing. Conversely, Short-Term Holder (STH) supply 🔴 has declined to 2.3M BTC, which is effectively a new all-time low.

This dynamic indicates the existing holders have become increasingly unwilling to part with their holdings, as they historically wait for the market to break to a new price ATH (see our prior report). This can be interpreted as investors requiring a higher unrealized profit (magnitude) before ramping up their distribution pressure.

The Road Ahead

We have now established that market profitability is slightly above its statistical midpoint. Next, we will explore how these tools can provide a macro blueprint of the road ahead based on prior cycles.

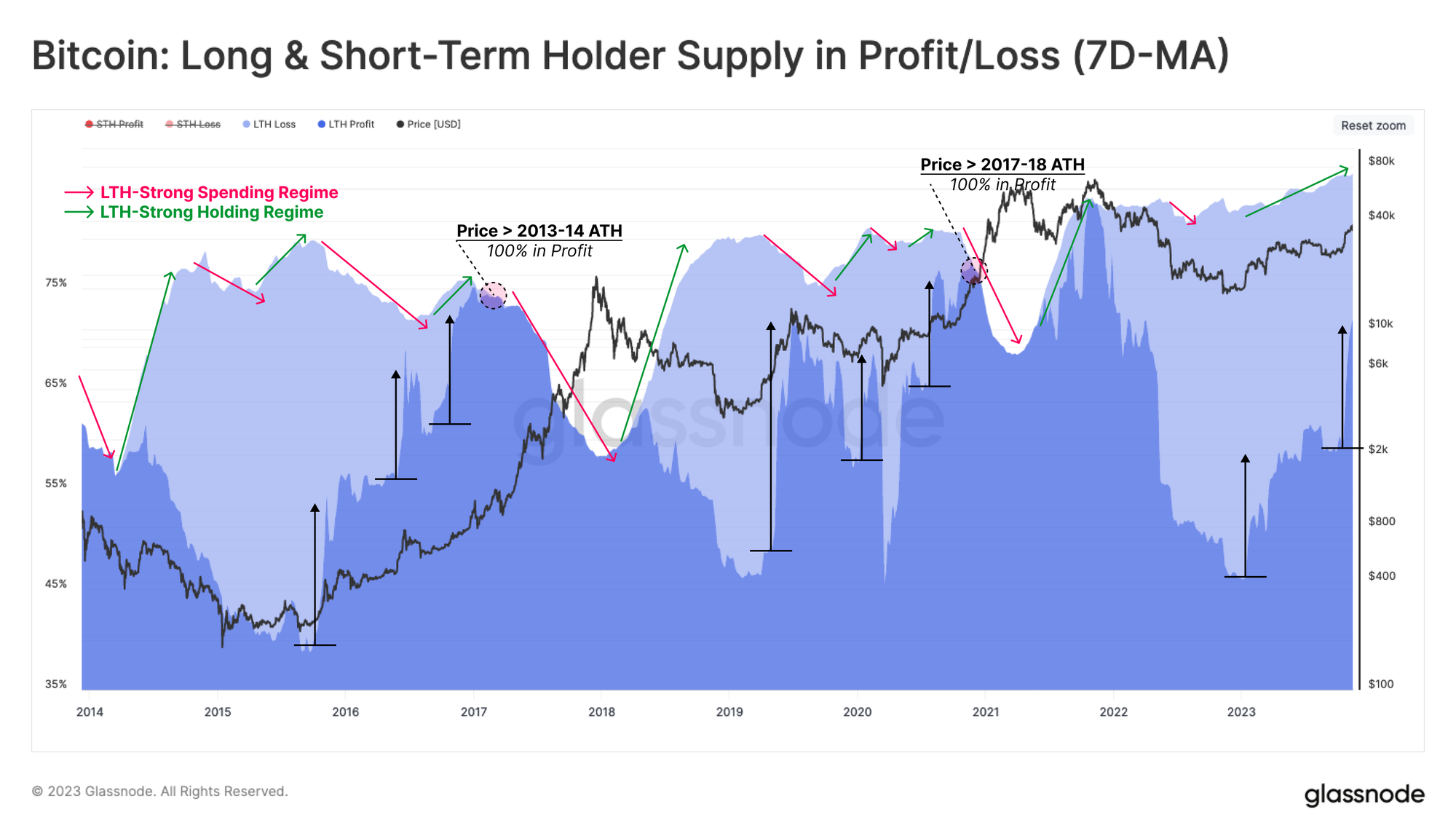

The first tool focuses on the supply held in Profit/Loss held by Long-Term Holders (LTH). We note that Long-Term Supply tends to be quite cyclical, and we have highlighted various regimes of strong spending 🔴 and strong holding 🟢 patterns on the chart below.

- Before reclaiming the ATH, LTH supply goes through a lengthy re-accumulation period, with a generally flat to modest rise in aggregate supply held.

- As the market breaks the previous cycle ATH, the incentive to ramp up spending increases significantly. This results in a dramatic decline in LTH supply, transferring coins to newer buyers at increasingly expensive prices.

Throughout the 2022 bear market, the first phase has played out very consistent with past cycles, with LTH supply climbing strongly. This shows a remarkable resilience of BTC holders, despite growing losses held by this cohort last year. However, unlike the 2015-26 and 2018-20 cycles, there have been fewer dips and oscillations due to spending, with LTH supply tending to push higher and higher. This speaks to a degree of supply tightness which we covered in WoC 45 and WoC 46.

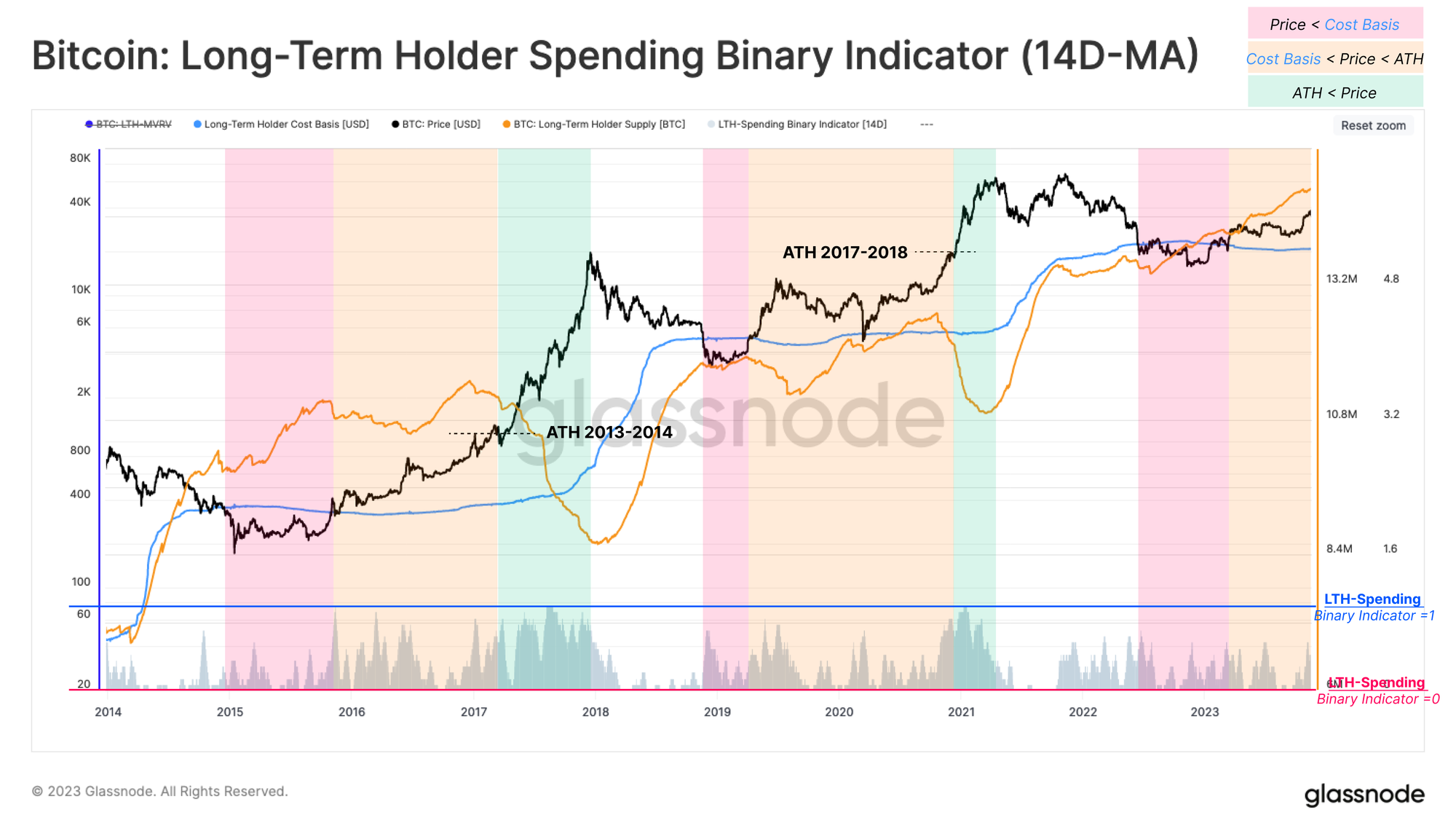

Using these observations, we revisit a compass we introduced in WoC 22, which gauges spending behavior by LTHs. This tool helps to break the long and rocky road between bear market lows and the new ATHs into three sub-intervals:

- Bottom Discovery 🟥 where price trades below the LTH Cost Basis.

- Equilibrium 🟧 where price trades above the LTH Cost Basis but below the previous ATH.

- Price Discovery 🟩 as price breaks above the last cycle ATH and LTH spending accelerates.

This Spending Binary Indicator (SBI) tracks whether LTH spending is of an intensity sufficient to decrease the total LTH Supply over a sustained 7-day period. It currently indicates very little spending is taking place by LTHs, adding further evidence to supply tightness.

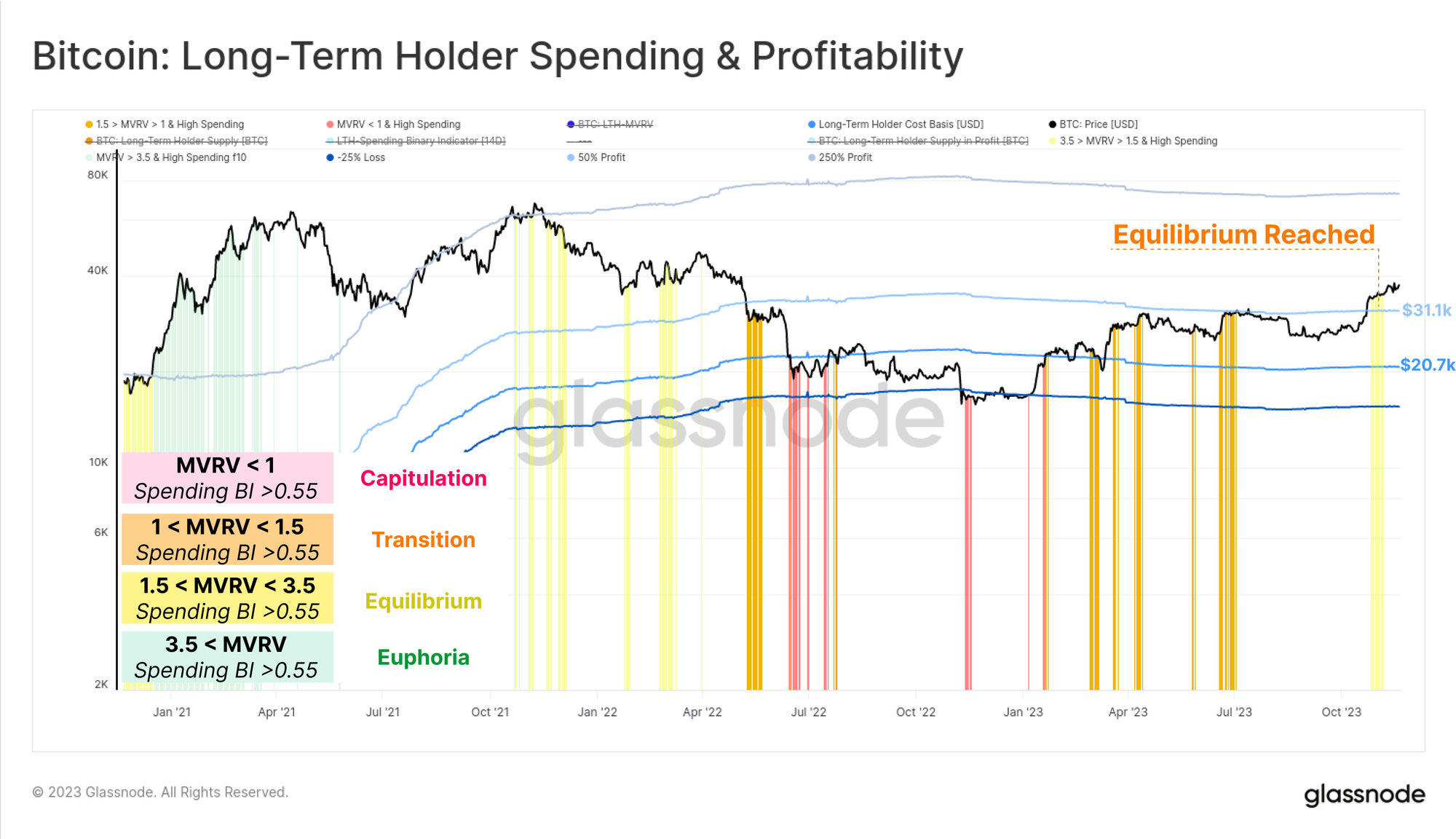

To wrap up, we can merge the SBI indicator and the relative position of the spot price, and LTH cost basis to construct a new tool for tracking market sentiment. We consider four sub-categories for spotting shifts in LTH divestment:

- Capitulation 🟥 where spot price is lower than the LTH cost basis, and therefore, any strong spending is likely due to financial pressure and capitulation (Conditions: LTH-MVRV < 1 and SBI > 0.55).

- Transition 🟧 where price trades slightly above the long-term holders' cost basis, and occasional light spending is part of day-to-day activity (Conditions: 1.0 < LTH-MVRV < 1.5 and SBI > 0.55).

- Equilibrium 🟨 after recovering from a prolonged bear, the market seeks a new balance between a light in-flow demand, lighter liquidity, and underwater holders from the previous cycle. Strong LTH spending during this stage is usually associated with sudden rallies or corrections (Conditions: 1.5 < LTH-MVRV < 3.5 and SBI > 0.55).

- Euphoria 🟩 as LTH-MVRV reaches 3.5 (historically aligned with the market hitting the prior ATH), LTHs are holding upwards of 250% profit on average. The market enters a euphoria phase, which motivates these investors to spend at very high, and accelerating rates (Conditions: LTH-MVRV > 3.5 and SBI > 0.55).

Following the recent rally above $37.1k (LTH at >50% profit), the market experienced an uptick in LTH’s spending, flagging the first intensive cash out by these players via the "Equilibrium Phase."

Conclusion

With the recent price rally, the volume of coins in profit has reached the levels that last was seen 2 years ago as the market came off the Nov 2021 ATH. However, the magnitude of unrealized profit held within these coins remains modest, and thus far insufficient to motivate long-term holders to lock in profits.

Disclaimer: This report does not provide any investment advice. All data is provided for information and educational purposes only. No investment decision shall be based on the information provided here and you are solely responsible for your own investment decisions.

Exchange balances presented are derived from Glassnode’s comprehensive database of address labels, which are amassed through both officially published exchange information and proprietary clustering algorithms. While we strive to ensure the utmost accuracy in representing exchange balances, it is important to note that these figures might not always encapsulate the entirety of an exchange’s reserves, particularly when exchanges refrain from disclosing their official addresses. We urge users to exercise caution and discretion when utilizing these metrics. Glassnode shall not be held responsible for any discrepancies or potential inaccuracies. Please read our Transparency Notice when using exchange data.

- Join our Telegram channel

- For on-chain metrics, dashboards, and alerts, visit Glassnode Studio

- For automated alerts on core on-chain metrics and activity on exchanges, visit our Glassnode Alerts Twitter