A Bear of Historic Proportions

2022 has been a tough year for Bitcoin and Ethereum, with valuations being hit hard and fast. With the extensive duration , and scale of capital destruction of the prevailing, it can reasonably be argued that 2022 is the most significant bear market in digital asset history.

Year to date, 2022 has been a historically challenging year for asset prices, with equities, bonds and digital assets alike struggling under ever tightening monetary conditions. The forces of inflation and tightening liquidity in the economy has placed extreme pressure upon the over-leveraged crypto ecosystem. Much of the recent pain is derived from highly leveraged funds, coupled with the rehypothecation of collateral coming due, both in on-chain, and off-chain venues.

In the midst of this, Bitcoin and Ethereum have both traded below their previous cycle ATHs which is a first in history. This has subsequently plunged a great proportion of the market into unrealized loss, with all 2021-22 investors now underwater. As this financial pain sets in, a growing proportion of investors are liquidating their holdings, locking in record realized losses.

In this article we will investigate the magnitude and statistical scale of capital destruction that is observable for both Bitcoin and Ether. The objective is to ascertain just how significant sell-off recent events are, and draw comparison to previous cycles as a gauge for the damage done.

Bitcoin: Drawdown and Duration

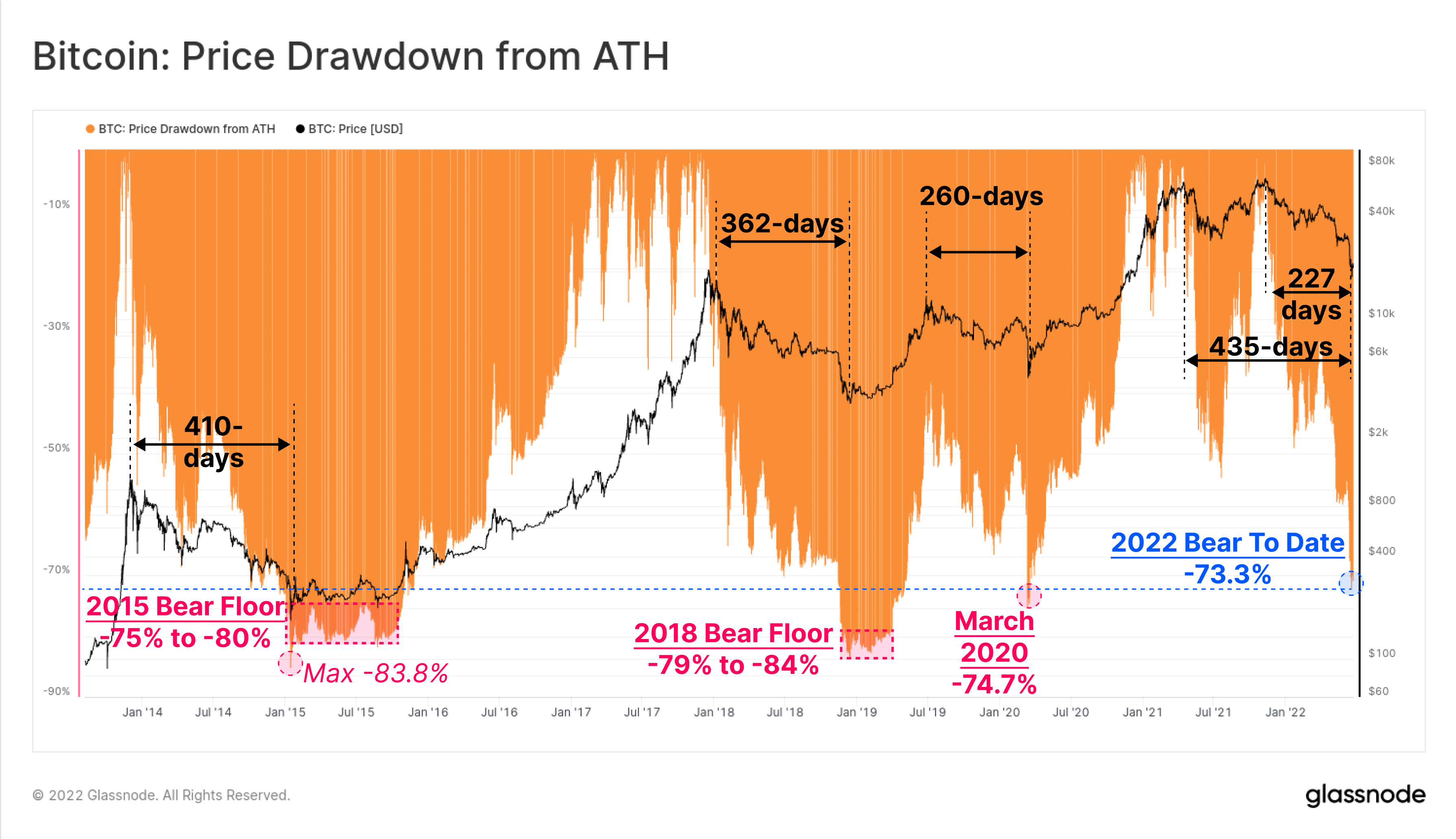

To start, we will assess the scale and duration of the present Bitcoin drawdown in comparison to the 2015. 2018 and 2019 bear cycles. We will also consider two definitions of the 2021-22 bear, one starting on the 14-April-2021 ATH, and the second the 8-Nov-2021 ATH. As we have explored previously, many signals point to the former as being most appropriate, since the May 2021 sell-off appears to be the true genesis of bear market sentiment, as a large proportion of the marginal buyer and seller were flushed from the market.

Bear market lows have historically been established with BTC drawdowns of -75% to -84% from the ATH, and taking a duration of 260-days in 2019-20, to 410-days in 2015.

With the current drawdown reaching -73.3% below the Nov-2021 ATH, and taking a duration between 227-days and 435-days, this bear market is now firmly within historical norms and magnitude.

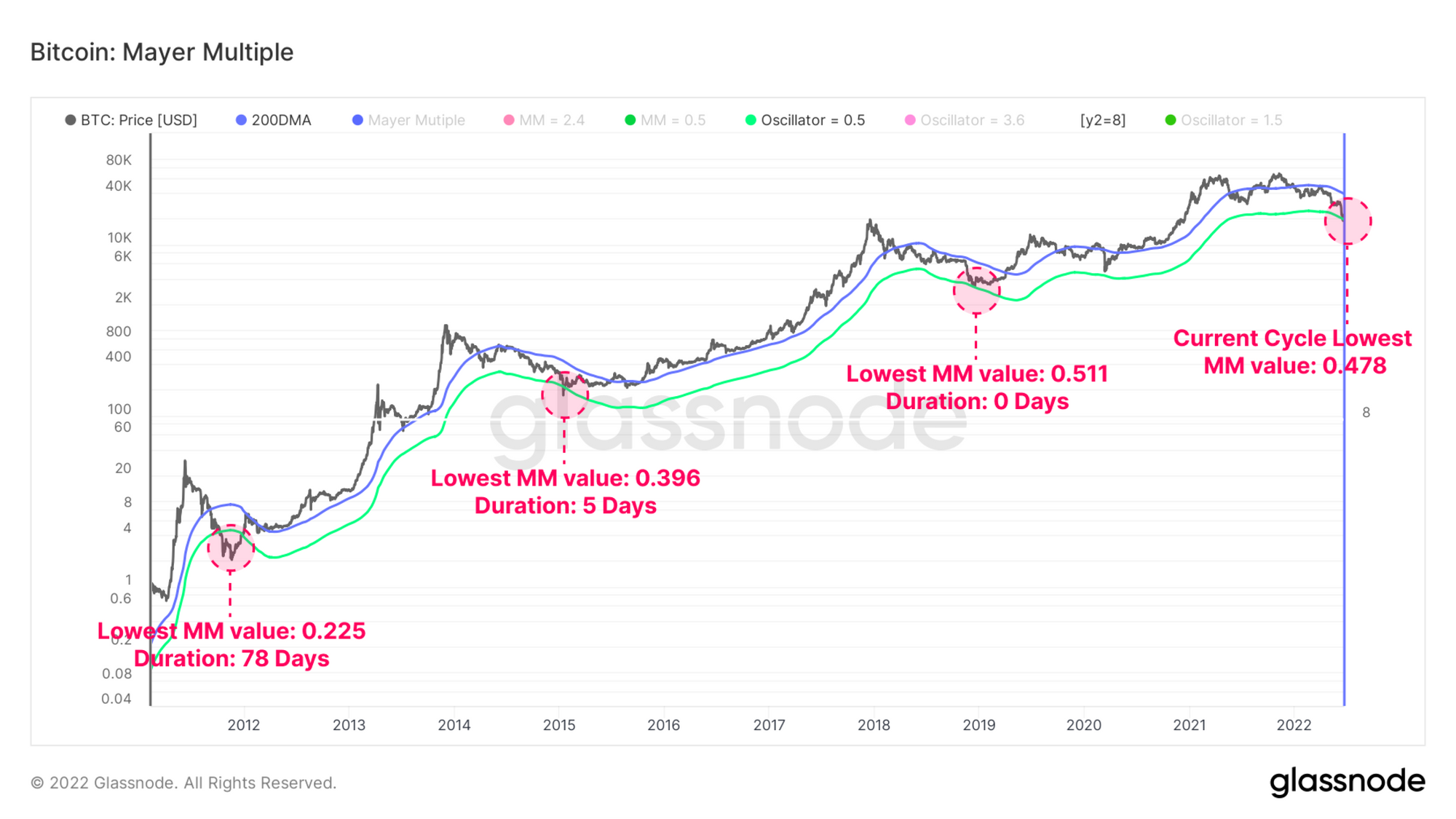

The Mayer Multiple is a metric derived from one of the most widely used indicators in Technical Analysis; the 200-day simple moving average. The 200d MA is commonly used to signal the breakpoint between a technical bull/bear market.

- When prices trade below the 200DMA, it is often considered a bear market.

- When prices trade above the 200DMA, it is often considered a bull market.

Over the years, macro-scale price action for Bitcoin has tended to abide by this framework. If we take the 200d MA as a long-term mean, the Mayer Multiple (MM) records price deviations above and below, to denote overbought or oversold conditions, respectively.

For the first time in history, the 2021-22 cycle has recorded a lower MM value (0.487) than the previous cycle's low (0.511). Only 84 out of 4160 trading days (2%) have recorded a closing MM value below 0.5. The chart below shows a price band corresponding to a MM value of 0.5 in green, and how few days have been spent below it through history.

Changes to Bitcoin’s Fundamental value

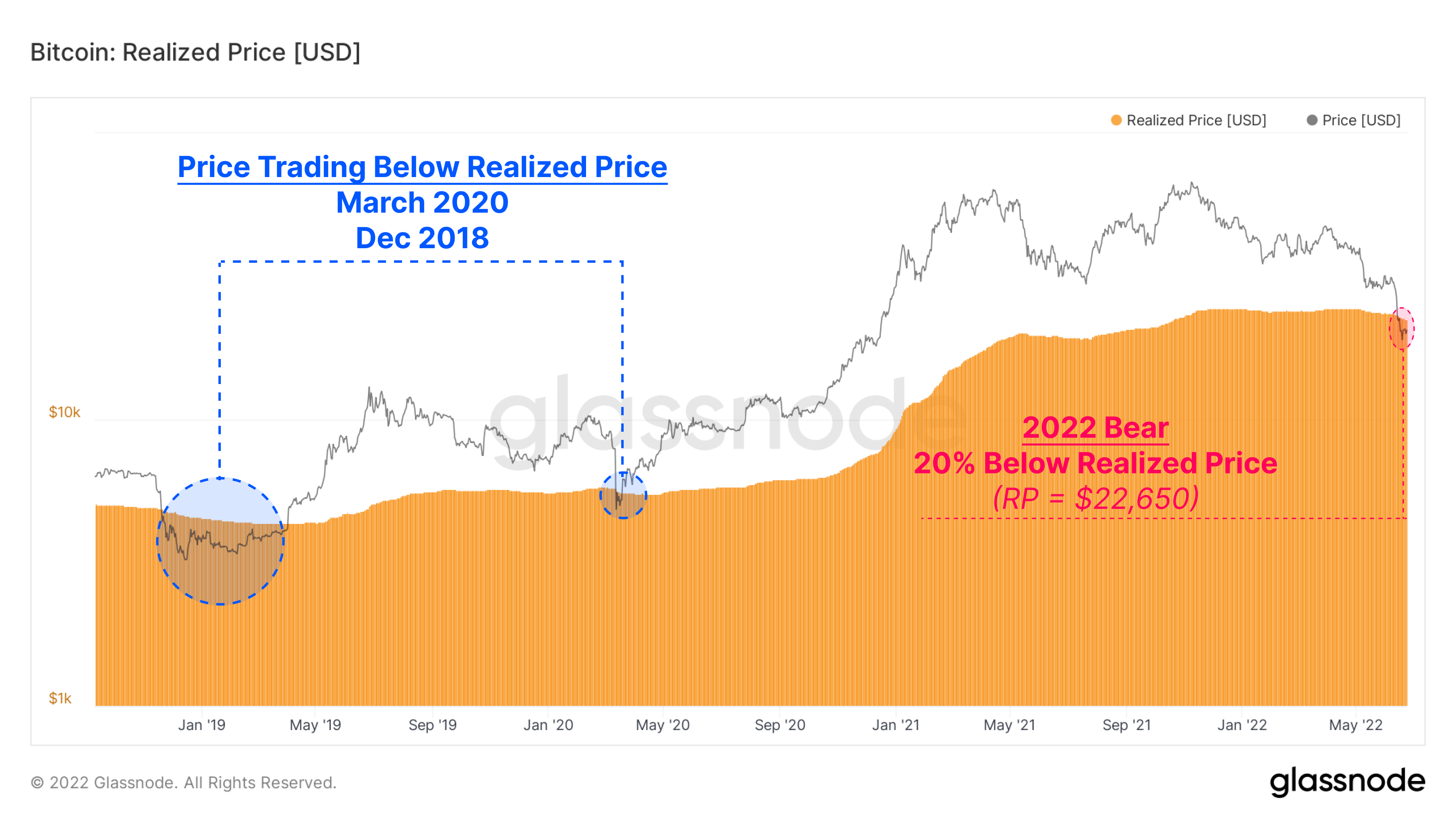

Using on-chain analysis, we can assess changes to Bitcoin’s fundamental valuation models based on actual coin holding and spending patterns. In particular, changes to the aggregate cost basis per coin, assessed via the Realized Price, can be used to gauge the extremity capital outflow and realized losses by investors.

- The Realized Price will rise as investors spend coins accumulated at cheaper prices, revaluing them higher. This is typical of bull markets and profit taking.

- The Realized Price will decline as investors spend coins accumulated at higher prices, as they realize losses and reflect a net capital outflow. This is typical of bear markets and market capitulations.

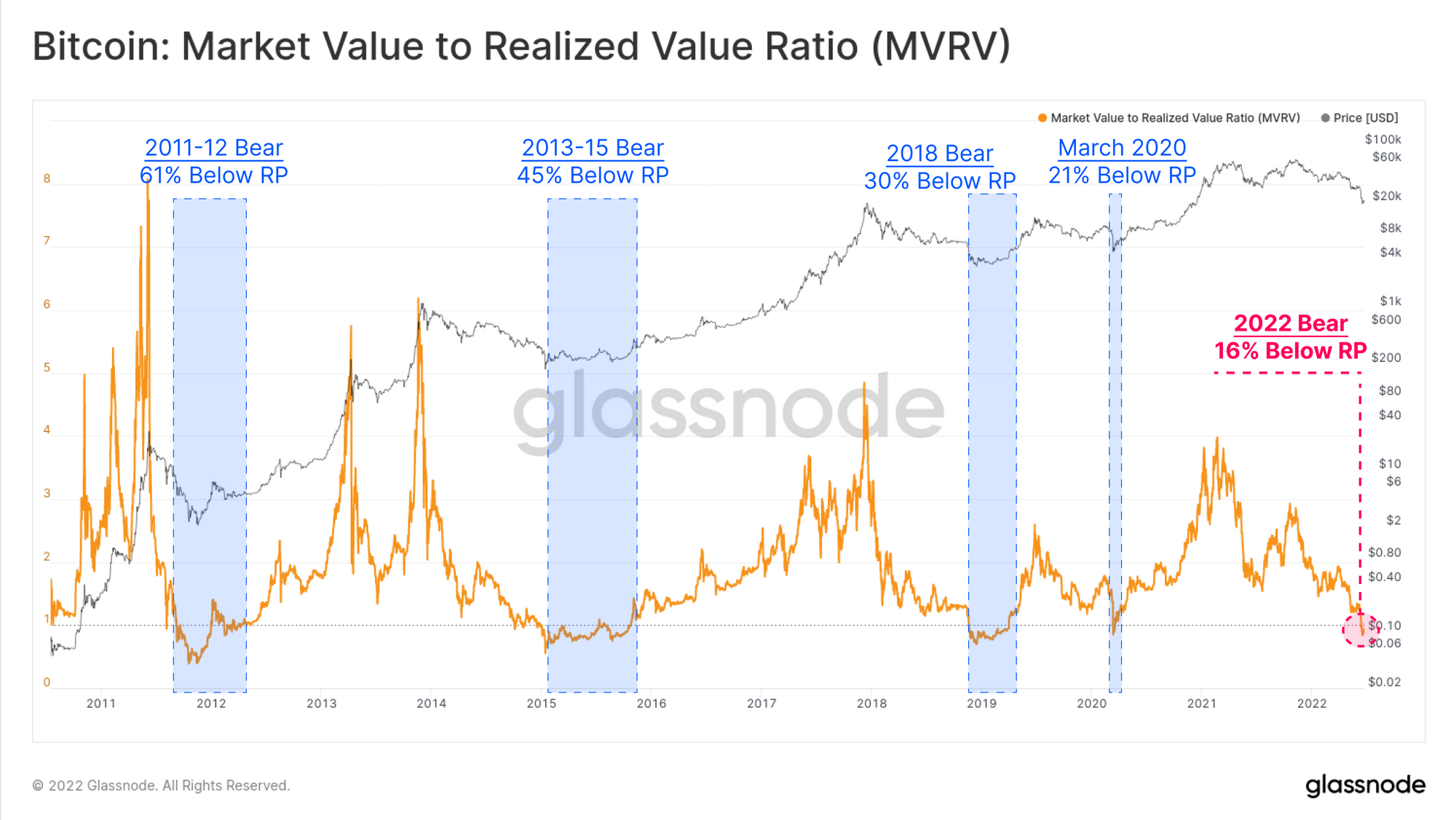

Moments, where spot prices trade under the realized price, are uncommon, with the current market being only the third time in the last six years. The last two events were the March 2020 COVID Crisis, and the Nov 2018 capitulation event, both of which put the bottom in for that bear market cycle.

Spot prices are currently trading at an 11.3% discount to the realized price, signifying that the average market participant is now underwater on their position.

We can next derive the MVRV Ratio, which is an oscillator comparing the Market Value to the Realized Value in a ratio. This allows us to visualize large deviations away from this mean.

The chart below shows blue zones where spot prices traded below realized prices. These events account for 604 out of 4160 daily closes, equivalent to just 13.9% of trading days.

The parent of the Realized Price is the Realized Cap, calculated as the summation of all coin volumes (BTC) multiplied by the price-stamp when they were last transacted. This metric provides us with a view into the intrinsic value stored within the network.

The 30 Day Position Change of the Realized Cap (Z-Score) allows us to view the relative monthly capital inflow/outflow into the BTC asset on a statistical basis. By this measure, Bitcoin is currently experiencing the largest capital outflow event in history, hitting -2.73 standard deviations (SD) from the mean. This is one whole SD larger than the next largest events, occurring at the end of the 2018 Bear Market, and again in the March 2020 sell-off.

Locking In Losses

Next, we assess the magnitude of these losses as a gauge of how network participants have responded to the years uncertainty and financial adversity.

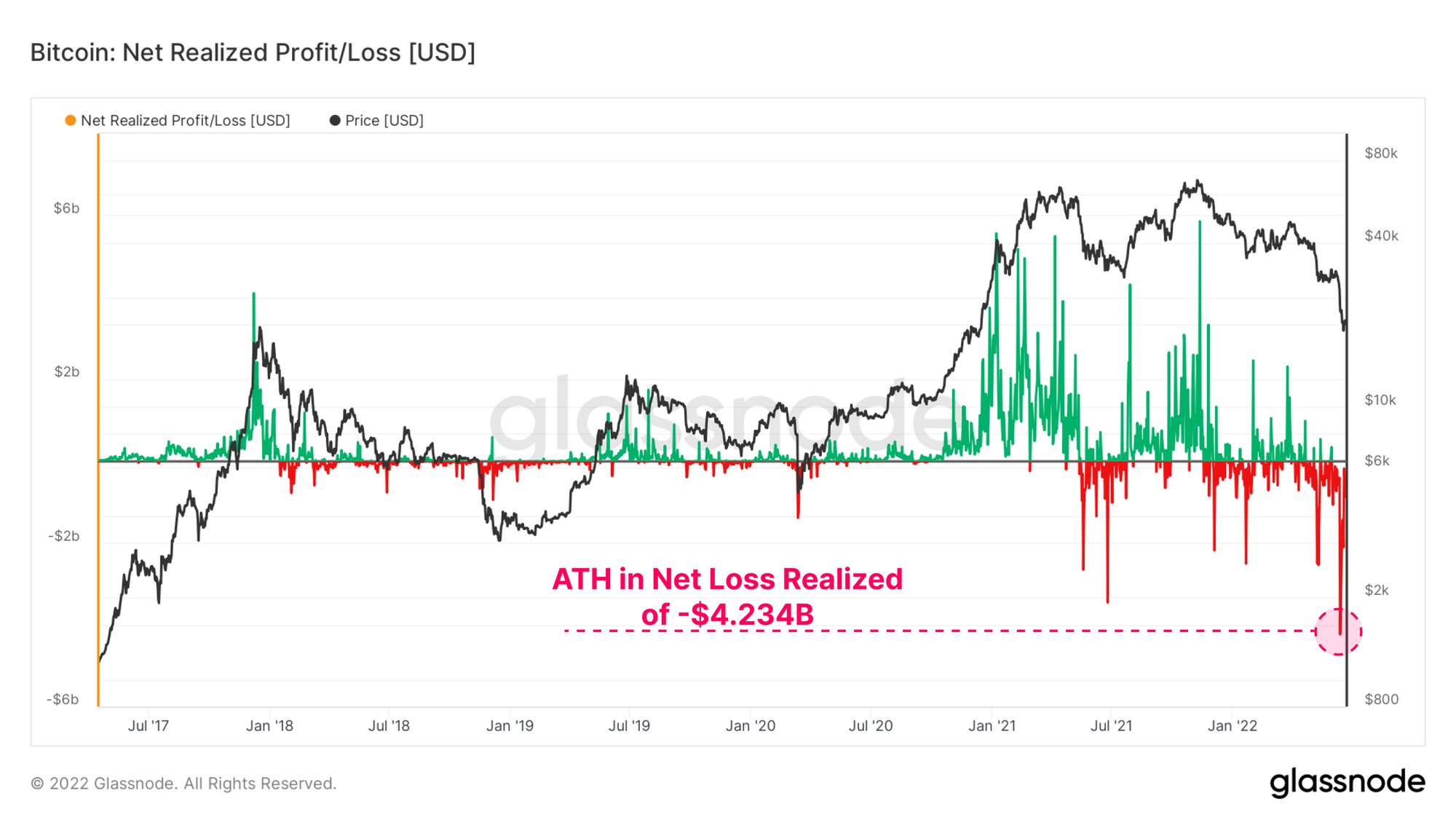

The Net Realized Profit/Loss metric captures the net capital flow regime precipitated by investors spending their coins on any given day. The recent price collapse through to the $20k region was punctuated with the largest daily USD denominated realized loss in history. Investors collectively locked in a loss of -$4.234B in a single day, which is a 22.5% increase from the previous record of $3.457B set in mid-2021.

As the Bitcoin market matures over time, the magnitude of potential USD denominated losses (or profits) will naturally scale alongside network growth. However, even on a relative basis, this does not minimize the severity of this $4+ Billion net loss.

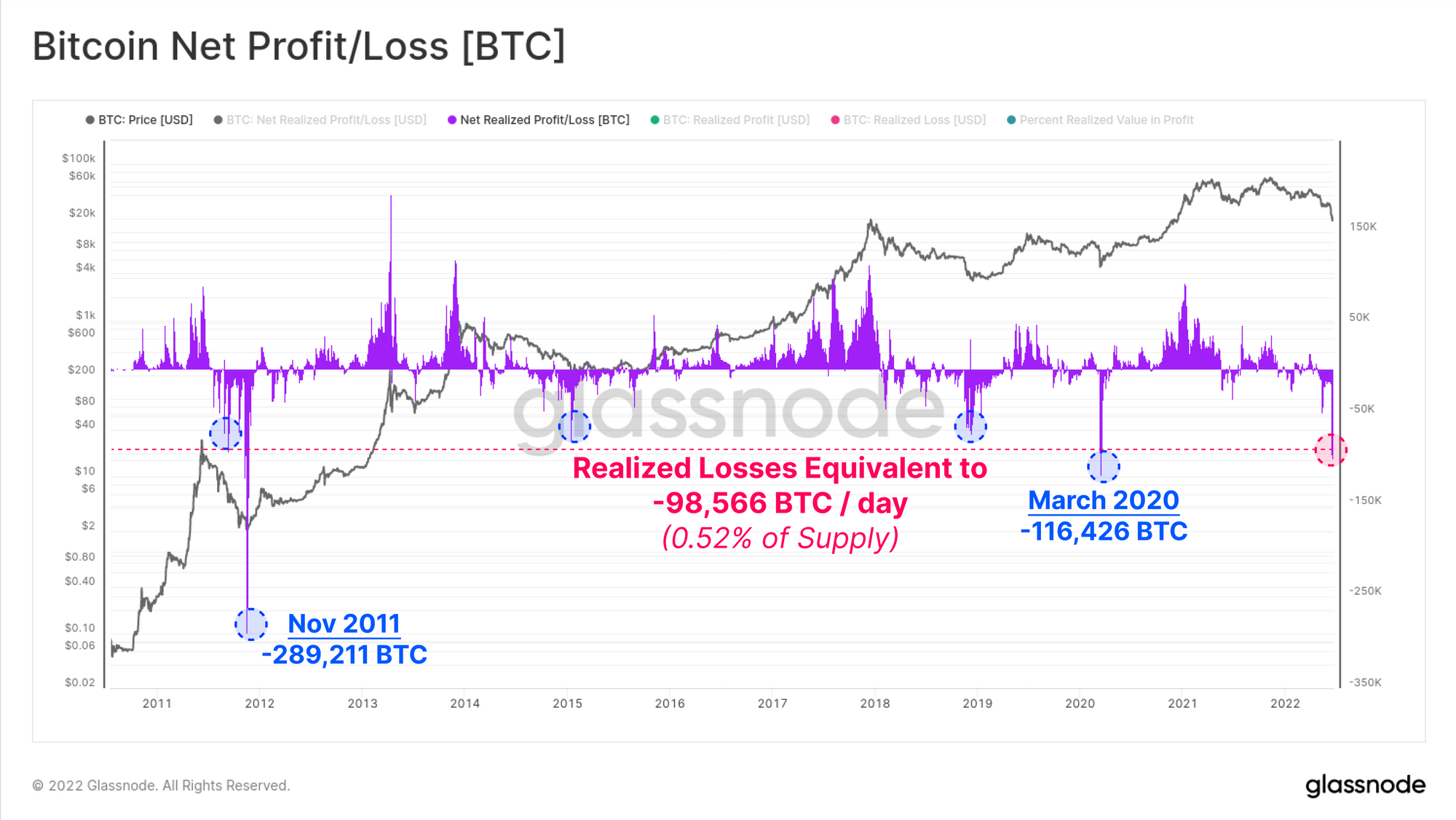

Gauging Net Realized Profit/Loss in units of BTC, which effectively normalizes for market size, the current drawdown is recording Realized Losses equivalent to -98,566 BTC per day (0.52% of the circulating supply). There have been only two recorded trading days with larger recorded Realized Losses, found in the 2011 bear market, and on March 2020.

We have now established two concepts:

- Bitcoin spot prices are trading well below the Realized Price, indicating the average market investor is underwater on their holdings.

- Actualized spending behaviors have precipitated extraordinary and historically significant net losses.

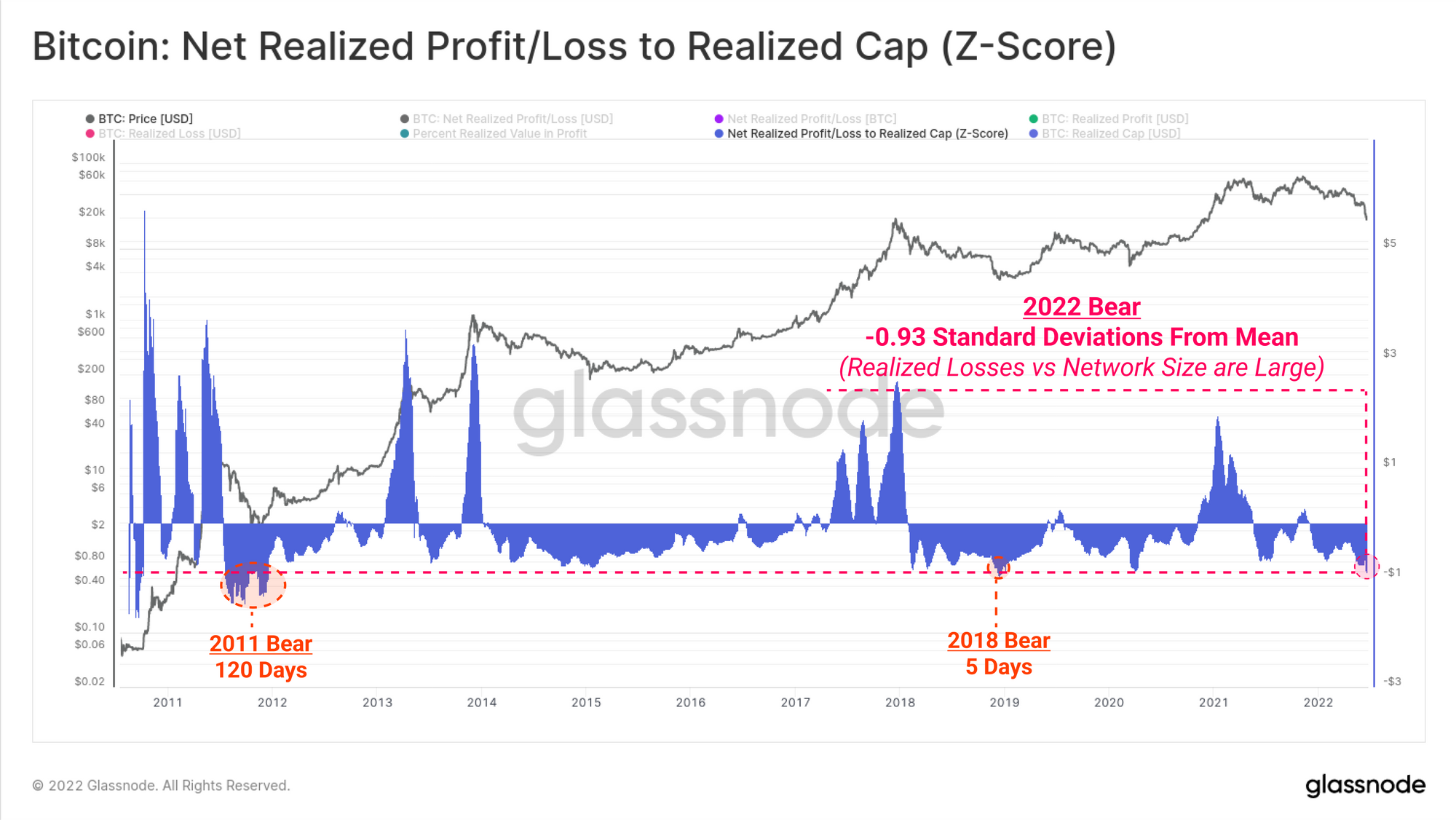

Following this, we can take a ratio between the actual spending, and the Realized Cap. This effectively captures a normalized view of capital inflows and outflows relative to market size.

The current reading indicates a negative deviation from the mean of -0.93 SD. Only 150-days have closed at a lower value, reflecting just 3.86% of Bitcoin’s trading history. This adds further evidence to quantify just how severe the 2022 bear has been.

Finally, we will assess the ratio between Transfer Volume in Loss against Transfer Volume in Profit on monthly average basis. Transfer Volume is simply the volume of coins moved on-chain in any given day.

The LUNA motivated crash in May 2022 saw the Volume in Loss-to-Profit ratio reach a 2.3x multiple. This indicates that 2.3x more volume in loss was transacted in comparison to volume in profit. Historically, such one sided transaction markets are uncommon, and with such a sharp percentage of volume in distress, it speaks to a significant investor capitulation event taking place.

To summarise the 2021-22 Bitcoin bear market (so far), we have the following statistics and observations:

- Prices have drawndown -73.3% below the ATH, which is coincident with the upper bound of previous bear market lows.

- Top-to-bottom duration is between 227 and 435-days, depending on where the bear market is determined to have commenced.

- Deviation below the 200-day MA is so large, that only 2% of trading days have been worse off.

- The market has seen the largest monthly decline of the Realized Cap in history on a statistical basis.

- This is supported by spending behavior which has locked in both absolkute and relative losses that are so large, that only 3.5% of trading days have seen larger capital outflows.

- The ratio between Transfer Volume in Loss vs Profit has reached historically high levels, synonymous with a deeply distressed investor base.

We can now conclusively claim that the 2021-22 Bitcoin bear market is one of, if not the most significant in history, both in its severity, depth, and magnitude of capital outflow and losses realized by investors.

The State of Ethereum

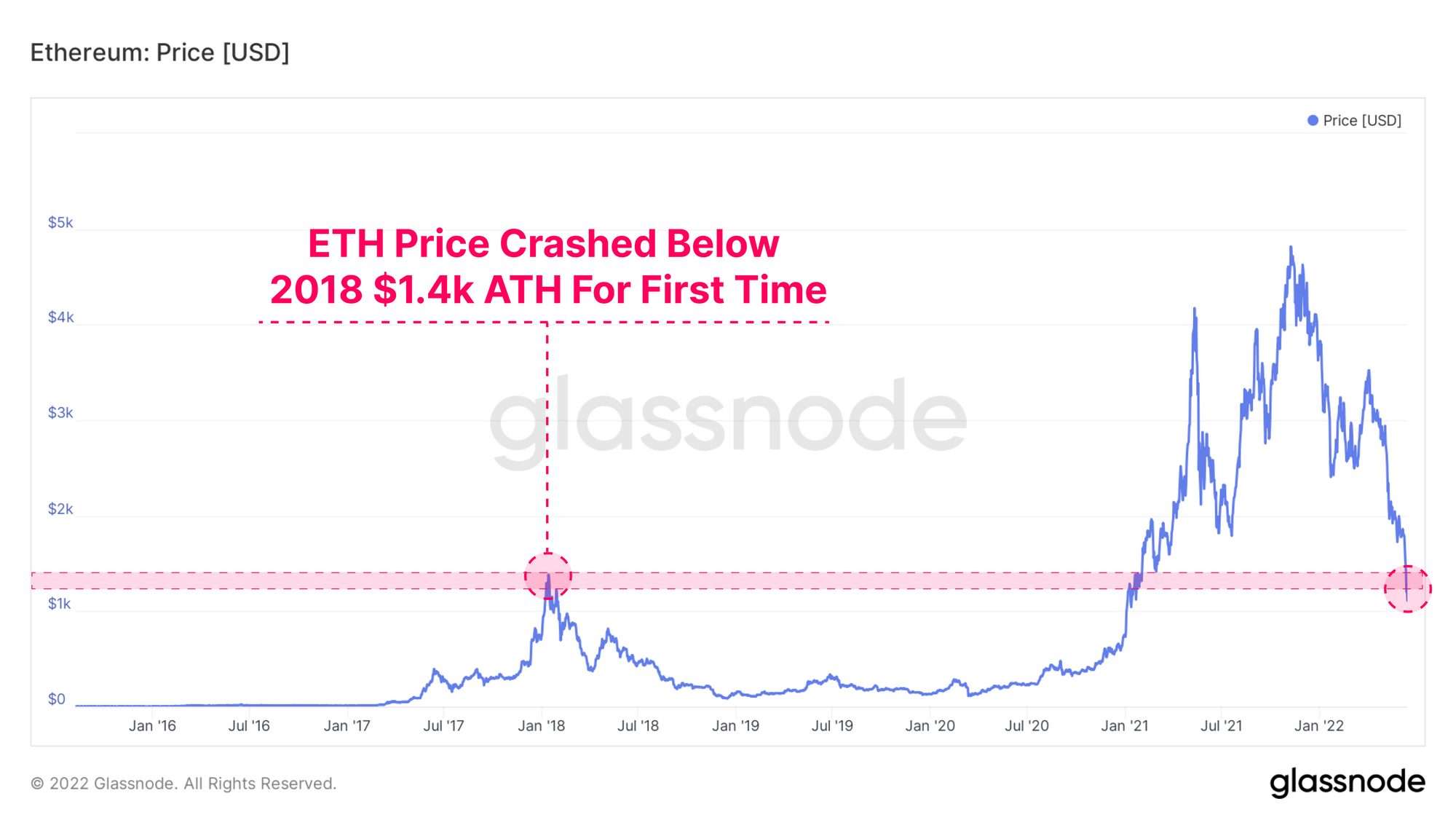

The price of the second largest digital asset, Ether (ETH) is hardly unscathed, having also retraced below the 2018 cycle ATH of $1.4k. With both the major digital assets trading below lasy cycles ATH, we can swiftly dispel any tropes about ATHs providing an ‘impenetrable’ support level.

Like Bitcoin, all investors who purchased Ethereum in 2021-22 are now currently all holding an unrealized loss. As we discussed in our recent research piece, a great proportion of this downside was driven by a large scale deleveraging in the DeFi ecosystem.

Comparing the rate of change of the Ethereum Market Cap against the Bitcoin allows us to compare the relative performance and dominance of the two major assets.

- A Bitcoin Dominant regime (high values) is indicative of BTC dominance, and an uptrend indicates general capital rotation in favour of BTC.

- An Ethereum Dominant regime (low values) is indicative of ETH dominance, and a downtrend indicates general capital rotation in favour of ETH, which is often accompanied by out-performance further out on the digital asset risk curve.

Ethereum Dominance has been in notable decline since the Nov 2021 ATH, and is close to the inflection point which has historically preceded a longer-term period of Bitcoin out-performance. This highlights the aggregate state of general risk-off sentiment in the market, where ETH under-performs BTC, and both tend to under-perform the US Dollar.

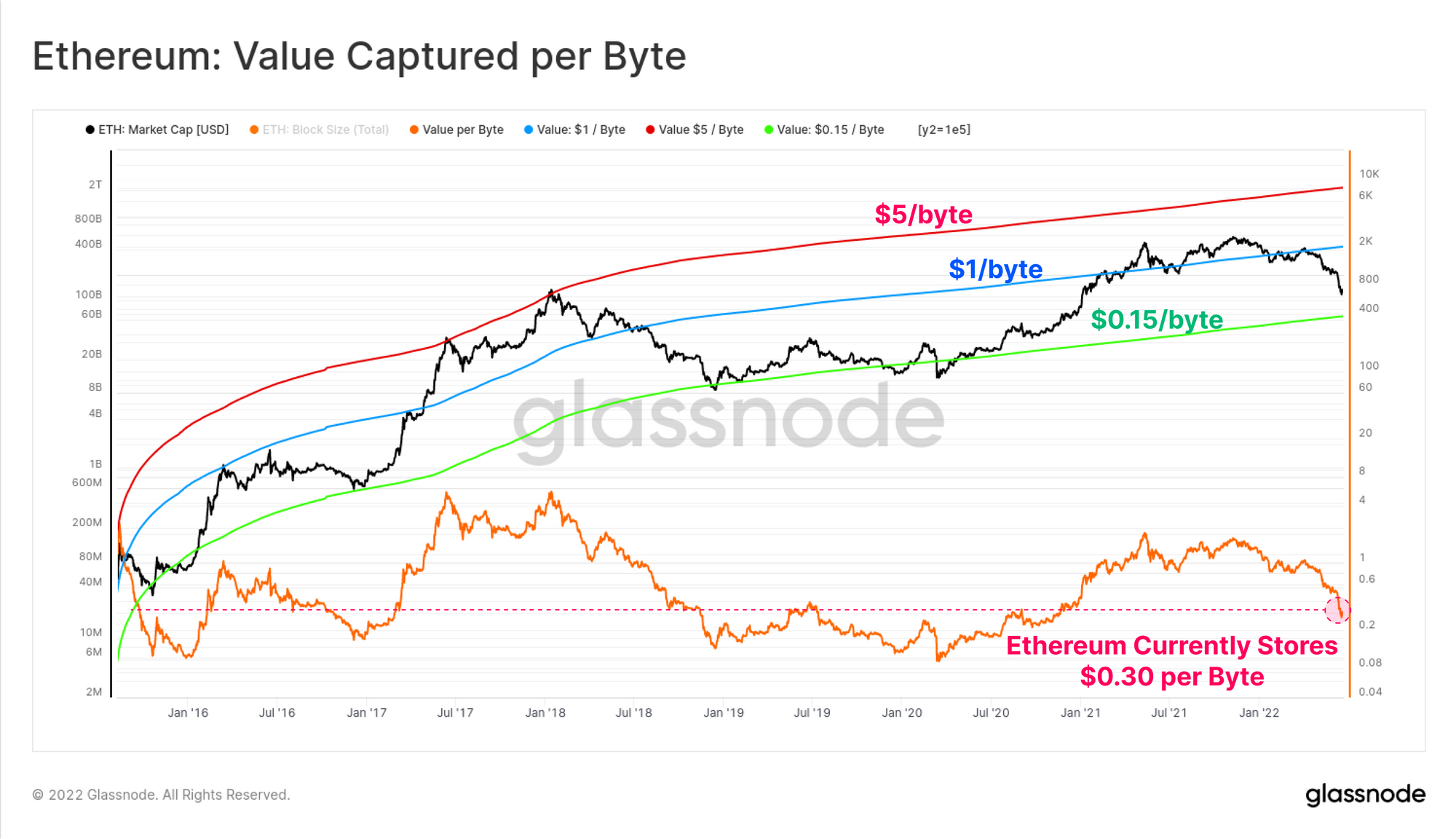

An interesting metric that was first proposed by Permabull Nino describes the value captured by Ethereum per blockchain byte. As the leading smart contract platform, and hosting a vibrant application ecosystem, it follows that the value captured per byte of data stored should theoretically increase with improving network effects (and vice-versa).

Ethereum is currently storing $0.30 per byte. This is just 2x higher than the lower bound of $0.15/byte which has historically coincided with late stage bear markets, and market lows. Unfortunately, this does suggest that a further -50% decline is possible if history were to repeat. This however assumes no fundamental improvement in value capture by the Ethereum network. DeFi, NFTs and much of the modern infrastructure did not exist in 2018.

ETH is also trading well below the 200-day Moving Average, with the Mayer Multiple hitting 0.37. This signifies that at the recent lows, ETH was trading at a 63% discount to the 200DMA. Just 1.4% of trading days ever seen larger downside deviations.

The Mayer Multiple band of 0.6 represents a level of downside deviation with approximately 10% of all ETH trading days being below it. In the 2018 bear market, ETH spent 187-days below this band during the worst of the price action. In the current market, ETH has traded below this band since early June, and has now been below it for 29-days.

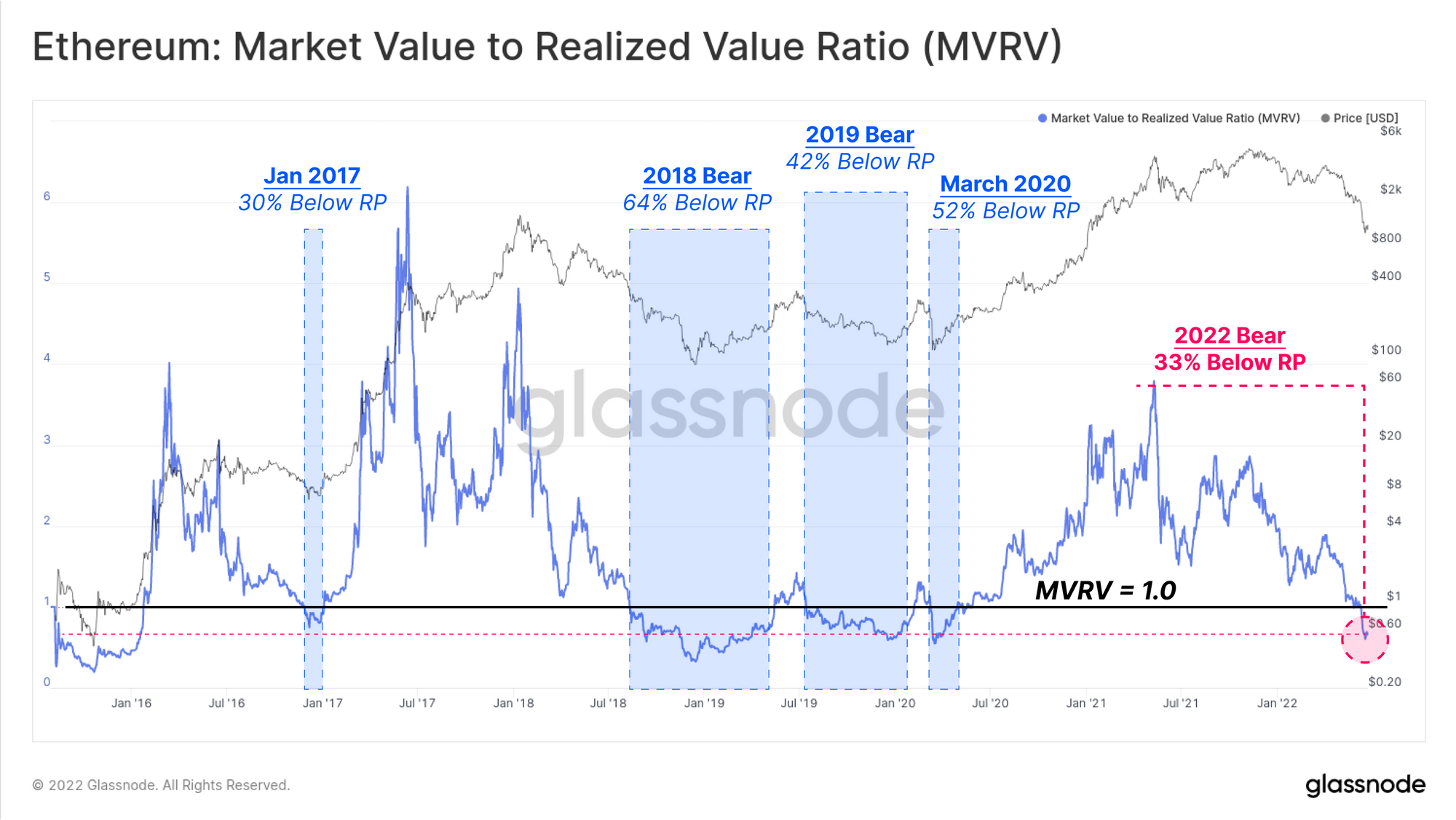

We can now implement a framework similar to the one we used for Bitcoin, to assess the Etheruem Realized Cap, and thus compare the scale of the Bitcoin and Ethereum bear markets. The Ethereum MVRV Ratio is now reaching negative deviations well below equilibrium, currently signalling that the market is holding an aggregate -33% unrealized loss.

Ethereum prices have spent 37.5% of its trading life in a similar regime under the Realized Price, a stark comparison to Bitcoin at 13.9%. This is likely a reflection of the historical out-performance of BTC during bear markets as investors pull capital higher up the risk curve, leading to longer periods of ETH trading below investor cost bases.

The current cycle low of the MVRV is 0.60, with only 277 days in history recording a lower value, equivalent to 11% of trading history.

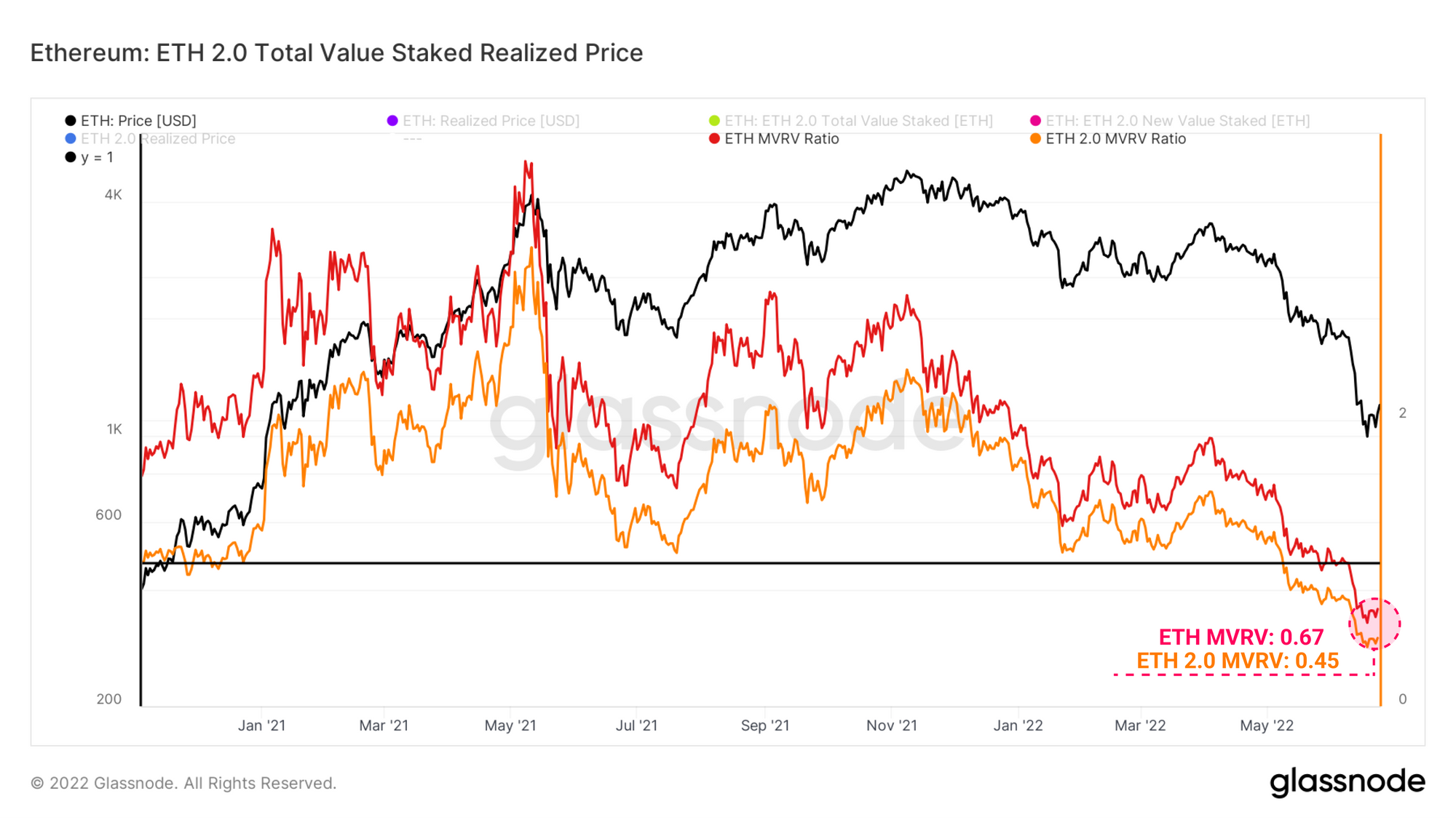

The MVRV Ratio for ETH 2.0 deposits can also be calculated based on the price-stamp when the deposits were made. Comparatively, the average price per staked ETH is $2.4k, which is more than twice the current spot price. This puts ETH 2.0 Stakers at an aggregate -55% unrealized loss, which is -22% worse performance compared to the average ETH investor.

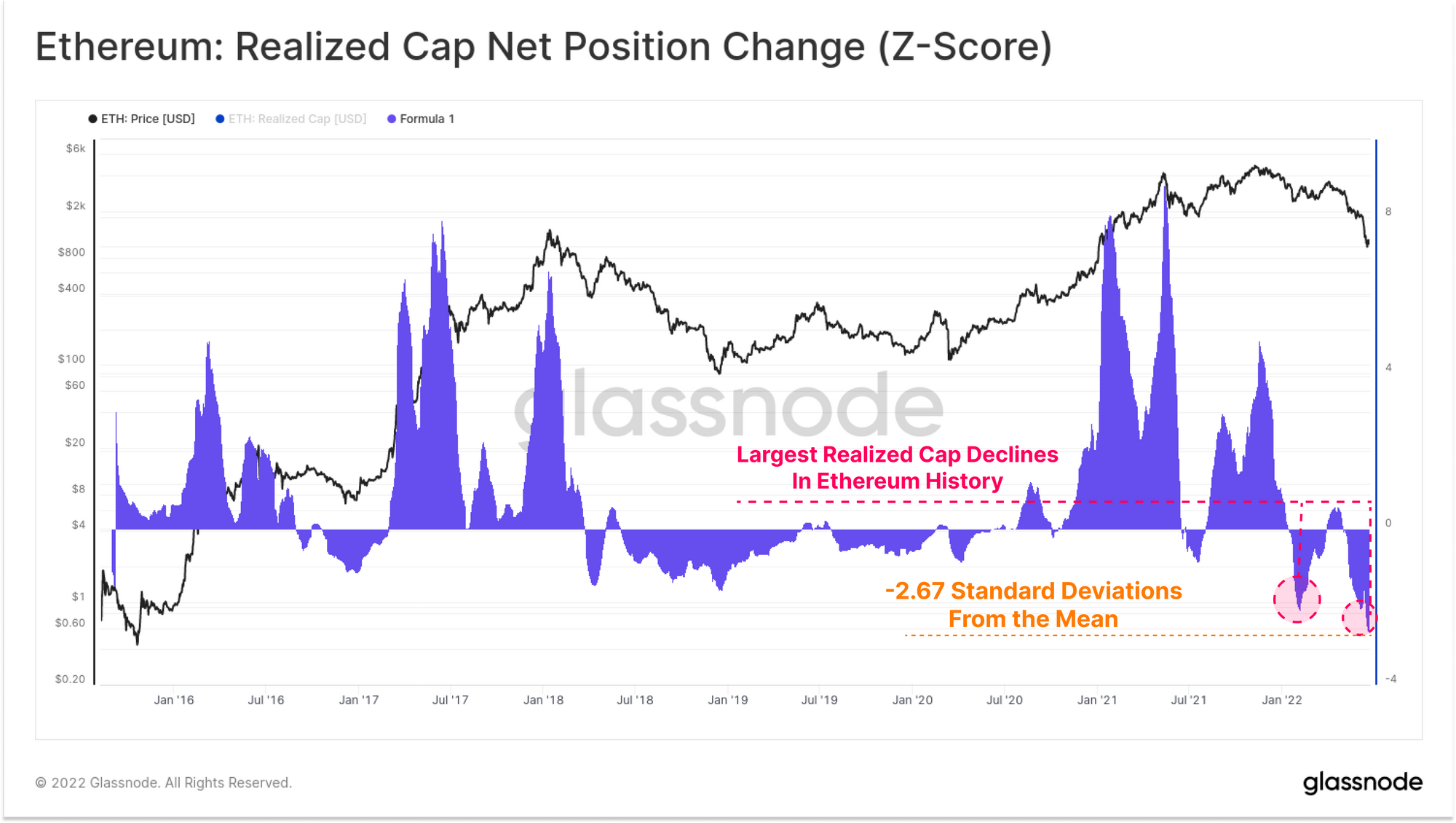

We can close this study by exploring the monthly change in the Ethereum Realized Cap, again demonstrating the net capital outflow from the network. Here we can see that recent downside price action is punctuated by two capitulation events:

- Dec 2021 - Market wide deleveraging event as $5.4B of Futures open interest was closed in liquidation amidst fears of the Omicron variant and initial Fed Bond Tapering causing a capital outflow of around $11.6B from Ethereum (See our previous article here).

- May-June 2022 - Luna Collapse and subsequent deleveraging from second order effects caused ripples across the entire digital asset ecosystem, precipitating a capital outflow from ETH of roughly $16.0B.

The latter event represents a -2.67 standard deviation move from the mean, and is clearly the largest monthly outflow from the ETH asset in history.

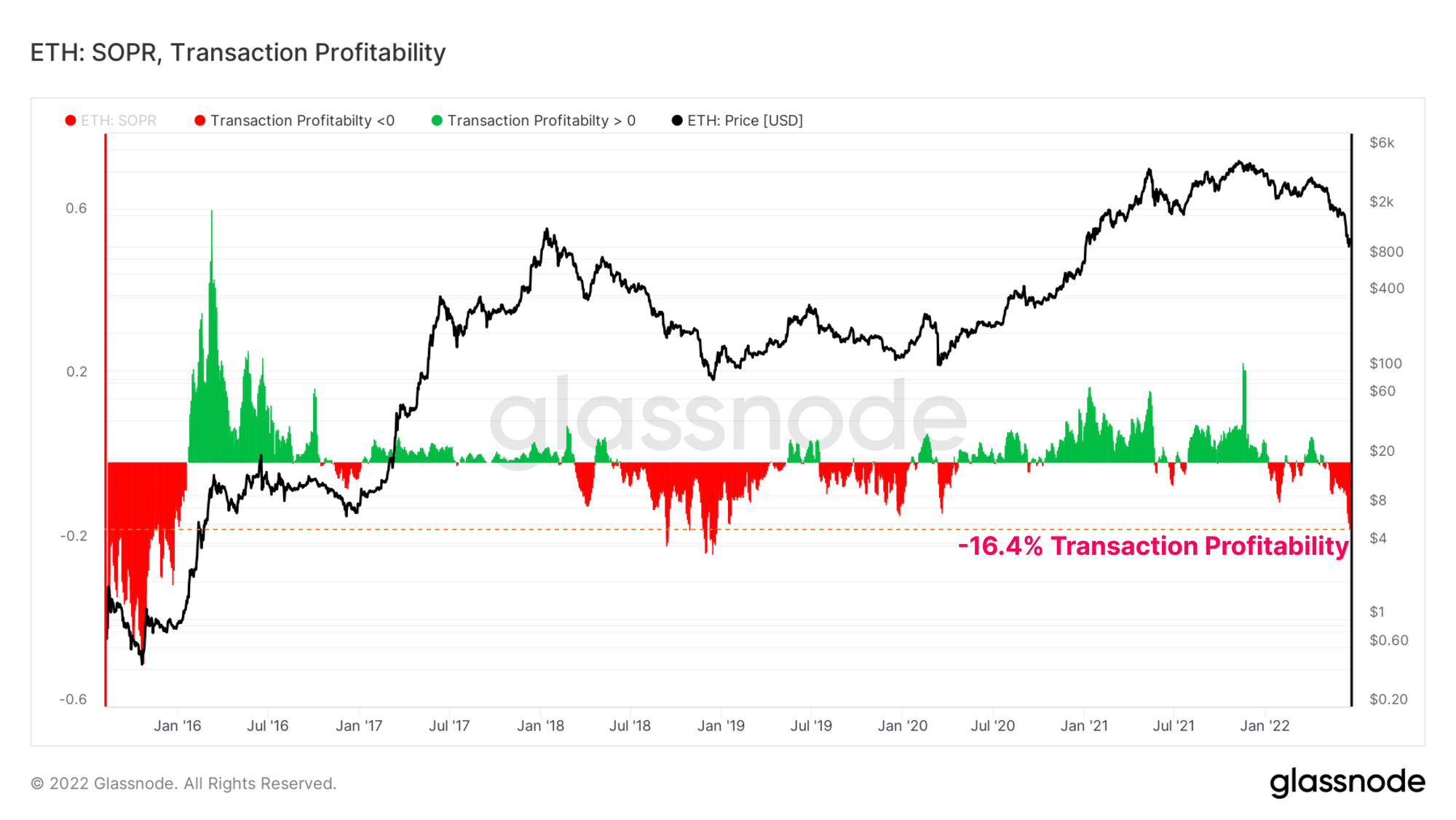

Ethereum Transaction Profitability displays the average profit (positive, green) or loss (negative, red) realized by all transactions that day.

Heavy dominance of realized losses can be seen to accompany downside price action in bear markets. In the current market, the average ETH transactor is realizing a loss of -16.4% on their spent coins. Such poor transactional profitability was last seen in the depths of the 2018 bear market when ETH was trading at $84.

To summarise the 2021-22 Ethereum bear market, we have the following statistics:

- Ethereum has seen a peak drawdown of -79.5% from its ATH placing this sell off within the upper-bound of previous bear market floors.

- BTC dominance is commanding the gravity of capital flows, which historically has signalled further ETH under-performance in following months.

- Ethereum Value captured per Byte is suggesting deteriorating capital efficiency, and alludes to a potential further 50% decline if $0.15/byte levels are revisited. Earlier recovery would indicate improved value capture mechanisms by the Ethereum network.

- The last 6 months has seen the two largest statistical capital destruction events in Ethereum history, worth a combined $27.6B in net outflows from the Realized Cap.

- The MVRV for both ETH and ETH 2.0 are experiencing significant drawdowns, signalling that the average ETH holder is holding large unrealized losses.

- Ethereum transaction profitability continues to languish at levels last seen in Jan 2019 where investors realize an average loss of -16% in each transaction.

Summary and Conclusions

2022 has been a tough year for digital assets. This particular bear market has hit both Bitcoin and Ethereum very hard. Many on-chain and market performance metrics have reached historically, and statistically significant lows.

In this piece, we normalized many metrics to adjust for increased market size and capital flows through years of asset maturation. Even under this relative and statistical framework, we can largely confirm the severity of 2022 bear market.

The various studies described above highlight the sheer magnitude of investor losses, the scale of capital destruction, and the observable capitulation events occurring over the last few months. Given the extensive duration and size of the prevailing bear market, 2022 can be reasonably argued to be the most significant bear market in the history of digital assets.

- Follow us and reach out on Twitter.

- Join our Telegram channel.

- Visit Glassnode Forum for long-form discussions and analysis.

- For on-chain metrics and activity graphs, visit Glassnode Studio.

- For automated alerts on core on-chain metrics and activity on exchanges, visit our Glassnode Alerts Twitter.

Disclaimer: This report does not provide any investment advice. All data is provided for information purposes only. No investment decision shall be based on the information provided here and you are solely responsible for your own investment decisions.